Jared Bernstein was VP Joe Biden’s former Chief Economist and is now chair of the United States Council of Economic Advisers. Pretty impressive! Except that Bernstein is not really an economist. He has a PhD in social welfare from Columbia University. In other words, Bernstein is a Progressive Marxist cheerleader, not a real economist. Perfect for The Biden Adminstration where they installed a small town Mayor with no experience (Buttigieg) as Transportation Secretary.

BERNSTEIN: “Yes, it depends on what your benchmark is.”

Bernstein’s answer reminds me of the infamous reply of President Clinton about having sex in the Oval Office with Monica Lewinsky: “It depends on what the definition of sex is.”

Well, Jared, here is the data.

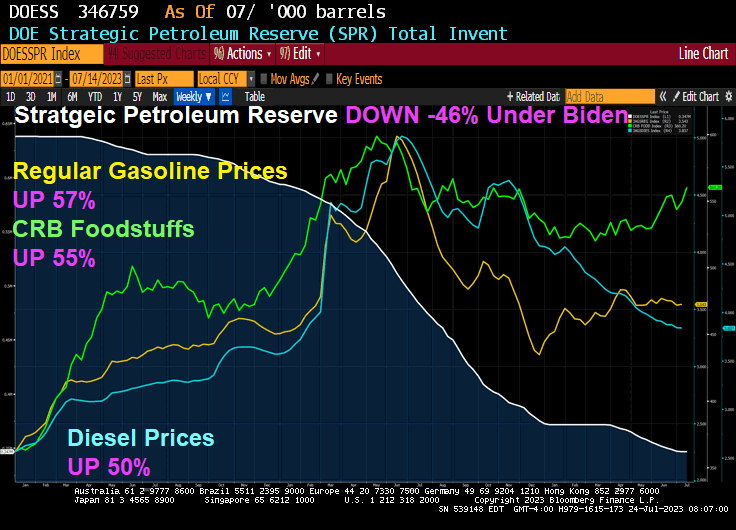

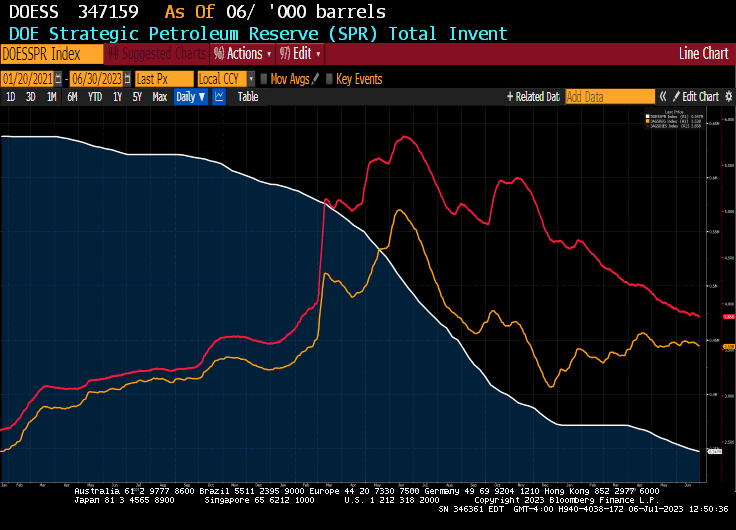

Since January 2021, regular gasoline prices are up 57% under Biden’s and Bernstein’s Reigns of Error. CRB Foodstuffs are up 55% under Clueless Joe and Diesel prices 50% under Bully Biden. Meanwhile, the Strategic Petroleum Reserves is DOWN -46% under Hidin’ Biden.

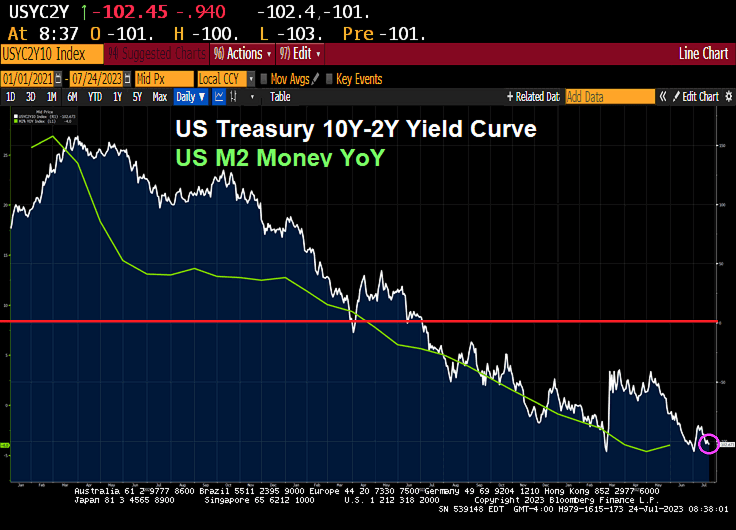

Meanwhile, the US Treasury 10Y-2Y yield curve has inverted to -102.45 as it does prior to a recession. I would love to hear “economist” Jared Bernstein explain that!

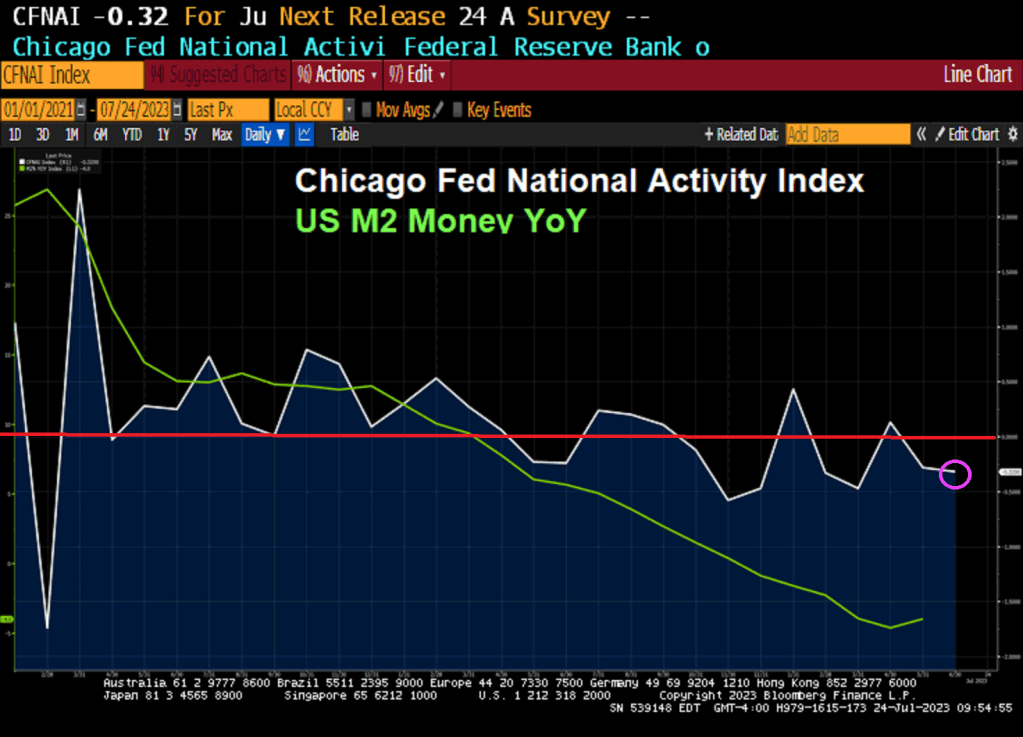

The Chicago Fed’s National Activity index fell to -0.32 in June. That is negative readings for 6 of the last 8 months.

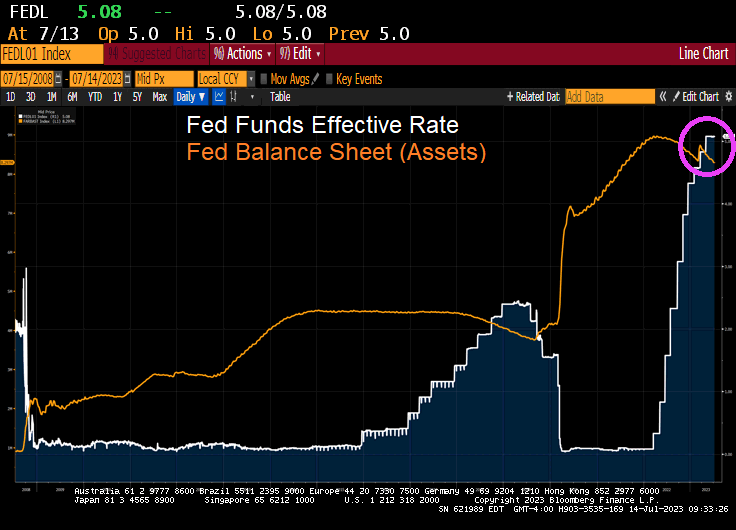

The Fed still hasn’t removed its monetary stimulypto from the market.

When I see the faces of Alan Greenspan, Ben Bernanke, Janet Yellen and Jerome Powell, all I think of is …. the Minsky Moment brigade!

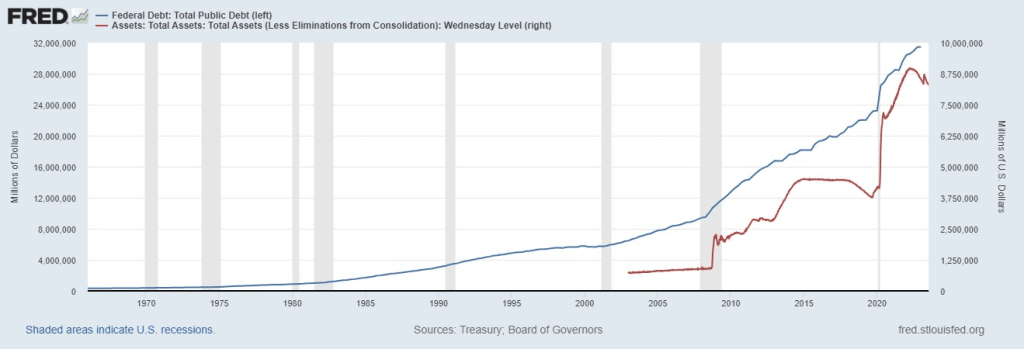

From Zero debt in 1776 to $21 trillion in 1997 and just in the last 4 years, debt has gone up by that same $21 trillion. This graph shows the debt explosion, a 63x increase.

And then we have Congress promising >$192 trillion in entitlements (wealth transfers) that will likley be added to the already >$32 trillion in Federal debt.

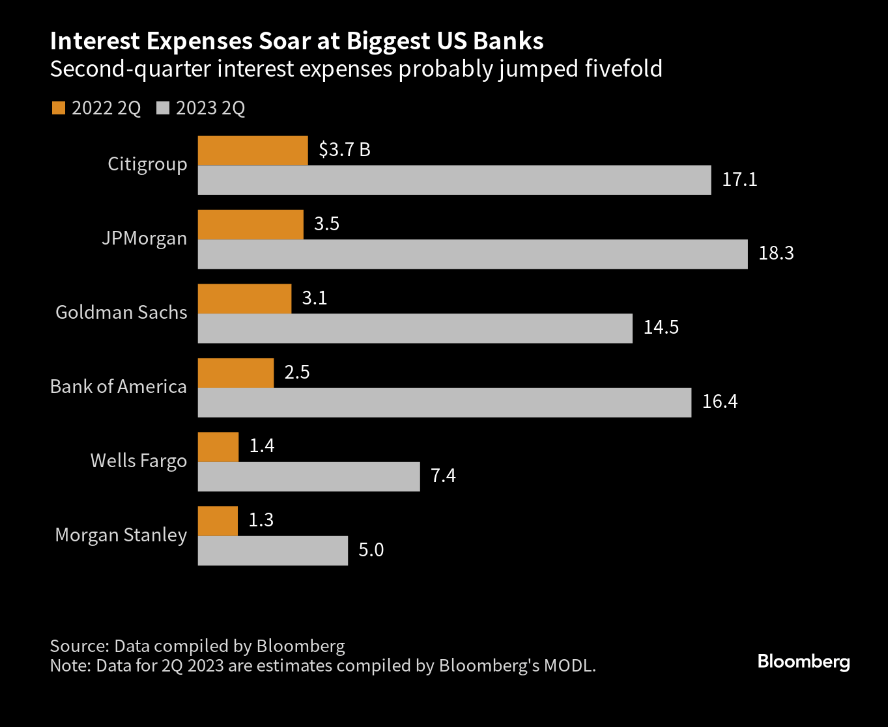

What screams may come! Actually, the aftermath of excessive monetary policies under Bernanke, Yellen and Powell are coming home to bit the big banks.

Interest expenses at big US banks are rising much more quickly than interest income. Across the six largest US banks, interest expenses are set to climb to roughly $78.7 billion from $15.5 billion in the same period last year.

There is still $8.3 Trillion in monetary stimulus sloshing around the monetary system.

Biden’s massive spending spree (aka, Build Back Better) has a new name: Build Back Bankrupt!

According to Epiq, Commercial Chapter 11 Filings Increased 68 Percent in the First Half of 2023.

NEW YORK – July 03, 2023— The 2,973 total commercial Chapter 11 bankruptcies filed during the first six months of 2023 represented a 68 percent increase over the 1,766 filed during the same period in 2022, according to data provided by Epiq Bankruptcy, the leading provider of U.S. bankruptcy filing data. Individual Chapter 13 filings increased by 23 percent during the same period.

Overall commercial filings registered 12,107 for the first half of 2023, representing an 18 percent increase from the commercial filing total of 10,258 for the first half of 2022. Small business filings, captured as Subchapter V elections within Chapter 11, totaled 814 in the first six months of 2023, a 55 percent increase from the 525 elections during the same period in 2022.

Overall commercial filings increased 12 percent in June 2023, as the 2,123 filings were up from the 1,891 commercial filings registered in June 2022. The 404 commercial Chapter 11 filings in June represented a 9 percent increase from the 371 filings in June 2022. Total Subchapter V elections within Chapter 11, experienced a 111 percent increase from 94 in June 2022 to 198 in June 2023.

“The increase in commercial and individual bankruptcy filings during the first half of 2023 underscores the economic challenges faced by businesses and individuals,” said Gregg Morin, Vice President of Business Development and Revenue at Epiq Bankruptcy. “Our objective is to provide bankruptcy professionals with timely and accurate data necessary for analyzing stakeholder volumes and trends for making informed business decisions.”

Total bankruptcy filings were 217,420 during the first six months of 2023, a 17 percent increase from the 185,352 total filings during the same period a year ago. Total individual filings also registered a 17 percent increase, as the 205,313 filings during the first half of 2023 were up from the 175,094 filings during the first six months of 2022. The 85,390 individual Chapter 13 filings in the first half of 2023 represent a 23 percent increase over the 69,367 filings during the same period in 2022.

All chapters increased in June 2023 compared to June 2022, with 37,700 total bankruptcy filings representing an increase of 17 percent from the 32,198 filed in 2022. Total commercial filings were up 12 percent from 1,891. Total Individuals were up 18 percent from 30,307.

While not the Epiq data, the Bloomberg Corp Bankruptcy Index shows the rise in bankruptcies as The Fed fights Bidenflation.

What is Bidenomics? It isn’t what Press Secretary Karine Jean Pierre thinks. She said Biden hates “trick down economics”. Instead, Biden prefers a Soviet-style command economy where The Federal Government spends trillions of dollars and directs where the money goes. We also have the Socialist Federal Reserve that relies on rate manipulation to achieve policy results.

A good example of Biden’s Soviet-style “Bidenomics” is his use of the Strategic Petroleum Reserve (SPR). Biden has now drained almost 50% of the SPR from when he was sworn in as President. And has drained the SPR for 14 straigth weeks to manipulate gasoline and diesel fuel prices in an effort to lower fuel prices ahead of the 2024 Presidential election. Watch Biden suddenly stop caring about fuel prices once he wins reelection!

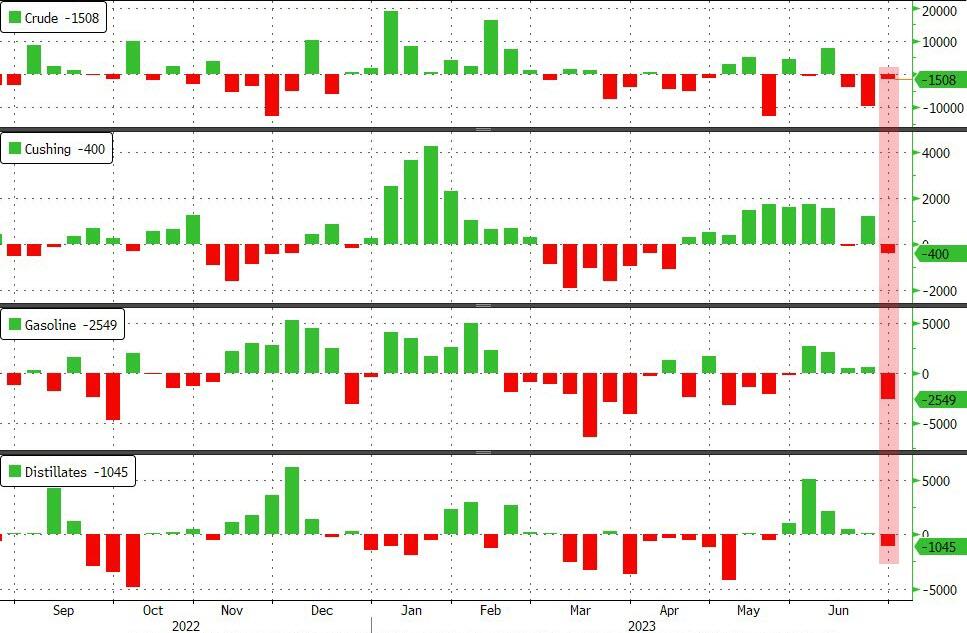

After last week’s huge draw, expectations were for a smaller draw (which API showed last night), but the actual crude draw was smaller – just 1.5mm barrels. Stocks at the Cushing hub fell 400k barrels and products also saw notable draws..

At least we now know who left cocaine in the White House!

The good news (if true)? ADP announced that 497k jobs were added in June.

The bad news? A 497k print on jobs (many seasonal, it is summer!) almost guarantees that The FOMC (Fed Open Market Committe) will raises rates again at at the July meeting.

The 2-year Treasury yield is up over 10 basis points.

The 2-year Treasury yield is up 16.5 basis points.

Bticoin Cash is up 10% today.

I should have bought nickel!

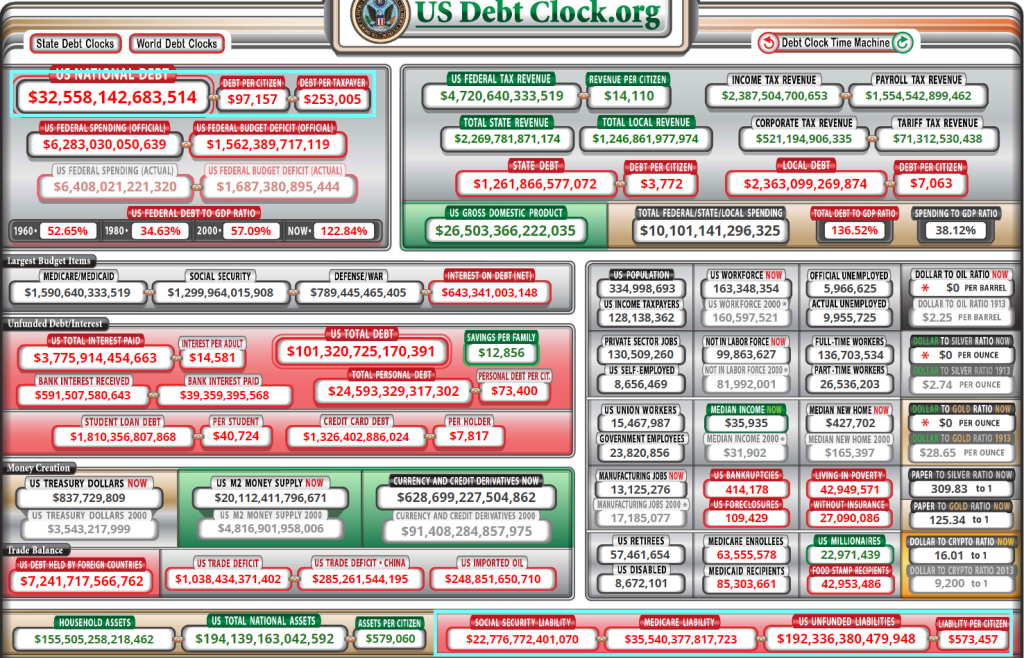

Why is Biden sending Treasury Secretary Janet “The Marxist Midget” Yellen to China? A Treasury Secretary and former Federal Reserve Chair? Likely trying to convince China that our $32 TRILLLION AND GROWING national debt is not a problem, since China is the third largest holder of US Treasury debt (after The Fed and Japan). Note that China has decreased its holdings of US Treasuries by -25.6% since January 2018.

Hopefully, Yellen isn’t acting as a bag man for The Biden Crime Family. 10% for The Big Guy?? How much does Yellen get??

The Federal Home Loan Bank system (aka, FLUBs), a relic of FDR and The Great Depression, subsidizes banks, not individuals. Much like its twin sibling, The Federal Reserve system, it is a Socialist institution that rely of manipulation rather than free markets.

The first sign of deep trouble in US banking this year came from a sunbaked office complex in a San Diego suburb. There, a small firm called Silvergate Capital Corp. assured investors it was weathering a run on deposits. Its lifeline: about $4.3 billion from a Federal Home Loan Bank.

Heads turned across the financial industry.

Silvergate didn’t have a network of branches serving consumers, and it barely offered mortgages. It specialized in moving dollars for cryptocurrency ventures.

Soon it became apparent that a roster of troubled regional banks was leaning on FHLBs — a relic of the Great Depression originally aimed at ensuring financial firms have cash to lend to homebuyers. Yet the banks had little to do with everyday mortgage lending.

Silicon Valley Bank, catering to venture capitalists and tech startups, said it held $15 billion from an FHLB at the end of 2022. Signature Bank, with clients including crypto platforms, had $11 billion. And by April, First Republic Bank, offering mortgages to millionaires on unusually sweet terms, ended up with more than $28 billion. All four banks collapsed.

For many, that was a crystallizing moment for the 90-year-old Federal Home Loan Bank system, which has ballooned to more than $1.5 trillion while playing a growing role as a backstop for banks taking all kinds of risks — and a diminishing role in funding new mortgages. That’s raising questions about the purpose of FHLBs and why the private institutions enjoy so much government support.

As Milton Friedman once said, “Nothing is so permanent as a temporary government program.”

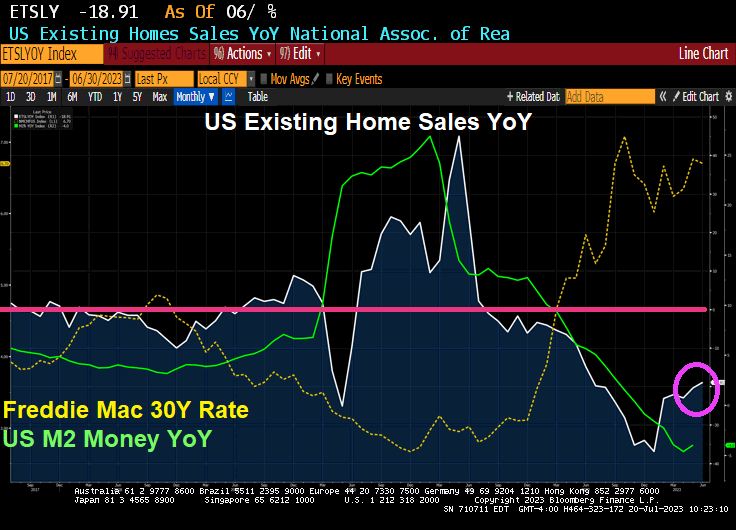

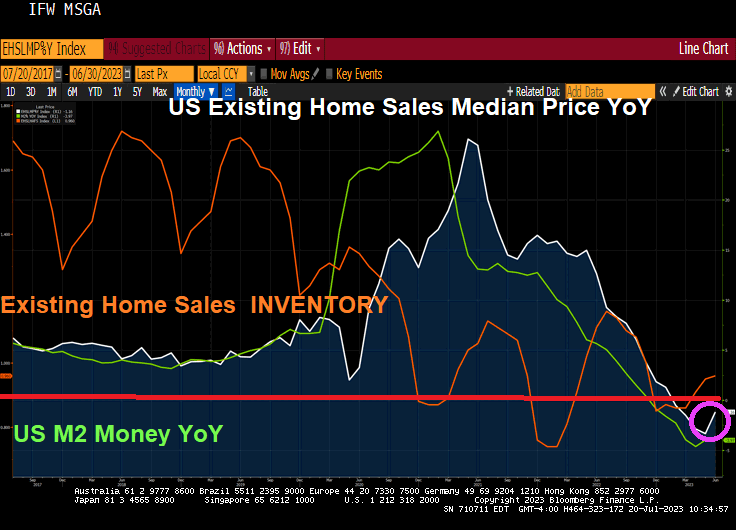

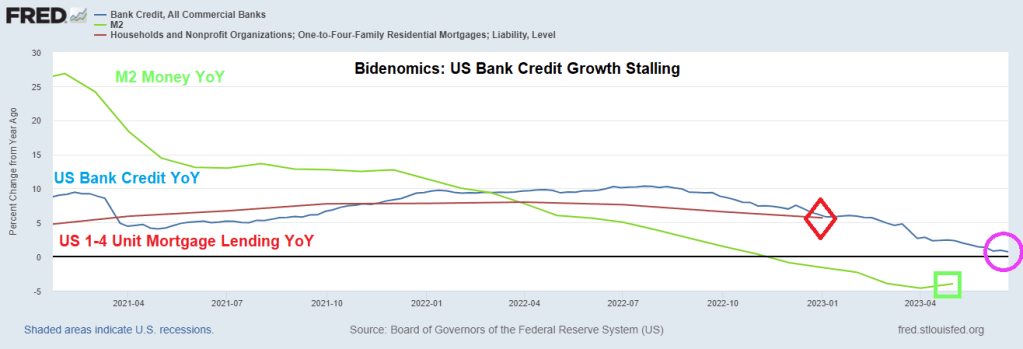

Of course, rate increases are crushing regional banks as well as the middle class. But as M2 Money growth crashes, home price growth is slowing into negative territory.

Bidenomics is based on massive Federal spending and massive Fed monetary stimulus. But like all stimulus, it wears off. Such is the case with bank lending as The Fed raises interest rates.

US bank credit year-over-year (YoY) has stalled to a lowly 0.7% rate as M2 Money growth YoY increases slightly to -4%.

Its figures. With the Socialist Federal Reserve manipulating interest rates and Biden/Congress spending like drunken sailors trying to manipuate economic growth, it makes sense that Biden wants to explore Bill Gate’s idiotic idea of blotting out the sun to prevent global warming.

Of course, Biden can hide at any of his 4 mansions and wear his Ray-ban Aviators to avoid the horror of his policies.

Jay Leno once quipped about the Obama meal. “Order anything you want and hand the bill to the person standing behind you.” Biden, like his boss Obama, is praciticing a similar strategy. Spend like a drunken sailor and just keep borrowing until the whole thing breaks.

The barrage of fresh Treasury bills poised to hit the market over the next few months is merely a prelude of what’s yet to come: a wave of longer-term debt sales that’s seen driving bond yields even higher.

Sales of government notes and bonds are set to begin rising in August, with net new issuance estimated to top $1 trillion in 2023 and nearly double next year to fund a widening deficit. The Treasury is already in the middle of an estimated $1 trillion bump in bills as it seeks to replenish its cash coffers in the wake of the debt-limit deal.

It’s an explosive mix for borrowing costs as debt sales are swelling and the Federal Reserve continues to reduce its balance sheet at a time when traditional buyers of Treasuries overseas are discouraged by currency hedging costs.

“A worsening fiscal profile, amid fairly modest spending cuts, suggests that the upcoming supply deluge will not be limited to T-bills,” wrote Anshul Pradhan, head of US rates strategy at Barclays Plc. “The Treasury will soon need to increase auction sizes meaningfully across the curve. We believe the rates market is too complacent.”

Barclays strategists predict the net rise in coupon-bearing debt from August to year-end will be nearly $600 billion. And that would only ramp up in 2024, they say, with an annual figure of $1.7 trillion. That would be nearly double this year’s expected debt issuance.

Pradhan says he doesn’t think the market appreciates the increase in issuance that’s going to be needed due to wide budget deficits and the fact the Treasury won’t want bills to become a substantial share of the total debt.

Total net new bill sales are set to bring their share of US debt to about 20%, according to JPMorgan Chase & Co. The issuance would hit a threshold seen by the Treasury Borrowing Advisory Committee as the upper limit for the US to fund deficits at the least possible cost to taxpayers.

Bank of America Corp. says the supply deluge could result in a “demand vacuum” for longer maturity bonds that could push yields higher and tighten financial conditions.

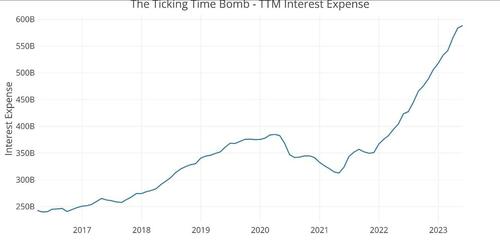

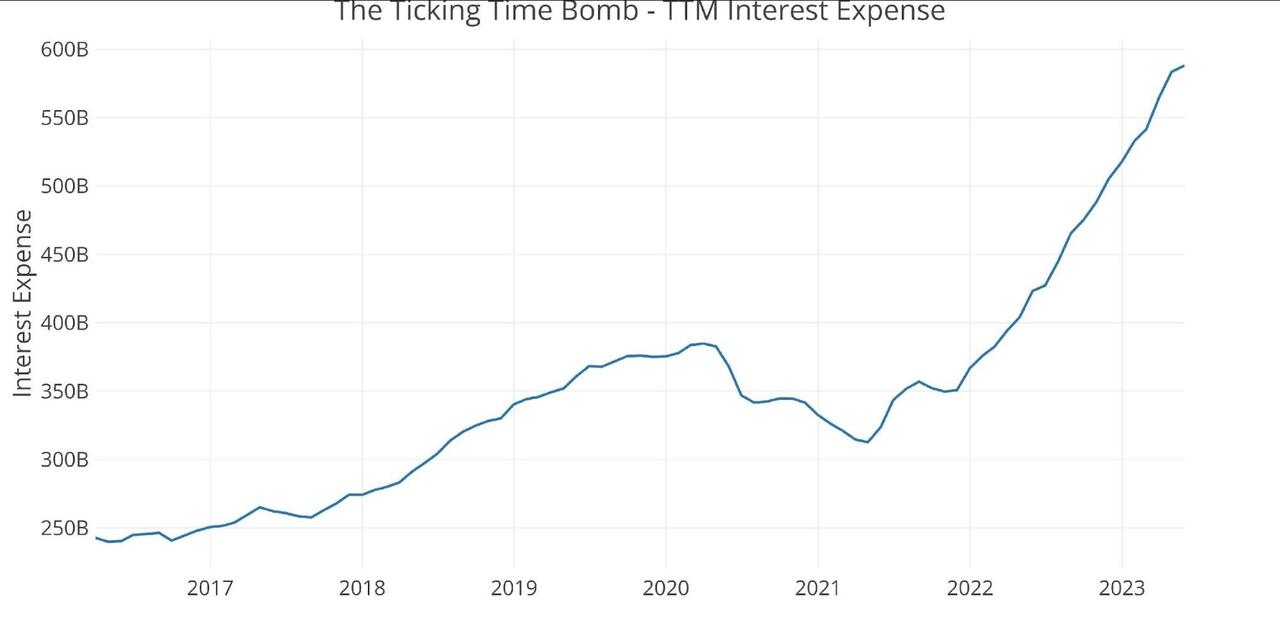

The problem isn’t purely a function of more debt. The bigger issue is that this new debt comes with a much steeper price tag. Interest on the national debt is rising at an alarming clip.

The trailing 12-month (TTM) interest on the debt clocked in at just under $600 billion in May. This was up from $350 billion at the start of 2022, less than 18 months ago. The government has added an extra $250 billion in expenses per year on just debt service.

This is just the beginning of an upward trend. Based on the current interest payments, the Treasury is paying less than 2% interest on the total debt. But a lot of the debt currently on the books was financed at very low rates before the Federal Reserve started its hiking cycle. Every month, some of that super-low-yielding paper matures and has to be replaced by bills, notes and bonds yielding much higher rates. That means interest payments will quickly climb much higher unless rates fall.

Looking at the Treasury sale on June 26 reveals the extent of the problem. The Treasury sold $162 billion in securities, with $120 billion in short-term Treasury bills with high yields.

$58 billion in six-month bills at an investment yield of 5.45%

$62 billion in three-month bills at an investment yield of 5.34%.

$42 billion in two-year notes at a high yield of 4.67%, amid very strong demand. Longer-term yields are still far below short-term yields.

With this flood of Treasury bills, the share of short-term paper underpinning the debt is approaching 20%. That’s considered the upper limit, meaning the Treasury will soon have to turn to issuing longer-term notes and bonds. That means the Treasury will be locking in higher interest rates for the long term.

{kind=link}

You must be logged in to post a comment.