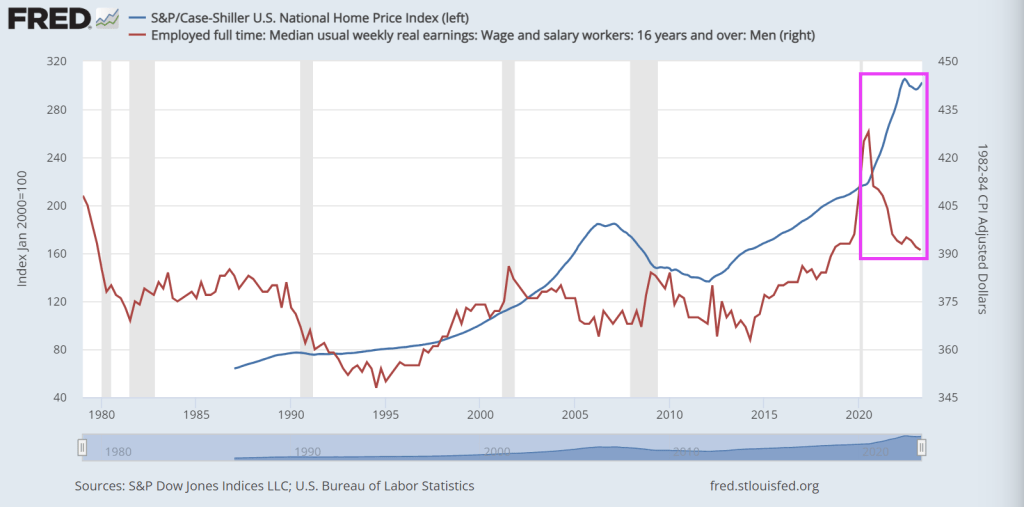

If we look at the Case-Shiller National home price index against real weekly wage growth, you can see the problem clearly. Since Covid and The Fed’s overreaction by providing staggering monetary stimulus, home prices shot up while real median weekly earnings collapsed.

Buying a house requires a much bigger slice of people’s income now — making this the most unaffordable housing market since 1984, by one measure.

And that crushing lack of affordability isn’t expected to improve much in the near future.

At today’s rates, buying a median-priced home would require a monthly principal and interest payment of $2,440 for those making a 20% down payment, according to Black Knight, a mortgage technology and data provider.

That’s $1,172 a month more in mortgage payments from just two years ago, before the Federal Reserve raised its benchmark lending rate 11 times in 18 months, Black Knight found. It’s a 92% increase — and is taking a growing chunk out of household budgets already facing inflation on many fronts.

Currently, 38.6% of the median household income is required to make the monthly payment on the average home purchase, making housing the least affordable it’s been since 1984, according to Black Knight.

“To put today’s affordability levels in perspective, it would take some combination of up to a 28% decline in home prices, a more than 4% reduction in 30-year mortgage rates, or up to a 60% growth in median household incomes to bring home affordability back to its 25-year average,” said Andy Walden, vice president of enterprise research and strategy at Black Knight.

Must as well face it, we’re addicted to gov. Or at least Fed monetary stimulus.

Just look at Personal Interest payments under Bidenomics.

Joe Biden will always be remembered for lying about never raising taxes on households making under $400,000. Inflation is a permanent tax, mostly on those making under $400,000 per year. And household essentials are up substantially under Biden: gasoline prices are up 72%, rent CPI of Primary Residence is up 16%, and food at home CPI is up 20%! That is a HUGE tax on the middle class.

When CPI falls this does not mean that prices on goods and services are going down, it only indicates that prices are rising slower than they were the month or the year before.

Another misconception about CPI is that it measures the inflation rate accurately for regular consumers on common purchases. In reality, the CPI represents mean average price rate increase for a vast basket of goods; over 94,000 items and services with over 200 separate categories. Most of these items and services you will never use or rarely purchase in the span of a year. In other words, inflation declines in uncommon goods can dilute the numbers, making it seem like inflation is dropping while prices on daily necessities continue to spike.

The CPI is weighted according to consumer spending patterns, which is where the calculations can be “adjusted” to a certain extent in an arbitrary manner. Then there is outright government manipulation through various means. As we witnessed recently with the Biden Administration’s claims that “Bidenomics” has defeated the inflation threat, what these reports don’t mention is that Biden has been dumping US strategic oil reserves on the market for the past year. And since energy prices effect the inflation of so many other categories, Biden has artificially manipulated the CPI down using one key resource.

Now that his ability to dump oil reserves has ended, CPI will rise once again along with energy prices.

The point is, it’s impossible to get a sense of the real damage from inflation without looking at the cumulative inflation in necessities (the goods and services that people are required to purchase on a regular basis to live day to day). If we throw out the CPI distraction and look at common necessities since 2020, the economic picture is far more bleak.

Overall food prices have soared by 25%-30% in only three years (again, this means that you are now paying 30% more this year for food than you were paying at the beginning of 2020). Chicken is up from $3 per pound to $4 per pound. Beef is up from $3.50 to $6 per pound. Corn is up from $3.50 per pound to $4.70 per pound. Wheat is up from $5 per pound to $7 per pound. In 2019 the average American household was spending $8100 on food annually; with a 30% increase, in 2023 Americans will be spending at least $10,500 per household.

By the end of 2019, the average rental price of a single family home was around $1450 per month. This year the price is around $2000 per month. At the beginning of 2020, the median cost of a home was $320,000; by 2023 the price skyrocketed to an average of $416,000.

For gasoline, the price in early 2020 was around $2.50 per gallon. The price has fluctuated dramatically due to Biden’s manipulation of the market using strategic reserves, but still remains high today at $3.80 per gallon.

The cost of electricity has risen swiftly, holding steady around .13 cents per kilowatt hour for a decade, then spiking to at least .17 cents per kilowatt hour by 2023.

Remember, most of these costs are static and are difficult to reduce through household spending cuts. These are not items that are easily removed from a monthly budget and the expenditures add up to considerable pressure on consumer accounts. This is probably why around 74% of the public in polls say that the economy is getting worse, not better. It’s because government statistics are not highlighting the true inflationary crisis.

When we look at the cumulative climb of prices in necessities since before the inflation crisis officially began, the truth is that Americans now have to increase their wages by at least 25%-30% on average to maintain the same standard of living they had three years ago. This is a disaster not seen since the stagflationary event of the 1970s and early 1980s. If you have a strange feeling like your bank account is being rapidly drained in recent months, that’s because it is.

And the 30-year mortgage rate is up 163% under Middle Class Joe.

Preliminary benchmark revision smaller than some had projected

Biggest payrolls adjustment in transportation and warehousing

Are you surprised that the Biden Administration has been lying about job creation?? Not really since Biden compulsively lies about everything. Including his corruption.

US job growth was probably less robust in the year through March than previously reported, according to government data released Wednesday.

The number of workers on payrolls will likely be revised down by 306,000 for March of this year, according to the Bureau of Labor Statistics’ preliminary benchmark revision.

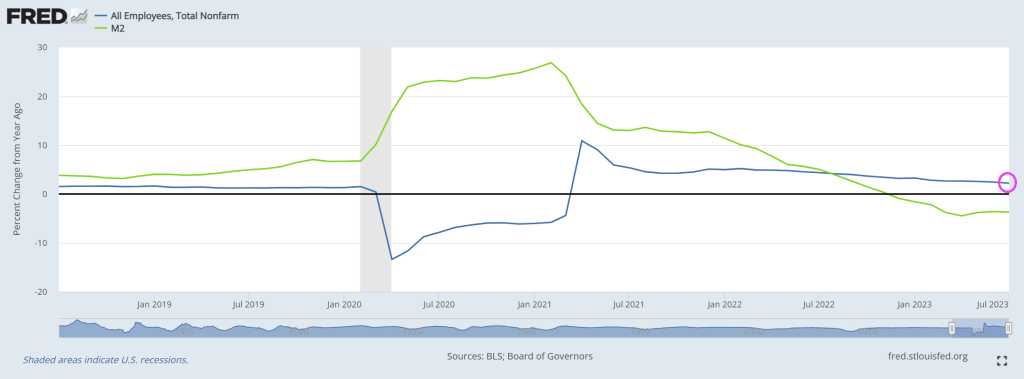

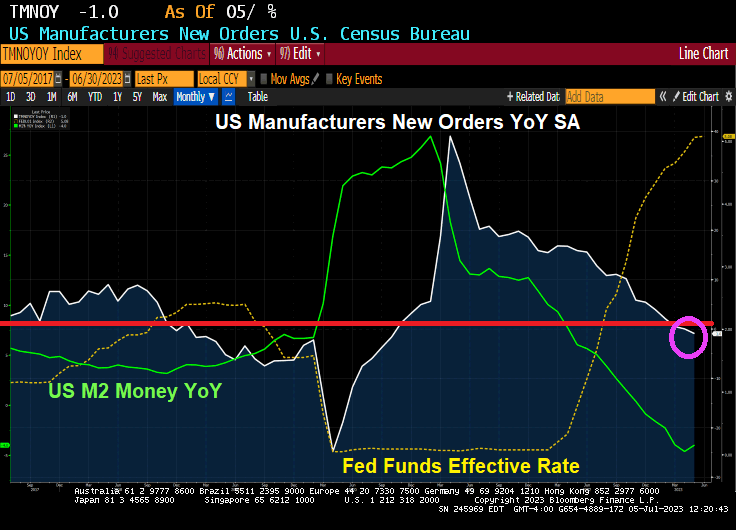

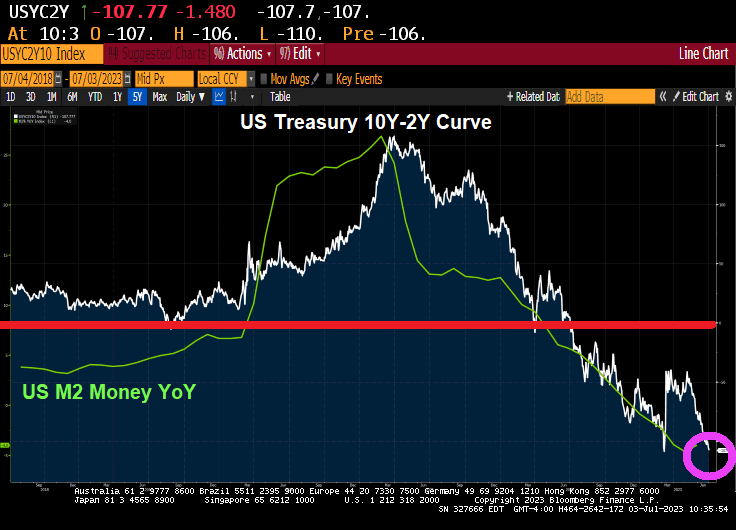

Even without the revision, job growth has slowed to 2.2% YoY in July as M2 Money growth slowed to -3.7% YoY.

Let see what our Overlords say at the Jackson Hole Fed symposium.

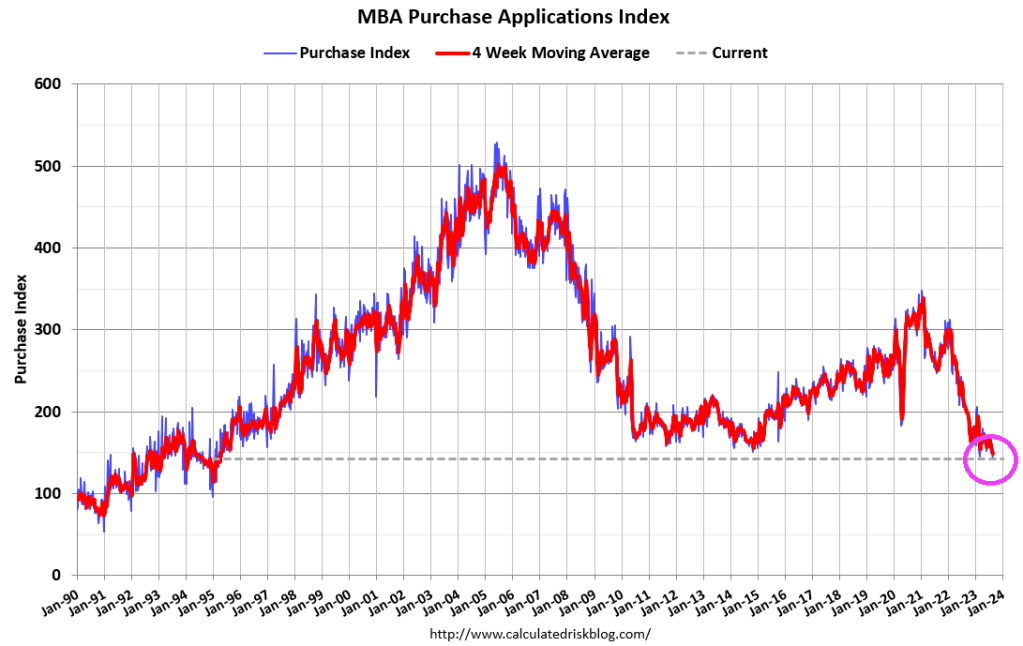

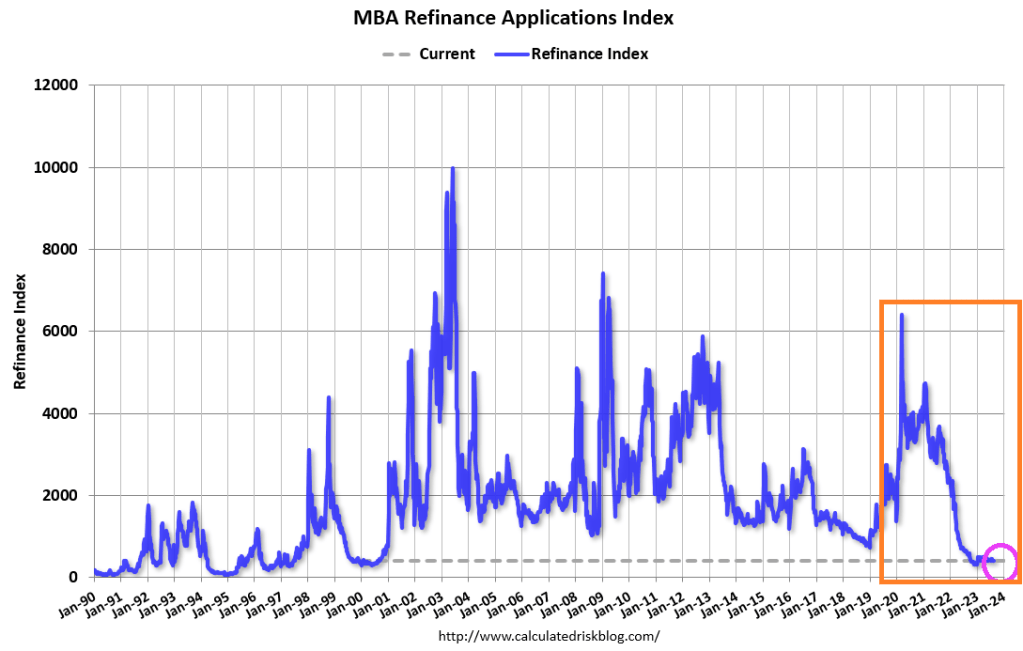

Mortgage demand (applications) decreased 4.2 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending August 18, 2023.

The Market Composite Index, a measure of mortgage loan application volume, decreased 4.2 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index decreased 6 percent compared with the previous week. The Refinance Index decreased 3 percent from the previous week and was 35 percent lower than the same week one year ago. The seasonally adjusted Purchase Index decreased 5 percent from one week earlier. The unadjusted Purchase Index decreased 7 percent compared with the previous week and was 30 percent lower than the same week one year ago.

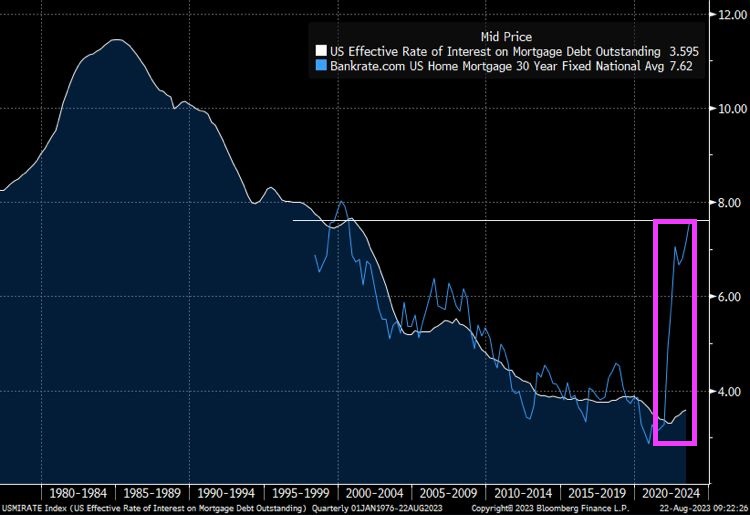

The spread betweenn Bankrate’s 30 year rate at 7.62% and the effective rate on mortgage debt outstanding at 3.595% has exploded as mortgage rates jump.

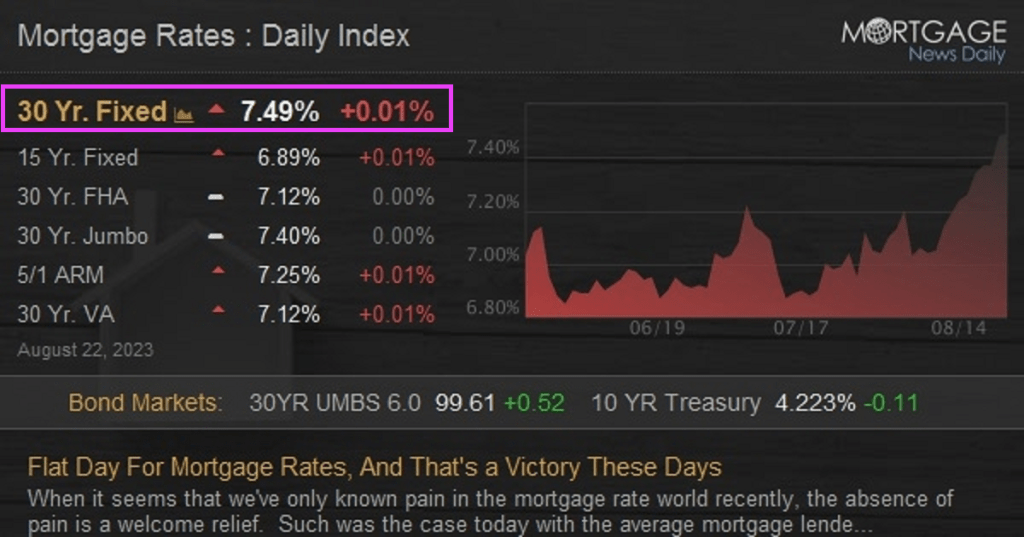

Today’s mortgage rates are up to 7.49%. OMG!

Bidenomics (code for making large donors wealthier and the middle class getting the boot) and catch-up for Yellenomics (rates too low for too long), and Powell are helping to burn down the housing market.

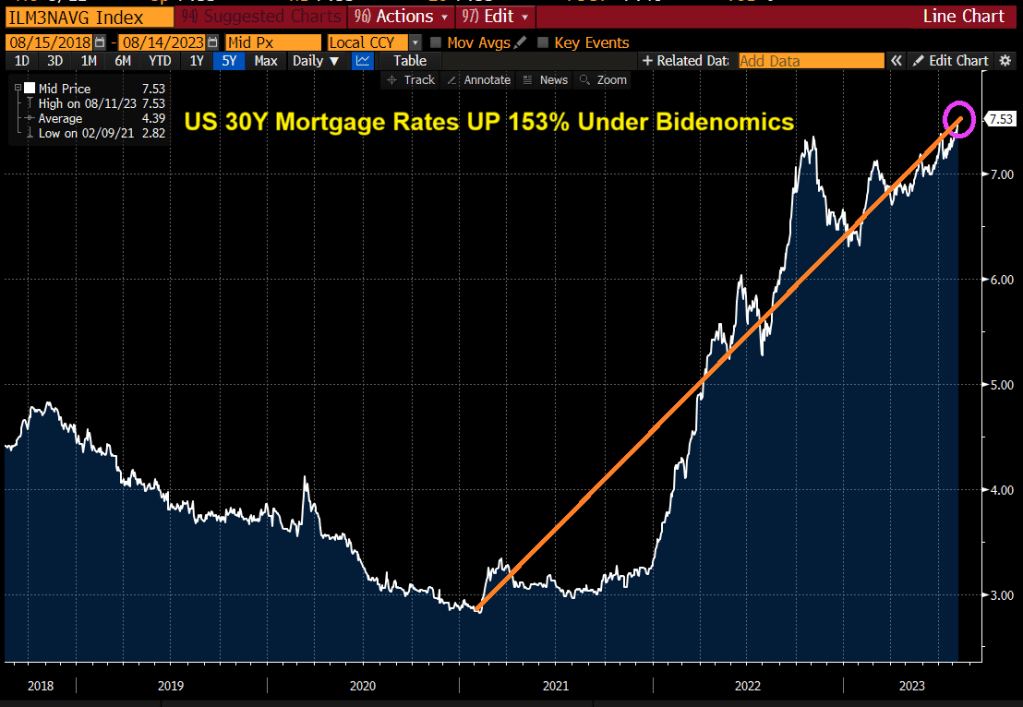

Rates on 30-year mortgages in the US are now the highest since 2000, at 7.53%. Mortgage rates are now up 153% under Bidenomics. Rates have gone from sub 3% to above 7.50% under Inflation Joe.

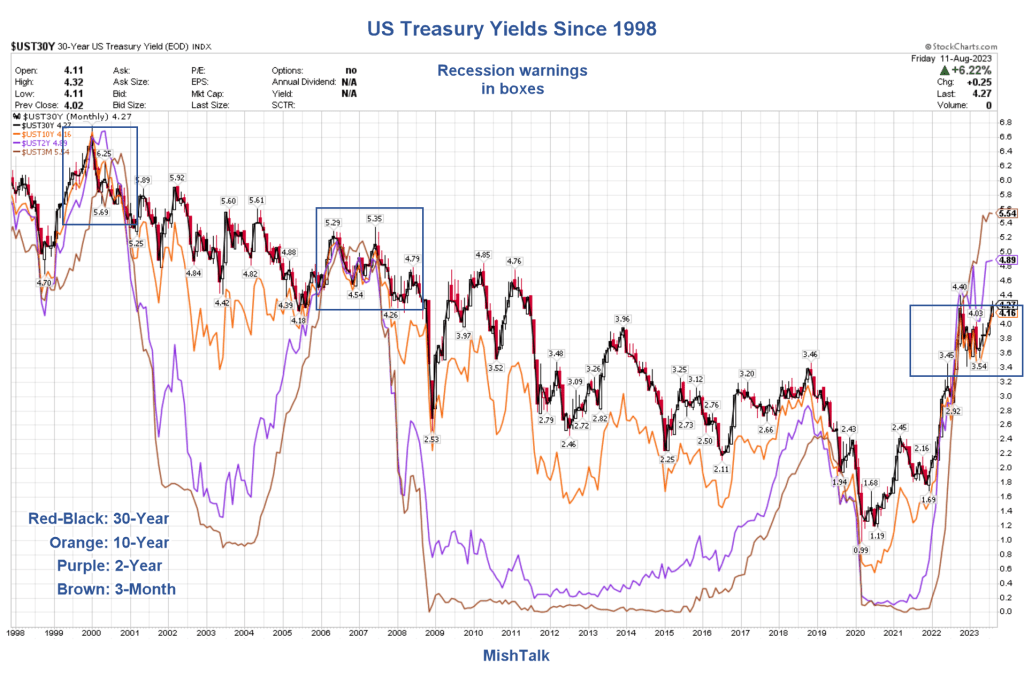

US Treasury yields are playing catch-up from Yellen’s “Too low for too long” monetary policies.

Yes, in part we are playing catch-up from Yellen’s Reign of Error as Fed Chair (keeping rates too low for too long). Only in Washington DC, does gross incompetance warrant a promtion to US Treasury Secretary. Career half-wit Mean Joe Biden is El Presidente and acting like a third world dictator.

“Bidenomics is indeed working!” claims Karine Jean-Pierre. “Cost is going down … wages going up, that is Bidenomics.”

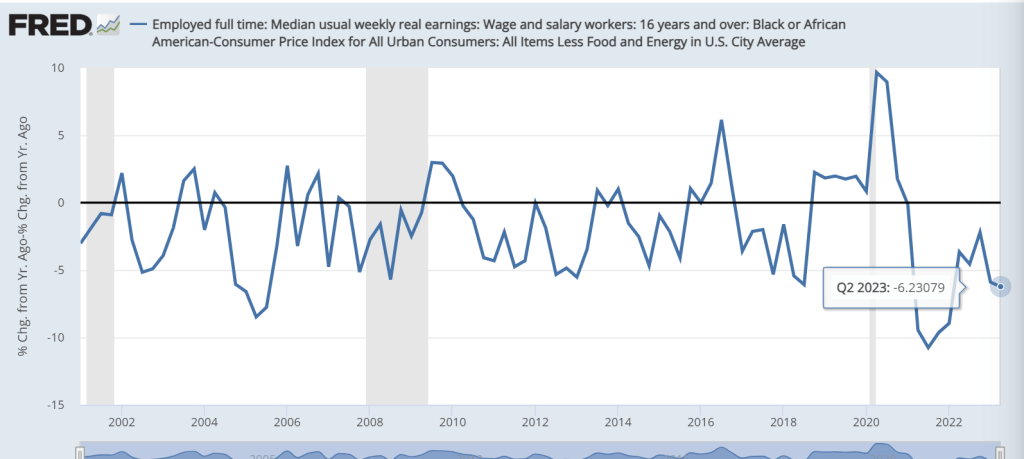

Excuse me Karine. REAL weekly earnings growth remains negative as inflation outpaces weekly earnings growth. As of Q2 2023, REAL median weekly earnings growth is a dismal -3.57% YoY.

And if you are black, Bidenomics has failed you even worse! Q2 Real weekly earnings growth for black households was -6.23% YoY.

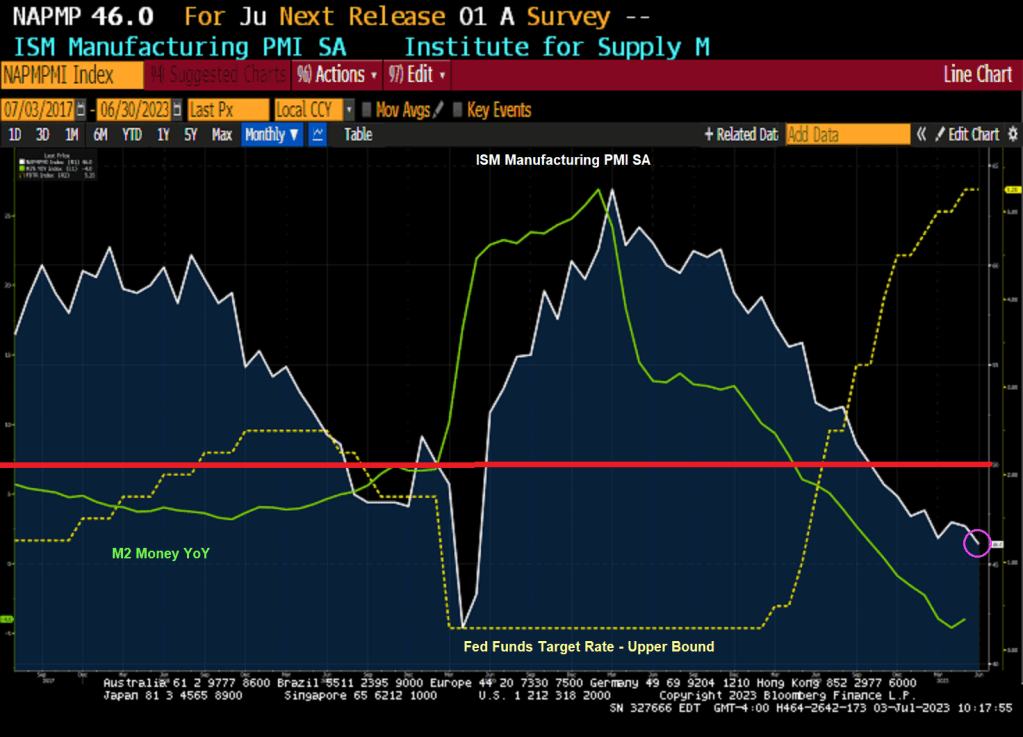

As Powell and The Gang raise interest rates, the more the economy is … slip slidin’ away. US Manufacturers New Orders YoY in May declined -1.0% for the first time since Covid.

Its the 4th of July, American Independence Day from England, but under Biden and The Federal Reserve, Americans are DEPENDENT on debt and Federal spending. In other words, Americans are addicted to gov.

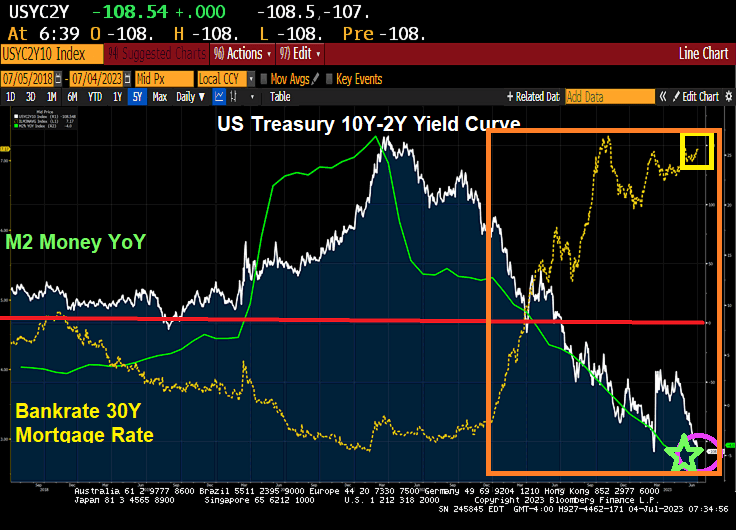

First, Bankrate’s 30-year mortgage rate index is up 150% under Biden. You can see the rapid rise in mortgage rates started with Biden (orange box). Meanwhile, the US Treasury yield curve (10Y-2Y) is the most inverted (negative slope) since 1981. Way to go, Joe!!

On the metals side, gold and silver are up slightly. (Go silver go!!)

On the crypto side, Polkadot is up 1.26% while Bitcoin is down -0.18%.

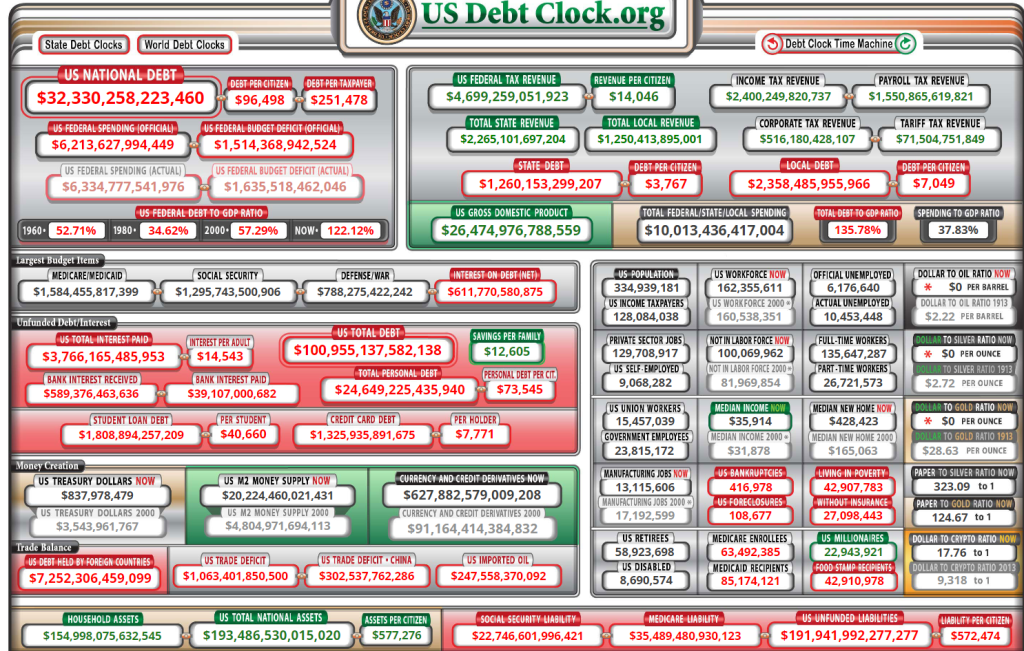

Memo To Fed: keep on printing! Why? US debt is currently $32.33 TRILLION with $192 TRILLION in unfunded Federal liabilties. That is 5 times the current level of debt!!

I was hoping that the week of July 4th would start off with fireworks, but we got bad news about the economy.

US factory activity contracted for an eighth month in June, slipping to the weakest level in more than three years as production, employment and input prices retreated.

The Institute for Supply Management’s manufacturing gauge fell to 46, the weakest since May 2020, from 46.9 a month earlier, according to data released Monday. The current stretch of readings below 50, which indicates shrinking activity, is the longest since 2008-2009.

The decline in the ISM production gauge, which also stands at the lowest level since May 2020, suggests demand for merchandise remains weak. The index of new orders contracted for the 10th straight month and order backlogs shrank, which may help explain a pullback in a measure of manufacturing employment.

The ISM gauge retreated to a three-month low and, at 48.1, indicates fewer producers adding to payrolls.

Many Americans continue to limit their spending on merchandise as they rotate to services and experiences. Others are simply tightening their belts as still-high inflation takes a toll on their incomes.

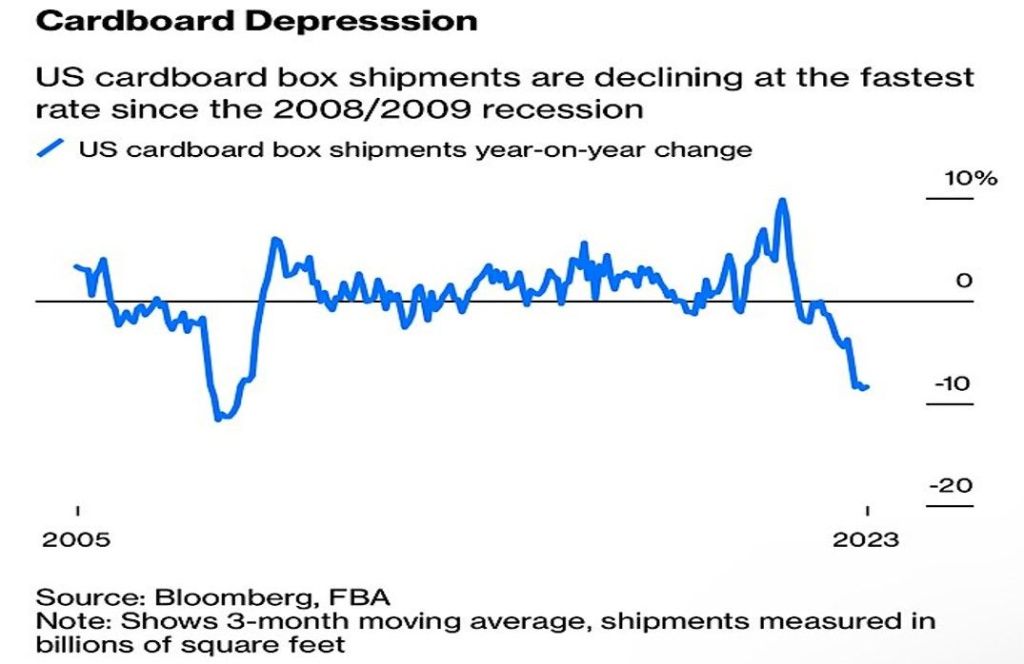

And then we have cardboard box shipments declining at fastest rate since 2008/2009.

At least Ethereum is up over 2% this morning.

And the US Treasury 10Y-2Y keeps on diving deeper into inversion.

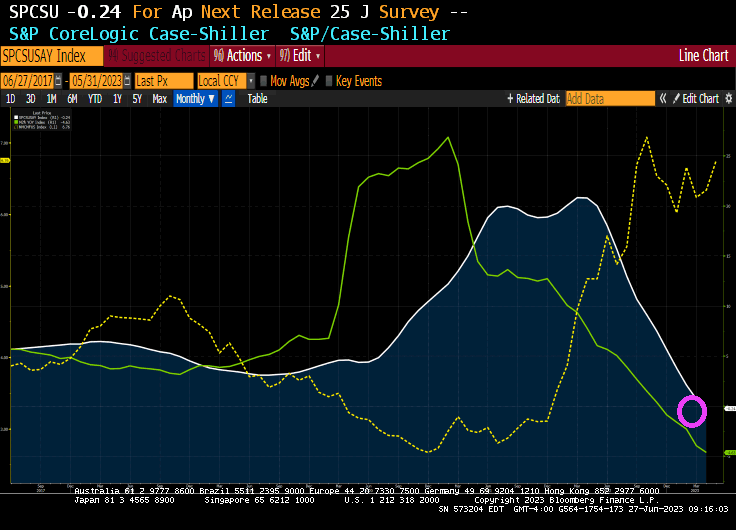

The S&P CoreLogic Case-Shiller U.S. National Home Price NSA Index, covering all nine U.S. census divisions, reported a -0.2% annual decrease in April, down from a gain of 0.7% in the previous month. The 10-City Composite showed a decrease of -1.2%, down from the -0.7% decrease in the previous month. The 20-City Composite posted a -1.7% year-over-year loss, down from -1.1% in the previous month.

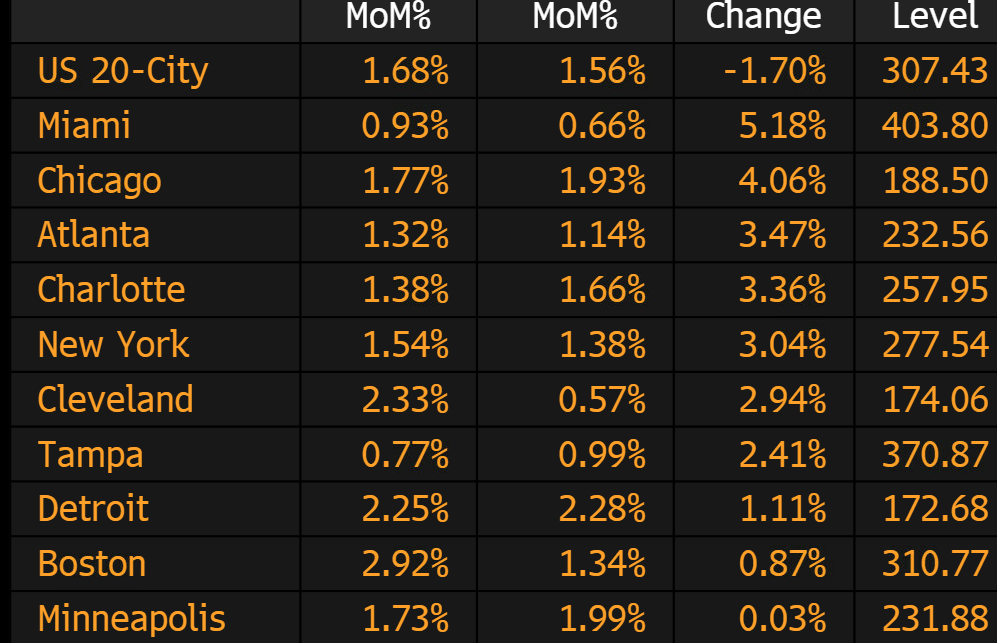

The winners in April? Miami and … Chicago?

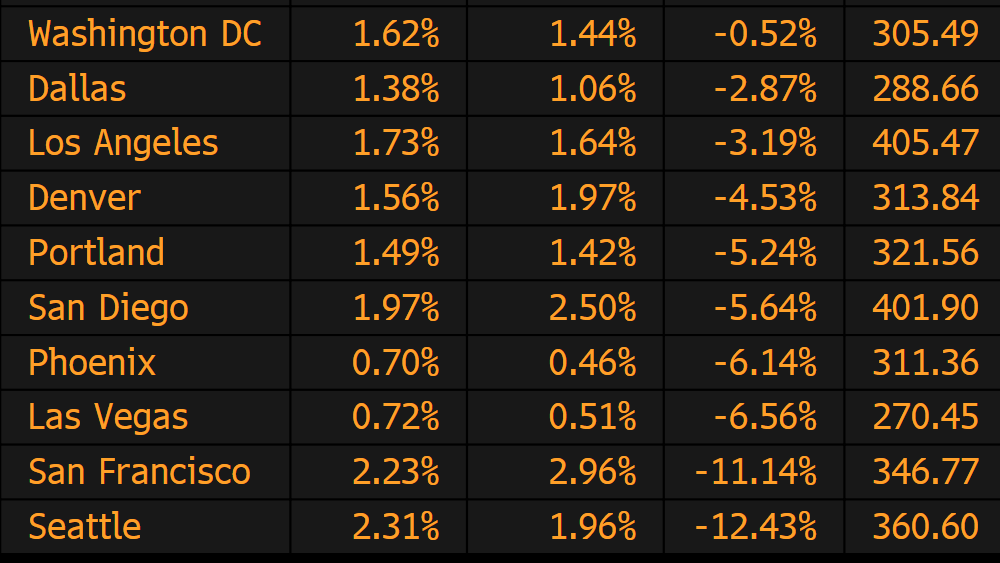

The biggest losers in April? Seattle and San Francisco both suffered YoY losses over -11%.

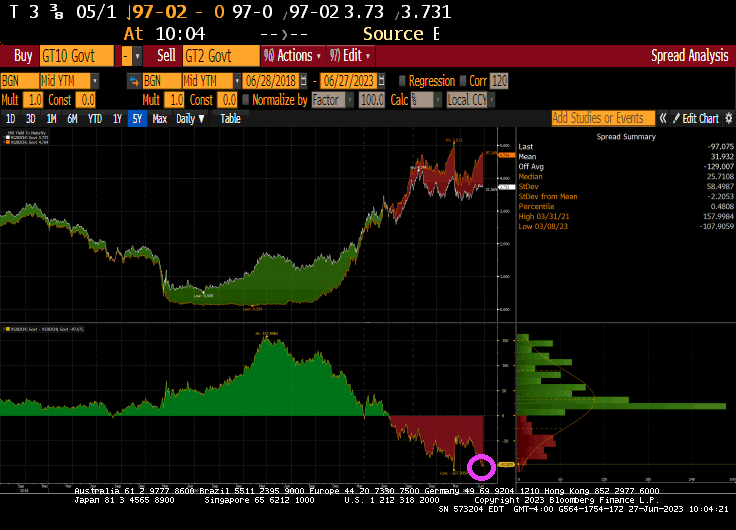

The US Treasury 10Y-2Y yield curve remains steeply inverted at -97 basis points.

You must be logged in to post a comment.