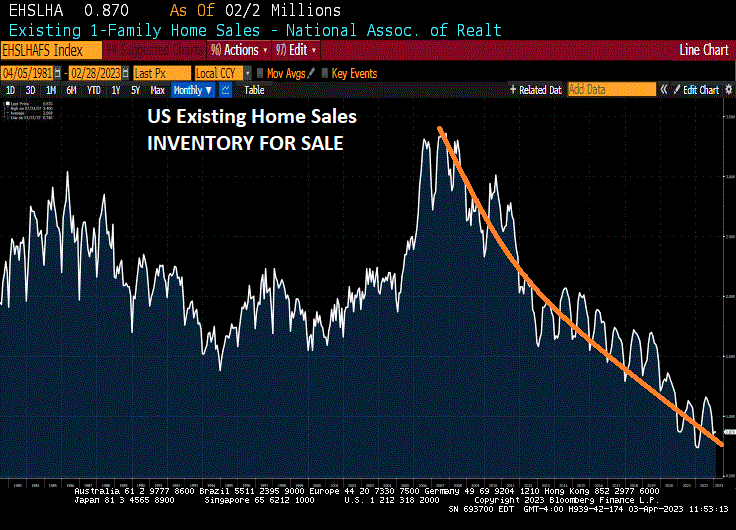

It’s only mid April and mortgage demand should be approaching it’s yearly high. But under Biden and The Fed, mortgage demand seems to have peaked earlier than normal. It’s already late in mortgage cycle.

Mortgage applications decreased 8.8 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending April 14, 2023.

The Market Composite Index, a measure of mortgage loan application volume, decreased 8.8 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index decreased 8 percent compared with the previous week. The Refinance Index decreased 6 percent from the previous week and was 56 percent lower than the same week one year ago. The seasonally adjusted Purchase Index decreased 10 percent from one week earlier. The unadjusted Purchase Index decreased 9 percent compared with the previous week and was 36 percent lower than the same week one year ago.

Joe Biden loves to brag about “his” great economic successes, particulary in jobs added. But the jobs added in March were not in higher-paying factory jobs, but Biden’s building from the bottom-up approach is mostly low-paying leisure and hospitality jobs.

And here is the rub on wages. Average hourly earnings growth fell to 4.2% YoY, too bad inflation is 6% and expected to rise with the summer.

236k jobs added in March, down from a revised 326k jobs added in February. The unemployment rate fell to 3.5% and labor force participation rose slightly to 62.6%.

Talk about an economy that seems dependent on Federal government money printing. The US economy seems hopelessly addicted to gov money printing.

Today, US job openings fell in February to 9,931k. While that is still a large number, look at the chart of job openings and M2 Money printing. There is a one year lag between maximum printing and job openings. But M2 Money growth has collapsed.

Silicon Valley Bank’s blunders were encouraged by US regulation, went untested by the Federal Reserve and were “hiding in plain sight” until Wall Street and depositors grew alarmed.

That’s JPMorgan Chase & Co. Chief Executive Officer Jamie Dimon’s assessment of the US banking crisis that sent markets careening last month, an episode he predicts is “not yet over” and will be felt for years. He said US authorities shouldn’t “overreact” with more rules.

In his wide-ranging annual letter to shareholders on Tuesday, Dimon described his firm’s aspirations for using artificial intelligence and ChatGPT, weighed in on geopolitics, and provided updates on JPMorgan’s activities in Ohio. This time, many of his sharpest remarks ripped at regulation, including capital rules that pushed banks to binge on low-interest assets that lost value as interest rates shot up.

“Ironically, banks were incented to own very safe government securities because they were considered highly liquid by regulators and carried very low capital requirements,” Dimon said. “Even worse,” he added, the Federal Reserve didn’t stress-test banks on what would happen as rates jumped.

When Silicon Valley Bank’s uninsured depositors realized it was losing money selling securities to keep up with withdrawal requests, they raced to pull their cash. Regulators then intervened and seized it.

Yes. Banking regulators were so focused on credit-exposure of banks (remember the subprime crisis of 2008?) that they really screwed up by having banks load-up on low credit-risk assets that usually have interest rate risk associated with them like Treasuries and mortgage-backed securities (MBS). What could go wrong?

What went wrong was that interest rates rose and unrealized losses on Treasuries and Agency MBS exploded.

Here is a chart of urealized losses on investment securities that banks have accumulated.

Apparently, The Fed and FDIC (and the myriad of Federal and State regulators) sit high on a mountain top and ignore interest rate risk.

While Resident Biden is on good terms with the Mexican drug and sex trafficing cartels that control our southern border, the oil cartel just stuck their fingers in Biden’s eyes by cutting oil productions. Riyadh, Saudi Arabia was irritated last week that the Biden administration publicly ruled out new crude purchases to replenish SPR

Cartel removes more than 1 million barrels a day from market

Analysts say the decline in oil inventories will accelerate

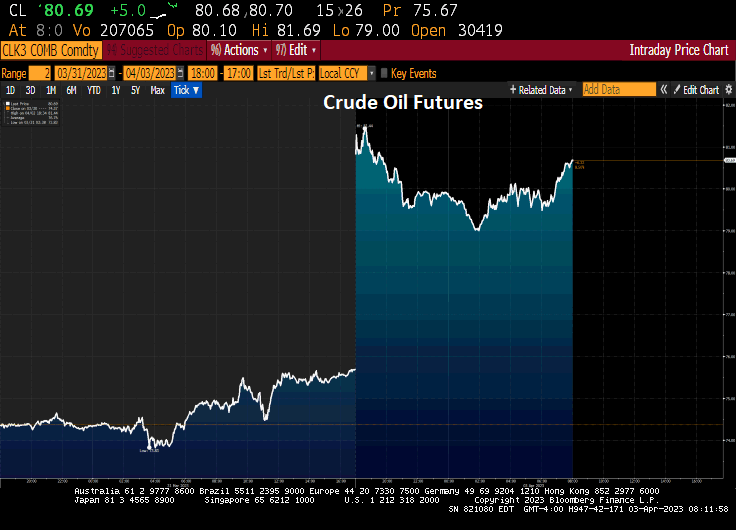

Today, crude oil futures are up 6.62% to over $80 per barrel.

Sunday’s surprise OPEC+ production cuts have redefined the outlook for crude prices, bringing $100 a barrel back into the frame.

Prior to the announcement, the cartel’s own numbers suggested the group would need to pump more oil, not less, in the second half. With the International Energy Agency expecting a demand surge later this year, there’s now renewed risk of a fresh inflationary impetus for the global economy.

Under Biden’s Reign of Error, diesel prices are up 64% while the Strategic Petroleum Reserves (SPR) have been drained by -42%.

St. Benedict, help protect us from Biden and The Federal Reserve.

Well, the University of Michigan consumer sentiment indices are out for March … and they are ugly.

As a baseline, consumer confidence in February 2020 (just before Covid) was 101. After Covid and massive Fed stimulus and Federal government spending spree, consumer confidence in March fell to 62.0, a far cry from 101 under Trump.

Even worse, the UMich buying conditions for housing hit 142 in February 2020 but has declined to 47 in March 2023.

Why would ANYONE have confidence in the US economy under a complete fool with dementia like “China Joe” Biden??

Consumer considence (according to the Conference Board) remains below pre-Covid levels despite the massive Federal spending spree and Fed money printing).

You must be logged in to post a comment.