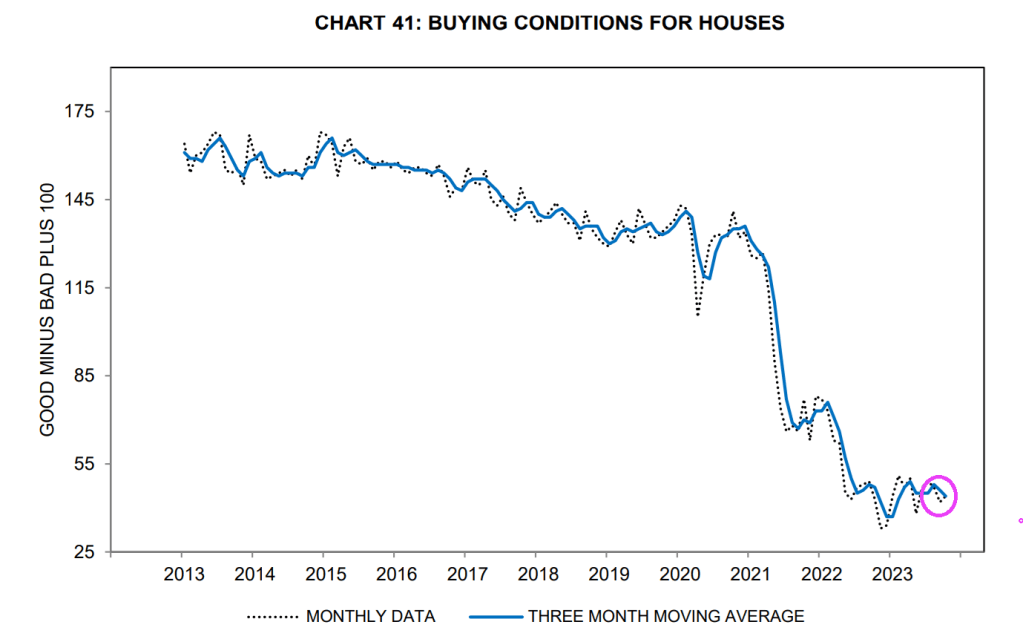

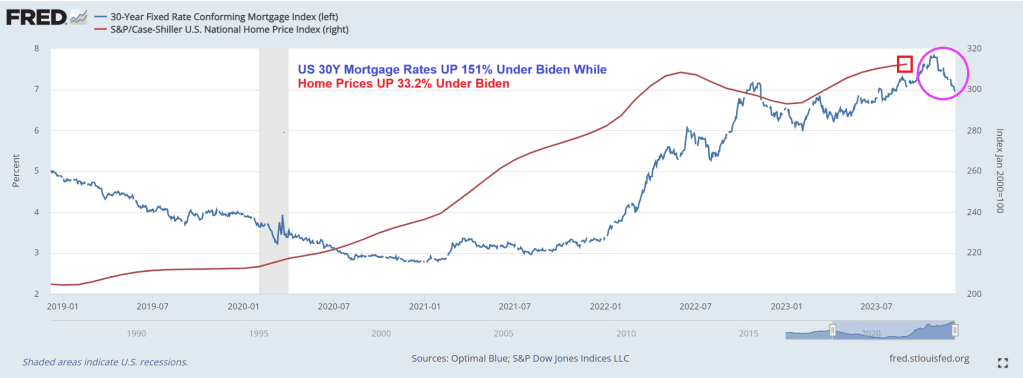

Why are buying conditions for houses so low? Well, mortgage rates, despite coming down recently, are still up 151% under Clueless Joe. And home prices are up 33.2% under Biden. So much for affordable housing for those renting.

Like the great Shoeles Joe Jackson on ChiSox and Cleveland Indian fame, Clueless Joe Biden cheated too. Except that Shoeless Joe was accused of accepting $5,000 to throw the World Series in 1919. Clueless Joe Biden and family are accused of accepting over $24 million from China, Ukraine, etc.

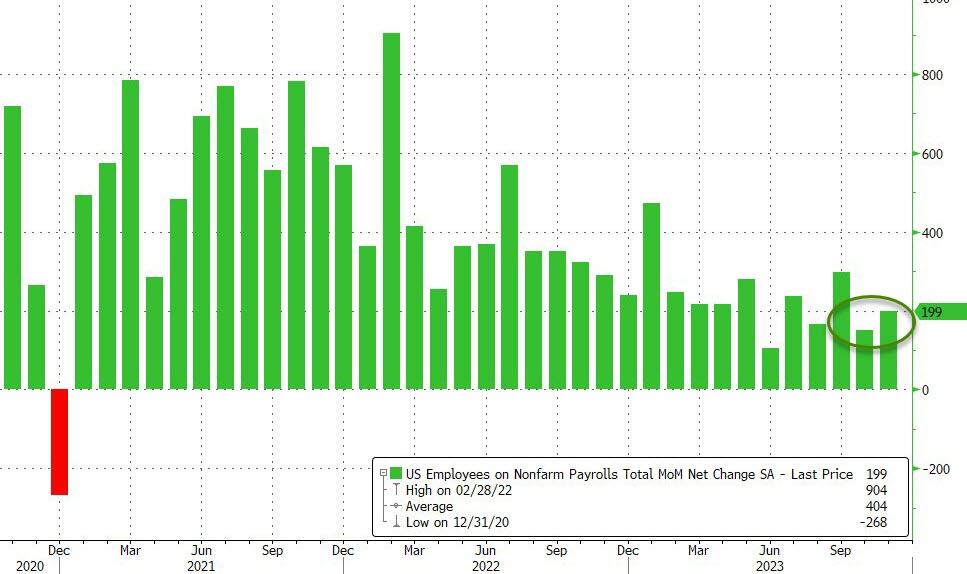

Several talking heads are salivating about the strong or solid jobs report in October. As if The Federal Reserve can’t read the jobs report. I call the report “Government gone wild!” since 51k government jobs were added in October.

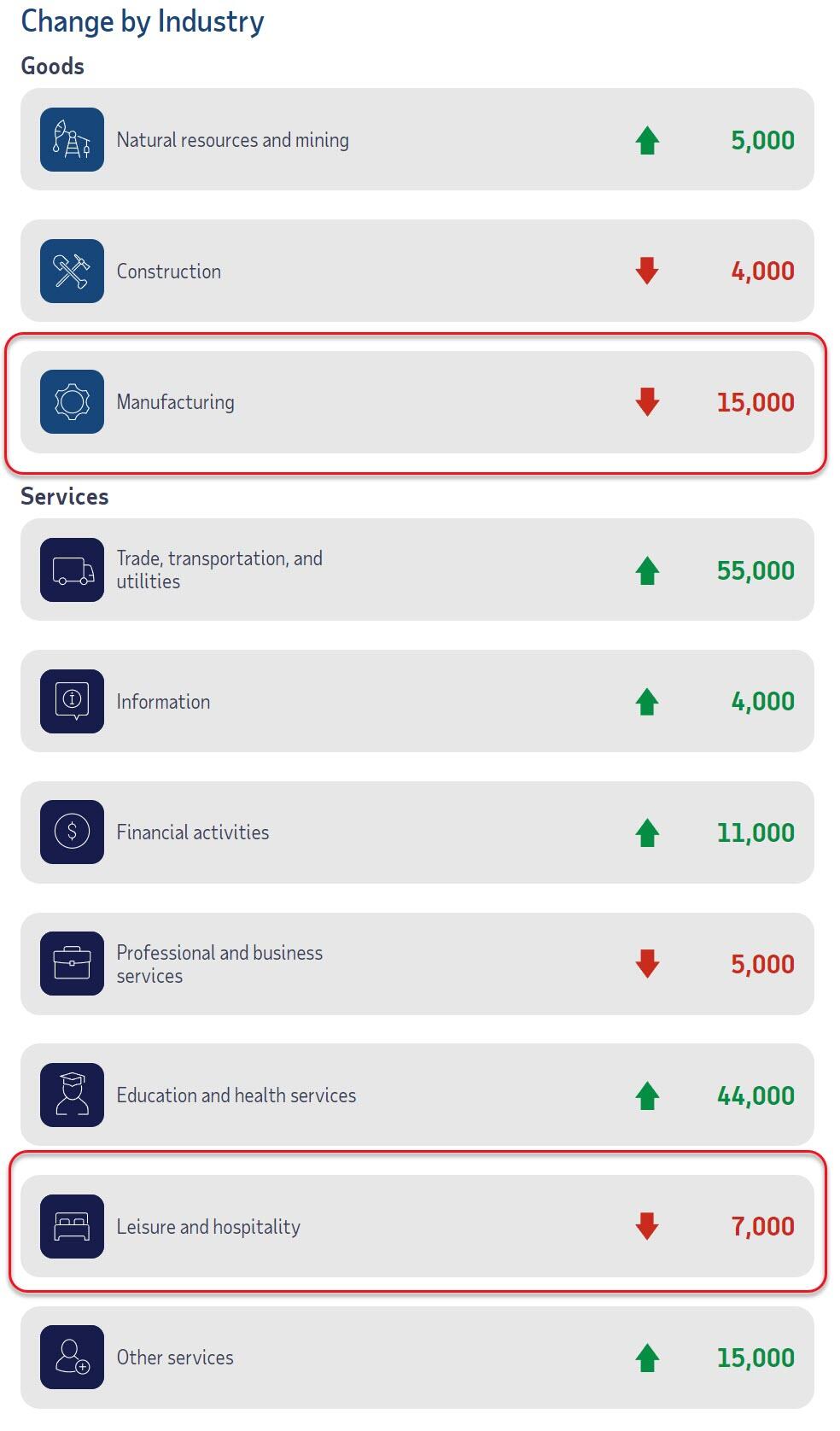

Job gains occurred in health care, government, and social assistance. Employment declined in manufacturing due to strike actvity.

Total nonfarm payroll employment increased by 150,000 in October, below the average monthly gain of 258,000 over the prior 12 months. In October, job gains occurred in health care, government, and social assistance. Employment in manufacturing declined due to strike activity. (See table B-1.) Health care added 58,000 jobs in October, in line with the average monthly gain of 53,000 over the prior 12 months. Over the month, employment continued to trend up in ambulatory health care services (+32,000), hospitals (+18,000), and nursing and residential care facilities (+8,000). Employment in government increased by 51,000 in October and has returned to its pre-pandemic February 2020 level. Monthly job growth in government had averaged 50,000 in the prior 12 months. In October, employment continued to trend up in local government (+38,000). Social assistance added 19,000 jobs in October, compared with the average monthly gain of 23,000 over the prior 12 months. Over the month, employment continued to trend up in individual and family services (+14,000). In October, construction employment continued to trend up (+23,000), about in line with the average monthly gain of 18,000 over the prior 12 months. Employment continued to trend up over the month in specialty trade contractors (+14,000) and construction of buildings (+6,000). Employment in manufacturing decreased by 35,000 in October, reflecting a decline of 33,000 in motor vehicles and parts that was largely due to strike activity. In October, employment in leisure and hospitality changed little (+19,000). The industry had added an average of 52,000 jobs per month over the prior 12 months. Employment in professional and business services was little changed in October (+15,000) and has shown little net change since May.

Speaking of Govzilla, my favorite quote showing the stupidity of BIG government is … Biden’s climate envoy John Kerry. “We’ve got to cut down on farming due to ‘Climate Change’…or people are going to starve…”

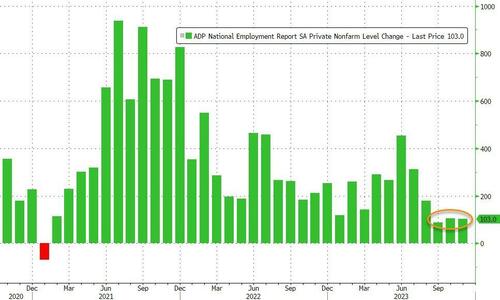

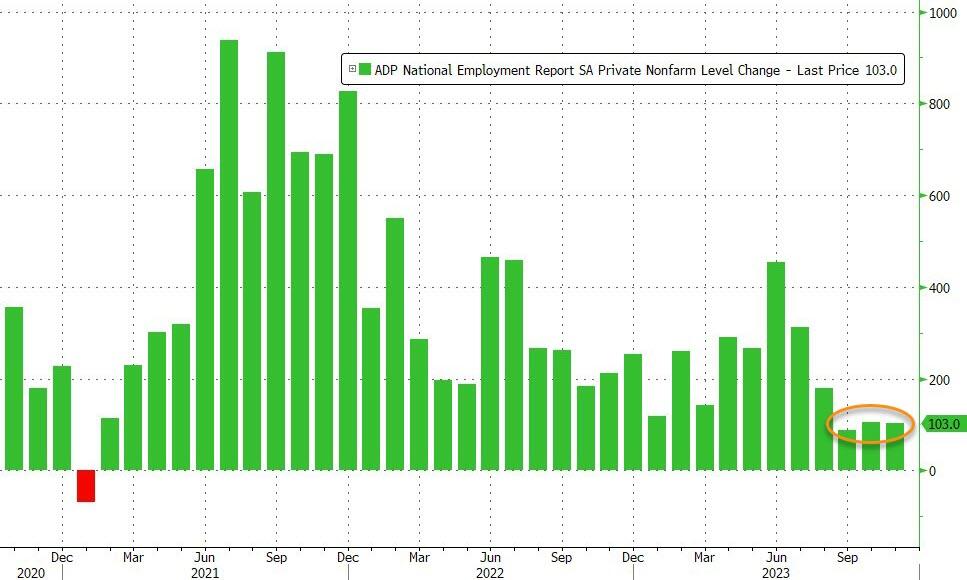

After ADP has printed lower than BLS for the last two months…

Source: Bloomberg

…expectations were for a small tick higher in November (from 113k to +130k), despite the ugly JOLTS print. However, ADP reported just 103k jobs added (and October revised down to 106k)…

Source: Bloomberg

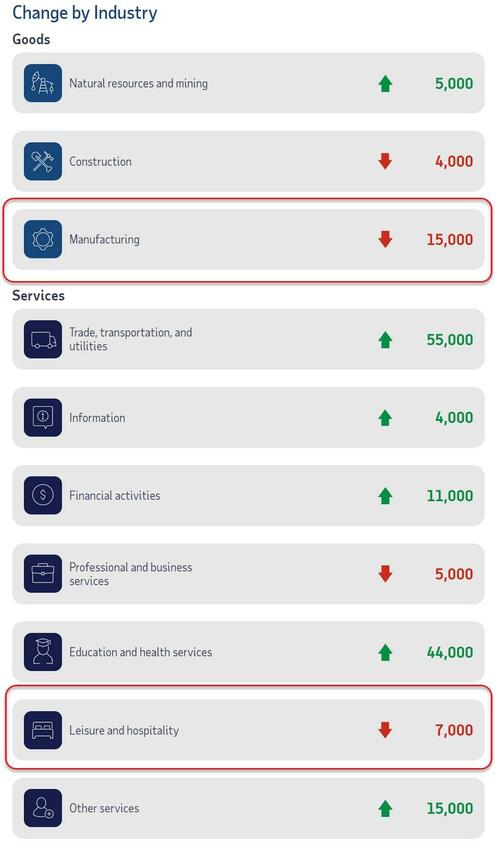

Manufacturing saw the biggest job losses but Leisure and Hospitality lost jobs for the first time since Feb 2021…

ADP’s Chief Economist Nela Richardson notes that:

“Restaurants and hotels were the biggest job creators during the post-pandemic recovery. But that boost is behind us, and the return to trend in leisure and hospitality suggests the economy as a whole will see more moderate hiring and wage growth in 2024.”

Bidenomics…

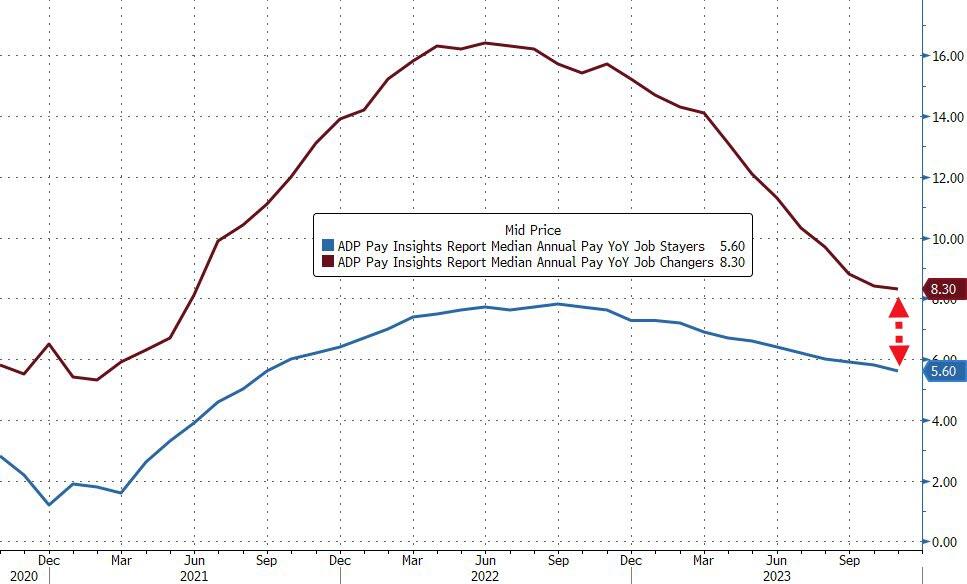

Job-stayers saw a 5.6 percent pay increase in November, the slowest pace of gains since September 2021. Job-changers, too, saw slowing pay growth, posting pay gains of 8.3 percent, the smallest year-over-year increase since June 2021. The premium for switching jobs is at its smallest in three years of data.

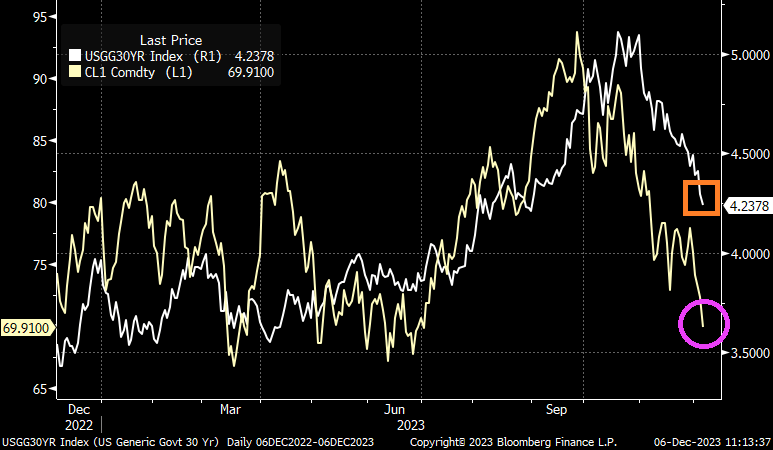

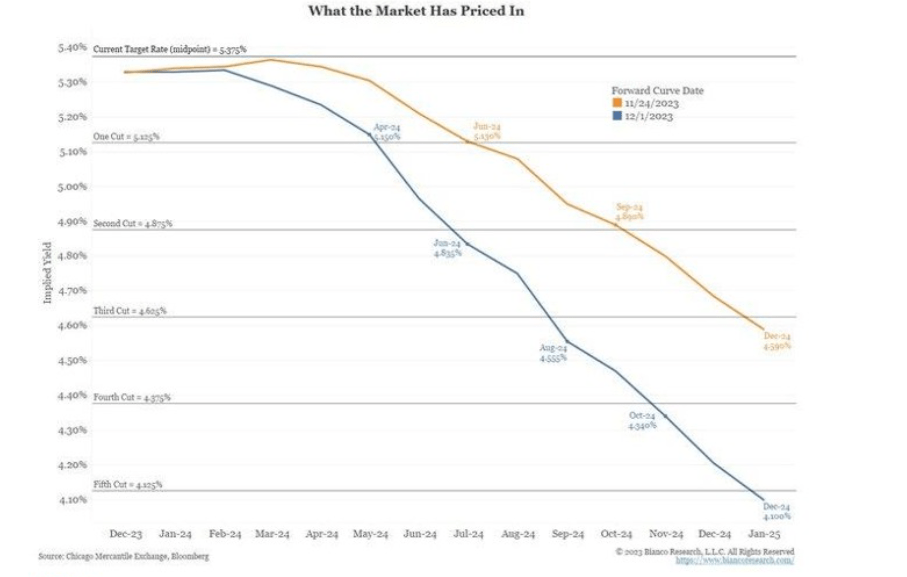

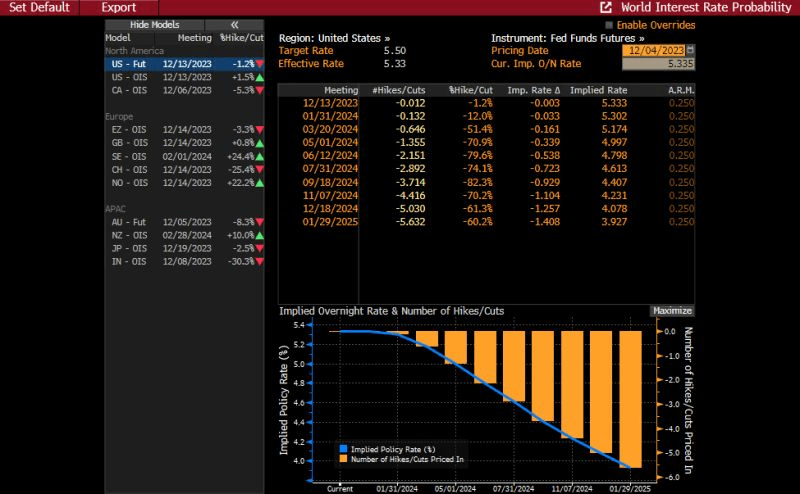

Is this the recessionary signals the STIRs market is banking on for 125bps of rate-cuts next year? Because stocks sure aren’t thinking recession.

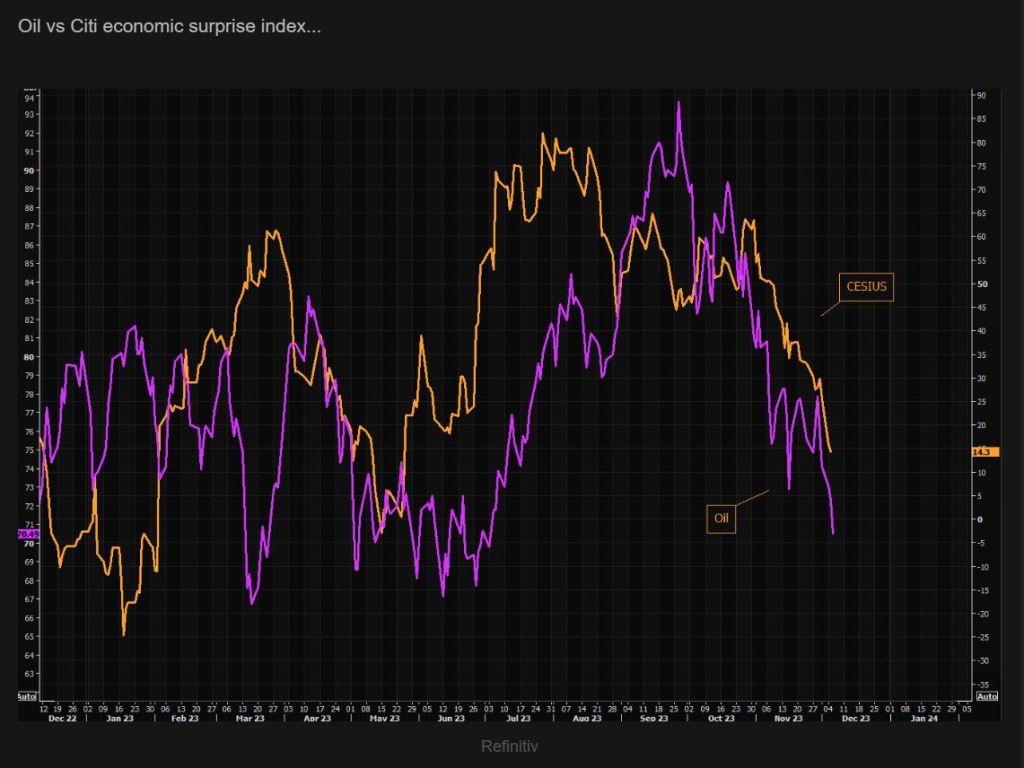

And as US Treasury 30Y yield drop, so do crude oil prices.

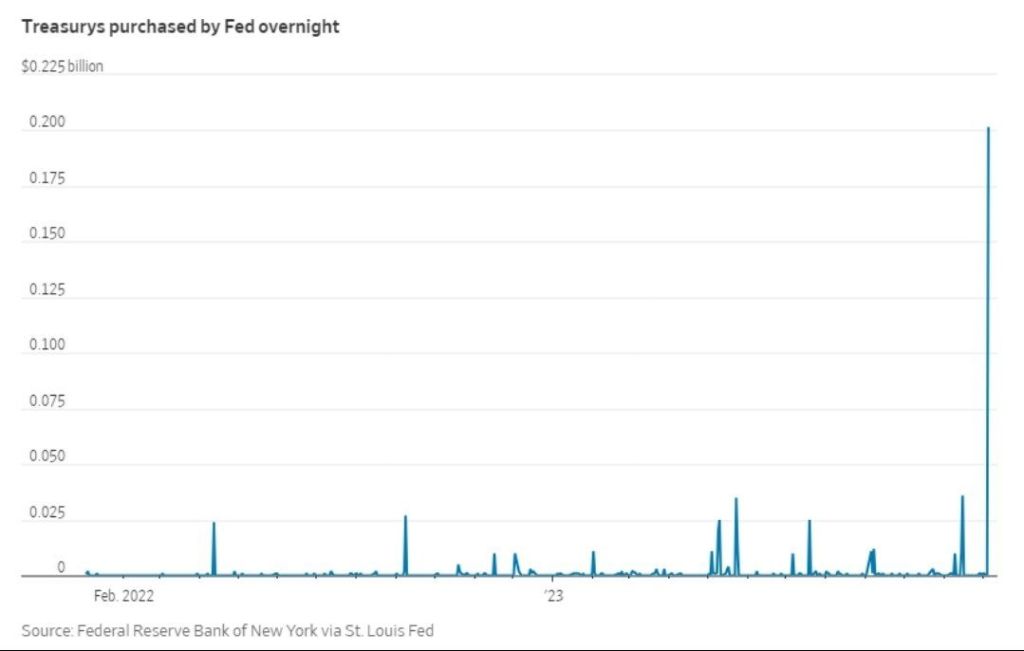

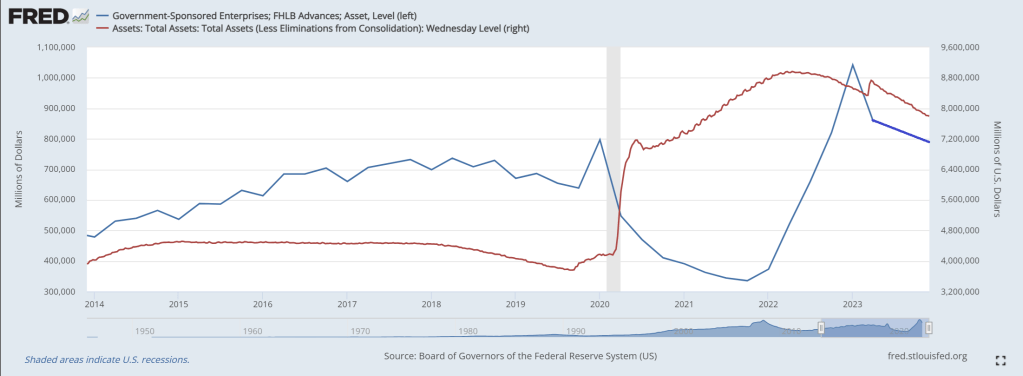

The Federal Home Loan Bank System (comprised of Federal Home Loan Banks or FLUBs) are a major source of American home loans and liquidity … at least until now.

According to a recently released report, the Federal Housing Finance Agency (FHFA) plans to propose rules that would curtail US banks’ borrowings from the Federal Home Loan Banks (FHLBs) to ensure they are not used as a “lender of last resort.” The announcement comes after the liquidity crunch in March spurred several banks to tap into the FHLB system, sending FHLB advances to a three-year high in the first quarter. During that quarter, when two large regional banks failed, FHLB advances totaled $804.39 billion, comprising 3.7% of banks’ total liabilities.

While totals have fallen since then, sitting at $602.62 billion, or 2.8% of total liabilities, in the third quarter, the FHFA is still seeking to impose limitations. Should the agency enact the new rules, banks’ liquidity options would be hindered. The FHFA wants Federal Reserve facilities to be used instead, but banks are reluctant to tap those because of the stigma attached to those sources, industry experts said.

“It is fair to argue that some banks have come to rely on FHLB funding as a crutch, and the ramp in lending to struggling banks during the mini-crisis in March is an area of continued debate,” Isaac Boltansky and Isabel Bandoroff of BTIG LLC wrote in a Nov. 11 note. “With that being said, there is still a clear stigma associated with tapping the Fed’s Discount Window and other facilities, which should be part of the conversation if the FHLB support will eventually be curtailed.”

Among the various rules the FHFA plans to propose is requiring that certain members have at least 10% of their assets in residential mortgage loans or equivalent mission assets, including assets that qualify as Community Financial Institution collateral, on an ongoing basis in order to stay eligible for FHLB financing.

The leading FLUB borrower? Columbus Ohio’s own JP Morgan Chase!

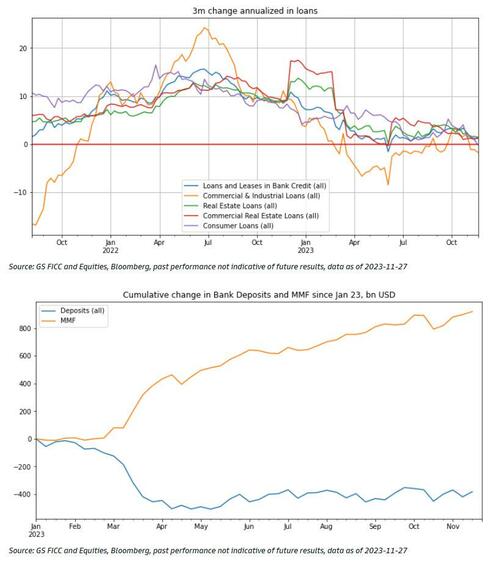

The problem is that bank credit growth has been contracting for several weeks now. 18th straight week of negative credit growth.

As FLUB advances decline with Fed balance sheet shrinkage.

You might as well face it, markets are “addicted to gov.” Government monetary interference, that is. Government money printing and massive Federal spending.

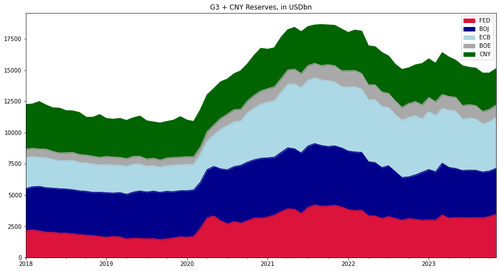

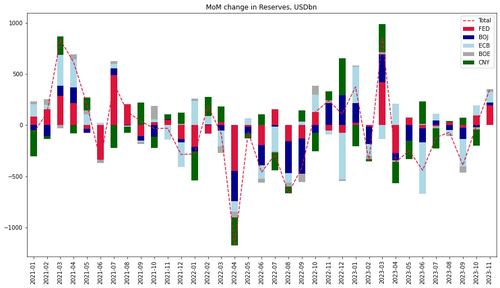

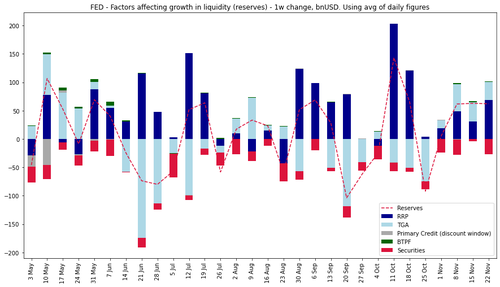

According to Goldman calculations, $350BN of liquidity (in USD terms) was added in November from the G4 central banks + the PBOC was nothing short of a fire hose.

In fact, this was the third largest monthly increase this year after January and March 2023.

The US addition of $60bn for a third consecutive week plus weaker dollar are the main drivers.

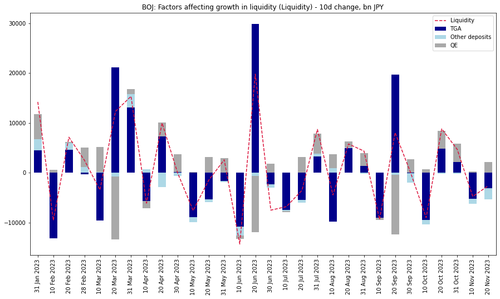

While the BoJ keeps adding liquidity via bond purchases, increases in the TGA balances in the past 20 days have net drained Yen liquidity.

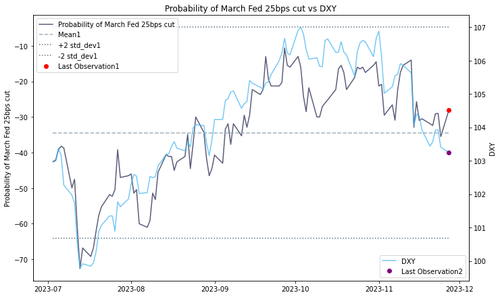

Looking forward over the year end and at the start of 2024, Goldman thinks that the US can keep adding liquidity via high bill issuance and RRP withdrawal over the next couple of months (something we discussed last month in “How Treasury Averted A Bond Market “Earthquake” In The Last Second: What Everyone Missed In The TBAC’s Remarkable Refunding Presentation“), while the dollar contribution to benign liquidity conditions could face some headwinds due to the risk of pricing out of some of the March Fed cuts as a result of the strong positive FCI impulse in November.

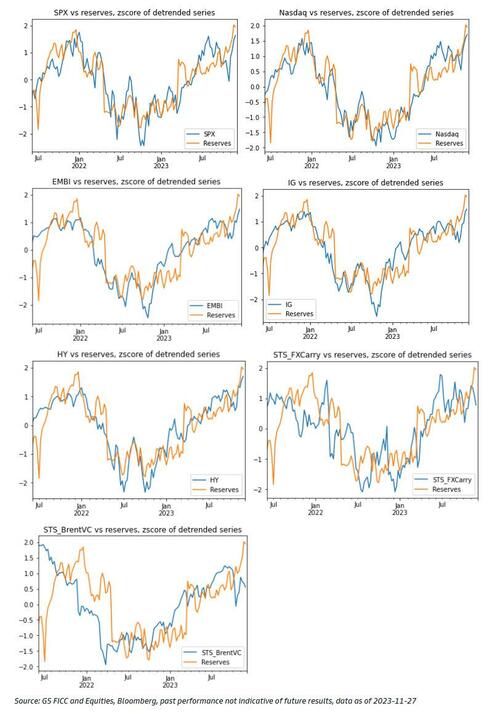

Goldman’s one-factor model for risky assets based on the liquidity cycle suggests that US IG and EM hard currency debt are cheap and the bank’s STS FX carry and Brent Vol Carry indices have under-performed the benign liquidity environment and may catch up the next two months.

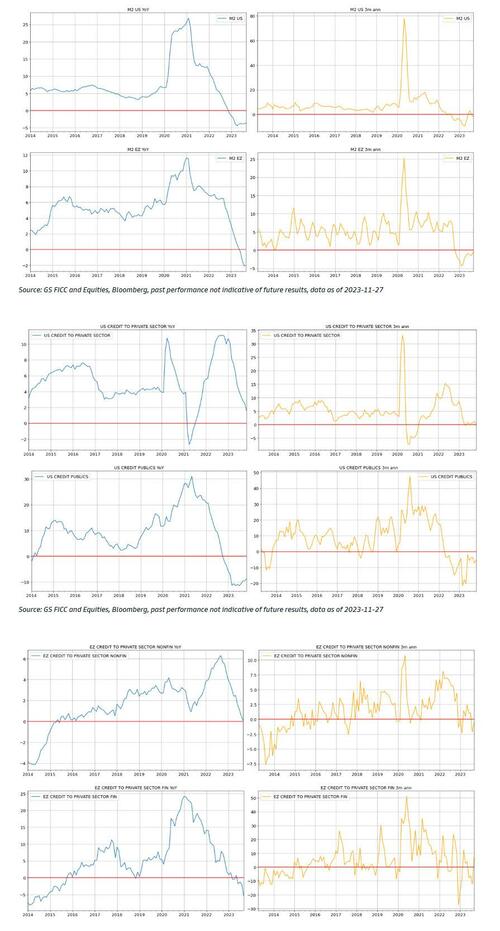

The US and Eurozone money supply and lending growth indicators remain weak, implying extended downside bias in domestic demand and inflation in H1-2024 (i.e., higher likelihood for easing absent a reflationary shock out of China or a supply-driven commodity price surge).

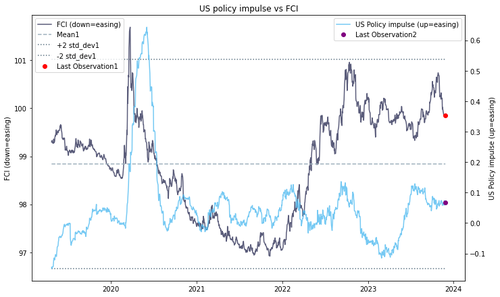

Finally, The US policy impulse (comprising of liquidity, fiscal stance, as well as nominal and real forward rates) has moved sideways in October and November after some renewed tightening in September. The GS FCI index eased nearly -100 basis points (-1.4z) in November.

Doctor, doctor (Yellen), we got a bad case of distortionomics (where the 1% wins and the 99% fall behind). After all, under Dr. Yellen as our Treasury Secretary, we are suffering from massive fiscal inferno with wild government spending. I would use “Government Gone Wild!” but the thought of Yellen … well, never mind.

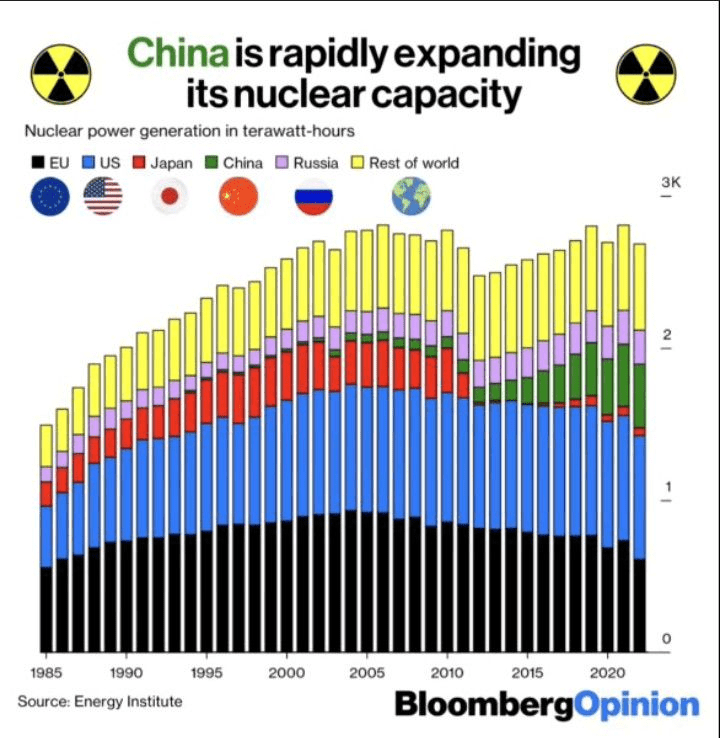

Meanwhile, while John Kerry pushes for ending ALL coal powered plants (good luck charging the thousands of EV charging stations on wind/solar power!), China is building NUCLEAR plants. While US green wimps (Kerry comes to mind) whine whenever nuclear plants are mentioned for the US.

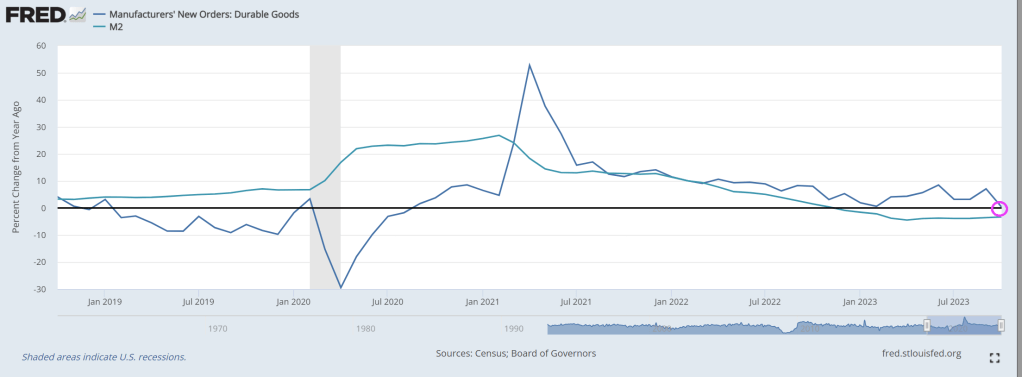

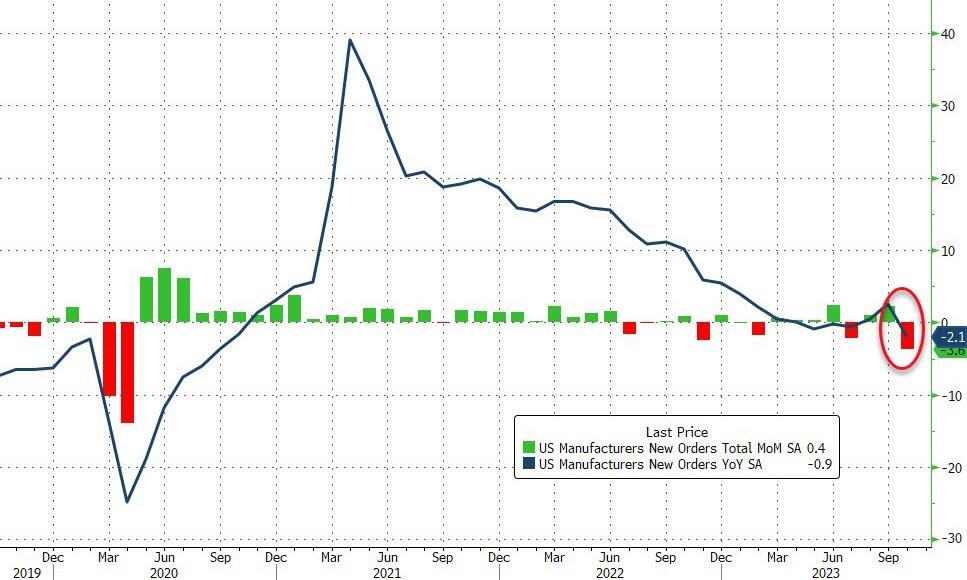

Factory orders tumbled even more than expected, down 3.6% MoM – the biggest drop since the COVID lockdowns (April 2020). September was also revised lower (making October’s decline even worse) from +2.8% MoM to +2.3% MoM…

Source: Bloomberg

The big monthly decline and revisions dragged orders down 2.1% YoY (the biggest drop since Sept 2020).

Core factory orders also dropped (-1.2% Mom), leaving them down 2.2% YoY – the eight month in a row of annual declines…

Source: Bloomberg

The final Durable Goods Orders data for October confirmed the preliminary print plunge down 5.4% MoM.

Finally, we note that it could have been a lot worse as Defense spending shot up 24.7% MoM (as non-defense dropped 15.8% MoM0…

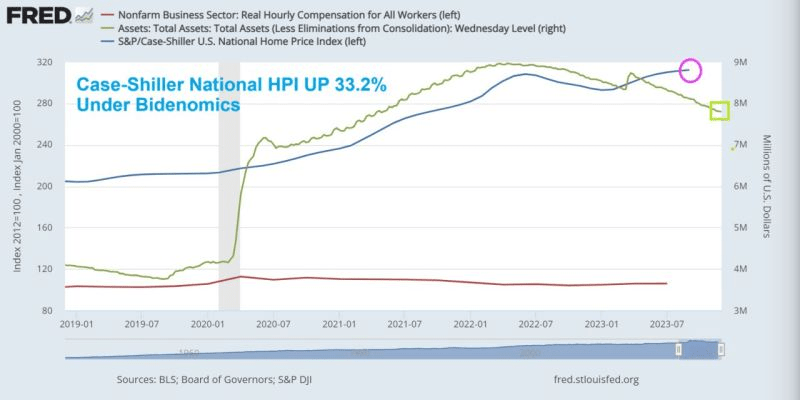

While the Case-Shiller National home price index is rising again, it has been slowing since March 2022. This is happening as “the honey pot” (aka, M2 Money printing) growth is now negative. While real hourly compensation growth is slightly, the average rate of growth since April 1, 2021, is -2.1%. (Not exactly what Biden wants to broadcast as a feature of Bidenomics).

According to a recent report from Point2 Homes, many recently bought homes, particularly in the hottest regions, are deep in the red. On average, single-family homeowners have been shedding $223 in property value every day since they bought their homes last year.

Condo owners are faring even worse, losing up to $336 a day in San Francisco, or a stunning $122,500 a year.

“This double-blow market means that the most newly minted owners were first hit by the highest home prices in history, only to be cut off from building wealth by the current falling prices,” analysts wrote.

Some major markets are seeing massive net losses

Single-family homes in 16 cities examined in the analysis have faced price declines of over $10,000 over the past year.

Memphis saw the most significant single-family price plunge, as well as the second-largest decline in condo prices, which analysts say could be due to rising inventory in the city.

Condo prices in 37 cities are also weakening, including in New York and Oakland.

So, what does this mean for homeowners? Folks who shelled out plenty of cash last year to secure their deals are now grappling with depreciating property values, which means it’s harder to build equity.

And if they want to sell in today’s market, they risk reaping less for their homes than what they paid for them. Zillow reports new buyers won’t sell at a profit until they’ve spent over a decade in their homes.

In another report from Redfin, analysts estimated that more than 3% of homes sold at a loss between August to October this year. The median amount was recorded at around $40,000, although some properties lost up to six figures on the sale.

Again, San Francisco sellers reported the biggest losses, with 1 in 7 homeowners losing money on their sales. And Memphis TN leads in percentage loss at -17.1%!

There are a couple of factors that could be contributing to the Golden City’s housing woes, including the rise of remote work coupled with tech layoffs pushing residents to relocate to other areas.

“There are buyers out there, but they’re a lot more cautious and picky than they were when mortgage rates were low,” Redfin Premier real estate agent Andrea Chopp said in September.

“The Bay Area housing market was unsustainable before, so this correction is probably healthy, but the unfortunate thing is prices remain unaffordable for a lot of people—especially with rates now above 7%,” she said.

97% of sellers are in the money, though

It’s not all doom and gloom for sellers—at least not for those who’ve been residing in their homes for a long time and bought when prices were much lower than they are today.

In many markets, sellers have been reluctant to let go of their low mortgage rates and apply for a home loan at a much higher rate, and that’s keeping inventory tight and prices high.

In the three months ending July 31, 97% of sellers across the country sold for a profit, with the typical home selling 78.4%, or $203,232, more than the seller bought it for, says Redfin.

And while San Francisco has been reporting more losses than usual, the median homeowner is still reaping $625,500 more on their home sale compared to the original purchase price.

The Godfather of San Francisco property losses, California Governor Gavin Newsom.

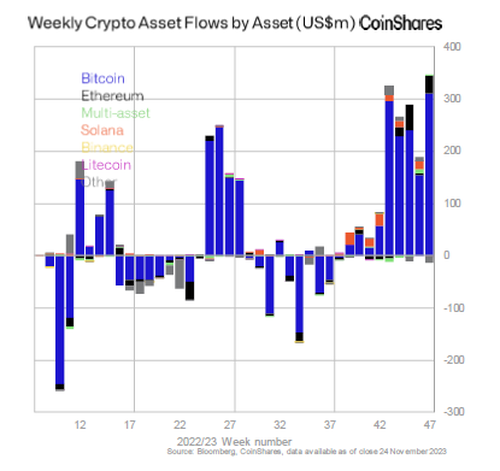

Joe Biden has a new name: the crypt keeper. As in the person through his economic screw-ups is causing a massive inflow to cryptos.

Anticipation of an eventual US spot Bitcoin ETF – which Bloomberg’s analysts assign a 90% probability of being approved by the SEC in January.

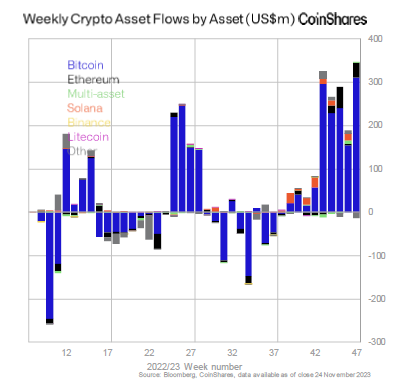

as well as surging prices, have helped to spur inflows into digital-asset investment products for a ninth consecutive week, the largest run since the crypto bull market in late 2021.

According to a recent report from CoinShares, these products which include trusts and exchange-traded products, saw inflows of $346 million last week, with Canada and Germany contributing to 87% of the total. Only $30 million came from the US, a sign of continued low participation from the country, the asset-management firm said. Of course, that will change as soon as investors start seeing double digit percentage weekly gains, and reallocating their money into crypto in droves, just like they did in 2020 and 2021.

Since early October, the crypto market has surged as traditional asset managers like BlackRock prepared for spot Bitcoin ETFs, potentially bringing in many more investors into the asset and resulting in inflows of tens of billions in fresh capital.

“The combination of price rises and inflows have now pushed up total assets under management to $45.3 billion, the highest in over one and half years,” the report said.

Bitcoin products raked in $312 million last week, pushing inflows to over $1.5 billion since the start of the year. Ether products saw $34 million in inflows last week, almost negating outflows all of 2023.

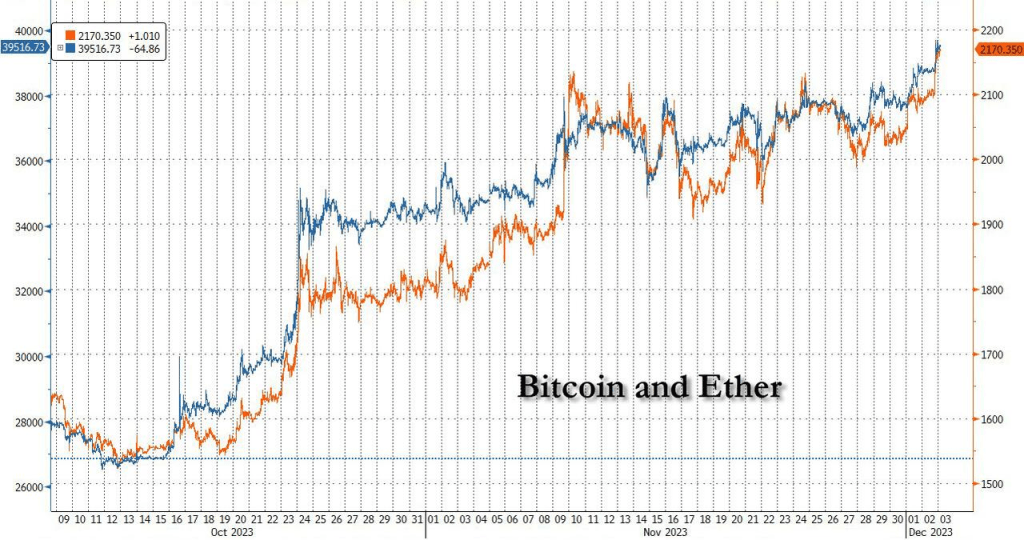

Amid the surging inflows, and amid expectations for imminent ETF approval by the SEC and a surge in March rate cuts odds, bitcoin and ethereum have continued their furious ascent, with the former now trading just shy of $40.

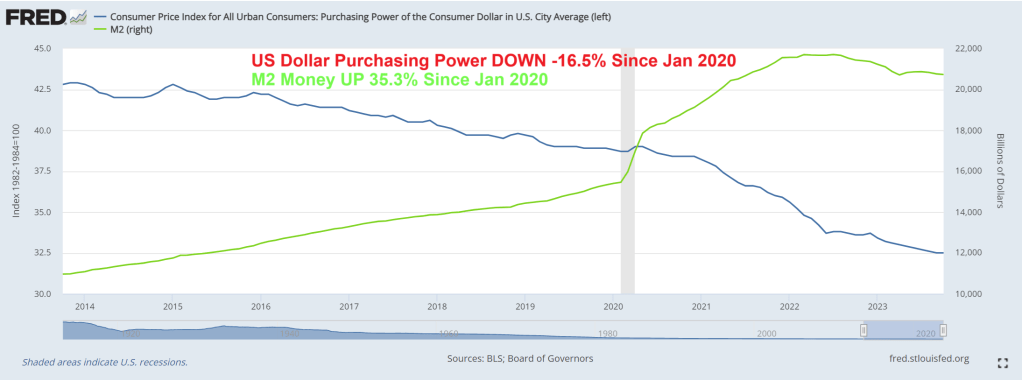

Since Covid and the idiotic government and school shutdowns of 2020, the purchasing power of the US Dollar has fallen -16.5% as M2 Money grew 35.3%. Keep on printing?

I suppose Biden’s biography can be called “Tales From The Crypt(o)”.

While members of the Biden Administration party at DC nightclubs, the rest of America are drinking Carlo Rossi wine (a favorite of mine in high school!) and eating Spam.

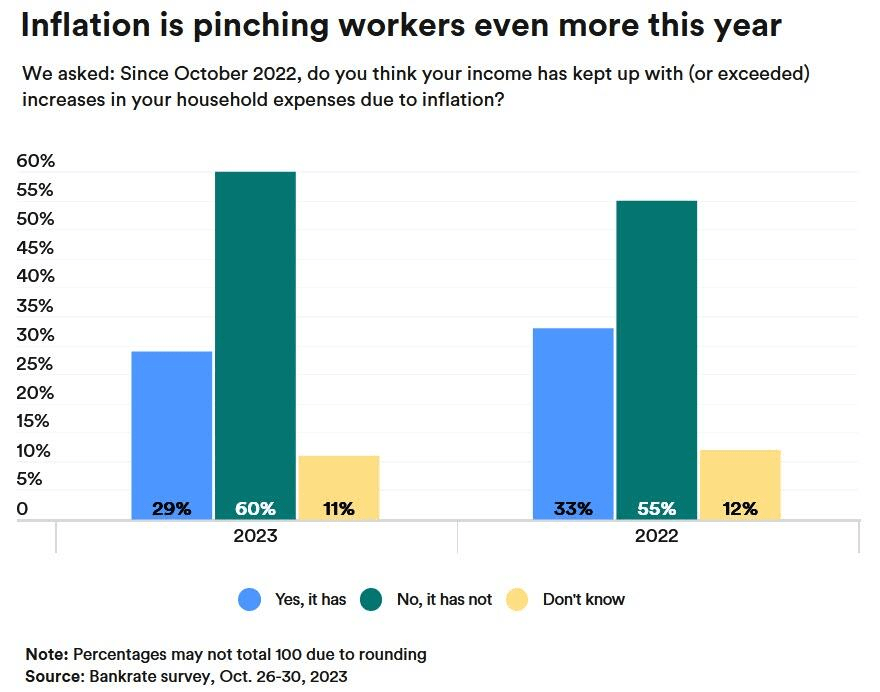

While hourly pay has increased, inflation has outpaced it.

Spending on basic survival needs like food, transportation, housing, and energy has increased, with households in the Mountain West facing the highest rates of inflation.

“We choose January 2021 as the base month because it was the last time inflation was within recent historical norms,” the report reads.

“Due to a combination of higher inflation rates and higher average household spending, inflation is imposing the highest monthly costs on families in the states of Colorado, Utah, and Arizona,” the report adds.

Families in Colorado and Washington, DC, are experiencing inflation costs higher than the national average.

Things are even worse in 2023 regarding inflation ravaging worker’s income. Over 60% of Americans reported that their wages were lagging well behind inflation.

Since January 2021, US purchasing power of the US Dollar is down a whopping -15.4% under Biden.

And home prices are up 33.2% under Biden, much of it due to The Feral Reserve money printing to fund Biden’s folicy initiatives. (I saw Biden claim he wrote the Inflation Reduction Act … the one thing we know is House legislation is written by an army of Congressional staffers, not El Presidente).

Home prices up 33.2% and purchasing power of US Dollar down -15.4% under Biden.

And like magic, Biden made $11,400 disappear from household income to pay for Bidenomics.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.