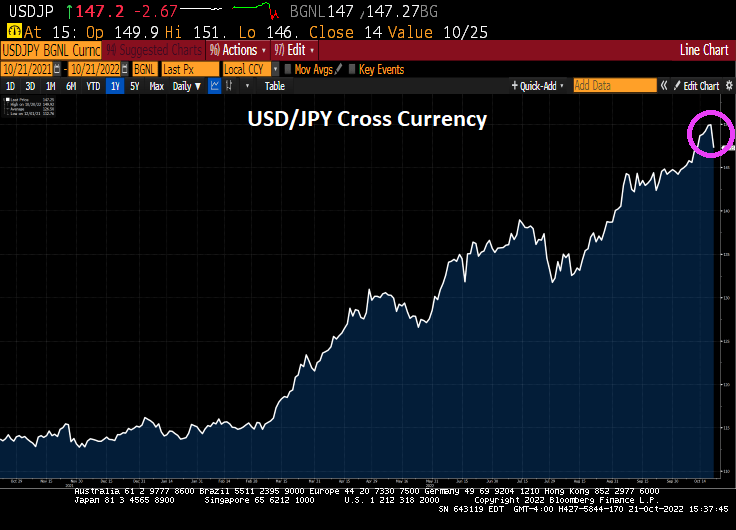

Wall Street saw another day of stunning reversals, with stocks rallying after a Treasury selloff sputtered. The yen jumped as Japan intervened again to prop up the currency.

After many twists and turns, the S&P 500 pushed solidly into the green and headed for its best week since June as 10-year yields fell from the highest since 2007.

Probably because The Fed is likely to pivot with impending recession. The Dow is up 774 points this Friday. And today was a huge option expiration day!!

And the 10-year Treasury yield fell -2.2 basis points.

Here is the result of Japan’s intervention.

But today’s numbers were largely monthly stock index option expiration.

Why did it fall upon Powell to be the wielder of the Fed tightening scimitar? Why didn’t Yellen? Because “Good Girls Don’t.” But Powell did.

Have a nice weekend. I will be rooting for Ohio State to annihilate the Iowa Hawkeyes at noon on Saturday.

One of my friends on Wall Street wrote my yesterday claiming “The 10-year Treasury yield is set to crash. Brace for impact!” Then I logged into Bloomberg this AM and saw the 10-year Treasury yield up almost 10 basis points (although it is down -2 BPS at 10:20am). Did markets not read his comments?? Maybe they did!

Well, The Fed is doing the Tighten Up. That is, The Fed is FINALLY removing their excessive monetary stimulus left over from the Bernanke Blowout (2008 adopting Japan’s print ’till you drop model).

But as The Fed removes their monetary stimulus (rate increases), we are seeing negative effects in the housing market. I call this chart “The X Factor.”

The US Treasury 10-year yield is up to 4.3% this morning, a far cry from 1.804% when Biden was crowned as President on January 20, 2021. The 30-year mortgage rate is up from 3.67% on Coronation Day to 7.32% yesterday, an increase of … 100% (that is, the 30-year mortgage rate has doubled under Biden). At the same time, Existing Home Sales YoY have gone from -2.41% in January 2021 to -23.79% in September 2022. THAT is a HUGE decline!

University of Michigan’s consumer sentiment for housing for 77 in January 2021 to 39 in November 2022. That is a -49% decline in consumer confidence. Also a big decline.

But going back to my pal’s email, he also said that The Fed is unwinding its balance sheet at a dangerously rapid rate (orange line). Relative to just increasing it, I would agree with him. But The Fed’s balance sheet is barely declining to my eyes. The troubling thing for housing is that inflation is so hot that REAL average hourly earnings YoY (yellow line) has fallen from +0.24% growth YoY on January 25, 2021 to a horrific -2.80% YoY rate in September 2022.

Bill’s point to me is that lending is still hot (at least commercial and industrial lending or C&I) while The Fed’s balance sheet remains in force (green line).

The Fed has a lot more work to do if they want to cool the commercial lending market. They have successfully slowed down the residential mortgage market.

Today’s existing home sales were … gruesome. While EHS month-over-month were down only -1.5%, on a year-over-year basis EHS was down a staggering -23.79%.

If you look at the declining growth rate of M2 Money (green line) and rising mortgage rates (yellow line), we can see why the housing market is struggling.

How about median price? That dropped to 8.07% YoY as inventory for sale remains lower than before Covid and Covid stimulypto.

US 30-year mortgage rates rose to 7.20% yesterday, the highest rate since 2000. Why?

Core inflation is rising and its the highest since 1992. Diesel prices, the all-important fuel for the transportation industry, is rising again after a brief respite and is near the all-time high.

But will mortgage rates continue to rise? That depends on The Federal Reserve. Will they continue to try to combat inflation (largely caused by … The Federal Reserve and voracious Federal spending under Biden/Pelosi/Schumer (The Three Amigos).

As of today, investors in Fed Funds Futures are pointing to a peak of Fed tightening in May 2023, then a slow decline in rates.

While this is The Fed Funds rate, it is likely that mortgage rates will continue to rise to May 2023 then level out at 9%-9.25%.

I really miss teaching college students. An example of a test question I gave was the first chart: who was The President when all hell broke loose (pink box)? 1) Joe Biden, 2) Donald Trump or 3) Millard Fillmore?

The answer, of course, is Joe Biden.

Doesn’t Millard Fillmore, the 13th President of the United States, look like actor Alec Baldwin after too many cheeseburgers and chocolate milkshakes at In-N-Out Burger?

Bear in mind that the are numerous wildcards in play, like the Russia/Ukraine war and the probability the China will invade Taiwan in the near future.

Well, this isn’t good. But it is consistent with the highest inflation rate in 40 years and The Federal Reserves’ counterattack. Basic mortgage applications are now down to their lowest level since 1997 as mortgage rates rise.

Mortgage applications decreased 4.5 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending October 14, 2022.

The Refinance Index decreased 7 percent from the previous week and was 86 percent lower than the same week one year ago. The seasonally adjusted Purchase Index decreased 4 percent from one week earlier. The unadjusted Purchase Index decreased 3 percent compared with the previous week and was 38 percent lower than the same week one year ago.

Bear in mind that these numbers are for the week of October 14, so the home purchase season is in the “house latitudes.” That is, the slow season for home sales. The refinancing applications index has dropped thanks to Fed tightening.

I love to teach, but my students at Chicago, Ohio State and George Mason would fall asleep when I would discuss repurchase and reverse repurchase agreements (or REPOs and Reverse REPOs). But repos and reverse repos are a critical part of the banking system.

In short, the Repo market is a window into what’s going on behind the scenes.

As Bidenflation soars, and The Fed counterattacks, we see Fed’s repo market remains elevated. Note that The Fed’s balance sheet (orange line) is only slowly being reduced.

Right now, the risk lurking in the shadows is Balance Sheet Runoff. The Fed, the markets, the regulators, have limited experience with the Fed shrinking the balance sheet. Bottom line: there’s a risk that Balance Sheet Runoff will breaking something.

The global stock market is up again today, despite Fed tightening and a war in Ukraine. The Dow is up 1.38% and the S&P 500 is up 1.75%.

Likely cause? Rumors that The Fed and other global central banks will pivot sooner than later.

It is likely that The Fed will pivot to prevent a crash and the stock market in pricing in that pivot.

Bernanke, Yellen and Powell are NOT Paul Volcker. In fact, I am coining a new nickname for Fed Chair Jerome Powell: Pivot Powell.

Over the past year, the dollar has been on a tear: The U.S. Dollar Index, which measures the dollar’s strength against a basket of foreign currencies, is up 18%. And up 25.2% under 80-year old US President Joe Biden (well, he will be 80 in November).

For tourists, a strong dollar is great news. It means you get more for your money abroad.

But for investors, a beefed-up buck is decidedly bad news.

When the dollar strengthens, that means foreign revenues are going to translate into fewer dollars. Those earnings are going to come in lower and any overseas investment you own is going to hurt you in a rising dollar environment.

The US CPI for electricity is up 24% under Nuclear Joe as The Fed continues to leave their balance sheet relatively untouched.

You might have to bail on the stock market to stay warm this winter, but it is a shame that the S&P 500 index is down -25.3% in 2022 as The Fed counterattacks Bidenflation.

You must be logged in to post a comment.