Nicolas Maduro of Venezuela must be envious of Joe Biden. I don’t think even Maduro has the stones to have his politiical opponent charged with espionage in the run-up to a Presidential election. Particularly when the US President has been bribed by China and Ukraine and has similiar sensitive document hoarding issues (at least Trump didn’t leave boxes of sensitive documents in a garage like Biden did when he keeps his Chevy Corvette).

So where do we sit today after Biden has signed the debt ceiling increase and massive spending splurge?

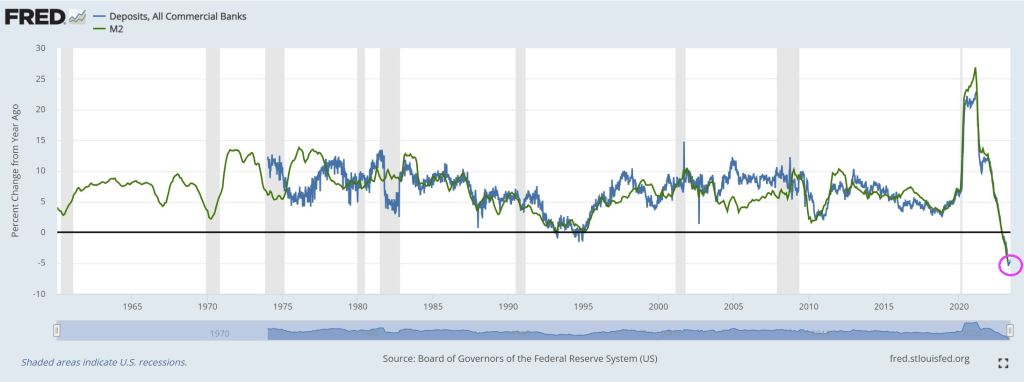

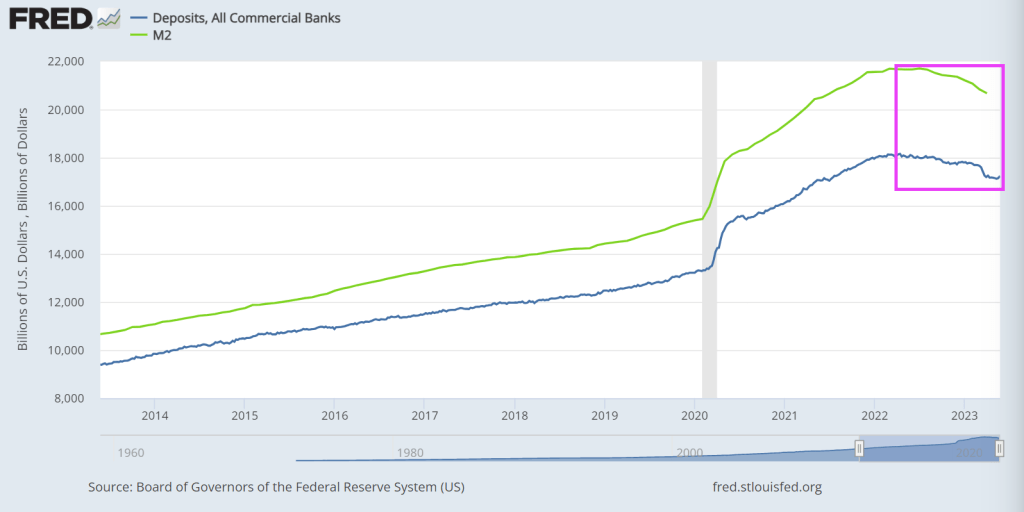

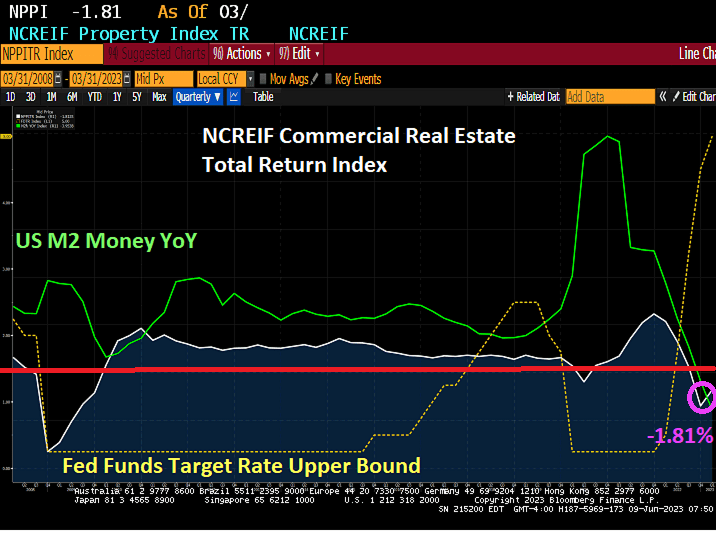

First, look at the crashing bank deposit problem. Well, the solution is for The Fed to fire up the money printing press! Keep on printing!

This not surprising if you have read Nobel Laureate George Stigler’s treastise on regulatory capture. Essentially, big corporations (big media, big tech, big banking, big pharma, big defense, big agriculture, etc.) essentially own Congress, the Biden Administration and Federal regulators. After all, Biden has been bribed with millions of dollars by China and Ukraine and, like a Banana Republic, has is avoiding prosecution and instead prosecuting his political opponent, Trump. Don’t worry, if they get Trump that will indict DeSantis for something.

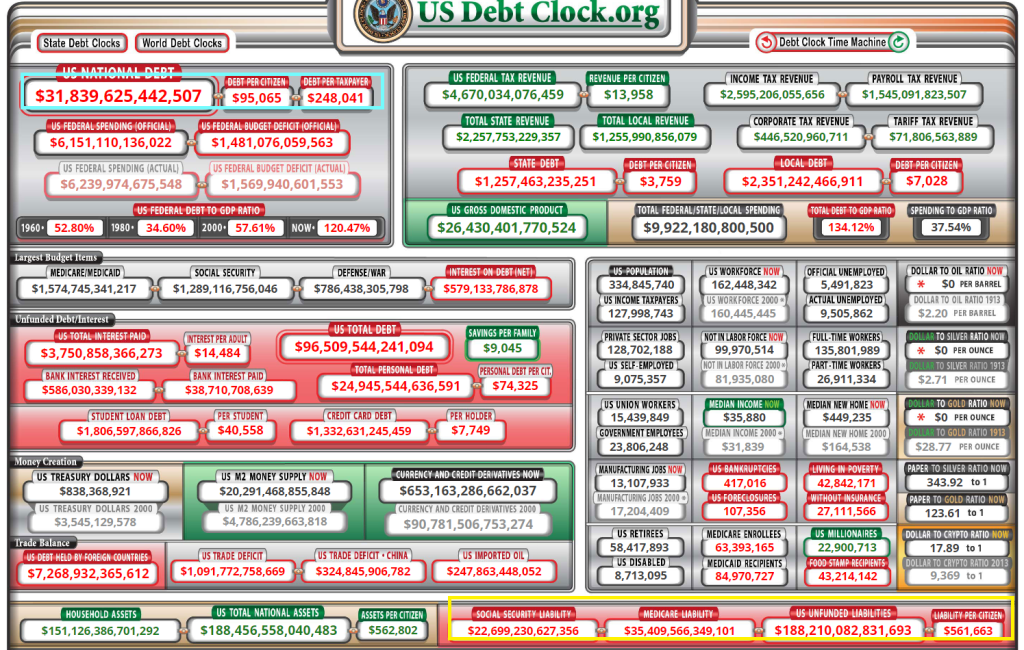

US debt stands at $31.8 TRILLION with $188 TRILLION in unfunded liabilities (which means higher personal taxes and much more debt).

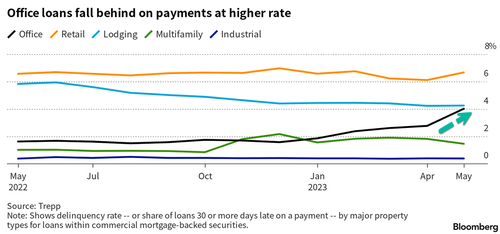

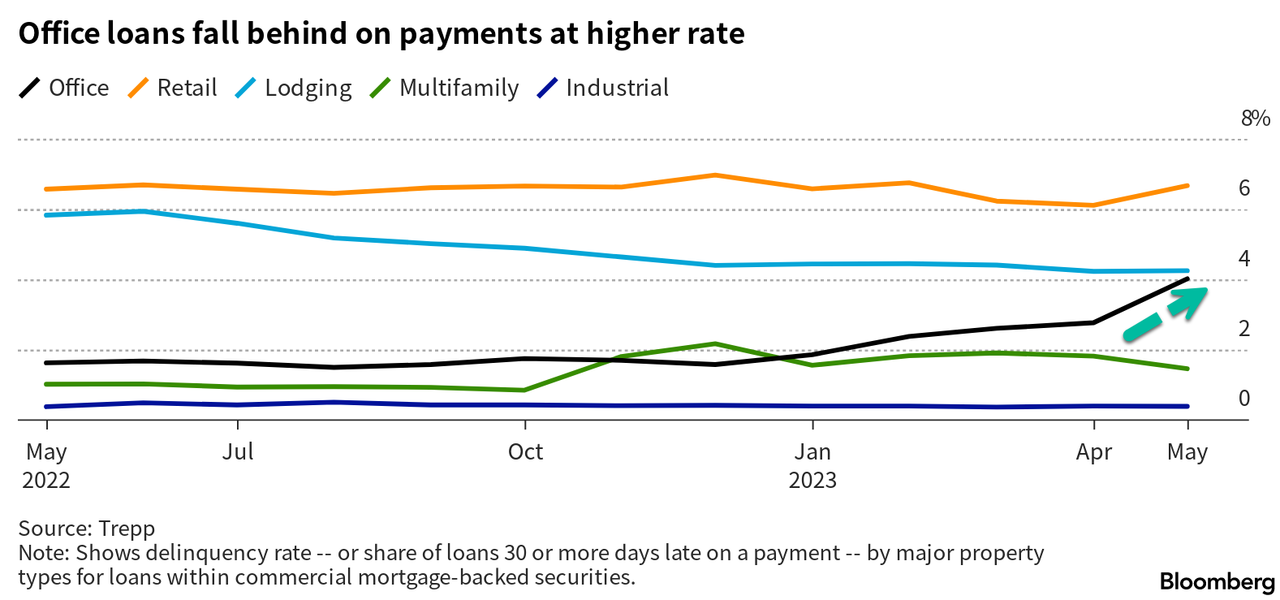

Some structural factors, such as remote work and hybrid work, have doomed the office space segment. This has left empty office buildings scattered across major US cities as the number of landlords falling behind on repayments due to the difficulty of refinancing and high vacancies has hit a five-year high.

According to real estate data firm Trepp, more than 4% of office loans packed into commercial mortgage-backed securities were delinquent in the last 30 days as of May, the highest level since 2018.

Dan McNamara, the founder of Polpo Capital Management, told Bloomberg about impending CRE turmoil:

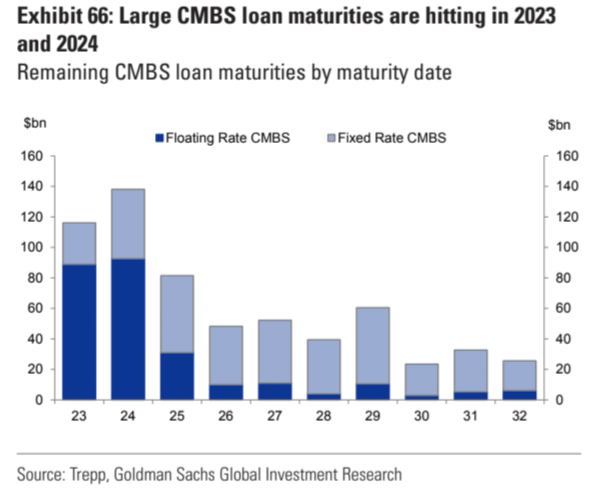

“This is just the tip of the iceberg for office delinquencies as $35 billion in CMBS office loans are scheduled to mature this year and the refinancing market is effectively shut to this asset class.”

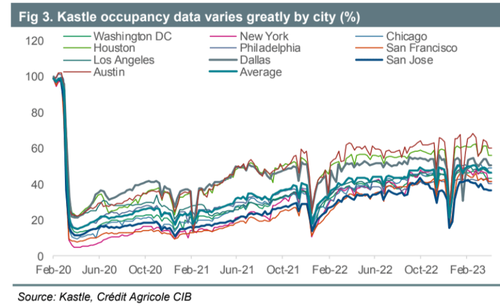

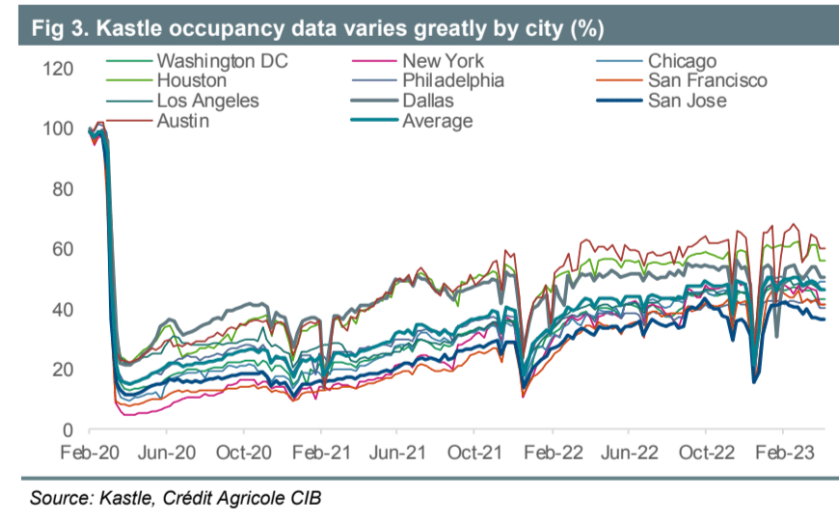

The rise in delinquencies comes as security card swipe data from Kastle shows many workers have yet to return to their desks in major US cities, resulting in high office space vacancies nationwide.

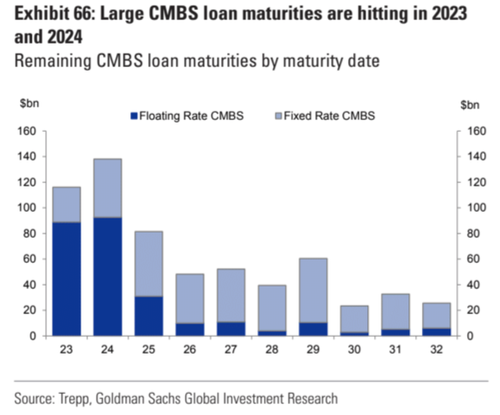

As Goldman pointed out to clients days ago, one major issue is a steep maturity wall of floating and fixed-rate CMBS loans due this year and next. The inability to refinance in these challenging market conditions will likely unleash a tidal wave of defaults in the second half of this year.

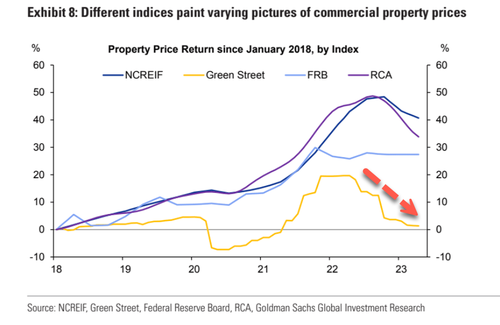

Goldman Sachs chief credit strategist Lotfi Karoui told clients last month, “the most accurate portrayal of current market conditions” is data via the Green Street Commercial Property Price Index, which suggests trouble ahead.

Just how much danger? Karoui believes “Green Street indicates a 25% year-over-year drop in office property values and a 21% drop in apartment property values.”

So the combination of high vacancies, sliding prices, and tightening lending standards is a perfect storm that could ignite an eruption of delinquencies in office loans in the coming quarters.

Treasury Secretary Janet “Too Low For Too Long” Yellen, and former Federal Reserve Chair, is partly responsible for a phenomenon plaguing America: the death of starter homes.

As Mish has discussed, with main markets no longer an option for first-time buyers, Point2 looked at the country’s 100 largest secondary cities for the median price of a starter home and renter households’ median income. Defined as large non-core cities within a metro, these cities used to be fruitful house-hunting grounds for first-time buyers exploring less-expensive options away from main cities. But as it turns out, unaffordability can put a dent in homeownership plans regardless of city type or size.

In 41 of the 100 largest secondary cities in the U.S., renters earn half or less than half of the income they would need to buy a median-priced starter home.

There are no non-core cities in which renters could comfortably make a move toward homeownership: In 10 cities, the necessary income is about triple what they earn.

Would-be buyers in Burbank and Glendale, CA have it worst: They lack 67% of the income they would need in order to make the move from renter to homeowner.

Renters in 9 California cities would need to earn about $100,000 more in order to afford a starter home. Based on the latest renter income figures, starter home prices, and mortgage rates, non-core cities in the LA and San Diego metros are the toughest for first-time homebuyers.

In 15 of the 100 largest secondary cities, renters would need less than 4 months’ worth of extra income to afford the transition to owning a starter home.

Homeownership is within reach in Independence, MO, and Broken Arrow, OK. Those who dream of owning here would need less than one month’s worth of extra income to afford a starter home.

California Tops the List of Worst Places to Look

California has the dubious distinction of having the top least affordable starter home cities.

A starter home, according to the Census Department is priced in the bottom third of homes in the area.

Pomona, CA, is in fourteenth place. The average renter in Pomona makes $49,000 a year and needs to get to $121,000 a year. That’s nearly 2.5 times current salary.

In Burbank, CA, the average renter makes $63,000 year an needs to get to $193,000. That’s over 3 times current salary.

Within Grasp

In no market can the average renter make the plunge.

But in Independence, Missouri, or Broken Arrow, Oklahoma, the average renter is respectively just 2% and 5% short of the amount needed for a starter home

Not Shocking

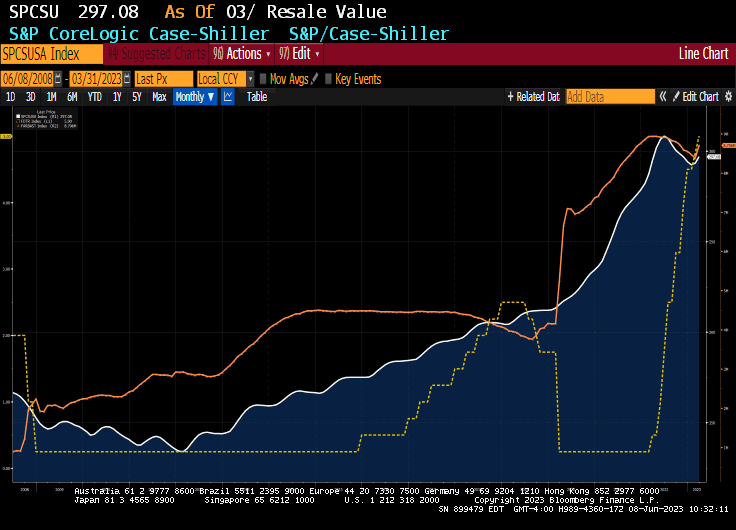

None of this is shocking. It matches one one should expect looking at Case-Shiller home prices and mortgage rates.

The Fed wanted to produce inflation and it did. But for years the Fed did not even see the inflation because the manifestation of inflation was in asset prices, not the price of consumer goods.

Case-Shiller Top City Home Prices Decline From Year Ago for the First Time Since May 2012

Housing starts, like mortgage purchase demand, remains depressed compared to the housing bubble of the 2000s.

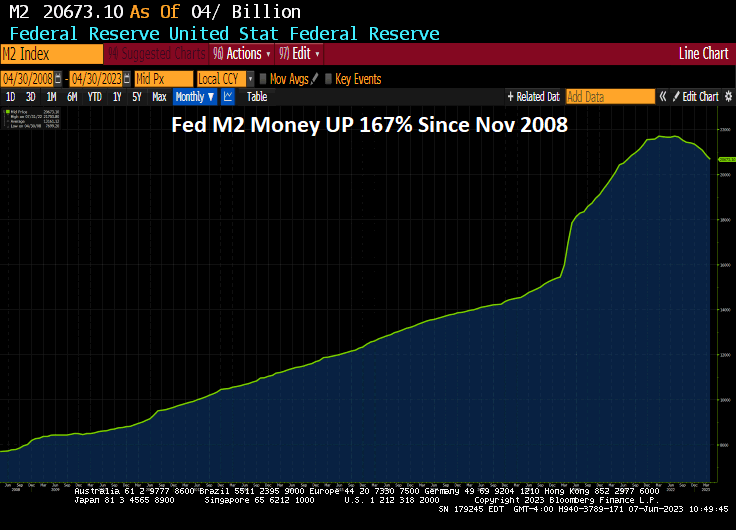

Now, will The anticipated Fed pause in rate hiking help? Not likely. The Fed still has over $8 trillion in monetary stimulus chasing assets. Too much Stimulypto.

One has to wonder about The Feral Reserve. Since The Great Recession of 2008, The Federal Reserve has printed a staggering amount of money (know as QE). There is still about $8.3 TRILLION in monetary stimulus sloshing around the economy.

And M2 Money printing is up 167% since November 2008.

So, despite the talking heads from The Fed and CNBC, etc blathering about Fed tightening, there remains over $8 TRILLION in monetary stimulus chasing asset prices.

Is The Fed ACTUALLY the US economy? Or is The Fed the financing arm of the Democrat party?

Yes, The Fed looks like they are pausing .. rate hikes.

Welcome to the Bidenville Mortgage Depot! Where Bidenflation (caused by idiotic energy policies, crazy Fed money printing and insane Federal spending) has caused The Fed to raise rates crushing the US mortgage market.

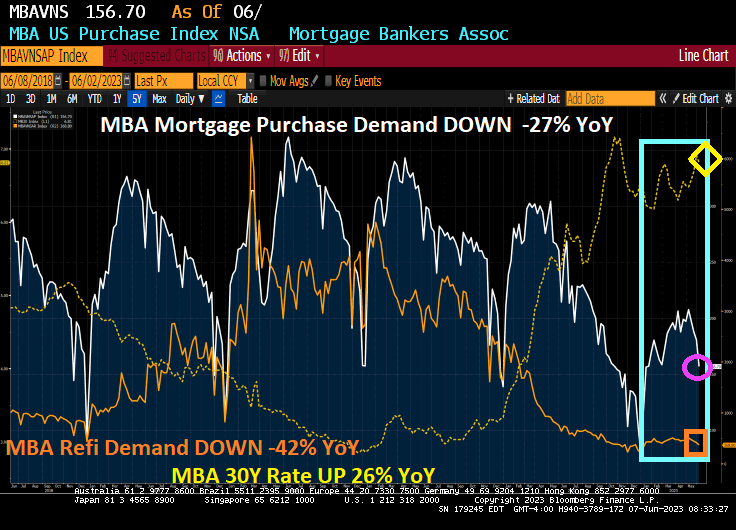

Mortgage applications decreased 1.4 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending June 2, 2023. This week’s results include an adjustment for the Memorial Day holiday.

The Market Composite Index, a measure of mortgage loan application volume, decreased 1.4 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index decreased 12 percent compared with the previous week. The Refinance Index decreased 1 percent from the previous week and was 42 percent lower than the same week one year ago. The seasonally adjusted Purchase Index decreased 2 percent from one week earlier. The unadjusted Purchase Index decreased 13 percent compared with the previous week and was 27 percent lower than the same week one year ago.

The rest of the story.

The East Palestine Ohio train wreck is symbolic of Biden’s economic programs. I don’t think the Vacationer in Chief (40% of time as President has been on vacation) has been there yet.

But it isn’t just San Francisco. Phil Hall reports that Fitch Ratings reduced its 2023 outlook for the U.S. real estate investment trust (REIT) sector outlook from “Neutral” to “Deteriorating,” citing the tumult in the commercial real estate space.

While Fitch noted that most of its rated REITs “have the capacity to withstand such a slowdown within rating sensitivities [and] those with ample dry powder could capitalize on distressed property sales by weaker capitalized players.” But at the same time, the ratings agency warned that banks – which account for nearly half of the $5.5 trillion commercial mortgage market – saw their lending levels drop by 20% between February and April, with more tightening expected.

“At minimum, this will lead to further contractions in CRE credit, further limiting conditions for property transactions,” Fitch added in its announcement of the outlook reduction, adding that “CRE transaction volume has steadily declined since early 2022 due to the confluence of operating fundamentals pressure, higher interest and capitalization rates, limited buyer financing, and looming recession risk. The rapid jump in rates has resulted in unusually wide value discrepancies between buyers and sellers across most property types and markets, particularly in the struggling office sector. Our forward-looking U.S. equity REIT ratings incorporate assumptions about future property disposition volumes and valuations.”

Fitch predicted the U.S. economy will go into a recession, most likely late in the year – a previous forecast put the downturn at mid-year – and forecasted property performances will vary by sector over the next two years.

“Sectors experiencing strong fundamentals, such as industrial and shopping centers, will likely see some cooling in demand, with tenants showing greater reluctance to lease space, including delaying decisions, resulting in less pricing power for landlords,” Fitch continued. “Tighter lending conditions and weaker economic growth will add to the secular pressures facing some property formats (e.g. office, enclosed malls). The office REIT sector has met, or modestly underperformed, our low expectations during 2023. Leasing volumes have generally underperformed as occupiers add the business cycle to the list concerns and reasons for conservatism, along with secular pressure from remote work. Conversely, the industrial sector, although no longer white hot, continues to deliver above average occupancies and outsized rent growth that have modestly exceeded our projections.”

While Fitch stressed that REITs were “unlikely to directly encounter meaningful stress” based on the recent problems in the banking industry, although it also acknowledged that it did not expect “REITs’ access to unsecured revolvers will be impeded, although facilities up for renewal will likely see higher pricing and some banks have reduced appetites for traditional bank syndicate activities, such as making funded term loans – particularly in hard hit sectors, such as office. We also do not expect meaningful portfolio vacancies caused by bank tenant failures, which are unlikely to be widespread.”

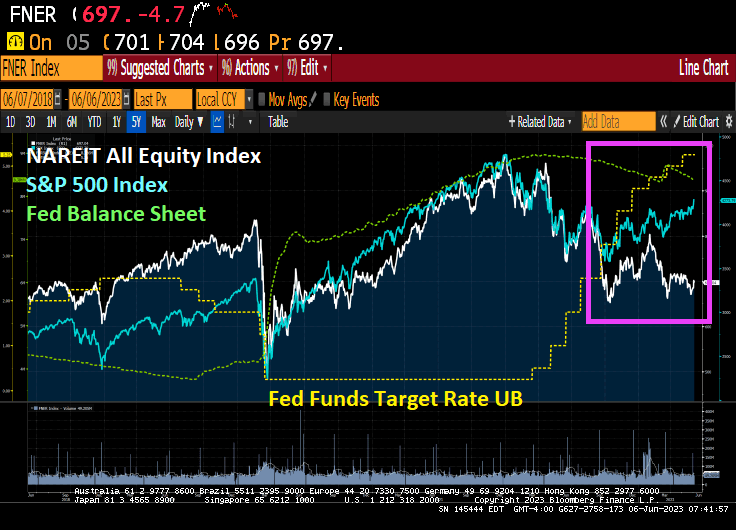

The NAREIT All-equity index has gotten pummelled by the S&P 500 index since The Fed started tightening monetary policy to fight inflation …. that The Fed helped cause in the first place.

Under Biden, the US is beginning to morph into a lawless Socialist sewer like Venezuela. Joe Maduro??

Biden signed the debt ceiling bill craftted by McCarthy (RINO-CA) and Schumer (Communist-NY). Its allows for uncontrolled spending and borrowing for at least 2 years. And as Milton Friedman once said “There is nothing more permanent than a temorary Federal program … or debt limitiations.

With Biden signaling that government has gone wild with no controls on fiscal responsibility (and Elizabeth Warren flailing her arms and screaming for regulations on cryptocurrencies), cryptos today are getting demolished.

China, Japan and the BRICs realize that there are no controls on ANYTHING coming out of Washington DC. Insane spending, an insane Federal Reserve, corrupt DOJ and FBI.

The US economy was sitting high on the global mountain top before Covid. Then Covid struck, The Federal Reserve and Congress went wild with stimulus spending and inflation went wild. This is Biden Country, a feeble shell of this once great nation.

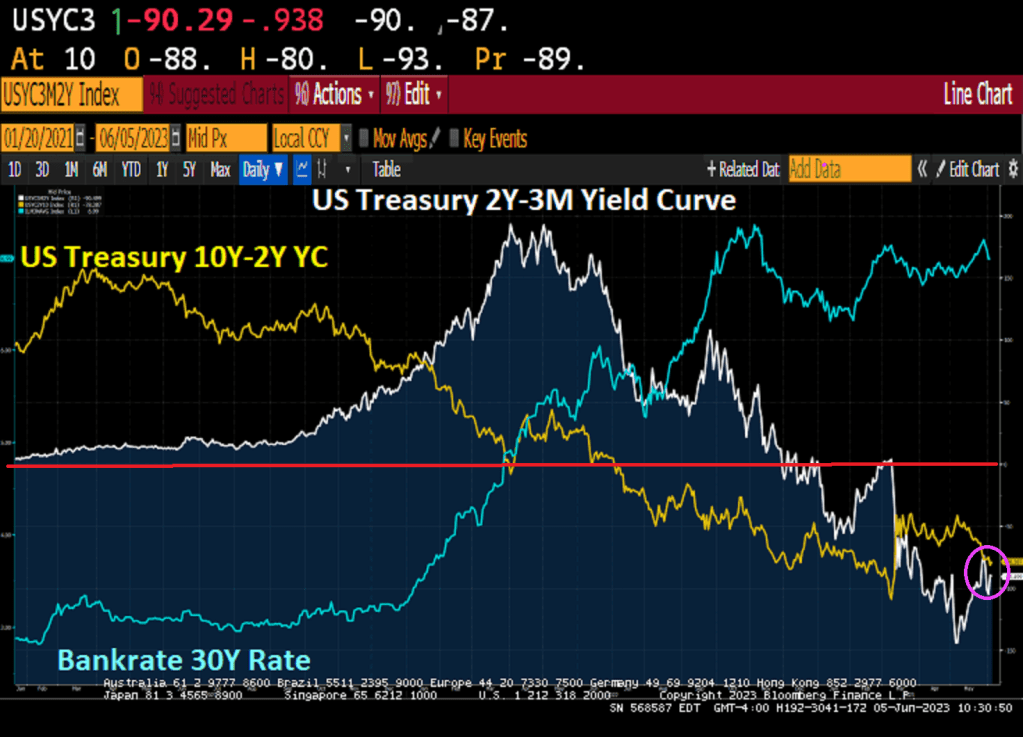

As The Fed tries to counter the years of excess monetary stimulus pre and post Covid by raising rates, we have seen mortgage rates rise 143% under Biden’s leadership. At the same time, the US Treasury yield curves (short 2Y-3m and long 10Y-2Y) remain deeply inverted.

As of this AM, The Fed Funds Futures market is pricing in a chance of continued rate hikes by The Fed, but mostly we are at 5.25% at least until November when rates are forecast to begin declining.

And the Taylor Rule is still signaling rate hikes to 10.12%. We are at only 5.25%. And with Biden feebily running for reelection, the only path forward is rate CUTS.

Well, Kevin McCarthy (RINO-CA) and Patrick McHenry (RINO-NC) along with Jim Jordan (RINO-OH) and Marjorie Taylor Greene (RINO-GA) sold out America to Green Joe Biden (the Jolly Green Giant?) and pretty much guaranteed a Biden reelection as President and Democrats winning the House majority at the next election. Way to go McCarthy, McHenry, Jordan an Greene! You sold out America to the Progressive, destructive Left.

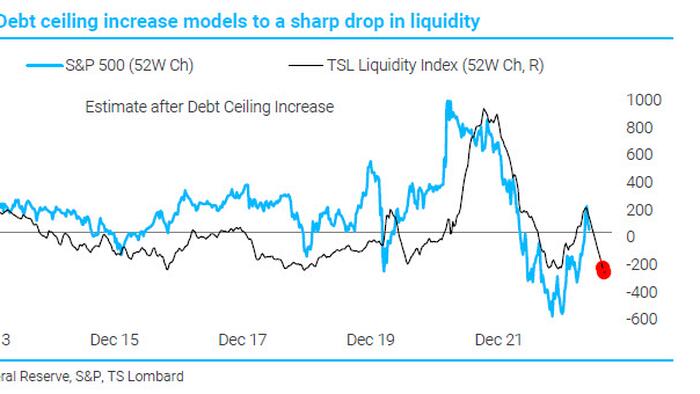

With a debt ceiling deal freshly inked, the US Treasury is about to unleash a tsunami of new bonds to quickly refill its coffers.This will be yet another drain on dwindling liquidity as bank deposits are raided to pay for it — and Wall Street is warning that markets aren’t ready.

The negative impact could easily dwarf the after-effects of previous standoffs over the debt limit. The Federal Reserve’s program of quantitative tightening has already eroded bank reserves, while money managers have been hoarding cash in anticipation of a recession.

JPMorgan Chase & Co. strategist Nikolaos Panigirtzoglou estimates a flood of Treasuries will compound the effect of QT on stocks and bonds, knocking almost 5% off their combined performance this year. Citigroup Inc. macro strategists offer a similar calculus, showing a median drop of 5.4% in the S&P 500 over two months could follow a liquidity drawdown of such magnitude, and a 37 basis-point jolt for high-yield credit spreads.

The sales, set to begin Monday, will rumble through every asset class as they claim an already shrinking supply of money: JPMorgan estimates a broad measure of liquidity will fall $1.1 trillion from about $25 trillion at the start of 2023.

“This is a very big liquidity drain,” says Panigirtzoglou. “We have rarely seen something like that. It’s only in severe crashes like the Lehman crisis where you see something like that contraction.”

It’s a trend that, together with Fed tightening, will push the measure of liquidity down at an annual rate of 6%, in contrast to annualized growth for most of the last decade, JPMorgan estimates.

The US has been relying on extraordinary measures to help fund itself in recent months as leaders bickered in Washington. With default narrowly averted, the Treasury will kick off a borrowing spree that by some Wall Street estimates could top $1 trillion by the end of the third quarter, starting with several Treasury-bill auctions on Monday that total over $170 billion.

What happens as the billions wind their way through the financial system isn’t easy to predict. There are various buyers for short-term Treasury bills: banks, money-market funds and a wide swathe of buyers loosely classified as “non-banks.” These include households, pension funds and corporate treasuries.

Banks have limited appetite for Treasury bills right now; that’s because the yields on offer are unlikely to be able to compete with what they can get on their own reserves.

But even if banks sit out the Treasury auctions, a shift out of deposits and into Treasuries by their clients could wreak havoc. Citigroup modeled historical episodes where bank reserves fell by $500 billion in the span of 12 weeks to approximate what will happen over the following months.

“Any decline in bank reserves is typically a headwind,” says Dirk Willer, Citigroup Global Markets Inc.’s head of global macro strategy.

Bitcoin Faces Downside Risks After Debt Deal Moves Forward

Just when markets appear to be moving past the months-long drama around the US debt ceiling, holders of risky assets such as cryptocurrencies are likely facing a fresh challenge while the Treasury looks to rebuild its depleted cash balance with an estimated $1 trillion Treasury-bill deluge.

“The impending reserve drawdown, due to the [Treasury General Account] rebuild, may prove to be a headwind,” Citi Research strategists including Alex Saunders wrote in a note.

Citi analyzed the performance of risky assets during drawdowns and found that they were vulnerable to higher volatility and weaker returns. As such, the near-term outlook doesn’t seem too rosy for Bitcoin and Ether. “Both coins average negative returns in these scenarios, and BTC has significantly underperformed in the median case,” the strategists wrote Thursday.

The TGA, which keeps money for the Treasury, ballooned during the pandemic. It expanded again last year and is now about as low as it has ever been. Treasury, as a result, will need to replenish its dwindling cash buffer to maintain its ability to pay its obligations through bill sales, estimated at well over $1 trillion by the end of the third quarter. This supply burst may drain liquidity from the banking sector and raise short-term funding rates against an economy many say is likely to fall into recession.

This doesn’t bode well for digital-asset investors, who were just recovering from fears of a no-deal scenario for the US debt ceiling. While Bitcoin edged higher on Friday, it’s still hovering around the $27,000-mark that it has failed to break away from for several weeks.

“Crypto markets were not immune to fears of the US defaulting on its debt, selling off on negative developments and rallying on headlines suggesting progress,” the strategists said. They added that crypto has typically “fared well” amid issues concerning traditional financial institutions, citing the banking turmoil in March, a period in which Bitcoin outperformed. But perhaps risks of an institution such as the US government defaulting “doesn’t paint a favorable outlook for decentralized digital assets.”

To illustrate, the strategists used the Cboe Volatility Index, or VIX, as an indicator of the market’s fear to gauge whether a resolution would be passed before hitting the ceiling. And whenever equity market concerns were eased, that’s when Bitcoin outperformed.

“While in theory the potential default of an institution as impactful as the US government would bode well for decentralized technologies and systems, this may not currently be the case given that the crypto industry is still in its infancy and regulation has yet to be well-defined,” they wrote. “Another theory is that not raising the debt ceiling would lead to reduced US government debt and a lower fiscal deficit, and provide more credibility to fiat, particularly the dollar.”

On Friday, the Senate passed legislation to suspend the US debt ceiling and impose restraints on government spending through the 2024 election. The measure now goes to President Joe Biden, who forged the deal with House Speaker Kevin McCarthy and plans to sign it just days ahead of a looming US default.

Year-to-date, Bitcoin has rebounded some 60% after starting the year at around $16,500. Such optimism comes after 2022’s 64% drop, its second-worst year in its history. It rose about 1% to $27,178 as of 3:32 p.m. in New York, and is marginally higher from last Friday.

Bitcoin’s support hovers around $26,500, said Fiona Cincotta, senior market analyst at City Index, adding that a break below $25,000 could mean a deeper sell-off.

“The problem is the macro backdrop, which is relatively uncertain going forward with recessionary fears,” she said. “I think what will be looking for to make Bitcoin shine is a nice dovish pivot from the Federal Reserve. That might be the tide where we will see another decent leg higher.”

Range-bound trading has been Bitcoin’s defining characteristic of late, with its 30-day volatility reigning low at 1.8%, firmly staying firm within its two-month-long trading range. Despite growing short-term volatility, options implied volatility trended lower over the past week, according to K33’s Bendik Schei and Vetle Lunde. Even so, Bitcoin exchange-traded products continued to see steady outflows while Bitcoin volumes — spot and futures — are trending lower.

McCarthy, McHenry, Jordan and Greene, honorary Frenchmen!

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.