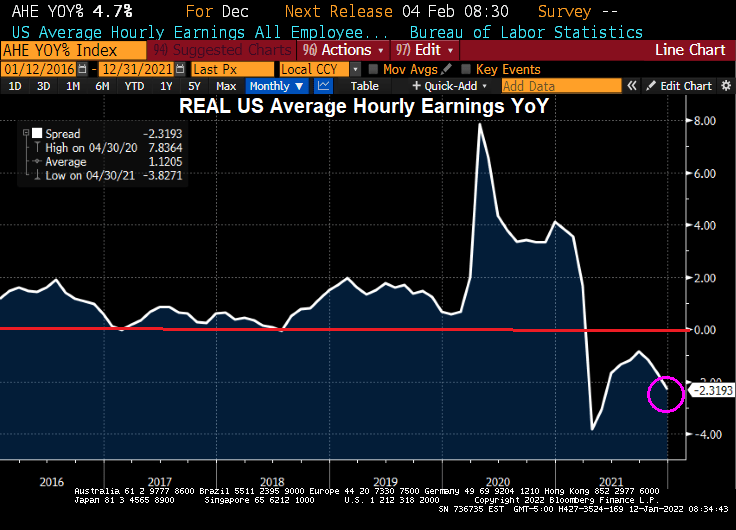

Well, the COVID hysteria from the Biden Administration and the media preparing us for a horrible jobs report was … incorrect. In fact, the January jobs report was “exceptional”. 467,000 jobs were added and average hourly earnings growth ROSE to 5.7% YoY.

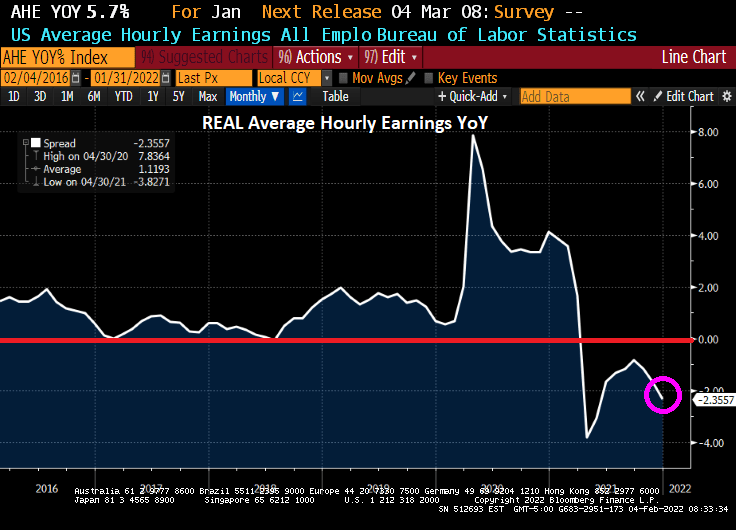

The bad news? Thanks to surging inflation, REAL average hourly earnings growth YoY FELL to -2.36%.

Unemployment ROSE to 4.0% from 3.9% as more people dropped out of the labor force in January. On the bright side, labor force participation rate rose to 62.2% from 61.9%.

Leisure and hospitality employment (one of the most vulnerable to inflation) expanded by 151,000 in January, reflecting job gains in food services and drinking places (+108,000) and in the accommodation industry (+23,000).

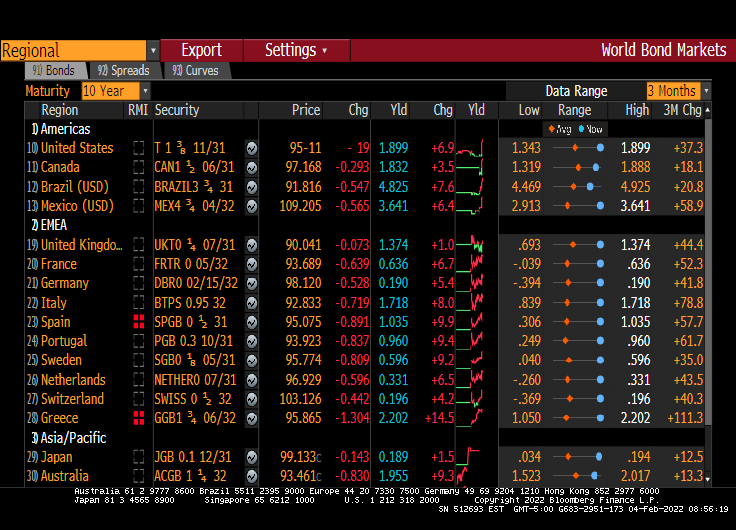

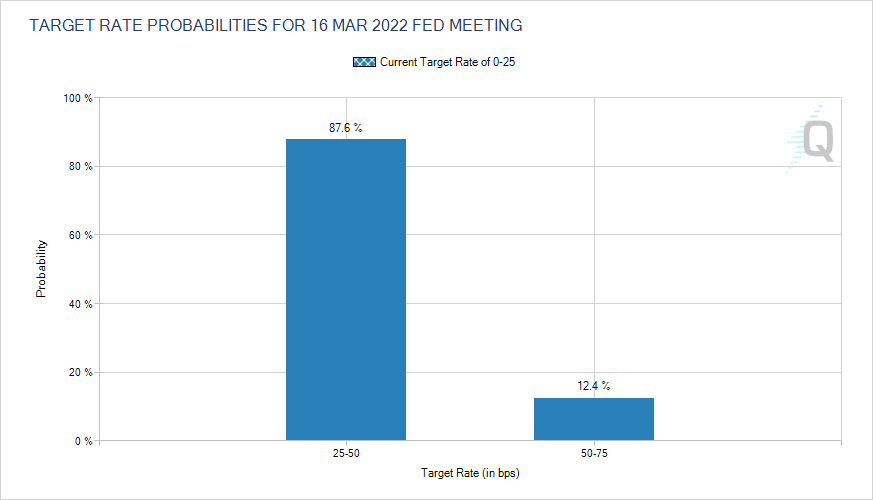

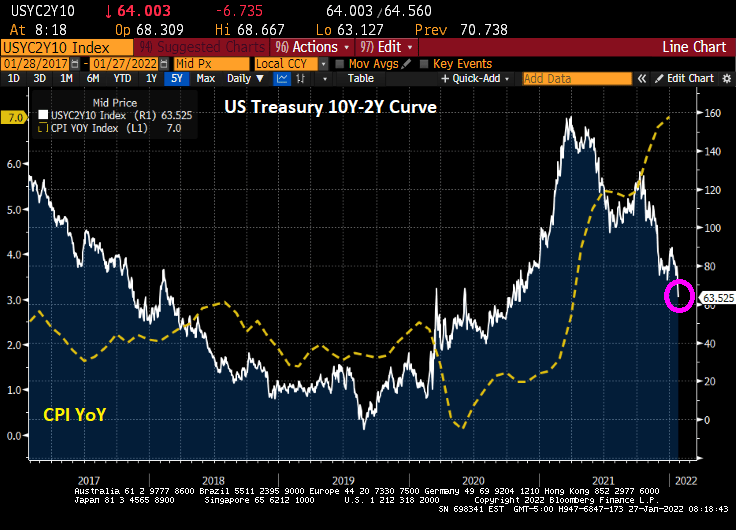

The reaction in the bond market? US 10-year yields are up 6.9 basis points as Eurozone is up across the board.

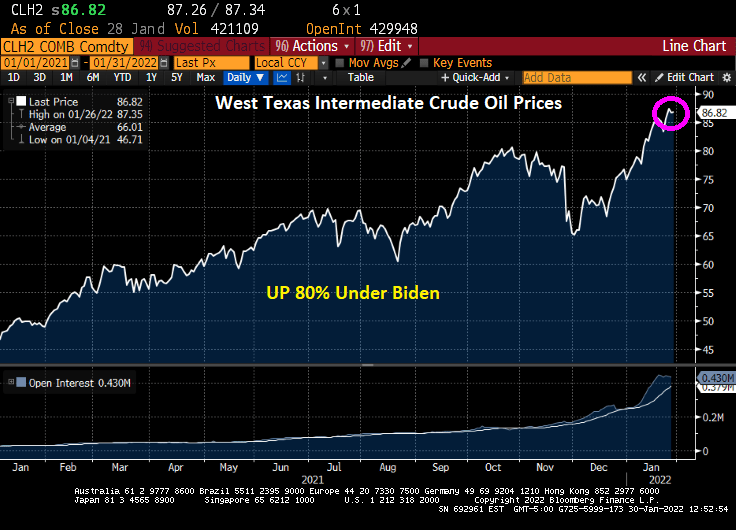

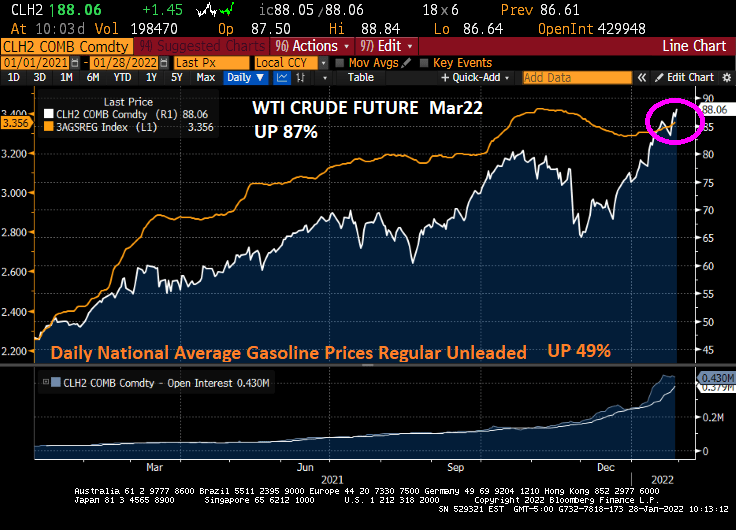

Energy prices are up (except natural gas futures).

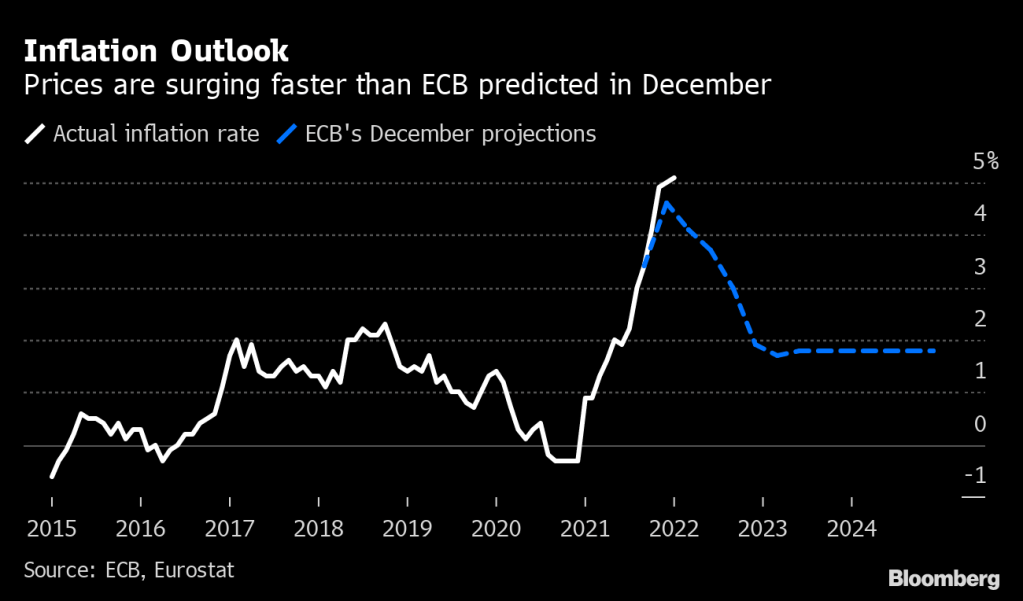

Another day in inflationville.

You must be logged in to post a comment.