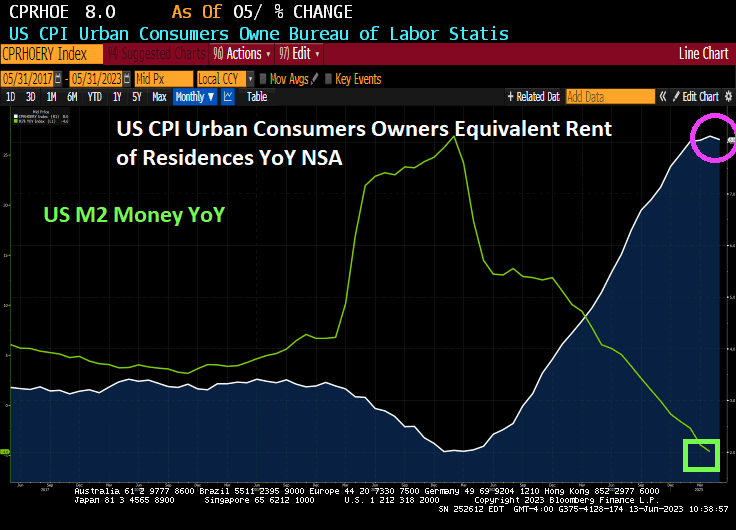

Fed Governor Christopher Waller said Friday headline inflation has been “cut in half” since peaking last year, but prices excluding food and energy (aka, CORE inflation) has barely budged over the last eight or nine months.

“That’s the disturbing thing to me,” Waller said during a question-and-answer session following a speech in Oslo, Norway. “We’re seeing policy rates having some effects on parts of the economy. The labor market is still strong, but core inflation is just not moving, and that’s going to require probably some more tightening to try to get that going down.”

At a separate event Friday, Richmond Fed President Thomas Barkin said inflation remained “too high” and was “stubbornly persistent.”

“I want to reiterate that 2% inflation is our target, and that I am still looking to be convinced of the plausible story that slowing demand returns inflation relatively quickly to that target,” Barkin said in a speech in Ocean City, Maryland. “If coming data doesn’t support that story, I’m comfortable doing more.”

The Federal Open Market Committee paused its series of interest-rate hikes Wednesday, but policymakers projected rates would move higher than previously expected in response to surprisingly persistent price pressures and labor-market strength.

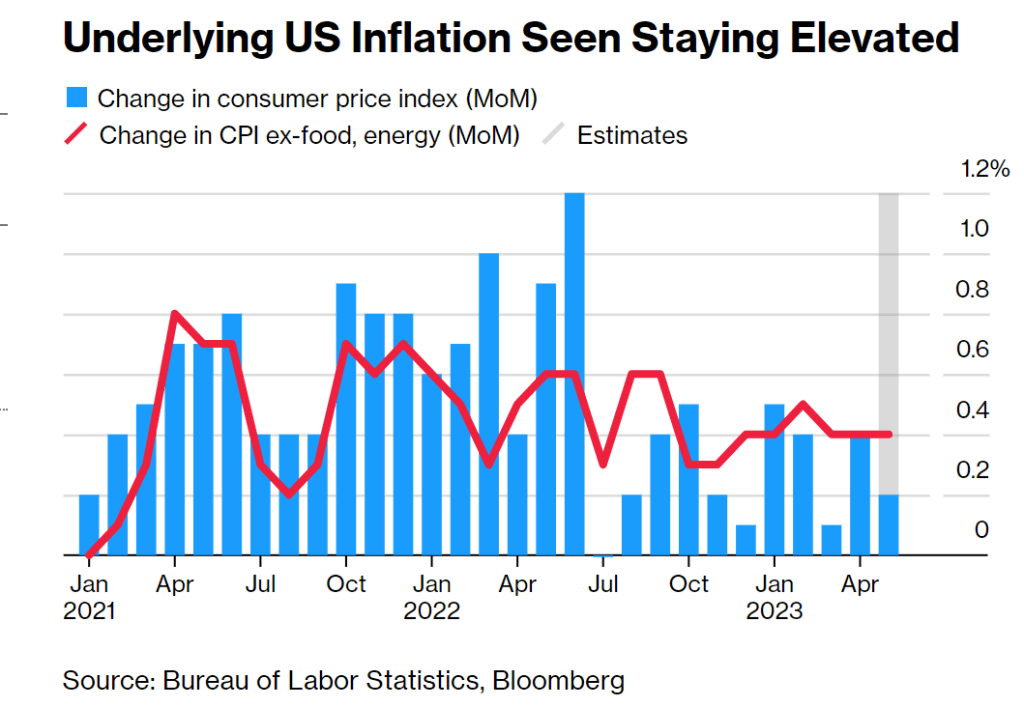

The consumer price index this week showed headline inflation slowed, but core prices excluding food and energy continued to rise at a pace that’s concerning for Fed officials. Employers continued adding jobs at a rapid clip in May, and job openings climbed in April, recent data showed.

Barkin warned that prematurely loosening policy would be a costly mistake.

“I recognize that creates the risk of a more significant slowdown, but the experience of the ’70s provides a clear lesson: If you back off inflation too soon, inflation comes back stronger, requiring the Fed to do even more, with even more damage,” he said. “That’s not a risk I want to take.”

Policy Report

Separately, the Fed released a new report Friday that said tighter US credit conditions following bank failures in March may weigh on growth, and that the extent of additional policy tightening will depend on incoming data.

“The FOMC will determine meeting by meeting the extent of additional policy firming that may be appropriate to return inflation to 2% over time, based on the totality of incoming data and their implications for the outlook for economic activity and inflation,” the Fed said in in its semi-annual report to Congress.

Read More: Fed Says Tighter Credit Conditions to Weigh on US Growth

The Fed report, which provides lawmakers with an update on economic and financial developments and monetary policy, was published on the central bank’s website ahead of Chair Jerome Powell’s testimony before the House Financial Services Committee on June 21. He will appear before the Senate banking panel the following day.

“Evidence suggests that the recent banking-sector stress and related concerns about deposit outflows and funding costs contributed to tightening and expected tightening in lending standards and terms at some banks beyond what these banks would have reported absent the banking-sector stress,” the report said.

Between work at home, Bidenflation and The Feral Reserve, commercial real estate and regional banks are suffering … and it could get a lot worse. And Joe Biden (aka, Negan) in general. Living in Negan Country!

The work-from-home trend has been taking its toll on office landlords and is now making its way through to banks’ commercial loan portfolios, leading some analysts to predict that more trauma could be on the way for regional banks this year.

And in the current climate of bank failures, short sellers, and nervous depositors, banks with large exposures to commercial real estate (CRE) loans are racing to clean up and sell down their loan portfolios in hopes that they will not fall victim to another round of bank runs.

“There is an estimated $1.5 trillion of commercial property debt that will be due for repayment in about 18 months,” Peter Earle, an economist at the American Institute for Economic Research, told The Epoch Times. “It’s not improbable that even if interest rates have fallen by that time, some of that real estate debt will nevertheless be impaired and have an adverse impact on regional banks.”

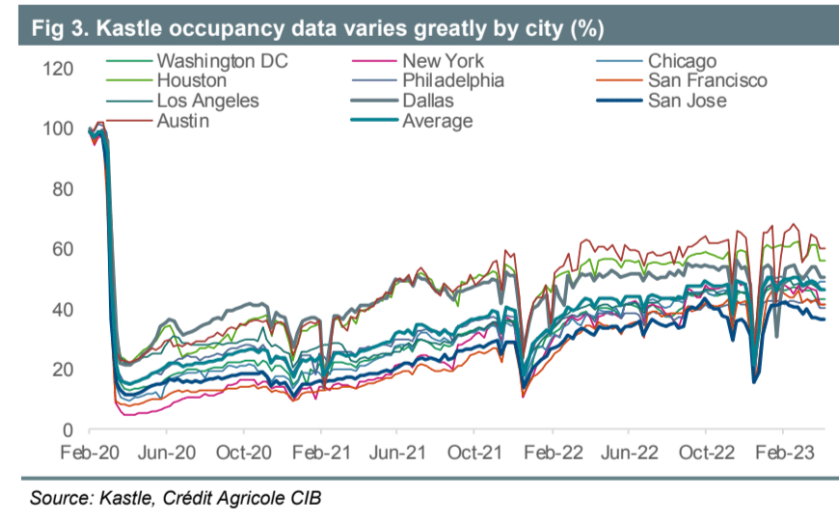

In step with a recent trend in the CRE market, tech giant Google announced in May that it was attempting to sublease 1.4 million square feet of vacant office space in its Silicon Valley home base in order to “match the needs of our hybrid workforce.” Despite more employees returning to their offices this year, average office occupancy rates across the United States are still below 50 percent.

According to a report by Bank of America, 68 percent of CRE loans are held by regional banks. Approximately $450 billion in CRE loans will mature in 2023. JPMorgan Chase estimated that CRE loans comprise, on average 28.7 percent of the assets of small and regional banks, and projected that 21 percent of CRE loans will ultimately default, costing banks about $38 billion in losses.

Double Hit (of Biden’s Policies) Commercial mortgages are getting hit on two fronts: first, by the lack of demand for office space, leading to credit concerns regarding landlords, and second, by interest rate hikes that make it significantly more expensive for borrowers to refinance.

According to a June 12 report by Trepp, a CRE analytics firm, CRE loans that were originated a decade ago, when average mortgage rates were 4.58 percent, are now coming due, and in today’s market, fixed-rate CRE loan rates are averaging around 6.5 percent.

Banks that make CRE loans consider factors like debt service coverage ratios (DSCRs), which measure a property’s income relative to cash payments due on loans. Simulating mortgage interest rates from 5.5 percent to 7.5 percent, Trepp projected that between 28 percent and 44 percent, respectively, of currently outstanding CRE loans would fail to meet the 1.25 DSCR ratio today, and thus be ineligible for refinancing.

These calculations were done assuming current cash flows from properties stay the same and that loans are interest-only, but with vacancies rising, many landlords may have substantially less cash flow available. In addition, whereas interest-only CRE loans were 88 percent of the market in 2021, lenders are now switching to amortizing mortgages to reduce risk, which significantly increases debt service payments.

Refinancing Issues Fitch, a rating agency, projected that approximately one-third of commercial mortgages coming due between April and December of this year will be unable to refinance, given current interest rates and rental income.

“It’s a very different world now from the one in which the majority of these loans were made,” Earle said. “In a zero-interest-rate environment, before the COVID lockdowns saw many businesses shift to a remote work basis, many of these loan portfolios full of office properties looked great. Now, a substantial portion of them look quite vulnerable.”

The Trepp report highlighted several regional markets, such as San Francisco, where office sublease offers jumped 140 percent since 2020, and Los Angeles, where office vacancies hit a historic high of 22 percent. Available office space in Washington D.C. increased to 21.7 percent in the first quarter of 2023.

New York has been hit hard, as well. Office occupancy rates in New York City plummeted from 90 percent to 10 percent in 2020 during the COVID pandemic, but only recovered to 48 percent this year. Revenue from office leases fell by 18.5 percent between December 2019 and December 2022.

Vacancy Rates at 30-Year High Overall, according to a report by analysts at New York University and Columbia Business School, office vacancy rates are at a 30-year high in many American cities.

The report found that “remote work led to large drops in lease revenues, occupancy, lease renewal rates, and market rents in the commercial office sector.”

The authors predict that, even if office occupancy returns to pre-pandemic levels, “we revalue New York City office buildings, taking into account both the cash flow and discount rate implications of these shocks, and find a 44% decline in long run value. For the U.S., we find a $506.3 billion value destruction.”

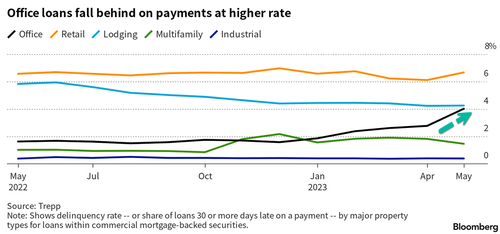

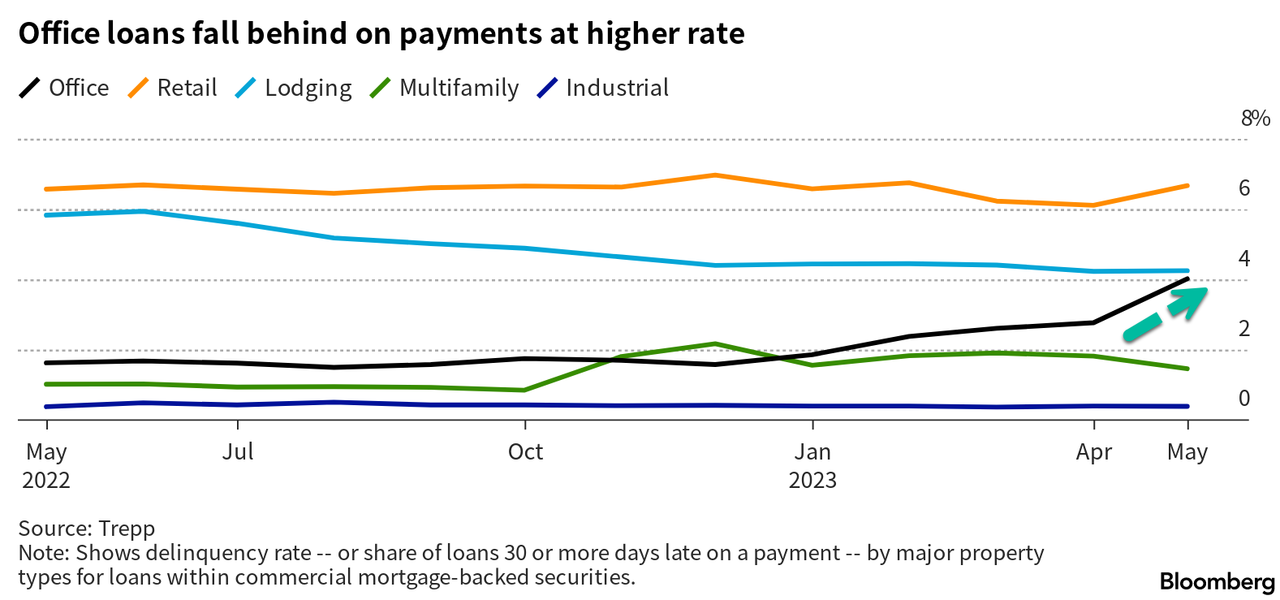

As predicted, delinquencies in commercial mortgage loans are now creeping up. Missed payments in commercial mortgage-backed securities (CMBS) increased half a percent in May over the prior month to 3.62 percent, Trepp reports. The worst component of the CMBS market, which includes multi-unit rental buildings, medical facilities, malls, warehouses, and hotels, was offices, where delinquencies increased 125 basis points to more than 4 percent.

To put this in perspective, however, CMBS delinquencies exceeded 10 percent in 2012 and 2020. And analysts say that lending criteria for CRE have been more conservative than they were before the mortgage crisis of 2008, leaving more cushion on ratios relative to a decade ago.

All the same, the credit crunch at regional banks has created a vicious circle, where banks race to pare down their CRE portfolios, and the dearth of financing leaves more landlords facing default as outstanding loans mature. To make matters worse, commercial property values, which provide collateral for the loans, appear to be taking a hit as well.

In an effort to rapidly clean up their CRE loan portfolios and avoid the fate of failed banks like Silicon Valley Bank, Signature Bank, and First Republic Bank, banks are now attempting to sell off the loans, often taking a loss in the process.

In May, PacWest, a regional bank, sold $2.6 billion of construction loans at a loss. Citizens Bank reportedly has put $1.8 billion of its CRE loans up for sale during the first quarter of this year. Customers Bancorp reduced its CRE lending by $25 million and put $16 million of its existing portfolio up for sale.

Wells Fargo, one of the top four largest U.S. banks, is also downsizing its CRE portfolio, and in announcing the move CEO Charlie Scharf stated, “we will see losses, no question about it.”

“Between the Fed’s 500+ basis point hikes over the past 16 months and the failure of Silicon Valley Bank, and others, earlier this year, a credit tightening is already underway,” Earle said. “That has put a lot of pressure on regional lenders.”

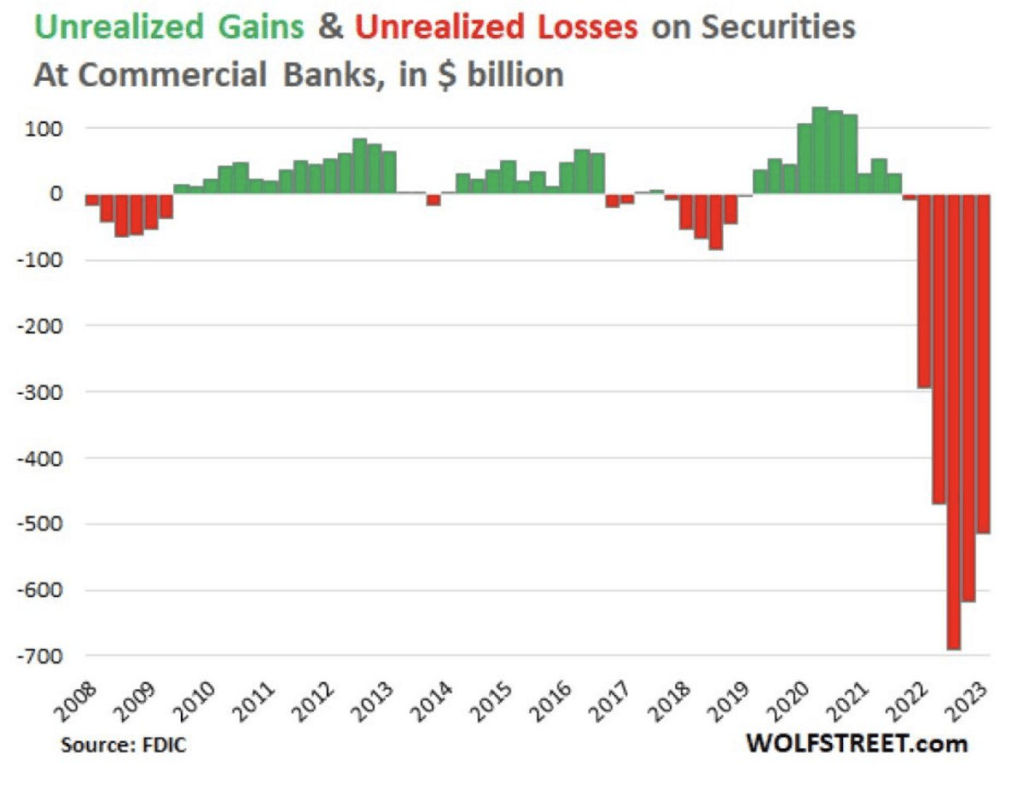

A March academic study titled “Monetary Tightening and U.S. Bank Fragility in 2023” stated that the market value of assets held by U.S. banks is $2.2 trillion lower than what is reported in terms of their book value. This represents an average 10 percent decline in the market value of assets across the U.S. banking industry, and much of this decline came from commercial real estate loans.

Consequently, the authors wrote, “even if only half of uninsured depositors decide to withdraw, almost 190 banks with assets of $300 billion are at a potential risk of impairment, meaning that the mark-to-market value of their remaining assets after these withdrawals will be insufficient to repay all insured deposits.”

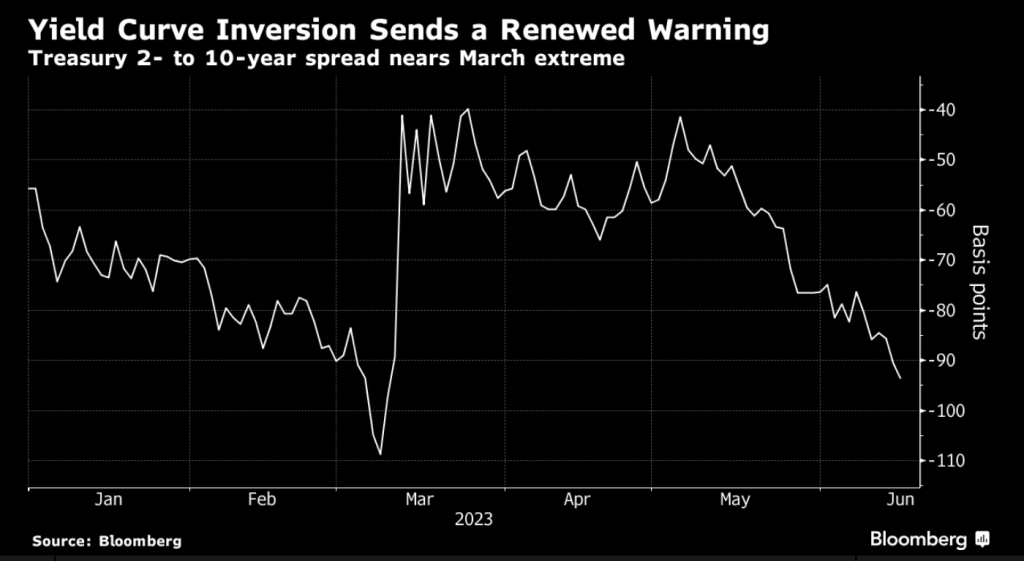

61% of Bloomberg terminal respondents (including me, by the way) see Fed hikes leading to recession.

Bond traders are stepping up wagers that the Federal Reserve will steer the US economy into a recession.

Policy-sensitive front-end Treasuries led a selloff Thursday, while longer-date bonds lagged, a day after Fed officials indicated that they’re prepared to raise interest rates by another half-point this year following the first pause in the central bank’s 15-month hiking campaign. That sent the yield-curve inversion, as measured by the gap between two- and 10-year securities, to 95 basis points — a level last sustained in March — and approaching this cycle’s 109-basis-point extreme.

The price action suggests bond traders are skeptical that policymakers can avoid a so-called hard landing as they continue to press the case for higher borrowing costs in an effort to get a handle on inflation that remains more than double their 2% target.

“The Fed runs the risk of solving one policy error of being too easy for too long with another policy error as they ignore the growing credit contraction and persistent losses from higher rates,” said George Goncalves, head of US macro strategy at MUFG. “The catch-22 is that for them to ease, something now has to break or the economy has to crack.”

It’s not just bond traders who are growing concerned.

Sixty-one percent of respondents in a Bloomberg poll of terminal users conducted in the hours after the Federal Open Market Committee decision said tighter monetary policy will ultimately cause a recession at some point in the next year.

“The Fed was clearly trying to send a hawkish message that they are not quite done yet and don’t think they have made enough progress on inflation,” said Michael Cudzil, portfolio manager at Pacific Investment Management Co. “You see curve flattening and rates not pricing in the full extent of hikes, so the thinking is that these hikes may bite and the Fed is closer to the end.”

Officials left their target range for the federal funds rate unchanged at 5% to 5.25% Wednesday, but projected the key rate will rise to 5.6% by the end of this year, implying two more quarter-point increases, up from 5.1% in March. They also revised higher estimates of core inflation for year-end to 3.9%, from 3.6%, owing to what Chair Jerome Powell called surprisingly persistent price pressures.

Still, markets aren’t convinced borrowing costs will rise as high as central bankers project.

The highest rate on swap contracts for future meetings by early Thursday was around 5.32% for both September and November, with July at 5.27%, compared to a current Fed effective rate of 5.08.

The Fed’s aggressive outlook for rate hikes through year-end may be an effort to dash bond-market expectations for cuts in the months ahead, according to Michael de Pass, global head of linear rates at Citadel Securities.

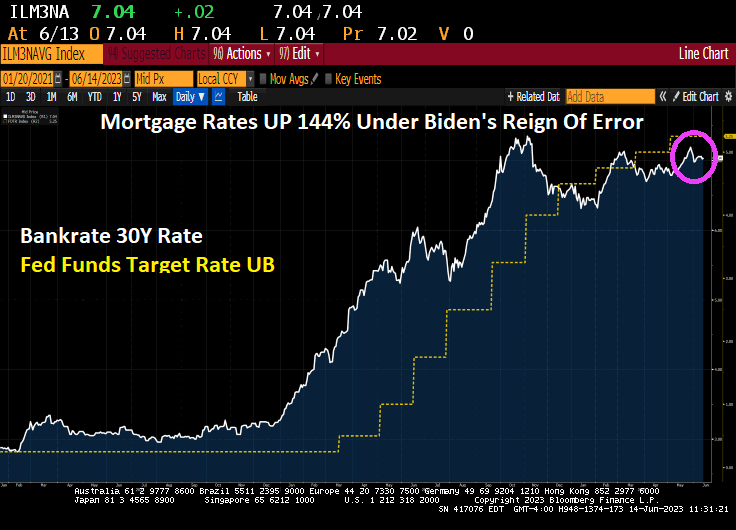

While The Fed paused at their recent FOMC meeting, they are expected to raise their target rate at the July meeting …. then stop. Despite being only a little over 50% of where they should be (10.12%) to cool inflation.

Biden’s “reign of error” is horrific. The inflation caused by Biden’s policies, The Federal Reserve and insane Federal spending has caused mortgage rates to soar 144% since Biden took office.

While The Fed is likely to pause today, but Fed Funds are pricing in a July rate hike.

The Fed will annouce a pause at today’s FOMC meeting, so don’t look for mortgage rates to do much today.

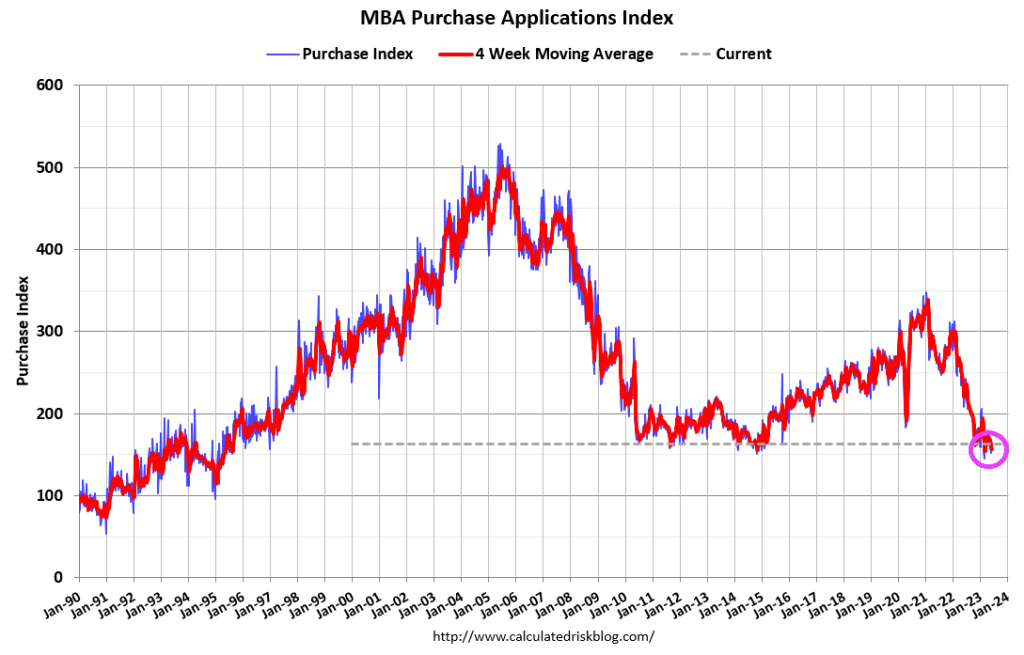

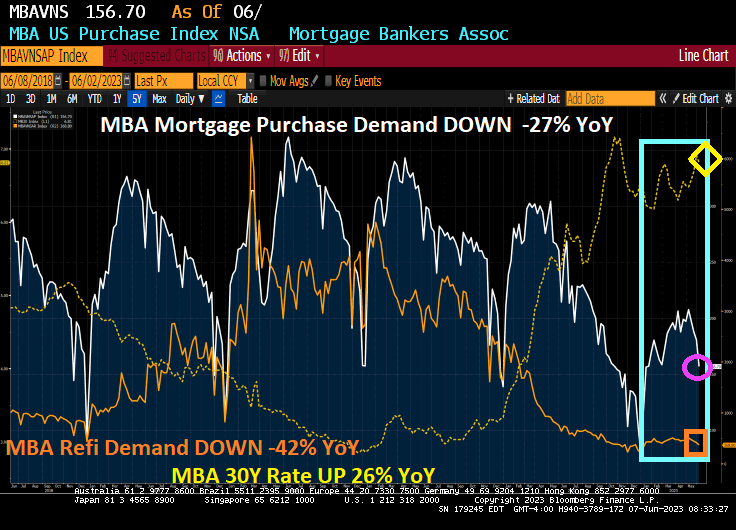

Mortgage applications increased 7.2 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending June 9, 2023.

The Market Composite Index, a measure of mortgage loan application volume, increased 7.2 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index increased 18 percent compared with the previous week. The Refinance Index increased 6 percent from the previous week and was 41 percent lower than the same week one year ago. The seasonally adjusted Purchase Index increased 8 percent from one week earlier. The unadjusted Purchase Index increased 17 percent compared with the previous week and was 27 percent lower than the same week one year ago.

Mortgage rates declined for the second straight week, with the 30-year fixed rate decreasing to 6.77 percent. Mortgage applications were up over the week, but remained well below levels from a year ago.

Joe Biden’s new nickname is “The 5 Million Dollar Bribe Man.” Sort of like Steve Austin.

Okay, Joe Biden was generally regarded as the dumbest member of the US Senate and mean-spirited (I won’t repeat podcaster Joe Rogan’s opinion of Biden). Now we realize how brazenly corrupt Biden is (taking bribes from China and Ukraine to influence American poliicies). Not only is Biden an attrocious human being, but his policies have damaged the US middle class terribly thanks to inflation.

Federal Reserve policymakers are about to take their first break from an interest-rate hiking campaign that started 15 months ago, even as they confront a resilient US economy and persistent inflation.

The Federal Open Market Committee on Wednesday is expected to maintain its benchmark lending rate at the 5%-5.25% range, marking the first skip after 10 consecutive increases going back to March of last year. While officials’ efforts have helped to reduce price pressures in the US economy, inflation remains well above their goal.

Source: Bureau of Labor Statistics, Bloomberg

Investors’ focus will be on the Fed’s quarterly dot plot in its Summary of Economic Projections, which is expected to show the policy benchmark rate at 5.1% at the end of 2023.

By contrast, markets are pricing in the possibility of a quarter-point hike in July followed by a similar-sized cut by December, and some Fed policymakers have emphasized that a pause in the hiking cycle shouldn’t be seen as the final increase.

Fed Chair Jerome Powell, who’ll hold a press conference after the meeting, has suggested he favors a break from hiking to assess the impact both of past moves and of recent banking failures on credit conditions and the economy. His commentary will be scrutinized for hints of the committee.

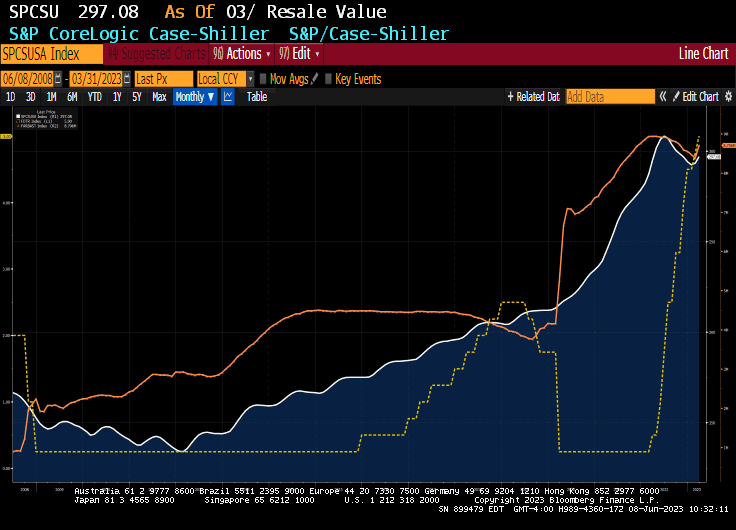

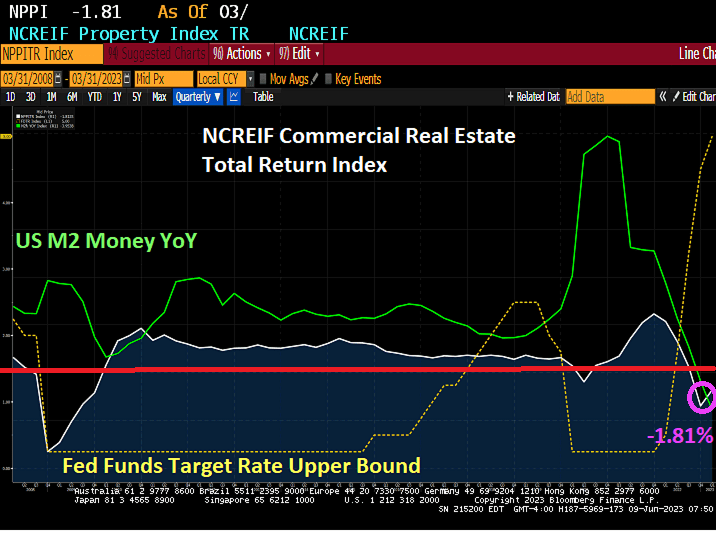

Remember, there is still over $8 TRILLION in Fed assets held sloshing around the economy. The Fed never really removed the excess liquidity and it continues to stoke asset bubbles.

Bear in mind that The Fed is pausing at 5.25% Fed Target Rate, while the Taylor Rule suggests rate hikes to 10.12%. So, Foul Powell is pausing at just over the half way mark.

Of course, Biden’s and Congress’ massive spending spree is causing inflation, and The Fed has no control over Biden/Congress irresponsible spending.

Some structural factors, such as remote work and hybrid work, have doomed the office space segment. This has left empty office buildings scattered across major US cities as the number of landlords falling behind on repayments due to the difficulty of refinancing and high vacancies has hit a five-year high.

According to real estate data firm Trepp, more than 4% of office loans packed into commercial mortgage-backed securities were delinquent in the last 30 days as of May, the highest level since 2018.

Dan McNamara, the founder of Polpo Capital Management, told Bloomberg about impending CRE turmoil:

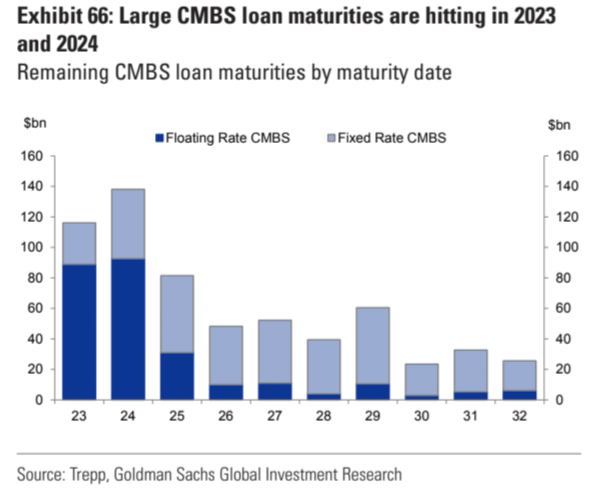

“This is just the tip of the iceberg for office delinquencies as $35 billion in CMBS office loans are scheduled to mature this year and the refinancing market is effectively shut to this asset class.”

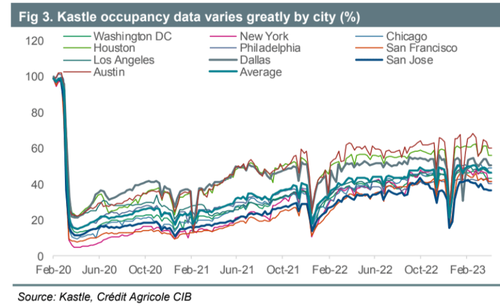

The rise in delinquencies comes as security card swipe data from Kastle shows many workers have yet to return to their desks in major US cities, resulting in high office space vacancies nationwide.

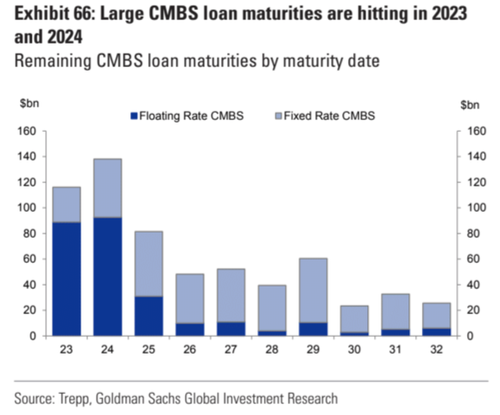

As Goldman pointed out to clients days ago, one major issue is a steep maturity wall of floating and fixed-rate CMBS loans due this year and next. The inability to refinance in these challenging market conditions will likely unleash a tidal wave of defaults in the second half of this year.

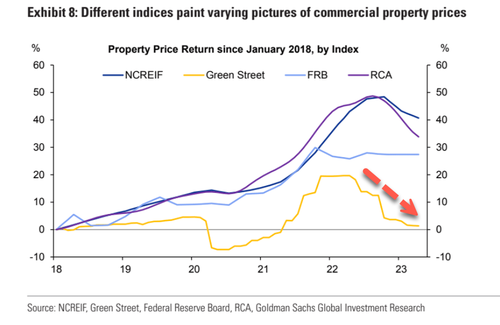

Goldman Sachs chief credit strategist Lotfi Karoui told clients last month, “the most accurate portrayal of current market conditions” is data via the Green Street Commercial Property Price Index, which suggests trouble ahead.

Just how much danger? Karoui believes “Green Street indicates a 25% year-over-year drop in office property values and a 21% drop in apartment property values.”

So the combination of high vacancies, sliding prices, and tightening lending standards is a perfect storm that could ignite an eruption of delinquencies in office loans in the coming quarters.

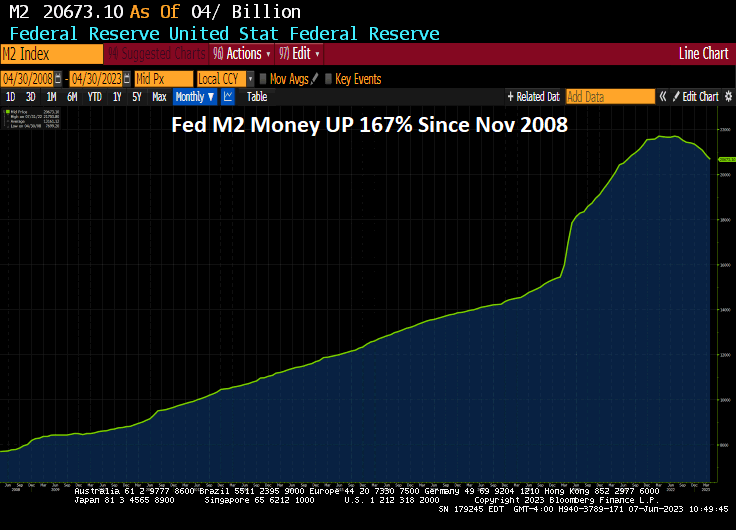

One has to wonder about The Feral Reserve. Since The Great Recession of 2008, The Federal Reserve has printed a staggering amount of money (know as QE). There is still about $8.3 TRILLION in monetary stimulus sloshing around the economy.

And M2 Money printing is up 167% since November 2008.

So, despite the talking heads from The Fed and CNBC, etc blathering about Fed tightening, there remains over $8 TRILLION in monetary stimulus chasing asset prices.

Is The Fed ACTUALLY the US economy? Or is The Fed the financing arm of the Democrat party?

Yes, The Fed looks like they are pausing .. rate hikes.

Welcome to the Bidenville Mortgage Depot! Where Bidenflation (caused by idiotic energy policies, crazy Fed money printing and insane Federal spending) has caused The Fed to raise rates crushing the US mortgage market.

Mortgage applications decreased 1.4 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending June 2, 2023. This week’s results include an adjustment for the Memorial Day holiday.

The Market Composite Index, a measure of mortgage loan application volume, decreased 1.4 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index decreased 12 percent compared with the previous week. The Refinance Index decreased 1 percent from the previous week and was 42 percent lower than the same week one year ago. The seasonally adjusted Purchase Index decreased 2 percent from one week earlier. The unadjusted Purchase Index decreased 13 percent compared with the previous week and was 27 percent lower than the same week one year ago.

The rest of the story.

The East Palestine Ohio train wreck is symbolic of Biden’s economic programs. I don’t think the Vacationer in Chief (40% of time as President has been on vacation) has been there yet.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.