Well, the University of Michigan consumer sentiment indices are out for March … and they are ugly.

As a baseline, consumer confidence in February 2020 (just before Covid) was 101. After Covid and massive Fed stimulus and Federal government spending spree, consumer confidence in March fell to 62.0, a far cry from 101 under Trump.

Even worse, the UMich buying conditions for housing hit 142 in February 2020 but has declined to 47 in March 2023.

Why would ANYONE have confidence in the US economy under a complete fool with dementia like “China Joe” Biden??

Inflation is slowing just a little. But my feeling about The Fed (that partly caused the problem in the first place by keeping rates too low for too long (TLTL) under Yellen is all I can do is laugh.

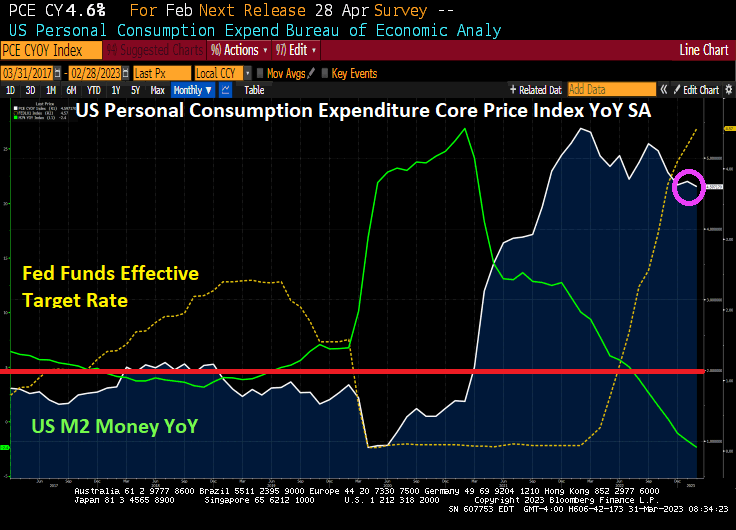

The US Core Deflator (Personal Consumption Expenditure CORE PRICE Index YoY fell only slightly in February to a still-high 4.6% in February despite The Fed jacking up interest rates and slowing M2 Money growth.

I thought Biden and Congress passed the inflation reduction act??

The Covid outbreak in early 2020 (from which I came close to dying) resulted in legendary Fed stimulus and Federal government spending. But as The Fed attempts to cool inflation by slowing M2 Money printing and raising The Fed’s target rate, we are seeing the lowest personal consumption expenditures print under Biden’s reign of error, a measly 1%.

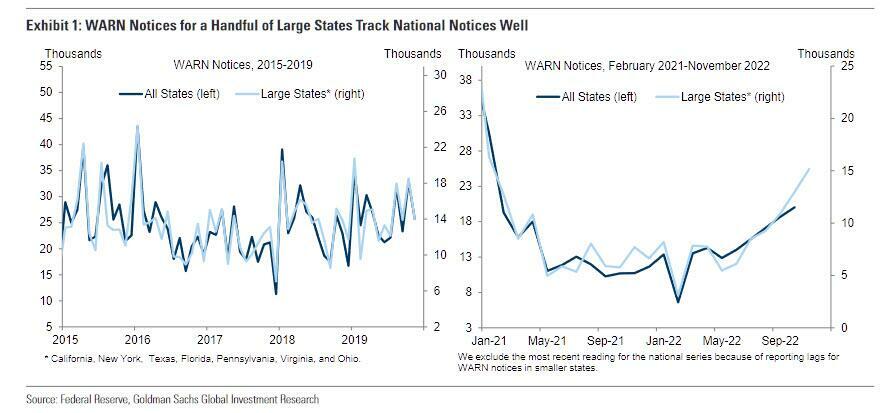

On top of the dismal revision to the Q4, we are seeing WARN notices increasing, particularly for large states. Worker Adjustment and Retraining (WARN) Notices are picking up which points to unemployment claims soon rising and a deterioration in the jobs market, posing a risk to stocks.

Biden’s reign of error continues with horrible policies. With the help of Congress.

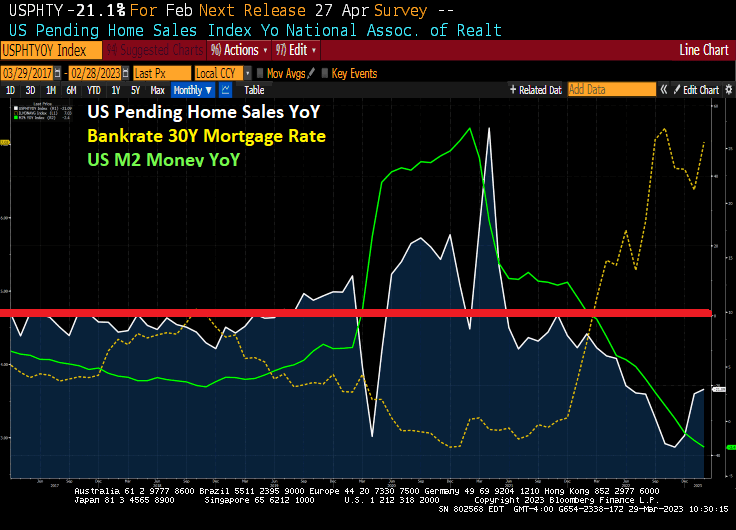

Pending home sales grew in February for the third consecutive month, according to the National Association of REALTORS®. Three U.S. regions posted monthly gains, while the West declined. All four regions saw year-over-year decreases in transactions.

The Pending Home Sales Index (PHSI)* — a forward-looking indicator of home sales based on contract signings — improved 0.8% to 83.2 in February. Year-over-year, pending transactions dropped by 21.1%. An index of 100 is equal to the level of contract activity in 2001.

More notably, the YoY growth rate has been NEGATIVE for 20 of the last 21 months. And 15 straight months.

Biden’s energy policies + insane Federal spending = inflation = Fed slowing M2 Money growth. Hence, pending home sales YoY is down -21.1%.

Well, the regional banking crisis has one positive outcome: mortgage rates dropped -46 basis points since last week. The result? Mortgage demand increased 2.9 percent week-over-week (WoW). Although I don’t recommend banking incompetence by bank management and “regulators” as a strategy to increase mortgage demand.

Mortgage applications increased 2.9 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending March 24, 2023.

The Market Composite Index, a measure of mortgage loan application volume, increased 2.9 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index increased 3 percent compared with the previous week. The Refinance Index increased 5 percent from the previous week and was 61 percent lower than the same week one year ago. The seasonally adjusted Purchase Index increased 2 percent from one week earlier. The unadjusted Purchase Index increased 2 percent compared with the previous week and was 35 percent lower than the same week one year ago.

The rest of the story.

We need a doctor to fix this mess, just not Dr. Yellen or Dr. Jill.

Consumer considence (according to the Conference Board) remains below pre-Covid levels despite the massive Federal spending spree and Fed money printing).

The US economy got beaten to a pulp by the Chinese Wuhan Covid virus outbreak in early 2020. The Fed intervened with massive money printing along with massive spending by Congress and the Administration. Result? 40-year highs in inflation and a Fed counterattack in terms of rate hikes.

The result of Fed rate hikes? Failing regional banks trying to cope with duration extention and scared depositors. And then we have the St Louis Fed Financial Stress index reaching its highest level since the Covid outbreak of early 2020. And with that, bond volatility is higher than that found during the Covid crisis.

With the expectation of MORE rate hikes, the 10-year Treasury yield jumped 12 basis points.

The architect of The Fed’s “too long for too long” is also the US Treasury Secretary, Janet Yellen.

You must be logged in to post a comment.