More bad news about the economy and housing sector under Biden/Yellen/Powell’s Reign of Economic Error.

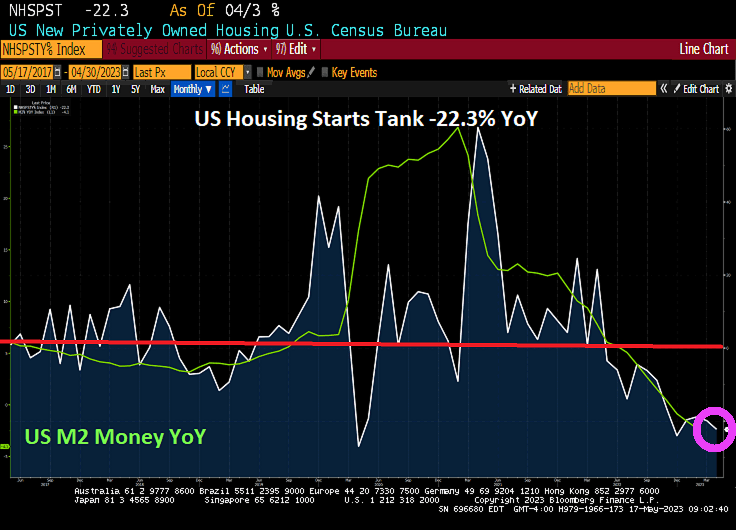

US housing starts are out for April 2023. The bad news? Housing starts tanked -22.3% year-over-year (YoY).

The good news? US housing starts were up 2.19% from March to April. 1-unit detached starts were up 1.56% MoM while 5+ unit starts up 5.24% MoM. Permits for multifamily were down -9.71% from March to April.

The media will no doubt try to ignore the horrifying Durham Report. The report showed that Hillary Clinton and the Obama administration knowingly smeared Presidential candidate Donald Trump with false Russian misinformation and knowingly tried to steal an election. I wonder if Attorney General Merrick Garland will open an investigation into Hillary Clinton’s involvement in election tampering? Oh wait, the IRS was told to stop investigating Hunter Biden’s nefarious dealings. Never mind.

I used to think that The Kabuki Theater surrounding the raising of the US debt limit and passing a Federal budget would be over by now. But since Biden is being controlled by the hard left “Progressives” in Washington DC, he may be reckless enough to let the US default just so he can blame Republicans. And with our useless and deeply-biased main street media (MSM) just repeating Democrat talking points blaming Republicans, we may actually see a US debt default.

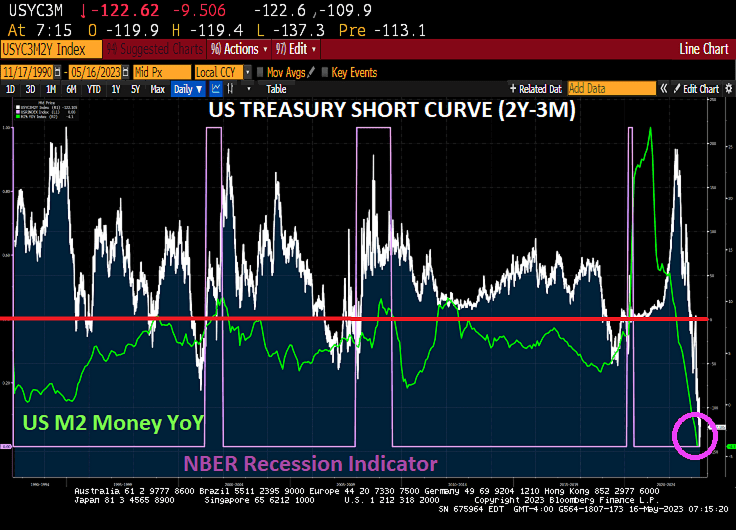

So while Yellen is warning that time is running out, notice she never encourage Blaming Biden to negotiate his insane budget downwards, we see a deeply inverted US Treasury short curve (2Y-3M).

(Bloomberg) Treasury Secretary Janet Yellen warned that “time is running out” to avert an economic catastrophe from failing to raise the debt ceiling, in remarks released as President Joe Biden and congressional leaders prepared to meet on the standoff.

Speaker Kevin McCarthy issued his own notice Monday evening ahead of Tuesday’s 3 p.m. gathering, saying, “We only have so many days left to deal with this.”

The two sides showed little signs of agreeing on much else other than the countdown in the runup to the second White House encounter on the debt ceiling in two weeks. While senior staff have been negotiating for days, Republicans are still pressing for sweeping spending cuts, while Democrats are determined to protect the president’s legislative achievements.

“We are already seeing the impacts of brinksmanship: investors have become more reluctant to hold government debt that matures in early June,” Yellen said in remarks prepared for delivery to a banking conference on Tuesday. “The impasse has already increased the debt burden to American taxpayers.”

The Treasury chief issued a fresh letter to congressional leaders Monday restating that the Treasury risks running out of sufficient cash for all federal obligations as soon as June 1. The livelihoods of millions of Americans “hang in the balance,” she said in excerpts of her speech to the Independent Community Bankers of America Capital Summit released by the Treasury.

There is the evil Hobbit! Sending a letter to Congress essentially blaming McCarthy for the fiasco when Biden could downsize his budget request to reasonable levels. But Yellen is an authoritarian Statist, not a free market type.

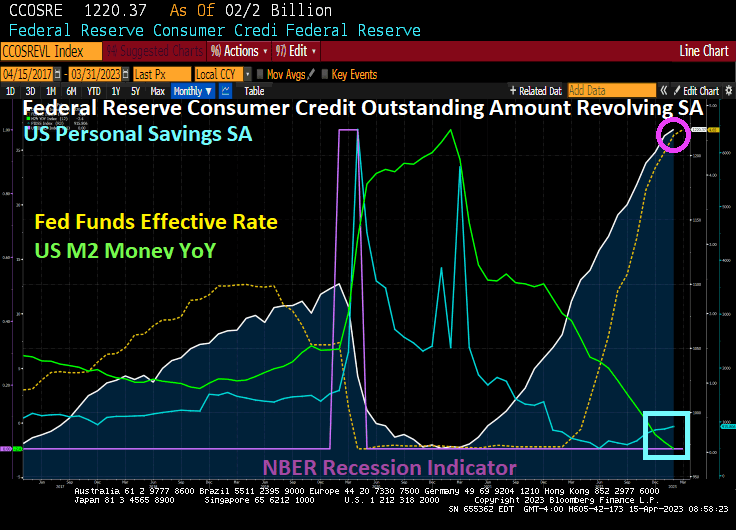

Of course, what is really troubling is that credit card useage is soaring as The Fed hikes interest rates to combat inflation … caused by Janet Yellen and The Fed keeping rates near zero for too long under Obama. Then we have Biden fighting fossil fuels and Congress spending like drunken sailors in port. All together? Consumers turn to credit cards to cope and their personal savings are dwindling.

How to protect yourself against out-of-control Fed money printing? Gold is up over $2,000.

Between inflation under Biden and The Fed’s counterattack to get inflation to 2%, I call this the Biden Blitz.

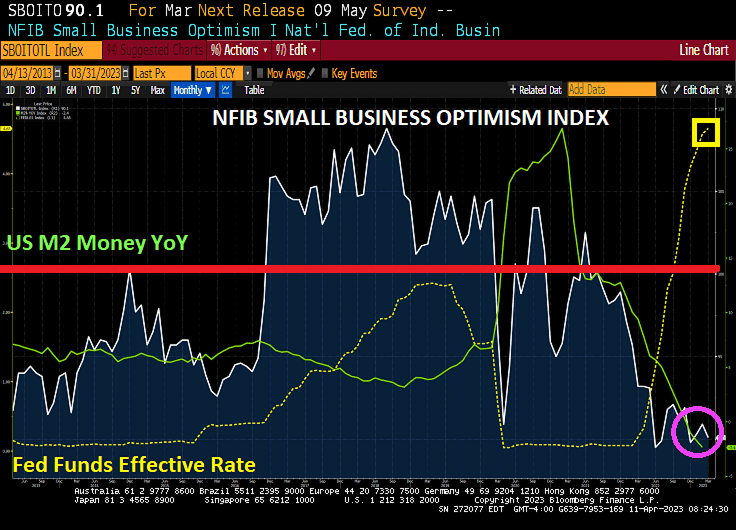

Unlike what the elites in Washington DC think, small business are the cornerstone of the US economy. Unfortunately, small business optimism is getting crushed and just fell in March to a level lower than that found during the Covid economic shutdowns of 2020. HOW is it possible for small businesses to be even less optimistic than it was in April 2002, the nadir of the Covid economic shutdown?

Small business optimism soared in November 2016 after the election of Donald Trump and remained high (above 100) until Covid struck in March 2020. Small business optimism rose above 100 again with the massive money printing by The Fed (green line) and Federal spending spree. But as M2 Money growth slowed, small business optimism hasn’t been above 100 since August 2021. It has been all downhill since then as The Fed started to raise The Fed Funds Target Rate quite rapidly.

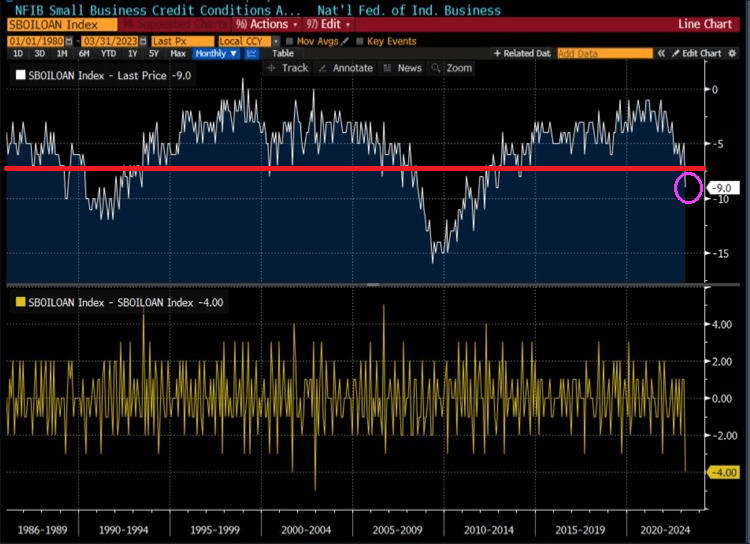

NFIB small business credit conditions are negative at -9.0 and sinking like The Titanic.

Biden is the face of big business (big banks, big pharma, big tech, big defense, big labor unions, big media, etc.). Biden just told Al Roker that he is indeed running for reelection, supported by …. big banks, big pharma, big tech, big defense, big labor unions, big media, etc.

Biden is no longer a President, but an old-time preacher screaming about MAGA Republicans as if they were demons. This is called Blitzkrieg Biden.

To show you how Yellen/Powell’s Too Low For Too Long (TLFTL) monetary polices coupled with Biden/Pelosi/Schumer’s (add McConnell to this foul-smelling witches’ brew), Powell and The Gang (aka, The Fed) slammed on the monetary brakes. On a year-over-year basis, M2 Money growth has crashed tl -3.13%. The shocking number is The Fed Fund Effective Rate which rose over 5,000% YoY.

Actually, the US has been on a money printing spree since 1995, but it was Covid spending and monetary expansion in 2020 that crushed M2 Money Velocity (GDP/M2).

Here is Supernatural’s Leviathan monster Dick Roman handing an award to sparkless President Joe Biden. But Biden did spark massive inflation that crushed the US middle class and low wage workers.

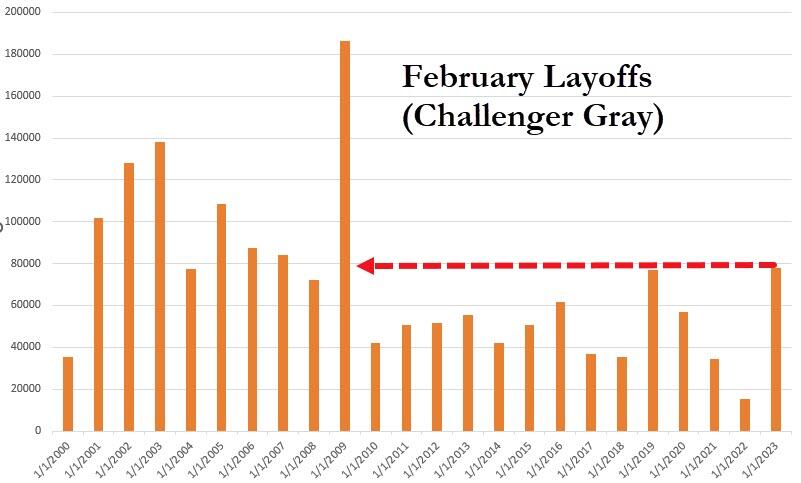

I am waiting for tomorrow’s employment report to see if the Biden Administration plays it straight or give another padded report like first half 2022. But in the meantime, according to Challenger Gray & Christmas, U.S.-based employers announced 77,770 job cuts in February. It is 410% higher than the 15,245 cuts announced in the same month last year.

February’s total is the highest for the month since 2009…

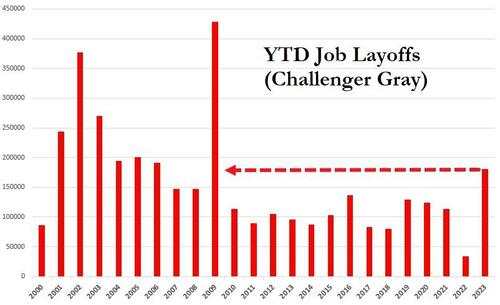

So far this year, employers announced plans to cut 180,713 jobs, up 427% from the 34,309 cuts announced in the first two months of 2022.It is the highest January-February total since 2009…

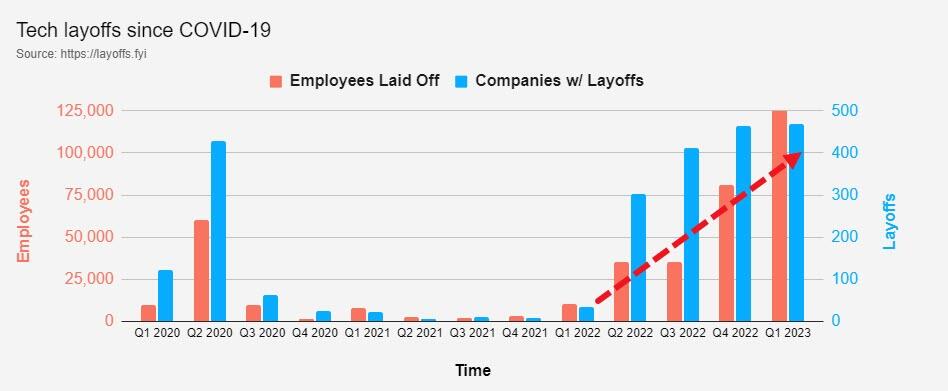

While many of the job cuts is coming in the tech sector,

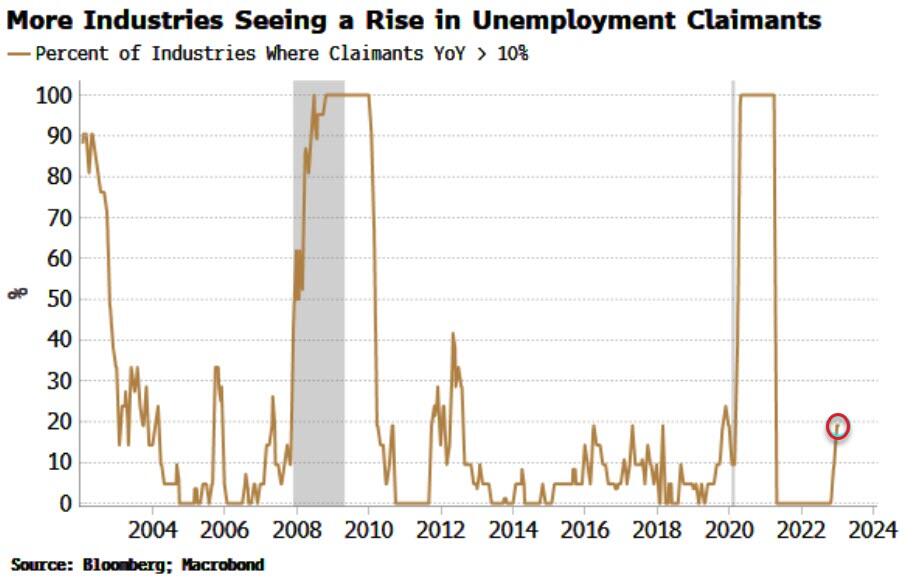

we are seeing more industries reporting a rise in unemployment claims.

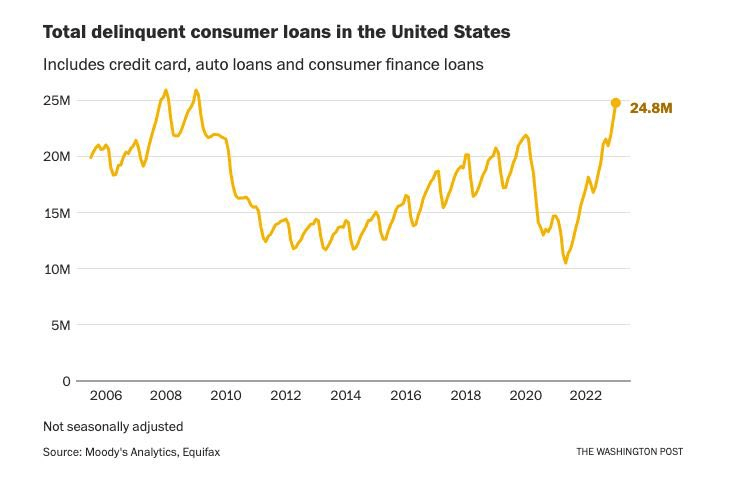

And then we have total delinquent consumer loans at 24.8 million. Highest since 2009.

I wonder if the answer to tomorrow’s employment report lies in one of the nine boxes of Biden’s documents taken from a Boston office?

There was a hilarious film with Hillary Swank and Aaron Ekhart called “The Core” where earth’s core stops spinning and the earth gets cooked by the Sun’s rediation. Now we learn that the Earth’s inne core has actually stop spinning. This time, however, all that has happened is that Joe Biden is President which is almost as bad,

But also related to “The Core” is that the important Personal Consumption Expenditures (PCE) are out for December along with PCE price deflator numbers. In short, personal income was up 0.2% month-over-month (MoM) in December while personal spending was down -0.2%. REAL personal spending was down -0.3% MoM.

But the all important PCE deflators numbers were down all well. The REAL PCE price index (or deflator) was down to 5.0% YoY in Decmember while REAL CORE price index was down to 4.40%. All this is happening as M2 Money growth has stop spinning (down to -1.3% YoY in December).

Based on a CORE PCE YoY of 4.40%, the Taylor Rules suggest that The Fed Fund Target rate should be … 10%. However, the current Fed Funds Target rate is only 4.50%, so The Fed is not even half way there.

Fed Funds Futures are pointing to a peak rate of 4.90% by the June ’23 FOMC meeting, then a pivot (despite denials from Fed talking heads).

Of course, The Fed doesn’t follow the Taylor Rule or any other transparent rule for rate management. Rather, Fed Chair Powell like former Chair (and current Treasury Secretary Janet Yellen) follow a more seat-of-the-pants approach.

Newly-minted US House Speaker Kevin McCarthy faces a daunting task: trying to avoid a US debt default. As I have discussed many times before, nothing has been the same since the US housing bubble and near-collapse of the banking system that produced an expensive bailout of seemingly all financial institutions. After 2008, Federal spending has gone out of control. The budgetary hawks (or pigeons) in the US House of Representatives (with Pelosi, Boehner, Ryan then Pelosi again) went on Federal spending sprees of epic proportions.

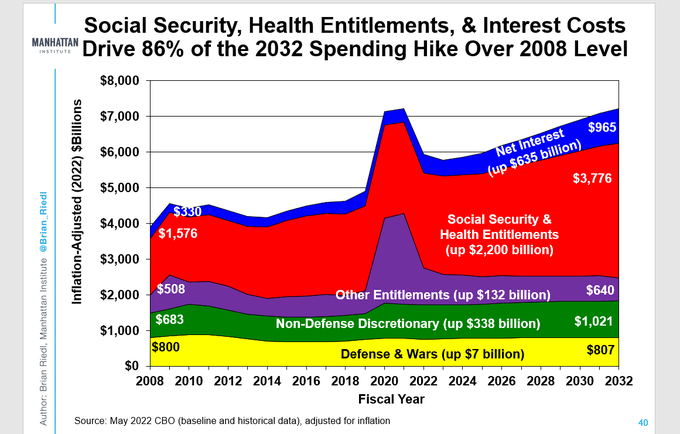

The Manhattan Institute has a nice chart showing the explosion in the Federal budget since 2008. Of particular note, interest payments on the Federal debt has increased by a staggering 192%. On the non-interest spending front, Social Security and Health Entitlements have increased by 140% while Nondefense Discretionary Spending has increased 76%.

The massive increase in Federal debt interest is due to both increased Federal spending and rising interest rates thanks to The Federal Reserve raising rates to fight inflation.

But what will McCarthy and House Republicans recommend cuts in? Tighter restrictions on who qualifies for Social Security and particularly Social Security Disability payments?

The odd factoid is that Defense and Wars budget is up less than 1% from 2008 to 2032. So, Ukraine military aid is coming from somewhere, but not from the Defense budget. Is Ukraine another entitlement program?

Rest assured that after debate, the House will pass a budget and, provided that virtually nothing was cut, the Senate will gleefully agree to more spending and “Top Secret Documents” Biden will sign it.

After he parks his gorgeous Corvette Sting Ray, that is.

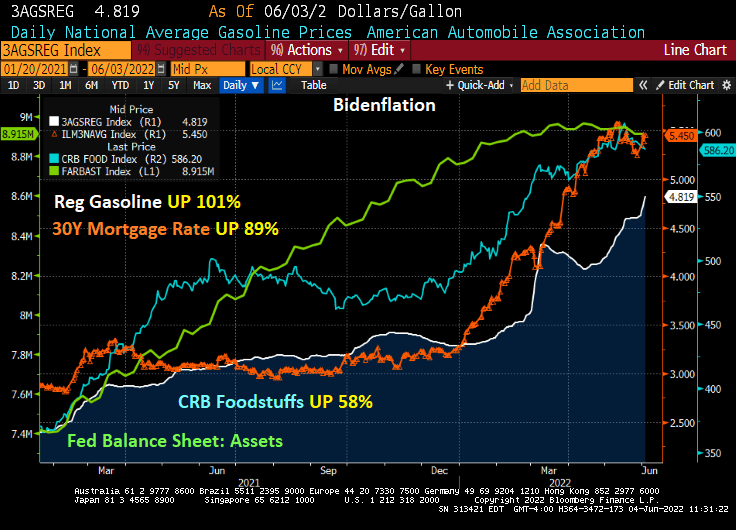

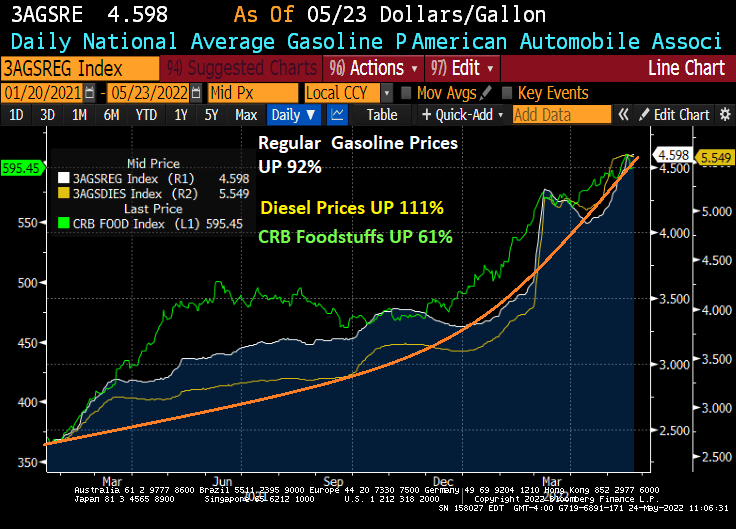

This is not the legacy that will endear President Biden to voters. Regular gasoline prices have risen 101% under Biden.

But it not just gasoline and diesel that are soaring (while the rest of us are sore!), CRB Foodstuffs are up 58% under Biden while the 30-year mortgage rate is up 89% under Biden.

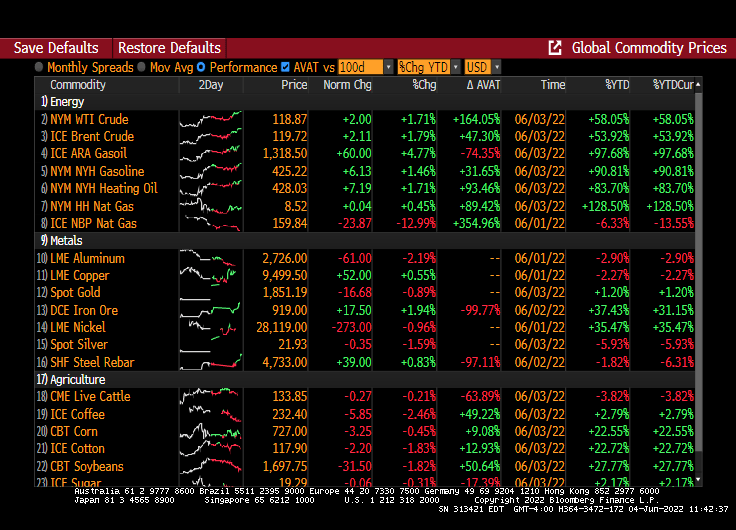

And this morning, WTI crude futures are up +1.71%.

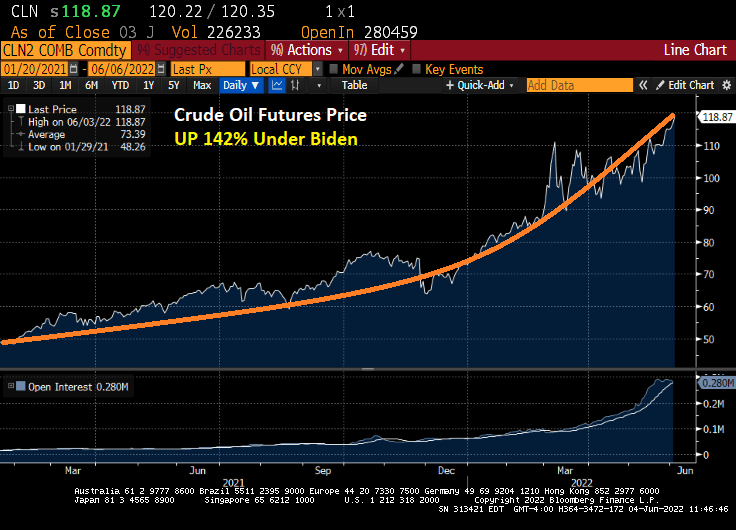

And up 142% under Biden.

Prices are sizzling and clobbering the American middle class and low wage workers. But former Federal Reserve Chair and current US Treasury Secretary Janet Yellen never saw it coming.

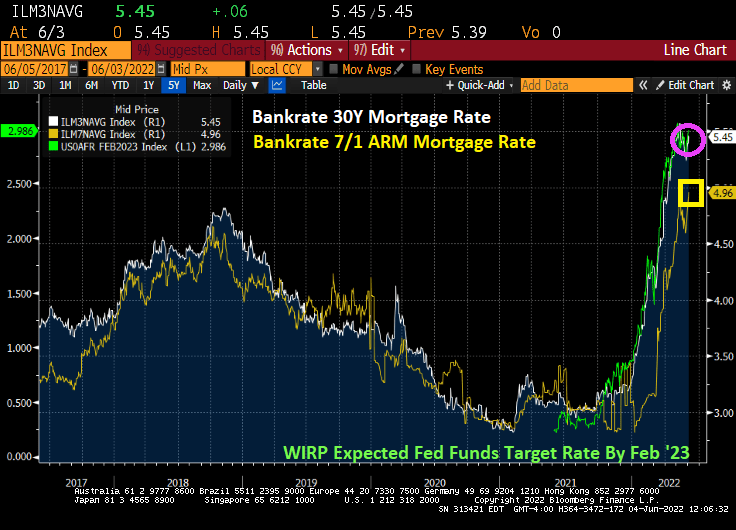

Biden’s just killing us. And Powell is making up for Yellen’s keeping monetary stimulus too high for too long. Price? Mortgage rates are soaring.

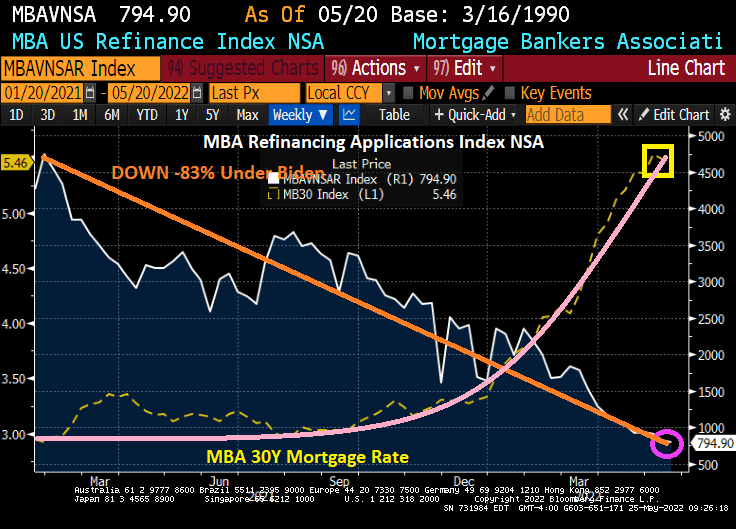

Mortgage applications decreased 1.2 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending May 20, 2022.

The Refinance Index decreased 4 percent from the previous week and was 75 percent lower than the same week one year ago. And under Biden, the refinance index is down -83.2%.

The good news? The seasonally adjusted Purchase Index increased 0.2 percent from one week earlier. The unadjusted Purchase Index decreased 1 percent compared with the previous week and was 16 percent lower than the same week one year ago. And the mortgage purchase applications index is down -12% under Biden.

While mortgage interest rates are up 71.7% than one year ago and mortgage rates are up 87% under Biden. As The Federal Reserve signals (but not yet accomplished) monetary tightening.

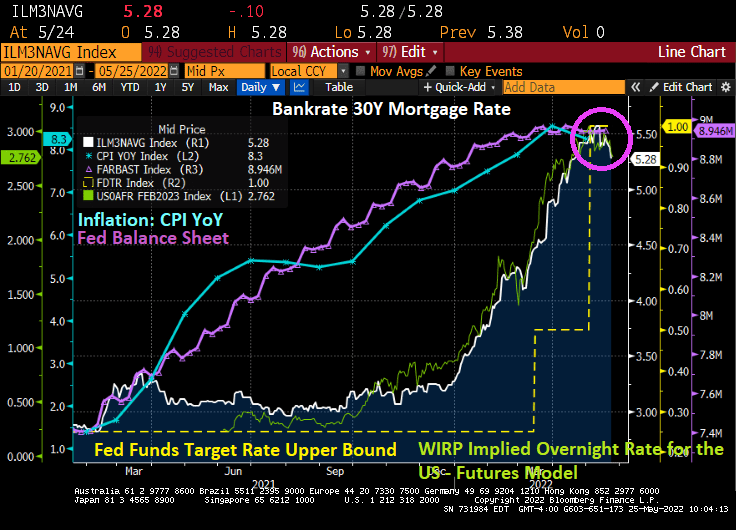

Once again, The Fed is dead set on cooling inflation caused by 1) Biden’s anti-drilling policies and 2) the remnants of the Federal government spending splurge to combat Covid. The Fed has been increasing their asset purchases (purple line) as inflation increase (blue line). Now they are signaling a decline in the balance sheet (green line) in the hope that it will cool inflation. Fat chance.

Let’s see how DEAD SET The Fed is about tightening monetary policy in the face of rising energy and food prices while a war rages in Ukraine and China in a Covid lockdown.

You must be logged in to post a comment.