Now here we are again with yet another bank contagion. First it was Silicon Valley Bank, now it is First Republic Bank (down -28% at opening).

And there is a trading halt on First Republic. But YoY growth on FRC’s earnings of -34.7% is horrendous.

At least cryptobank Silvergate isn’t down as much as Silicon Valley Bank and First Republic Bank.

And the SPDR Regional Bank index is getting clobbered as Fed withdraws stimulus.

SVB’s management’s solution appears to have been to seek out yield through a lot of long-duration bonds. The bank started to lose deposits as VCs pulled cash/burnt through operating capital.

SVB’s CEO Greg Becker saw this coming and dumped his holdings.

The last US debt crisis occured in 2013 when Congress finally raised the debt ceiling … and kept on borrowing and spending, But if you thought that a debt crisis would scare Congress (and the Administration) into balancing the Federal budget, you would be wrong. In fact, since the 2013 debt crisis, Federal debt is up 88% (+$14.7 TRILLION over the last 10 years).

And with the massive growth in Federal debt under Obama, Trump and Biden has resulted in an explosion in interest payments on the Federal debt.

What a mess in Washington DC. While House Republicans are at lagerheads with Senate Democrats and Resident Biden over Federal spending cuts, the price of insuring against a debt default just rose to 76.75.

How bad it that? Put it this way. Millions are fleeing Mexico and Guatemala and coming to the US. But Mexico has a lower cost of insuring against a debt default than the USA. And Guatemala is almost as expensive as the USA.

It will all be over soon, according to CDS prices.

Not really a surprise, but January’s personal spending numbers came in hot at 1.8% MoM. Also, Personal Consumption Expenditures PRICE index (aka, inflation) rose to 5.4% YoY.

Here comes The Fed! The 2-year Treasury yield rose 10 basis points this morning.

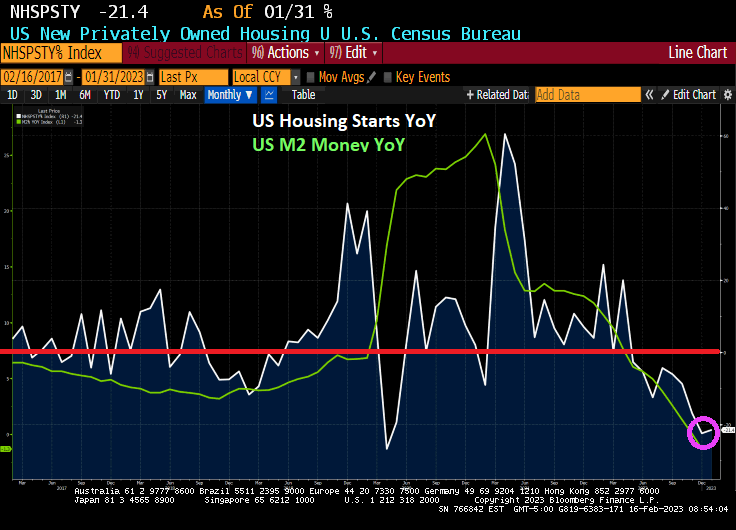

First, US housing starts are now down -21.4% year-over-year (YoY) and down -4.5% month-over-month (MoM) in January 2023 as The Fed removes its massive monetary stimulus.

PPI Final Demand PRICES are still elevated at 6% YoY, so expect more Fed tightening.

Today’s data dump.

On a final note, I am appalled at the Biden Administration’s “response” to the East Palestine Ohio derailment. Where is Mayor Pete, the US Transportation Secretary??

First, Sam Bankman-Fried agreed to testify in the House Financial Services Committee meeting on December 13, 2021. Then Bankman-Fried said he would testify remotely. Then ,,, he was arrested by the Bahama’s police. How convenient!

WASHINGTON, Dec 12 (Reuters) – Sam Bankman-Fried, the founder and former CEO of now-bankrupt crypto exchange FTX, on Monday said he would testify remotely at Tuesday’s U.S. House Financial Services Committee hearing to examine the collapse of the company.

FTX filed for U.S. bankruptcy protection last month and Bankman-Fried resigned as chief executive, triggering a wave of public demands for greater regulation of the cryptocurrency industry.

That might be kind of difficult, since Sam Bankman-Fried has been arrested in the Bahamas.

Perhaps, The SEC Gary Genslar will testify as to why he met with SBF and gave him the green light for his trading? And why did Genslar erase Hillary Clinton from his schedule after meeting with her? And why was Genslar meeting with Hillary in the first place since she is now just an American cititzen??

Will SBF be extricated by tomorrow morning hearing time?

This will be the last time (Fed rate hikes) as the US economy is forecast to either go into a recession in 2023 or slow down to an anemic 1.20% Real GDP YoY. Even the Fed is forecasting 3.10% core inflation in 2023, still higher than their target rate of 2%.

One of the sectors that is suffering is commercial real estate.

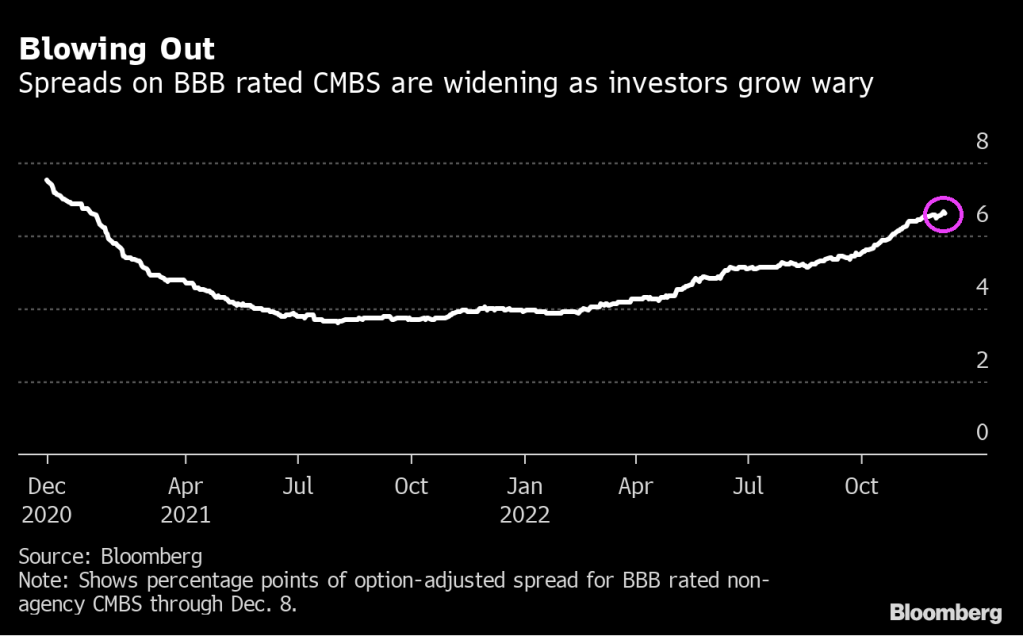

Commercial mortgage bonds could get clobbered in the coming months, and investors are backing away from the securities.

Some $34 billion of the bonds come due in 2023, and refinancing property loans is difficult now. Property prices could fall 10% to 15% next year, according to JPMorgan Chase & Co. strategists. And some types of properties seem particularly vulnerable as, for example, city workers are slow to come back to their offices full time.

That may be why spreads on BBB commercial mortgage bonds have widened by about 2.7 percentage points this year through Thursday to around 6.6%, for the securities without government backing. They are now at their widest since January 2021. They’ve been getting hit particularly hard in the last few months, even as risk premiums on investment-grade and high-yield corporates have been shrinking on hopes the Federal Reserve will scale back its tightening campaign.

“For CMBS investors, there’s lots of uncertainty, especially around whether maturing loans are going to get refinanced or not, and if not, what the resolution will be,” said David Goodson, head of securitized credit at Voya Investment Management, in an interview. “Layering in risk from lower office utilization makes the assessment even tougher.”

The trouble that the bonds face won’t necessarily translate to a surge in defaults in the near term, which is part of why betting against them is so difficult. When property owners can’t refinance mortgages that have been bundled into bonds, noteholders have a difficult choice to make. They can seize the buildings and liquidate them, or they can extend the debt and accept repayment later. They usually go for the second option.

Extending maturities allows bondholders to kick the can down the road and potentially recover more later, said Stav Gaon, head of securitized products research at Academy Securities. The question is whether properties have permanently lost value as, for example, people reorder their lives after the pandemic, or whether declines may be more temporary because of higher rates.

“Foreclosing on a loan, rather than granting an extension, can be really messy — that’s a lesson that was learned during the great financial crisis,” said Gaon. “The lenders also recognize that today’s higher interest rates are a very sudden development that many high-quality borrowers need time to adjust to.”

Some investors that are still buying are focusing on higher-quality borrowers and properties, that are likelier to withstand any downturn in real estate prices without having to seek extensions on loans.

“We think trophy properties will fare better due to better access to the debt markets, lower potential property declines, and a continued tenant flight to quality,” said Zach Winters, senior credit analyst at USAA Investments.

He acknowledges that this strategy isn’t always popular now, even if it turns out to make sense.

“When we go out and bid on a bond tied to a trophy office building now, usually the number of buyers is significantly less than before,” Winters said.

After the Pandemic

The market for commercial mortgage bonds without government backing was about $670 billion as of the end of 2021, and although the securities soared in the second half of 2020 as the Fed opened the money spigots, they’re facing more difficulty now. With office occupancy still below 50% in many cities as more people work from home, corporate buildings may see their values drop. Retail space is similarly under pressure as consumers have grown used to buying more online. And while travel volume is rising, many hotels are struggling to reach 2019 levels for room charges.

A survey of institutional real estate market professionals in November found that firms expect office values to fall about 10% next year, and overall commercial property declines of 5%, according to the Pension Real Estate Association.

The $34 billion of bonds due next year includes mostly fixed-rate CMBS bonds sold without government backing. It’s a steep increase from the $24.4 billion of such bonds maturing this year, according to Academy Securities.

There’s another $103 billion of a type of CMBS known as single-asset single-borrower bonds maturing next year, according to Academy — although most of that debt pile has a built-in contractual ability to extend loans, meaning they’ll be able to seek extensions more easily.

Next year won’t be the first time that CMBS bondholders and servicers have faced tough choices about whether to allow en masse extensions to the underlying borrowers. After the 2008 financial crisis, commercial property values plummeted and many lenders chose to give owners of those properties more time to pay back their loans. As a result they ended up getting more money back than if they’d immediately foreclosed on the loans and liquidated the properties, said Jeff Berenbaum, head of CMBS and agency CMBS strategy at Citigroup.

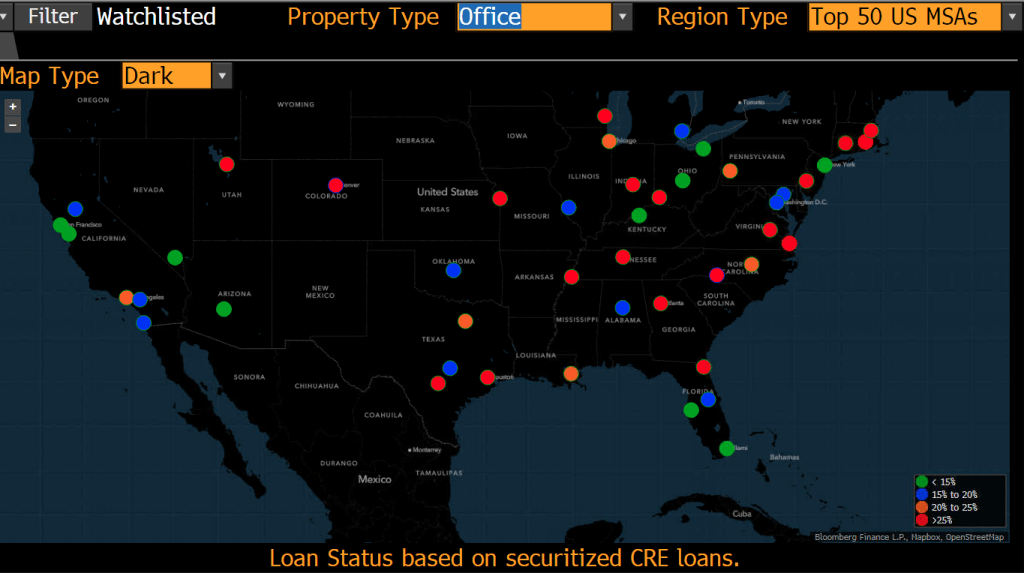

In terms of watchlisted CMBS loans, currently most of the USA is in the green (good) except for San Francisco, New Orleans, Memphis and Chicago all have elevated commercial loans on the watchlist (loans being watched for going late and into default). Puerto Rico is also in the red (>25%) watchlisted commercial loans, so I expect AOC to be asking for a bailout.

On the office property front, we can see red (>25% of commercial loans watchlisted) pretty much across the board.

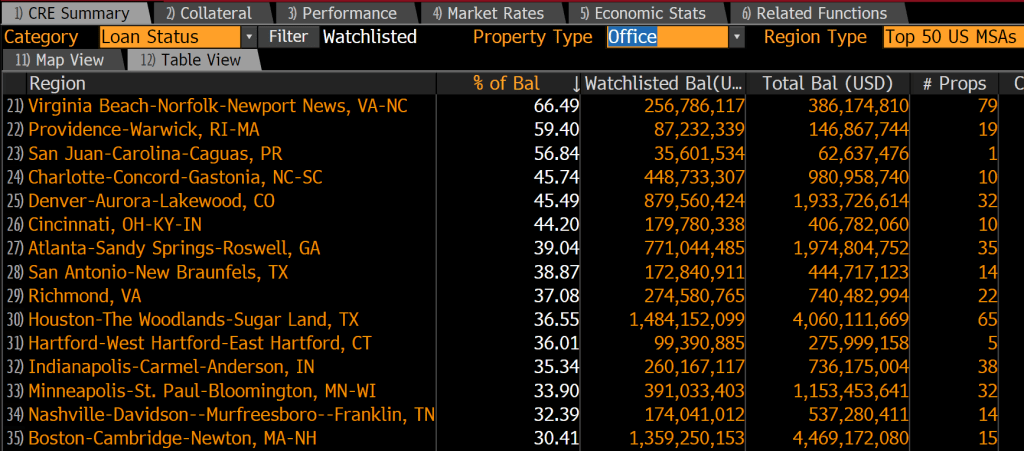

The leading metro area in terms of watchlisted office property loans is … Virginia Beach-Norfolk-Newport News VA-NC at 66.49% (that is pretty bad). Providence RI is second and San Juan Puerto Rico is third followed by Charlotte NC in fourth place. The only Ohio city in top 15 is Cincinnati, home of Skyline Chili and Montgomery Inn.

While most are calling for more rate hikes in 2023, I predicted that December’s likely 50 basis point hike with be the last one for a while as the US economy grinds to a halt. Or it’s all over now for Fed rate hikes.

While The Fed predicts slow growth, markets are pointing to recession. The Fed is out of touch with reality. As is the US Secretarty of Treasury, “Too low for too long” Janet Yellen.

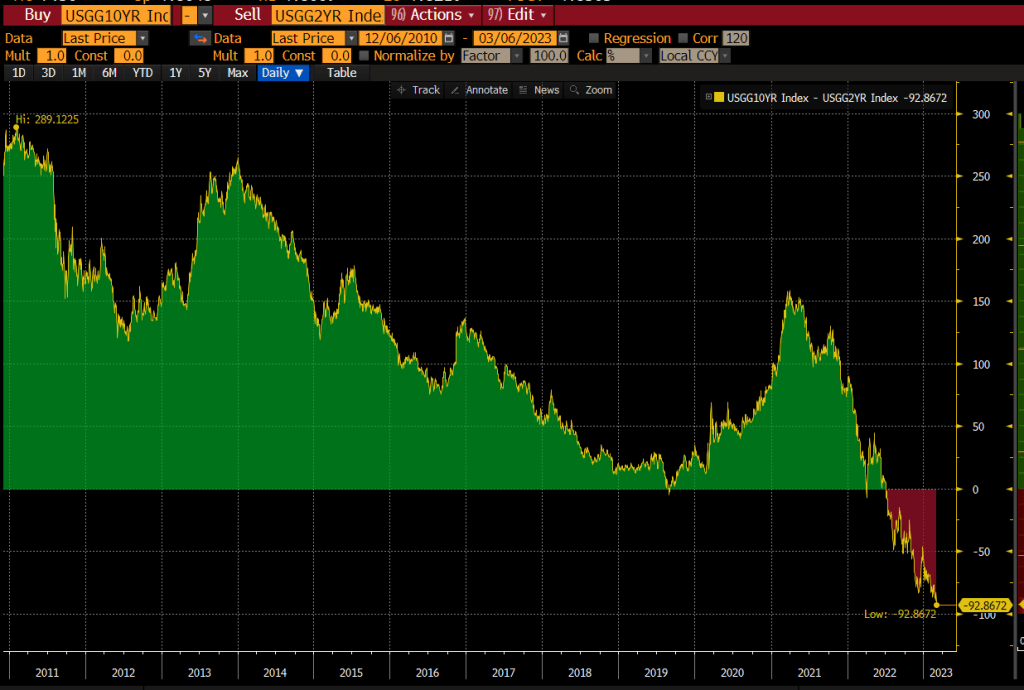

As I frequently told my investment and fixed-income securities students at Chicago, Ohio State and George Mason University, any 10 basis point change in the US Treasury 10-year yield is significant.

But how about today’s 20 basis point decline in the US Treasury 10-year yield?

The UK’s 10-year yield is down even more at -24.1 basis points. Germany is down -18 bps and France is down -10.3 bps.

Speaking of credit default swaps, Credit Suisse is back to financial crisis levels while UBS and Deutsche Bank are not … yet.

With all the turbulence in markets thanks to the war in Ukraine and Biden’s green energy mandates and spending (not to mention Statists like Klaus Schwab screaming about a Great Reset), I was reminiscing about more simple times.

Dear Mr. Fantasy, play us a tune, something to make us all happy (like hitting 2% inflation WITHOUT crashing the economy). Do anything take us out of this gloom (caused by The Fed, Biden’s energy policies and Federal spending). Sing a song, play guitar, Make it snappy. Or in the case of housing, make it crappy.

(Bloomberg) — Federal Reserve Bank of Richmond President Thomas Barkin said the central bank was resolved to curb red-hot inflation, even if that meant risking a US economic recession.

“We’re committed to returning inflation to our 2% target and we’ll do what it takes to get there,” Barkin said Friday during an event in Ocean City, Maryland. He said that this could be achieved without a “tremendous decline in activity” but acknowledged that there were risks.

“There’s a path to getting inflation under control but a recession could happen in the process,” he said.

The US central bank hiked interest rates by 75 basis points in July for the second straight month as policy makers tackle inflation that’s running near 40-year highs. Fed officials speaking in recent days have said more rate increases are needed, but they are still deciding how big to move at their next policy meeting.

St. Louis Fed President James Bullard, one of the most hawkish policy makers, on Thursday urged another 75 basis-point move while Kansas City’s Esther George struck a more cautious tone.

Well, The Fed (aka, Der Kommissars) let the monetary stimulus blow out of control since 2000.

With the 2001 recession, The Fed crashed the target rate (white line) causing home price growth (blue line) to soar. Then The Fed decided that the economy was overheated and cranked up their target rate. This sudden rise in The Fed’s target rate helped to slow/crash housing prices. Resulting in … a frantic decrease in the target rate (late 2007- late 2008) and the adoption of asset purchases of Treasury Notes/Bonds and Agency Mortgage-backed Securities in late 2008.

The Bernanke/Yellen “loose as a goose” policies from late 2008 to Feb 2018 created a total mess. Bernanke/Yellen raised the target rate only one before Trump was elected President, and 8 times AFTER Trump was elected. And Yellen’s Fed began to let the balance sheet shrink a bit before Covid struck in early 2020. And with Covid came another massive expansion of The Fed’s Balance Sheet WHICH HAS NOT YET BEEN WITHDRAWN (despite Fed talking heads saying it would be reduced).

Here we sit with The Fed NOW trying to extinguish inflation (yellow line) by raising their target rate (white line) but NOT shrinking the balance sheet (orange line).

Wonder why this is a horrible homeless problem in the US, particularly in California? While Stanford University has an excellent study of the causes of California’s homeless problem, there is another cause of homelessness … The Federal Reserve’s insane monetary policies since late 2008. The Case-Shiller National Home Price Index is 65% higher in May than during the calamitous home price bubble of 2005-2007, helping to exacerbate the homeless problem.

One of the many problems created by the reckless Bernanke/Yellen/Powell monetary policies is the M2 Money Velocity is near an all-time low making a return to “easy money policies” far more difficult.

I won’t post any photos of the homeless encampments in Los Angeles since it is very sad. But here is a photo of the Dunder-Mifflin paper company “office” on Saticoy Street. The point is that thanks to The Federal Reserve’s loose monetary policies, housing is unaffordable for millions of households forcing many to live on the streets.

Figure 2: Median Rent for a Two-Bedroom Apartment, California, 2022

And a point of trivia. The Office’s Charles Miner (played by the GREAT Idris Elba) was allegedly hired from Saticoy Steel. The Dunder-Mifflin paper company site was on Saticoy Street in sunny LA, not Scranton PA.

Good luck to The Federal Reserve in combating inflation without causing a recession.

TED refers to the difference between the three-month Treasury bill and the three-month LIBOR based in U.S. dollars, a measure of fear in the market.

The 3-month TED spread is rising awfully fast. A sign of impending recession.

US bank credit default swaps (CDS) are rising fast as inflation gets ugly.

The US Treasury 10Y-3M curve is bumping against the zero barrier.

I am still shaking my head at President Biden chastising gasoline stations for not lowering prices at the pump when refiners are near full capacity and the Biden Administration is doing nothing to increase the supply of US-source non-green energy.

You must be logged in to post a comment.