The Philly Fed non-manufacturing sentiment index just tanked to -12.8 as The Federal Reserve removes its Covid-related stimulus.

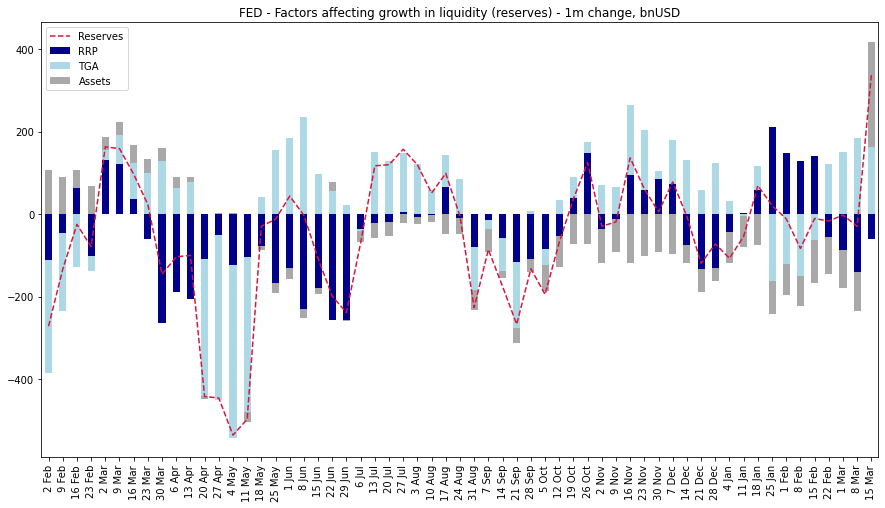

The banking fiasco (SVB, Signature, etc.) has caused The Fed’s balance sheet to expand … again.

And Fed Funds Futures are pricing in a meager 20 basis points increase at tomorrow’s FOMC meeting (some betting on no change, some betting on 25 basis points). Then another rate hike at the May FOMC meeting, then all downhill from there.

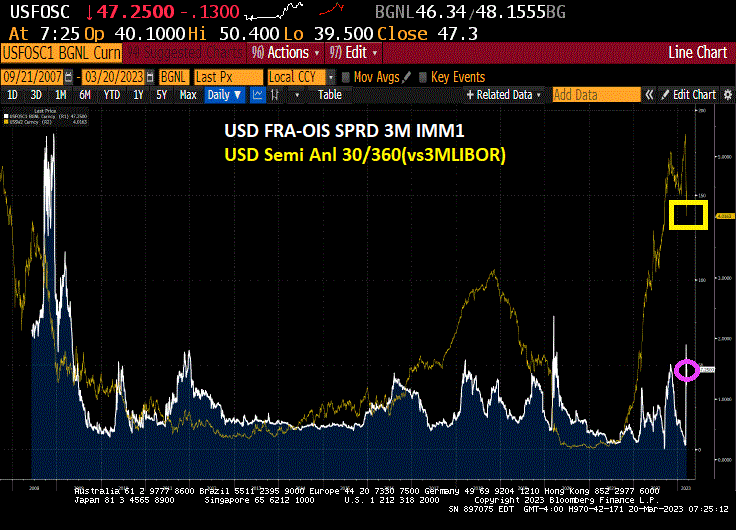

Its the start of a new week after the closure of several US banks (SVP, Signature) and the failure of Credit Suisse. But swaps spreads have calmed down a bit and are no where near the credit crisis highs of late 2008. Or the plain vanilla swap between fixed and variable contracts (white line) has simmered down a bit. BUT was never as high as it was during the financial crisis. Panic by The Fed and FDIC much?

And the 2-year Treasury yield dropped -10 basis points … again.

The Bank of Canada, the Bank of England, the Bank of Japan, the European Central Bank, the Federal Reserve, and the Swiss National Bank are today announcing a coordinated action to enhance the provision of liquidity via the standing U.S. dollar liquidity swap line arrangements.

To improve the swap lines’ effectiveness in providing U.S. dollar funding, the central banks currently offering U.S. dollar operations have agreed to increase the frequency of 7-day maturity operations from weekly to daily. These daily operations will commence on Monday, March 20, 2023, and will continue at least through the end of April.

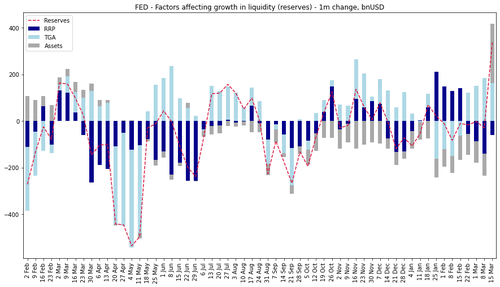

And once the USD swap lines are reopened, the rest of the cavalry follows: rate cuts, QE (the real stuff, not that Discount Window nonsense), etc, etc. In fact, we have already seen a near record surge in reserve injections:

The Fed may as well formalize it now and at least preserve some confidence in the banking sector, even if it means destroying all confidence left in the “inflation fighting” Fed, with all those whose were in charge handing in their resignation for their catastrophic handling of this bank crisis.

Its Gov’t Gone Wild! Insane spending budget by “Sloppy Joe” Biden, Yellen asking Warren Buffet for banking advice (seriously??), a war in Ukraine that America doesn’t seem to actually want to win, etc. But its the banking system where banks are getting crushed by rising inflation and interest rates (but failed to hedge). Sigh.

As I always told my investments and fixe-income students at University of Chicago, Ohio State University and George Mason University, a 10 basis point change in the 2-year and 10-year US Treasury yield is a big deal. This morning, the US Treasury 2-year yield fell -32 basis points while the 10-year Treasury yield fell -14.8 basis points.

At the same time, gold 3.8% and silver rose 4.7% on banking fears.

Debt would hit a new record by 2027, rising from 98 percent of GDP at the end of 2023 to 106 percent by 2027 and 110 percent by 2033. Nominal debt would grow by $19 trillion, from $24.6 trillion today to $43.6 trillion by 2033.

Deficits would total $17.1 trillion (5.2 percent of GDP) between FY 2024 and 2033, rising to $2.0 trillion, or 5.1 percent of GDP, by 2033.

Spending and revenue would average 24.8 and 19.7 percent of GDP, respectively, over the next decade, with spending reaching 25.2 percent of GDP and revenue totaling 20.1 percent by 2033. The 50-year historical average is 21.0 percent of GDP for spending and 17.4 percent of GDP for revenue.

Proposals in the budget would reduce projected deficits by $3 trillion through 2033, including $400 billion through 2025 when it could help fight inflation. The budget proposes $2.8 trillion of new spending and tax breaks, $5.5 trillion of revenue and savings, and saves $330 billion from interest.

The budget relies on somewhat optimistic economic assumptions, including stronger long-term growth, lower unemployment, and lower long-term interest rates than the Congressional Budget Office (CBO). The budget assumes 0.4 percent growth this year, 2.1 percent growth next year, and 2.2 percent by the end of the decade – compared to CBO’s 0.1 percent, 2.5 percent, and 1.7 percent, respectively. The budget also assumes ten-year interest rates fall to 3.5 percent by 2033, compared to CBO’s 3.8 percent.

And then we have Sloppy Joe and Statist Janet Yellen meeting with mega donor Warren Buffet for advice on dealing with the banking crisis … made by Biden’s energy policy and insane Covid spending by the Administration. And, of course, The Fed’s “too low for too long” monetary policy. What is 92-year old Warren Buffet going to say?

Meanwhile, Fed Funds Futures are pointing to one more rate hike then a series of rate cuts down to 3.737 by January 2024.

Despite endless promises from Washington DC that there would never be another bank bailout, the Biden Administration bailed out Silicon Valley Bank (SVB) by removing the $250,000 cap on deposit insurance. Then Treasury Secretary Janet Yellen added that in the future, only banks that posed SYSTEMIC RISK to the economy will be bailed out. Translation: only the big four Too Big To Fail (TBTF) banks will be bailed out. Meaning that the Biden Administration prefers big banks to community banks. “Middle-class Joe” loves BIG Pharma, BIG defense, BIG tech, BIG media and now BIG banks. He should rename himself “Big Joe” Biden for the 2024 Presidential election.

Of course, we are aware of The Fed’s about face on shrinking their balance sheet (green line). While Bankrate’s 30-year mortgage rate has now declined below 7% to 6.97%, it has only fallen -15 basis points since the recent peak of 7.12% on 3/2/2023 when the 10-year Treasury yield was 4.056%. So, the 10-year Treasury yield has fallen -62.7 basis points since 3/2/2023 while the 30-year mortgage rate dropped only -15 basis points.

On the European banking front, Credit Suisse is kaput and both Swiss Bank and Deutsche Bank are considering buying the assets of Credit Suisse. In other words, MORE bank consolidation.

Here is a chart of US bank consideration as of 2009 with 37 banks in 1990 shriveling to 4 mega, TBTF banks in 2009 that remain today. But will the now unprotected community and local banks be absorbed into the 4 superbanks? Time will tell, but if history is repeated, the answer is yes.

The KBW bank index continued to fall despite the bailouts of SVB and Signature Banks. But at least total returns on Treasuries and MBS that banks hold increased with the return of QE!

Yellen and Biden compete for the Knucklehead Of The Century Award. While not as sloppy as the sudden Afghanistan withdrawal, bailing out the Silicon Valley elites will not end well.

Cry for Argentina! Their central bank boosted its benchmark Leliq rate by 300 basis points to 78%. The monetary authority’s board considered the increase in response to accelerating inflation and after leaving the key rate unchanged for several months.

Of course, the US Federal Reserve is going in the opposite direction to combat the US banking crisis created by inflation and Yellen’s “Too low for too long” Fed policies.

I am beginning to wonder in Treasury Secretary Janet Yellen and Chicago Mayor Lori Lightfoot are the same person. Both complete Statist screw-ups.

So, the Biden Administration made a horrible error by guaranteeing deposits at Silicon Valley Bank for deposits over $250,000. Essentially, Biden bailed out big tech that kept their deposits at SVB.

But what triggered the run on SVB and other banks? Simple. Biden and Congress spent like drunken sailors with Covid and The Federal Reserve went nuts printing money. Viola! We got inflation. But with inflation came The Fed’s attempt to get inflation back to its 2% target (difficult since Biden/Congress refuse to return spending to pre-Covid levels). But as interest rates rise, duration (weighted average life of MBS) rose dramatically meaning that risk increased. But banks like SVP ignored the risk, or didn’t hedge, or were spending time worrying about non-bank related issues.

So, what happened? Banks are holding Treasuries and MBS (orange line) that are getting clobbered with rate hikes (yellow line).

Talk about volatility. Today, the 2-year Treasury yield is up over 20 basis points as bond volatility hits levels last seen in 2008, just prior to the subprime credit crisis.

So, Biden’s bailout of SVP depositors stopped the deposit run for the moment. But if The Fed keeps hiking rates, banks are going to be hurting worse and worse. They could rebalance their portfolios and/or hedge. But with Uncle Spam (Biden) at the helm, bailouts are always on the table.

Argetina’s inflation rate just hit 102.5% as their M2 Money printing hit 80%

Argentina’s central bank is considering raising its benchmark rate on Thursday for the first time since September after inflation data showed prices increased by more than 100% annually last month, according to two people with direct knowledge.

The monetary authority’s board will consider an increase after leaving the key Leliq rate unchanged at 75% for several months, the people said, asking not to be named discussing internal decisions. The board has not yet decided on the size of the hike in case they opt for such move, they said.

A cautionary tale for Washington DC spendacrats and Fed officials.

Brought to the same country that gave us Statist Juan Peron and his wife Eva.

Apparently, the NEO financial crisis (not the subprime, but The Fed’s “too low for too long” crisis) is still with us.

Credit Suisse Group AG’s top shareholder, whose stake has lost more than one-third of its value in three months, ruled out investing any more in the troubled Swiss bank as a bigger holding would bring additional regulatory hurdles.

“The answer is absolutely not, for many reasons outside the simplest reason, which is regulatory and statutory,” Saudi National Bank Chairman Ammar Al Khudairy said in an interview with Bloomberg TV on Wednesday. That was in response to a question on whether the bank was open to further injections if there was another call for additional liquidity.

Credit Suisse says it has identified material weaknesses in its internal control over financial reporting as of December 31, 2022 and 2021, according to the annual report.

The material weaknesses relate to the failure to design and maintain an effective risk assessment to identify and analyze the risk of material misstatements in its financial statements and the failure to design and maintain effective monitoring activities relating to: – Providing sufficient management oversight over the internal control evaluation process to support the Group’s internal control objectives – Involving appropriate and sufficient management resources to support the risk assessment and monitoring objectives Assessing and communicating the severity of deficiencies in a timely manner to those parties responsible for taking corrective action

And it could simply be that Credit Suisse was caught in the Central Bank “Bear Trap” where banks get clobbered as interest rates rise.

Credit Suisse’s CDS (credit default swap) is soaring!

And on the “it ain’t over till its over” news from Credit Suisse, the US Treasury 2-year yield plunged -40.4 basis points.

And the US Treasury 10-year yield plunged -24.8 basis points.

The official logo of the Federal Reserve should be Munch’s The Scream.

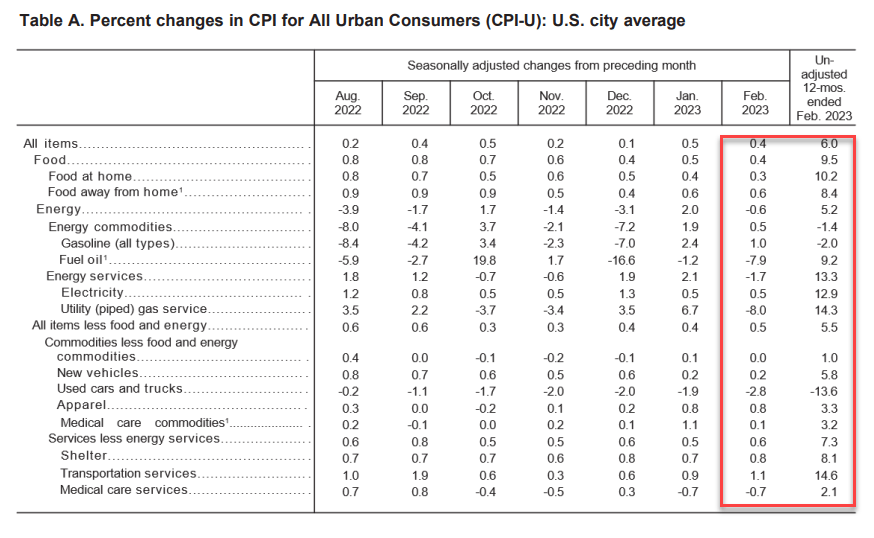

While headline inflation (CPI) came in a 6% (considerably higher than The Fed’s 2% target), core inflation came in at 5.5% year-over-year (YoY), which was expected.

The truly nasty number is today’s inflation report is that weekly earnings YoY remained the same at a terrible -1.9%. Meaning that inflation is higher than nominal wage growth. This is the 23rd straight month of negative real weekly earnings. Well done, Fed and Biden!

Food is up 10.2% YoY. Electricity up 12.9%, shelter up 8.1%.

On the news, the US Treasury 2-year yield rose 34.3 basis points.

Somehow I doubt that Biden’s press secretary will tout 23 straight months of negative weekly earnings growth as one of Biden’s economic accomplishments.

{kind=link}

You must be logged in to post a comment.