Albert Collins said it best about the US economy under Joe Biden: “Lights Are On But Nobody’s Home”.

The Federal Reserve forecast for the US economy is a dismal 0.50% YoY. Do I detect a trend?

The FOMC forecast for 2023 and 2024. Core PCE YoY (inflation) is forecast to drop to 3.50%, still considerably higher than The Fed’s target rate of inflation of 2%. And unemployment is forecast to be 4.60%.

To cope with Bidenflation, US personal savings rate as of October is -67.9% YoY. The “good” news is that rents YoY are crashing. But food prices under Inflation Joe remain very high. But most everything is slowing down, not due to Biden’s policies, but a global and US economic slowdown.

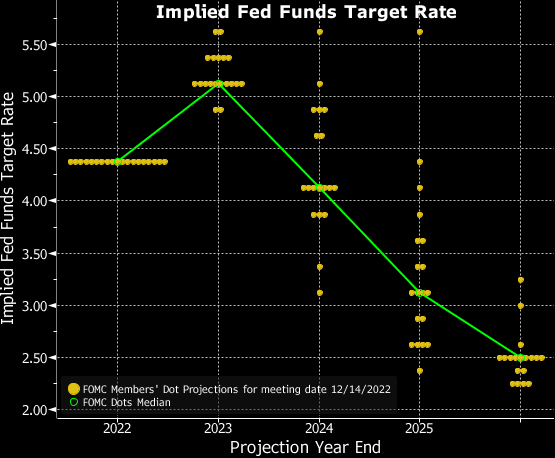

With a big slowdown coming our way, you can understand why The Fed’s December Dot Plot is showing declining Fed Funds Target rate starts declining in 2024.

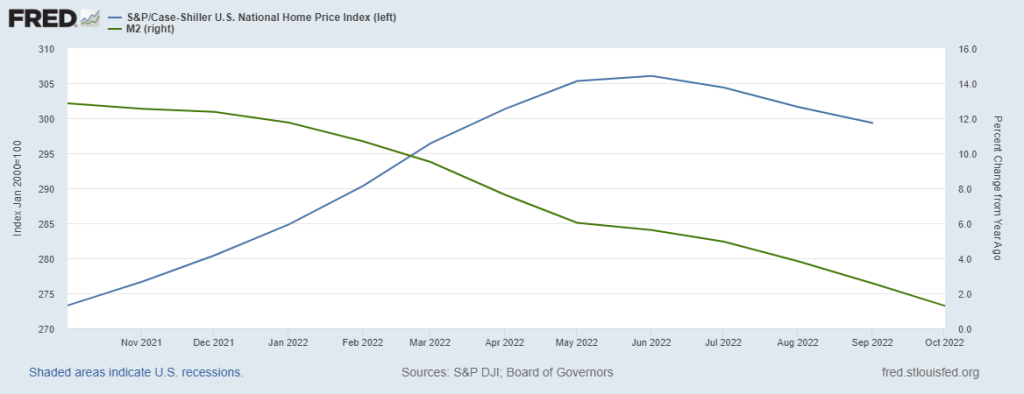

Even US mortgage rates are headed down.

Speaking of going down, cryptos are down across the board with Cardano leading the decline at -6.91%.

All aboard the SS Biden!

You must be logged in to post a comment.