Joe Biden is an incredibly weak President. I am not talking about his age or his deteriorating mental faculties. I am talking about ordering his attorney general to indict his chief political opponent, Donald Trump. How does the world interpret this weakness? BADLY.

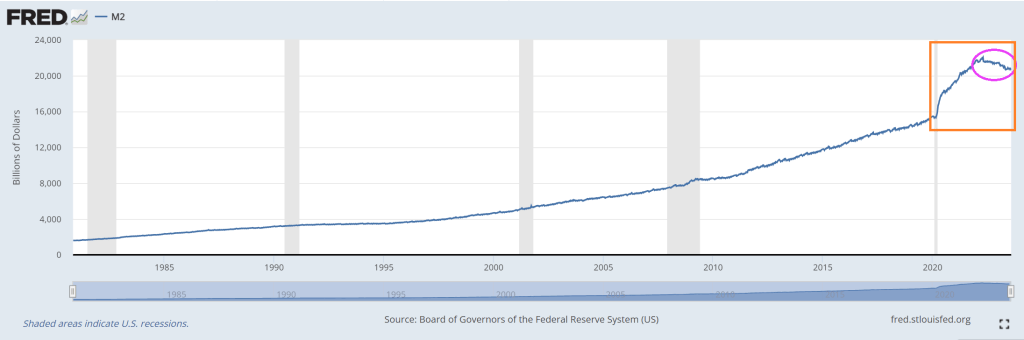

The US has gone off the rails in terms of printing money, particularly since COVID struck and money printing went wild.

Under Biden’s Reign of Error and the US reckless money printing, more countries are abandoning King Dollar (based of fiat currency) and joining BRICS. Brazil, Russia, India, China, South Africa and a host of countries joining like Argentina, Saudi Arabia, Iran, Egypt, UAE, etc.

Now, the rest of the world is still stuck on the US Dollar as reserve currency … for now. But as Biden gets weaker and weaker, watch more countries join BRICs.

According to Reuters, there are over 40 countries that have expressed interest in joining BRICS. A smaller group of 16 countries have actually applied for membership, though, and this list includes Algeria, Cuba, Indonesia, Palestine, and Vietnam. Pretty soon, under Biden’s crazy leadership, we may be the last man standing in using the US Dollar as reserve currency.

Then we have the other shoe dropping with Bidenomics.

As soon as Biden took office, he set out to destroy industries that produce reasonably priced energy. He focused tremendous effort on deficit spending and borrowing to hand out “government goodies” to buy votes; recipients of this government largesse, in large part, included debt-saddled students, the green mafia, and leftist activists.

When Biden took office, inflation was under 2%, despite COVID and supply chain disruptions; shortly after, it skyrocketed to over 9%. Now inflation increases are “down” but prices remain exceptionally high compared to pre-Biden.

For example, crude oil prices, which affect almost everything and are used in over 6,000 products, are roughly double what they were when Biden took over.

President Trump focused on reduced regulations and energy independence, and implemented lower tax rates, all moves that greatly helped the American people. In contrast, Biden focuses on ensuring bureaucrats rapidly increase regulations which raises costs for everyday Americans; he’s waging economic war against us. Very few of Biden’s regulations go through Congress. From the White House archives:

Between FY 2017 and FY 2019, the Trump Administration has cut nearly eight regulations for every new, significant regulation….

The Council of Economic Advisers (CEA) estimates that this pro-growth approach to Federal regulation will raise real incomes by upwards of $3,100 per household per year.

Here are some recent reports of how well Biden policies are working:

Leading economic indicators have fallen for sixteen straight months. Maybe that is why people think the economy is moving in the wrong direction?

The current cost-of-living crisis is a manufactured one. As inflation rose, the Federal Reserve was forced to raise interest rates, which saw fewer people move. The cycle is very understandable, as simply explained in this one headline, “Housing Crunch: Home Sales Fall To Six Month Low…But Prices Rise Anyway”.

Parcel volumes are dropping by so much, freight pilots are “worried” about job security.

People are running up credit card debt and defaulting on car loans because of high inflation, and because their real wages haven’t been able to sustain them. Now, even more are falling behind on their payments. From CNN:

More Americans are failing to make payments on their credit cards and auto loans, another sign of rising financial pressure on consumers.

New credit card and auto loan delinquencies have now surpassed pre-Covid levels, according to a Wednesday report issued by Moody’s Investors Service.

After years of promoting and subsidizing electric cars, they represent around 6% of total sales, and demand is clearly slowing. It wasn’t that long ago that well-to-do people were buying these electric toys so quickly that they were placed on waiting lists; now, inventories are building because they are too impractical and expensive:

Auto News understands that there is currently a 103-day supply of unsold EVs in the United States. While it did not specify how many units are sitting on dealership lots, it says there is a higher supply of unsold EVs than any other automotive segment, except those in the ultra-luxury and high-end luxury segments with supplies also reaching over 100 days.

So what is Biden’s solution? Force people to buy them.

Here are some simple economics questions for the media and other Democrats:

Does flooding the U.S with illegals help or hurt housing availability and affordability?

Will the intentional destruction of oil and coal companies help or hurt the middle class and the poor?

Yet, the media and other Democrats brag that Biden’s economic policies are great, and when the public gives Biden poor marks, they say that we just don’t understand, and we’re not willing to get behind a candidate if they fail to make us feel “warm and fuzzy.”

Are journalists really that unaware?

Of course, they always sought to destroy Trump as his policies, even as poverty sank to record lows amongst minorities, because they don’t really care about anything but big government. According to Census data:

In 2019, the poverty rate for the United States was 10.5%, the lowest since estimates were first released for 1959.

Poverty rates declined between 2018 and 2019 for all major race and Hispanic origin groups.

Two of these groups, Blacks and Hispanics, reached historic lows in their poverty rates in 2019.

Results and facts haven’t mattered to the complicit leftist media for a long time.

And perhaps the worst mistake Biden made (amongst his laundry list of horrible mistakes, [Afghanistan retreat, not showing up to E Palestine Ohio, Bidenomics that is a payoff to green donors and BIG corporate interests, an embarrasing visit to Maui two weeks after the fire, indicting his leading political opponent, ….) is the appointment of the WORST Federal Reserve Chair (Janet Yellen) as Treasury Secretary.

Preliminary benchmark revision smaller than some had projected

Biggest payrolls adjustment in transportation and warehousing

Are you surprised that the Biden Administration has been lying about job creation?? Not really since Biden compulsively lies about everything. Including his corruption.

US job growth was probably less robust in the year through March than previously reported, according to government data released Wednesday.

The number of workers on payrolls will likely be revised down by 306,000 for March of this year, according to the Bureau of Labor Statistics’ preliminary benchmark revision.

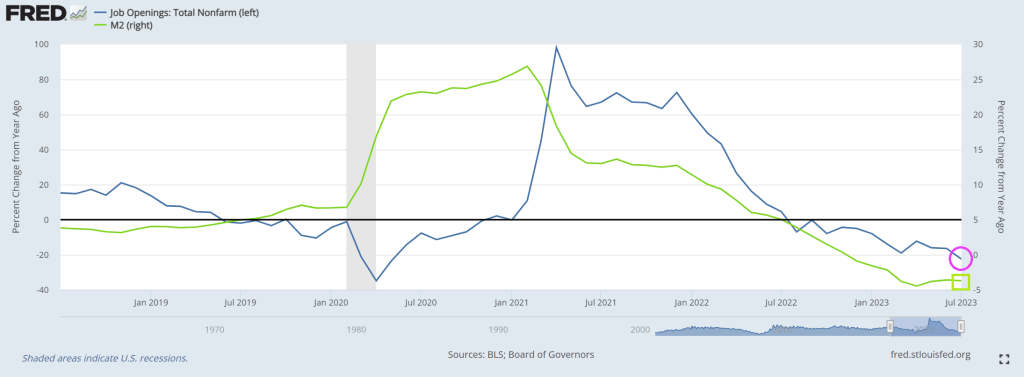

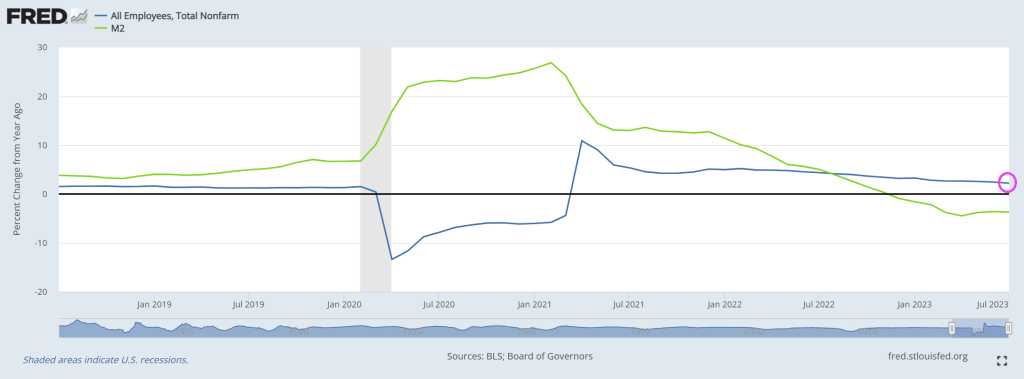

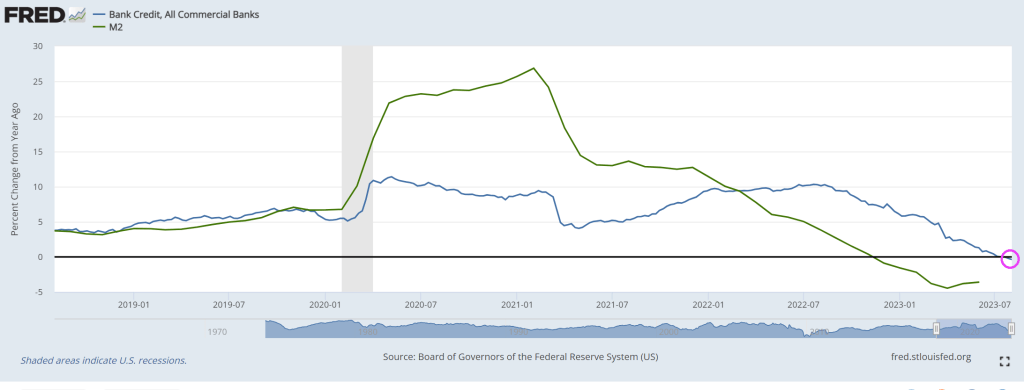

Even without the revision, job growth has slowed to 2.2% YoY in July as M2 Money growth slowed to -3.7% YoY.

Let see what our Overlords say at the Jackson Hole Fed symposium.

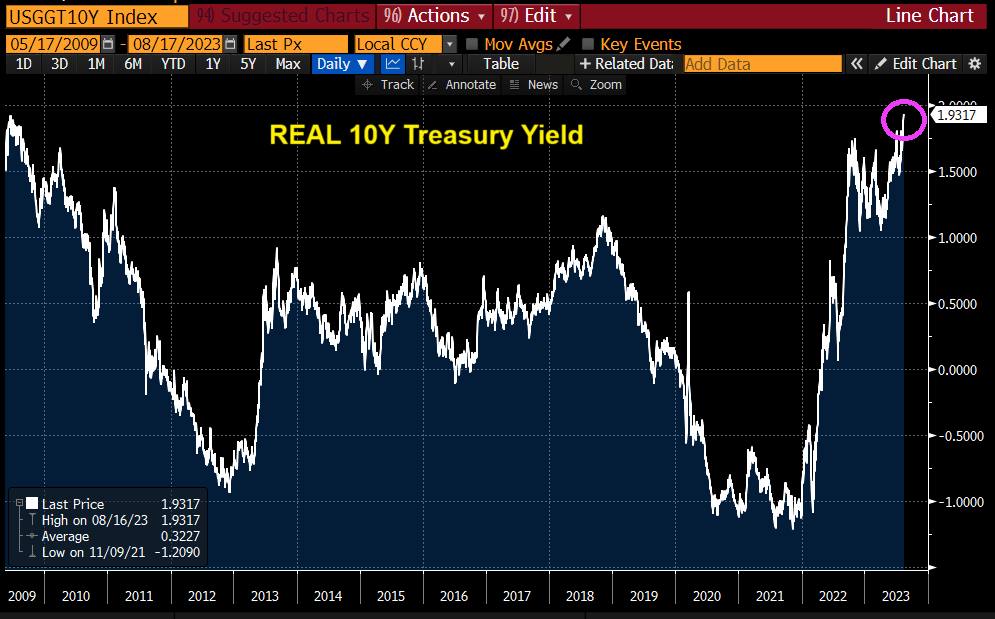

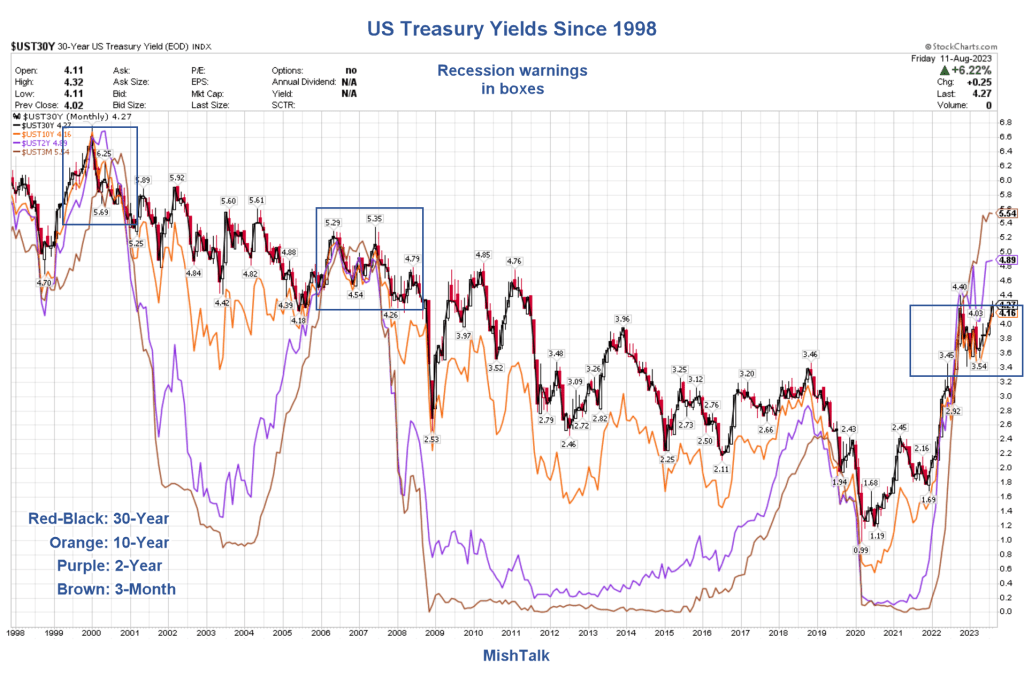

This is very strange. Global Treasury Yields just rose to a 15-year high (2008). This is primarily due to Central Bank moneta

And REAL 10-year Treasury yields also the highest since 2009.

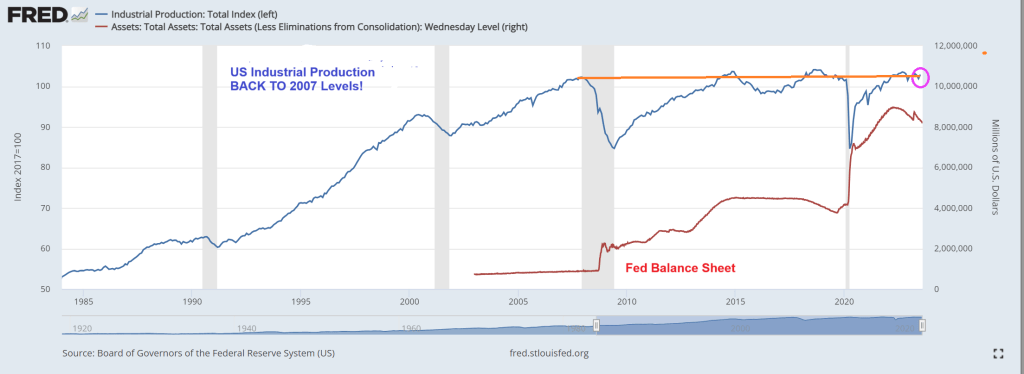

At the same time, US industrial production is at the same level as pre-financial crisis (2007). Despite Federal Reserve monetary stimulypto (remember, The Fed’s balance sheet remains abouve $8 trillion.

This is Obama/Biden/Yellenomics. Trillions of dollars of fiscal (green) stimulus and monetary stimulus only to have industrial production be at the same level BEFORE The Great Recession and financial crisis.

Well, its now August 2023 and US Industrial Production for July increased … to 2007 levels. This comes after the massive spending out of Washington DC and massive Federal Rerserve stimulus.

Is that all there is??

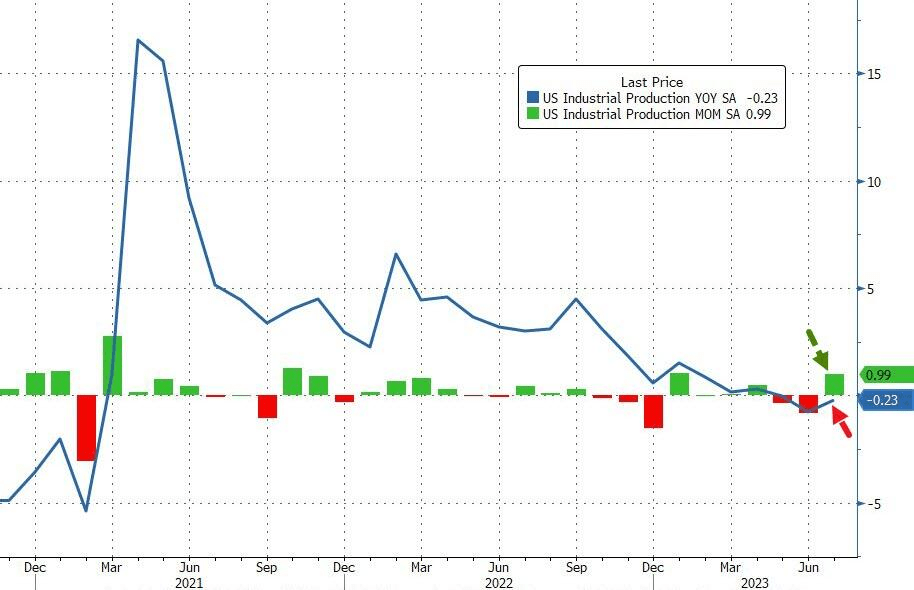

US Industrial Production is DOWN -0.23% YoY while up slightly in MoM terms.

As I said a couple of days ago, the Obama/Biden economic model is a Soviet/Chinese Communist Party (CCP) style of COMMAND economics, not free market DEMAND economics.

“Ice Cream Joe” Biden is at Lake Tahoe for a week, probably to avoid being asked questions about his tin-ear respoonse to the tragic Maui fires that have killed 106 people so far. Instead, Joe is inappropriately chuckling (showing he doesn’t care!) and taking photo ops of him eating ice cream. The Biden administration angered a lot of people when it was announced that households that have been affected by the fires would only be getting a one time emergency aid payment of $700 while he gives billions for Ukraine.

At least housing starts were up 6% year-over-year (YoY).

However, the picture was more mixed with starts rising 3.9% MoM (vs +1.1% exp), but that was impacted by a notable downward revision in June (from -8.0% to -11.7%).Building Permits rose just 0.1% MoM (well below the 1.5% MoM expected).

On a SAAR basis, Permits disappointed (1.442mm vs 1.463mm exp) while Starts were in line at 1.452mm (up from a significantly downwardly-revised 1.398mm in June).

Source: Bloomberg

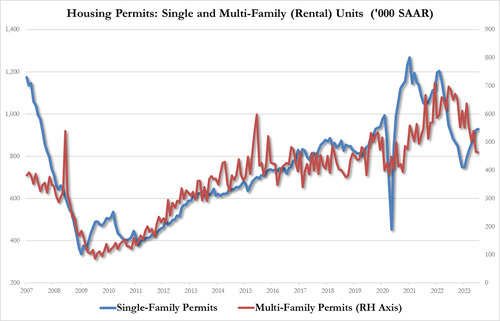

On the Permits side, single-family rose as multi-family fell:

Single-family up to 930K from 924K, highest since June 2022

Multi-family down to 464K from 465K, lowest since Oct 2020

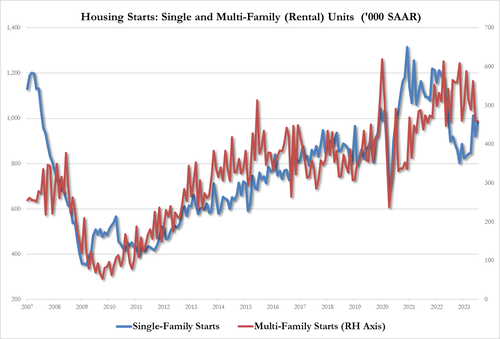

July Housing Starts data followed the same trajectory with rental units growth underperforming single-family:

single-family housing up 6.7% to 983K, up from 921K, highest since May

multi-family housing unch at 460K, tied for lowest since July 2022

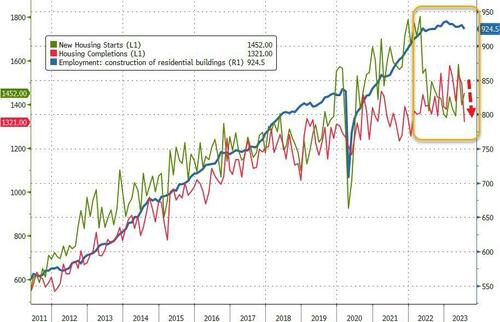

Additionally, we note that while Housing Starts and Completions remain well off their 2022 highs, Construction Jobs remain very close to those highs…

Source: Bloomberg

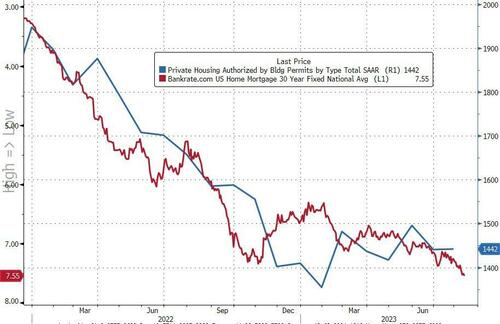

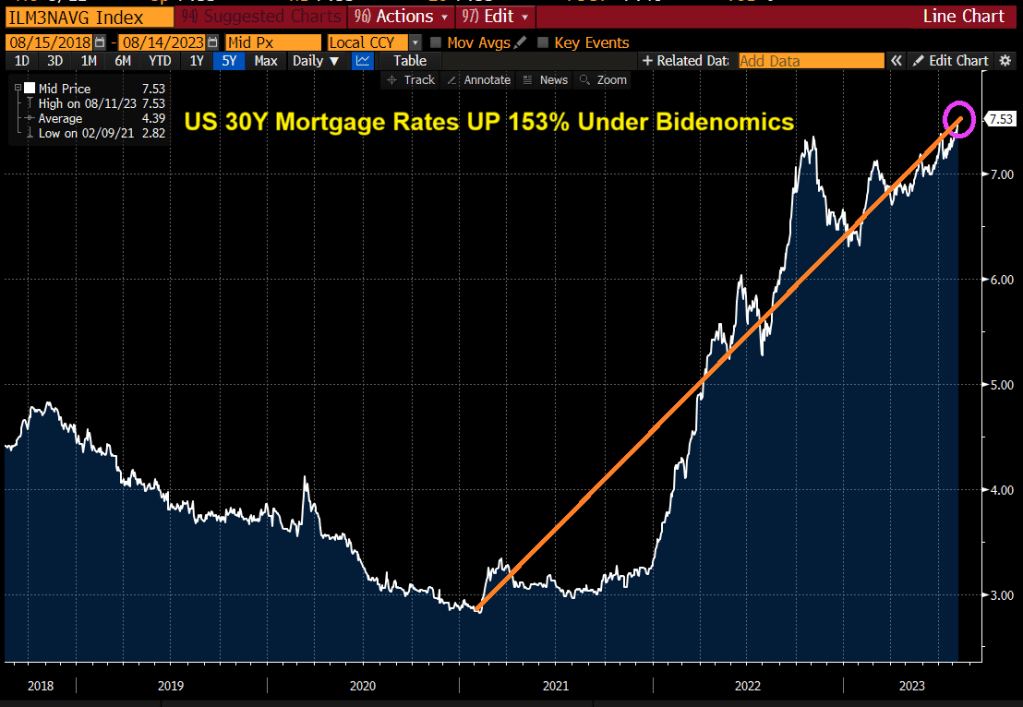

Finally, we note that Mortgage Bankers Association data released earlier this morning showed applications for home purchases dropped again last week (back near 1996 lows) as the contract rate on a 30-year fixed mortgage surged above 7% (highest since Dec 2001).

Source: Bloomberg

This won’t end well.

Speaking of not ending well, mortgage applications decreased 0.8 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending August 11, 2023.

The Market Composite Index, a measure of mortgage loan application volume, decreased 0.8 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index decreased 2 percent compared with the previous week. The Refinance Index decreased 2 percent from the previous week and was 35 percent lower than the same week one year ago. The seasonally adjusted Purchase Index decreased 0 percent from one week earlier. The unadjusted Purchase Index decreased 2 percent compared with the previous week and was 26 percent lower than the same week one year ago.

Rates on 30-year mortgages in the US are now the highest since 2000, at 7.53%. Mortgage rates are now up 153% under Bidenomics. Rates have gone from sub 3% to above 7.50% under Inflation Joe.

US Treasury yields are playing catch-up from Yellen’s “Too low for too long” monetary policies.

Yes, in part we are playing catch-up from Yellen’s Reign of Error as Fed Chair (keeping rates too low for too long). Only in Washington DC, does gross incompetance warrant a promtion to US Treasury Secretary. Career half-wit Mean Joe Biden is El Presidente and acting like a third world dictator.

Example? Take Checkable Deposits of the to 1% (blue line) of wealth compared to the bottom 50% of wealth (red line) after The Fed cranked up monetary stimulus to combat the Covid shutdowns.

On the wealth side, Covid-related monetary stimulus benefitted the top 1%.

But the middle class is expericing a tighening of credit coutesy of Cap’n Crunch (Fed Chair Powell).

We quickly found out in June that one downtown San Francisco office building sold for roughly 70% less than its previously estimated value, an ominous sign of what would come as the commercial real estate market dominos appear to be falling.

Now Sixty Spear St., an 11-story building that is 30% occupied and is expected to be entirely vacant by summer 2025, has been sold to Presidio Bay Ventures for $40.9 million, about a 66% discount versus the most recent assessed property value of $121 million, according to local media SFGATE.

“We acknowledge the formidable challenges that confront San Francisco,” Cyrus Sanandaji, founder and managing principal of Presidio Bay, who is now the office tower’s proud new owner. He remains a bull on the San Francisco office market and wants to expand the building’s square footage from 157,436 to 170,000 square feet and transform it into a “Class-A trophy office building with exceptional design and hospitality-driven amenities.”

All we have to say to Sanandaji’s CRE bet is good luck. The crime-ridden metro area covered in poop must come to terms with City Hall’s horrendous progressive policies that have entirely backfired and led to an exodus of businesses and people. Until Mayor London Breed can instill law and order once more — the ability for the downtown area to thrive once more will remain challenging.

Marc Benioff, the chief executive officer of Salesforce, the city’s largest employer and anchor tenant in its tallest skyscraper, warned last month that the metro area is in danger. He offered a grim outlook: The downtown area is “never going back to the way it was” in pre-Covid times when workers commuted to offices daily.

“We need to rebalance downtown,” Benioff said, adding Breed needs to initiate a program to convert dormant office space into housing and hire additional law enforcement to restore law and order.

… and documenting how the downtown area has rapidly transformed into a ghost town is Youtuber METAL LEO, who walks around with a video camera, revealing empty stores, malls, and towers.

Besides Sixty Spear, SFGATE provided data on other recent tower transactions:

The 13-story 180 Howard St. building, known for being the headquarters of the State Bar of California, sold for about $62 million after being expected to sell for about $85 million.

The offices at 350 California St. reportedly sold for roughly 75% less than its previously estimated value in May, and the 22-story Financial District edifice mostly sits empty. Just a few weeks later, nearby 550 California changed hands for less than half of what owner Wells Fargo paid for the building in 2005.

Things are so bad that some building owners are just walking away from properties:

If you’re curious where we could be in the CRE crisis cycle, a recent analysis by CoStar Group shows 55% of office leases signed before the pandemic that were active during Covid haven’t expired, meaning vacancies will continue to rise.

Here’s what could be next: The collapse of WeWork will only cause more pain for CRE markets nationwide. The coworking company occupies 16.8 million square feet across the US.

The US Federal Reserve has not created a CBDC … yet. Our woefully corrupt El Presidente Jose Biden (more of a Latin American, tinhorn Banana Republic dictator than as US President) has ordered the study of a CBDC. Since everything Biden touches reeks of “boodle” I am suspicious as to Biden’s motives.

There are some positives to a CBDC, mostly with WHOLESALE CBDCs. Wholesale CBDCs are similar to holding reserves in a central bank. The central bank grants an institution an account to deposit funds or use to settle interbank transfers. Central banks can then use monetary policy tools, such as reserve requirements or interest on reserve balances, to influence lending and set interest rates.

It is the RETAIL CBDC that is the cause for concern. Retail CBDCs are government-backed digital currencies used by consumers and businesses. Retail CBDCs eliminate intermediary risk—the risk that private digital currency issuers might become bankrupt and lose customers’ assets.

There are two types of retail CBDCs. They differ in how individual users access and use their currency:5

Token-based retail CBDCs are accessible with private keys or public keys or both. This method of validation allows users to execute transactions anonymously.

Account-based retail CBDCs require digital identification to access an account.

The real problem with CBDCs is that The Federal Reserve and Federal government can trace EVERY EXPENDITURE of a household. Including political contributions, firearm and ammo purchases, etc. With this much information at their disposal, this allows for DIRECT CONTROL of the population.

Given that we now know that Biden used social media platforms to pass false narratives and repress alternative views, can we trust The Federal Reserve with this much information about consumer spending? Of course not. This is a consolidation of censorship and repression of individual liberties.

Yes, paper and coin currency serve a purpose in society as an alternative to barter. Imagine trying to buy a Ford F-150 Lightning (LMAO!) using barter? Ok, we have a system of credit where you can obtain a car loan. But barter, an old system of exchange, is inefficient. That leaves us with physical currency (certain restaurants only allow payment in cash). But many consumers are using Debit Cards as a substitute for physical cash, so this is a giant step towards RETAIL CBDC already.

Alternatives to the US Dollar? Of course, gold and silver are popular choices historically. Then we have rise of the cryptocurrencie market, which some Congressional members want heavily regulated or banned. Why? First, there are some shady crypto activities (see Sam Bankman-Fried and his shady political contributions to Democrats). Second, cryptos are volatile. Why is this of any interest to Congress? Third, cryptos can be used for illegal activities (but so can cash. Just watch Netflix’s Narcos for the shipment of US Dollars to Columbia in mattresses, etc. No, the goal of some members of Congress is to overregulate or obliterate alternatives to the US Dollar … unless The Federal government does it, like The Fed’s CBDC!

With Biden’s Department of Injustic and several Democrat state Attorney Generals indicting Biden’s top political opponent Donald Trump with the intent of preventing him from campaigning for President (sounds so much like other Totalitarian regimes in history), trust in the Federal government and Federal Reserve are almost nonexistant.

Here is chart of the purchasing power of the US Dollar (blue line) since the creation of The Federal Reserve system and core CPI YoY which is still relatively high at 4.86%. That is over twice The Fed’s target rate of 2%.

I am sure that Billions Biden doesn’t understand moral hazard risk. For him, there is no risk, But for the middle class and lower wage worker class, CBDC represent a clear moral hazard risk, particularly if cash vanishes and Congress tries to ban cryptos.

The face of why so many Americans don’t trust The Fed. Or The Biden Administation.

Or this face, Urban Joe Biden (Stalin was Country Joe).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.