Silence is not golden. Particularly when it comes to a silent DEPRESSION. Talking is cheap, people follow like sheep. Particularly when are told by Biden, Press Secretary Karine Jean-Pierre and NY Times economic spinster Paul Krugman say its the best economy in decades. It isn’t. In fact, the US is in a silent depression.

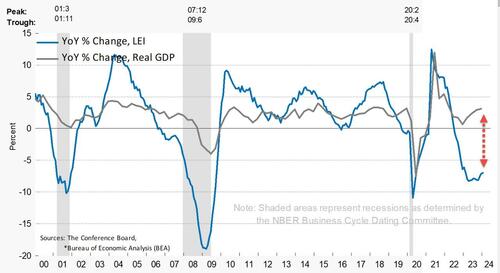

Typically, a recession is defined as two consecutive quarters of negative GDP growth. If we use 2 consecutive quarter of negative GDP growth, we are not in a recession. But ….

Challenges include increasing part-time employment in recent months, declining household employment in three of the last four months for a net decline of 398,000 job holders, mounting public debt burdens, and declining real wages, which have fallen by 4.4 percent since January 2021. Again, just look at the WORST jobs report from January.

Why these results? Bidenomics is based on costly Keynesian boom-and-bust policies. With so much whiplash, it’s no wonder people are conflicted about the economy.

In the latest jobs report for January, a net increase of 353,000 nonfarm jobs from the establishment survey appears robust, as it was well above the consensus estimate of 185,000 new jobs. But let’s dig deeper.

Last month, household employment declined by 31,000, contradicting the headlines. The divergence of jobs added between the household survey and the establishment survey has widened since March 2022. This period coincides with declining real gross domestic product in the first and second quarters of 2022 (usually that’s deemed a recession, but it hasn’t been yet). Indexing these two employment levels to 100 in January 2021, they were essentially the same until March 2022, but nonfarm employment was 2.5 percent higher in January 2024.

While this divergence mystifies some, a primary reason is how the surveys are conducted.

The establishment survey reports the answers from businesses and the household survey from individual citizens. The establishment survey often counts the same person working in multiple jobs, while the household survey counts each person employed. This likely explains much of the divergence, as many people work multiple jobs to make ends meet. The surge in part-time employment and more discouraged workers underscores

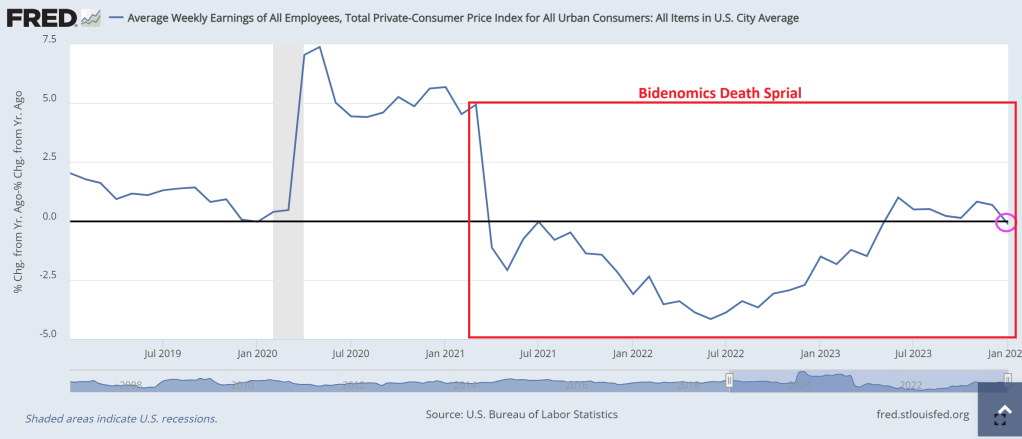

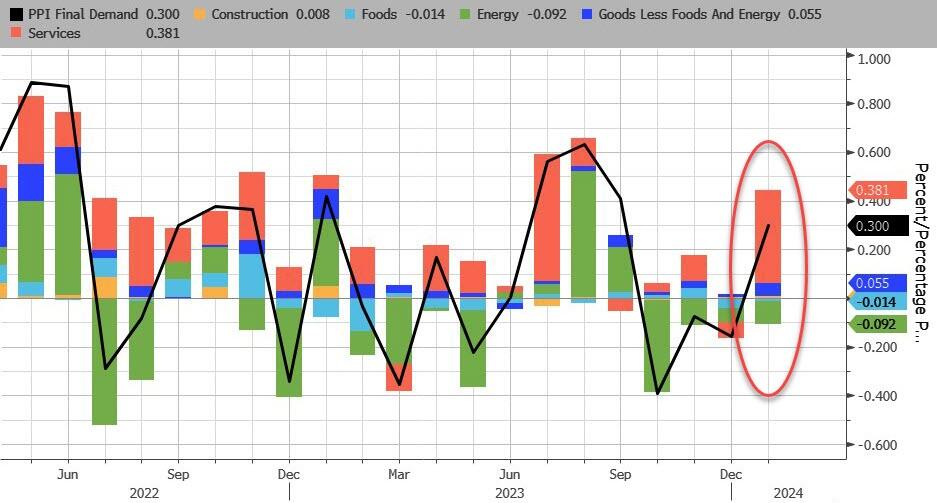

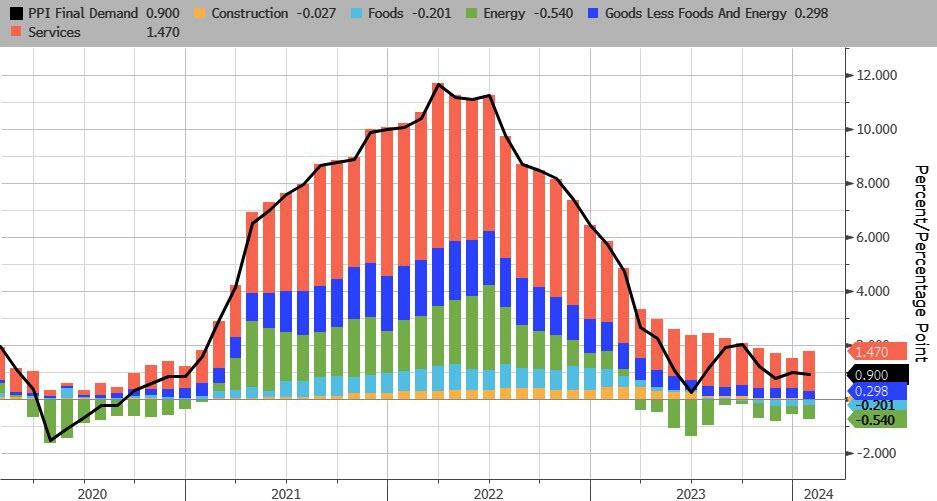

Though average weekly earnings increased by 3 percent in January over a year prior, this is below inflation of 3.1 percent. Real average weekly earnings had increased for seven months before falling last month. And there had been declines in year-over-year average weekly earnings for 24 of the prior 25 months before June 2023. These real wages are down 4.4 percent since Biden took office in January 2021.

As purchasing power declines, mounting debts become more urgent.

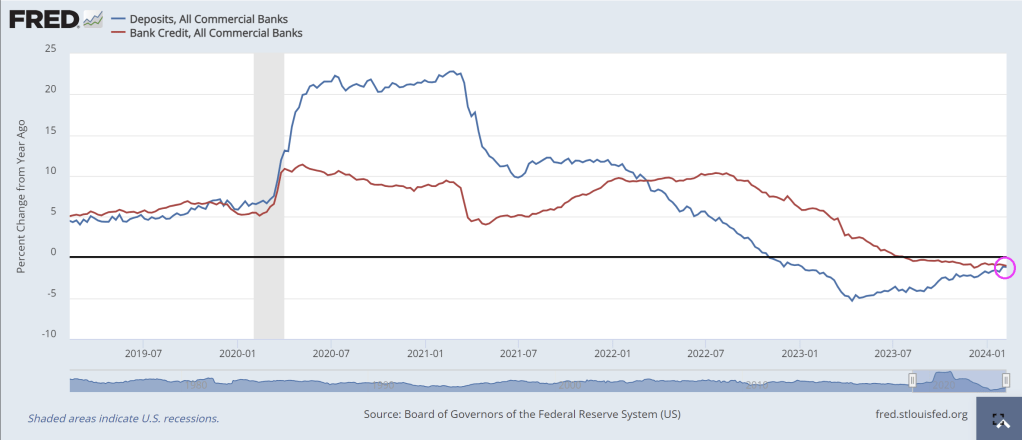

Total US household debt has reached unprecedented levels, with credit card debt soaring by 14.5 percent over the last year to a staggering $1.13 trillion in the fourth quarter of 2023. Such substantial growth in debt raises concerns about the current (unsustainable?) consumption trends, business investment, and a looming financial crisis.

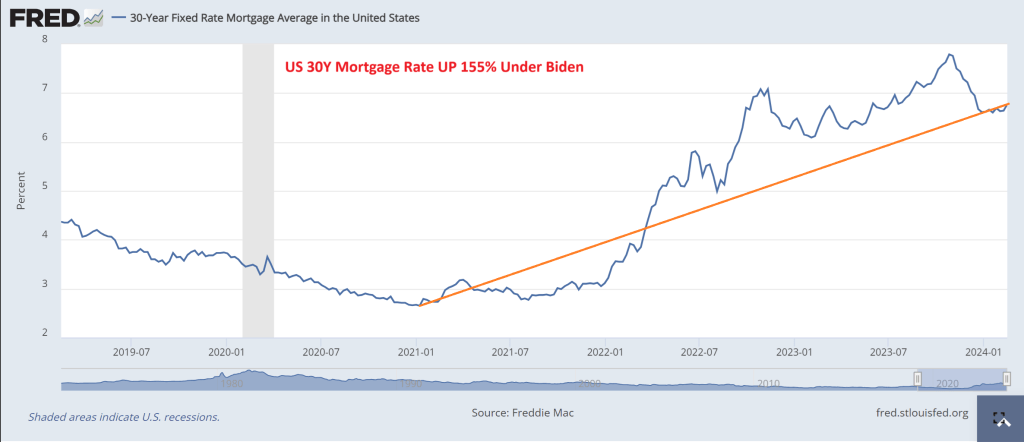

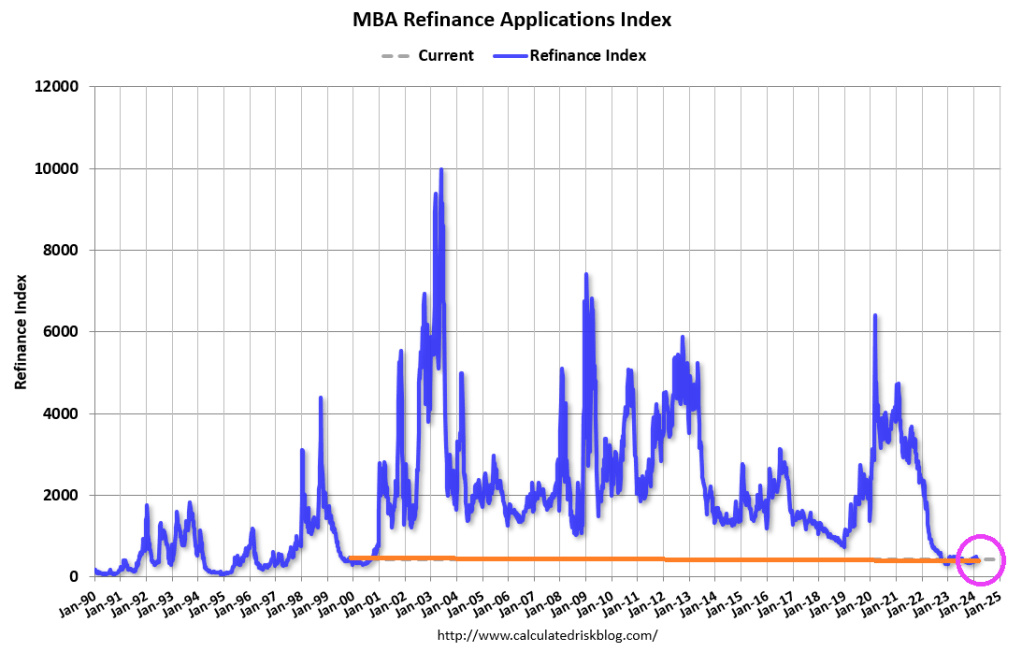

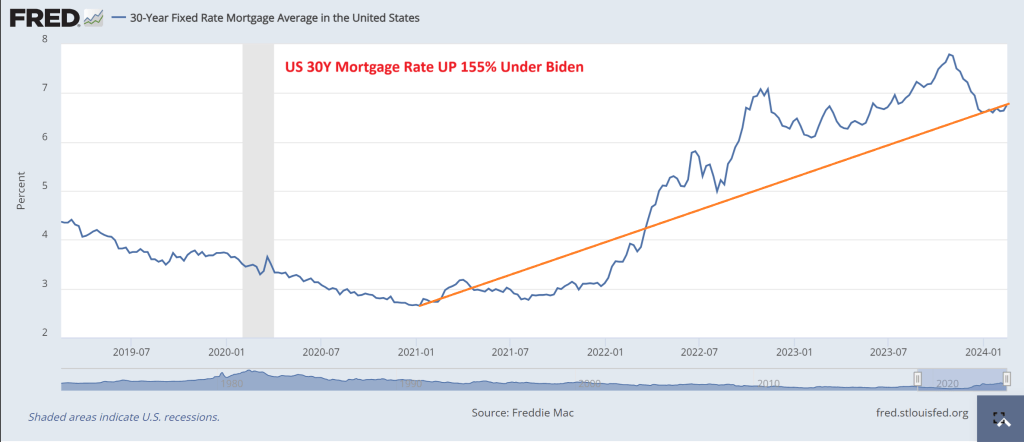

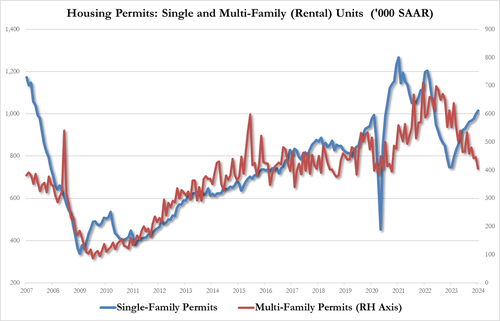

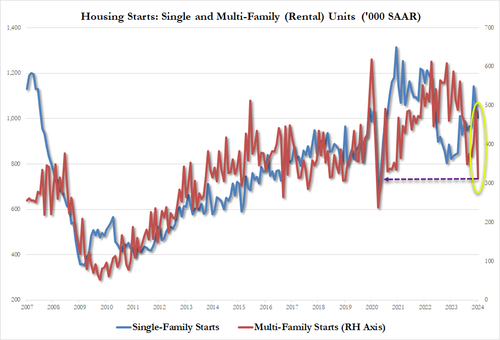

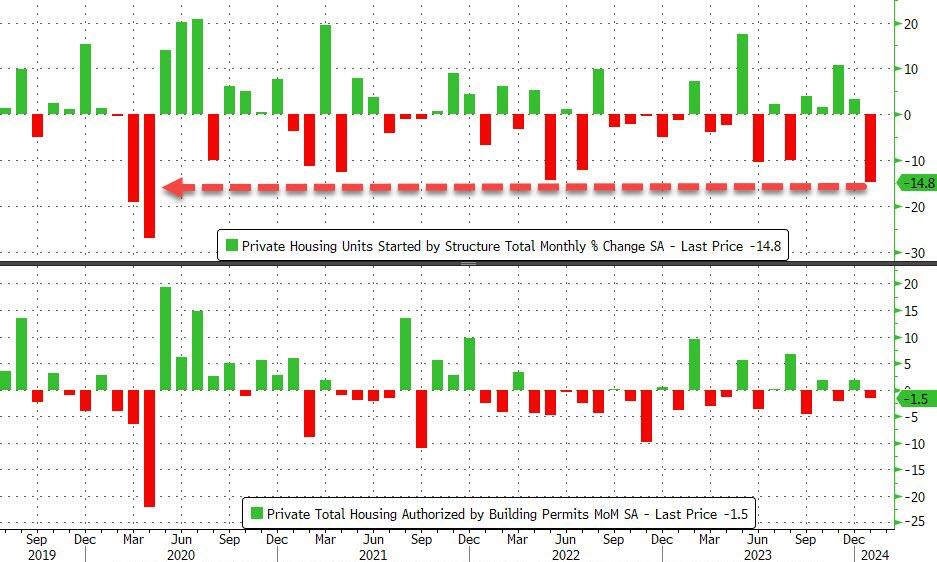

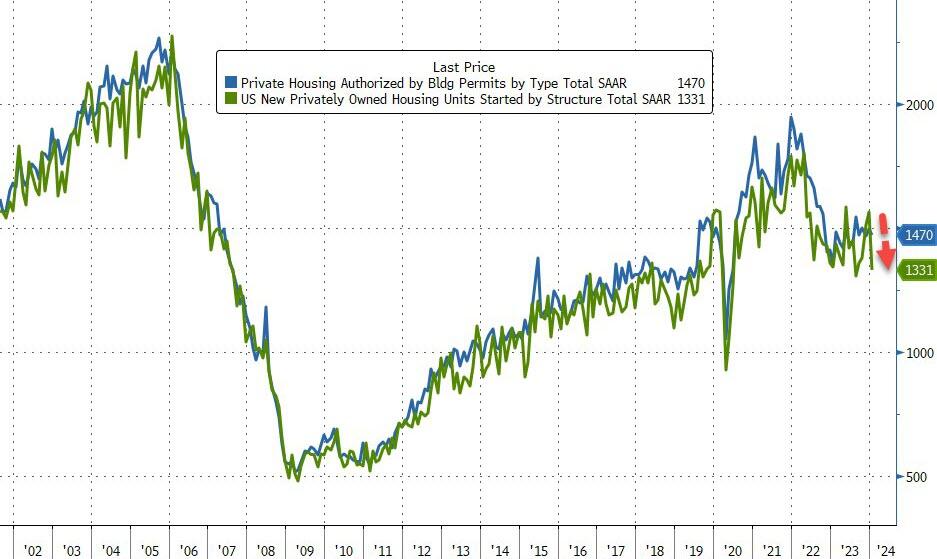

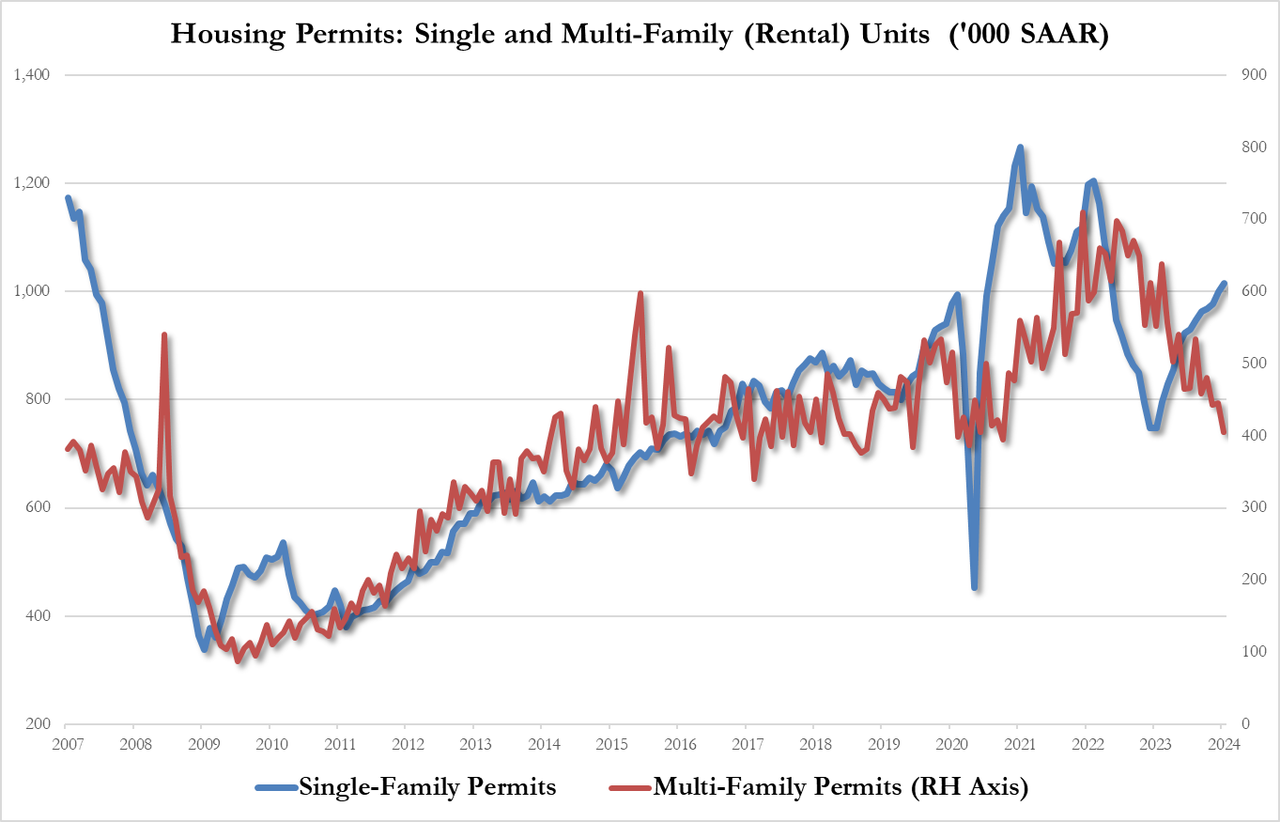

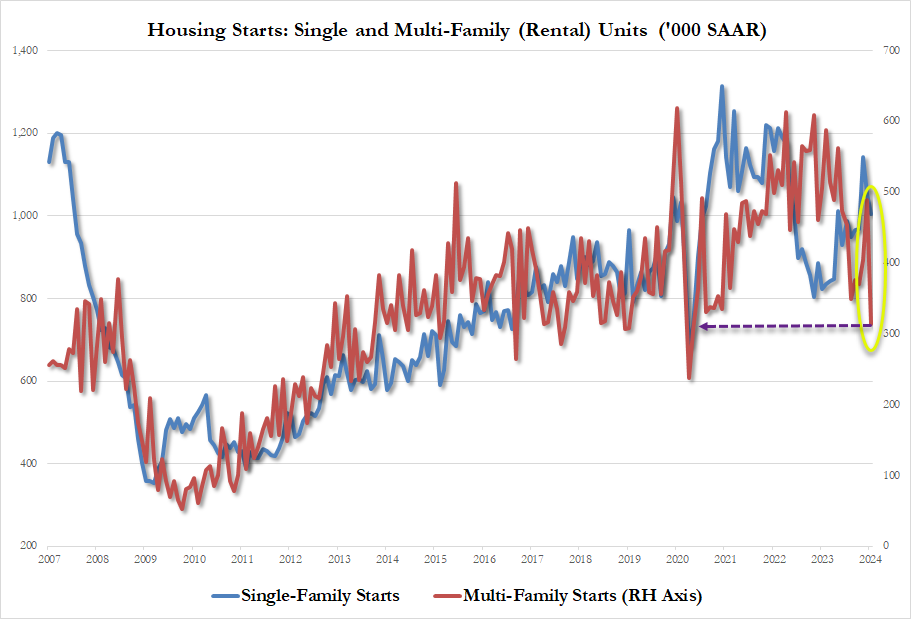

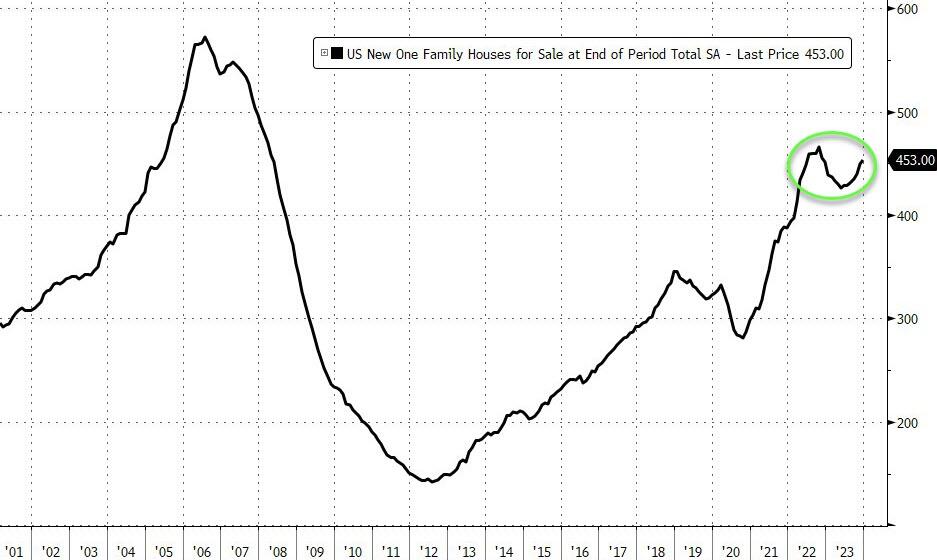

The surge in mortgage rates to over seven percent for the first time since December and rising home prices exacerbate housing affordability challenges, particularly for aspiring homeowners. An integral component of what some consider the “American Dream,” housing affordability is a major factor discouraging Americans. Remember, Bidenomics has seen a 155% increase in mortgage rates.

The euphoria surrounding the January 2024 jobs report is misplaced. Policymakers should heed these warning signs and enact meaningful reforms to address root causes.

Biden’s policy approach undergirds most of these difficulties. Bidenomics focuses on his Build Back Better agenda that picks winners and losers by redistributing taxpayer money for supposed economic gains through large deficit spending (and most of the gains went to political donors).

We haven’t seen an agenda of this magnitude since LBJ’s Great Society in the 1960s or possibly since FDR’s New Deal in the 1930s. Both were damaging, as the Great Society dramatically expanded the size and scope of government, contributing to the Great Inflation in the 1970s, and the New Deal contributed to a longer and harsher Great Depression.

Just since January 2021, Congress passed the following major spending bills upon request of the Biden administration:

- $2 trillion American Rescue Plan Act in March 2021

- $1 trillion Infrastructure Investment and Jobs Act in November 2021

- $280 billion CHIPS and Science Act in August 2022

- $1 trillion Inflation Reduction Act in August 2022

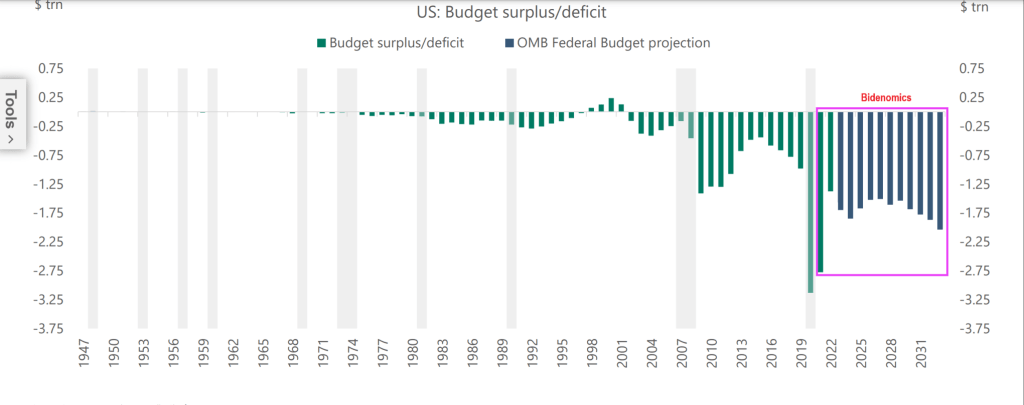

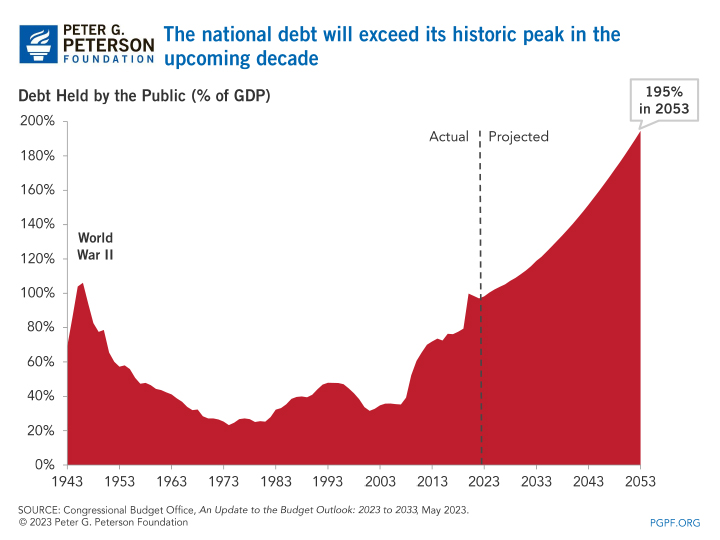

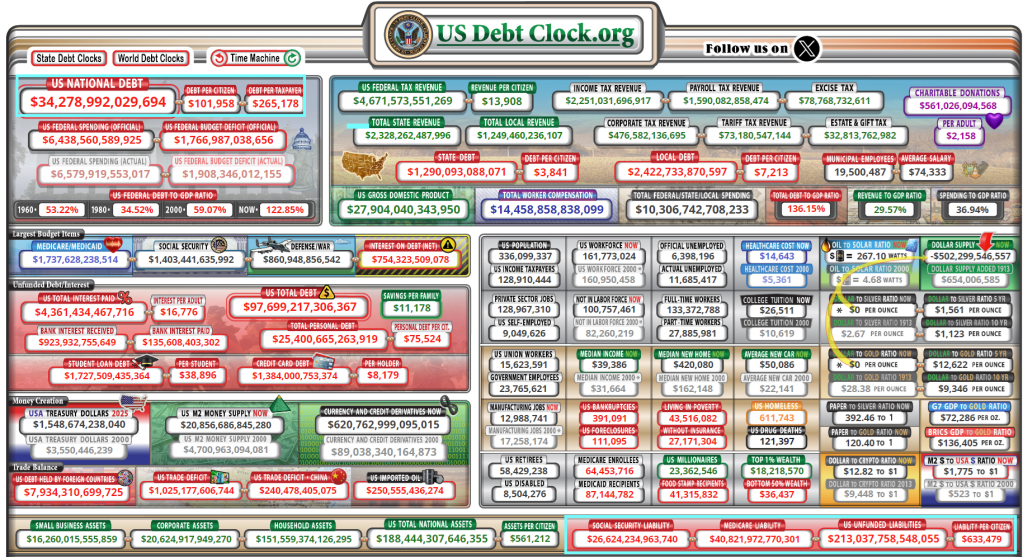

These four bills will add nearly $4.3 trillion to the national debt. But at least another $2.5 trillion will be added to the national debt for student loan forgiveness schemes, SNAP expansions, net interest increases, Ukraine funding, PACT Act, and more. In total over the past three years, excessive spending will lead to more than $7 trillion added to the national debt, which now totals $34 trillion — a 21 percent increase since 2021. There seems to be no end to soaring debt with the recent discussions of more taxpayer money to Ukraine, Israel, the border, and the “bipartisan tax deal,” collectively adding at least another $700 billion to the debt over a decade.

Record debts accrued by households and by the federal government (paid by households) are not signs of a robust economy. This will likely worsen before it improves, as household savings dry up. And with interest rates likely to stay higher for longer because of persistent inflation, debts will crowd out household finances and the federal budget.

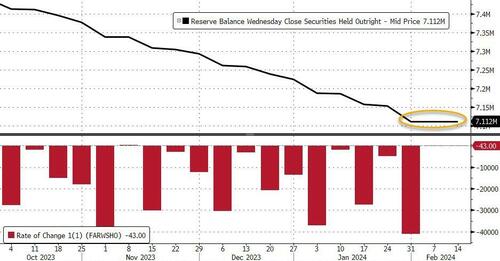

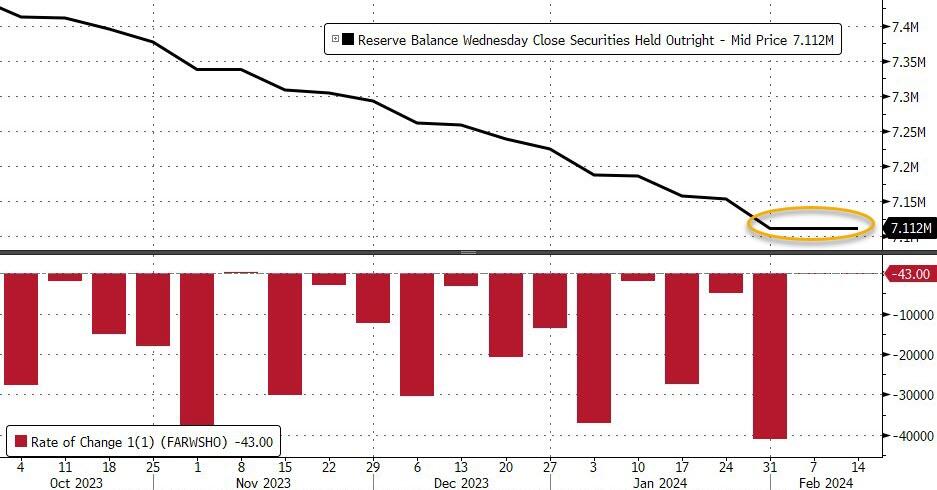

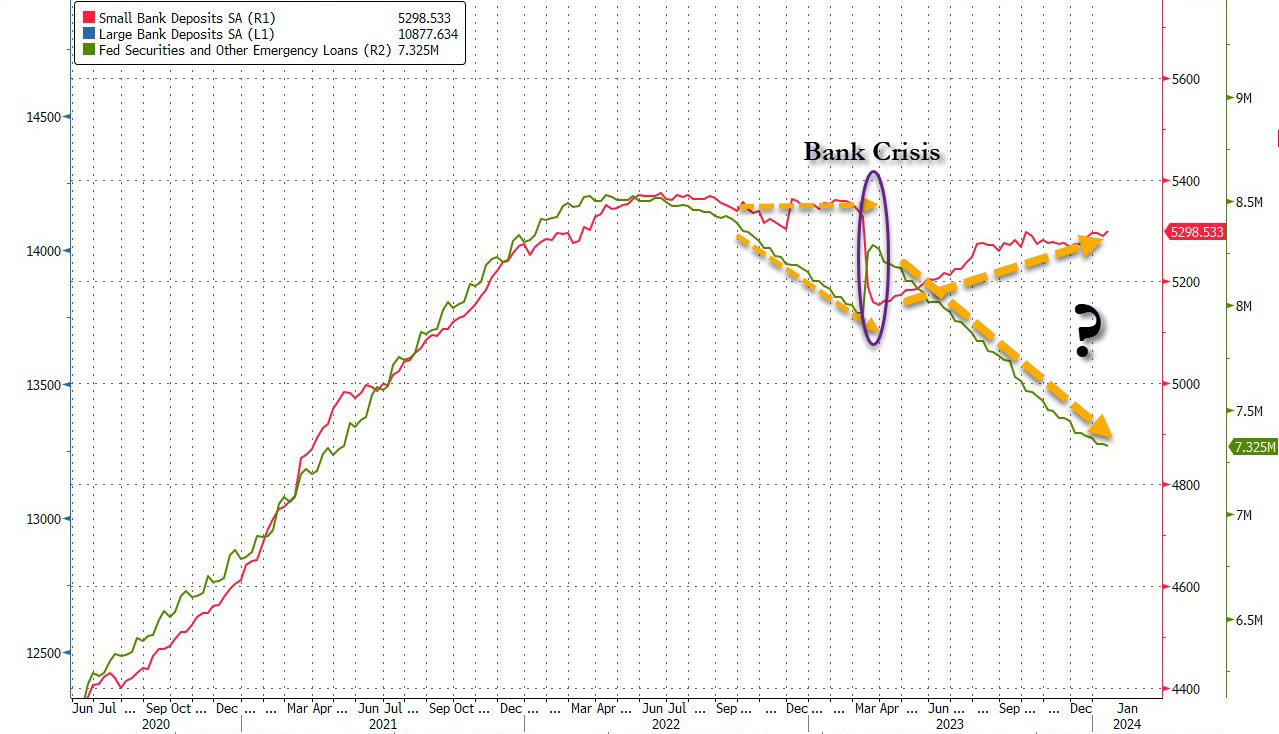

The Federal Reserve has monetized much of this increased national debt over the last few years by ballooning its balance sheet from $4 trillion to $9 trillion and back down to a still-bloated $7.6 trillion. This helps explain persistent inflation, massive misallocation of resources, and costly malinvestments across the economy, keeping the economy afloat yet fragile.

Excessive deficit spending weighs heavily on future generations, saddling them with unsustainable debt levels they have no voice in. Today, everyone owes about $100,000, and taxpayers owe $165,000, toward the national debt. Of course, these amounts don’t include the hundreds of trillions of dollars in unfunded liabilities for the quickly-going-bankruptwelfare programs of Social Security and Medicare.

Future generations will be on the hook for even more national debt if Bidenomics continues and Congress doesn’t reduce government spending now. This is why the national debt is the biggest national crisis for America. We’re robbing current and future generations of their hopes and dreams.

Fortunately, there’s a better path forward if politicians have the willpower. This path should be chosen before we reap the major costs of a bigger crisis. Look at Argentina’s president Javier Milei who managed to balance the budget in 60 days and generate a whopping SURPLUS of $589,000,000. How? By cutting massive government waste and closing agencies and programs.

In short, we need a fiscal rule of a spending limit covering the entire budget based on a maximum rate of population growth plus inflation. There should also be a monetary rule that ideally reduces and caps the Fed’s current balance sheet to at least where it was before the lockdowns. My work with Americans for Tax Reform shows that had the federal government used this spending limit over the last 20 years, the debt would have increased by just $700 billion instead of the actual $20.2 trillion. That’s much more manageable and would point us in a more sustainable fiscal and monetary direction.

Together, fiscal and monetary rules that rein in government will help reduce the roles that politicians and bureaucrats have in our lives so we can achieve our unique American dreams. If not, we will have wasted many dreams on Bidenomics that can make things look good on the surface, but cause rot underneath.

Clarification: When Biden and various members of Congress tout Biden as having created more jobs that previous Presidents, that is the ultimate gaslighting of the American people. Trump actually saw more job creation than Biden until Covid struck and politicians shut down the economy (and schools closed). Then like magic, after Biden was elected, many jobs returned. Biden and his lackies take credit for the incredible job market, but NEW jobs (rather than simply old jobs returning) had nothing to do with Biden’s Keynesian policies. Rather, Biden’s policies have helped destroy the jobs market.

And yes, the US is under invasion by the United Nations who are helping millions of migrants ILLEGALLY cross the US border, creating horrible stress on the economy and helping keep inflation high. Not to mention soaring crime. Its as if Biden (and his master Obama) are using the Cloward-Piven strategy of overwhelming the economy so it breaks.

All we hear about from Biden and Schumer (and their ilk) is about spending billions MORE on Ukraine and their oligarchs to “protect their borders” while Biden and Mayorkas (Cuba Pete) leave American borders over to invasion.

Yes, Democrats like The Clintons, Obamas and Bidens LOVE the Cloward-Piven strategy. Hey, they are all multi-millionaires and are insulated from all the damage they inflict on the middle class and low wage workers.

And by the way, Donald Trump is NOT an isolationist. He is a Jacksonian Nationalist, much reviled by the globalists in Washington DC and the World Economic Forum.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.