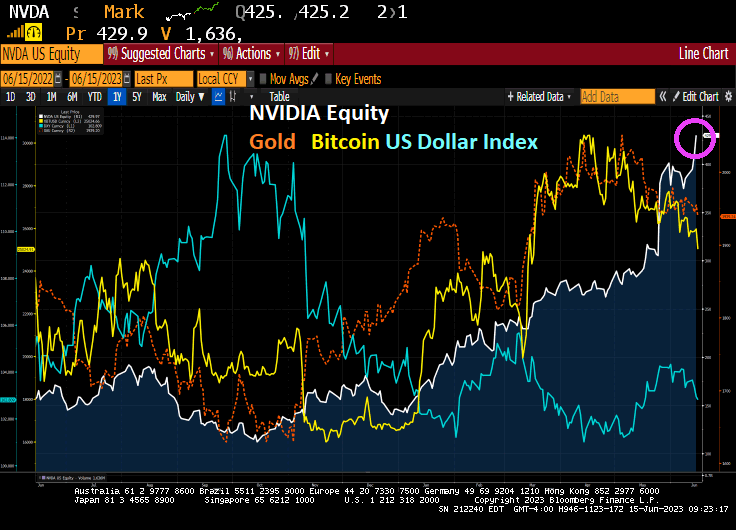

The Artificial intelligence (AI) boom is resulting in Nvidia’s stock soaring to 429.9. At the same time, Bitcoin (yellow), the US Dollar (blue) and Gold (gold) are declining.

Of course, markets are dynamic and gold/silver are likely to start up again along with bitcoin and other cryptos..

The leading crypto today? Dogecoin!

AI versus no intelligence. I give you Resident Joe Negan.

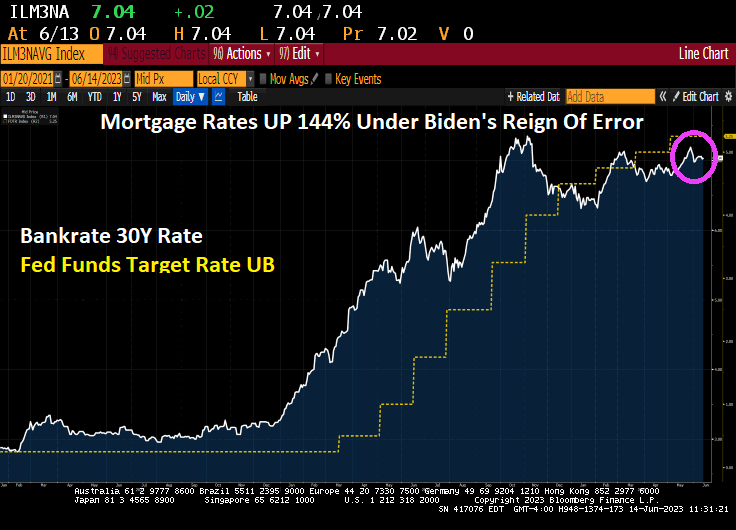

Biden’s “reign of error” is horrific. The inflation caused by Biden’s policies, The Federal Reserve and insane Federal spending has caused mortgage rates to soar 144% since Biden took office.

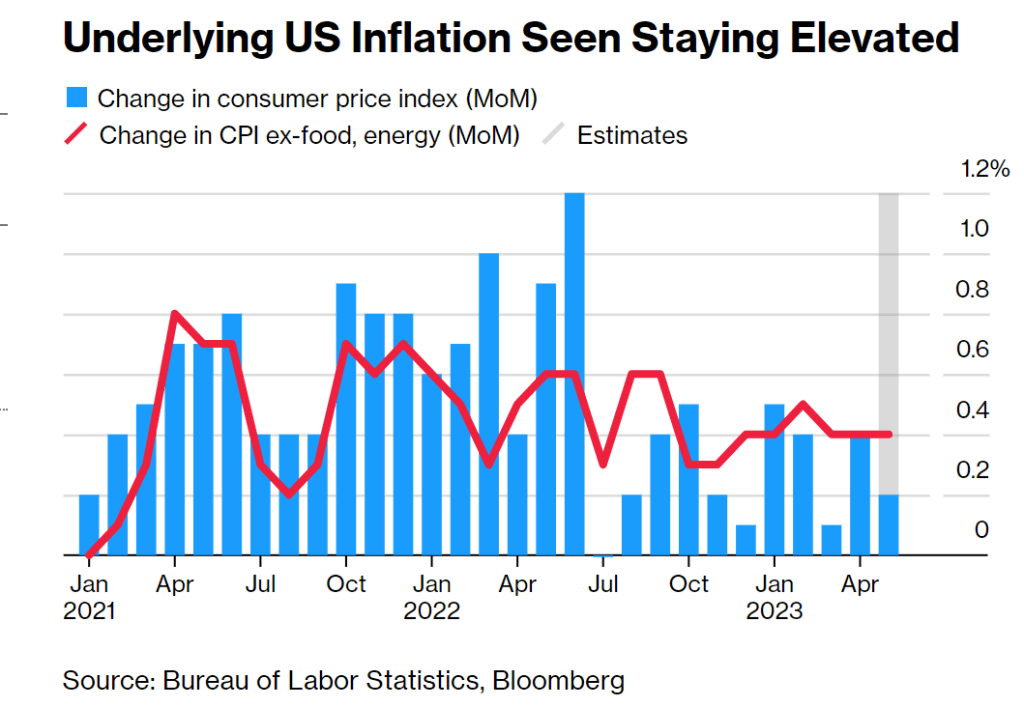

While The Fed is likely to pause today, but Fed Funds are pricing in a July rate hike.

Federal Reserve policymakers are about to take their first break from an interest-rate hiking campaign that started 15 months ago, even as they confront a resilient US economy and persistent inflation.

The Federal Open Market Committee on Wednesday is expected to maintain its benchmark lending rate at the 5%-5.25% range, marking the first skip after 10 consecutive increases going back to March of last year. While officials’ efforts have helped to reduce price pressures in the US economy, inflation remains well above their goal.

Source: Bureau of Labor Statistics, Bloomberg

Investors’ focus will be on the Fed’s quarterly dot plot in its Summary of Economic Projections, which is expected to show the policy benchmark rate at 5.1% at the end of 2023.

By contrast, markets are pricing in the possibility of a quarter-point hike in July followed by a similar-sized cut by December, and some Fed policymakers have emphasized that a pause in the hiking cycle shouldn’t be seen as the final increase.

Fed Chair Jerome Powell, who’ll hold a press conference after the meeting, has suggested he favors a break from hiking to assess the impact both of past moves and of recent banking failures on credit conditions and the economy. His commentary will be scrutinized for hints of the committee.

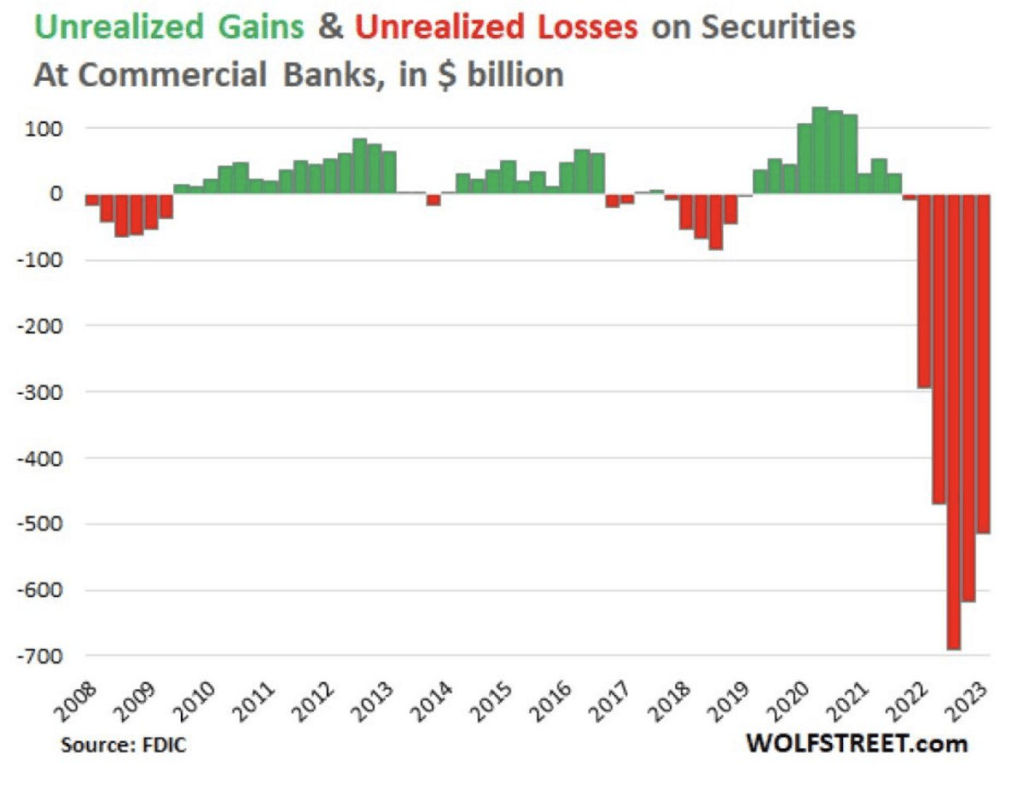

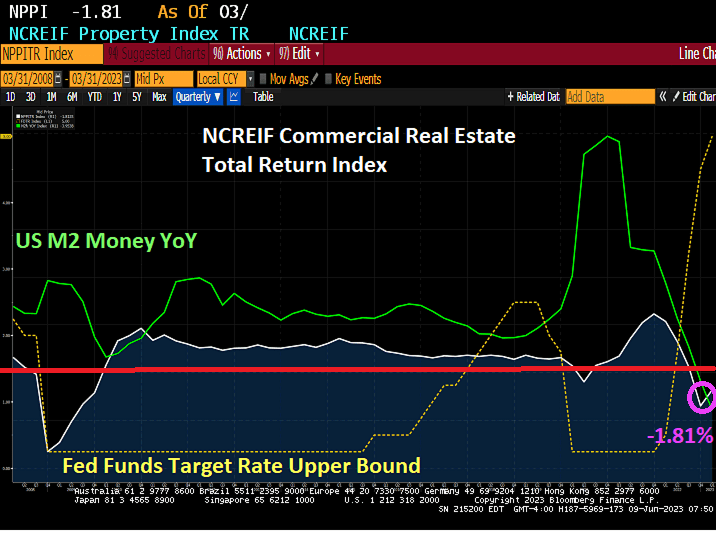

Remember, there is still over $8 TRILLION in Fed assets held sloshing around the economy. The Fed never really removed the excess liquidity and it continues to stoke asset bubbles.

Bear in mind that The Fed is pausing at 5.25% Fed Target Rate, while the Taylor Rule suggests rate hikes to 10.12%. So, Foul Powell is pausing at just over the half way mark.

Of course, Biden’s and Congress’ massive spending spree is causing inflation, and The Fed has no control over Biden/Congress irresponsible spending.

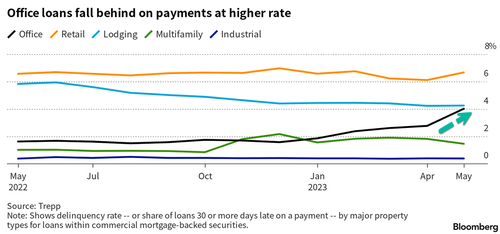

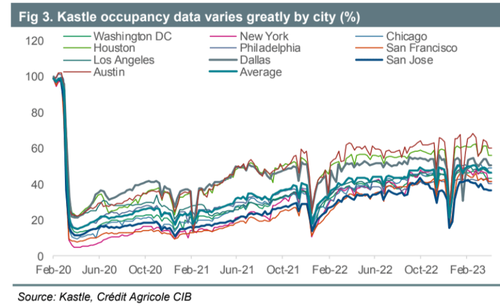

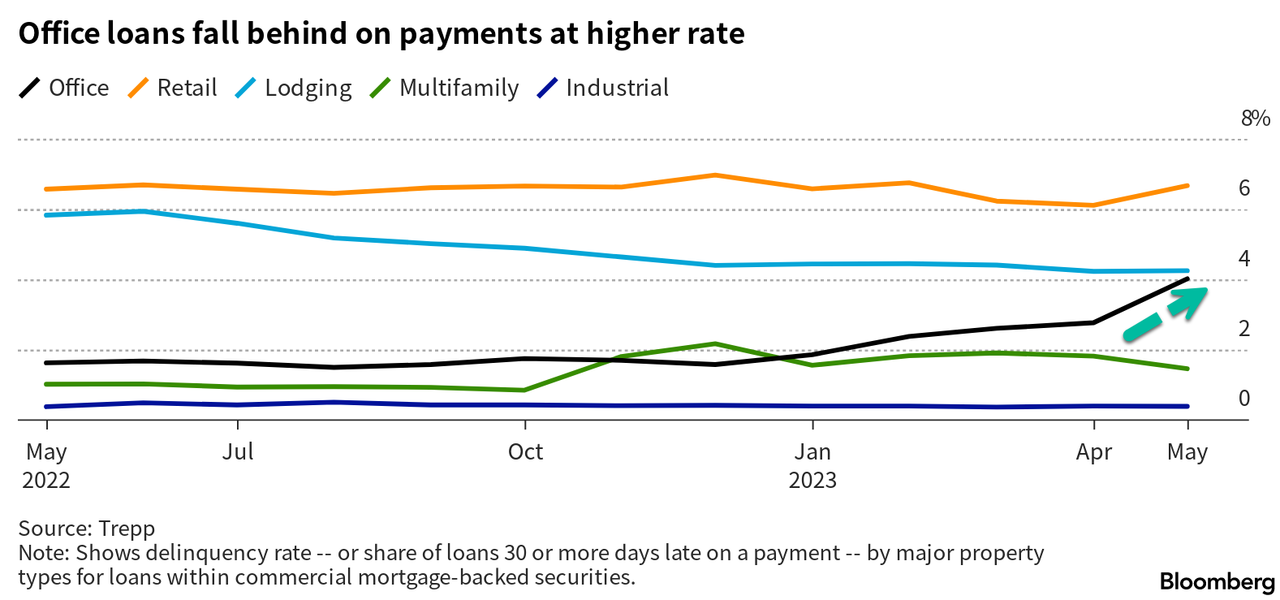

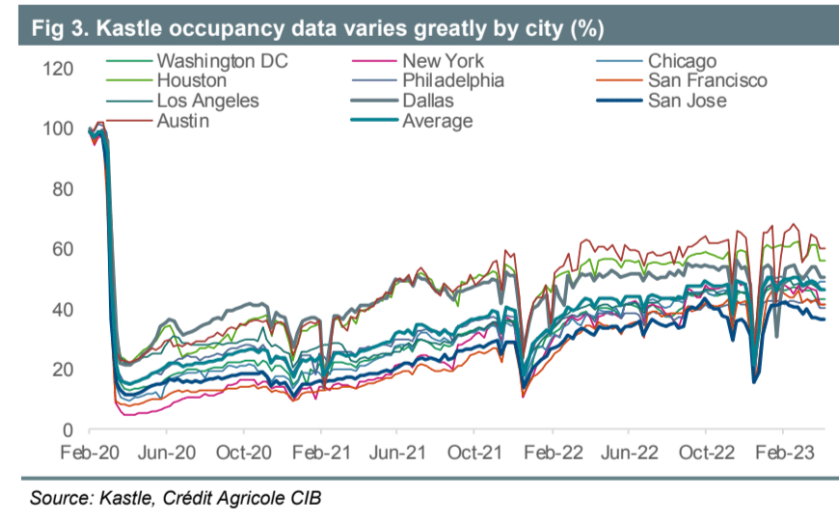

Some structural factors, such as remote work and hybrid work, have doomed the office space segment. This has left empty office buildings scattered across major US cities as the number of landlords falling behind on repayments due to the difficulty of refinancing and high vacancies has hit a five-year high.

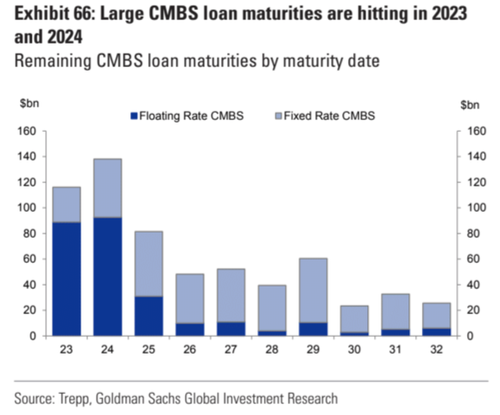

According to real estate data firm Trepp, more than 4% of office loans packed into commercial mortgage-backed securities were delinquent in the last 30 days as of May, the highest level since 2018.

Dan McNamara, the founder of Polpo Capital Management, told Bloomberg about impending CRE turmoil:

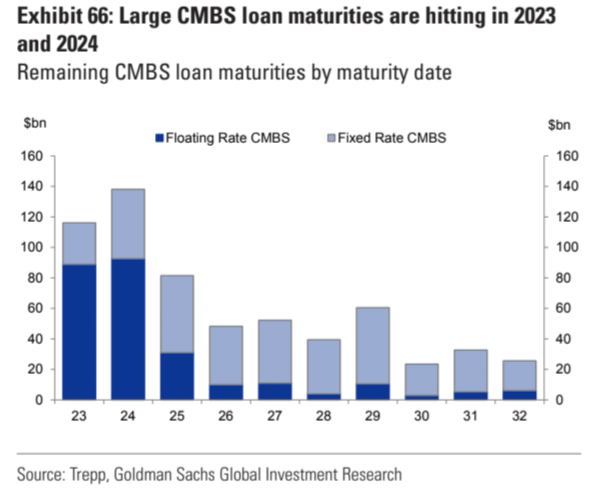

“This is just the tip of the iceberg for office delinquencies as $35 billion in CMBS office loans are scheduled to mature this year and the refinancing market is effectively shut to this asset class.”

The rise in delinquencies comes as security card swipe data from Kastle shows many workers have yet to return to their desks in major US cities, resulting in high office space vacancies nationwide.

As Goldman pointed out to clients days ago, one major issue is a steep maturity wall of floating and fixed-rate CMBS loans due this year and next. The inability to refinance in these challenging market conditions will likely unleash a tidal wave of defaults in the second half of this year.

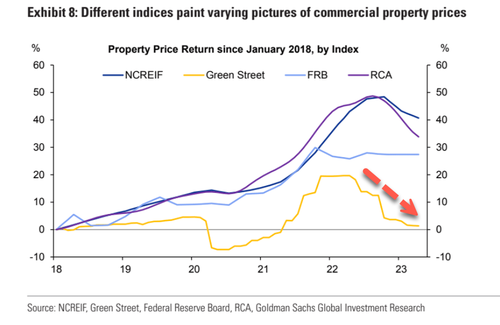

Goldman Sachs chief credit strategist Lotfi Karoui told clients last month, “the most accurate portrayal of current market conditions” is data via the Green Street Commercial Property Price Index, which suggests trouble ahead.

Just how much danger? Karoui believes “Green Street indicates a 25% year-over-year drop in office property values and a 21% drop in apartment property values.”

So the combination of high vacancies, sliding prices, and tightening lending standards is a perfect storm that could ignite an eruption of delinquencies in office loans in the coming quarters.

Treasury Secretary Janet “Too Low For Too Long” Yellen, and former Federal Reserve Chair, is partly responsible for a phenomenon plaguing America: the death of starter homes.

As Mish has discussed, with main markets no longer an option for first-time buyers, Point2 looked at the country’s 100 largest secondary cities for the median price of a starter home and renter households’ median income. Defined as large non-core cities within a metro, these cities used to be fruitful house-hunting grounds for first-time buyers exploring less-expensive options away from main cities. But as it turns out, unaffordability can put a dent in homeownership plans regardless of city type or size.

In 41 of the 100 largest secondary cities in the U.S., renters earn half or less than half of the income they would need to buy a median-priced starter home.

There are no non-core cities in which renters could comfortably make a move toward homeownership: In 10 cities, the necessary income is about triple what they earn.

Would-be buyers in Burbank and Glendale, CA have it worst: They lack 67% of the income they would need in order to make the move from renter to homeowner.

Renters in 9 California cities would need to earn about $100,000 more in order to afford a starter home. Based on the latest renter income figures, starter home prices, and mortgage rates, non-core cities in the LA and San Diego metros are the toughest for first-time homebuyers.

In 15 of the 100 largest secondary cities, renters would need less than 4 months’ worth of extra income to afford the transition to owning a starter home.

Homeownership is within reach in Independence, MO, and Broken Arrow, OK. Those who dream of owning here would need less than one month’s worth of extra income to afford a starter home.

California Tops the List of Worst Places to Look

California has the dubious distinction of having the top least affordable starter home cities.

A starter home, according to the Census Department is priced in the bottom third of homes in the area.

Pomona, CA, is in fourteenth place. The average renter in Pomona makes $49,000 a year and needs to get to $121,000 a year. That’s nearly 2.5 times current salary.

In Burbank, CA, the average renter makes $63,000 year an needs to get to $193,000. That’s over 3 times current salary.

Within Grasp

In no market can the average renter make the plunge.

But in Independence, Missouri, or Broken Arrow, Oklahoma, the average renter is respectively just 2% and 5% short of the amount needed for a starter home

Not Shocking

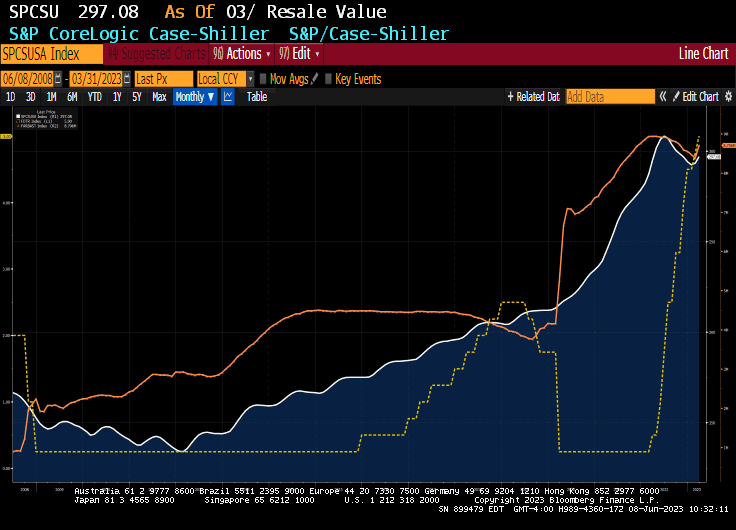

None of this is shocking. It matches one one should expect looking at Case-Shiller home prices and mortgage rates.

The Fed wanted to produce inflation and it did. But for years the Fed did not even see the inflation because the manifestation of inflation was in asset prices, not the price of consumer goods.

Case-Shiller Top City Home Prices Decline From Year Ago for the First Time Since May 2012

Housing starts, like mortgage purchase demand, remains depressed compared to the housing bubble of the 2000s.

Now, will The anticipated Fed pause in rate hiking help? Not likely. The Fed still has over $8 trillion in monetary stimulus chasing assets. Too much Stimulypto.

Biden signed the debt ceiling bill craftted by McCarthy (RINO-CA) and Schumer (Communist-NY). Its allows for uncontrolled spending and borrowing for at least 2 years. And as Milton Friedman once said “There is nothing more permanent than a temorary Federal program … or debt limitiations.

With Biden signaling that government has gone wild with no controls on fiscal responsibility (and Elizabeth Warren flailing her arms and screaming for regulations on cryptocurrencies), cryptos today are getting demolished.

China, Japan and the BRICs realize that there are no controls on ANYTHING coming out of Washington DC. Insane spending, an insane Federal Reserve, corrupt DOJ and FBI.

The US economy was sitting high on the global mountain top before Covid. Then Covid struck, The Federal Reserve and Congress went wild with stimulus spending and inflation went wild. This is Biden Country, a feeble shell of this once great nation.

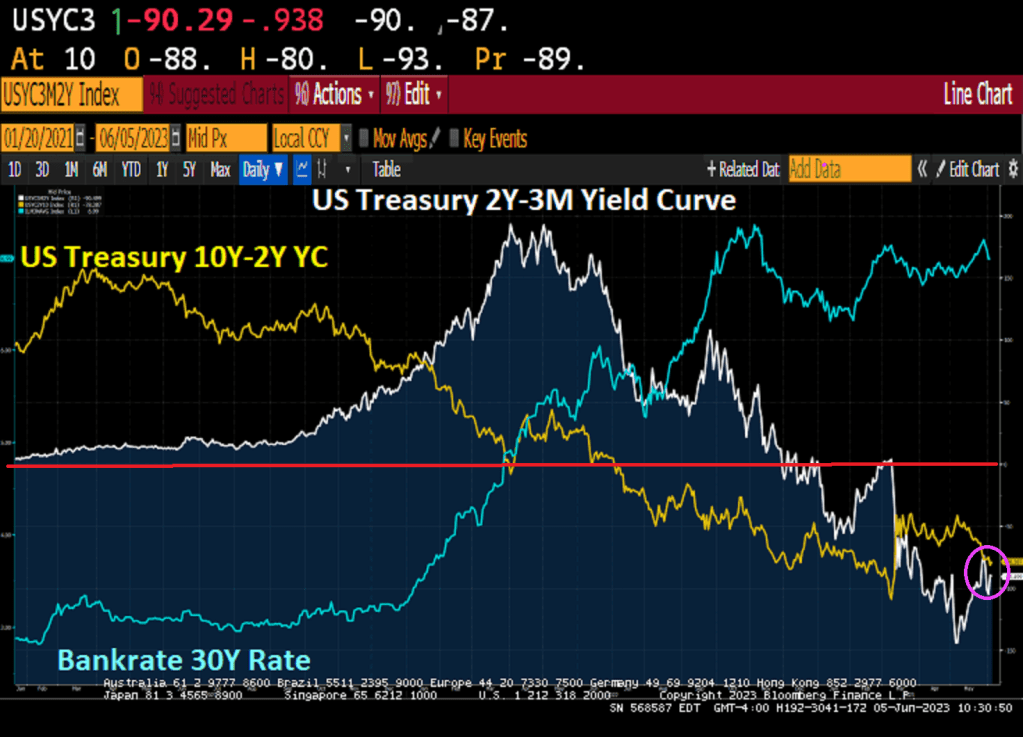

As The Fed tries to counter the years of excess monetary stimulus pre and post Covid by raising rates, we have seen mortgage rates rise 143% under Biden’s leadership. At the same time, the US Treasury yield curves (short 2Y-3m and long 10Y-2Y) remain deeply inverted.

As of this AM, The Fed Funds Futures market is pricing in a chance of continued rate hikes by The Fed, but mostly we are at 5.25% at least until November when rates are forecast to begin declining.

And the Taylor Rule is still signaling rate hikes to 10.12%. We are at only 5.25%. And with Biden feebily running for reelection, the only path forward is rate CUTS.

Well, Kevin McCarthy (RINO-CA) and Patrick McHenry (RINO-NC) along with Jim Jordan (RINO-OH) and Marjorie Taylor Greene (RINO-GA) sold out America to Green Joe Biden (the Jolly Green Giant?) and pretty much guaranteed a Biden reelection as President and Democrats winning the House majority at the next election. Way to go McCarthy, McHenry, Jordan an Greene! You sold out America to the Progressive, destructive Left.

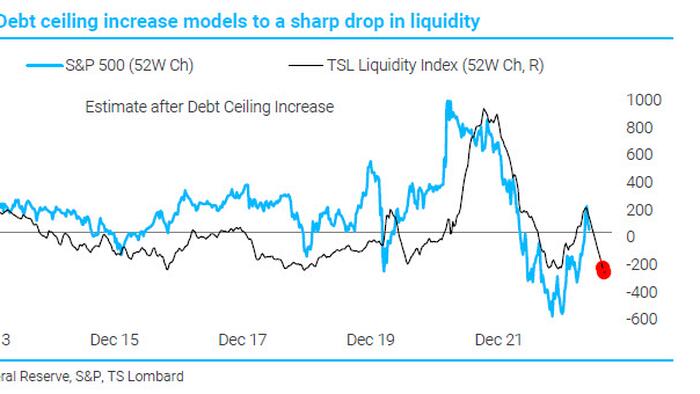

With a debt ceiling deal freshly inked, the US Treasury is about to unleash a tsunami of new bonds to quickly refill its coffers.This will be yet another drain on dwindling liquidity as bank deposits are raided to pay for it — and Wall Street is warning that markets aren’t ready.

The negative impact could easily dwarf the after-effects of previous standoffs over the debt limit. The Federal Reserve’s program of quantitative tightening has already eroded bank reserves, while money managers have been hoarding cash in anticipation of a recession.

JPMorgan Chase & Co. strategist Nikolaos Panigirtzoglou estimates a flood of Treasuries will compound the effect of QT on stocks and bonds, knocking almost 5% off their combined performance this year. Citigroup Inc. macro strategists offer a similar calculus, showing a median drop of 5.4% in the S&P 500 over two months could follow a liquidity drawdown of such magnitude, and a 37 basis-point jolt for high-yield credit spreads.

The sales, set to begin Monday, will rumble through every asset class as they claim an already shrinking supply of money: JPMorgan estimates a broad measure of liquidity will fall $1.1 trillion from about $25 trillion at the start of 2023.

“This is a very big liquidity drain,” says Panigirtzoglou. “We have rarely seen something like that. It’s only in severe crashes like the Lehman crisis where you see something like that contraction.”

It’s a trend that, together with Fed tightening, will push the measure of liquidity down at an annual rate of 6%, in contrast to annualized growth for most of the last decade, JPMorgan estimates.

The US has been relying on extraordinary measures to help fund itself in recent months as leaders bickered in Washington. With default narrowly averted, the Treasury will kick off a borrowing spree that by some Wall Street estimates could top $1 trillion by the end of the third quarter, starting with several Treasury-bill auctions on Monday that total over $170 billion.

What happens as the billions wind their way through the financial system isn’t easy to predict. There are various buyers for short-term Treasury bills: banks, money-market funds and a wide swathe of buyers loosely classified as “non-banks.” These include households, pension funds and corporate treasuries.

Banks have limited appetite for Treasury bills right now; that’s because the yields on offer are unlikely to be able to compete with what they can get on their own reserves.

But even if banks sit out the Treasury auctions, a shift out of deposits and into Treasuries by their clients could wreak havoc. Citigroup modeled historical episodes where bank reserves fell by $500 billion in the span of 12 weeks to approximate what will happen over the following months.

“Any decline in bank reserves is typically a headwind,” says Dirk Willer, Citigroup Global Markets Inc.’s head of global macro strategy.

Bitcoin Faces Downside Risks After Debt Deal Moves Forward

Just when markets appear to be moving past the months-long drama around the US debt ceiling, holders of risky assets such as cryptocurrencies are likely facing a fresh challenge while the Treasury looks to rebuild its depleted cash balance with an estimated $1 trillion Treasury-bill deluge.

“The impending reserve drawdown, due to the [Treasury General Account] rebuild, may prove to be a headwind,” Citi Research strategists including Alex Saunders wrote in a note.

Citi analyzed the performance of risky assets during drawdowns and found that they were vulnerable to higher volatility and weaker returns. As such, the near-term outlook doesn’t seem too rosy for Bitcoin and Ether. “Both coins average negative returns in these scenarios, and BTC has significantly underperformed in the median case,” the strategists wrote Thursday.

The TGA, which keeps money for the Treasury, ballooned during the pandemic. It expanded again last year and is now about as low as it has ever been. Treasury, as a result, will need to replenish its dwindling cash buffer to maintain its ability to pay its obligations through bill sales, estimated at well over $1 trillion by the end of the third quarter. This supply burst may drain liquidity from the banking sector and raise short-term funding rates against an economy many say is likely to fall into recession.

This doesn’t bode well for digital-asset investors, who were just recovering from fears of a no-deal scenario for the US debt ceiling. While Bitcoin edged higher on Friday, it’s still hovering around the $27,000-mark that it has failed to break away from for several weeks.

“Crypto markets were not immune to fears of the US defaulting on its debt, selling off on negative developments and rallying on headlines suggesting progress,” the strategists said. They added that crypto has typically “fared well” amid issues concerning traditional financial institutions, citing the banking turmoil in March, a period in which Bitcoin outperformed. But perhaps risks of an institution such as the US government defaulting “doesn’t paint a favorable outlook for decentralized digital assets.”

To illustrate, the strategists used the Cboe Volatility Index, or VIX, as an indicator of the market’s fear to gauge whether a resolution would be passed before hitting the ceiling. And whenever equity market concerns were eased, that’s when Bitcoin outperformed.

“While in theory the potential default of an institution as impactful as the US government would bode well for decentralized technologies and systems, this may not currently be the case given that the crypto industry is still in its infancy and regulation has yet to be well-defined,” they wrote. “Another theory is that not raising the debt ceiling would lead to reduced US government debt and a lower fiscal deficit, and provide more credibility to fiat, particularly the dollar.”

On Friday, the Senate passed legislation to suspend the US debt ceiling and impose restraints on government spending through the 2024 election. The measure now goes to President Joe Biden, who forged the deal with House Speaker Kevin McCarthy and plans to sign it just days ahead of a looming US default.

Year-to-date, Bitcoin has rebounded some 60% after starting the year at around $16,500. Such optimism comes after 2022’s 64% drop, its second-worst year in its history. It rose about 1% to $27,178 as of 3:32 p.m. in New York, and is marginally higher from last Friday.

Bitcoin’s support hovers around $26,500, said Fiona Cincotta, senior market analyst at City Index, adding that a break below $25,000 could mean a deeper sell-off.

“The problem is the macro backdrop, which is relatively uncertain going forward with recessionary fears,” she said. “I think what will be looking for to make Bitcoin shine is a nice dovish pivot from the Federal Reserve. That might be the tide where we will see another decent leg higher.”

Range-bound trading has been Bitcoin’s defining characteristic of late, with its 30-day volatility reigning low at 1.8%, firmly staying firm within its two-month-long trading range. Despite growing short-term volatility, options implied volatility trended lower over the past week, according to K33’s Bendik Schei and Vetle Lunde. Even so, Bitcoin exchange-traded products continued to see steady outflows while Bitcoin volumes — spot and futures — are trending lower.

McCarthy, McHenry, Jordan and Greene, honorary Frenchmen!

It is not a surprise that the ill-advised COVID economic shutdowns would harm small businesses that large corporations.

Yes, The Fed’s M2 Money printing press went wild with COVID emergency refief. And so did the discrepancy between the top 1% and the bottom 50% in terms of “Share of Total Net Worth Held.” The top 1% is in blue and the bottom 50% is in red. M2 Money is in green.

Compared to pre-COVID, the top 1% increased their share of total net worth from 29.7% to 31.9%, an increase of 7.4% since January 2020. The bottom 50% fell from 30% to 28.5%, a -5% decline. An elitist wonderland!

And The Biden family keeps raking in the money far about Joe’s salary.

And I assume Fed Chair Jerome Powell and Treasury Secretary Janet Yellen also made fortunes from COVID relief.

Well, Biden and McCarthy have agreed in principle to a budget revision, raise the debt ceiling and avoid a US debt default. The Uniparty strikes again! No restraint of reckless Federal spending t speak of . The big donor class wins and middle class Americans lose.

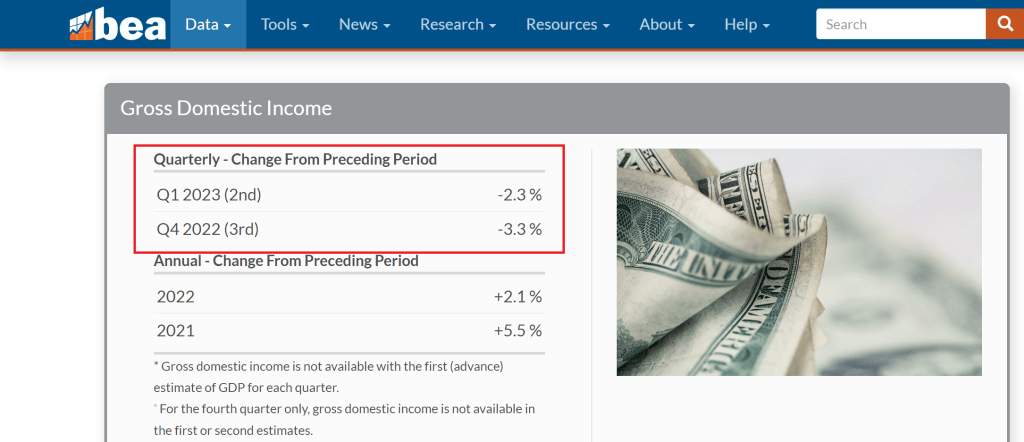

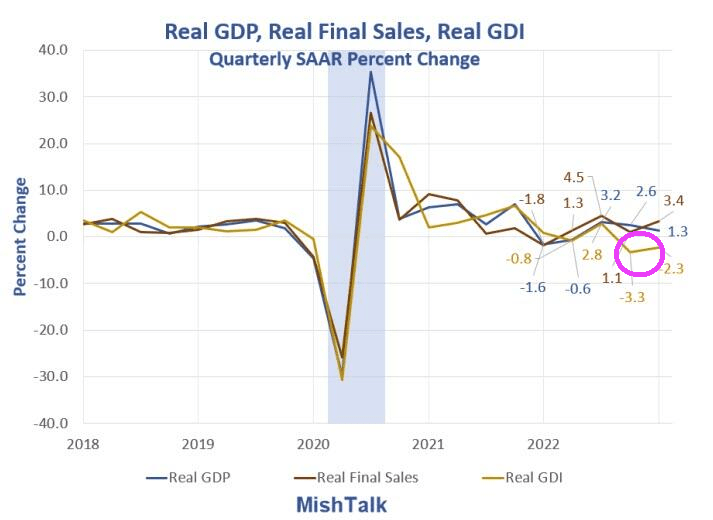

Mike Shedlock (aka, Mish) makes a good point: the US is already in recession if we look at GDI (gross domestic income) rather than GDP (gross domestic product). The US has already declined two consecutive quarters in terms of negative GDI growth.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.