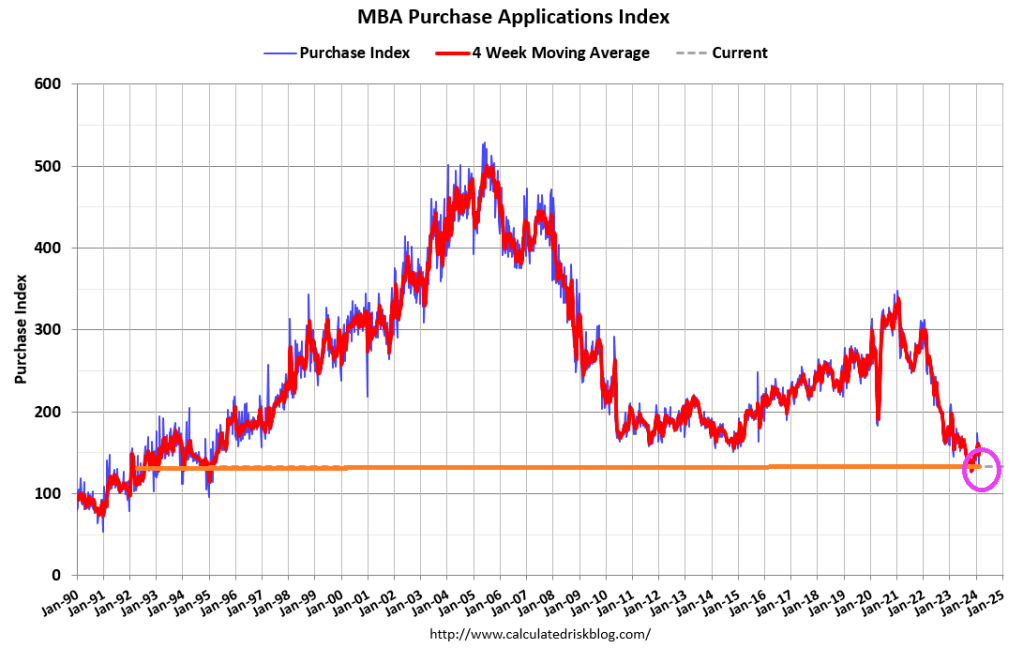

Mortgage applications decreased 10.6 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending February 16, 2024.

The Market Composite Index, a measure of mortgage loan application volume, decreased 10.6 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index decreased 8 percent compared with the previous week. The seasonally adjusted Purchase Index decreased 10 percent from one week earlier. The unadjusted Purchase Index decreased 6 percent compared with the previous week and was13 percent lower than the same week one year ago.

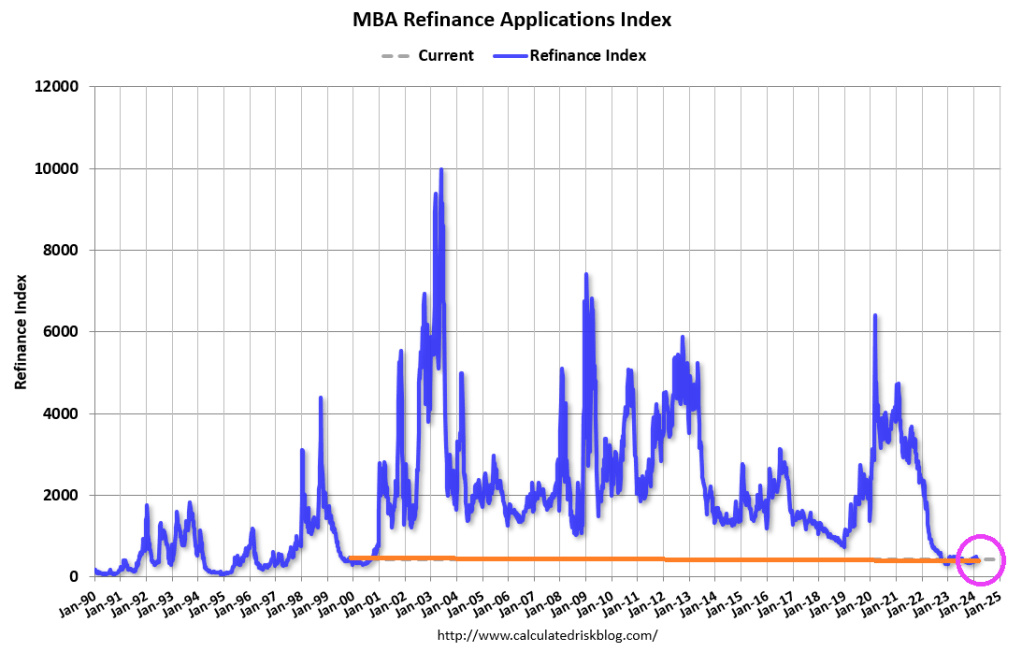

The Refinance Index decreased 11 percent from the previous week and was 0.1 percent higher than the same week one year ago.

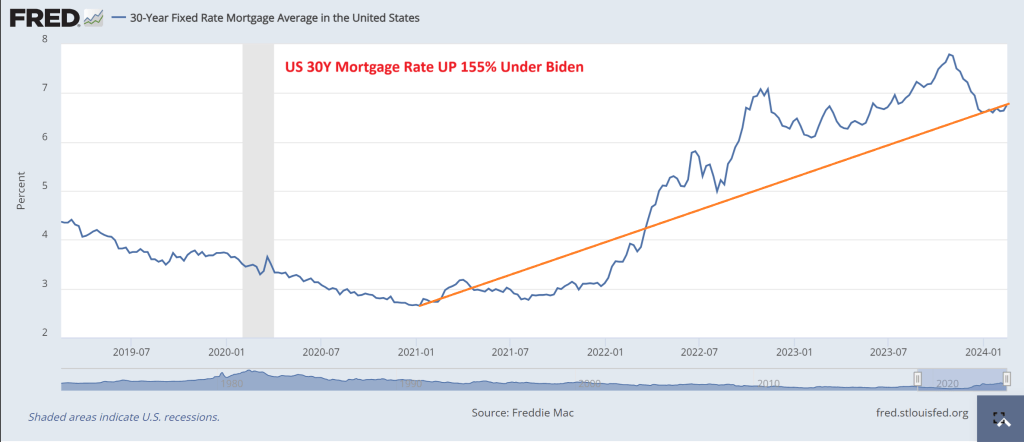

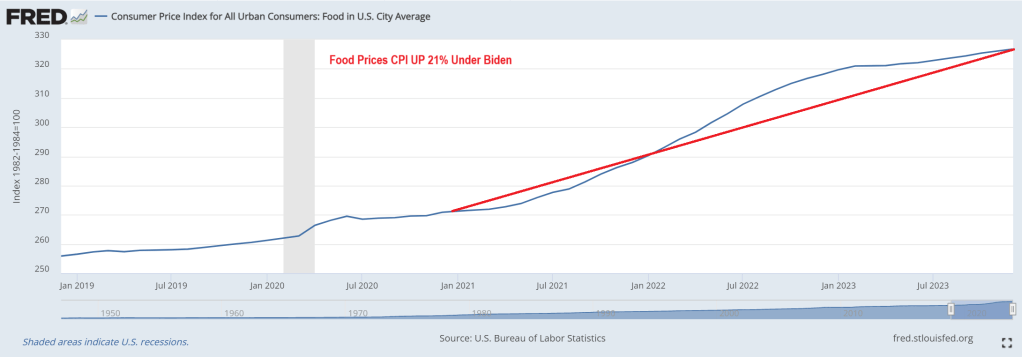

One reason why mortgage demand is so low is that mortgage rates are up 155% under Biden.

Is it sundown for the US mortgage market? And when will it improve?? Probably won’t improve in New York City after Judge Engmoron’s idiotic fine of Donald Trump and family for non-crimes.

When Arnold Schwarzenegger was Governor California, his budget chief, a former high school pal of mine, called me to look at California’s budget. He sent me his spreadsheets with forecasts and asked me what I thought. Even back then, I called back and said “California is on an unsustainable fiscal path and seems to be committing suicide.” He agreed, but noted that Schwarzenegger would not like that conclusion. I told him to blame me for the report, as an unpaid consultant to The Golden State. But even back then, I could foresee the absolute mess that the California State legislature would make, particularly if they elected a Democrat governor.

California’s budget deficits look a lot like Biden’s (call him Newsom’s elderly intellectual grandpa) budget deficits where Biden and Congress went on a spending spree from “the honey pot” (US Treasury) and borrowed funds.

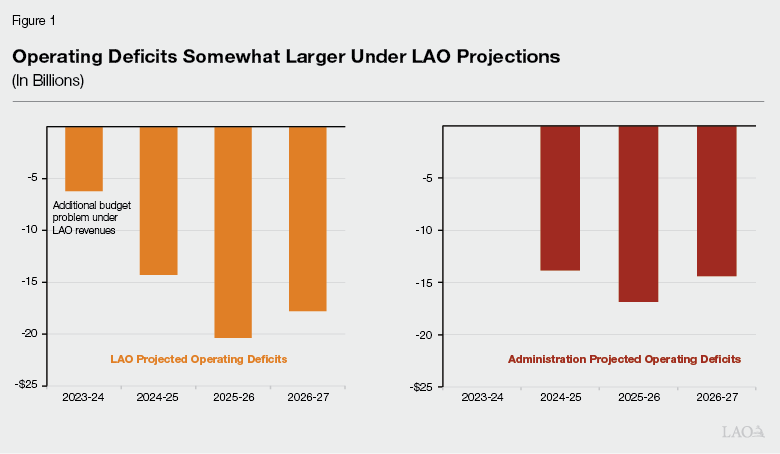

California’s budget crisis is projected to expand more than previously thought and could hit a record deficit of $73 billion, according to a new report from the state’s nonpartisan Legislative Analyst’s Office (LAO).Her

“The actual increase in the state’s budget problem will depend on a number of factors, including formula-driven spending changes, most notably Proposition 98 spending requirements for schools and community colleges,” the report said.

H.D. Palmer, the deputy director of the California Department of Finance and Newom’s spokesperson on budget matters, responded to the new LAO report by telling Fox News Digital that their budget shortfall differs from the $38 million they estimate.

“From now through April, more than $51 billion in income and corporate tax receipts are forecast to come in,” Palmer said. “No one can say today with certainty how those numbers may change the budget estimate of a $38 billion shortfall.”

“A responsible step would be for the Legislature to act now on the early action budget measures needed for $8 billion in solutions to help close this gap,” he added.

The projected bad news comes as Newsom has worked to increase his profile nationwide. It also occurred as California experienced a mass exodus.

California saw its first-ever population decline in 2020 when the state imposed rigid lockdowns during the COVID-19 pandemic. From January 2020 to July 2022, the state lost well over half a million people, with the number of residents leaving surpassing those moving in by almost 700,000.

Census data has shown that Texas is the most popular destination for residents fleeing the state, followed by Arizona, Florida, and Washington. (Of course, Arizona where I used to live has flipped from a Red state to a Blue state with immigration and Democrats are working hard to flip Texas to a Blue state. Washington, has already flipped Blue. Florida remains a Red state under Ron DeSantis).

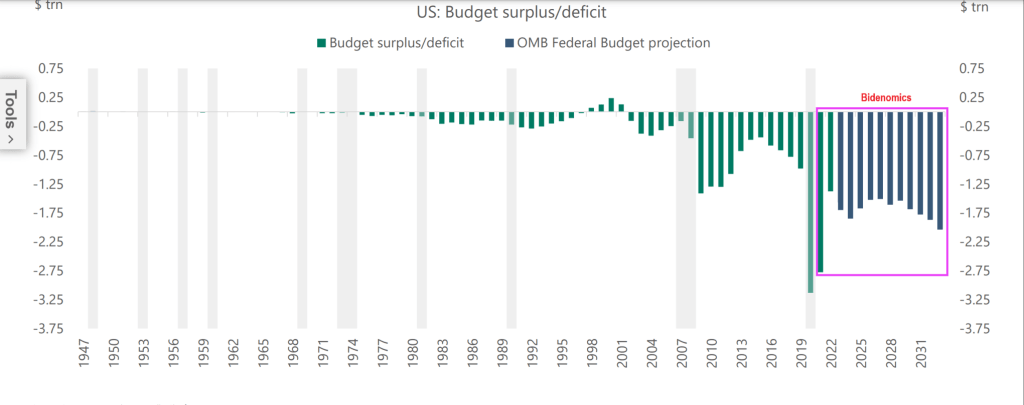

Here is Biden’s budget deficit chart under the hilariously termed “Bidenomics.” Ah, so maybe Governor Newsom is a perfect fit for the wild spenders in Washington DC.

Lest we forget, Biden/Congress can borrow endless funds and stick the bill to Gen Zers and the unborn.

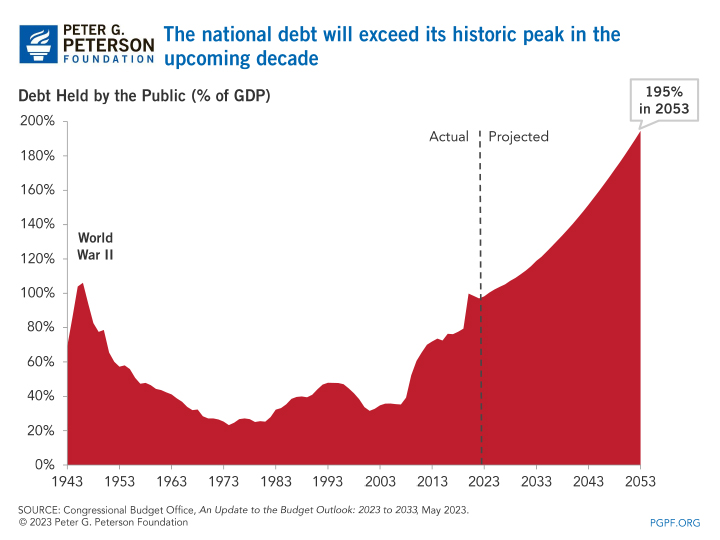

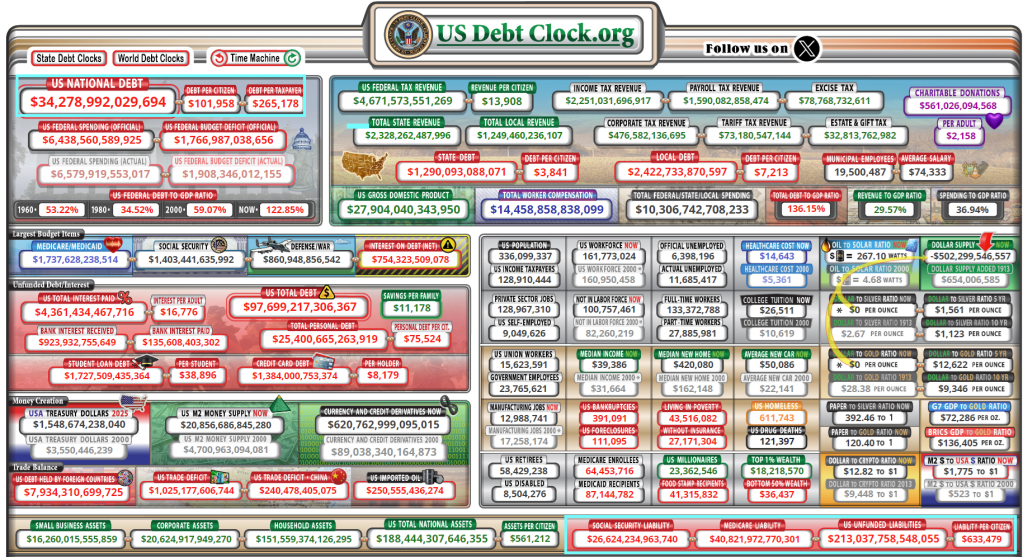

And remember, US politicians have promised $213 TRILLION in unfunded payments that will require cuts (LOL!) or a massive increase in Federal debt.

Biden and Newsom could sing “Fiscal inferno” together! “Here is my demented, doddering grandfather!”

This headline from Zero Hedge makes me so glad I have eaten heart-healthy Quaker Oats and Cheerios every morning for the last 20 years! Study Finds 80% Of Americans Exposed To Fertility-Lowering Chemicals In Cheerios, Quaker Oats. The chemical (chlormequat chloride) was detected in “92 percent of oat-based foods purchased in May 2023, including Quaker Oats and Cheerios.” But that was nothing compared to this Zero Hedge headline: EU “Suicide Pact” Threatens To Flood Continent With 75 Million More Migrants. Makes me wonder if Biden/Mayorkas are under orders from the UN/WEF/Soros to let immigrants pour across our southern border (including 20,000+ Chinese military age males). But back to the economy.

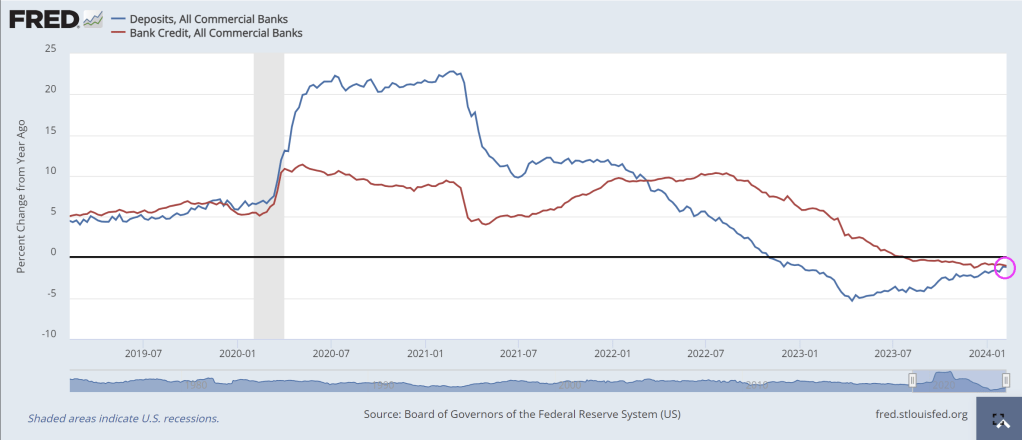

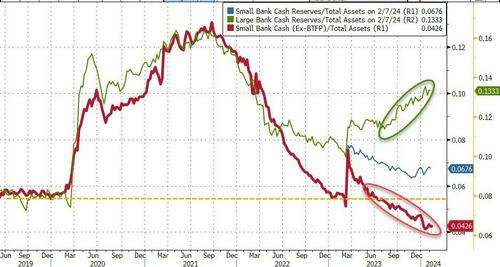

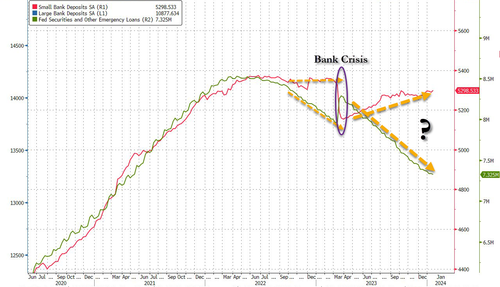

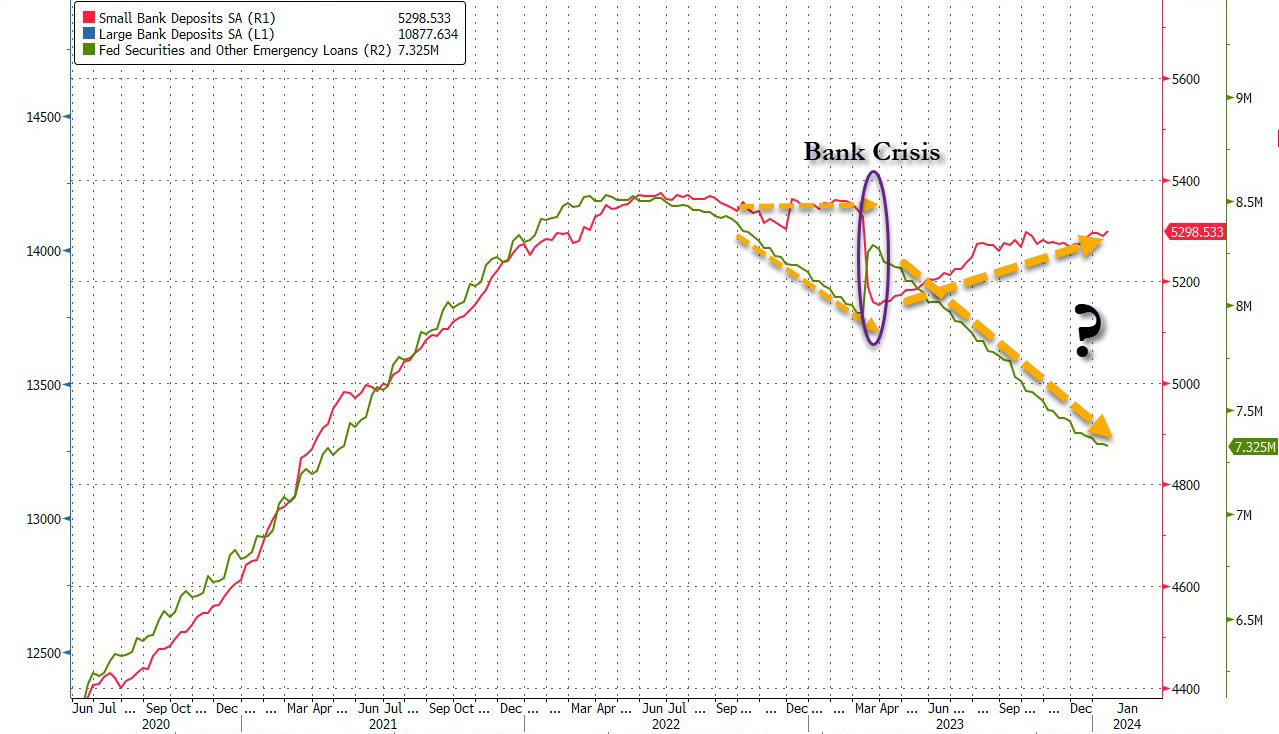

Both bank credit growth year-over-year (YoY) and bank deposit growth (YoY) are NEGATIVE. Covid resulted in massive Federal government stimulus spending (and Federal Reserve hyper stimulus) in 2020, but as the stimulus wears out, so does bank lending and deposits.

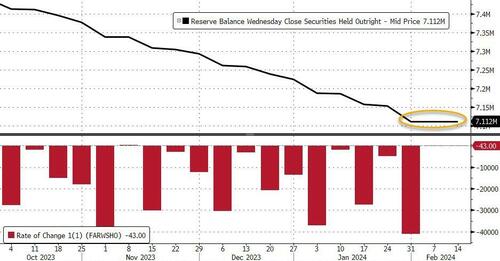

And after the prior week’s miraculous surge in deposits (again, according to The Fed), last week saw total bank deposits (seasonally-adjusted) drop $57BN – the biggest weekly drop since October…

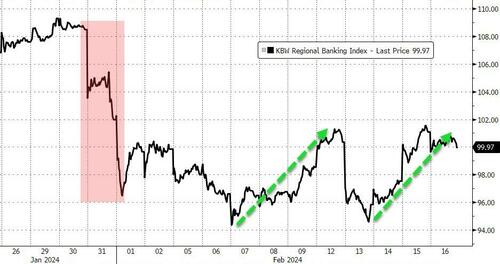

This data is from the week when Regional bank shares shit the bed thanks to NYCB…

Interestingly, on a non-seasonally-adjusted basis, total bank deposits declined about the same as SA -$58BN (and are down $180BN YTD)…

And, excluding foreign banks, domestic deposits dropped $52BN SA (Large Banks -$40BN, Small Banks -$12BN), and tumbled $65BN NSA (Large Banks -$57BN, Small Banks -$$8BN)

As the chart above shows, on an NSA basis, domestic banks have only seen one week of inflows in 2024.

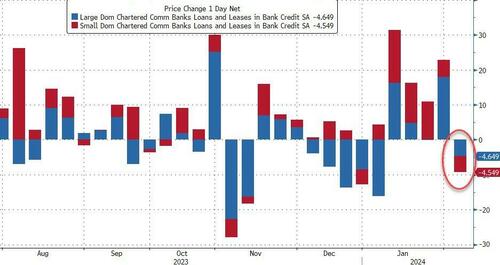

As one might expect, loan volumes shrank during that week by just over $9BN (Large banks -$4.6BN, Small banks -$4.4BN)…

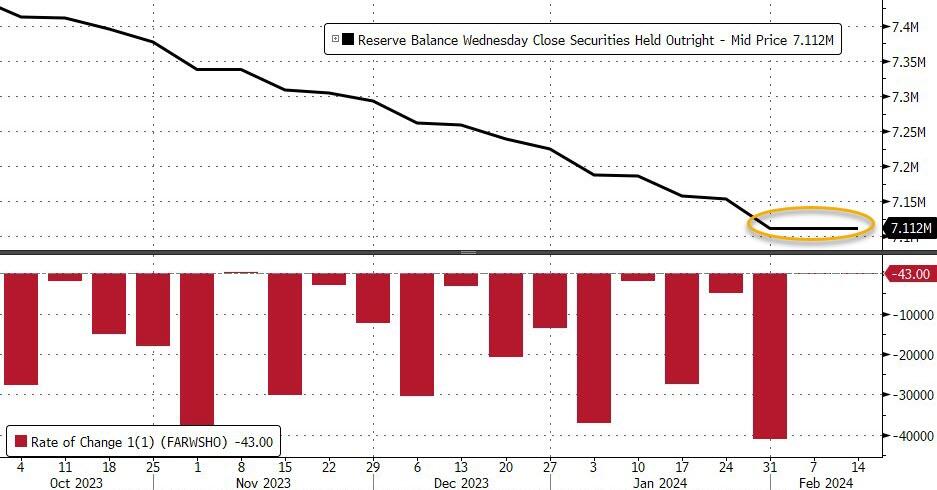

And finally, as a reminder – despite the rebound off the lows again this week in regional bank shares, which must mean everything is awesome, right? – the regional bank crisis is still very much alive as evidenced by the red line below (without The Fed’s imminently expiring BTFP facility)…

…what else are big banks (green line) going to do with all that cash burning a hole in their pockets?

The bottom line is – this looks a lot like a ‘Small Bank’ crisis. The last time this happened, the crisis sparked a sudden $300BN ‘run’ in small bank deposits…

Is The Fed ‘hoping’ for a controlled bank-run this time – so as many small bank deposits are drained voluntarily, before they are drained all at once in a panic (and the Reverse Repo facility is empty, unable to provide any cushion)?

It is looking like a recession in mid-2024 as Covid Stimulypto has run its course. Is the US economy so lame that is requires constant Federal government and Federal Reserve manipulation??

Joe Biden (President of the top 1% of Americans) and his likely replacement “Greasy Gavin” Newsom, wrecker of the California economy. Two economy wreckers on the same stage.

Remember when Democrats were the party of the working man and Republicans (like George HW Bush) were called “Country Club Republicans”? Now Biden and Democrats represent the elitist top 1% of wealth and Trump/Republicans (that Biden snidely calls “Maga Republicans”) represent the bottom 99%. Who woulda thunk??

The asset management arms of JPMorgan Chase and State Street dropped out of Climate Action 100+, home to more than 700 investment firms totaling $68 trillion in assets under management.

BlackRock, the world’s largest asset manager, with more than $10 trillion in assets, distanced its U.S.-based operations from Climate Action 100+ by transferring its membership to BlackRock International.

The coalition, founded in 2017, revealed plans last year to hold members more accountable by encouraging them to disclose more details about their investment decisions. Some high-profile members raised legal concerns about maintaining their fiduciary duties.

State Street said the changes jeopardized the company’s independence. Climate Action 100+ officials say they need the disclosure standards to chart a better course for corporations to reach net-zero emission portfolios by 2050.

“After careful review, State Street Global Advisors has concluded the enhanced Climate Action 100+ Phase 2 requirements for signatories will not be consistent with our independent approach to proxy voting and portfolio company engagement,” State Street spokesman Randall Jensen said. “As a result, we have decided to withdraw from Climate Action 100+.”

JPMorgan suggested that its in-house guidelines for environmental, social and corporate governance, or ESG, investing already exceeded the Climate Action 100+ goals.

Aka, MARXISM.

Ford learned that their ESG Ford F-150 Lightning Electric pick up truck was NOT in demand, so production is being curtailed. Harvard (which should be renamed Harvurd thanks to President Gay’s horrible record of plagiarism) and Biden’s leadership team of unqualified but ESG-friendly faces (“Admiral” Rachel Levine, formerly Richard Levine) symbolizes the failure of ESG.

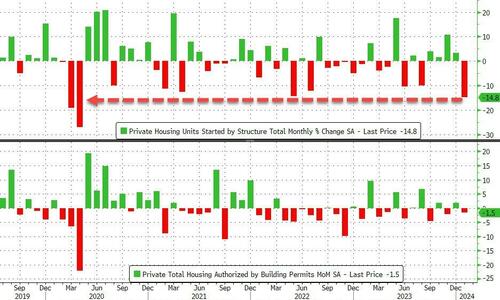

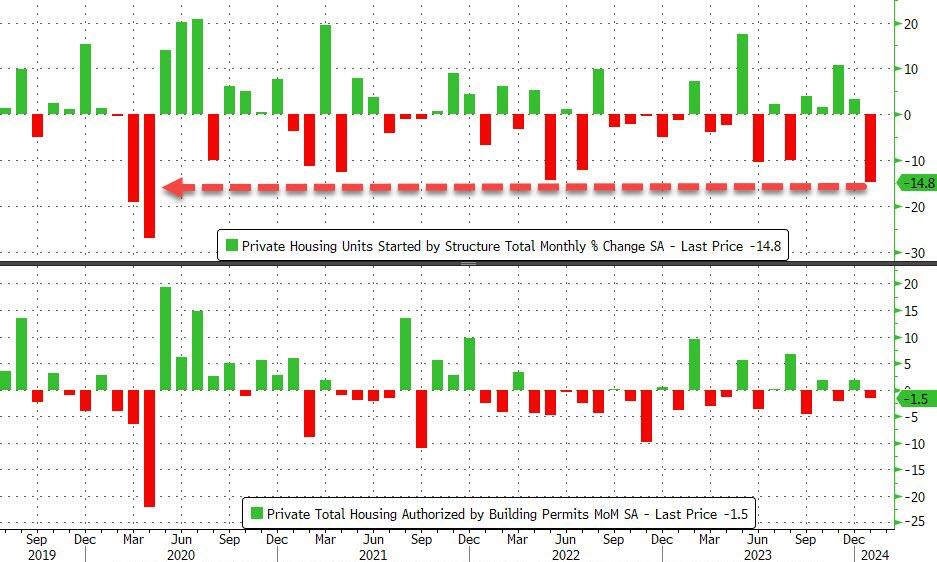

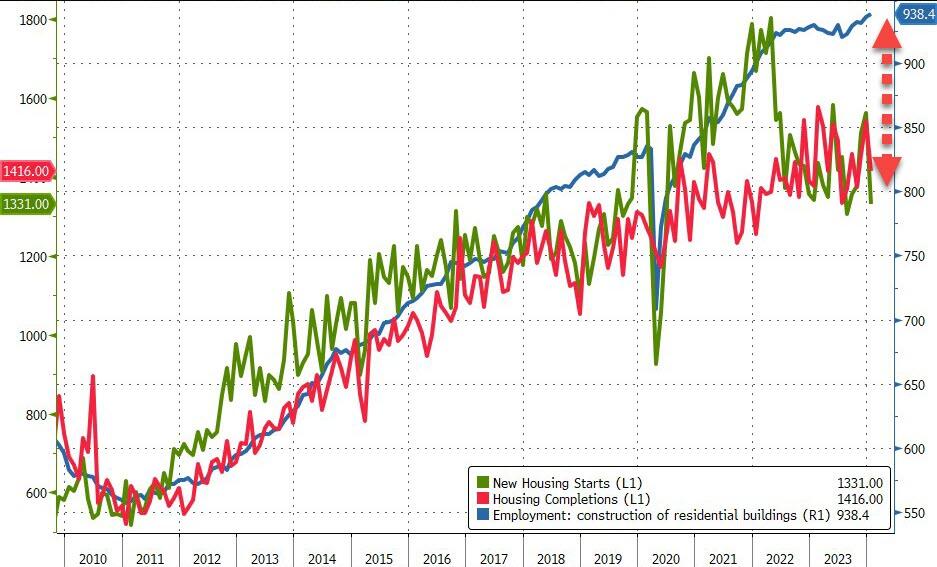

Analysts were way off. Housing Starts puked 14.8% MoM in January (vs unchanged exp), but December’s 4.3% MoM decline was revised up to a 3.3% MoM rise. Building Permits also tumbled, down 1.5% MoM (vs +1.3% exp) and well down from the +1.8% MoM in December…

Source: Bloomberg

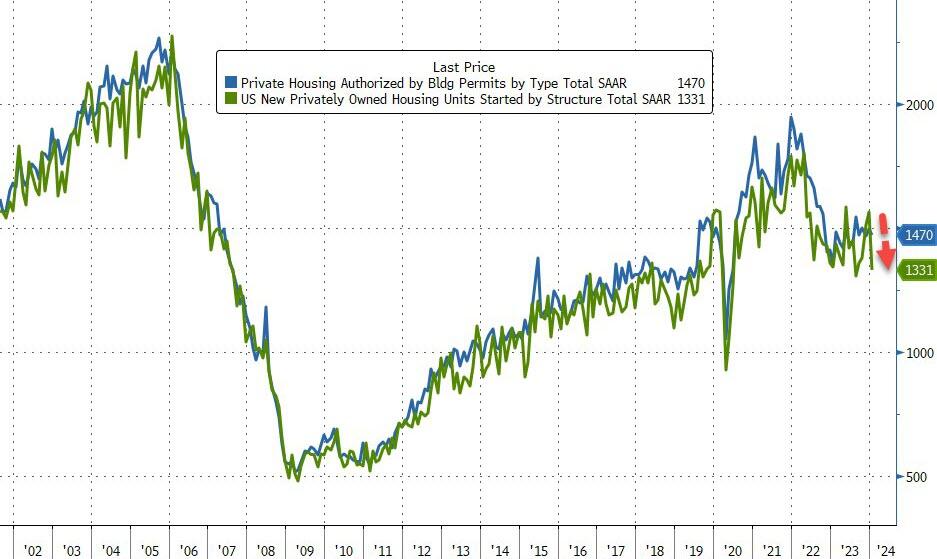

This pushed the Housing Starts SAAR back near post-COVID lows…

Source: Bloomberg

DO NOT BLAME THE WEATHER! It’s January – we know there are weather issues and that should be more than ‘priced-in’ on a seasonal adjustment basis.

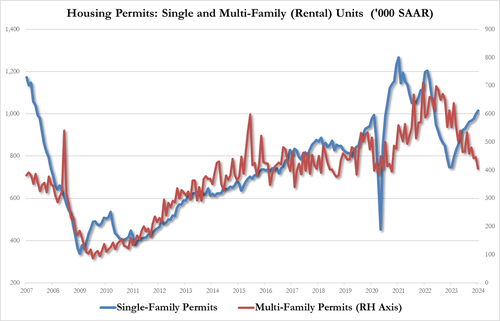

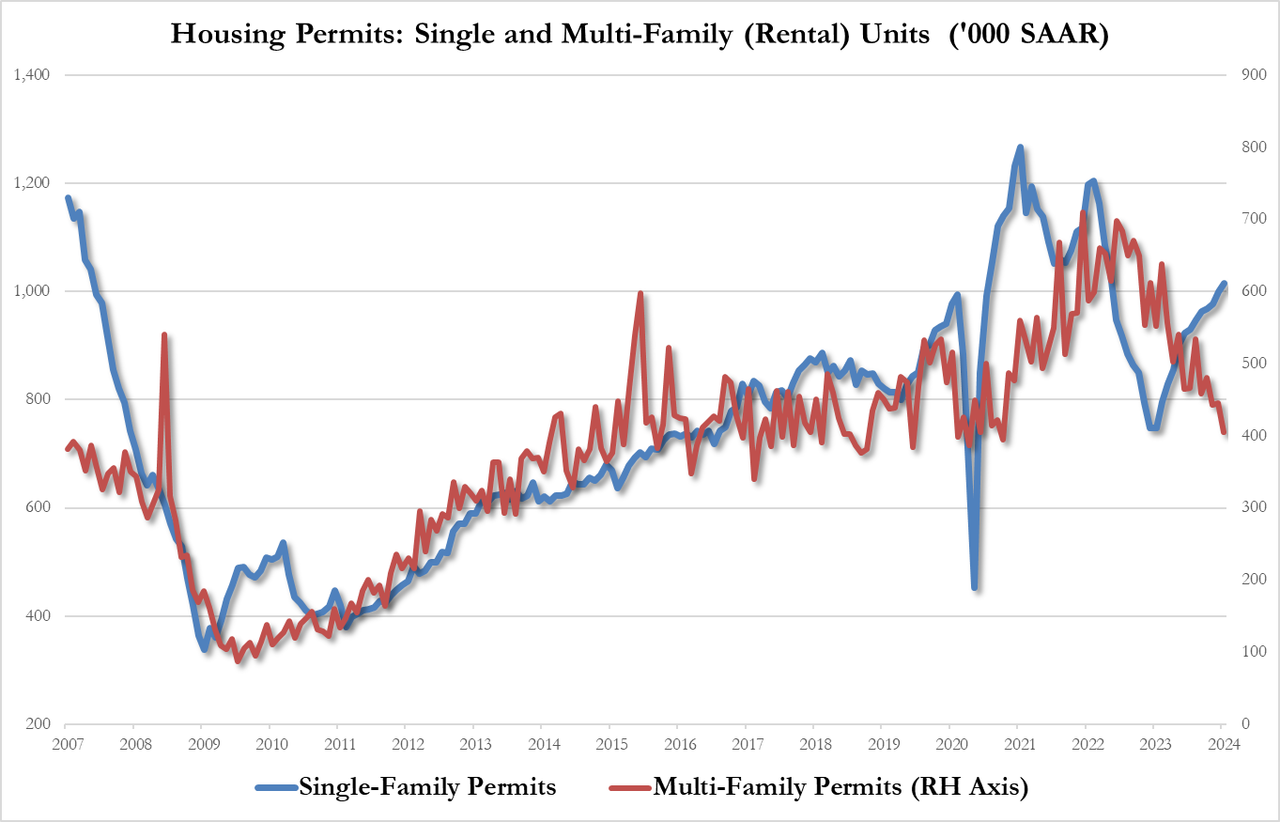

Multi-family permits cratered to their lowest since Oct 2020. Permits for one-family homes edged higher after rising consistently throughout 2023

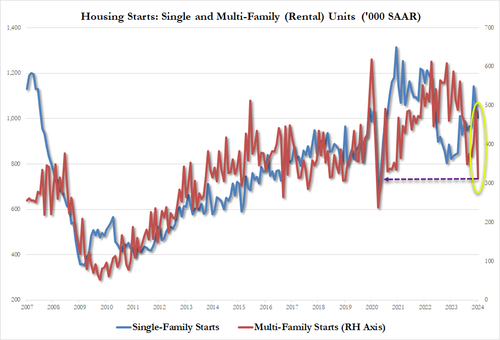

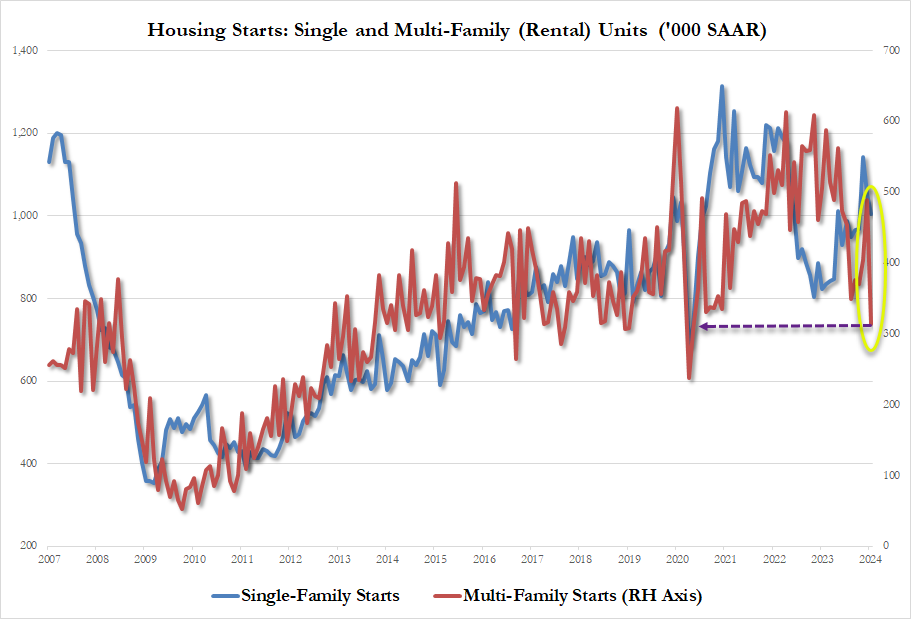

And multi-family starts were even worse, plunging from 489k SAAR to 314k SAAR – the lowest since May 2020 (when the economy was closed)…

The government’s report showed housing starts fell in all four of the nation’s regions, led by the Midwest and Northeast. The number of single-family homes completed plunged to the lowest level since May 2020.

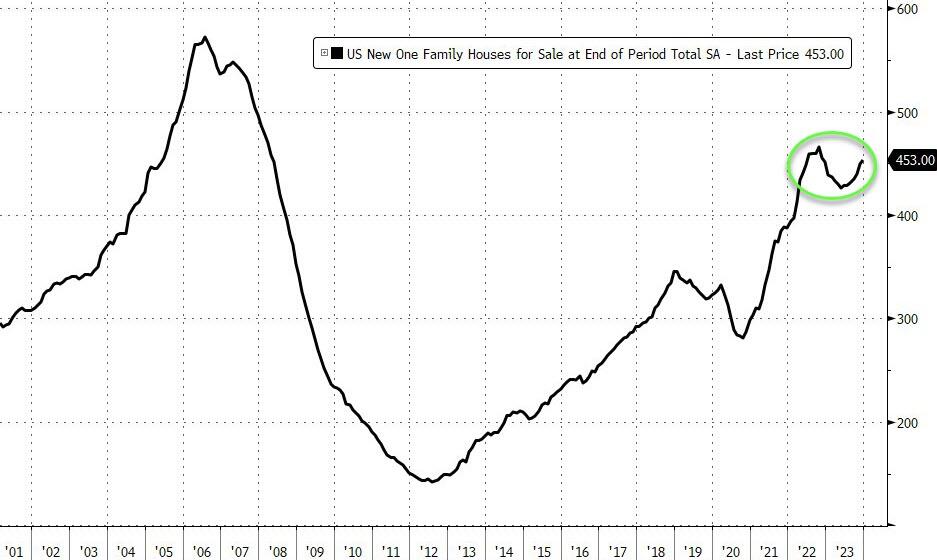

They built it, but no one came… the inventory of new houses for sale remains elevated and suggests builders may be cautious about beginning new projects.

Don’t expect Permits to be reaccelerating anytime soon as mortgage rates have started to rise once again…

Source: Bloomberg

Which is not good news for CPI either as it suggests there is little rent relief coming soon.

And finally, there is a record gap between what the government tells us about construction employment and actual construction activity…

Makes you wonder, eh? Did builders all suddenly get massively less productive? Or is the BLS just making shit up as usual?

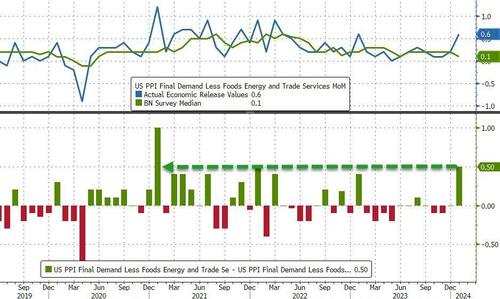

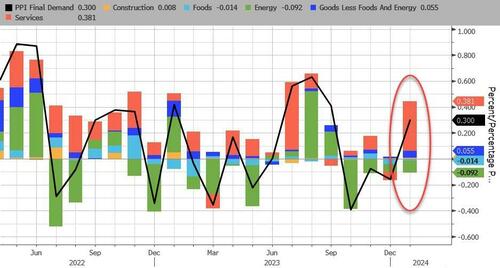

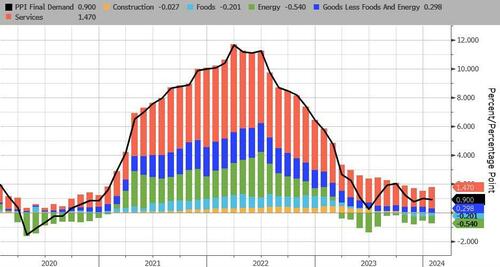

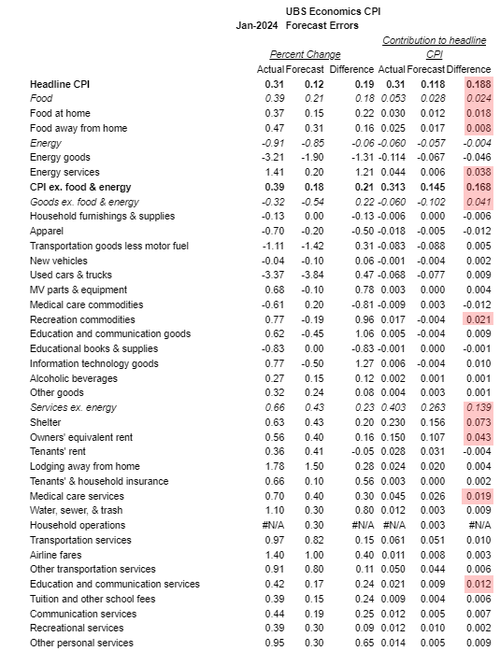

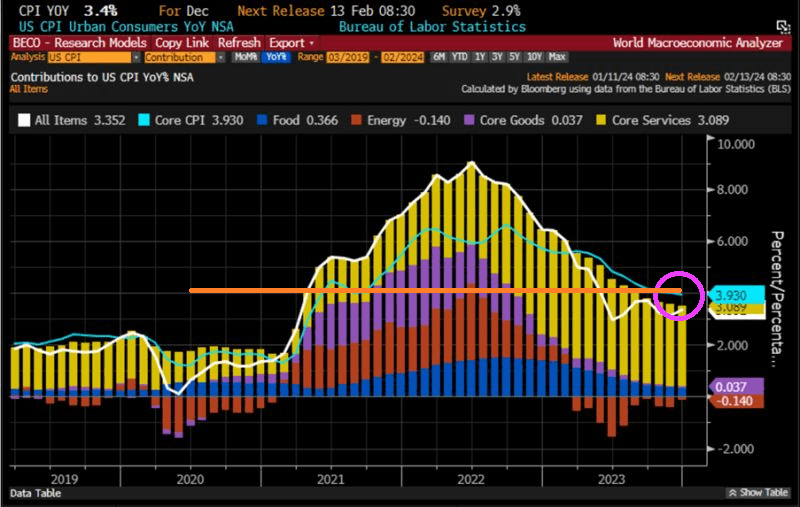

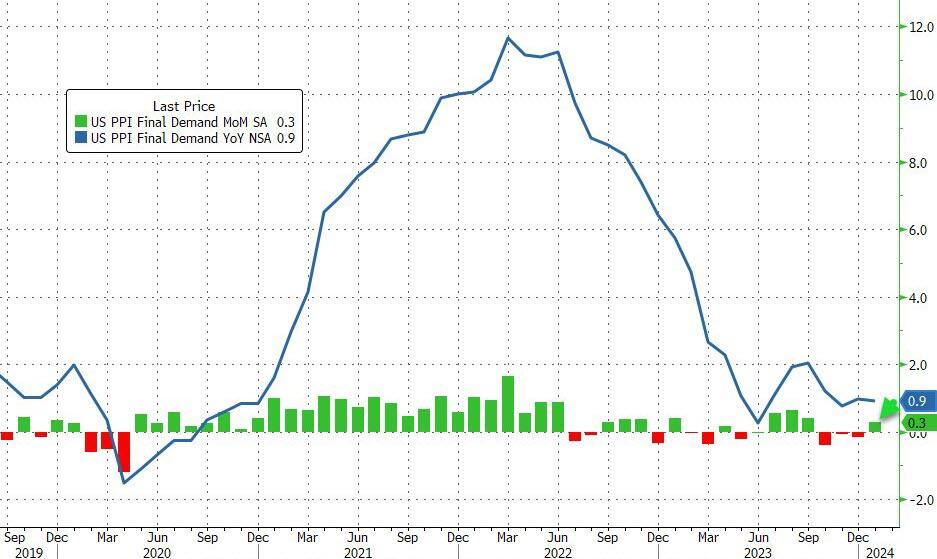

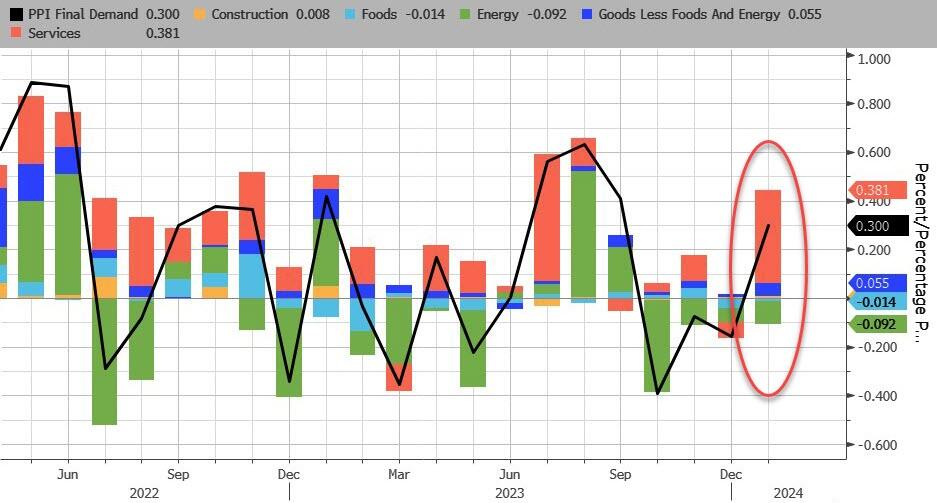

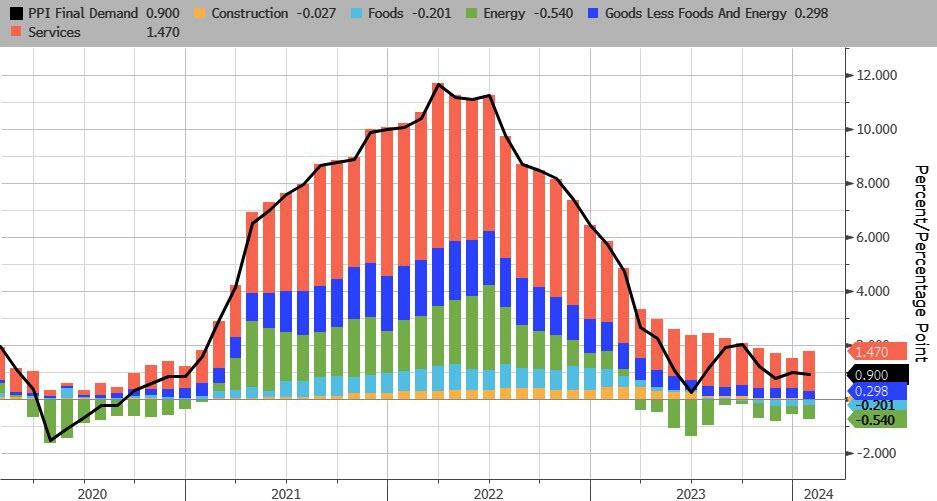

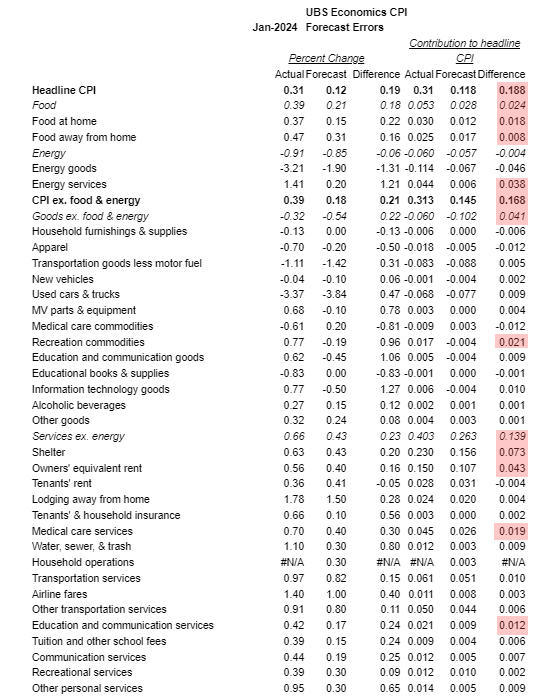

After the hotter-than-expected CPI (which has been shrugged off entirely by the stock market), Producer Prices were expected to rebound very modestly MoM but continue to slow on a YoY basis in January. Instead, like CPI, it re-accelerated with headline rising 0.3% MoM (+0.1% MoM exp), which left PPI up 0.9% YoY (down from December but hotter than the +0.6% exp)…

Source: Bloomberg

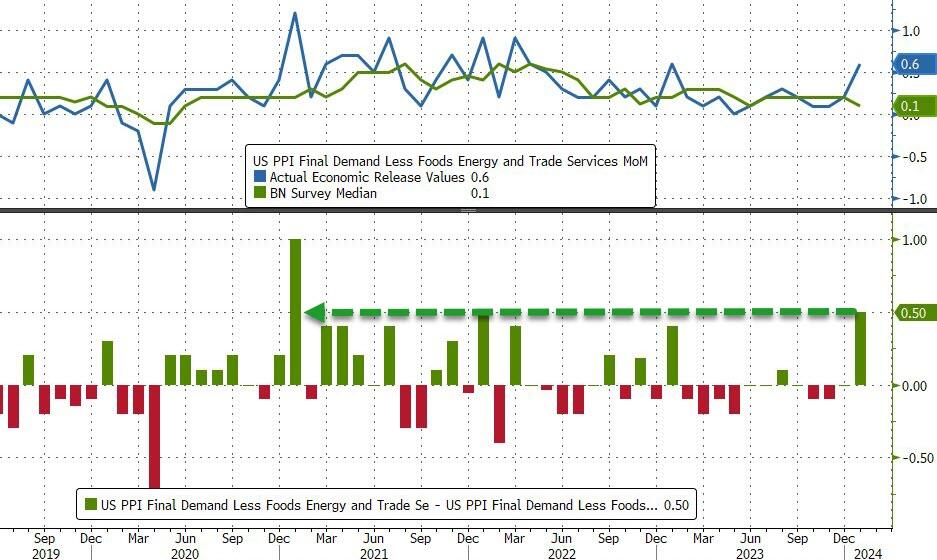

The picture was even worse under the hood with PPI ex food and energy up 0.5% MoM (vs +0.2% prior and +0.1% exp) and ex-food, energy, and trade up 0.6% MoM (vs +0.1% exp).

This was the biggest ‘beat’ for Core PPI since Jan 2021…

In fact, core PPI reached a new record high (reminder, disinflation does not mean lower prices), now up 17.4% since Biden was elected…

Services PPI soared MoM, and energy continues to be a driver of deflation (but is losing its power)…

Source: Bloomberg

And on a YoY basis, Services PPI is also re-accelerating (+1.47% from +1.14%). Energy continues to be the deflationary driver…

Source: Bloomuberg

This is not good news for the disinflationistas. And it will stop President Biden’s narrative that ‘prices are coming down’…

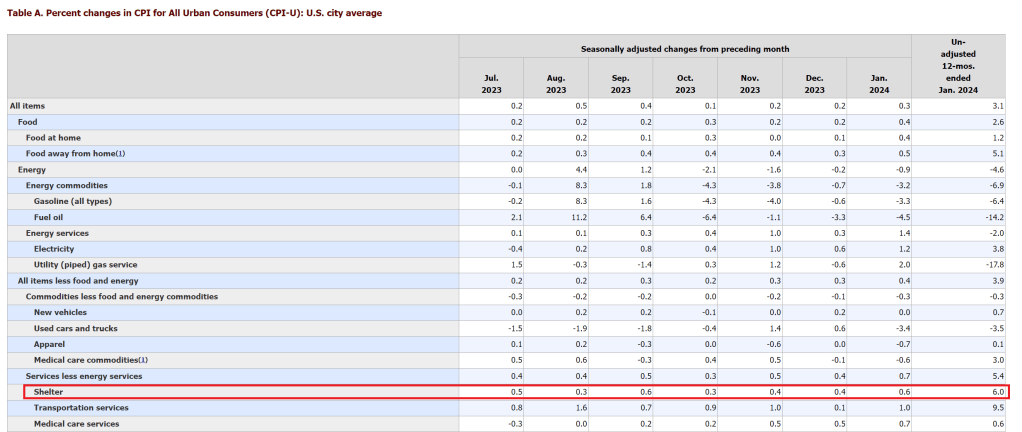

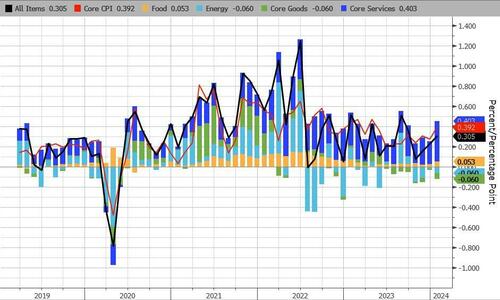

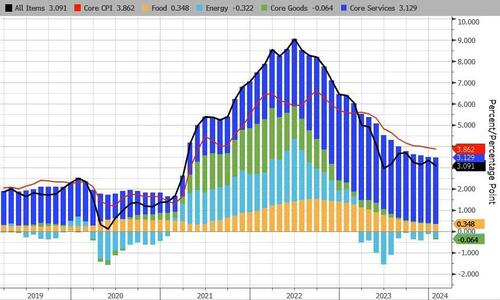

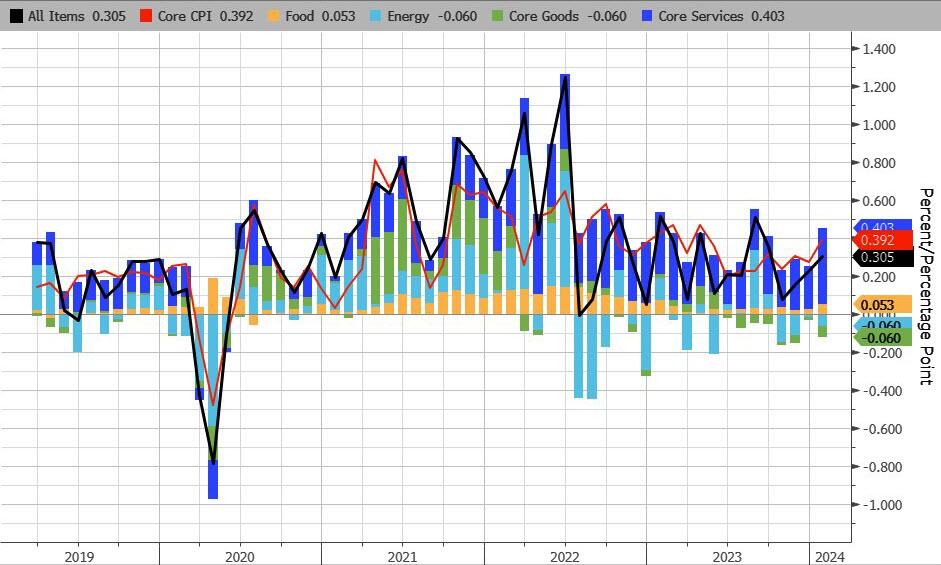

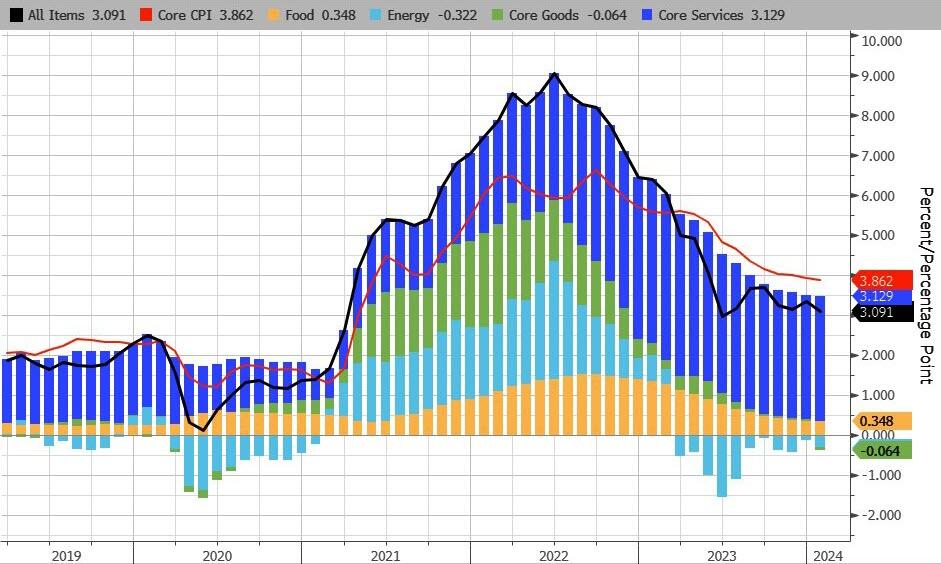

Core CPI fell below 4.00% YoY for the first time since May 2021, but the +3.86% YoY print was hitter than the 3.7% exp (with prices rising 0.4% MoM – the biggest jump since April 2023)…

Source: Bloomberg

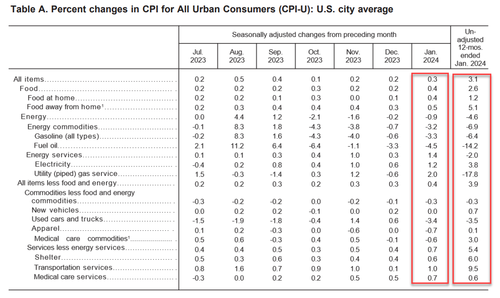

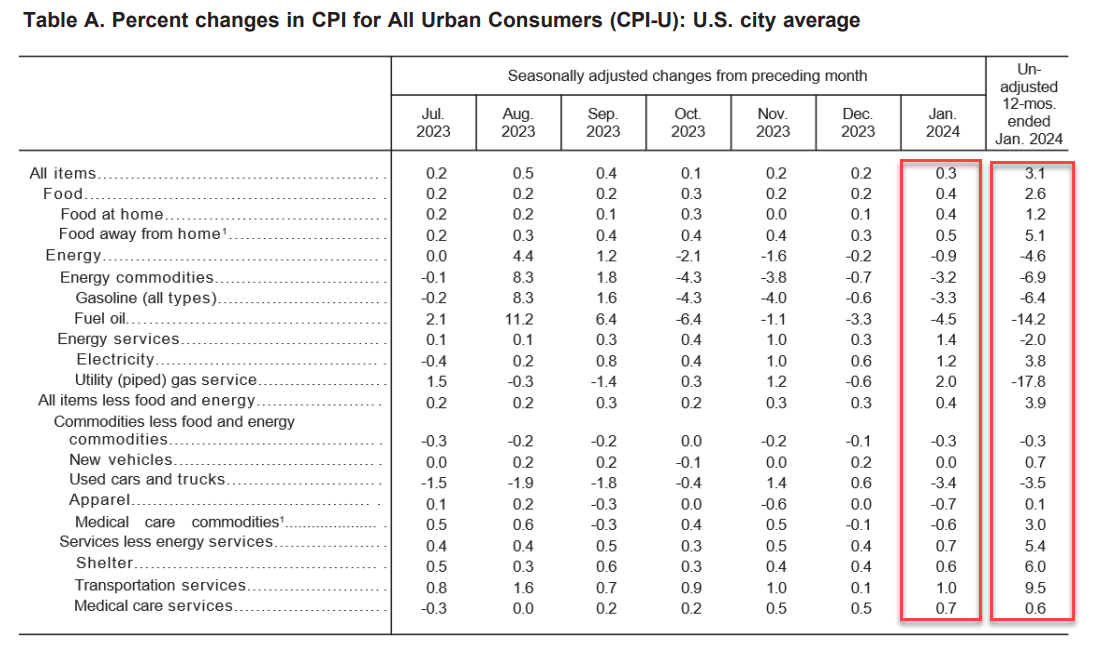

CPI Core: The index for all items less food and energy rose 0.4 percent in January.

The shelter index increased 0.6 percent in January, and was the largest factor in the monthly increase in the index for all items less food and energy.

The index for owners’ equivalent rent rose 0.6 percent over the month, while the index for rent increased 0.4 percent.

The lodging away from home index increased 1.8 percent in January. The motor vehicle insurance index increased 1.4 percent in January, and the recreation index rose 0.5 percent in January.

Among other indexes that rose in January were communication, personal care, airline fares, and education.

The medical care index rose 0.5 percent in January.

The index for hospital services increased 1.6 percent over the month and the index for physicians’ services increased 0.6 percent.

The prescription drugs index fell 0.8 percent in January.

The index for used cars and trucks fell 3.4 percent in January.

The index for new vehicles was unchanged in January.

The apparel index also decreased, falling 0.7 percent over the month.

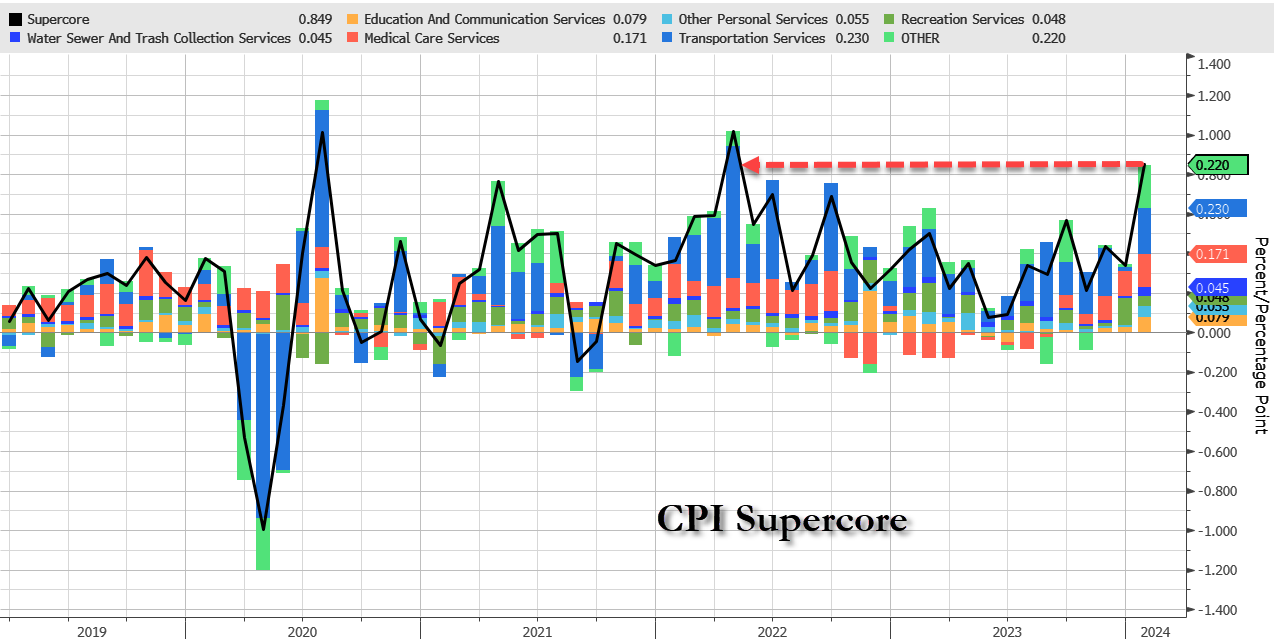

Core Service inflation picked up MoM…

..and accelerated YoY

Source: Bloomberg

Under the hood, food and Energy services costs jumped MoM along with transportation services…

Here’s the biggest component upside surprises…

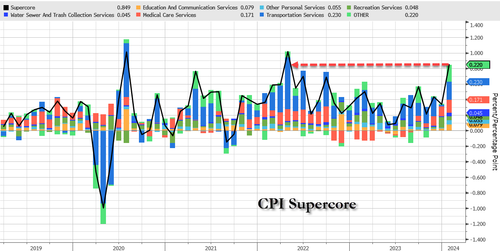

And one step deeper – the so-called SuperCore: Core CPI Services Ex-Shelter index – soared 0.7% MoM (the biggest jump since Sept 2022…

… driving the YoY change up to +4.4% – the hottest since May 2023….

Source: Bloomberg

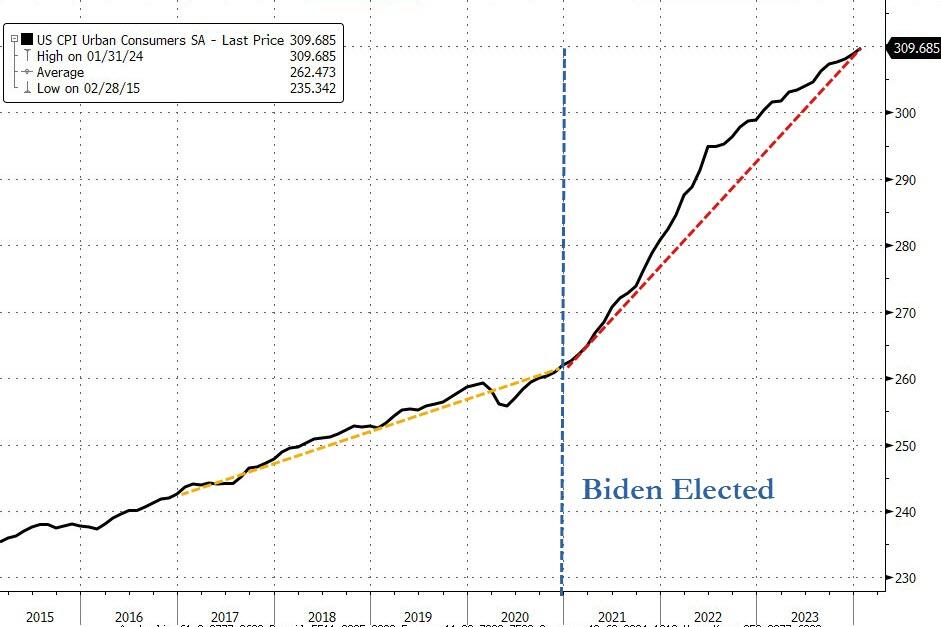

Finally, as a reminder, lower inflation does not mean lower prices.

Source: Bloomberg

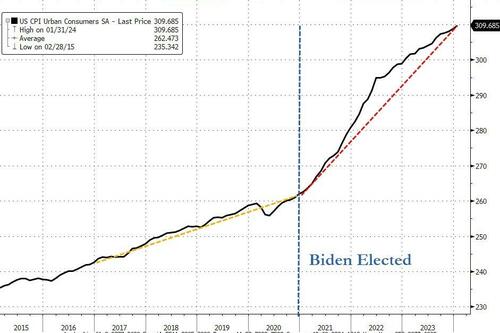

The actual index of consumer prices hit a new record high this month – and is up over 18% since President Biden’s term began(it was up 8% over President Trump’s full four year term).

And it gets worse…

Source: Bloomberg

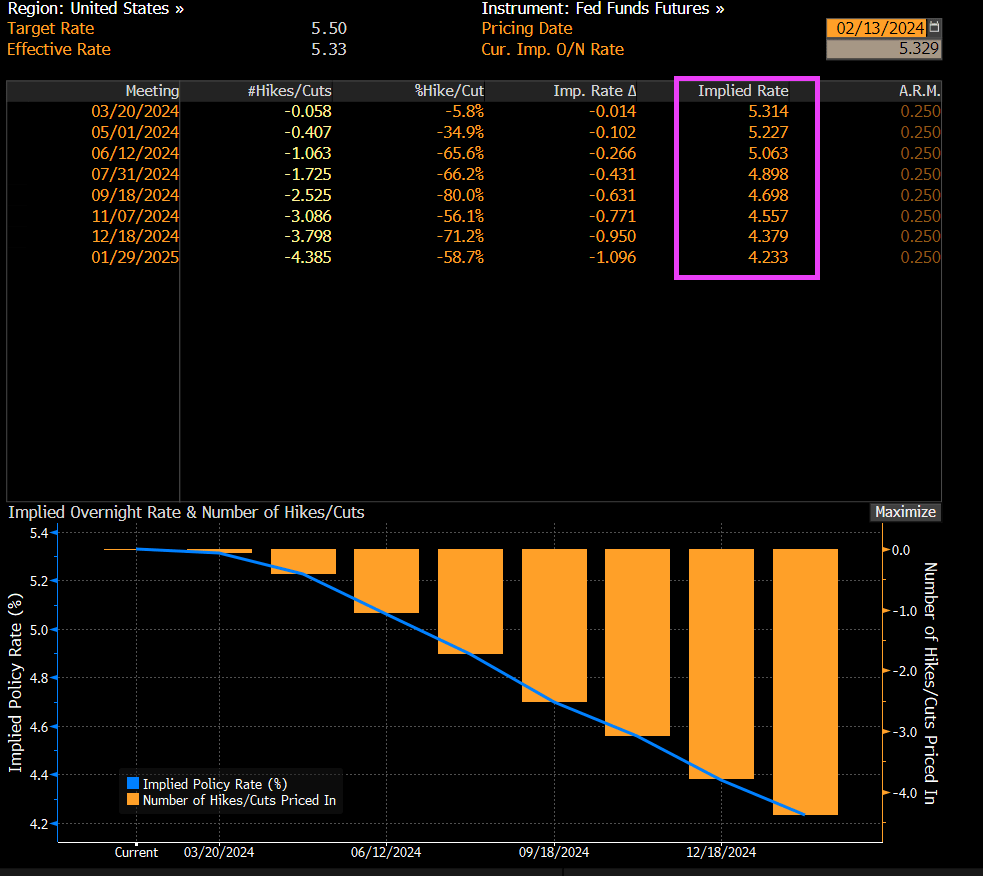

And on the higher than expected inflation report, we are still seeing bets on Fed Funds rate falling from 5.50% to 4.233% over the coming year.

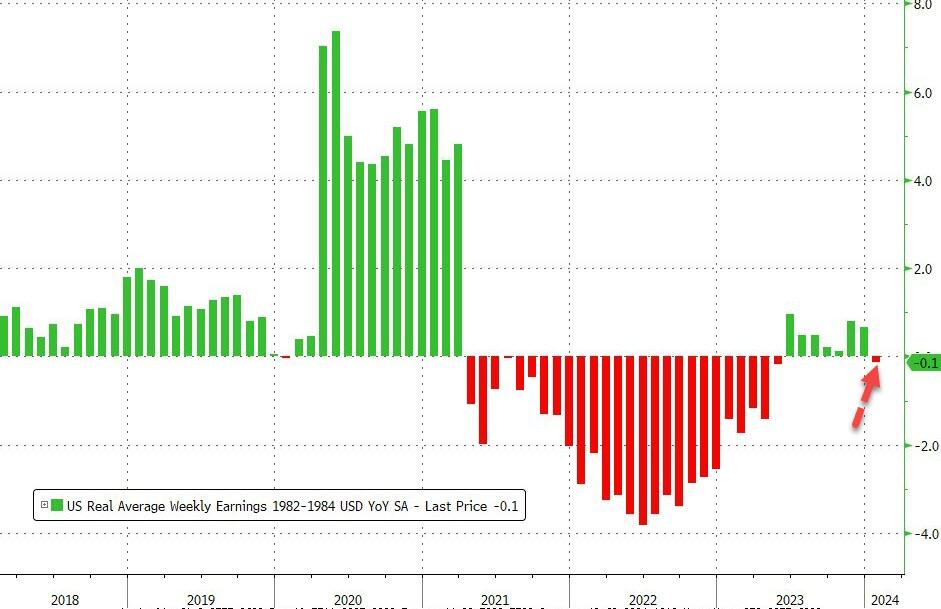

The re-accleration of inflation means wage growth is back in the red relative to prices.

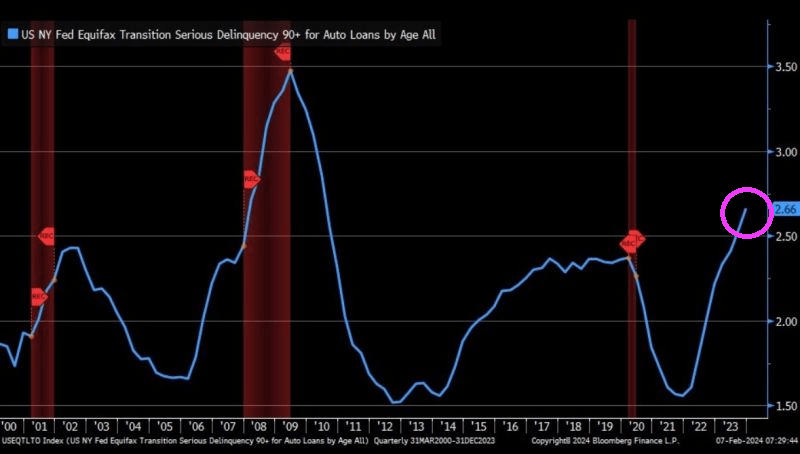

And with the God awful jobs report, serious delinquencies on auto loans is SOARING. To the highest rate since The Great Recession.

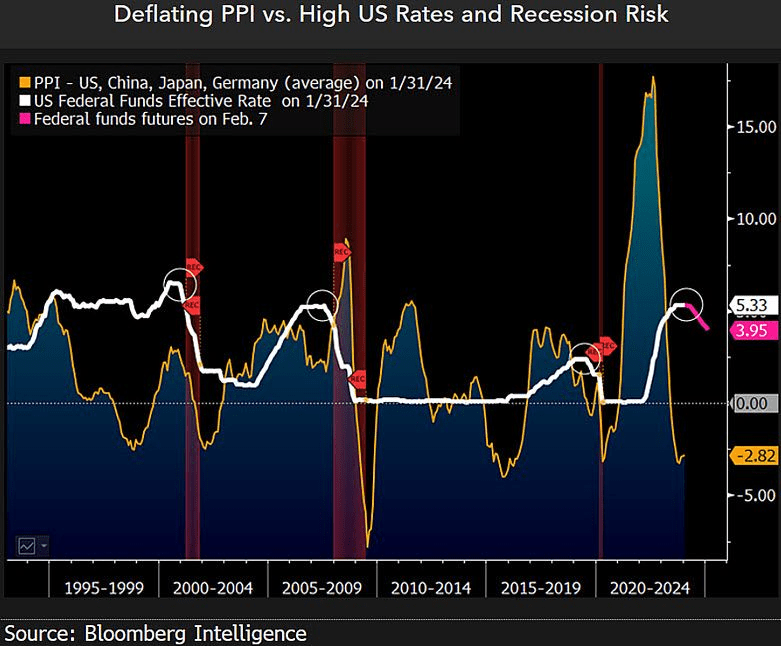

The Producers Price Index is deflating.

At least inflation is cooling down, but still higher than under he that can’t be mentioned on The View, Rachel Maddow or Morning Joe, Donald Trump, the Left’s Voldemort.

I admit, Travis Kelce should have been benched for shoving Head Coach Andy Reid during The Super Bowl. “Damn it, Taylor (Swift) flew here from Tokyo to watch me play and you aren’t throwing enough to me!” Welcome Travis Kelce to the elitist 1% who think the rules don’t apply to them. And your 2.0 GPA at University of Cincinnati certainly qualifies you to opine on the economy … on The View or MSNBC.

I watched Tucker Carlson’s interview with Russian President Vladimir Putin. Putin is an amazing contrast to our 81-year old President with dementia who can barely speak while Putin was articulate. Not at all what Hillary Clinton was raving about (she is still furious about losing to Trump after losing to Obama). One thing that caught my attention was Putin talking about The Fed’s endless printing of money. Well, THAT is how the US grows GDP these days. Borrow and spend with the private sector as an after thought.

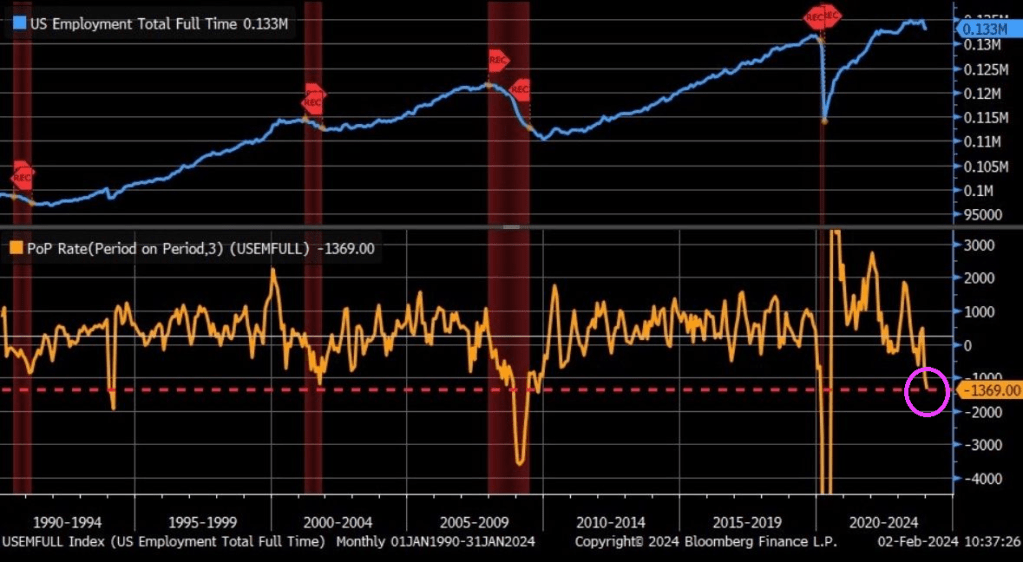

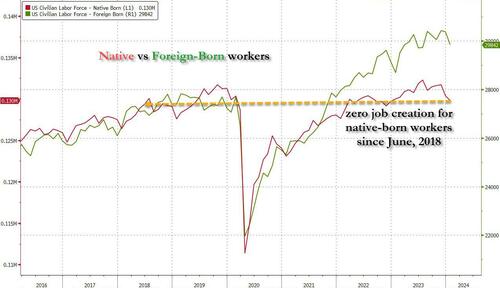

Let’s revisit the HORRIBLE jobs report from December. Not only were all job gains in the past year entirely thanks to part-time workers, but native-born workers plunged by a another whopping 560 thousand, bringing the two-month total drop to just under 2 million.This meant that not only has all job creation in the past 4 years been exclusively for foreign-born workers, but there has been zero job-creation for native-born American workers since July 2018 (don’t believe us? go ahead and check the data directly from the Fed).

So, the Federal government is borrowing trillions of dollars so that 1) part-time jobs are created and 2) foreign born workers have jobs, but not native born Americans?? (Blogger Paul Krugman thinks that immigration will add $7 trillion in real GDP over the next 10 years and this will save Social Security and Medicare. Huh? I admit, millions of immigrants will spend money, but many will be on the Federal and State doles, so its tax dollars going to immigrants to spend.) This seems like Obama/Biden are using Cloward-Piven tactics to overwhelm Social Security, Medicare and other social services, NOT grow the economy as Krugman projects.

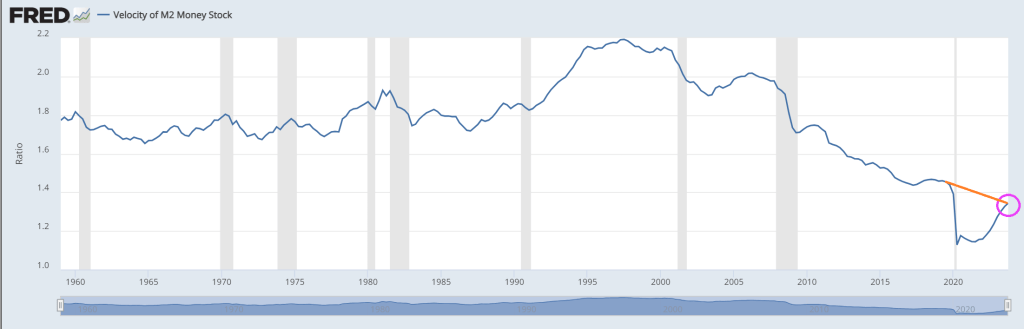

Typically, economists look at measures like M2 Money Velocity (Real GDP/M2). M2 Money Velocity is rising … but still remains below where it was pre-Covid under Donald Trump.

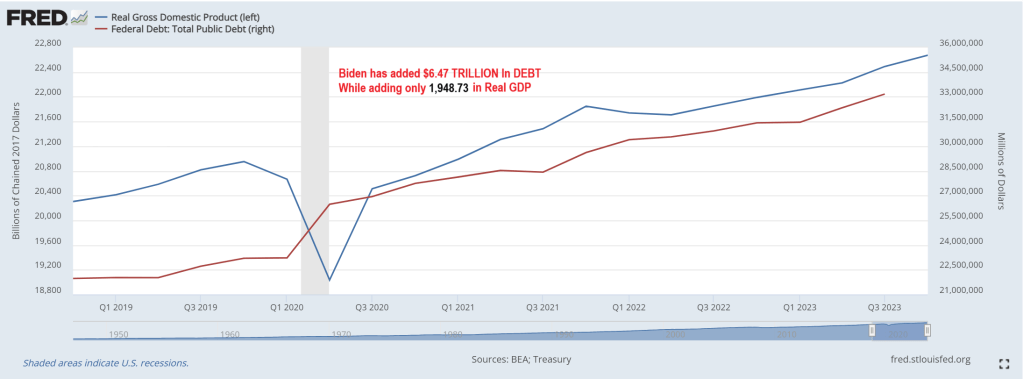

But a more relevant velocity is the velocity of DEBT. As in GDP/Debt. Under Biden, the US has added almost $6.5 TRILLION in debt while real GDP has risen by only $1.949 trillion. That amounts to a DEBT velocity of 0.30. Meaning that the US gets an anemic $30 in real GDP for every $100 in additional Federal debt.

Yes, the US economy is broken and requires endless money printing and debt financing to pay for endless wars and now millions of illegal immigrants getting on “the dole.” Then we have Biden’s forgiving student loan debt (inappropriately) and now Big Tech wants $7 trillion to develop AI (in a normal economy, tech companies would develop AI themselves, but under Obama/Biden, we are not in a normal economy).

Here is Daddy (Ukraine) Warbucks Biden with his biting dog and daughter Ashey.

Remember the Chicago Bears’ “Super Bowl Shuffle”? Well, Joe Biden is thedemented (according to Hur) shuffler so a Super Bowl shuffle video featuring Biden talking about how he is reducing prices.

A week out from kickoff, rooms at five-star hotels like the Bellagio, Aria, and The Venetian started at $1,500 or more per night for Super Bowl weekend, according to Expedia. Travelers seeking an affordable stay on the Las Vegas Strip, such as at Excalibur, can find an average nightly rate of $88 on Priceline for this weekend. That jumps to $486 during Super Bowl weekend, an increase of 426 percent. Prices do dip a bit if Super Bowl fans want to stay away from the Strip’s hotels and casinos. Downtown and hotels away from the main drag do offer some cheaper options, with some hotels charging around $200 per night on Fremont Street. Circa, which contains one of the most popular sportsbooks in Las Vegas, is an exception. Rooms this weekend are going for $179 per night on Priceline. That shoots up to $1,232 per night, with only a few rooms remaining at that price, for Super Bowl weekend.

And then, of course, there are the costs of getting there and subsisting. Intrepid drivers looking to travel from San Francisco to Los Angeles (a trip of between 8 and 9 hours) will do so with gasoline prices at $3.66/gallon. That’s down markedly from the mid-2022 spike, but still vastly above levels before the pandemic. Like hotel and ticket prices, airfare into and out of Las Vegas around the big game has alsovaulted in price, although a number of carriers have increased capacity to meet surging demand.

Celebrating at Home Of course, the vast majority of Super Bowl LVIII viewers will not be in Allegiant Stadium, which holds 65,000 spectators. The remainder of viewers, averaging north of 100 million people, will be watching at home or in their hometown sports bars and restaurants. But the persistent inflation of the past three years extended the financial burden into that seemingly more affordable alternative: hosting or attending Super Bowl parties at home. What was once a casual affair of chips, dips, and budget-friendly beverages has transformed into a costly endeavor, as the price of groceries, alcoholic beverages, and even party supplies have surged, affecting the way fans plan to experience one of America’s most iconic sporting events.

The top Super Bowl snacks and dishes include chicken wings, guacamole, potato skins, and deviled eggs, so a look at the recent price trends in chicken, beef, pork, avocados, eggs, beans, potatoes, eggs and condiments is relevant. Pizza, alcoholic beverages, and soft drinks are other popular choices prices have been creeping up.

Below are the prices of a handful of foodstuffs and ingredients which feature prominently in Super Bowl festivities, as well as the price changes from the pre-pandemic period to the most recent data (December 2019 to December 2023). The prices are provided by the US Bureau of Labor Statistics Average Prices by Product series, not seasonally adjusted:

Dec-19 to

Dec 2019

Dec 2023

Dec-23

Grade A Large Eggs

$1.54

$2.51

63.30%

White Sugar All Sizes

$0.59

$0.96

62.30%

Price Frozen Concentrate OJ

$2.34

$3.72

59.10%

Coffee

$4.05

$6.09

50.30%

White Bread

$1.36

$2.02

48.50%

All Ham Ex Canned and Slices

$3.04

$4.40

45.00%

Chocolate Chip Cookies

$3.58

$5.12

42.80%

Grapefruits

$1.25

$1.78

41.90%

Potato Chips

$4.53

$6.41

41.40%

Long Grain White Rice

$0.71

$0.99

38.70%

All Uncooked Beef Steaks

$7.71

$10.65

38.10%

Sirloin Steak Boneless

$8.48

$11.69

37.80%

All Other Uncooked Beef ExVeal

$5.05

$6.91

36.70%

Round Roast Choice Boneless

$5.07

$6.89

35.80%

Boneless Ham Excluding Canned

$4.07

$5.50

35.10%

Ground Beef 100% Beef

$3.86

$5.21

34.90%

Fresh Whole Chicken

$1.45

$1.96

34.80%

Whole Wheat Bread

$1.96

$2.65

34.80%

Round Steak Boneless

$5.98

$7.99

33.70%

All Uncooked Beef Roasts

$5.54

$7.35

32.70%

All Other Pork Ex Can/Sliced

$2.76

$3.64

31.80%

Boneless Chicken Breast

$3.11

$4.08

31.10%

Chuck Roast Choice Boneless

$5.65

$7.38

30.70%

All Uncooked Ground Beef

$4.30

$5.57

29.40%

Ice Cream

$4.74

$6.02

26.90%

Processed American Cheese

$3.91

$4.96

26.80%

Ground Chuck

$4.07

$5.12

25.90%

Fresh Fortified Whole Milk

$3.19

$4.01

25.70%

All Pork Chops

$3.39

$4.26

25.50%

All Purpose White Flour

$0.43

$0.54

25.40%

Sliced Bacon

$5.47

$6.77

23.70%

Chicken Legs Bone In

$1.51

$1.86

23.30%

Romaine Lettuce

$2.18

$2.68

23.30%

White Potatoes

$0.78

$0.96

23.20%

Malt Beverages

$1.42

$1.75

23.00%

Boneless Beef for Stew

$5.75

$7.03

22.20%

Lean Ground Beef

$5.52

$6.67

20.90%

Navel Orange

$1.33

$1.60

20.60%

Boneless Chops

$3.81

$4.56

19.80%

Iceberg Lettuce

$1.30

$1.53

17.30%

Spaghetti and Macaroni

$1.19

$1.38

15.80%

Dry Pint Fresh Strawberries

$3.10

$3.57

15.40%

Center Cut Bone In Chops

$3.77

$4.33

14.70%

Dried Beans

$1.40

$1.59

13.60%

Red and White Table Wine

$12.04

$13.32

10.60%

Bananas

$0.57

$0.63

9.10%

Natural Cheddar Cheese

$5.30

$5.55

4.60%

Lemon

$2.00

$2.07

3.60%

Field Grown Tomatoes

$1.95

$2.00

2.10%

And although disinflation has proceeded, by their nature the various indices (Consumer Price Index, Personal Consumption Expenditure Price Index) obscure individual price changes. For example: the US CPI Urban Consumers Food-at-Home index, in December 2023, showed a year-over-year change of 1.31 percent (from 299.089 to 303.005). Below are the actual December 2022 to December 2023 changes in individual food items which are prominent in Super Bowl celebrations.

Dec-22 to

Dec 2022

Dec 2023

Dec-23

Price Frozen Concentrate OJ

$2.72

$3.72

36.80%

Sirloin Steak Boneless

$10.17

$11.69

15.00%

White Sugar All Sizes

$0.84

$0.96

13.30%

Round Steak Boneless

$7.06

$7.99

13.20%

All Uncooked Beef Steaks

$9.46

$10.65

12.50%

Round Roast Choice Boneless

$6.22

$6.89

10.70%

Whole Wheat Bread

$2.42

$2.65

9.40%

All Uncooked Beef Roasts

$6.72

$7.35

9.30%

All Ham Ex Canned and Slices

$4.05

$4.40

8.70%

Ground Beef 100% Beef

$4.80

$5.21

8.50%

Ice Cream

$5.56

$6.02

8.20%

White Bread

$1.87

$2.02

8.10%

Navel Orange

$1.49

$1.60

7.80%

Chuck Roast Choice Boneless

$6.86

$7.38

7.60%

Ground Chuck

$4.76

$5.12

7.60%

All Uncooked Ground Beef

$5.19

$5.57

7.30%

Fresh Whole Chicken

$1.83

$1.96

6.80%

Processed American Cheese

$4.66

$4.96

6.30%

All Other Uncooked Beef ExVeal

$6.59

$6.91

4.80%

Lean Ground Beef

$6.39

$6.67

4.50%

All Purpose White Flour

$0.52

$0.54

3.10%

Chocolate Chip Cookies

$4.97

$5.12

2.90%

Boneless Ham Excluding Canned

$5.37

$5.50

2.40%

Boneless Beef for Stew

$6.87

$7.03

2.20%

Potato Chips

$6.28

$6.41

2.00%

Long Grain White Rice

$0.97

$0.99

2.00%

White Potatoes

$0.95

$0.96

1.40%

Malt Beverages

$1.74

$1.75

0.70%

Boneless Chops

$4.56

$4.56

0.00%

All Other Pork Ex Can/Sliced

$3.64

$3.64

0.00%

Bananas

$0.63

$0.63

-0.50%

Lemon

$2.09

$2.07

-0.90%

All Pork Chops

$4.31

$4.26

-1.30%

Red and White Table Wine

$13.66

$13.32

-2.50%

Sliced Bacon

$6.96

$6.77

-2.60%

Spaghetti and Macaroni

$1.43

$1.38

-4.00%

Chicken Legs Bone In

$1.95

$1.86

-4.60%

Fresh Fortified Whole Milk

$4.21

$4.01

-4.80%

Coffee

$6.47

$6.09

-5.80%

Boneless Chicken Breast

$4.35

$4.08

-6.10%

Dried Beans

$1.70

$1.59

-6.40%

Dry Pint Fresh Strawberries

$3.86

$3.57

-7.30%

Center Cut Bone In Chops

$4.67

$4.33

-7.40%

Natural Cheddar Cheese

$6.00

$5.55

-7.50%

Field Grown Tomatoes

$2.23

$2.00

-10.50%

Romaine Lettuce

$3.57

$2.68

-24.80%

Grade A Large Eggs

$4.25

$2.51

-41.00%

Avocado prices, according to the Mexico Products CPI, have risen 27.2 percent from December 2019 (83.80) to December 2023 (106.554). From December 2022 (95.922) to December 2023, they rose 11.1 percent.

Determining the average price of a delivery pizza is more difficult. In local contexts, the price of a slice of pizza can act as an inflationary benchmark of sorts, but estimates indicate that from February 2023 to February 2024 the price of an average delivery pizza has increased from $17.81 to $18.33, or 2.9 percent.

Comparing these numbers with the year-over-year headline and core CPI numbers (3.4 percent and 3.9 percent, respectively), two significant insights emerge. The individual price changes above, over a four- and one-year period, frequently underscore how price indices obscure trends in prices which, at specific times can be considerably graver than the headline figures suggest. Second, that one needn’t be anywhere near Las Vegas to feel the damage of expansionary monetary policies acutely. Well over a year after the lies about Vladimir Putin, gas station owners, ocean shippers, and corporate profits have been told and forgotten, and despite the cynical political impudence of calling a massive green spending bill an “Inflation Reduction Act,” spending Super Bowl Sunday at home in 2024 will be much more expensive than it was in 2023, and vastly more than it was four short years ago.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.