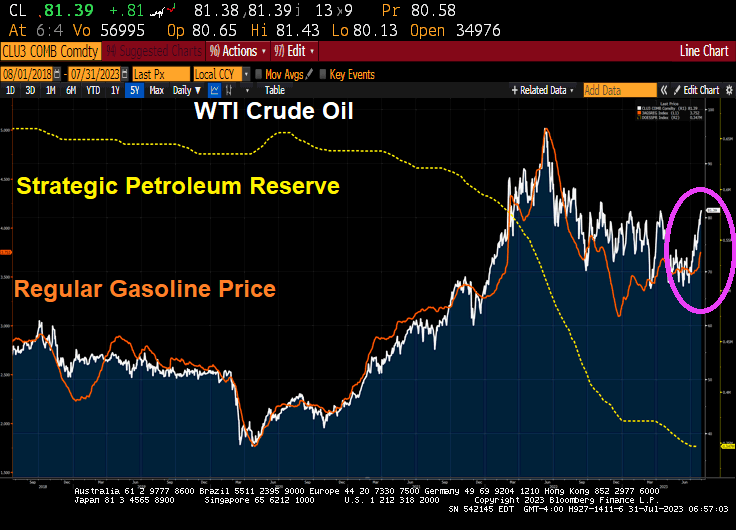

But on the middle class front, we can see “cheap rates” are a thing of the past as markets have to deal with Biden’s inflation problem and Fed rate hikes.

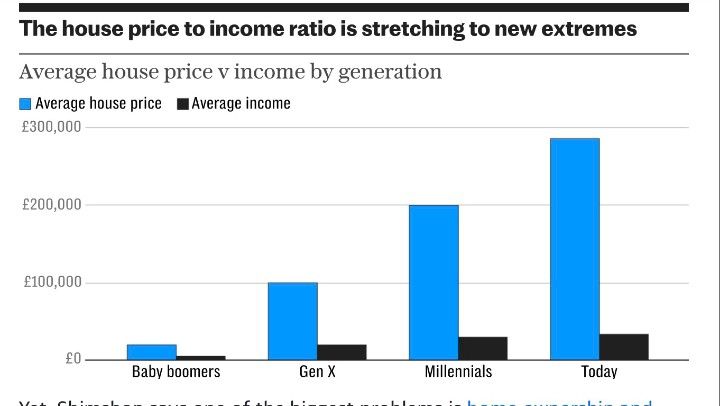

And with rising home prices under Biden, the house price to income ratio is out of control and causing pain for the middle class.

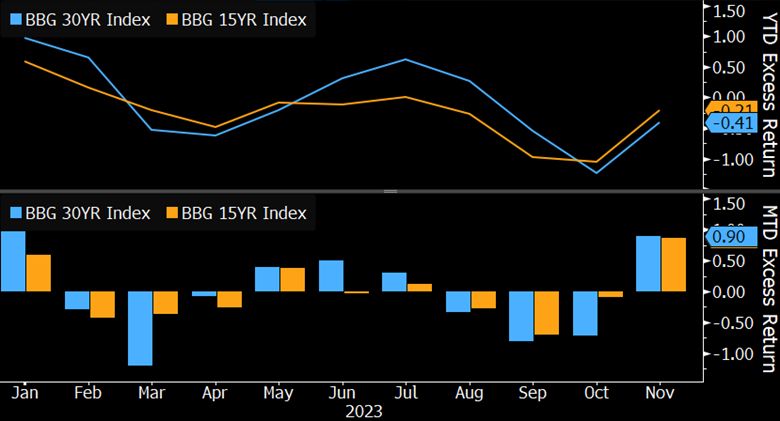

On the MBS front, we see negative returns.

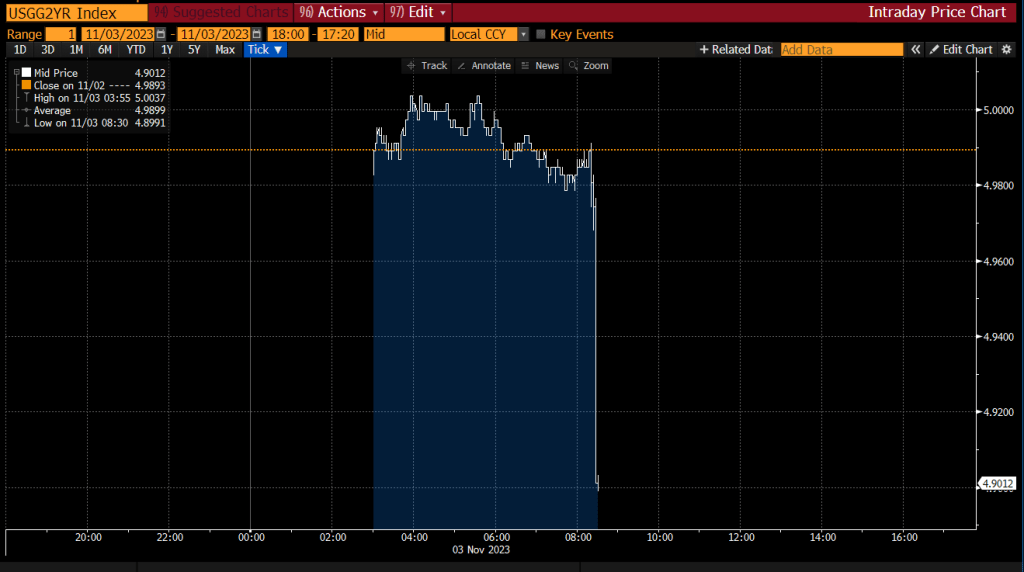

The 2-year Treasury yield is dropping faster than Biden’s polling numbers.

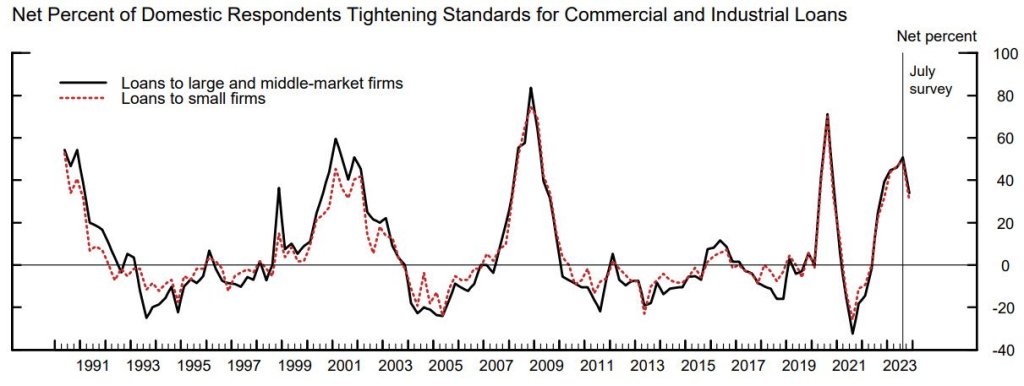

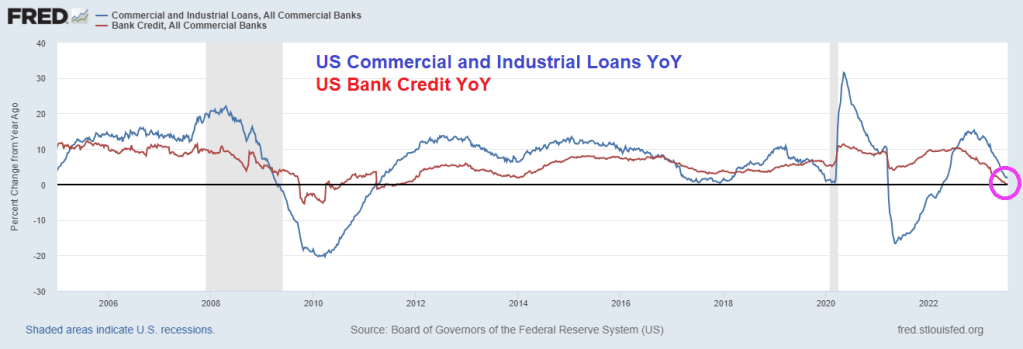

On the credit side, more lenders are tightening standards for C&I loans.

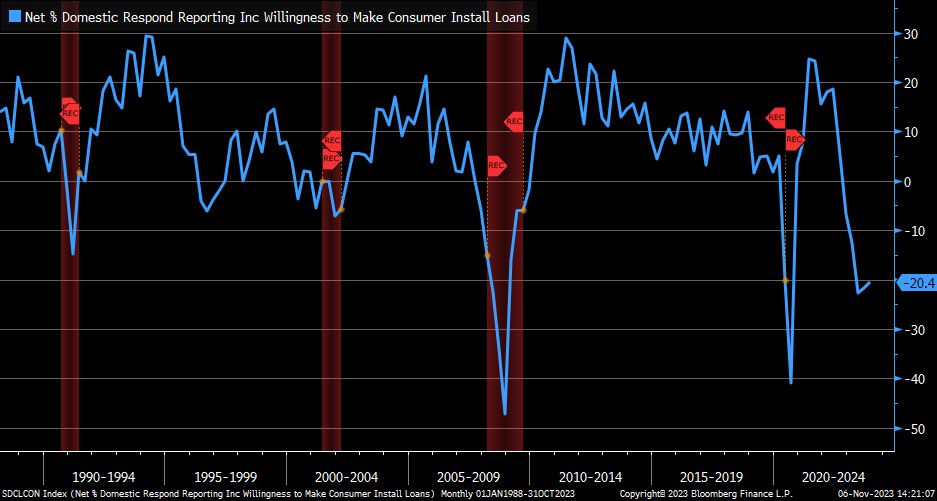

And banks remained restrictive in their willingness (or lack thereof) to make consumer loans, but there was a marginal improvement from prior release.

On the global front, Maersk announces plans to cut at least 10,000 jobs due to weakening global trade.

Here is a picture of Hinky Dink (Joe Biden) and Bathhouse Barry Soetoro. I mean Bathhouse John Coughlin, the Lords of the Levee.

Back in red? As US fiscal policy deteriorates further thanks to endless Federal spending (not to mention seemingly endless wars under Biden and Nobel Peace Prize winner Obama), we are seeing pain in the bank lending business.

Commercial and industrial (C&I) loan lending standards is tightening (blue line) to levels typically seen in recessions. Even though Barclays HY-10Y spreads remains low.

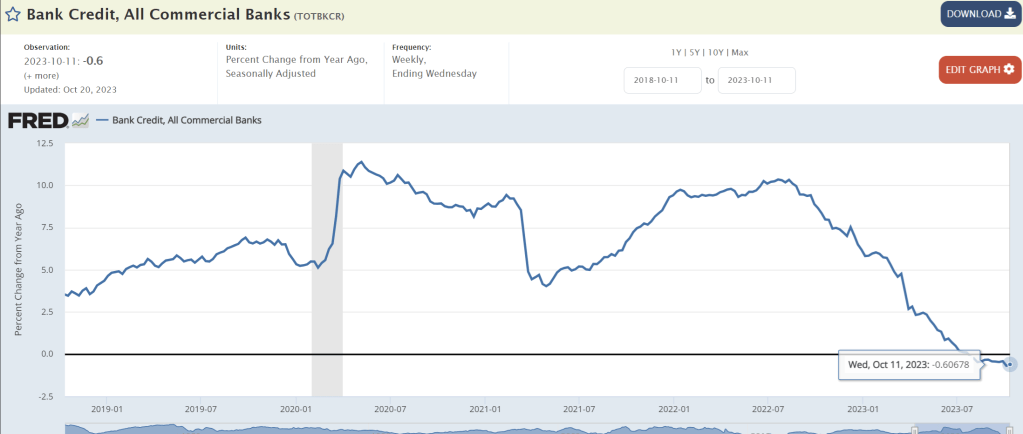

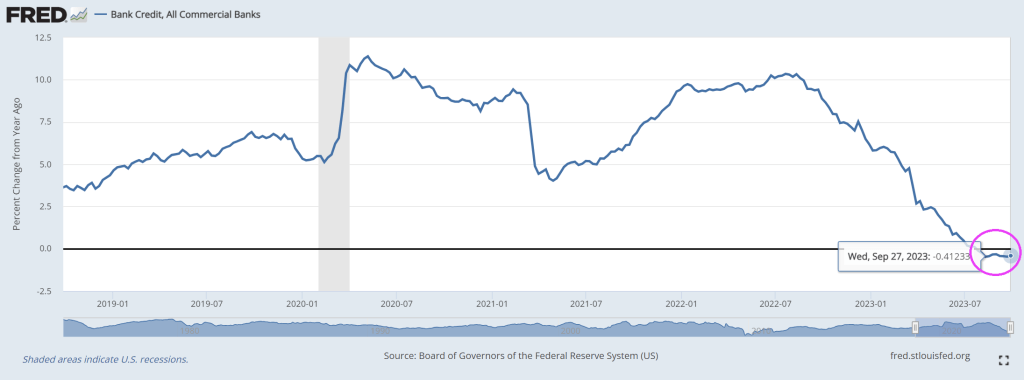

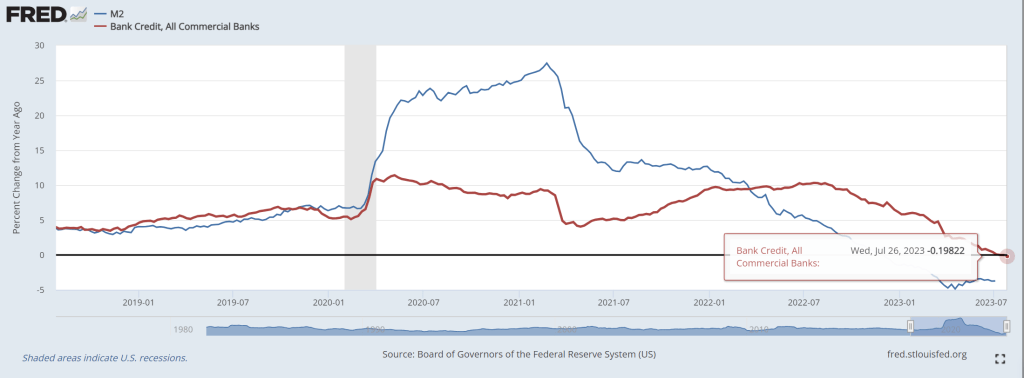

Bank credit growth remains negative for the twelve straight week.

Billions Biden’s spending spree has led to the budget gap has doubled in the last year.

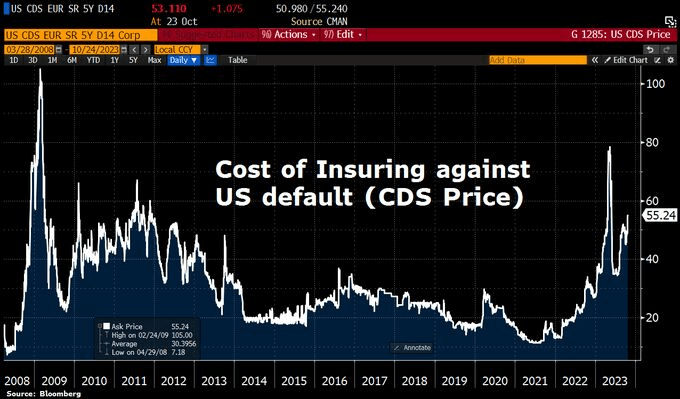

CDS is now at 55.24, highest after the Covid shock.

Under Biden/Yellen’s economic model, the appropriate themesong is “Hell’s Bells.”

Bidenomics is failing catestropically. Example? As interest rates rise to fight Biden’s Federal spending splurges, bank credit growth slowed to -0.41% YoY for the 10th straight week of negative credit growth.

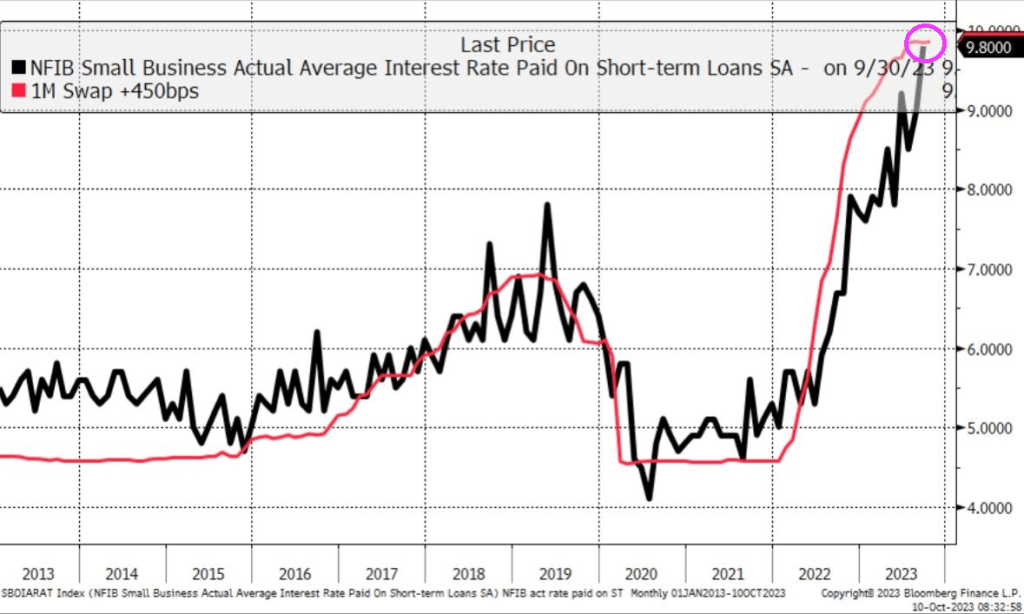

While interest paid on short-term loans almost 10%!!

“Jimmy, watch me tank the economy even worse than you did!”

Fear the talking Fed! Various Fed Presidents are talking this week and when they do. WATCH OUT!

The latest fear mongering will be … inflation is persistent and they might have to keeep raising rates.

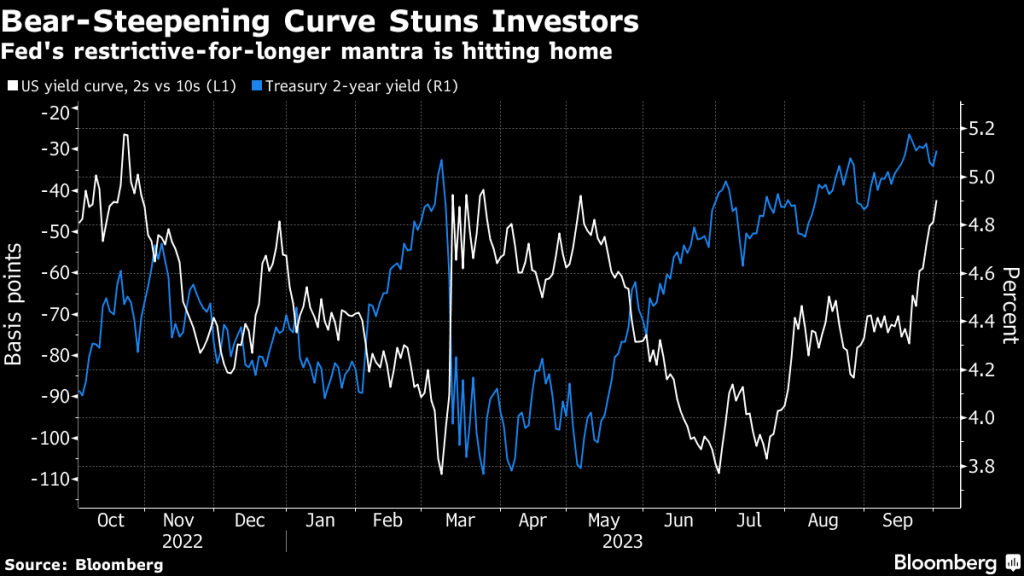

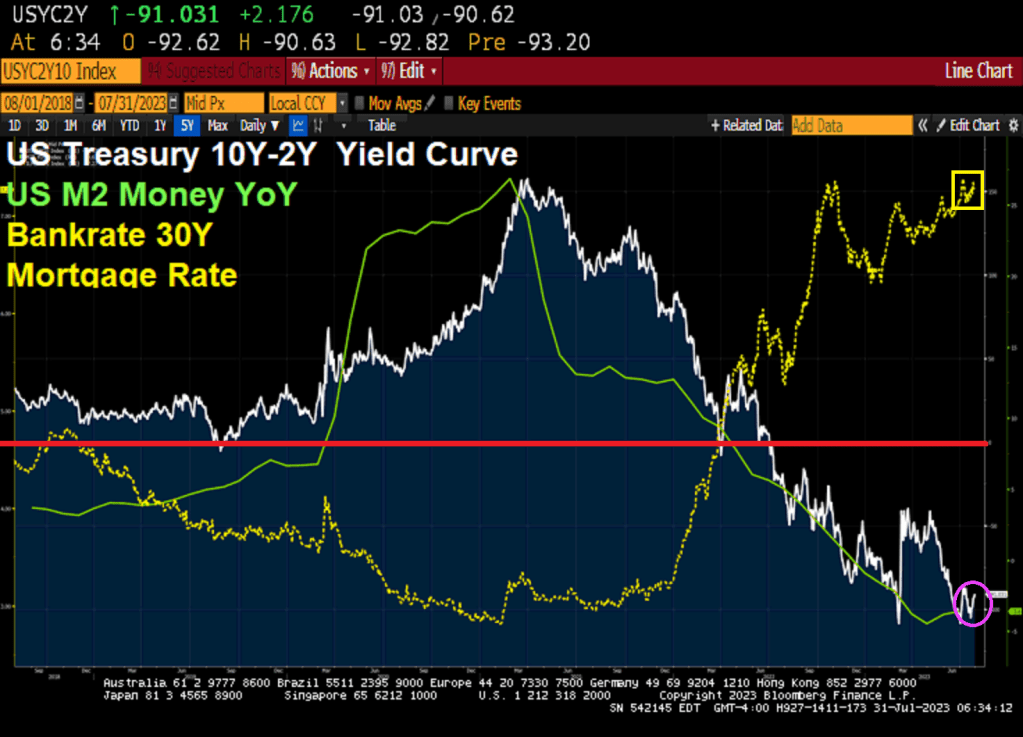

The two-year Treasury remains above 5% and the 10Y-2Y T-Curve remains inverted.

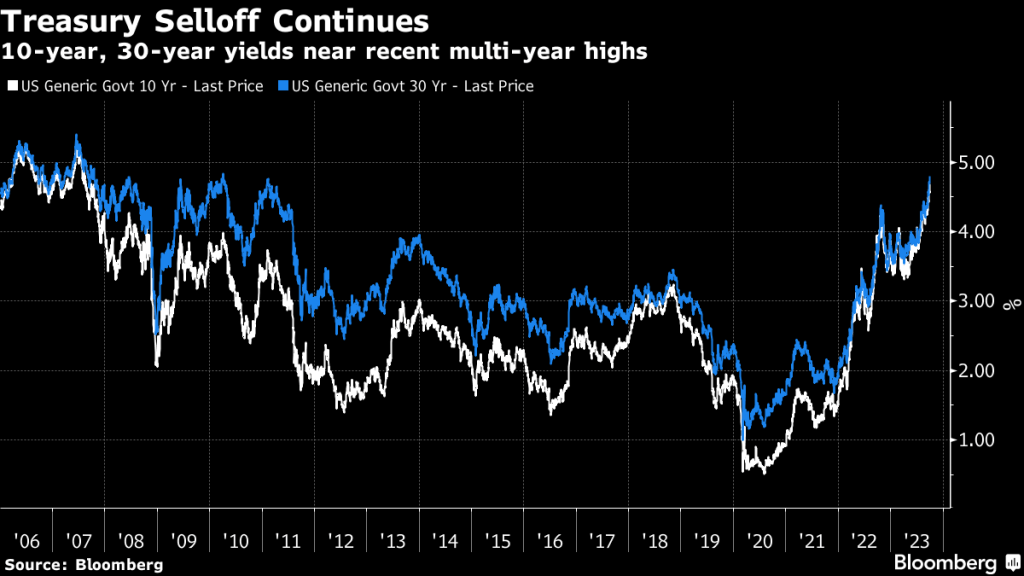

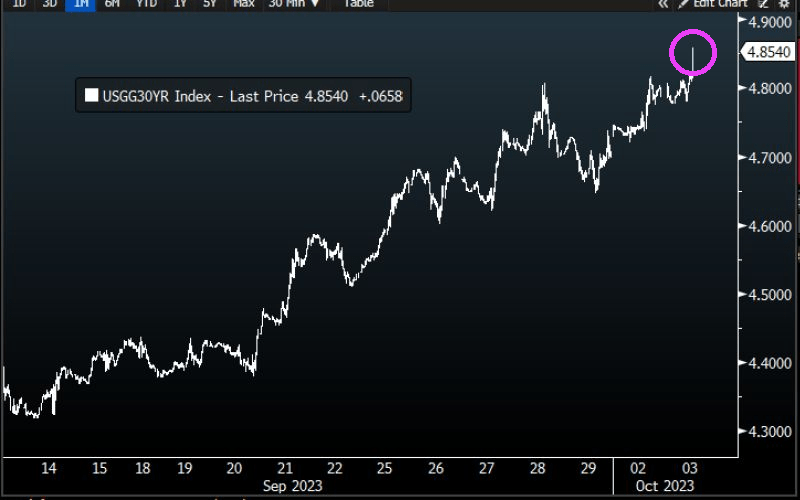

Treasury 30-year yield rose to 4.856%, HIGHEST SINCE 2007.

The likelhood of another Fed rate hike is growing.

While inflation is cooling (but still elevated), The Fed could choose to rate hikes again.

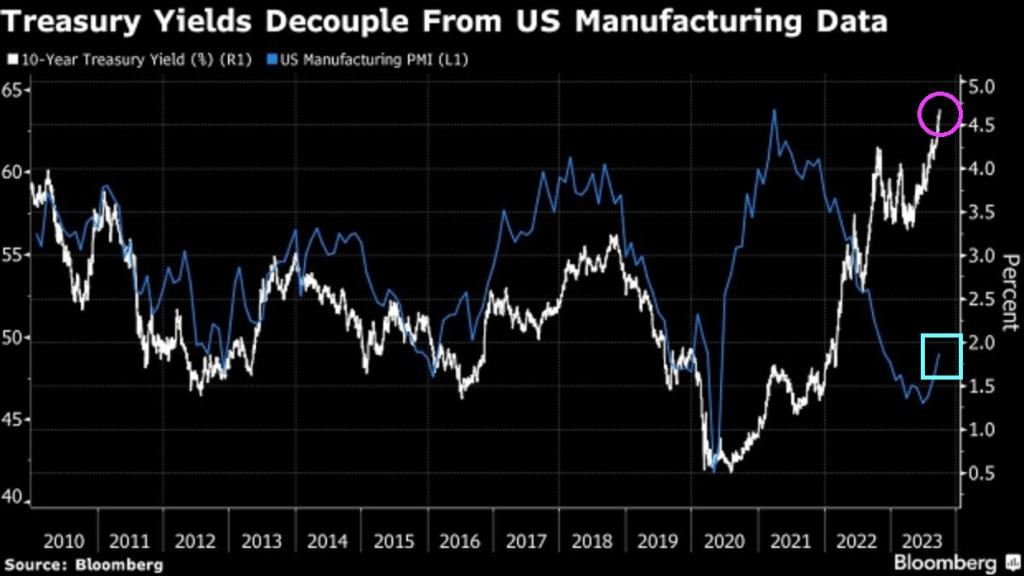

Treaury yields have decoupled from US manufacturing data.

Best picture of Lael Brainard, Director of the National Economic Council of the United States and former Federal Reserve member and talking head. Or screaming head.

As Bidenomics fails to do anything other than make big donors wealthier (green energy companies, big tech and union bosses, etc), we are seeing the impacts of Fed monetary tightening to combat inflation caused by Biden/Pelosi/Schumer’s spending spree.

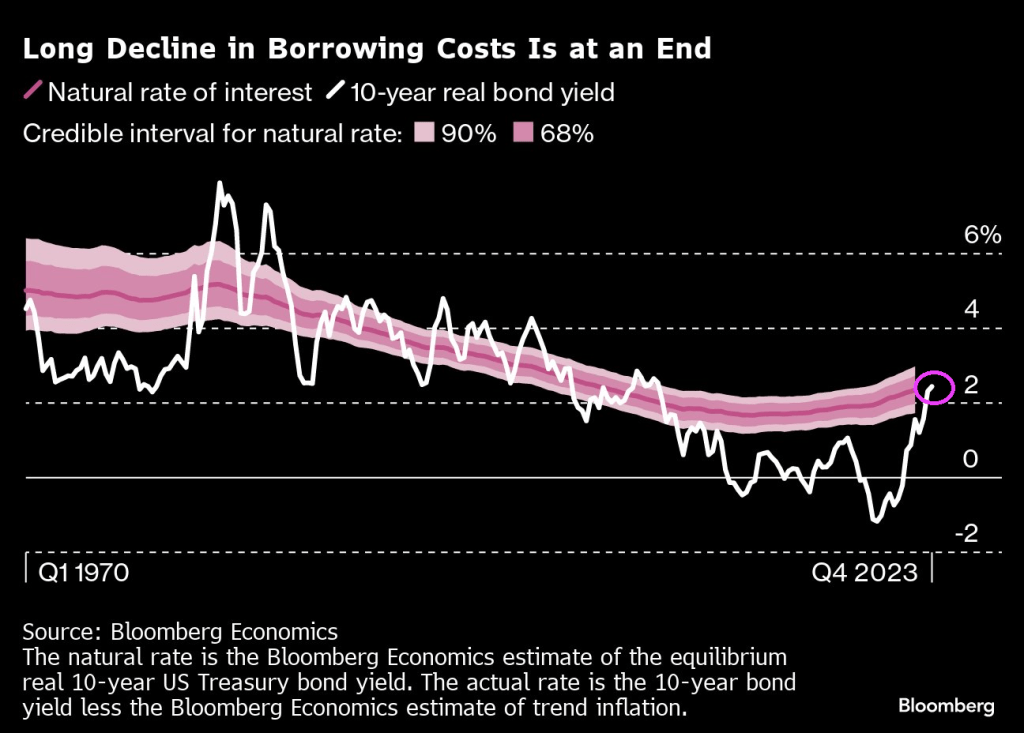

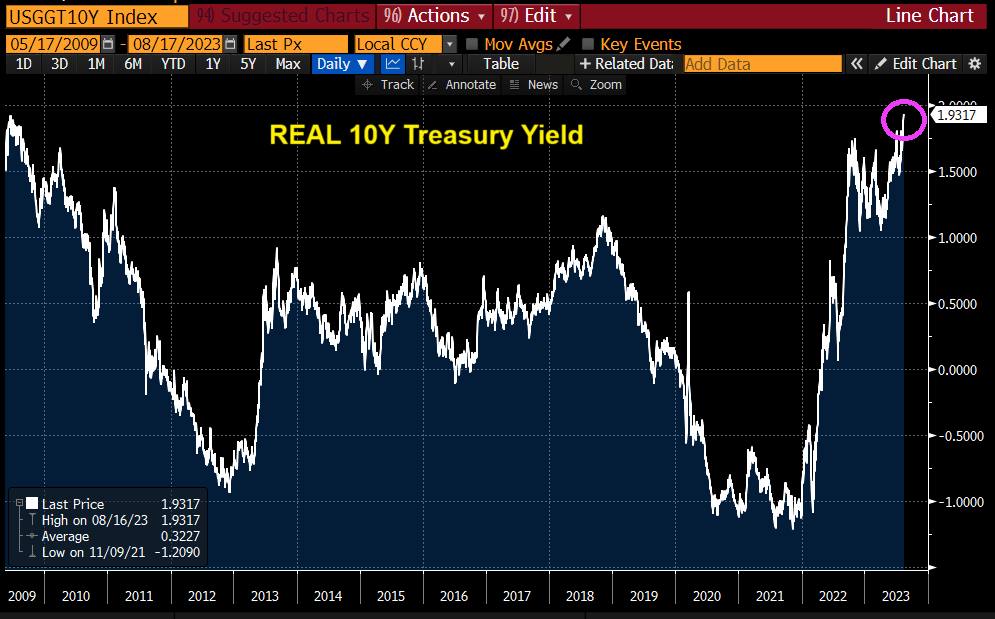

First, the 10-year REAL Treasury yield is close to breaching 2%.

Second, 30-year mortgage rates are now 7.62%, up over 150% under Bidenomics.

Third, mortgage purchase applications crashed to the lowest level since 1995.

Fourth, the 2-year Treasury yield just breached 5%.

Fifth, the 10Y-2Y yield curve remains deeply inverted.

This is very strange. Global Treasury Yields just rose to a 15-year high (2008). This is primarily due to Central Bank moneta

And REAL 10-year Treasury yields also the highest since 2009.

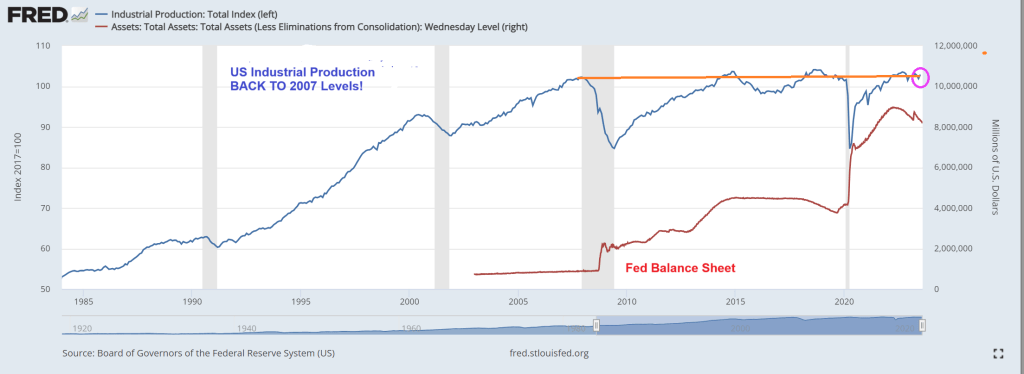

At the same time, US industrial production is at the same level as pre-financial crisis (2007). Despite Federal Reserve monetary stimulypto (remember, The Fed’s balance sheet remains abouve $8 trillion.

This is Obama/Biden/Yellenomics. Trillions of dollars of fiscal (green) stimulus and monetary stimulus only to have industrial production be at the same level BEFORE The Great Recession and financial crisis.

We quickly found out in June that one downtown San Francisco office building sold for roughly 70% less than its previously estimated value, an ominous sign of what would come as the commercial real estate market dominos appear to be falling.

Now Sixty Spear St., an 11-story building that is 30% occupied and is expected to be entirely vacant by summer 2025, has been sold to Presidio Bay Ventures for $40.9 million, about a 66% discount versus the most recent assessed property value of $121 million, according to local media SFGATE.

“We acknowledge the formidable challenges that confront San Francisco,” Cyrus Sanandaji, founder and managing principal of Presidio Bay, who is now the office tower’s proud new owner. He remains a bull on the San Francisco office market and wants to expand the building’s square footage from 157,436 to 170,000 square feet and transform it into a “Class-A trophy office building with exceptional design and hospitality-driven amenities.”

All we have to say to Sanandaji’s CRE bet is good luck. The crime-ridden metro area covered in poop must come to terms with City Hall’s horrendous progressive policies that have entirely backfired and led to an exodus of businesses and people. Until Mayor London Breed can instill law and order once more — the ability for the downtown area to thrive once more will remain challenging.

Marc Benioff, the chief executive officer of Salesforce, the city’s largest employer and anchor tenant in its tallest skyscraper, warned last month that the metro area is in danger. He offered a grim outlook: The downtown area is “never going back to the way it was” in pre-Covid times when workers commuted to offices daily.

“We need to rebalance downtown,” Benioff said, adding Breed needs to initiate a program to convert dormant office space into housing and hire additional law enforcement to restore law and order.

… and documenting how the downtown area has rapidly transformed into a ghost town is Youtuber METAL LEO, who walks around with a video camera, revealing empty stores, malls, and towers.

Besides Sixty Spear, SFGATE provided data on other recent tower transactions:

The 13-story 180 Howard St. building, known for being the headquarters of the State Bar of California, sold for about $62 million after being expected to sell for about $85 million.

The offices at 350 California St. reportedly sold for roughly 75% less than its previously estimated value in May, and the 22-story Financial District edifice mostly sits empty. Just a few weeks later, nearby 550 California changed hands for less than half of what owner Wells Fargo paid for the building in 2005.

Things are so bad that some building owners are just walking away from properties:

If you’re curious where we could be in the CRE crisis cycle, a recent analysis by CoStar Group shows 55% of office leases signed before the pandemic that were active during Covid haven’t expired, meaning vacancies will continue to rise.

Here’s what could be next: The collapse of WeWork will only cause more pain for CRE markets nationwide. The coworking company occupies 16.8 million square feet across the US.

Bidenomics, which is also Yellenomics (the former Fed Chair and current Treasury Secretary) has The Good, The Bad and The Ugly to say for it.

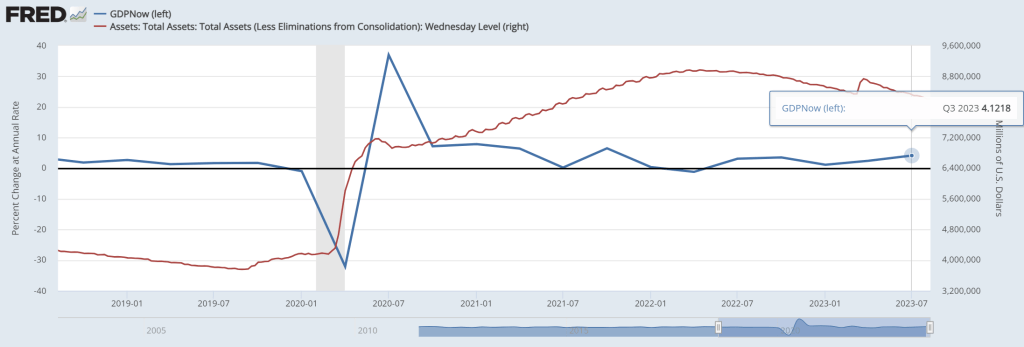

First, The Good! The Atlanta Fed’s GDP Now real time GDP tracker has Q3 GDP at … 4.12%. Pretty good, but bear in mind that there is still more than $8 trillion in Fed Monetary Stimulus outstanding (aka, Yellenomics).

Second, The Bad. Bank credit growth is now negative.

As lenders are tightening credit standards for commercial and industrial loans.

The ugly? There are several candidates for this dishonor.

One, The Conference Board’s leading economic indicators is down -10.

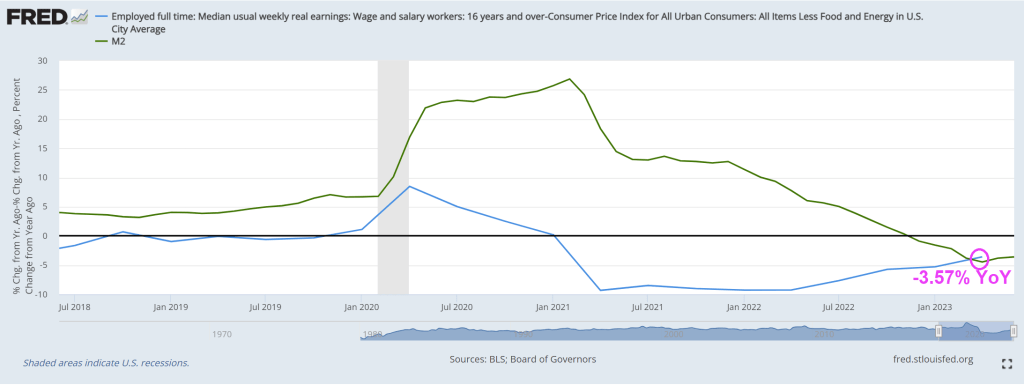

Two, REAL median weekly earnings growth remains negative at -3.57% YoY.

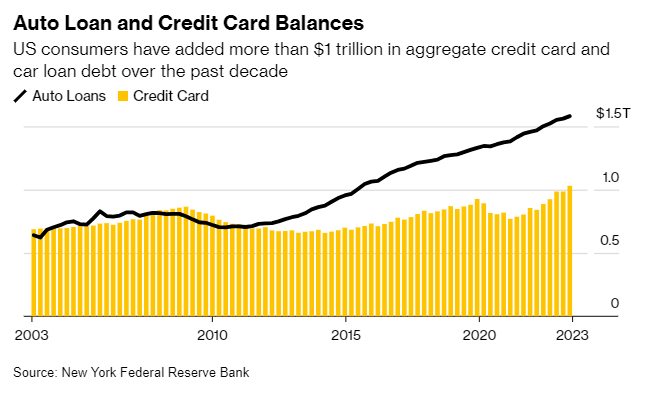

Third, auto loan and credit card balances are at $1.5 TRILLION making further consumer credit more difficult to finance GDP growth.

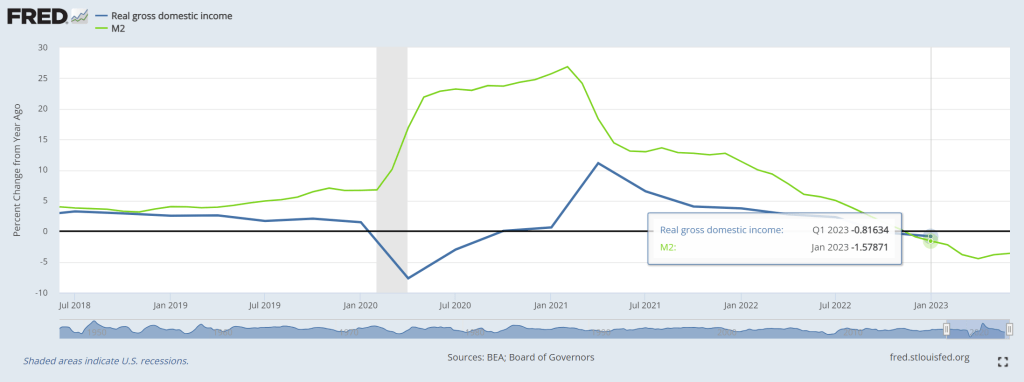

Fourth, Real Gross Domestic Income growth was negative in Q1 2023.

I could go on and on about the negatives of Bidenomics (e.g., massive distortion of Federal spending towards green energy and big donors). Isn’t the earth moving closer to the Sun in its elliptical orbit?? HOW is spending trillions on green energy work as we move closer to the Sun??

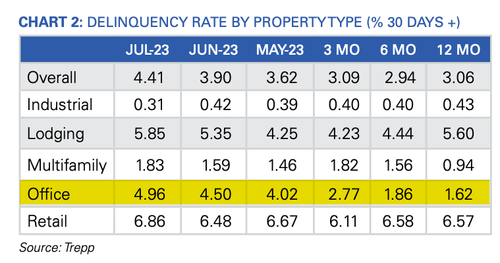

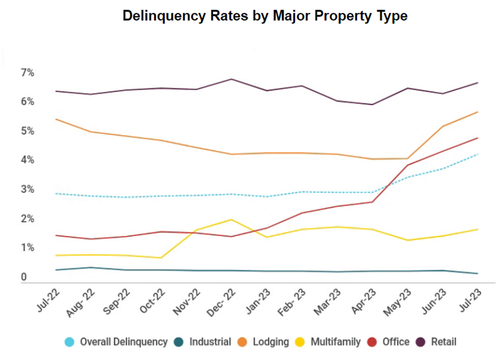

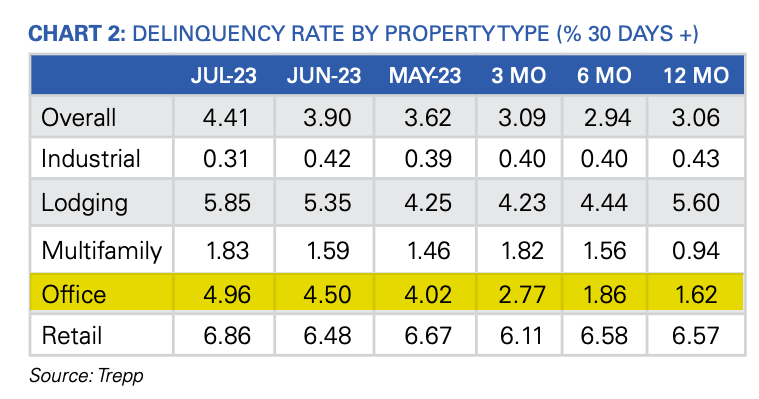

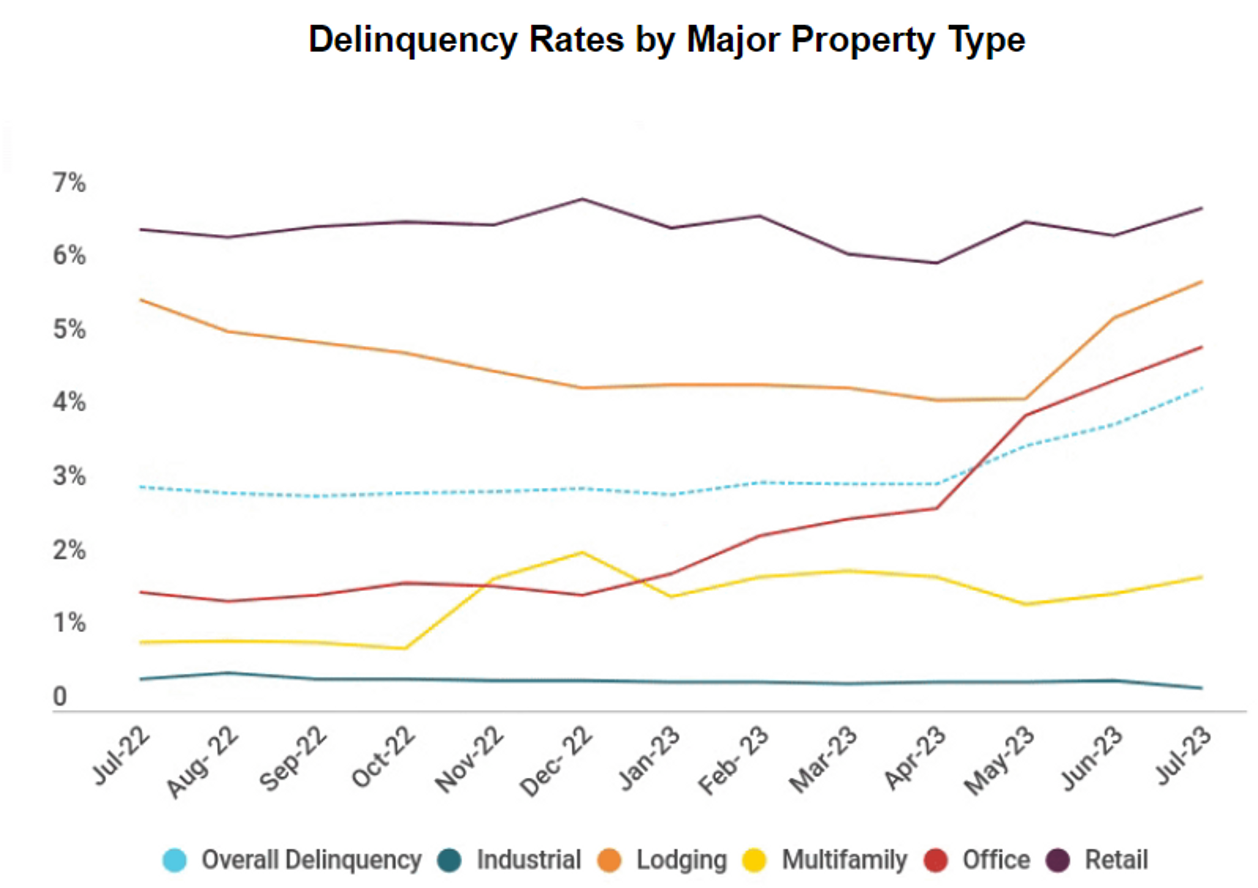

The latest data from Trepp, which tracks commercial mortgage-backed securities (CMBS) securities market data, shows the delinquency rate of commercial property loans packaged up by Wall Street jumped again in July, with four of the five major property segments posting increases.

“While the rest of the US economy has seen relief in terms of higher equity prices, better-than-expected corporate earnings, and falling inflation numbers, the commercial real estate (CRE) market continues to be left behind,” Trepp wrote in the report.

Trepp data found the delinquency rate rose 51 basis points to 4.41% last month — the highest level since December 2021. Office delinquencies increased by 46 basis points to 4.96% — up more than 350 basis points since the end of 2022. The deterioration in the office segment is intensifying at an alarmingly rapid pace.

A broad overview of the US CMBS market shows the delinquency rate increased to 4.41%, a 51bps rise compared to the previous month, but still significantly lower than the 10.34% rate recorded in July 2012. The rate peaked at 10.32% in June 2020 during the government-forced Covid lockdowns.

Here are more highlights from the report:

Year over year, the overall US CMBS delinquency rate is up 135 basis points.

Year to date, the rate is up 137 basis points.

The percentage of loans that are seriously delinquent (60+ days delinquent, in foreclosure, REO, or non-performing balloons) is now 3.92%, up 20 basis points for the month.

If defeased loans were taken out of the equation, the overall headline delinquency rate would be 4.64%, up 51 basis points from June.

One year ago, the US CMBS delinquency rate was 3.06%.

Six months ago, the US CMBS delinquency rate was 2.94%.

To better understand what might come next for the CRE market, Kiran Raichura, Capital Economics’ deputy chief property economist, recently warned in a note to clients that the office segment might experience a 35% plunge in values by the second half 2025 and “is unlikely to be recovered even by 2040.”

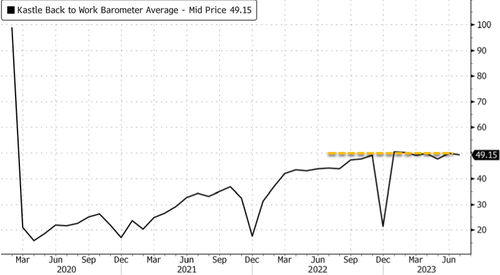

According to swipe data from Kastle Systems, the US office occupancy rate is less than 50%. The figure has plateaued since September, indicating a new reality of remote work.

One major hurdle for CRE space is that “more than 50% of the $2.9 trillion in commercial mortgages will need to be renegotiated in the next 24 months when new lending rates are likely to be up by 350 to 450 basis points,” Lisa Shalett, chief investment officer for Morgan Stanley Wealth Management, wrote in a note to clients.

Shalett expects a “peak-to-trough CRE price decline of as much as 40%, worse than in the Great Financial Crisis.”

Bank of America analysts expect challenges in the CRE space but noted, “They are manageable and do not represent a systemic risk to the US economy.”

Meanwhile, analysts at UBS warned:

“About $1.3 billion of office mortgage loans are currently slated to mature over the next three years.

“It’s possible that some of these loans will need to be restructured, but the scope of the issue pales in comparison to the more than $2 trillion of bank equity capital. Office exposure for banks represents less than 5% of total loans and just 1.9% on average for large banks.”

We’ve already seen major building owners returning their office towers and malls to lenders in California (here & here) and elsewhere (here). This will result in an uptick in CMBS delinquencies moving forward.

Bidenomics, aka the Federal government takeover of the US economy with Soviet-style economic central planning, is highly dependent on loose Federal Reserve monetary policy (Janet Yellen and Powell’s wild overreaction to the massively inappropriate Covid shutdowns),

So, how is Bidenomics working out? On the bank lending front, commercial and industrial (C&I) lending growth is crashing along with bank credit growth YoY.

The US Treasury 10Y-2Y yield curve remains deeply inverted at -91.031 basis points and M2 Money growth has crashed. The 30 year mortgage rate is hovering around 7.27%.

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.