US 30-year mortgage rates are above 7% as The Federal Reserve slowly withdraws its Covid-related monetary stimulus and attempt to combat near 40-year highs in inflation under Biden (aka, Bidenflation).

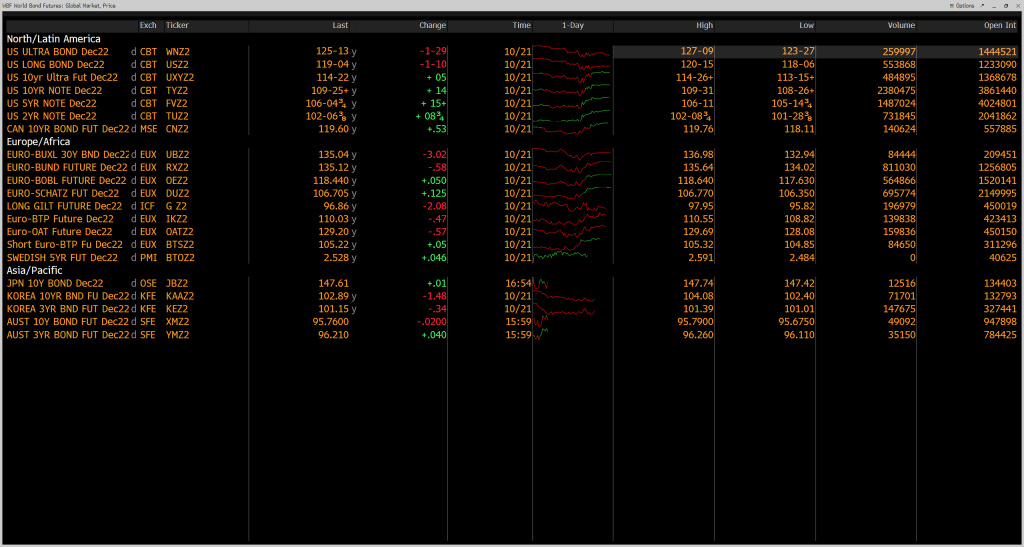

However, the US Treasury 10-year yield is down -12 basis points this morning.

And we have an important predictor of recession, the Treasury 10yr-3mo yield curve.

And if the Republicans win The House (and maybe the Senate) at the midterms, Biden can blame Republicans for the recession.

The next Federal Reserve Open Market Committee (FOMC) meeting in on Wednesday, November 2nd. Let’s see what The Fed does with its BIG GREEN BAG … OF MONEY.

As I set here on Sunday morning waiting to see how the Cleveland Browns will lose to cross-state rival Cincinnati Bengals, I see that both the US Treasury 10yr-2yr and 10yr-3mo yield curves are inverted (below zero).

Core inflation (CPI less food and energy) YoY (blue line) was only 1.3% in February 2021 shortly after Biden was sworn-in as President and is now 6.6% in September 2022. That is over a 400% increase in core inflation!

We have this tantalizing headline on Bloomberg:

Goldman Sachs Now Sees Fed Rates Peaking at 5% in March By Simon Kennedy(Bloomberg) —

Goldman Sachs Group Inc. economists said they now expect the US Federal Reserve to raise interest rates to 5%, higher than previously predicted.

The central bank will lift its benchmark rate to a range of 4.75% to 5% in March, 25 basis points more than earlier expected, economists led by Jan Hatzius wrote in an Oct. 29 research report.

The route to the new peak includes increases of 75 basis points this week, 50 basis points in December and 25 basis points in February and March, they said.

The economists cited three reasons for expecting the Fed to hike beyond February: “uncomfortably high” inflation, the need to cool the economy as fiscal tightening ends and price-adjusted incomes climb, and to avoid a premature easing of financial conditions.

Well, not exactly earth-shattering. Fed Funds Futures data point to a peak of near 5% (4.905%) for the May 2023 FOMC meeting, so Goldman Sachs is calling for an earliest peak at the March 2023 FOMC meeting,

Regardless of what Goldman Sachs thinks, Fed officials are expecting a peak in 2023 followed by a decline to 2.5%.

Brainard and Bostic are the only “doves.” Which is silly because Chicago’s Evans is a perma-dove. Let’s see how the Dots Plot changes at the November 2nd meeting.

America’s distressed debt pile is biggest since September 2020.

One reason is diesel fuel prices are up 102% under Biden’s Reign of Error. While inventory of diesel fuel down -37%. Meanwhile core inflation is up from a measly 1.3% to a whopping 6.6% at the latest inflation report.

Introducing Biden’s Thanksgiving dinner … in a can to cope with rising prices.

Just kidding. This is too clever for the clueless Biden Administration. But Karine Jean-Pierre might get as confused as Joe Biden and repeat it as one of the ways that The Biden Administration is helping consumers.

As I told my Chicago, Ohio State and George Mason University finance and real estate students, repeatedly, “Watch out when The Fed begins to tighten monetary policy. It will be a bloodbath for taxpayers.”

Well, here we are. I argue that Biden’ green energy knucklehead policies are driving inflation, or it could be the insane level of Federal spending that Obama economist Larry Summers warned us about, or rising wages (in part due to Federal spending) is to thank for inflation. Or all of the above.

Regardless of the cause, the bond market is enduring its worst selloff in a generation, triggered by high inflation and the aggressive interest-rate hikes that central banks are implementing. Falling bond prices, in turn, mean paper losses on the massive holdings that the Fed and others accumulated during their rescue efforts in recent years.

Rate hikes also involve central banks paying out more interest on the reserves that commercial banks park with them. That’s tipped the Fed into operating losses, creating a hole that may ultimately require the Treasury Department to fill via debt sales. The UK Treasury is already preparing to make up a loss at the Bank of England.

The Reserve balance has crashed into negative territory.

And Fed losses are skyrocketing.

Agency MBS prices are up today, but are down since August 2022. But risk measures duration and convexity are zooming upwards.

Things are getting interesting in DC, to say the least. The US is 100% likely to face a recession in the next 12 months while The Federal Reserve is on its crusade to fight inflation caused by … The Federal Reserve, Biden’s green energy shenanigans and massive, irresponsible Federal spending that even Former Obama economist Lawrence Summers warned would cause inflation. So what will The Fed do? Lower rates and expand their assets purchases to fight the impending recession OR keep tightening to fight Bidenflation? But where we are now is that the fixed-income market could be in big, big trouble.

For months, traders, academics, and other analysts have fretted that the $23.7 trillion Treasuries market might be the source of the next financial crisis. Then last week, U.S. Treasury Secretary Janet Yellen acknowledged concerns about a potential breakdown in the trading of government debt and expressed worry about “a loss of adequate liquidity in the market.” Now, strategists at BofA Securities have identified a list of reasons why U.S. government bonds are exposed to the risk of “large scale forced selling or an external surprise” at a time when the bond market is in need of a reliable group of big buyers.

“We believe the UST market is fragile and potentially one shock away from functioning challenges” arising from either “large scale forced selling or an external surprise,” said BofA strategists Mark Cabana, Ralph Axel and Adarsh Sinha. “A UST breakdown is not our base case, but it is a building tail risk.”

In a note released Thursday, they said “we are unsure where this forced selling might come from,” though they have some ideas. The analysts said they see risks that could arise from mutual-fund outflows, the unwinding of positions held by hedge funds, and the deleveraging of risk-parity strategies that were put in place to help investors diversify risk across assets.

In addition, the events which could surprise bond investors include acute year-end funding stresses; a Democratic sweep of the midterm elections, which is not currently a consensus expectation; and even a shift in the Bank of Japan’s yield curve control policy, according to the BofA strategists.

The BOJ’s yield curve control policy, aimed at keeping the 10-year yield on the country’s government bonds at around zero, is being pushed to a breaking point.

Well. Bidenflation certainly isn’t helping, but Statist Economist and Cheerleader Janet Yellen can’t bring herself to blame green energy policies, rampant Federal spending or irresponsible Federal Reserve policies for the crisis.

You will note the differences between today and the financial crisis of 2008-2009. The financial crisis gave us a massive surge in government securities liquidity thanks to then Fed Chair Ben Bernanke imitating Japan’s Central Bank and buying US government securities. Fast forward to today and the liquidity index hasn’t budged much since 2010 (except for a little blip around the Covid Fed intervention of early 2020), but we are now seeing near 40-year highs in inflation and a barely declining Fed balance sheet. And M2 Money YoY (mostly commercial bank deposits) are crashing.

I am guessing that The Fed will pivot given that stock futures are way up for Monday. The Dow Jones mini is up 770 points and the S&P 500 mini is up 88.75 points.

Bond market futures (specifically the US Ultra Bond) is down for Monday, meaning yields will be climbing.

I remember giving a speech at The Brookings Institute in Washington DC. Talk about stranger in a strange land. One person who I was debating got frustrated and said “You are such a … Republican!!!” As if that was the worst slur he could throw at me.

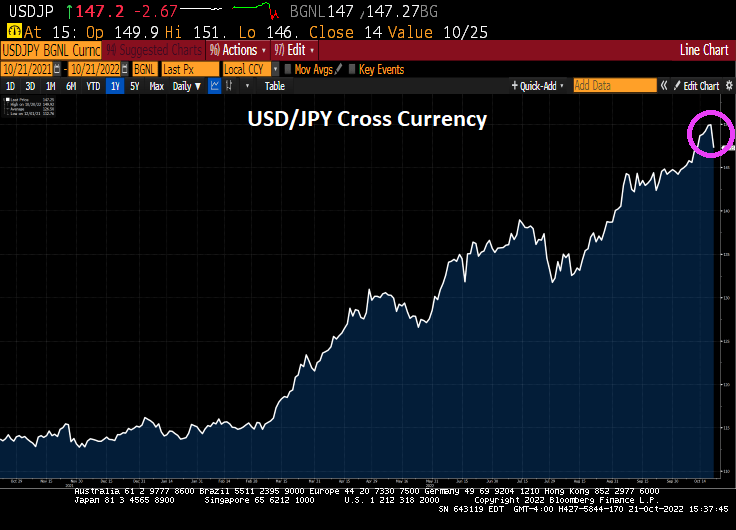

Wall Street saw another day of stunning reversals, with stocks rallying after a Treasury selloff sputtered. The yen jumped as Japan intervened again to prop up the currency.

After many twists and turns, the S&P 500 pushed solidly into the green and headed for its best week since June as 10-year yields fell from the highest since 2007.

Probably because The Fed is likely to pivot with impending recession. The Dow is up 774 points this Friday. And today was a huge option expiration day!!

And the 10-year Treasury yield fell -2.2 basis points.

Here is the result of Japan’s intervention.

But today’s numbers were largely monthly stock index option expiration.

Why did it fall upon Powell to be the wielder of the Fed tightening scimitar? Why didn’t Yellen? Because “Good Girls Don’t.” But Powell did.

Have a nice weekend. I will be rooting for Ohio State to annihilate the Iowa Hawkeyes at noon on Saturday.

Bloomberg’s recession probability over next 12 months is … 100%.

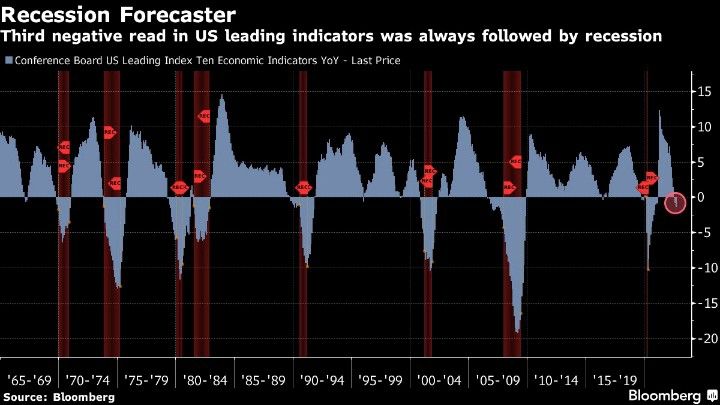

And how about the Conference Board’s Leading index of 10 economic indicators YoY? Third negative read ALWAYS followed by recession.

The Federal Reserve may be forced to pivot. This may be one reason why the Dow is up 565 points today (+1.86%) as recession and pain become ever more likely.

Look at commercial banks deposits. Wonder why liquidity is drying up?

Over the past year, the dollar has been on a tear: The U.S. Dollar Index, which measures the dollar’s strength against a basket of foreign currencies, is up 18%. And up 25.2% under 80-year old US President Joe Biden (well, he will be 80 in November).

For tourists, a strong dollar is great news. It means you get more for your money abroad.

But for investors, a beefed-up buck is decidedly bad news.

When the dollar strengthens, that means foreign revenues are going to translate into fewer dollars. Those earnings are going to come in lower and any overseas investment you own is going to hurt you in a rising dollar environment.

Diesel, the lifeline of the shipping industry, is UP 100% under Biden (that is, diesel prices have doubled) while the inventory of diesel fuel has declined by -37.5% under Biden.

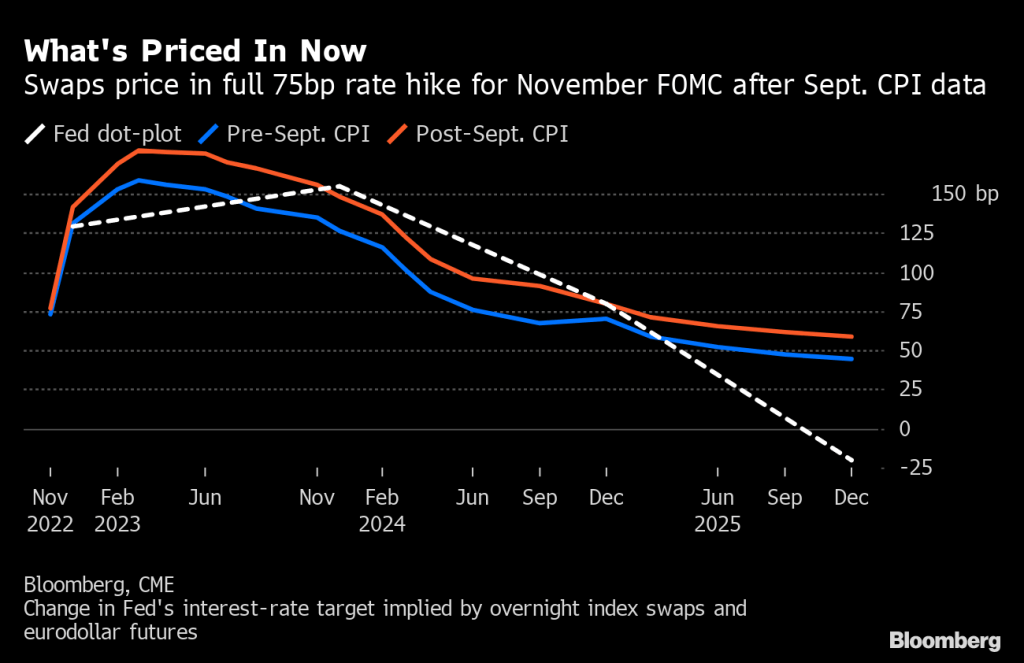

* Fed Swaps Lean Toward Back-to-Back Three-Quarter-Point Hikes * Hotter-than-expected September inflation data spark shift

(Bloomberg) — The market for wagers on the Federal Reserve’s policy rate is leaning toward pricing back-to-back 75 basis point rate hikes in the next two central bank meetings after consumer prices rose more than forecast in September.

The rate on the November overnight index swap contract rose to 3.86%, more than 75 basis points above the current effective fed funds rate, while the one referring to December climbed to 4.50%. A total of 142 basis points of rate hikes are now priced in for the next two policy meetings, just short of consecutive three-quarter-point hikes.

Prior to the inflation data, OIS markets were leaning toward the central bank cooling the pace of tightening to a 50 basis point move in December. At Wednesday’s close, swaps priced in around 130 basis points of hikes over the remaining of the year, which is equivalent to 55 basis points for December.

The market also priced in a higher eventual peak for the policy rate, with the March 2023 contract touching 4.864%.

The CPI data was “clearly a shock for the markets and the markets are off because of it,” Seth Carpenter, chief global economist at Morgan Stanley said on Bloomberg television. “There is persistence, particularly in the services side of inflation.”

Excluding food and energy, the Consumer Price Index increased 6.6% from a year ago, the highest level since 1982, Labor Department data showed Thursday. From a month earlier, the core CPI climbed 0.6% for a second straight month.

The Fed has raised its policy rate five times since March, most recently to a range of 3%-3.25% in September, after dropping the lower bound to 0% two years earlier at the onset of the pandemic.

The Fed Funds Futures data is pointing further Fed rate hikes with a turnaround in March 2023.

And with that awful inflation report and the likely Fed counterattack, the two year US Treasury yield has risen to 4.4361%, the highest since The Great Recession and banking crisis.

Fed Fireball! Comin’ at ya!!

Biden and Powell should appear on Saturday Night Live as the joint Debbie Downer. Or Democrat Downer.

You must be logged in to post a comment.