Biden is the opposite of the miserly Scrooge McDuck. He gives billions to Ukraine and spends trillions on various Federal projects without batting an eye as to how and who is going to pay for all the spending. And Biden’s latest election pandering is no different.

Speaker Pelosi claims that Biden’s bold action on student loan forgiveness is a strong step in Democrats’ fight to … make college even MORE expensive and lead to colleges hiring even MORE administrators (aka, apparatchiks) making colleges even MORE bogged-down in red tape.

And Speaker Pelosi, the costs of Biden’s midterm election buy of votes is estimated to be $300 BILLION. And a report from the Brookings Institution observed that one-third of student debt is owed by the wealthiest 20% of households, while only 8% is owned by the bottom 20%.

So, Biden is letting AOC write-off $10k of her student loan obligation. Bear in mind that the $10k forgiveness is taxed by The Federal government as income.

It looks like The Fed will have to expand the M2 Money supply to pay for “Billions Biden’s” spending spree.

The phrase “crossing the Rubicon” is an idiom that means that one is passing a point of no return. Its meaning comes from allusion to the crossing of the river Rubicon by Julius Caesar in early January 49 BC.

Indeed, the US crossed the FISCAL Rubicon in Q4 2012. That is when US Treasury Public Debt outstanding exceeded Real GDP. And the gap has been growing ever since.

In case you were wondering why M2 Money Velocity is so low, it is because the US is in constant crisis management mode as an excuse to spend trillions of dollars …. that generates progressively lower real GDP.

They built this nation on MMT (Modern Monetary Theory) which translates to the Federal government and Federal Reserve just wanting to spend trillions and trillions. Since 2005 (the peak of the housing bubble), the US Federal Reserve has increased the M2 Money stock more than real GDP growth in almost every quarter.

I remember when macroeconomists used to say “Everything is beautiful … as long as M2 Money growth is LESS than real GDP growth.” But we have apparently shifted to MMT when Everything is beautiful as long as there is a crisis and Congress can spend trillions.

Now Biden/Congress are spending billions in trying to reduce inflation (seriously, only in Washington DC would they think that massive spending bills would REDUCE inflation).

Under President Biden, inflation has soared and The Federal Reserve claims that they want to extinguish the inflation fire by tightening monetary policy … resulting in rising mortgage rates. Under Biden, mortgage purchase applications are DOWN -41.5% while mortgage rates are UP 96%.

(Bloomberg)The US mortgage industry is seeing its first lenders go out of business after a sudden spike in lending rates, and the wave of failures that’s coming could be the worst since the housing bubble burst about 15 years ago.

There’s no systemic meltdown coming this time around, because there hasn’t been the same level of lending excesses and because many of the biggest banks pulled back from mortgages after the financial crisis. But market watchers nonetheless expect a string of bankruptcies broad enough to trigger a spike in layoffs in an industry that employs hundreds of thousands of workers, and potentially an increase in some lending rates. More of the business is now controlled by independent lenders, and with mortgage volumes plunging this year, many are struggling to stay afloat.

Please note that mortgage purchase applications are DOWN -41.5% under Biden while mortgage rates are UP 96%.

Margin Calls Many other lenders have seen the value of their loans drop, said Scott Buchta, head of fixed-income strategy at Brean Capital, an independent investment bank. The Federal Reserve has tightened rates by 2.25 percentage points this year in an effort to tame inflation, and 30-year US mortgage rates have surged above 5% for government-backed loans. That’s close to their highest levels since the financial crisis, from around 3.1% at the end of last year.

That’s beaten down the value of home loans made just a few months ago. A mortgage made in January and not eligible for government backing could have traded in early August somewhere around 85 cents on the dollar. Lenders usually try to make loans worth somewhere around 102 cents to cover their upfront costs.

For a lender whose loans dropped to 85 cents, the losses can be debilitating, even if they aren’t realized yet. On top of that, business is broadly plunging. Overall mortgage application volume has plunged by more than 50% this year, according to the Mortgage Bankers Association. These business conditions are spurring banks that provide lines of credit known as warehouses to make margin calls and cut credit.

“The warehouse lenders in this industry seem to be extremely on top of things in this downturn, unlike in ‘08,” said bankruptcy attorney Mark Power, who is representing creditors in the First Guaranty bankruptcy. “They are making margin calls quickly.”

Banks have emergency funding they can tap in times of crisis, which can often allow them to stay afloat in hard times. But not always: emergency financing from the Federal Reserve is usually only available for solvent institutions with a chance of recovering. In the last downturn, so many banks had so many soured loans and struggling assets of all kinds that hundreds failed. Nonbanks went bust as well.

The US housing market is sensitive to Fed “catch-up” monetary tightening. For example, the NAHB’s traffic of prospective homebuyers declined rather dramatically in August as The Fed tightened rates and the 30yr mortgage rate rose. That is what I call a “Nestea Plunge.”

How are mortgage rates impacted by Fed monetary policy? While The Fed began really “sloshing” markets with excess stimulus (QE in late 2008), the latest round of QE (or asset purchases) came with the US Covid shutdowns (what genius thought of that??) and that stimulus has NOT been withdrawn yet. Only the Fed Funds Target rate has tightened.

The 30yr mortgage rate rose with Fed rate tightening, but the Fed’s System Open Market Holdings (SOMH) of Treasury Notes and Treasury Bonds has come down a bit. But not the pare-down The Fed has hinted at. The 30yr mortgage rate is cooling as the prospect of future Fed rate hikes declines.

As of this morning, The Fed Funds Futures market points to rates rising until March 2023 … then easing again.

One reason The Fed has been slow to sell assets off its balance sheet is that a large chunk of T-Notes and T-Bonds are maturing shortly. It will be a matter of whether The Fed reinvests the proceeds or lets the balance sheet wind-down.

Real estate investment trusts (REITs) are an interesting asset class, allowing investors to purchase shares in large-ticket assets like multi-family properties or shopping centers. But given the changing landscape due to online shopping (aka, the Amazon effect), Covid economic shutdowns, etc., REITs should be having a hard time. But aren’t. How come?

Covid economic shutdowns definitely took its toll on retail shopping centers, as an example. And you can see the plunge in the NAREIT All equity index in early 2020. But the NAREIT All-equity index rallied … until The Federal Reserve started tightening their loose monetary policy. Note that as the implied O/N rate rose (orange line), REIT shares declined.

But as the WIRP implied O/N rate settled (pink box), the NAREIT index began to climb again. It is clear that REITs, like other equities, benefit from Fed easing. But how long will The Fed continue tightening?

As of this morning, The Federal Reserve is anticipated to raise their O/N rate to 3.738% by March 22, 2023. Then begin lowering their target rate … again.

Sadly, REITs, like other equity investments such as the S&P 500 index, are sensitive to The Fed’s easing/tightening. Look for REITs to struggle as The Fed tightens, then rally as The Fed eases again.

Here is the (in)famous Hindenburg Omen. Notice how the Hindenburg Omen alarm bells (yellow and red dots) have been silenced by The Fed. But as The Fed tightens (at least until March ’22), we may see the Hindenburg Omen flashing again. Call it the Powellburg Omen.

The NCREIF property index had a decline in the Covid-outbreak era (early 2020) and you can see a slight slowdown in the NCREIF index as The Fed started tightening to fight inflation.

Today’s US industrial production and capacity utilization numbers showed a nice “steady as she goes” slow decline from previous months, though still positive at 3.90% YoY.

And it is difficult to argue that the US is in a recession when capacity utilization is at 80.27%.

Notice that industrial production growth falls below 0% during a recession and capacity utilization slumps. We are NOT there … yet.

However, M2 Money growth is shrinking awfully fast.

While the US is technically in default (two consecutive quarters of negative GDP growth), it doesn’t FEEL like a recession with 3.90% YoY industrial production growth and capacity utilization above 80%. During the Covid recession in early 2020, industrial production growth YoY had declined to -17.65% and capacity utilization shrank to 64.53%.

Speaking of a recession SIGNAL, the 10Y-2Y Treasury yield curve is SCREAMING impending recession.

The 2020 Covid outbreak led to a massive (and generally awful) reaction. There were economic shutdowns that caused extensive damage (particularly to small firms), but it was the massive overreaction by The Federal government in terms of Covid relief and The Federal Reserve’s expansion of the money supply that caused considerable damage.

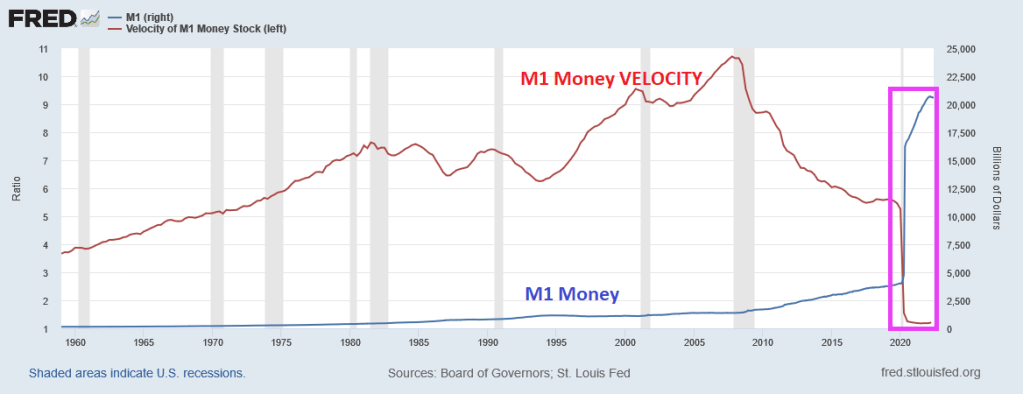

One truly horrific chart is that of M1 Money and M1 Money Velocity (M1/GDP). M1 Money surged with Covid driving M1 Money Velocity down to levels never seem before.

The broader measure of money, M2, isn’t as dramatic, but we also see that M2 Money VELOCITY has plunged to levels never seen before.

What does low money velocity indicate? Simply put, The Fed is printing trillions of dollars, but GDP isn’t moving much. But that won’t stop Congress from spending (and using The Fed to buy its debt).

So, here we sit. This morning, the US Treasury yield curve (10Y-2Y) remains inverted. This AM, the curve inverted another -.591 basis points to -42.725, a sign of impending recession.

Yes, we are living through Jay Powell’s famous chili episode where money velocity is near historic lows and we have an inverted yield curve.

BTW, congratulations to Will Zalatoris (aka, Happy Gilmore’s caddy) for his first PGA Tour victory at the FedEx St. Jude Championship!

Politicians like to (falsely) take credit for things, such as Biden bragging about gasoline prices declining. Bear in mind that regular gasoline prices were $2.88 when Biden was inaugurated as President, rose to over $5 a gallon in June and now have declined to $3.98 for which Biden is taking credit. So, regular gasoline prices are still up 34% under Biden. Ouch!

But other rates and prices are dropping too. Bankrate’s 30yr mortgage rate started at , broke the 6% plane on June 21, 2022 only to drop to 5.53% on Friday. CRB’s foodstuffs price index started at 370.58 on Biden’s inauguration as President, rose to 606.71 on May 17, 2022 then retreated to 561.32 on Friday, August 13th. Even headline inflation (CPI YoY) is cooling … slightly.

You can see the recent declines in mortgage rates, gasoline and food prices (pink box) that corresponds to a shrinking of the US M2 Money stock growth. M2 Money is still growing at torrid pace (8.5% YoY) almost back to pre-Covid stimulypto levels of 6.8% YoY. So shrinking M2 Money growth is helping reduce mortgage rates and inflation, food/gasoline prices.

Instead of trying to remove Fed stimulus even more, Biden and Congress passed the “Inflation Reduction Act” which will barely scratch inflation and raises taxes across the board (despite Biden’s promise that no one making under $400,000 will see a cent of increase taxes). And Biden’s preposterous promise ignores the inflation tax which has been severe and still growing at 8.5% YoY. Not 0% as Biden and Harris claimed.

But wait for winter as food, gasoline and heating prices start to soar again.

My favorite dim-witted explanation of inflation belongs to Democrat Representative Pramila Jayapal who recently claimed that “inflation is a theoretical word that economists use.” Like the brilliant Milton Friedman???

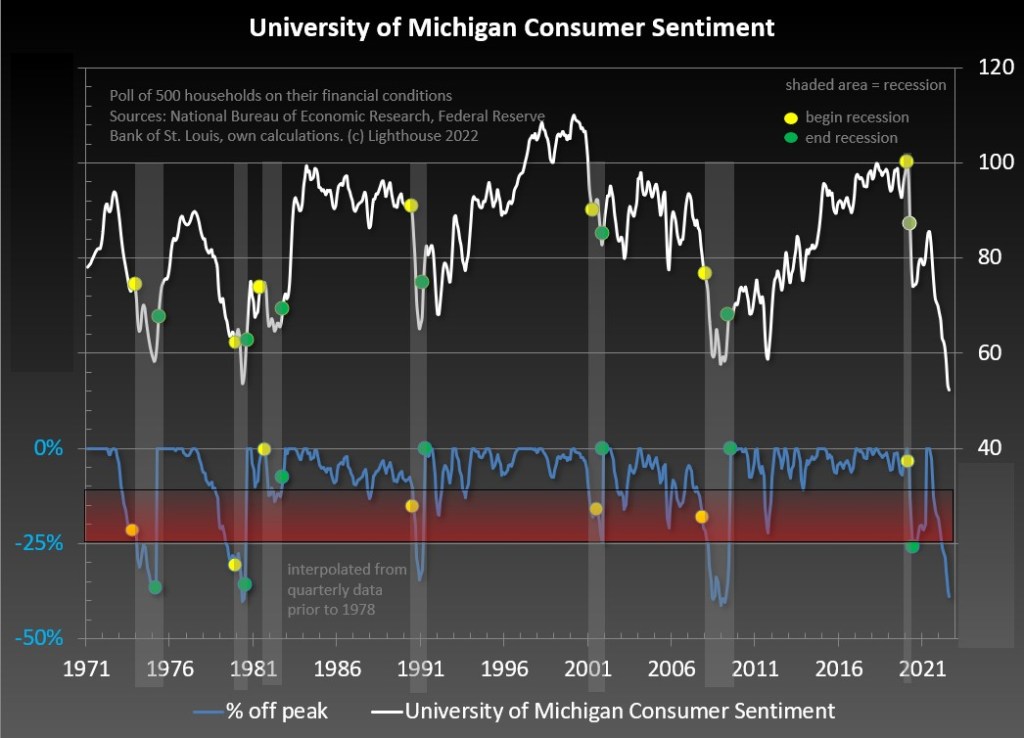

The University of Michigan consumer survey is out for August and the results show improvement … from disastrous to just plain horrible.

The University of Michigan Buying Conditions for Houses remained depressed and didn’t improve.

Bear in mind that today’s consumer sentiment reading in the lowest since 1970, lower than during any recession.

The Conference Board’s leading economic indicator plunged in June despite nearly $8 trillion in Fed stimulus still outstanding.

The good news? President Biden and his son Hunter boarded Air Force One for a carbon-spewing plane trip to South Carolina for a one-week vacation. At least he can do less damage to the US while on vacation.

I scratch my head when I here Fed talking heads discuss how to get inflation back down to 2%.

Of course, the easiest way is to 1) remove Biden’s anti-fossil fuel executive orders that limit the supply of crude oil and natural gas, but that isn’t going to happen. 2) stop Federal spending, but Manchin and Sienma enabled Biden/Schumer/Pelosi’s “drunken sailors in port” spending sprees, so Federal spending is likely to not be stopped. 3) raise taxes (Larry Summer’s suggestion) to cool-off demand. And give MORE money our Federal government? No thanks. 4) raise The Fed target rate to 22%.

Yes, the Taylor Rule suggests a target rate of … 22% to tame the savage inflation beast, based on 8.50% CPI YoY.

The problem, of course, is that 22% is higher than the previous high of 20% under Fed Chair Paul Volcker in 1981. And Volcker didn’t have the Bernanke Bonanza (aka, quantitative easing). Look at the monetary stimulypto, since 1981 and particularly since Covid.

Will The Fed raise rates to 22%? Well, Fed Futures is pointing at the target rate hitting 3.6% by March 2023, then falling again.

Its mission impossible to get to 22%, particularly since Biden/Schumer/Pelosi won’t cool it on Federal spending.

You must be logged in to post a comment.