The US midterm elections are Tuesday. I was denied an absentee ballot for some reason, but I will get my disabled body over to the local precinct to cast my ballot.

Fortunately for Democrats, the next inflation report is not due out until November 10th. Because the forecast for the next inflation report is ugly.

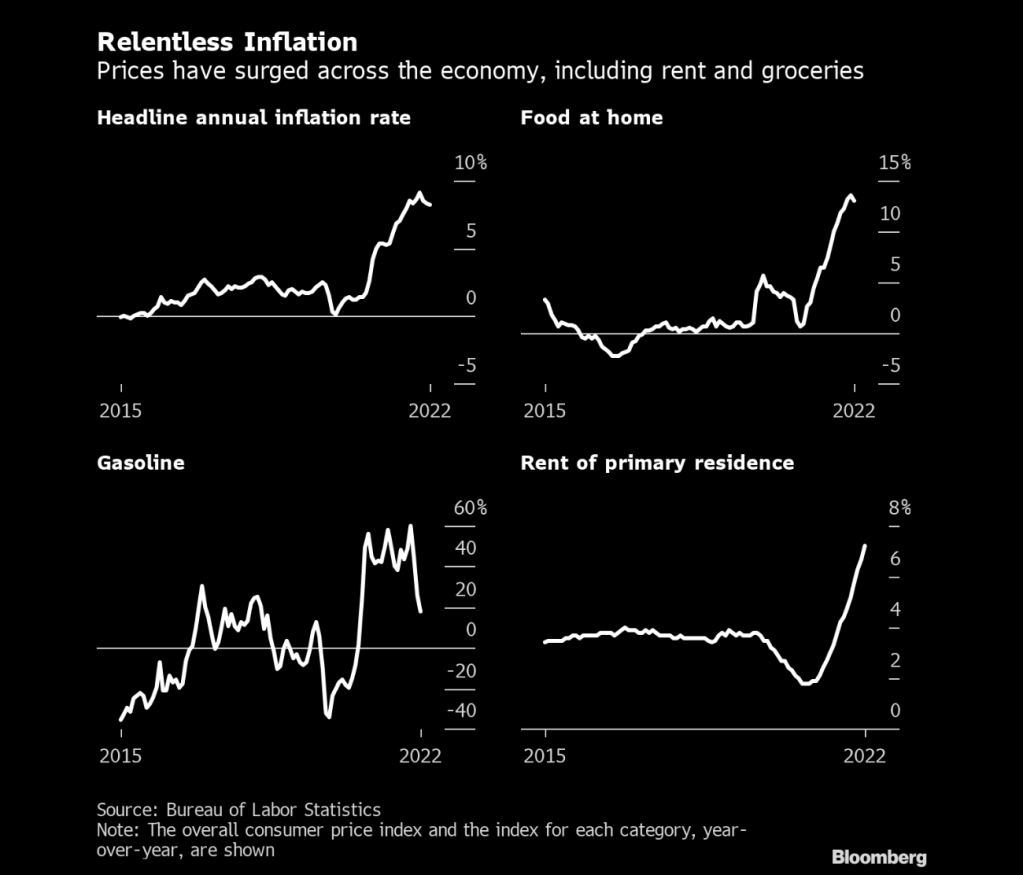

Headline CPI YoY = 7.9%

Core CPI YoY = 6.5%

These numbers are slightly lower than the last inflation report, but Americans are still suffering mightily under Biden’s Reign of Error.

Diesel fuel prices, the lifeline of the food industry, is up 102% under Biden’s mandates with the inventory of diesel fuel down 36%.

Inflation is relentless like Jason from Halloween.

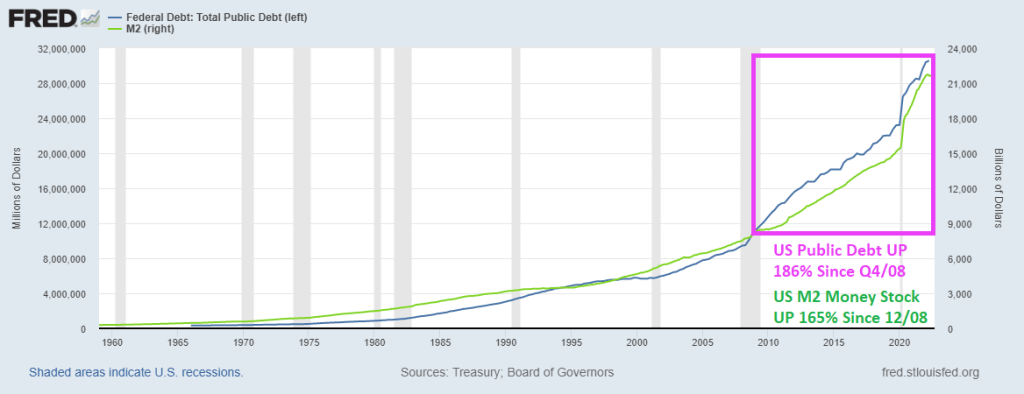

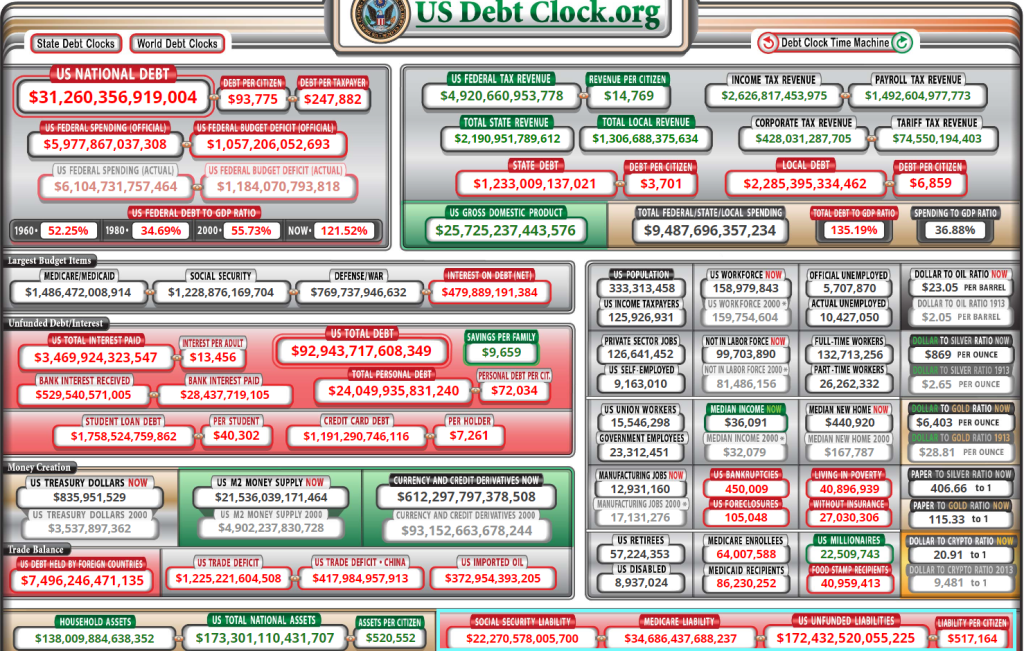

Ever since the financial crisis of 2008 and the election of President Obama and a Democrat Congressional sweep, the US has embraced Modern Monetary Theory (MMT or borrow, print and spend without consequence). And between the financial crisis and the Covid crisis of 2008, we have seen an increase in US public debt from $10.7 trillion in Q4 2008 to a staggering $30.6 trillion as of Q2 2022. That is a staggering increase of 186% in only 14 years.

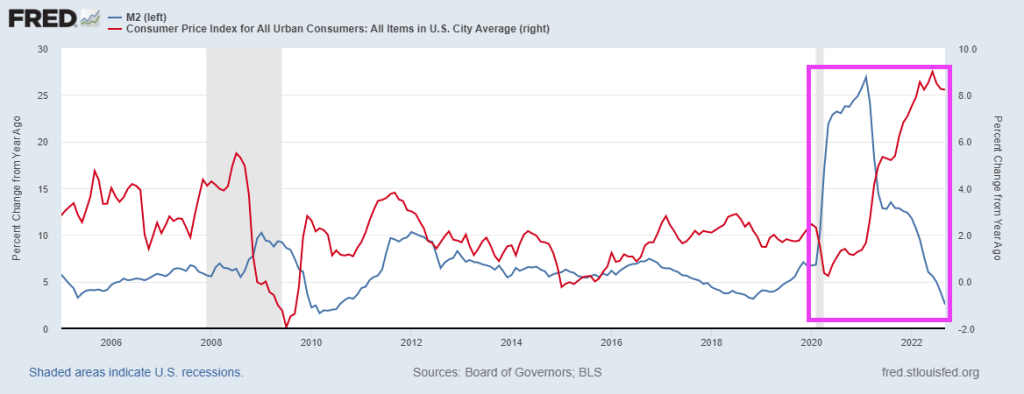

How about US Money stock? M2 Money stock has grown by 162.5% since the beginning of 2009 and the “Blue Wave” of 2008. And nothing has been the same.

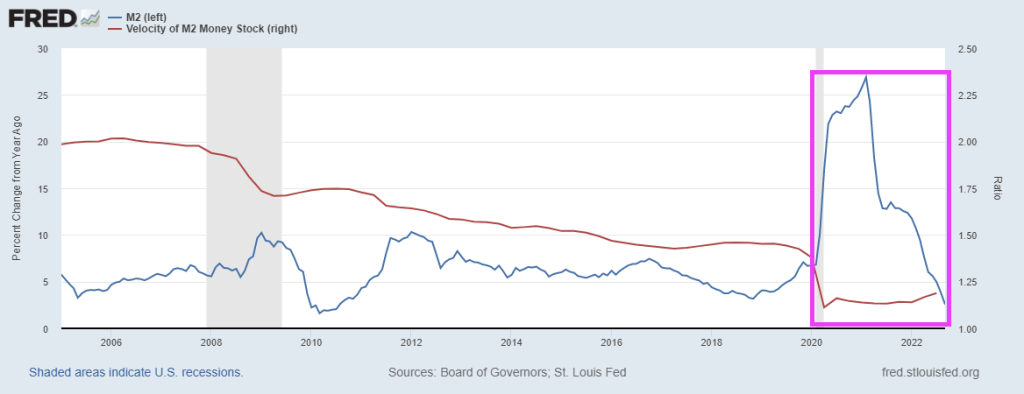

The Covid outbreak in early 2020, we saw Fed money printing that has never seen before … or since. But one thing is for sure, M2 Money Velocity (GDP/M2) is near all-time lows.

Then we have headline US inflation as a function of M2 Money growth YoY.

And it is the midterm election “silly season” where no politician will discuss the complete and utter mess they have made. According to US Debt Clock, US national debt is already up to $31.26 trillion (OMG!), but the REALLY scary number that not a single politician will address is UNFUNDED LIABILITIES OF $172.4 TRILLION.

Can we go back to the gold standard? Or silver standard? Or ANY standard for that matter??

Instead, we have porous borders and patently UNSOUND money, thanks to MMT.

In addition to rampant 40-year highs in inflation, we have the Clark Griswold of the economy, Fed Chair Jerome Powell, slamming his foot on the economic breaks to combat inflation created by Biden’s energy mandates and reckless Federal spending (like the aforementioned, laughable “Inflation Reduction Act.”

So, Biden helps creates massive inflation and Powell and the Gang counterattacked by raising their target rate with more to come (at least until May 2023). And with the implied Fed Funds rate soaring (red line), we are seeing the FANG stocks (Facebook or Meta, Amazon, Netflix and Google) falling more rapidly (white line) than the S&P 500 index. Which is also falling like a rock (yellow line). All this is happening as M2 Money YoY crashes and burns.

How about growth versus value under Cousin Eddie and Clark Griswold? The Vanguard Growth ETF and Vanguard Real Estate ETF are plunging with Fed tightening (red line). Vanguard’s Value ETV (yellow line) is down too, but not by as much.

Yes, Washington DC elites. The gift that keeps on giving … bad things.

Thanks to my former GMU student Andrew Edwards for the Cousin Eddie suggestion!

Private payrolls added 233k jobs in October, which is a -27% decline from September’s revised private payroll figures.

The good news? Average hourly earnings growth is still positive, but fell to 3.7% YoY. But with inflation raging at 8.2% YoY, workers are getting clobbered by inflation.

Here is the rest of the story.

The Fed is now green-lighted to raise rates even higher.

Biden’s campaign promise was to unite rather than divide. But Biden has morphed into Gustaf Holst’s, Mars – Bringer of War! Both domestically and in the Ukraine.

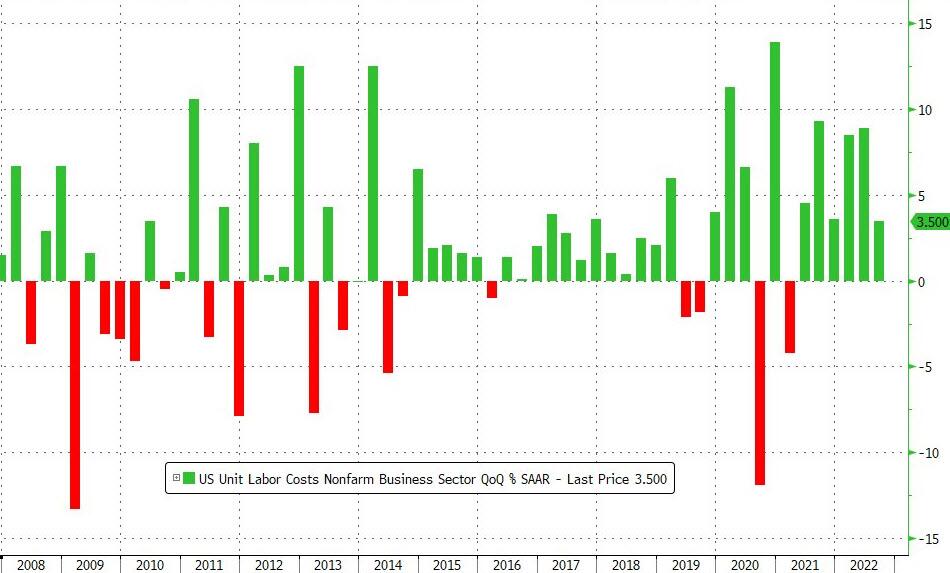

On a YoY basis, US Productivity is down for the 3rd straight quarter (and 4th quarter of the last 5).

On the mirror image of productivity, unit labor costs rose 3.5% QoQ (a notable slowing from the 8.9% QoQ growth in Q2). This was the 6th quarter in a row of rising unit labor costs (but was less than the +4.0% QoQ expected)…

However, on a YoY basis, that is the fastest growth since Q3 1982.

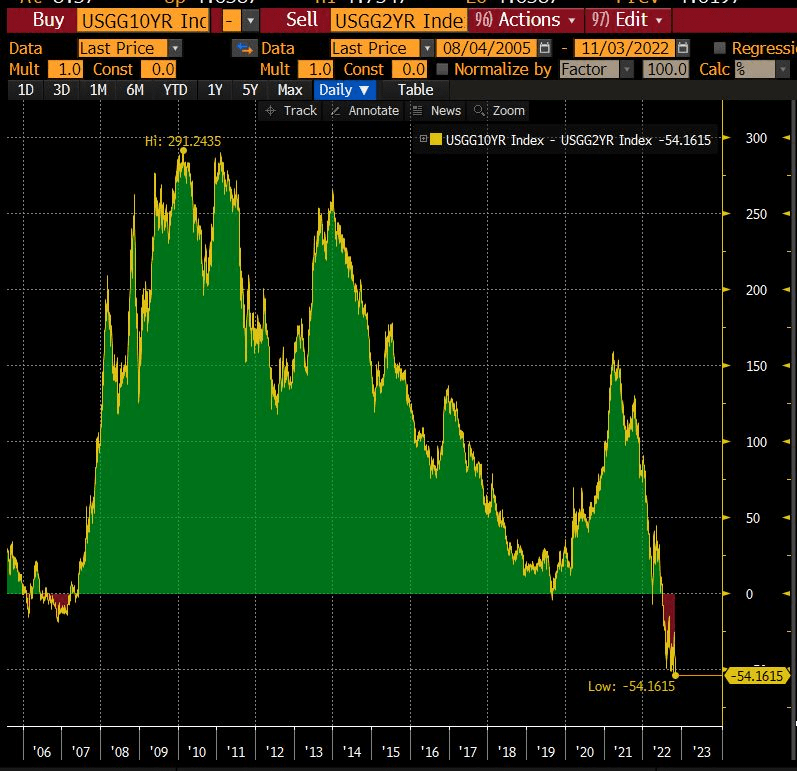

Yikes! The 2s10s Yield Curve Inversion Is the worst since the 1980s.

The S&P 500 index tanked -2.35% after Powell and The Fed failed to pivot.

Federal Reserve Chair Jerome Powell opened a new phase in his campaign to regain control of inflation, saying US interest rates will go higher than previously projected, but the path may soon involve smaller hikes.

Addressing reporters Wednesday after the Fed raised rates by 75 basis points for the fourth time in a row, Powell said “incoming data since our last meeting suggests that ultimate level of interest rates will be higher than previously expected.”

Powell said is it would be appropriate to slow the pace of increases “as soon as the next meeting or the one after that. No decision has been made,” he said, while stressing that “we still have some ways” before rates were tight enough.

“It is very premature to be thinking about pausing,” he said.

Fed Funds Futures data point now to a June peak in the target rate of 5.055%, then a decline.

The next Federal Reserve Open Market Committee (FOMC) meeting in on Wednesday, November 2nd. Let’s see what The Fed does with its BIG GREEN BAG … OF MONEY.

As I set here on Sunday morning waiting to see how the Cleveland Browns will lose to cross-state rival Cincinnati Bengals, I see that both the US Treasury 10yr-2yr and 10yr-3mo yield curves are inverted (below zero).

Core inflation (CPI less food and energy) YoY (blue line) was only 1.3% in February 2021 shortly after Biden was sworn-in as President and is now 6.6% in September 2022. That is over a 400% increase in core inflation!

We have this tantalizing headline on Bloomberg:

Goldman Sachs Now Sees Fed Rates Peaking at 5% in March By Simon Kennedy(Bloomberg) —

Goldman Sachs Group Inc. economists said they now expect the US Federal Reserve to raise interest rates to 5%, higher than previously predicted.

The central bank will lift its benchmark rate to a range of 4.75% to 5% in March, 25 basis points more than earlier expected, economists led by Jan Hatzius wrote in an Oct. 29 research report.

The route to the new peak includes increases of 75 basis points this week, 50 basis points in December and 25 basis points in February and March, they said.

The economists cited three reasons for expecting the Fed to hike beyond February: “uncomfortably high” inflation, the need to cool the economy as fiscal tightening ends and price-adjusted incomes climb, and to avoid a premature easing of financial conditions.

Well, not exactly earth-shattering. Fed Funds Futures data point to a peak of near 5% (4.905%) for the May 2023 FOMC meeting, so Goldman Sachs is calling for an earliest peak at the March 2023 FOMC meeting,

Regardless of what Goldman Sachs thinks, Fed officials are expecting a peak in 2023 followed by a decline to 2.5%.

Brainard and Bostic are the only “doves.” Which is silly because Chicago’s Evans is a perma-dove. Let’s see how the Dots Plot changes at the November 2nd meeting.

America’s distressed debt pile is biggest since September 2020.

{kind=link}

{kind=link}

You must be logged in to post a comment.