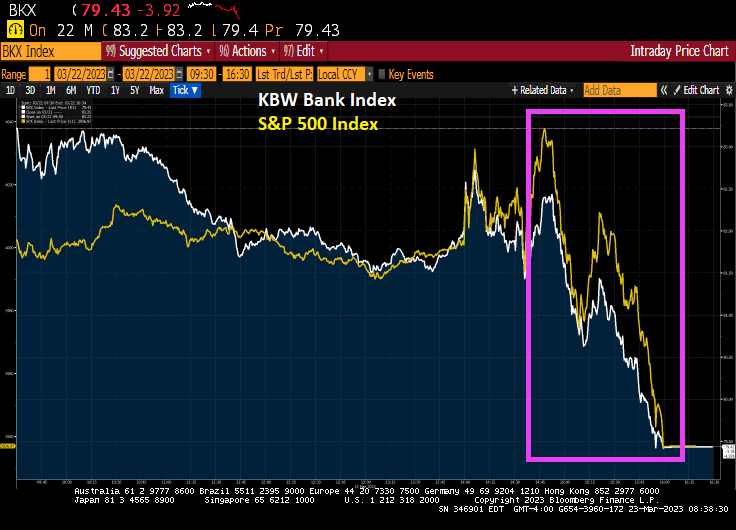

Like the old EF Hutton ads, when Treasury Secretary Janet “Too Low For Too Long” Yellen speaks, people listens. Particularly when she reverses course after bailing out he Silicon Valley/Big Tech buddies by guaranteeing deposits. Then in a US Senate hearing AFTER Fed Chair Powell tried to calm markets, Treasury Secretary Janet Yellen told Senators yesterday that ‘Blanket insurance’ of bank deposits is not being discussed. Look out below!

So why did the Biden Administration and Janet Yellen bail out Silicon Valley Bank (SVB), regulated by San Francisco Federal Reserve (run by Mary Daly)? And then tell the US Senate “That’s it!”??

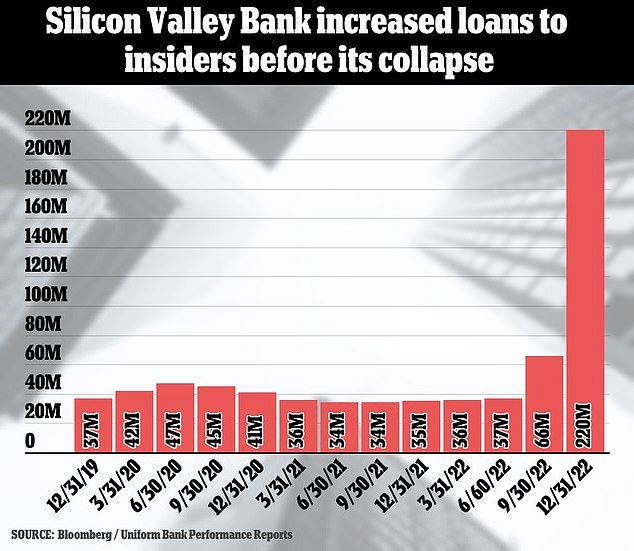

Where was Mary Daly when SVB increased loans to INSIDERS before its collapse? And will Daly/Yellen actually punish the CEO of SVB who jetted off to Maui after the collapse rather

Perhaps SF Fed’s Mary Daly should be prosecuted for negligence. Or thinking that SVB is unreserved.

You must be logged in to post a comment.