What happened to Biden? He used to be a “reasonable” Senator (reasonable for a racist Democrat, that is), willing to negotiate with the opposition on budgetary issues and the debt ceiling. Now we have “Progressive Joe” who is acting like crazy Progressive Congresswoman Pramila Jayapal from Seattle. {Aka, Seattle’s Worst!} But his newly found Progressive identiy is leading down a terrible path. Rating agencies are putting the US of credit watch because of Biden’s newly found Progressive back bone. (Progressive means progressing towards full blown Communism).

Ratings company warns on worsening political partisanship

US AAA ratings on review with negative implications at DBRS

The tension around the US debt-limit negotiations ratcheted up after Fitch Ratings warned the nation’s AAA rating was under threat from a political standoff that’s preventing a deal.

Fitch may downgrade its assessment to reflect the increased partisanship that is hindering a resolution despite the fast-approaching so-called X date, it said, referring to the point at which Washington runs out of cash. It moved the US to “rating watch negative” under its classification. Meantime, DBRS Morningstar placed the US ratings of AAA under review “with negative implications.”

Markets have been showing increasing nervousness over the standoff, with Treasury-bill yields slated to mature early next month surging past 7%, while the S&P 500 Index has declined for two days. Economists project a US default could trigger a recession, with widespread job losses and a surge in borrowing costs.

Fitch’s warning “underscores the need for swift bipartisan action by Congress to raise or suspend the debt limit and avoid a manufactured crisis for our economy,” said Lily Adams, a spokesperson from Treasury.

Biden’s childish refusal to reduce his insanely huge budget (crammed with pork for large donors and Progressives) is causing ripples to be felt overseas. Look look at the Japanese Yen.

Pramila Jayapal, Joe Biden’s intellectual soulmate.

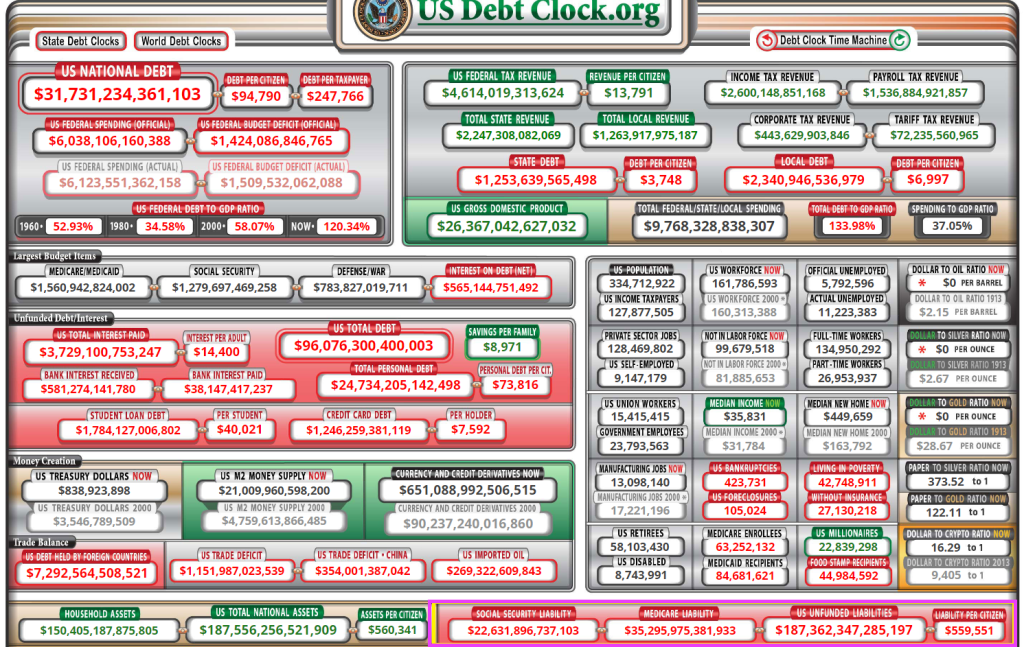

Reminder, the US already has $32 TRILLION in debt and politicians have promised $188 TRILLION in entitlement spending. yet we are sending billions to Ukraine, etc. Yet Biden is visiting Japan (hide your little girls, Hiroshima!) and Biden/Congress still haven’t solved the debt limit crisis and Biden’s insane budget yet. Meanwhile, Americans are suffering from Biden’s inflation (aka, Bidenflation) and bad economic policies.

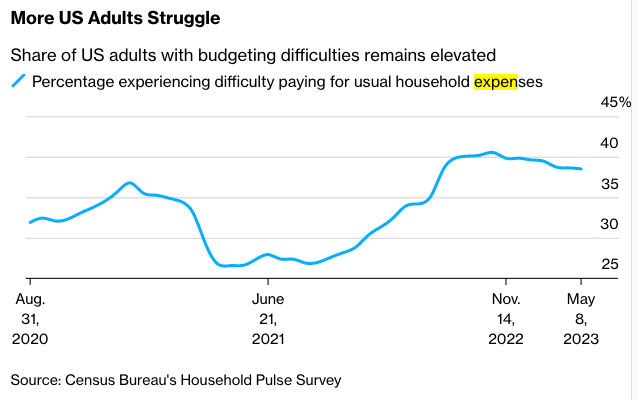

As many as 89.1 million American adults (or about 38.5%) were found to experience some form of difficulty in covering expenses between April 26 and May 8, according to Bloomberg, citing new data from the Household Pulse Survey. This is up from 34.4% in 2022 and 26.7% during the same period in 2021.

The rising trend is alarming but not surprising. Consumers have been battered by two years of negative real wage growth.

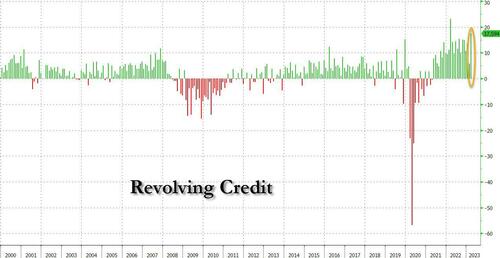

As wages fail to outpace the cost of living, many consumers have burned through savings and resorted to credit cards. The latest revolving credit data shows consumers appear to be ‘strong,’ but that’s only because they use their plastic cards more than ever to survive.

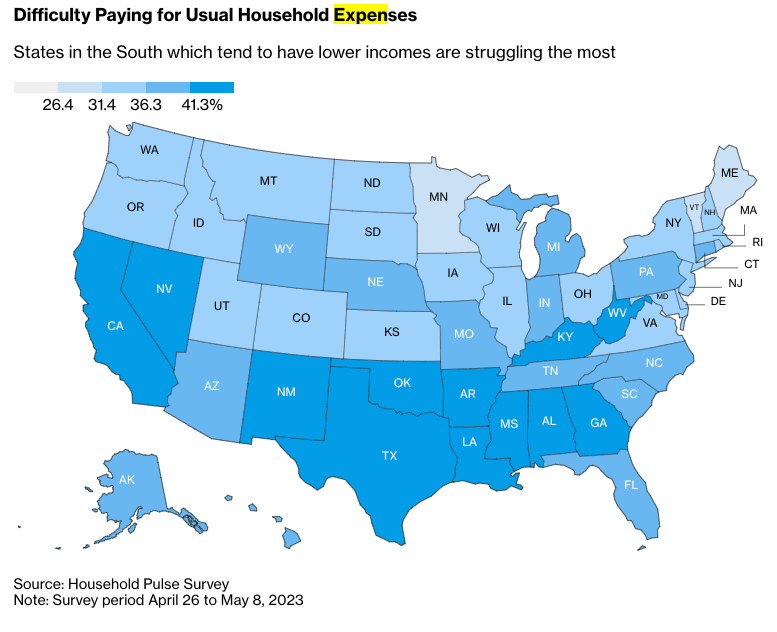

The Household Pulse Survey found struggling households were primarily based across West Coast and the South.

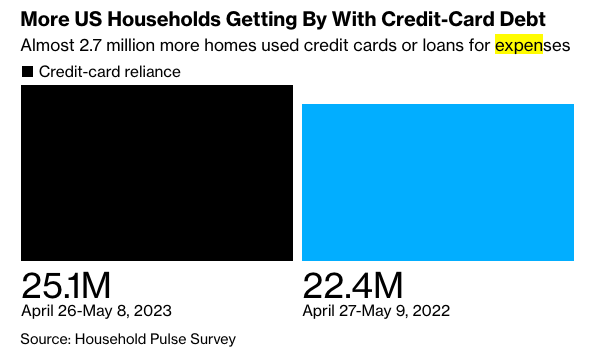

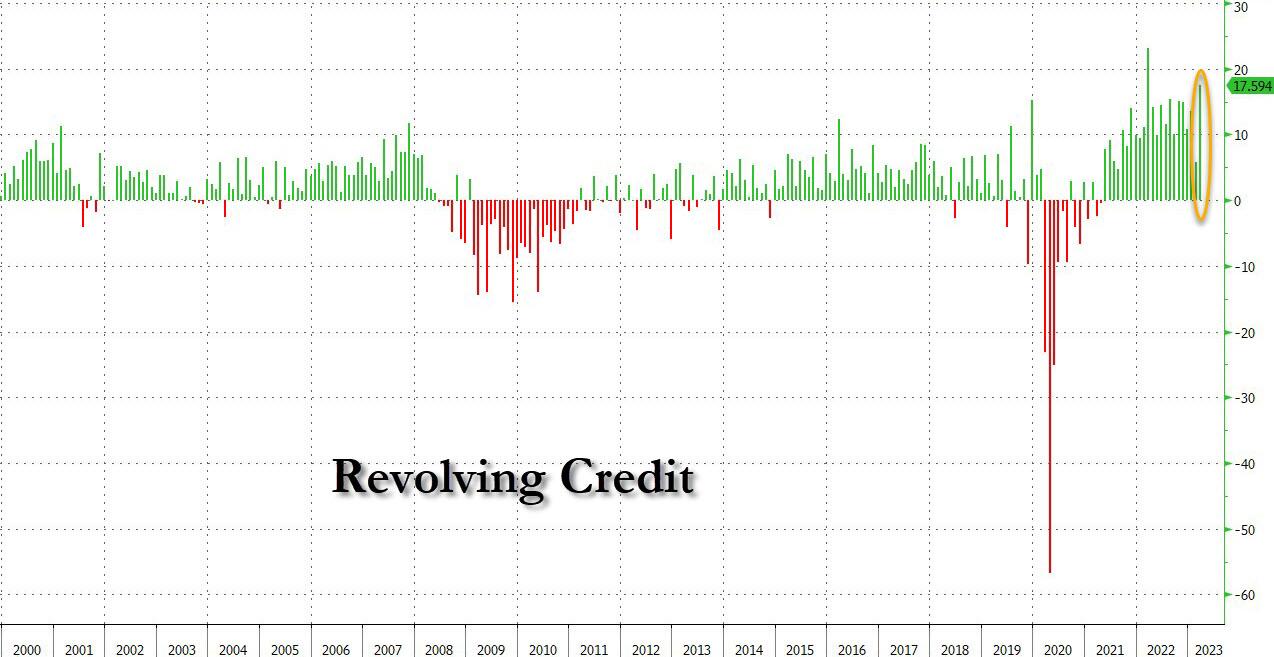

Compared with the same period last year, the survey found 2.7 million more households were relying on credit cards to cover expenses.

Consumers have record card debt and ultra-low savings rates and are paying some of the highest borrowing costs in a generation (the average interest rate on cards now exceeds 20%). This debt is becoming insurmountable for some as delinquencies rise.

And what we have now is new debit and credit card data published by the Bank of America Institute that shows not just spending slowdown for lower-income consumers, but also the upper-income cohort is finally starting to crack.

However, it is appropriate that Biden is visiting Hiroshima Japan where a nuke was detonated to help end World War II.. Biden is doing the same to the US.

I used to think that The Kabuki Theater surrounding the raising of the US debt limit and passing a Federal budget would be over by now. But since Biden is being controlled by the hard left “Progressives” in Washington DC, he may be reckless enough to let the US default just so he can blame Republicans. And with our useless and deeply-biased main street media (MSM) just repeating Democrat talking points blaming Republicans, we may actually see a US debt default.

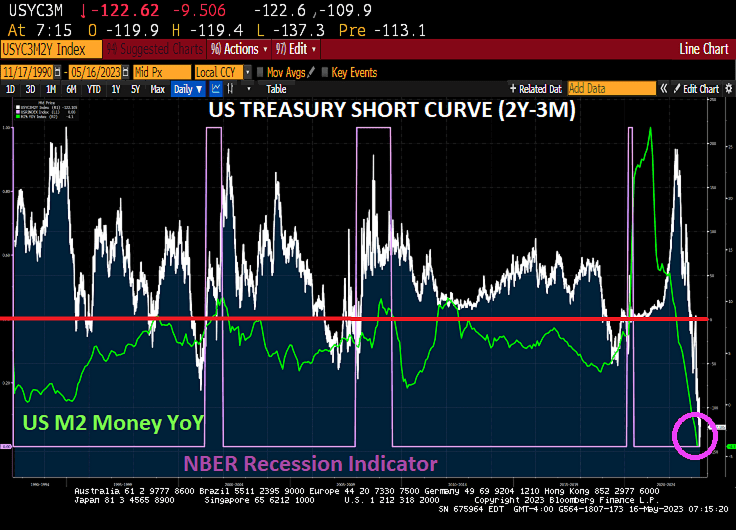

So while Yellen is warning that time is running out, notice she never encourage Blaming Biden to negotiate his insane budget downwards, we see a deeply inverted US Treasury short curve (2Y-3M).

(Bloomberg) Treasury Secretary Janet Yellen warned that “time is running out” to avert an economic catastrophe from failing to raise the debt ceiling, in remarks released as President Joe Biden and congressional leaders prepared to meet on the standoff.

Speaker Kevin McCarthy issued his own notice Monday evening ahead of Tuesday’s 3 p.m. gathering, saying, “We only have so many days left to deal with this.”

The two sides showed little signs of agreeing on much else other than the countdown in the runup to the second White House encounter on the debt ceiling in two weeks. While senior staff have been negotiating for days, Republicans are still pressing for sweeping spending cuts, while Democrats are determined to protect the president’s legislative achievements.

“We are already seeing the impacts of brinksmanship: investors have become more reluctant to hold government debt that matures in early June,” Yellen said in remarks prepared for delivery to a banking conference on Tuesday. “The impasse has already increased the debt burden to American taxpayers.”

The Treasury chief issued a fresh letter to congressional leaders Monday restating that the Treasury risks running out of sufficient cash for all federal obligations as soon as June 1. The livelihoods of millions of Americans “hang in the balance,” she said in excerpts of her speech to the Independent Community Bankers of America Capital Summit released by the Treasury.

There is the evil Hobbit! Sending a letter to Congress essentially blaming McCarthy for the fiasco when Biden could downsize his budget request to reasonable levels. But Yellen is an authoritarian Statist, not a free market type.

I wish Biden would spend more time trying to negotiate with McCarthy to end the debt crisis rather than stir up race hatred like he did at Howard University graduation. C’mon Joe! White “supremacy” is not the most dangerous terrorist threat. I would actually say that Biden, Yellen and Schumer (throw in Pelosi’s spending splurge as Speaker) are the biggest terrorist threat. They are the 4 horsemen of the US debt apocalypse.

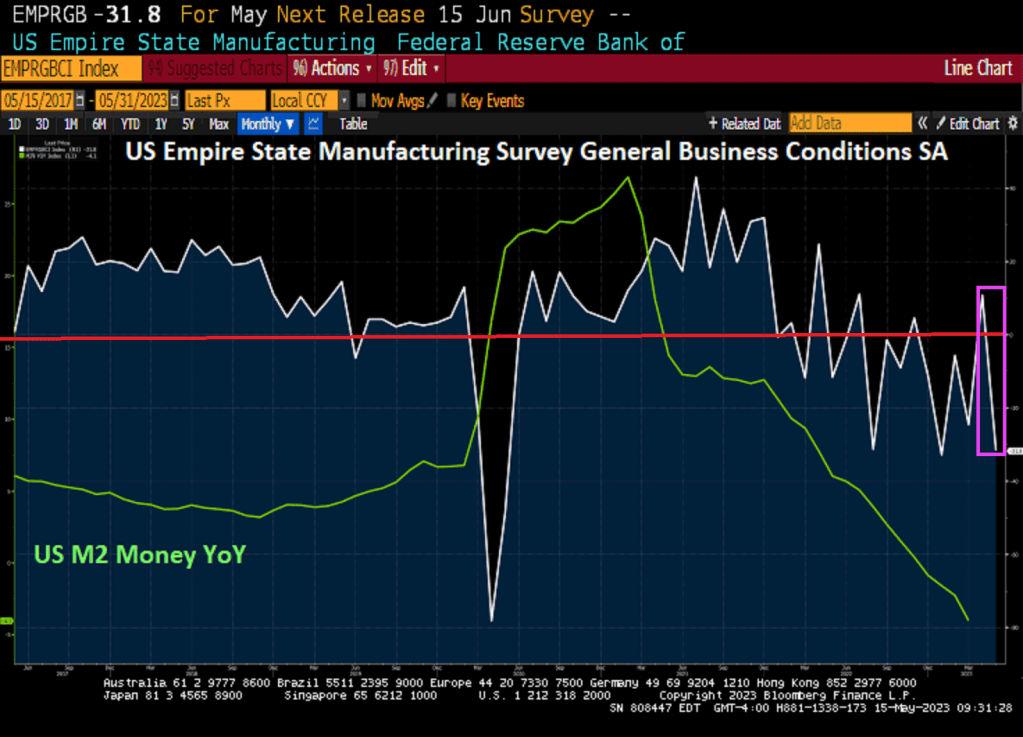

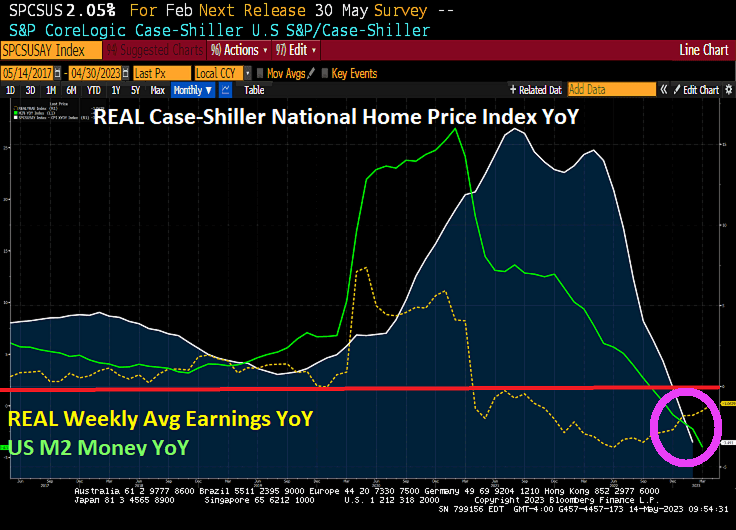

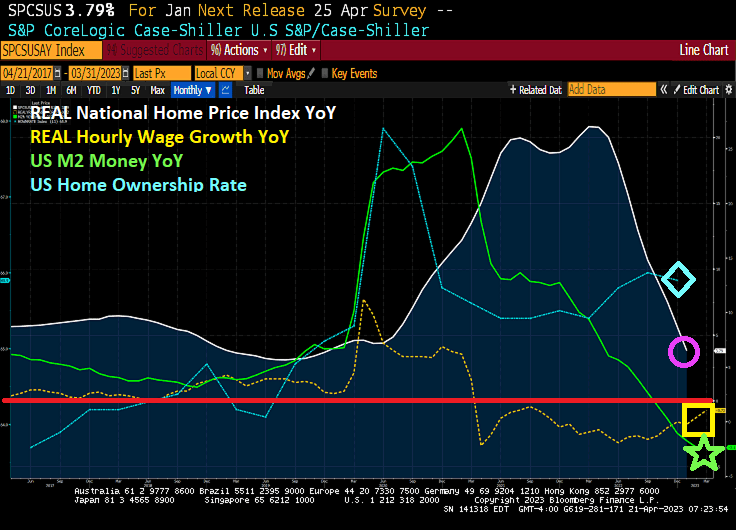

Let’s see how Bidenflation (caused by staggering Federal misspending) and years of Yellen’s TLTL (too low too long) monetary policy has caused a massive dislocation in the housing market.

The February Case-Shiller National home price index less core inflation (CPI less food and energy) year-over-year is declining by -3.5%. This is happening as REAL average weekly earnings growth is at -1.06% YoY and has been negative growth for 25 straigth months.

Look at The Fed’s massive overreaction to the unnecessary government shutdowns of economies and schools. It really sent home price growth soaring, then when The Fed starts slowing the monetary stimulus, we get the largest slowdown of REAL home price growth since 2012.

The 4 Horsemen of the US Debt Apocalypse. I would add Mitch McConnell and Fed Chair Powell, but then would have an entire Cavalry company like George Armstrong Custer had at Little Big Horn.

California just did what Slow Joe Biden and Senate Majority Leader Chuckles Schumer are threatening to do. Biden and Schumer still refuse to negotiate (allegedly) sending the US Federal government careening towards a staggering debt default. The source of both California and US Federal government fiscal problems? Out of control government spending, aka, government gone wild!

In any case, California borrowed approximately $20 billion from the federal government to cover unemployment benefits during the pandemic, and with Gov. Gavin Newsom’s recent decision to not pay it back, employers are now saddled with the expense, according to experts.

“The state should have taken care of the loans with the COVID money it received from the government in 2021,” Marc Joffe, policy analyst at the Cato Institute—a public policy think tank headquartered in Washington, D.C.—told The Epoch Times.

In the proposed 2023–2024 budget, $750 million was allocated to start paying down the loans, but Newsom made changes to the plan in January and withdrew the funding.

The Epoch Times’ request for comment from Newsom’s office was not returned on deadline.

The decision leaves businesses in the state responsible for the loans—as mandated by federal regulations—so the federal unemployment tax rate of .6 percent is set to increase by .3 percent annually, starting in 2023, until the loan is extinguished.

“California is just not really an employer-friendly state,” Joffe said. “This one thing will not be a difference between a business remaining open or closing, but it’s just another burden on top of the many burdens the state puts on employers.”

Twenty-two states borrowed money for unemployment insurance from the federal government during the pandemic, with all but four—California, Colorado, Connecticut, and New York—paying back their debts.

California owes the most, by far, with approximately $18.6 billion outstanding as of May 2, followed by New York’s $8 billion, Connecticut’s $187 million, and Colorado’s $77 million, according to U.S. Treasury Department data.

The discrepancy in amounts borrowed and owed by states lies in the different approaches to managing the pandemic, with California’s stricter lockdown causing unemployment to remain higher and longer, according to experts

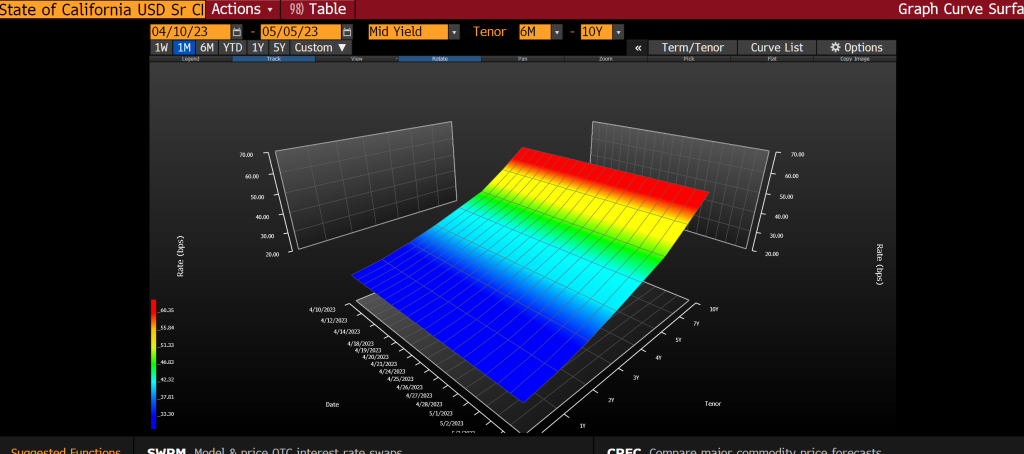

And CA CDS 1Y is tame (only 31), the CDS curve over a longer time frame looks miserable.

Now, Gruesome Newsom only default on Covid-related loans. The California municipal bond market is huge and CA has defaulted on those loans …. yet.

Speaking of insane fiscal “management,” a repartations plan in California could cost billions.

California’s reparations task force, which first convened nearly two years ago, has given the final approval to a list of recommendations on how the state may compensate and apologize to Black residents for historical discrimination. “Reparations are not only morally justifiable, but they have the potential to address long standing racial disparities and inequalities,” Representative Barbara Lee (D-CA) said during a weekend meeting. The proposals now go to state lawmakers to consider reparations legislation and a final sum, which some economists could cost the state upwards of $800B, or almost 3x the state’s annual budget.

To be initially eligible, applicants must be a descendant of Black people who were in the country by the end of the 19th century, thouqh there are not yet details on how the payments would be funded. Age, state residence, and other factors will also play a role in determining compensation.

There is the rub – how does California finance the reparations? Raise taxes (unfair to people who never did anything wrong to blacks)? Borrow billions? Given that Newsom just defaulted on loans to California might mean that there will be relucatance to lend CA billions more.

CA Governor Gavin “Slick” Newsom. The Defaulter In Chief of California.

The Federal government in Washington DC is broken beyond repair. Politicians get elected by promising free or cheap things, so they keep delivering the bacon. Or pork to political donors. The top 1% get massive payoffs (like green energy subsidies or bank bailouts), the bottom 99% get out of control entitlements like Social Security, Medicare and Medicaid. And other unsustainable entitlements. In fact, student loans are now an entitlement since some voters will vote for the corrupt politician (no, Joe Biden isn’t the only corrupt politician in Washington DC) who will forgive their student loans.

In fact, we now have $187 TRILLION in UNFUNDED liabilities that were promised to the 99%. The 1% will always get their political contributions paid. Biden and Schumer have promised their donor class trillions in spending, so that are threatening to let the US debt default to protect the 1%.

And unfunded entitlements are expected to soar, particularly Medicare.

Mandatory spending is expected to soar while discretionary spending is almost flat in terms of growth.

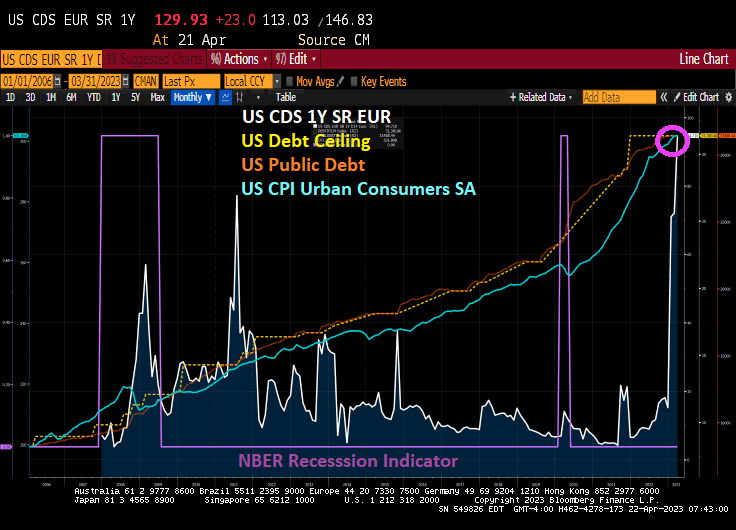

Meanwile, the US credit default swap remains elevated as the US Treasury short curve (2Y-3M) is near the most inverted in history.

And this headline, “Biden Not Ready Yet to Invoke 14th Amendment to Avoid US Default”. That means Biden would adopt extraordinary powers to prevent a debt default. Hence, the idiocy like the trillion dollar coin.

Nobel Laureate and Statist useful idiot Paul Krugman wants to keep spending trillions. As a result, he argues “Don’t worry about the declining US dollar hegemony … as long as the US doesn’t default.” Translation: Krugman agrees with Dementia Joe that Republicans should just pass Biden’s budget with no strings attached. C’mon Krugman. The growth of BRICs (Brazil, Russia, India, South Africa and growing) is partly due to 1) perceived weakness of Senile Grandpa Joe and 2) the fiscal spending and debt growth in Washington DC. Of course it matters, but Krugman wants to keep spending on green lunacy and entitlements until we break the back of the country. Sounds like Krugman is on board with Cloward-Piven.

They can’t cut promised entitlements. Look at France where Macron raised the retirement age by 2 years and there are endless riots. So debt default is the only option, though painful.

Will Congress and future administrations stop prominsing endless spending that benefits the 1%? Not likely. Our political system is hopelessly broken.

I am sure that China’s Communist Party has sent Dementia Joe a message “We own you! You better not default on what you owe us!!” Or default so we can own you financially.

Three of the four horsemen of the financial apocalypse. Yellen is the fourth horseman, but is too short to appear in the picture.

Thanks to O’Biden (Obama/Biden) and Senate Majority Leader Chuck Schumer’s failure to negotiate a debt ceiling increase, the US has officially become a banana republic. Crazy government, lawless censoring and arrest of opposing political candidates.

The US CDS 1Y SR Eur just hit a staggering 176.53. That is the price of insuring against a debt default by O’Biden and Treasury Secretary Janet Yellen.

Is a US debt default likely? It shouldn’t be. But you never know with the circus clowns in the White House and nasty Chuck Schumer. But arresting the leading Republican Presidential candidate before the elections is pure Chavez/Maduro Banana Republic politics.

2 year Treasury yield up over 11 basis points today.

It has been a tough road for the US economy since Covid and Biden’s Reign of Error. For the first time since July 2020 under President Trump, we have finally seen average hourly earnings growth YoY exceed average home price growth YoY.

In REAL terms (after substracting out headline inflation), we see that US housing market is still plagued by 24 straight months of negative wage growth with REAL wage growth still being lower than REAL home price growth.

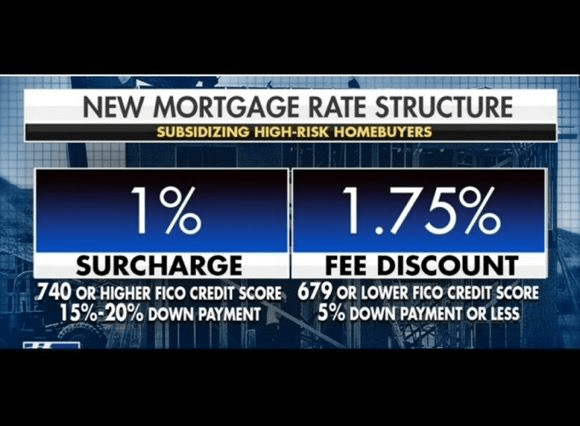

Then we have Biden’s Marxist mortgage model, making those who who saved and showed care in managing their credit score given money to those who didn’t save and are terrible at financial management. Just like taxpayers trusting DC bureaucrats to carefully spend their money.

This is life under Joe Biden. Record sovereign risk, record high debt, near 40-year highs in inflation, a hot war in Ukraine with Russia, failure of DOJ/FBI to do anything about the content of Hunter Biden’s laptop, repression of free speech, soaring crime, out of control borders. Should I keep going? It is a disastrous mess created by Obama/Biden and their creepy allies.

US sovereign risk just hit 130, the highest since CDS was recorded. This alligns with Biden/Congress massive borrow and spend policies where Federal debt has soared to it highest level in history. Inflation, while cooling, remains high.

On the housing front, REAL national home price growth is negative which makes sense since REAL average hourly wage growth has been negative for the last 24 months.

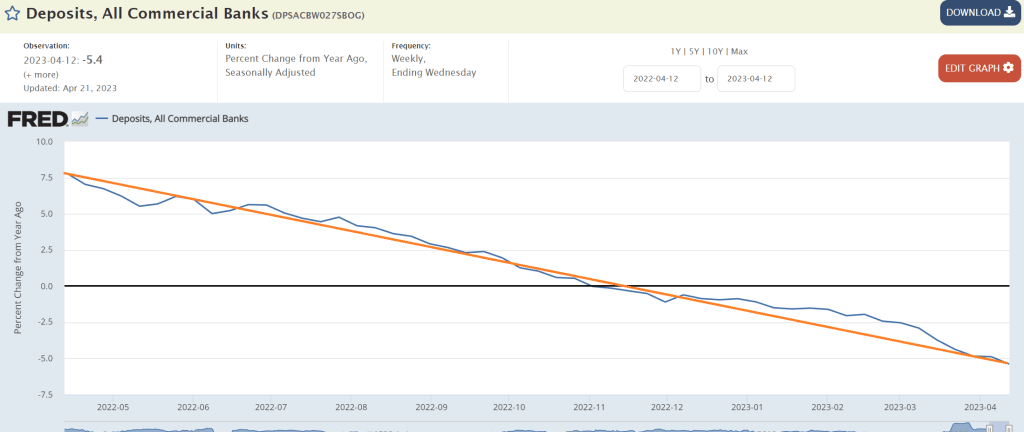

And just over the past year, commericial bank deposits are falling like a paralyzed falcon.

Biden and Obama’s chief hack in the White House, Susan Rice, are burning down the house.

{kind=link}

{kind=link}

You must be logged in to post a comment.