All together now. The Fed has been printing too much money for too long and Biden restricts fossil fuel production. Ad in rampant Federal spending and we have INFLATION. Inflation led to The Fed to raise rates. And with rate increases and down go the banks.

Of course, The Fed and Biden Administration will overeact (e.g. offering deposit insurance on ALL deposits above $250,000 creating moral hazard risk). As such, we are seeing gold prices soar by 2% this AM.

In adddition to gold rising 2%, natural gas futures are up 6%

One indicator that the Biden Administration will herald is that average hourly earnings rose to 4.6% Year-over-year (YoY). Too bad headline inflation is still at a whopping 6.4% YoY.

More jobs were added to the US economy than forecast (311k actual versus 225k forecast). The U-3 unemployment rate rose to 3.6% from 3.4% in January.

The aftermath of the jobs report? 2-year Treasury yields are down a whopping -15.8 basis points. But Europe is seeing double digit declines in sovereign yields as well.

At the 10-year tenor, we see the US Treasury yield drop -12.8 basis points. Much in line with European sovereign yield declines.

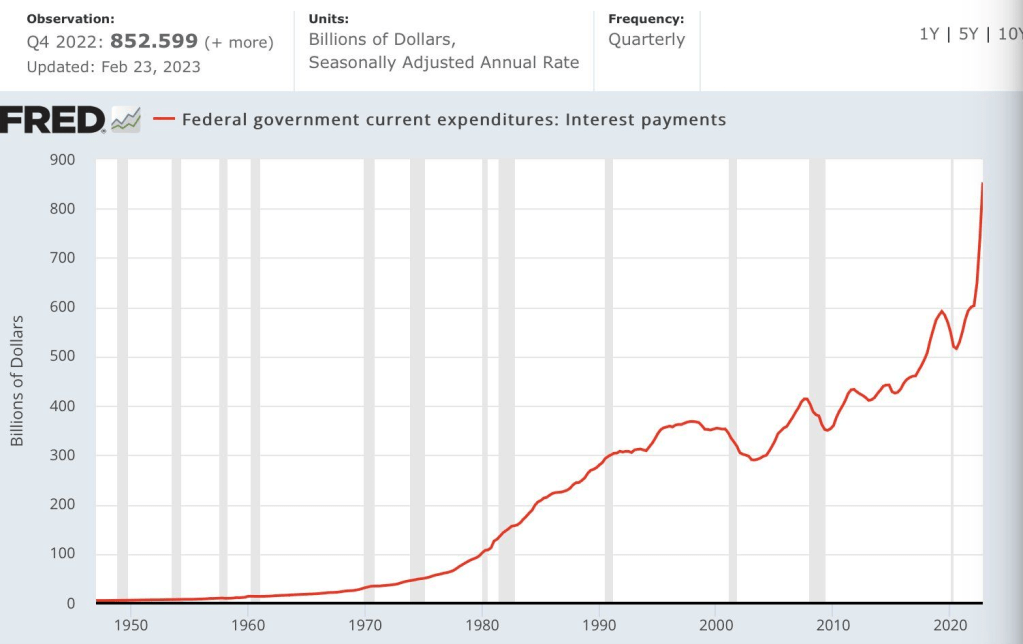

As Americans are painfully aware, inflation is still haunting us. Despite Administration proclamations that inflation is declining, it is rising again. And with rising inflation (and an overheated labor market), The Federal Reserve is in full counterattack mode, withdrawing stimulus and raising rates.

And with Fed tightening comes rising 30-year mortgage rates.

Out of boredom, I watched the Clive Barker film “Hellraiser” and noticed perpertual Democrat Presidential candidate Hillary Rodham Clinton in the cast as the female Cenobite.

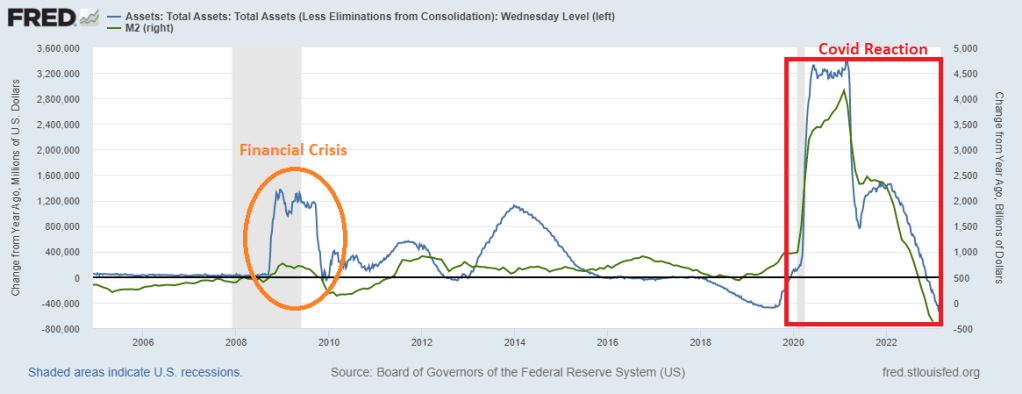

But despite how bad the financial crisis of 2008/2009 was, the growth of Fed assets on it balance sheet (orange oval) paled in comparison to The Fed’s overreaction to the Covid outbreak of 2020. And the government shutdowns and mask mandates.

The good news? The rate of growth YoY of both The Fed’s balance sheet and M2 Money is negative. But it is still startling to see the comparison of Fed reactions to crises.

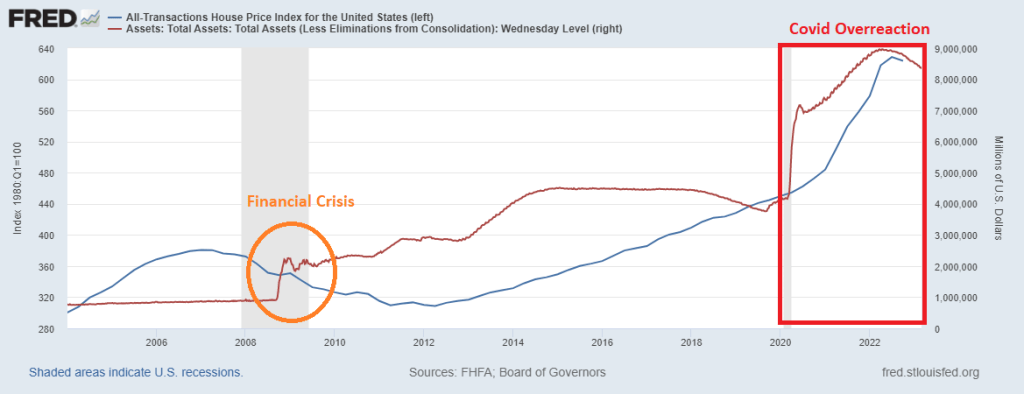

Give The Fed three steps to catch up to the mayhem they created. Particularly in inflation home prices.

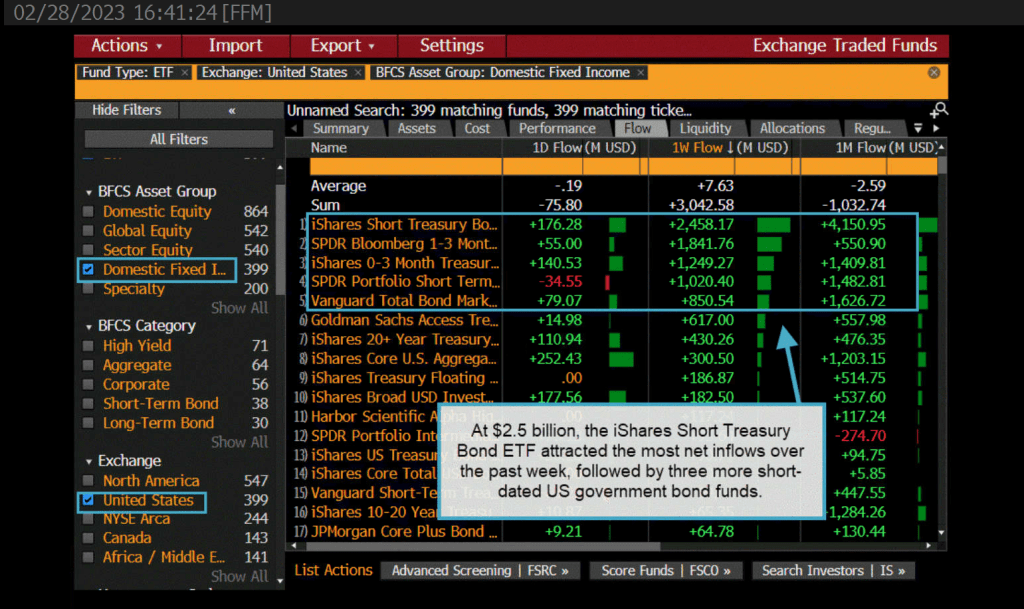

As The Federal Reserve reaffirms their draining of the monetary punch bowl, we are seeing investors flock towards the bond market. Particularly the iShares Short Treasury ETF. $2.5 BILLION to be exact.

Meanwhile, credit ETFs are hammered by record outflows of almost $12 Billion.

The reason why? Inflation remains elevated which is leading The Fed to keep their foot on the monetary brake pedal.

The gap between the VIX Put-call volume and CBOE Put-call ratio is the widest since 2006, the precursor of a major volatility spike.

Meanwhile, for those of you interest in railroad regulatory issues, as a general matter, regulations are rarely ever “reversed,:” but rather modified or replaced with changes. No administration would be able to outright “repeal” a major safety regulation because it almost certainly be immediately enjoined by a court and found to be counter to Congressional delegation.

I assume most of the attention will be on this final rule (https://www.federalregister.gov/documents/2020/10/07/2020-18339/rail-integrity-and-track-safety-standards) published and effective on Oct 7, 2020. It is considered”deregulatory” in the sense that it results in an economic or compliance cost savings, mostly owing to a change in the permissible type of track integrity monitoring, and decrease in the resulting number of “slow orders.”

Unlike Pete Buttigieg who apparently did not read the regulations when he blamed Trump, read the actual published “deregulation.” A faulty railcar axel which was the cause of the East Palestine Ohio trail derailment was NOT impacted by the “deregulation.” Instead of Mayor Pete, he should be called “Cheap Shot Pete.”

Mortgage rates increased across all loan types last week, with the 30-year fixed rate jumping 23 basis points to 6.62 percent – the highest rate since November 2022. The jump led to the purchase applications index decreasing 18 percent to its lowest level since 1995.

Mortgage applications decreased 13.3 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending February 17, 2023.

The Market Composite Index, a measure of mortgage loan application volume, decreased 13.3 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index decreased 4 percent compared with the previous week. The Refinance Index decreased 2 percent from the previous week and was 72 percent lower than the same week one year ago. The seasonally adjusted Purchase Index decreased 18 percent from one week earlier. The unadjusted Purchase Index decreased 4 percent compared with the previous week and was 41 percent lower than the same week one year ago.

Did Biden appoint “Pothole Pete” Buttigieg to oversee the mortgage market??

Biden’s State of the Union address saw him bragging about his record job creation (actually, it was the private sector, not Biden than created jobs) and historic unemployment rate. What Biden didn’t mention (along with not discussing the porous Mexican border with fentanyl pouring across or why he failed to shoot down a Chinese spy balloon until after it has passed over numerous military reservation) is that the unemployment rate always hit a low point just prior to a recession.

So, here we sit at 3.4% unemployment. But we also see the US Treasury yield curves (10Y-3M and 10Y-2Y) remaining deeply inverted.

The US Treasury 10-year yield is up 5.5 basis points today.

And Bankrate’s 30-year mortgage survey rate is up slightly today.

Here is where we set today. The cost of insuring for a US debt default remains elevated as the US has hit its statutory debt limit. This is happening at the effective rate of interest on US mortgage debt is rising.

Help us McCarthy! Because Biden and Schumer don’t want to cut ANY spending.

There was a hilarious film with Hillary Swank and Aaron Ekhart called “The Core” where earth’s core stops spinning and the earth gets cooked by the Sun’s rediation. Now we learn that the Earth’s inne core has actually stop spinning. This time, however, all that has happened is that Joe Biden is President which is almost as bad,

But also related to “The Core” is that the important Personal Consumption Expenditures (PCE) are out for December along with PCE price deflator numbers. In short, personal income was up 0.2% month-over-month (MoM) in December while personal spending was down -0.2%. REAL personal spending was down -0.3% MoM.

But the all important PCE deflators numbers were down all well. The REAL PCE price index (or deflator) was down to 5.0% YoY in Decmember while REAL CORE price index was down to 4.40%. All this is happening as M2 Money growth has stop spinning (down to -1.3% YoY in December).

Based on a CORE PCE YoY of 4.40%, the Taylor Rules suggest that The Fed Fund Target rate should be … 10%. However, the current Fed Funds Target rate is only 4.50%, so The Fed is not even half way there.

Fed Funds Futures are pointing to a peak rate of 4.90% by the June ’23 FOMC meeting, then a pivot (despite denials from Fed talking heads).

Of course, The Fed doesn’t follow the Taylor Rule or any other transparent rule for rate management. Rather, Fed Chair Powell like former Chair (and current Treasury Secretary Janet Yellen) follow a more seat-of-the-pants approach.

You must be logged in to post a comment.