Like virtually everything in Biden’s economy, the price of turkey (often the main staple for Thanksgiving dinner) is way up in price. Turkey prices are UP 73% since last year. The price per pound of an 8- to 16-pound turkey has risen to $1.99, a 73% increase from $1.15 last year, according to USDA data.

Speaking of turkeys, in recent speeches, President Joe Biden has been misleadingly taking credit for cutting federal deficits by historic amounts, though most of the reduction in deficits is the result of expiring emergency pandemic spending. Deficits fell between fiscal year 2020 and 2021 far less than initially projected after Biden added to them with more emergency pandemic and infrastructure spending.

And apparently Biden (or Jill) haven’t looked at the data recently. While there was a momentary budget surplus in April 2022, the Federal budget deficit has increased dramatically in September 2022 to the worst deficit since March 2021 shortly after Biden took office.

The only thing that is strong under Biden is the labor market. But even the accomplishment is grossly misleading. Under Trump, the U-3 unemployment rate was 3.5% in February 2020 just before Covid-13 struck and the Fauci-ites shut down the economy causing unemployment to rise to 14.7% in April 2020. Most of the reduction in the unemployment rate was the result of the economy slowly opening back up under Trump. When Biden took over, the unemployment rate was 6.4% and it is finally back to Trump’s 3.5% in September 2022. At least Biden didn’t screw that up, as Obama has said. Perhaps that should be his new midterm campaign slogan!

But Biden DID screw up the labor market with Bidenflation. REAL average hourly earnings growth (yellow line) is NEGATIVE..

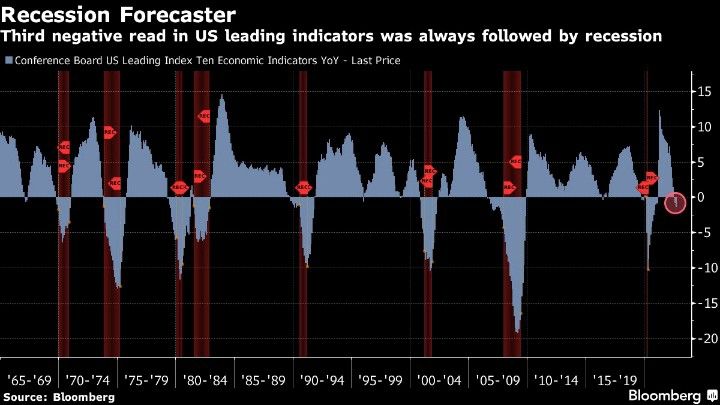

And yes, the US is rapidly approaching recession which will result in a spike in unemployment. So much for Biden’s “Strong as hell!” economy.

Two turkeys taking a stroll, but I would rather listen to the shorter turkey. At least the speeches would be coherent.

You must be logged in to post a comment.