Biden signed the debt ceiling bill craftted by McCarthy (RINO-CA) and Schumer (Communist-NY). Its allows for uncontrolled spending and borrowing for at least 2 years. And as Milton Friedman once said “There is nothing more permanent than a temorary Federal program … or debt limitiations.

With Biden signaling that government has gone wild with no controls on fiscal responsibility (and Elizabeth Warren flailing her arms and screaming for regulations on cryptocurrencies), cryptos today are getting demolished.

China, Japan and the BRICs realize that there are no controls on ANYTHING coming out of Washington DC. Insane spending, an insane Federal Reserve, corrupt DOJ and FBI.

Well, Kevin McCarthy (RINO-CA) and Patrick McHenry (RINO-NC) along with Jim Jordan (RINO-OH) and Marjorie Taylor Greene (RINO-GA) sold out America to Green Joe Biden (the Jolly Green Giant?) and pretty much guaranteed a Biden reelection as President and Democrats winning the House majority at the next election. Way to go McCarthy, McHenry, Jordan an Greene! You sold out America to the Progressive, destructive Left.

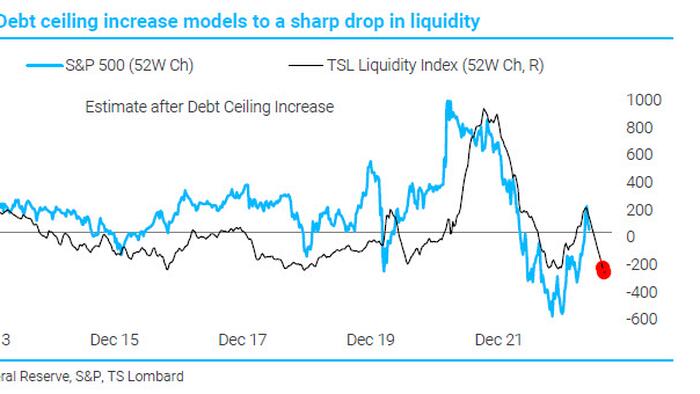

With a debt ceiling deal freshly inked, the US Treasury is about to unleash a tsunami of new bonds to quickly refill its coffers.This will be yet another drain on dwindling liquidity as bank deposits are raided to pay for it — and Wall Street is warning that markets aren’t ready.

The negative impact could easily dwarf the after-effects of previous standoffs over the debt limit. The Federal Reserve’s program of quantitative tightening has already eroded bank reserves, while money managers have been hoarding cash in anticipation of a recession.

JPMorgan Chase & Co. strategist Nikolaos Panigirtzoglou estimates a flood of Treasuries will compound the effect of QT on stocks and bonds, knocking almost 5% off their combined performance this year. Citigroup Inc. macro strategists offer a similar calculus, showing a median drop of 5.4% in the S&P 500 over two months could follow a liquidity drawdown of such magnitude, and a 37 basis-point jolt for high-yield credit spreads.

The sales, set to begin Monday, will rumble through every asset class as they claim an already shrinking supply of money: JPMorgan estimates a broad measure of liquidity will fall $1.1 trillion from about $25 trillion at the start of 2023.

“This is a very big liquidity drain,” says Panigirtzoglou. “We have rarely seen something like that. It’s only in severe crashes like the Lehman crisis where you see something like that contraction.”

It’s a trend that, together with Fed tightening, will push the measure of liquidity down at an annual rate of 6%, in contrast to annualized growth for most of the last decade, JPMorgan estimates.

The US has been relying on extraordinary measures to help fund itself in recent months as leaders bickered in Washington. With default narrowly averted, the Treasury will kick off a borrowing spree that by some Wall Street estimates could top $1 trillion by the end of the third quarter, starting with several Treasury-bill auctions on Monday that total over $170 billion.

What happens as the billions wind their way through the financial system isn’t easy to predict. There are various buyers for short-term Treasury bills: banks, money-market funds and a wide swathe of buyers loosely classified as “non-banks.” These include households, pension funds and corporate treasuries.

Banks have limited appetite for Treasury bills right now; that’s because the yields on offer are unlikely to be able to compete with what they can get on their own reserves.

But even if banks sit out the Treasury auctions, a shift out of deposits and into Treasuries by their clients could wreak havoc. Citigroup modeled historical episodes where bank reserves fell by $500 billion in the span of 12 weeks to approximate what will happen over the following months.

“Any decline in bank reserves is typically a headwind,” says Dirk Willer, Citigroup Global Markets Inc.’s head of global macro strategy.

Bitcoin Faces Downside Risks After Debt Deal Moves Forward

Just when markets appear to be moving past the months-long drama around the US debt ceiling, holders of risky assets such as cryptocurrencies are likely facing a fresh challenge while the Treasury looks to rebuild its depleted cash balance with an estimated $1 trillion Treasury-bill deluge.

“The impending reserve drawdown, due to the [Treasury General Account] rebuild, may prove to be a headwind,” Citi Research strategists including Alex Saunders wrote in a note.

Citi analyzed the performance of risky assets during drawdowns and found that they were vulnerable to higher volatility and weaker returns. As such, the near-term outlook doesn’t seem too rosy for Bitcoin and Ether. “Both coins average negative returns in these scenarios, and BTC has significantly underperformed in the median case,” the strategists wrote Thursday.

The TGA, which keeps money for the Treasury, ballooned during the pandemic. It expanded again last year and is now about as low as it has ever been. Treasury, as a result, will need to replenish its dwindling cash buffer to maintain its ability to pay its obligations through bill sales, estimated at well over $1 trillion by the end of the third quarter. This supply burst may drain liquidity from the banking sector and raise short-term funding rates against an economy many say is likely to fall into recession.

This doesn’t bode well for digital-asset investors, who were just recovering from fears of a no-deal scenario for the US debt ceiling. While Bitcoin edged higher on Friday, it’s still hovering around the $27,000-mark that it has failed to break away from for several weeks.

“Crypto markets were not immune to fears of the US defaulting on its debt, selling off on negative developments and rallying on headlines suggesting progress,” the strategists said. They added that crypto has typically “fared well” amid issues concerning traditional financial institutions, citing the banking turmoil in March, a period in which Bitcoin outperformed. But perhaps risks of an institution such as the US government defaulting “doesn’t paint a favorable outlook for decentralized digital assets.”

To illustrate, the strategists used the Cboe Volatility Index, or VIX, as an indicator of the market’s fear to gauge whether a resolution would be passed before hitting the ceiling. And whenever equity market concerns were eased, that’s when Bitcoin outperformed.

“While in theory the potential default of an institution as impactful as the US government would bode well for decentralized technologies and systems, this may not currently be the case given that the crypto industry is still in its infancy and regulation has yet to be well-defined,” they wrote. “Another theory is that not raising the debt ceiling would lead to reduced US government debt and a lower fiscal deficit, and provide more credibility to fiat, particularly the dollar.”

On Friday, the Senate passed legislation to suspend the US debt ceiling and impose restraints on government spending through the 2024 election. The measure now goes to President Joe Biden, who forged the deal with House Speaker Kevin McCarthy and plans to sign it just days ahead of a looming US default.

Year-to-date, Bitcoin has rebounded some 60% after starting the year at around $16,500. Such optimism comes after 2022’s 64% drop, its second-worst year in its history. It rose about 1% to $27,178 as of 3:32 p.m. in New York, and is marginally higher from last Friday.

Bitcoin’s support hovers around $26,500, said Fiona Cincotta, senior market analyst at City Index, adding that a break below $25,000 could mean a deeper sell-off.

“The problem is the macro backdrop, which is relatively uncertain going forward with recessionary fears,” she said. “I think what will be looking for to make Bitcoin shine is a nice dovish pivot from the Federal Reserve. That might be the tide where we will see another decent leg higher.”

Range-bound trading has been Bitcoin’s defining characteristic of late, with its 30-day volatility reigning low at 1.8%, firmly staying firm within its two-month-long trading range. Despite growing short-term volatility, options implied volatility trended lower over the past week, according to K33’s Bendik Schei and Vetle Lunde. Even so, Bitcoin exchange-traded products continued to see steady outflows while Bitcoin volumes — spot and futures — are trending lower.

McCarthy, McHenry, Jordan and Greene, honorary Frenchmen!

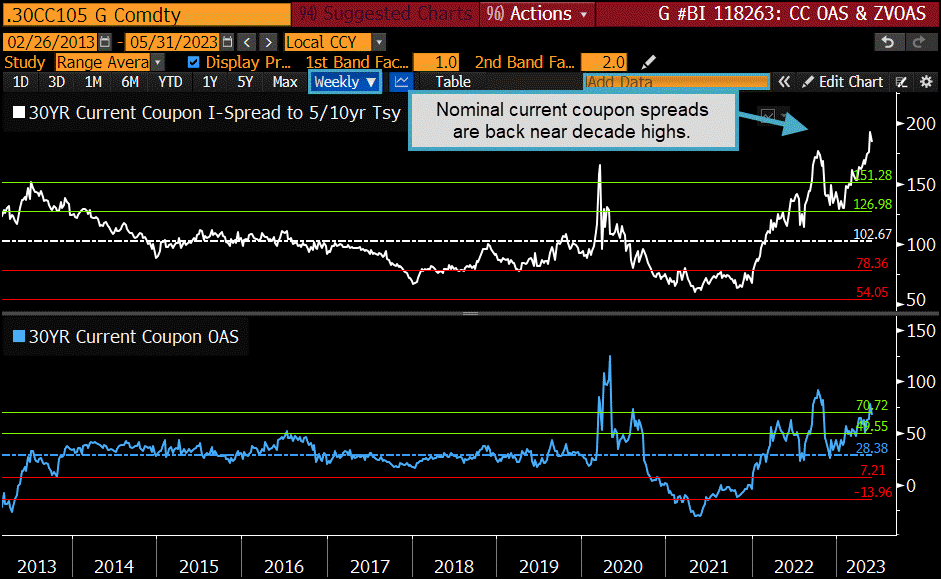

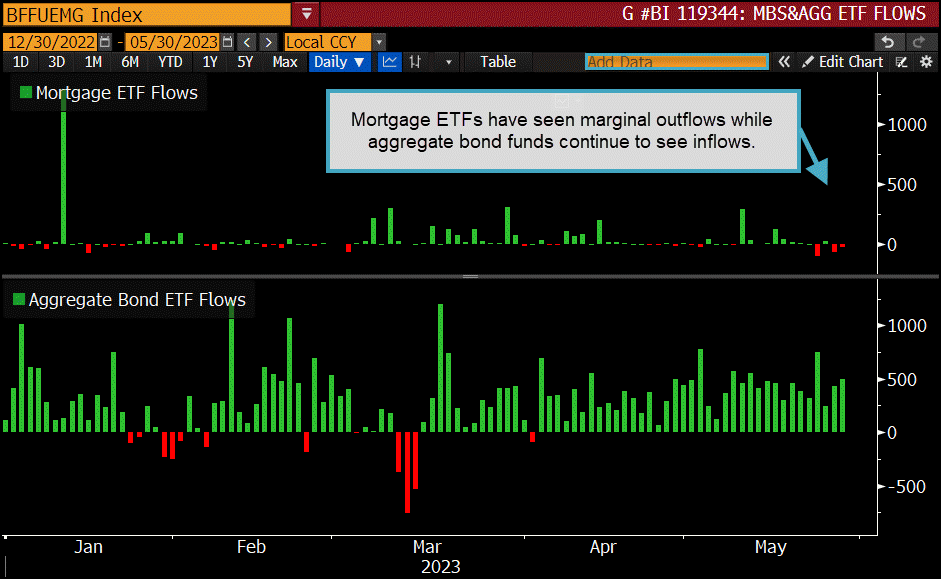

Worsening conditions in the US mortgage-backed securities market are doing little to ease fears over financial contagion as a recession looms.

MBS current-coupon yield spreads over Treasuries are near the highest level since 2008 subprime crisis, as economic and political concerns weigh on performance, Erica Adelberg, a Bloomberg Intelligence strategist, wrote in a BI Chart Book. Mortgage-related exchange traded funds are seeing outflows, even as bond funds as a whole enjoy inflows. Applications for loans are near 25-year lows as the housing market languishes.

Use the GP tool for charting and run BI to search for research, data and chart books.

The top panel shows nominal current-coupon yield spreads are back near decade highs, surpassing those seen in the fourth quarter and reaching peak levels from the pandemic panic in March 2020. The bottom panel shows option-adjusted spreads are also wide, trading near two standard deviations of the average level, though slightly more in line than nominals, Adelberg wrote.

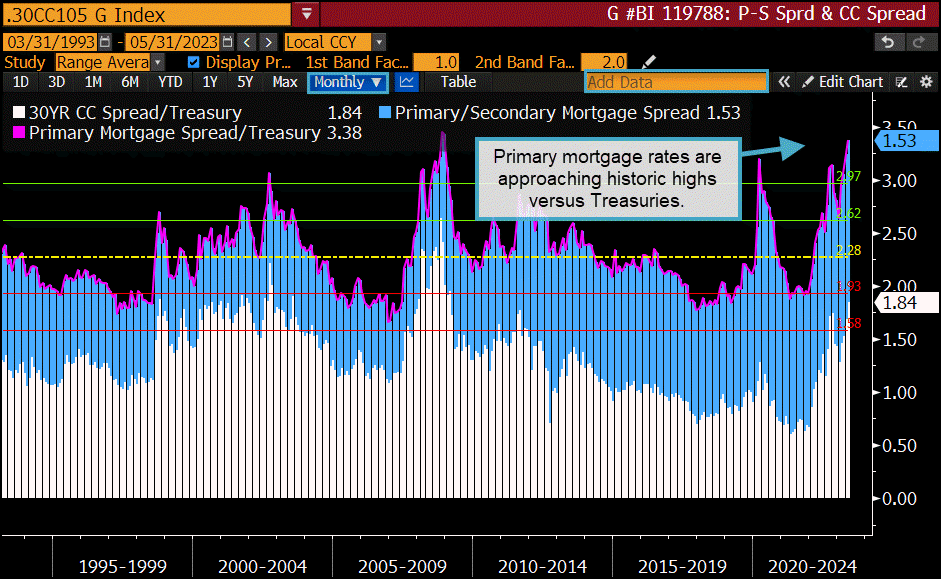

Primary mortgage rates are approaching historic highs versus Treasuries too.

Both the secondary mortgage spread to Treasuries (white) and the primary mortgage spread to secondaries (blue) have blown wider. That has increased the total spread between 30-year-fixed consumer mortgage rates and 10-year Treasuries (pink) to near financial-crisis levels.

Elevated spreads could make it harder for borrowers to find rate relief, even if Treasuries rally and secondary mortgage spreads tighten, Adelberg wrote.

Mortgage ETFs saw marginal outflows while bond funds as a whole continued to see inflows. To monitor ETF flows:

Flows into US aggregate bond ETFs are mostly positive this year, as investor demand has improved on higher yields. Agency MBS-specific ETF flows, however, are more muted, Adelberg wrote.

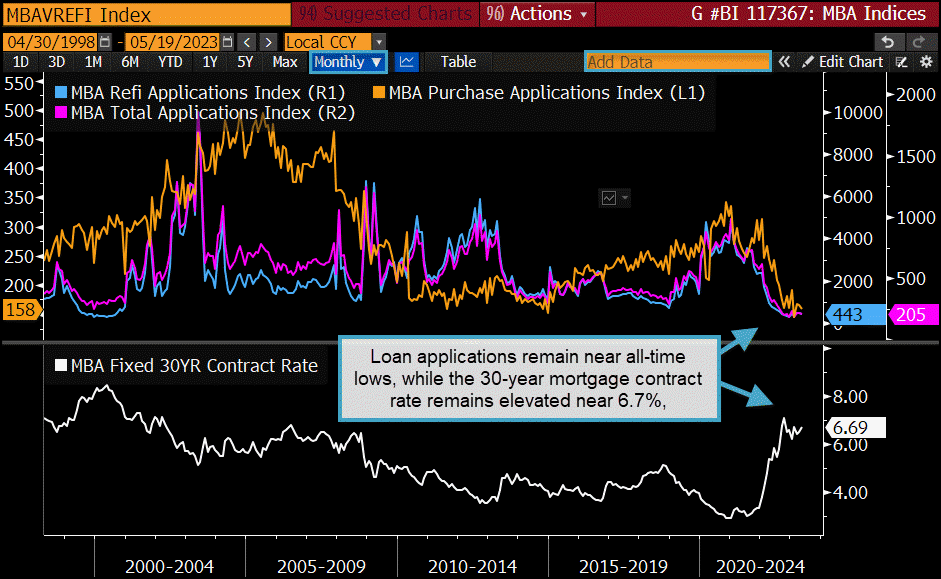

Loan applications remain near all-time lows, showing no signs of life yet.

Loan applications for refinancings and purchases are near 25-year lows as housing-market activity is still depressed, and most refinancings are uneconomical at current rates, Adelberg wrote. The 30-year fixed mortgage contract rate hovers around 6.7%.

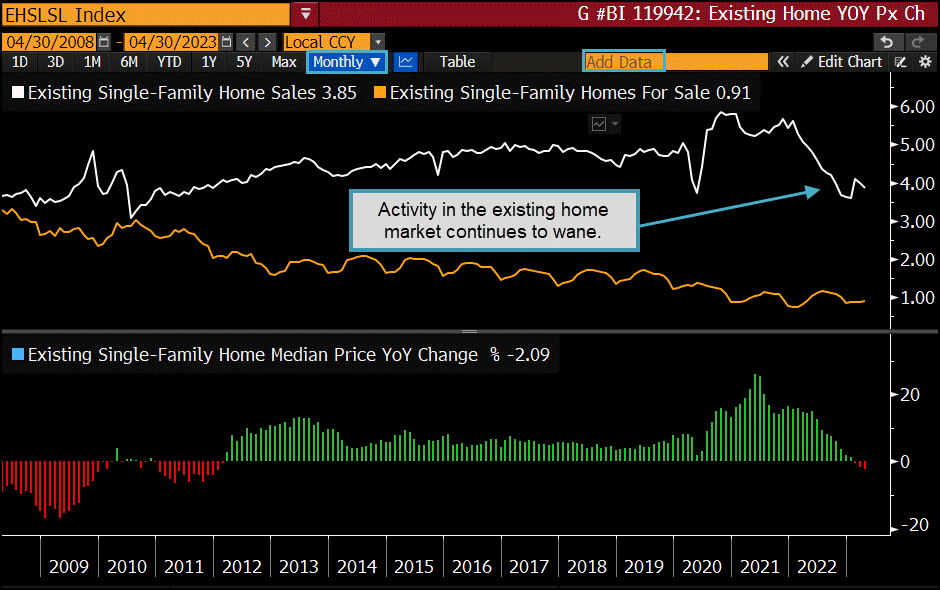

Activity in the existing-home market continues to wane.

Single-family existing-home sales in April fell 3.5% month-over-month and are down more than 20% from a year ago. Existing-home median prices continued to decline as well, seeing their largest year-over-year drop since early 2012, though this may partly reflect the mix of homes purchased. Low existing homes for sale, with many homeowners locked into low-rate mortgages, are depressing resale activity.

MBS spreads may remain under pressure until the economic and inflation outlooks become more optimistic, Adelberg wrote on May 31.

It is not a surprise that the ill-advised COVID economic shutdowns would harm small businesses that large corporations.

Yes, The Fed’s M2 Money printing press went wild with COVID emergency refief. And so did the discrepancy between the top 1% and the bottom 50% in terms of “Share of Total Net Worth Held.” The top 1% is in blue and the bottom 50% is in red. M2 Money is in green.

Compared to pre-COVID, the top 1% increased their share of total net worth from 29.7% to 31.9%, an increase of 7.4% since January 2020. The bottom 50% fell from 30% to 28.5%, a -5% decline. An elitist wonderland!

And The Biden family keeps raking in the money far about Joe’s salary.

And I assume Fed Chair Jerome Powell and Treasury Secretary Janet Yellen also made fortunes from COVID relief.

What happened to Biden? He used to be a “reasonable” Senator (reasonable for a racist Democrat, that is), willing to negotiate with the opposition on budgetary issues and the debt ceiling. Now we have “Progressive Joe” who is acting like crazy Progressive Congresswoman Pramila Jayapal from Seattle. {Aka, Seattle’s Worst!} But his newly found Progressive identiy is leading down a terrible path. Rating agencies are putting the US of credit watch because of Biden’s newly found Progressive back bone. (Progressive means progressing towards full blown Communism).

Ratings company warns on worsening political partisanship

US AAA ratings on review with negative implications at DBRS

The tension around the US debt-limit negotiations ratcheted up after Fitch Ratings warned the nation’s AAA rating was under threat from a political standoff that’s preventing a deal.

Fitch may downgrade its assessment to reflect the increased partisanship that is hindering a resolution despite the fast-approaching so-called X date, it said, referring to the point at which Washington runs out of cash. It moved the US to “rating watch negative” under its classification. Meantime, DBRS Morningstar placed the US ratings of AAA under review “with negative implications.”

Markets have been showing increasing nervousness over the standoff, with Treasury-bill yields slated to mature early next month surging past 7%, while the S&P 500 Index has declined for two days. Economists project a US default could trigger a recession, with widespread job losses and a surge in borrowing costs.

Fitch’s warning “underscores the need for swift bipartisan action by Congress to raise or suspend the debt limit and avoid a manufactured crisis for our economy,” said Lily Adams, a spokesperson from Treasury.

Biden’s childish refusal to reduce his insanely huge budget (crammed with pork for large donors and Progressives) is causing ripples to be felt overseas. Look look at the Japanese Yen.

Pramila Jayapal, Joe Biden’s intellectual soulmate.

Between Biden’s push to tax those borrowers with good credit and reward those with bad credit and Rocket Mortgage annoucing 1% down payments in a declining home price economy, Biden’s housing market is looking more like a house of cards.

Here is another bit of bad news for the housing market.

Mortgage applications decreased 4.6 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending May 19, 2023.

The Market Composite Index, a measure of mortgage loan application volume, decreased 4.6 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index decreased 5 percent compared with the previous week. The Refinance Index decreased 5 percent from the previous week and was 44 percent lower than the same week one year ago. The seasonally adjusted Purchase Index decreased 4 percent from one week earlier. The unadjusted Purchase Index decreased 5 percent compared with the previous week and was 30 percent lower than the same week one year ago.

I have gotten a flood of emails and text messages asking about what happens if Biden defaults on the US debt. In short, Biden has made a career out of spending money, as has Speaker McCarthy. They both have an incentive to raise the debt ceiling, but whether it is cuts to Biden’s insane budget (higher than Covid-era spending) and wants to raise taxes on the middle class to pay for it. McCarthy wants a trimmed budget (aka, back to pre-Covid spending levels) and NOT raises taxes. They will eventually agree somewhere in the middle (US Congress member Pramila Jayapal will be outraged, but then again, she is ALWAYS outraged like Senator Elizabeth Warren) and AOC.

The Federal Reserve has taken a brief respite from fighting inflation that they helped cause. But with $188 TRILLION in unfunded entitlements promised by politicians, The Fed will undoubtedly start buying assets again (aka, QEInfinity) and the debt ceiling will keep being raised. In essence, the DC merry-go-round is broken and politicians will keep pushing it around until it collapses.

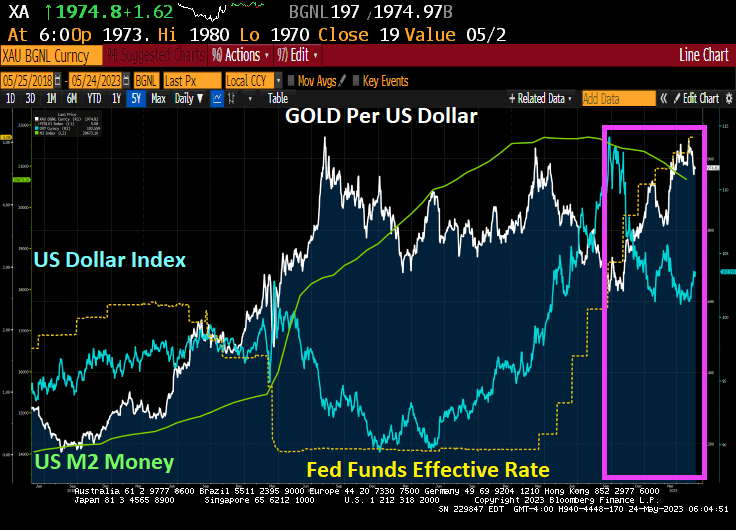

For the moment, The Federal Reserve is reducing M2 Money (green line). With it, the US Dollar (blue line) has declined. Gold (white line fever) is on the rise along with The Fed’s effective funds rate.

WTI crude is up over 1% this AM. And gold is up 2.29%. Heating oil is up 3.56%.

Face it, I have no confidence in Treasury Secretary Janet Yellen, one of the biggest propronents of MMT (modern monetary theory or borrow and spend without consequences). Yellen is NOT making lose my blues.

The US middle class is wasting away in Bidenville. While Climate Envoy John Kerry threatens to seize farms in the name of … climate change? The moral hazard problems associated with farm seizures boggle the mind.

So, everyone keeps talking about the debt ceiling and the fact that America is about to run out of money. How did we just find $375 million dollars AGAIN to ship on over to Zelenskyy?

Biden and McCarthy met on the debt ceiling and nothing has been resolved. They both represent the BIG donor class and big Pharma, big defense, big tech, big media, big tech, anything that is big runs Congress and the Administration. So of course they will finally agree to raise the debt ceiling and continue their insane spending on the donor class.

As of right now, there is no deal to raise the debt limit. Biden wants to raise the already insane and irresponsible Federal budget. McCarthy wants no new taxes. Who will cave in this game of chicken? My guess is that McCarthy will cave. Biden may whip out the 14th Amendment to bypass McCarthy and Congress, but this makes Biden a dictator (which would suit him fine, but would be a horrible precedent).

Core Inflation Rate UP 244% under Biden, Food UP 46%, Gasoline Prices UP 60%, Rental Growth UP 268%. What a disaster under Biden’s Reign of Error.

But at least the Biden family are getting wealthy beyond comprehension. Isn’t that Ashley Biden in the blue?

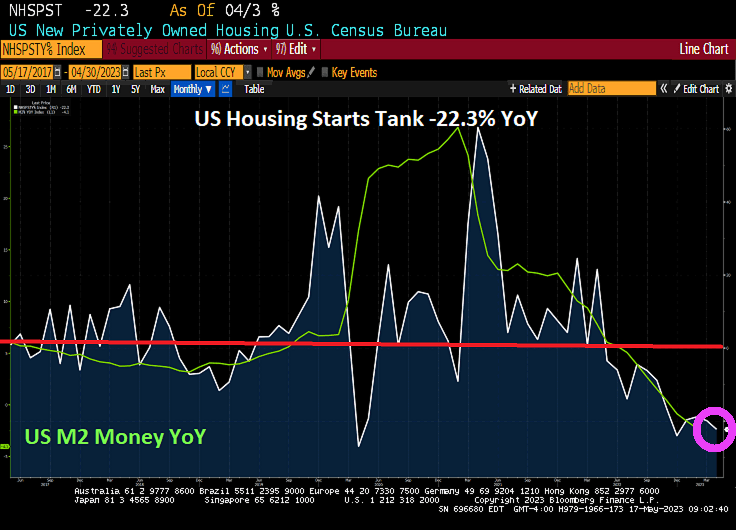

More bad news about the economy and housing sector under Biden/Yellen/Powell’s Reign of Economic Error.

US housing starts are out for April 2023. The bad news? Housing starts tanked -22.3% year-over-year (YoY).

The good news? US housing starts were up 2.19% from March to April. 1-unit detached starts were up 1.56% MoM while 5+ unit starts up 5.24% MoM. Permits for multifamily were down -9.71% from March to April.

The media will no doubt try to ignore the horrifying Durham Report. The report showed that Hillary Clinton and the Obama administration knowingly smeared Presidential candidate Donald Trump with false Russian misinformation and knowingly tried to steal an election. I wonder if Attorney General Merrick Garland will open an investigation into Hillary Clinton’s involvement in election tampering? Oh wait, the IRS was told to stop investigating Hunter Biden’s nefarious dealings. Never mind.

Face it, nothing has been the same since 1) the Covid economic shutdowns, 2) the massive spending spree by Congress, the massive expansion of monetary stimulus by The Federal Reserve and 3) the election of Unaffordable Joe Biden,

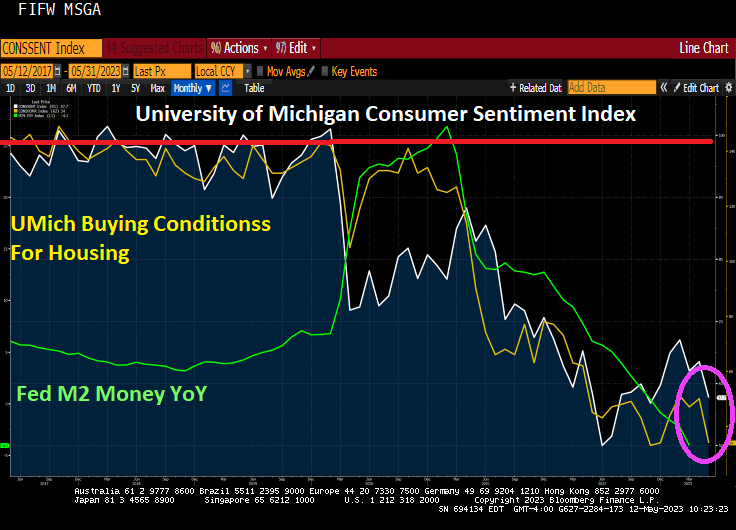

The latest University of Michigan consumer survey is out and it is ugly, reflecting Biden’s ugly approval ratings. A sentiment value of 100 is a good baseline and US consumers were about at 100. Then Covid struck and the ensuing economic and school shutdowns (thank a lot Randi Weingarten, President of the American Federation of Teachers). Then we have the selection of Joe Biden as President, the WORST President in history.

Housing sentiment? It is now near the lowest level since 1982.

Here is Parks and Recreation’s Leslie Knope, one of the only political non-donor class that still likes unaffordable Joe. But big Democrat donors LOVE Biden doling out billions to them!

You must be logged in to post a comment.