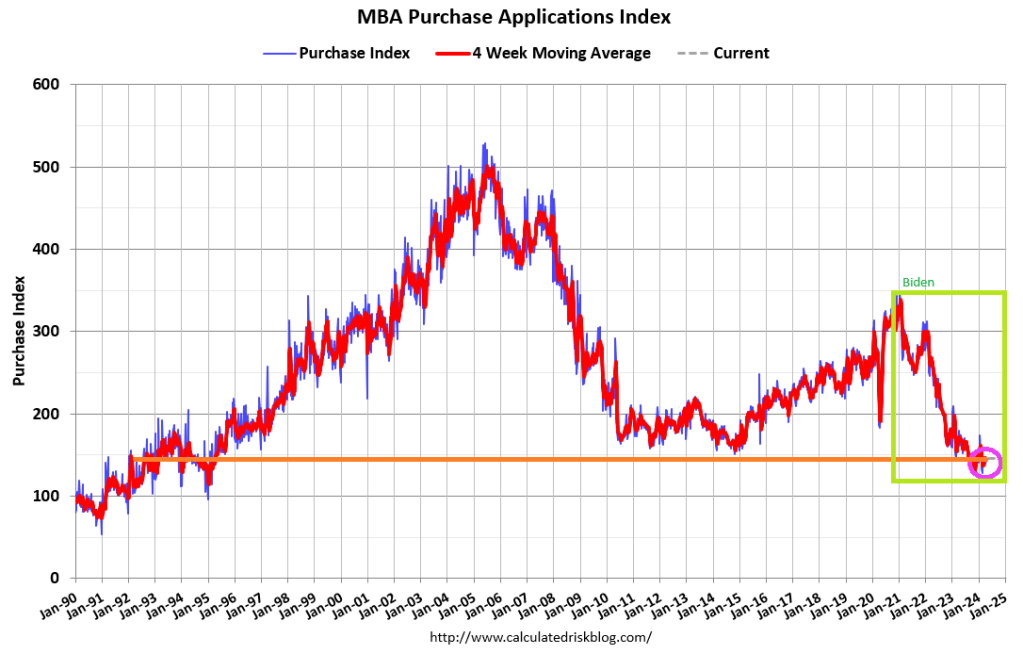

Mortgage applications increased 3.3 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending April 12, 2024.

The Market Composite Index, a measure of mortgage loan application volume, increased 3.3 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index increased 4 percent compared with the previous week. The seasonally adjusted Purchase Index increased 5 percent from one week earlier. The unadjusted Purchase Index increased 6 percent compared with the previous week and was 10 percent lower than the same week one year ago.

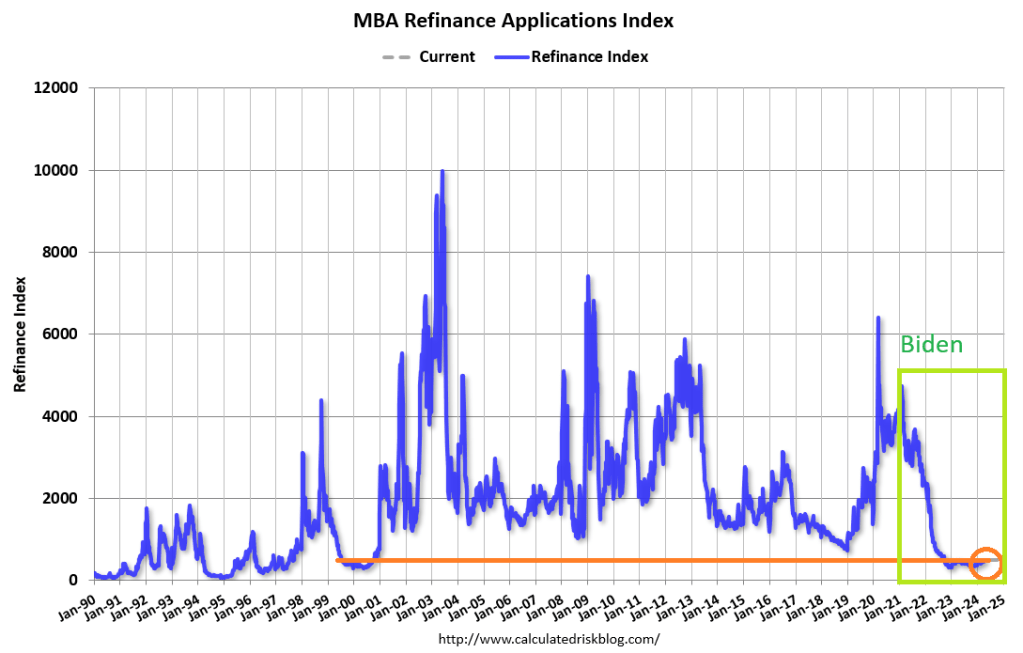

The Refinance Index increased 0.5 percent from the previous week and was 11 percent higher than the same week one year ago.

Bidenomics, a massive subsidy to the political donor class, but heartless towards the middle class.

Joe Biden, his Administration, and The Federal Reserve are really “The Alligator People.” Despite what they tell you, they have small brains (particularly Biden) and are hyperfocused on spending.

A good example comes from “Wall Street On Parade” where they show that The Federal Reserve is still paying BILLIONS to US Treasury in the form of remittances (losses). While at the same time, paying the mega banks on Wall Street high interest loans.

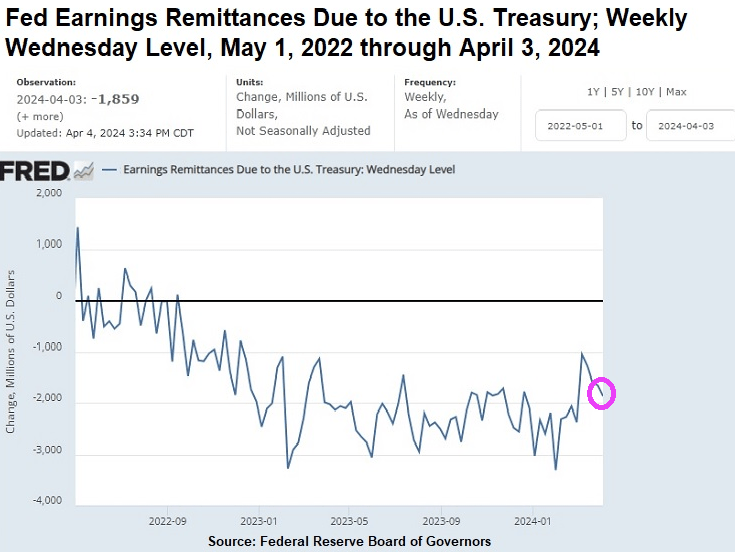

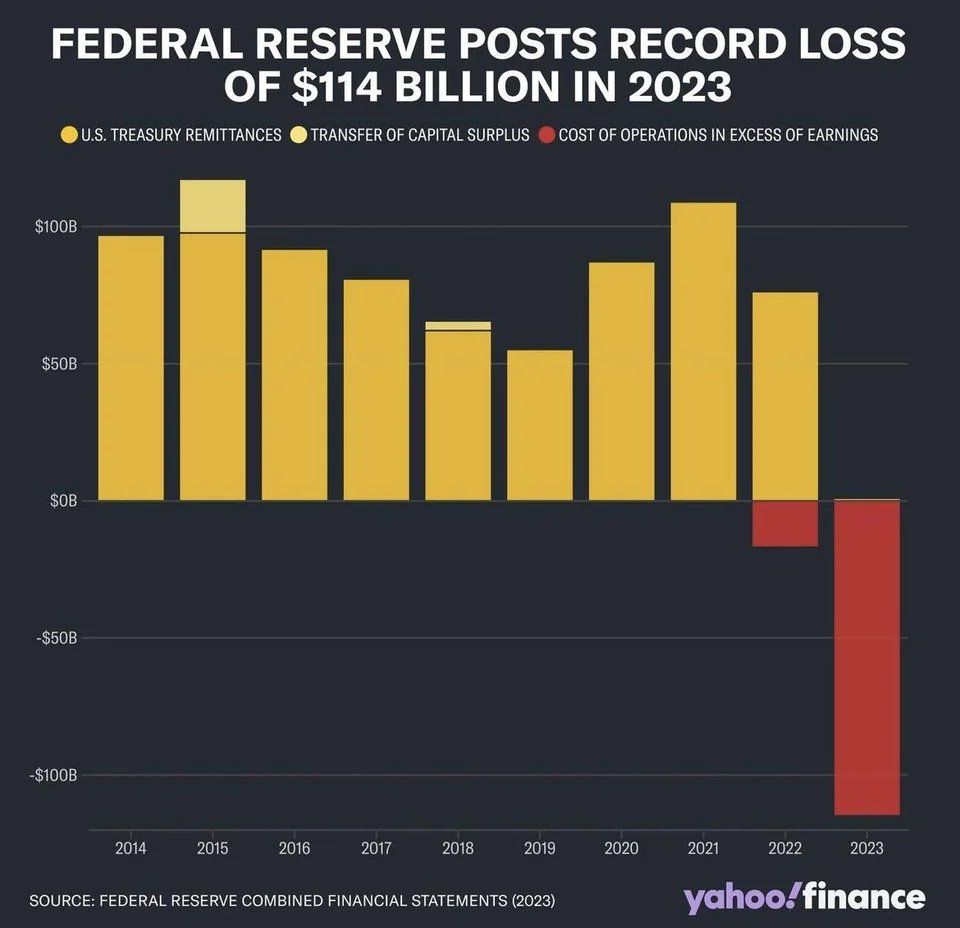

As of April 3 of this year, the Federal Reserve (Fed) has racked up $161 billion in accumulated losses. We’re not talking about unrealized losses on the underwater debt securities the Fed holds on its balance sheet, which it does not mark to market. We’re talking about real cash losses it is experiencing from earning approximately 2 percent interest on the $6.97 trillion of debt securities it holds on its balance sheet from its Quantitative Easing (QE) operations while it continues to pay out 5.4 percent interest to the mega banks on Wall Street (and other Fed member banks) for the reserves they hold with the Fed; 5.3 percent interest it pays on reverse repo operations with the Fed; and a whopping 6 percent dividend to member shareholder banks with assets of $10 billion or less and the lesser of 6 percent or the yield on the 10-year Treasury note at the most recent auction prior to the dividend payment to banks with assets larger than $10 billion. (This morning the 10-year Treasury is yielding 4.41 percent.)

Operating losses of this magnitude are unprecedented at the of Fed, which was created in 1913. In a press release dated March 26, the Fed stated this: “The Reserve Banks’ 2023 sum total of expenses exceeded earnings by $114.3 billion.”

As the chart above indicates, the Fed’s ongoing weekly losses have ranged from a high of $3.3 billion for the week ending Wednesday, January 31, 2024, to $1.86 billion for the most recent week ending Wednesday, April 3, 2024.

American taxpayers have good reason to sit up and pay attention to the Fed’s giant and ongoing losses. That’s because when the Fed is operating in the green, as it was on an annual basis for 106 years from 1916 through 2022, the Fed, by law, turns over excess earnings to the U.S. Treasury – thus reducing the amount the U.S. government has to borrow by issuing Treasury debt securities. According to Fed data, between 2011 and 2021, the Fed’s excess earnings paid to the U.S. Treasury totaled more than $920 billion.

WHO pays for the student loan forgiveness? It just doesn’t vanish, it is transferred to taxpayers. Alligators like Alexandria Ocasio Cortez going on talk shows to argue the benefits of being free from financial obligations that student voluntarily agreed to. Say, can AOC get my mortgage forgiven?? Just kidding. Now those same students can borrow additional money to get MBA degrees with the expectation that the student loan is “free money.”

Yes, Biden is acting recklessly (no surprise). Here is a picture of King Gator, Joe Biden.

The Biden Administration and The Federal Reserve ARE the alligator people. Except these gators are hungry for your money and votes constantly.

We are living in the USA where corruption, favoritism, open borders and an out-of-control Federal budget and debt are destroying this once great nation.

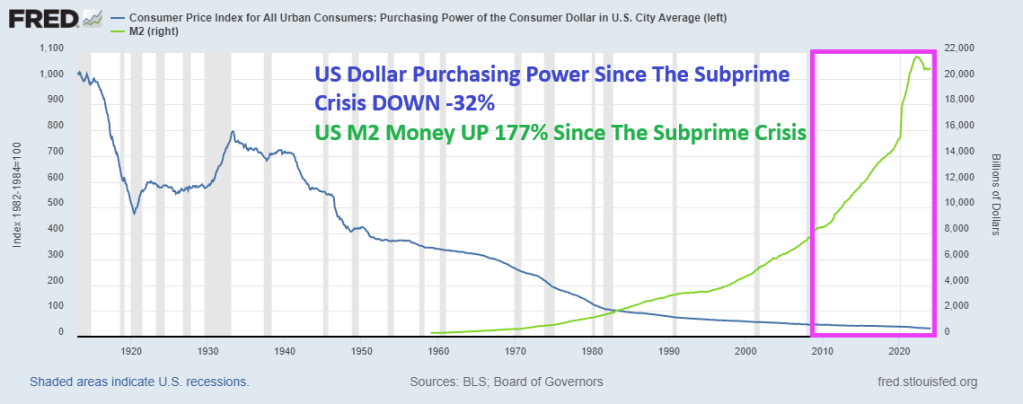

Former Kansas City Fed President Thomas M. Hoenig was absolutely right when he said recently that The Federal Reserve panders to Wall Street, Congress and special interest groups, prioritizing immediate relief over financial stability. Bernanke’s zero-interest rate policies (ZIRP) and Quantitative Easing (QE) were short-term fixes that never went away. Indeed, since the subprime mortgage crisis of 2008-2009, US Dollar purchasing power is DOWN -32% and M2 Money is up a staggering 177%. While Yellen stuck with zero-interest policies until Trump was elected, then raised The Fed Funds Target Rate 8 times. Yellen only raised the target rate once under Obama. Clearly playing political favoritism.

The Federal Reserve’s lack of transparency comes amidst reports that countries are removing their gold and other assets from the U.S. in the wake of the unprecedented Western sanctions imposed on Russia over its invasion of Ukraine. According to a 2023 Invesco survey, a “substantial percentage” of central banks expressed concern about how the U.S. and its allies froze nearly half of Russia’s $650 billion gold and forex reserves.Headline USA filed a FOIA request with the Fed for records reflecting how much gold the Federal Reserve Bank of New York currently holds in its vault, as well as records reflecting the ownership stake that each of FRBNY’s central bank/government clients have in that gold. The FOIA request also sought records about the Fed’s gold holdings prior to Russia’s February 2022 invasion of Ukraine. However, the Federal Reserve denied the FOIA request on Wednesday.

It influences the price of nearly everything, as well as the availability of jobs, the stability of our banking system, and the purchasing power of our money.

When the Fed Chair speaks, the entire world stops to listen.

But the average person has a poor understanding of how this colossally important entity operates. Or even why it exists.

And after a series of asset price bubbles — which some argue we’re in another one now — a chorus skeptical of the Fed’s actions has emerged.

So today we’re doing our best to shine as bright a light as possible on the Fed: how & why it operates, the good & as well as the shortcomings of its actions to date, what direction its policies are likely to take from here, and how all of this impacts the households of regular people like you and me.

Here are my top takeaways from from a speech by former KC Fed President Thomas Hoenig:

Dr Hoenig admits the Federal Reserve has experienced substantial “mission creep” since its creation as a lender of last resort. Its track record is very much “mixed” in terms of delivering on the intent of its policies. In Dr. Hoenig’s opinion, its efforts to add stability sometimes instead only create more instability.

While very critical of the Fed’s QE and ZIRP policies in the wake of the GFC, and more recently in the $trillions in monetary & fiscal stimulus unleashed post-COVID, Dr Hoenig thinks current Fed policy is “about right”. Though he expects the Fed to come under serious pressure soon as ebbing liquidity allows recessionary forces to build. He thinks the Fed will need to make an important decision within the coming year: return to QE and re-flame inflation, or allow a recession to occur.

Dr Hoenig criticizes the Federal Reserve for pandering to various interests, noting that short-term thinking and pressures from Wall Street, Congress, and interest groups often lead to decisions that prioritize immediate relief over long-term stability — a sort of “We’ll act now for optics sake and hopefully figure things out later”

In Dr Hoenig’s opinion, our fiscal policy is a runaway disaster. He criticizes both political parties of Congress for their roles in the cycle of ever-increasing deficits. Democrats advocate increased spending and tax hikes, while Republicans aim to keep taxes low but fail to curb spending. He warns of dire long-term consequences for future generations due to this impasse.

Dr Hoenig is very worried about the current stability of the banking system (and this from a former Direct of the FDIC!). He advocates for essential reforms to address government spending, prioritize essential areas without relying on future borrowed funds or inflationary measures, and communicate transparently with the public. He stresses the importance of reducing debt growth substantially below national income growth to avoid a full-blown crisis scenario in the future.

Dr Hoenig predicts the purchasing power of the US dollar (and other world fiat currencies) will continue to decline due to current policies and the lack of a “discipline” to money creation. Until such a discipline is restored (perhaps a return to some sort of hard backing of the currency), the dollar’s fall in purchasing power won’t abate.

Dr Hoenig suggests investing time in reading history and biographies as a valuable way to learn about leadership and gain insights into what strategies works and which don’t.

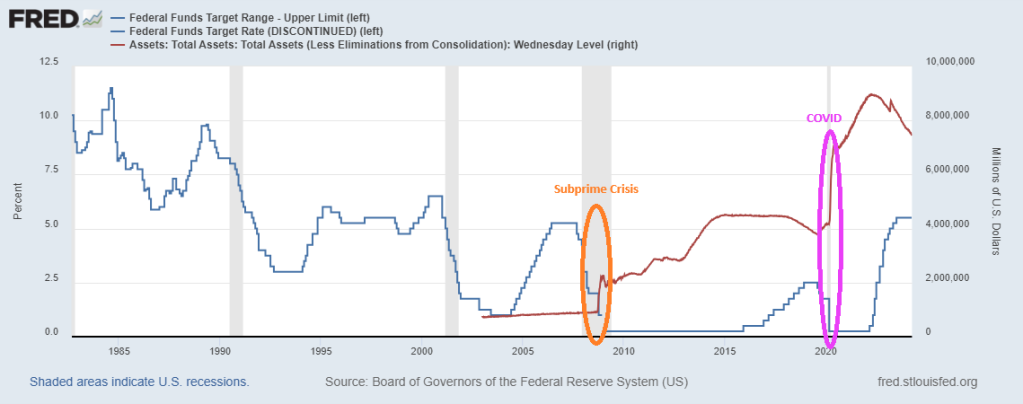

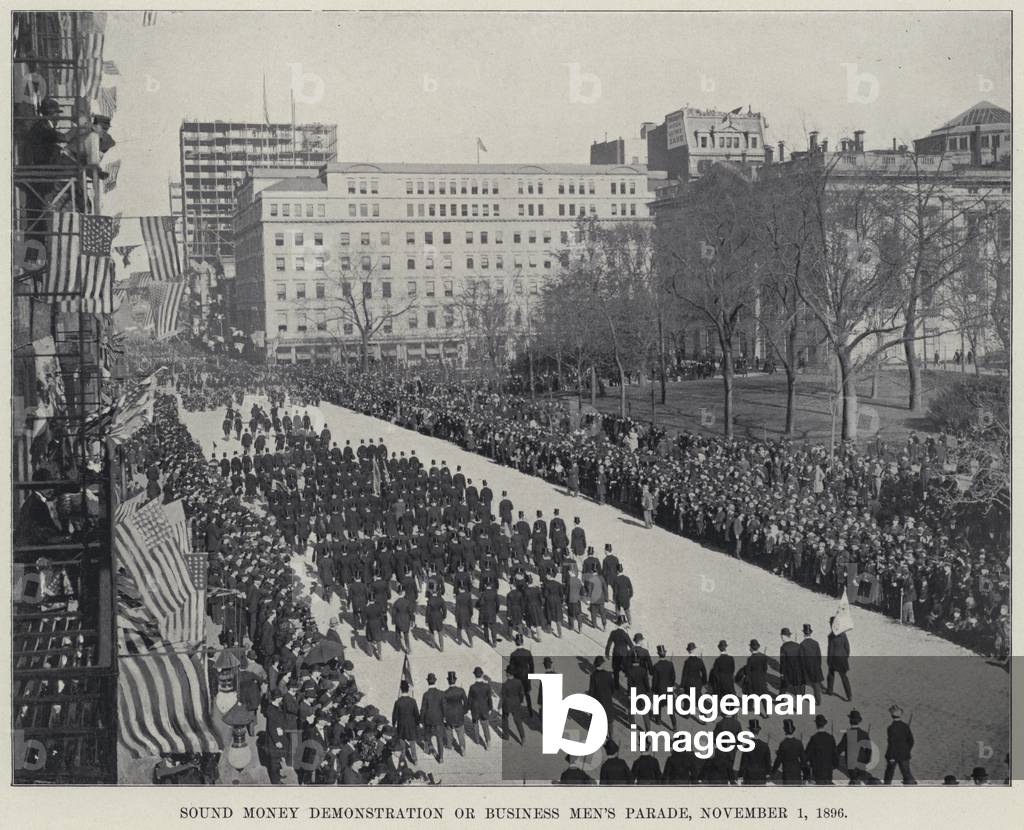

Here is the “Sound Money Parade” in 1896. By the aftermath of the subprime crisis, Janet Yellen (1993-2020) adopted the UNSOUND Money Fest, an orgy of printing and charging near zero interest rates. Powell in 2021 is ever-so-slowly unwinding The Fed’s balance sheet, but Powell has raised The Target Rate to its highest level since 1998 to fight inflation caused by Biden’s policies.

Combine The Fed not telling us how much gold they hold and their overprinting problems since 2008, and you can see why investors are turning to gold and silver and crypto currencies. The adoption of Central Bank Digital Currency (CBDC) is a step towards financial collapse.

Here is a parade you will NEVER see in Washington DC. A Sound Money Parade!

Powell is beginning to act like a sound money fan, but he still is taking his sweet time shriking the balance sheet.

I am thinking of fleeing to Lilliehammer Normay like Frank Tagliano.

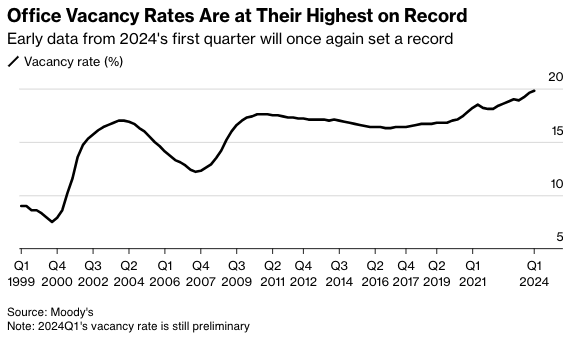

The rising supply of office space is due to a combination of surging remote and hybrid work that forces companies to reduce corporate footprints. Also, companies are exiting imploding progressive cities and high-taxed blue states for red ones while downsizing space. In the report, office tower vacancies rose to a record 19.8%, up from 19.6% in the fourth quarter of 2023.

Even with the increase, there is an eerily calm across the commercial real estate sector. This comes as the Federal Reserve’s interest rate hiking cycle is higher for longer, indicating that the pain train is nearing (perhaps after the presidential election).

“The office stress isn’t quite done yet,” Thomas LaSalvia, Moody’s head of commercial real estate economics and one of the authors of the report, told Bloomberg in an interview. He noted recent positive economic indicators stave off a “perfect storm in the office sector.”

“There are spots of light and there are spots of extreme darkness,” LaSalvia said, adding, “This is part of a longer-term evolution where we are seeing obsolete buildings in obsolete neighborhoods.”

The high office vacancy rate continues to be terrible news for landlords and developers eager to fill their buildings, and the Fed’s hiking cycle has made refinancing very challenging.

Viswanathan said there have been no major fireworks in CRE tower debt because the debt is being “extended and modified rather than refinanced,” which “mitigates a default wave and a sharp pick-up in losses on CRE loan portfolios.”

Yes, both residential and commercial real estate are thunderstruck under Bidenomics.

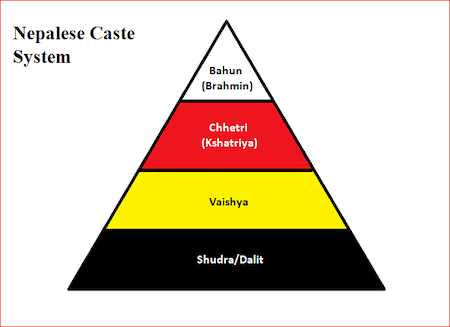

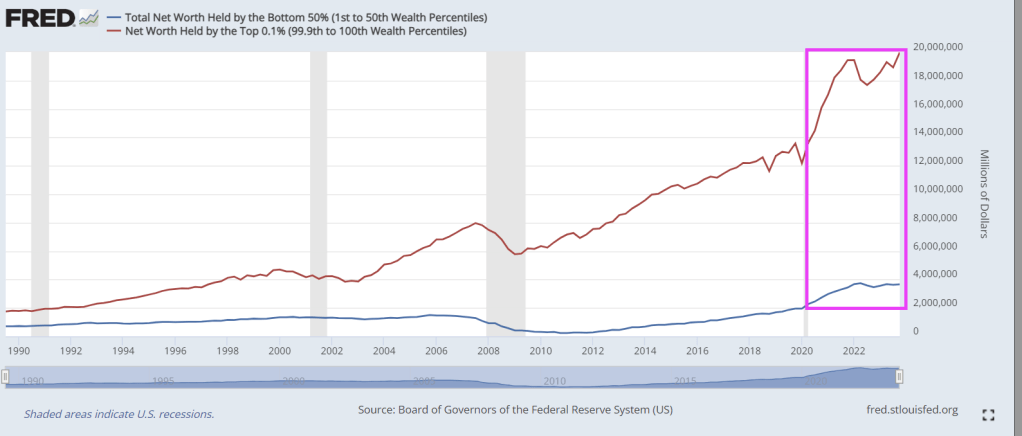

The Federal Reserve has created America’s version of India’s caste system. At the top of the neo American caste system are bankers and the political donor class. The top 1%. The other 99% are losing ground to the Brahmin Banker Class.

In 1913, Woodrow Wilson and his progressives promised that the Federal Reserve would avert both depressions and inflation, while preventing the wealthy from controlling America’s financial markets at the expense of the poor, the new untouchable class.

As you can see, the Brahmin Banker class (top .1% of net worth) are beating the socks off the bottom 50% of the new American caste system. This problems has greatly accelerated under Biden’s Reign of Error.

For two decades, the Fed kept interest rates artificially low to help finance massive government spending. When that spending reached unprecedented heights in 2020, the Fed intervened more drastically than ever, creating trillions of dollars and devaluing the currency.

Thus began an unparalleled transfer of wealth that continues to this day, and which has driven a wedge between different groups of Americans.

The painful inflation of the last three years has increased prices throughout the economy, distorting the signals that prices are supposed to convey to buyers and sellers. For example, the cost to own a median-price home today has doubled since January 2021, but it’s still the same house.

This phenomenon represents the monetization of housing, where a dwelling becomes a much better store of value than the currency, even if the real value of the house hasn’t improved.

Likewise, Americans’ earnings have increased substantially over the last three years, but not in the most meaningful sense—that is, what they can buy. Instead, the opposite has happened, and today’s larger incomes buy less.

What would have been a decent salary in 2019 is no longer enough to even get by in many places, and it’s certainly not enough to ever fulfill the American dream of homeownership.

A family earning the median household income can afford a median-price home in only a handful of major metropolitan areas in the entire country. In many cities, the cost to own a median price home exceeds the take-home pay from the median household income. Even if you didn’t spend a dime on other necessities such as food, you still wouldn’t have enough for your mortgage payment.

It’s truly a condemnation of the status quo when even those with seemingly high incomes cannot afford a typical house.

Worse, as prices continue marching upward, people can save less, making it harder to accrue a sufficient down payment. Even by the time a family reaches their goal, home prices have increased again, and they’re back on the hamster wheel, trying to save for an even larger down payment.

Meanwhile, inflation is steadily, though silently, taxing away the real value of the family’s savings as they sit in the bank.

This has left countless Americans as perpetual renters, with almost an entire generation of young people giving up on having the standard of living that their parents had. An artificial chasm has been constructed between those who already own capital, like housing, and the remaining Americans who can only borrow such assets, as they do by renting.

Similarly, many of those struggling to afford sharply increased rents are going deeply into debt to keep a roof over their head while those who locked in a mortgage with a fixed interest rate before both home prices and interest rates exploded have shielded themselves from one of the largest drivers behind the cost-of-living increases of the last three years.

Many homeowners could not afford to buy their same home today. The monthly mortgage payment on a median-price home has doubled since January 2021. Thus, even if two families have identical incomes, the one that bought a home three years ago has a nearly insurmountable advantage over the other family trying to do so today.

The Fed’s monetary manipulations have financed trillions of dollars in federal budget deficits, but they’ve also created a permanent American underclass, something antithetical to the Founders’ vision for the country.

Class mobility is at the heart of the American dream, and the Fed has turned it into a nightmare.

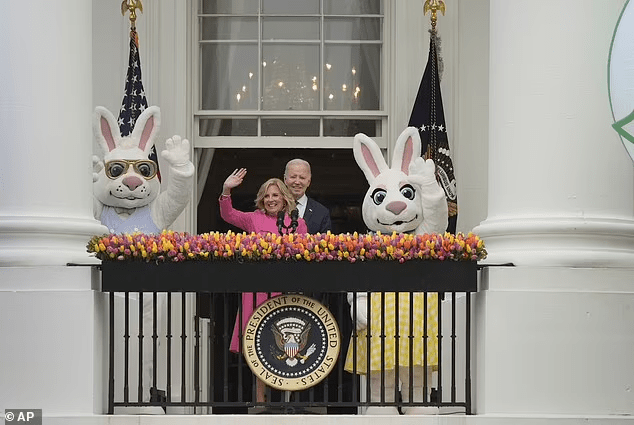

Here is a photo of Joe Biden with “Doctor” Jill on Easter Sunday flanked by Fed Chair Jerome Powell and Jared Bernstein (whom I once debated in Washington DC).

Update: KJP confessed that it was Obama who created the Trans Day of Awareness back in 2009 (although strangly not enacted until this part Easter Sunday).

As The Federal Reserve continues to support bad Bidenomics policies, they … like millions of Americans … are suffering catestrophic losses.

The #Fed said on Tuesday that it officially saw a net negative income of $114.3 billion in 2023, a record loss tied to expenses related to managing the U.S. central bank’s short-term interest rate target. The loss last year follows $58.8 billion in net income in 2022, the Fed said.

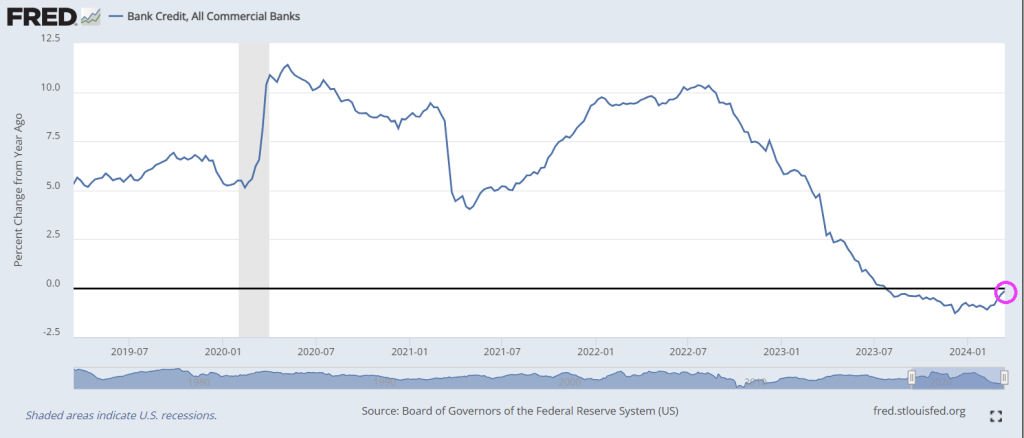

The good news? Bank credit growth is ALMOST back to 0%!

I wonder if KJP or Jared Bernstein will tout almost 0% credit growth as a sign that economists were wrong about Bidenomics?

Biden loves to blame Republicans for the border crisis. Although he has it in his power to close and secure the border, but won’t. It’s easier to blame the opposition, like “extreme MAGA Republicans.” Huh, I didn’t realize that as a conservative American I am considered extreme by the Biden Administration.

Unfortunately, Biden, Schumer and Johnson only provided financial support for Jordan, Lebanon, Egypt, Tunisia and Oman. In the form of $380 million.

As the US falls to 23rd in World Happiness ranking. Based, in part, on Biden’s idiotic open borders policy.

1. Everybuddy: 100% of workforce 2. Wisense: 100% of workforce 3. CodeSee: 100% of workforce 4. Twig: 100% of workforce 5. Twitch: 35% of workforce 6. Roomba: 31% of workforce 7. Bumble: 30% of workforce 8. Farfetch: 25% of workforce 9. Away: 25% of workforce 10. Hasbro: 20% of workforce 11. LA Times: 20% of workforce 12. Wint Wealth: 20% of workforce 13. Finder: 17% of workforce 14. Spotify: 17% of workforce 15. Buzzfeed: 16% of workforce 16. Levi’s: 15% of workforce 17. Xerox: 15% of workforce 18. Qualtrics: 14% of workforce 19. Wayfair: 13% of workforce 20. Duolingo: 10% of workforce 21. Rivian: 10% of workforce 22. Washington Post: 10% of workforce 23. Snap: 10% of workforce 24. eBay: 9% of workforce 25. Sony Interactive: 8% of workforce 26. Expedia: 8% of workforce 27. Business Insider: 8% of workforce 28. Instacart: 7% of workforce 29. Paypal: 7% of workforce 30. Okta: 7% of workforce 31. Charles Schwab: 6% of workforce 32. Docusign: 6% of workforce 33. Riskified: 6% of workforce 34. EA: 5% of workforce 35. Motional: 5% of workforce 36. Mozilla: 5% of workforce 37. Vacasa: 5% of workforce 38. CISCO: 5% of workforce 39. UPS: 2% of workforce 40. Nike: 2% of workforce 41. Blackrock: 3% of workforce 42. Paramount: 3% of workforce 43. Citigroup: 20,000 employees 44. ThyssenKrupp: 5,000 employees 45. Best Buy: 3,500 employees 46. Barry Callebaut: 2,500 employees 47. Outback Steakhouse: 1,000 48. Northrop Grumman: 1,000 employees 49. Pixar: 1,300 employees 50. Perrigo: 500 employees

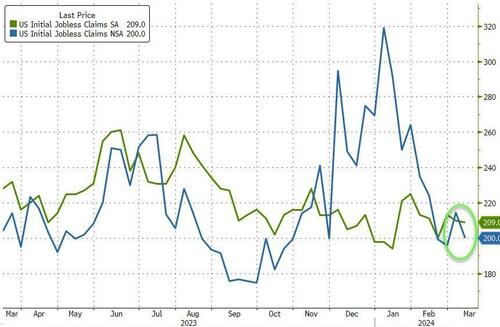

But, according to the government-supplied data…

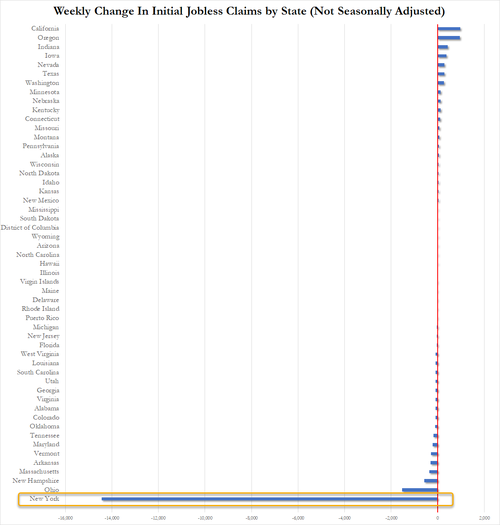

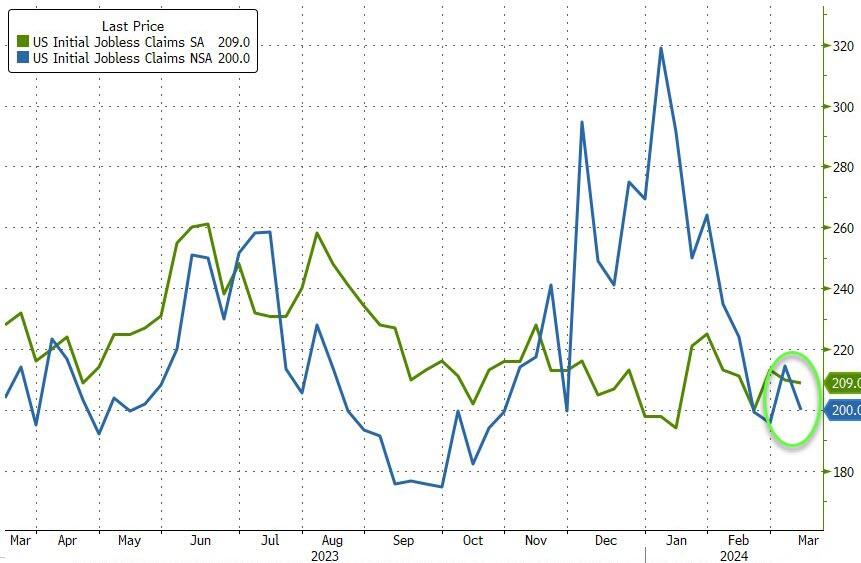

The number of American filing for jobless benefits for the first time last week dropped to 209k (vs 218k exp) with the NSA number tumbling to 200k…

Source: Bloomberg

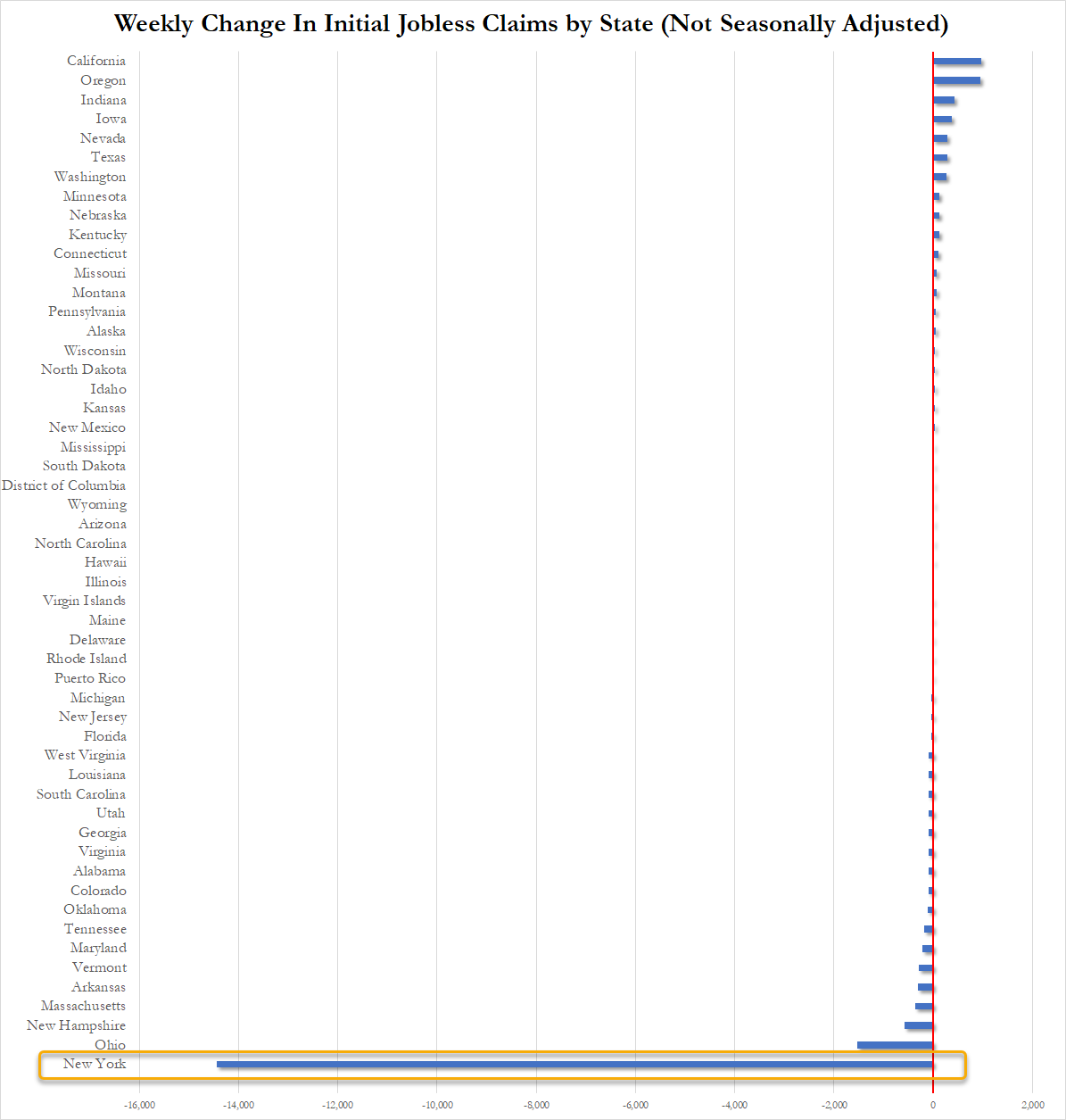

How is this possible, you may ask… well let us show you the ways… New York State claims that its jobless benefits rolls collapsed last week. New York accounted for 99.75% of the weekly change in initial claims across the entire US as shown below…

Source: Bloomberg

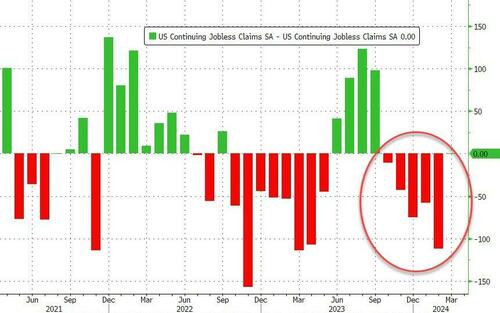

Continuing Claims was a shit show – with a massive 112k person downward revision for last week from 1.906 million to 1.794mm. That is the 5th straight weekly downward revision of continuing claims…

Source: Bloomberg

But thanks to the adjustments, it all looks ‘normal’ and ‘stable’ at around 1.8 million Americans…

Source: Bloomberg

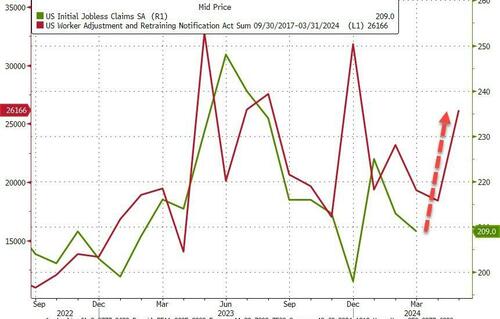

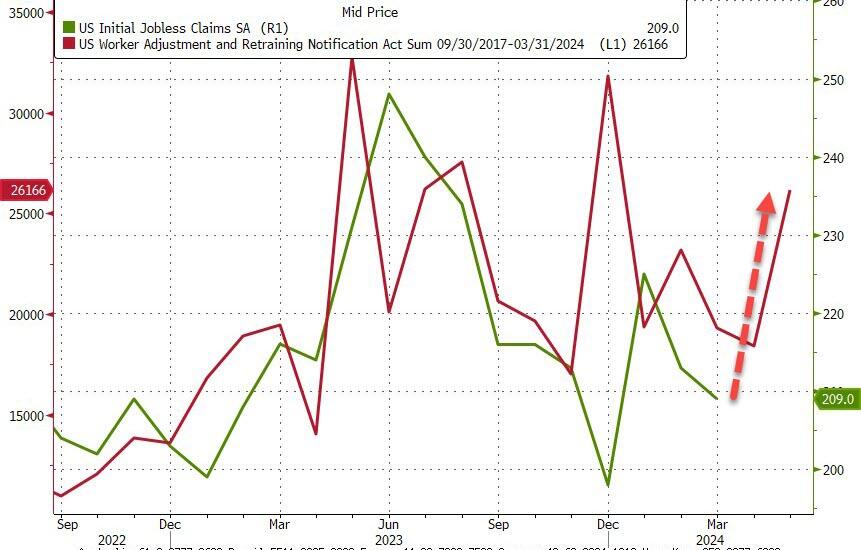

And WARN numbers are rising rapidly…

Source: Bloomberg

As a reminder, if you doubt the accuracy of the Biden admin’s data, here’s what the most recent FOMC Minutes said:

“While the recent trends prior to the meeting had been remarkably positive, Fed officials judged that some of the recent improvement “reflected idiosyncratic movements in a few series.”

Even they aren’t buying it, and neither should you!

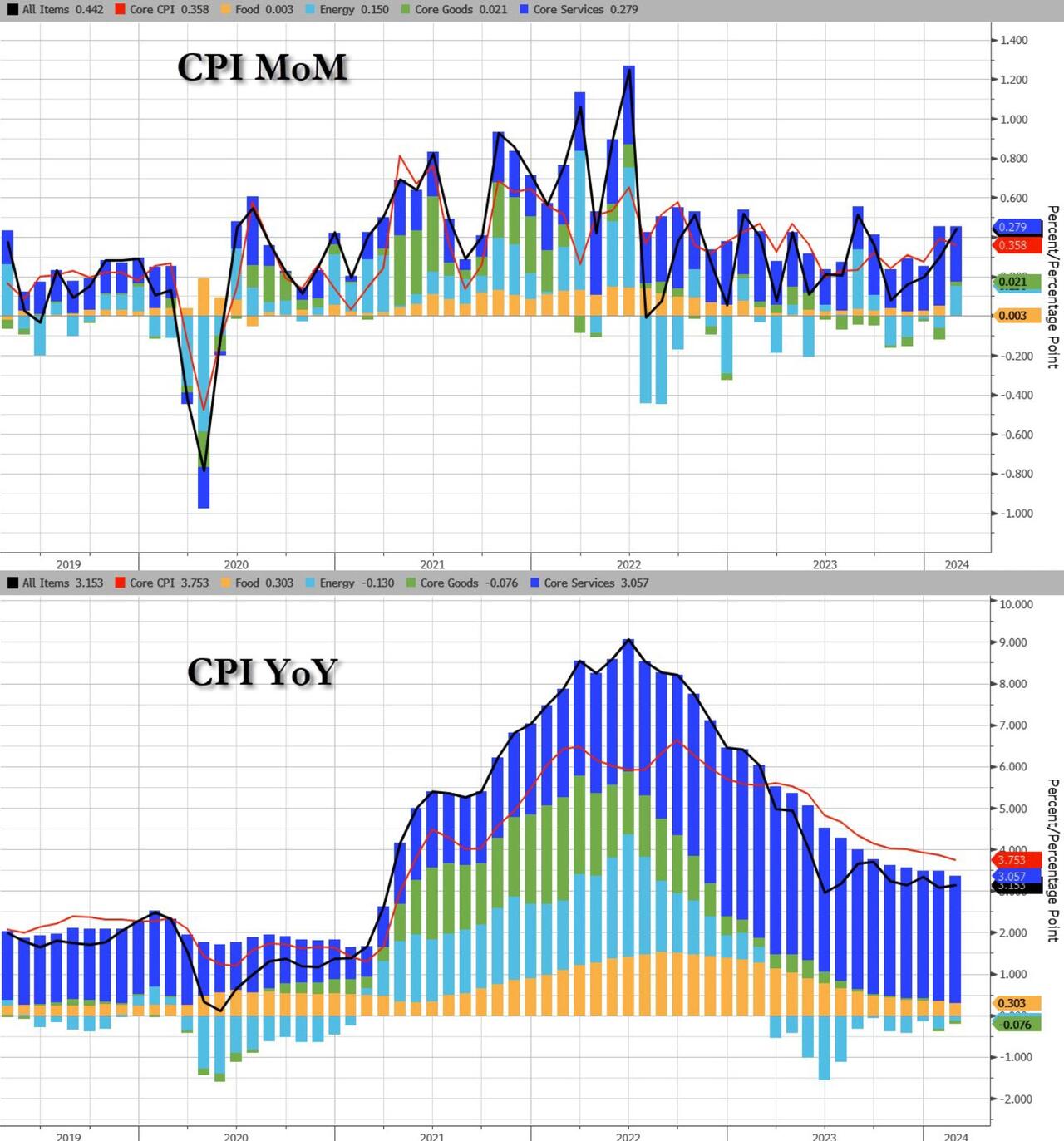

Unlike what Grand-dad Joey Biden screamed at the State of The Union (SOTU) address, inflation is NOT been defeated. In fact, inflation has defeated Biden and The Federal Reserve.

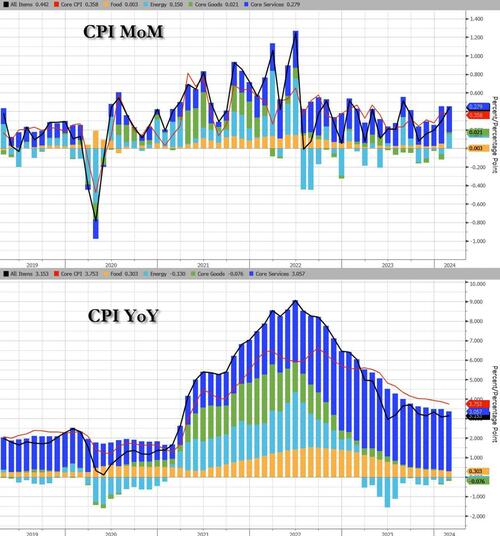

The 3-month annualized CPI rate was rose to 2.8% from 1.9%. The 6-month annualized core rate dropped to 3.2% from 3.3%.

Energy costs surged MoM as Core Services inflation slowed MoM…

Source: Bloomberg

Full CPI MoM breakdown:

The index for all items less food and energy rose 0.4 percent in February, as it did the previous month.

The shelter index increased 0.4 percent in February and was the largest factor in the monthly increase in the index for all items less food and energy.

The index for rent rose 0.5 percent over the month, while the index for owners’ equivalent rent increased 0.4 percent.

The lodging away from home index increased 0.1 percent in February, after rising 1.8 percent in January.

The airline fares index rose 3.6 percent in February, following a 1.4-percent increase in January.

The index for motor vehicle insurance increased 0.9 percent over the month.

The medical care index was unchanged in February after rising 0.5 percent in January.

The index for hospital services decreased 0.6 percent over the month and the index for physicians’ services decreased 0.2 percent.

The prescription drugs index fell 0.1 percent in February.

The index for dental services was among those that rose in February, increasing 0.4 percent.

The index for personal care fell 0.5 percent in February, following a 0.6-percent increase in January.

The household furnishings and operations index fell 0.1 percent over the month, as did the new vehicles index.

Among other indexes that rose in February were apparel, recreation, and used cars and trucks.

Full CPI YoY breakdown:

The index for all items less food and energy rose 3.8 percent over the past 12 months.

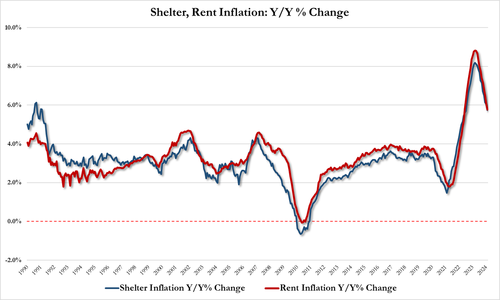

The shelter index increased 5.7 percent over the last year, accounting for roughly two thirds of the total 12-month increase in the core CPI index

Feb Shelter inflation: 5.74% down from 6.04% in Jan

Feb rent inflation: 5.77%, down from 6.09% in Jan

Other indexes with notable increases over the last year include motor vehicle insurance (+20.6 percent), medical care (+1.4 percent), recreation (+2.1 percent), and personal care (+4.2 percent).

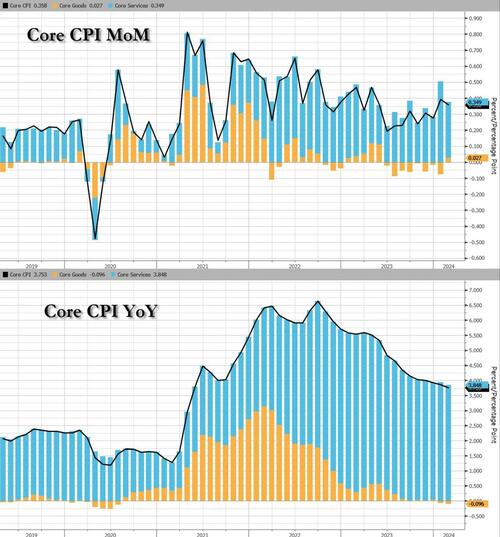

Core CPI rose 0.4% MoM (hotter than the +0.3% exp) and up 3.8% YoY (hotter than the +3.7% exp), but still the lowest since April 2021…

Source: Bloomberg

The 3-month annualized Core CPI rate was rose to 4.1% from 3.9%. The 6-month annualized core rate rose to 3.8% from 3.5%.

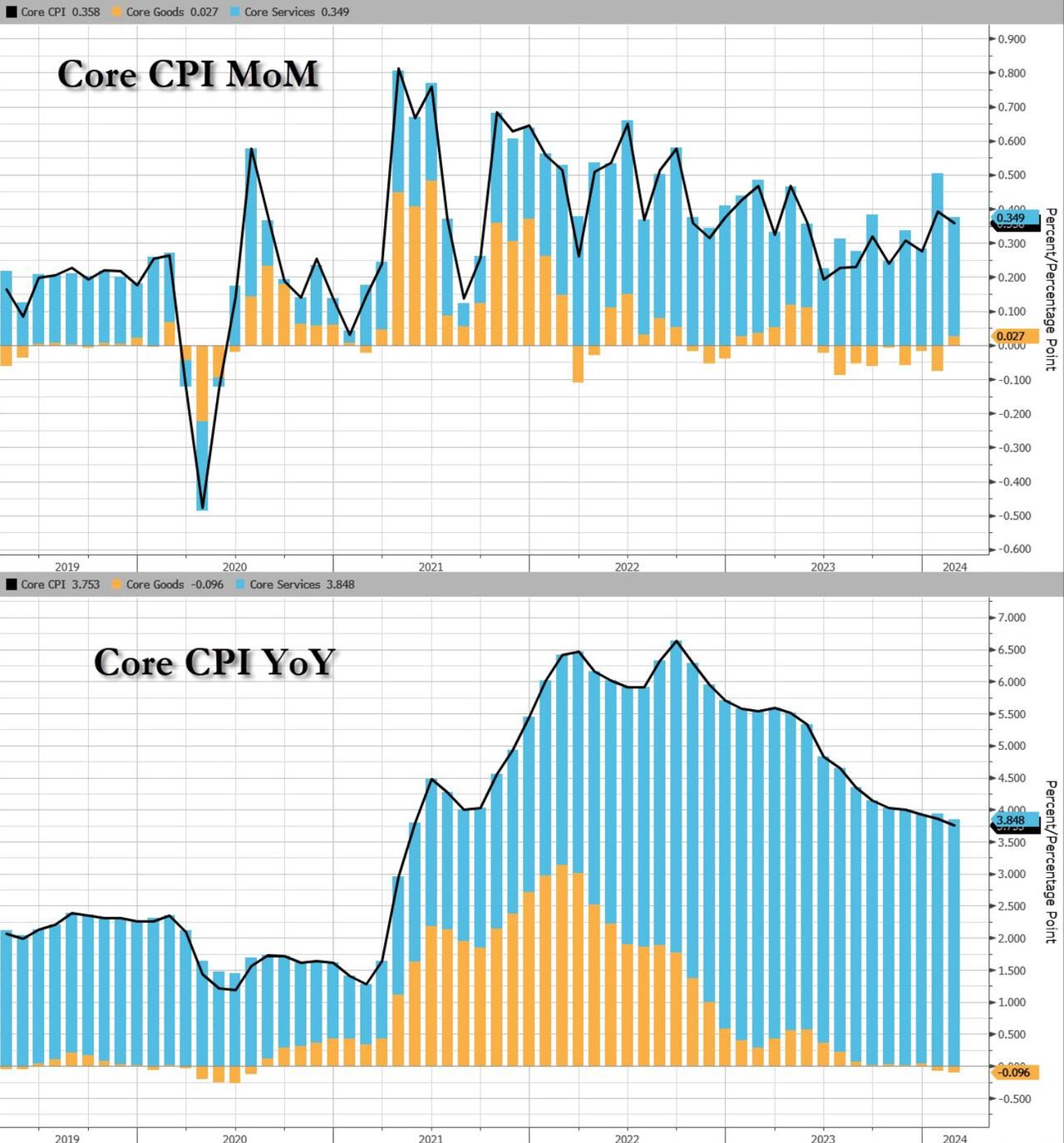

Core Goods actually rose MoM for the first time since June 2023…

Goods deflation continues (-0.3% YoY) but has flattened out, while services inflation remains stubbornly high at +5.2% YoY…

Source: Bloomberg

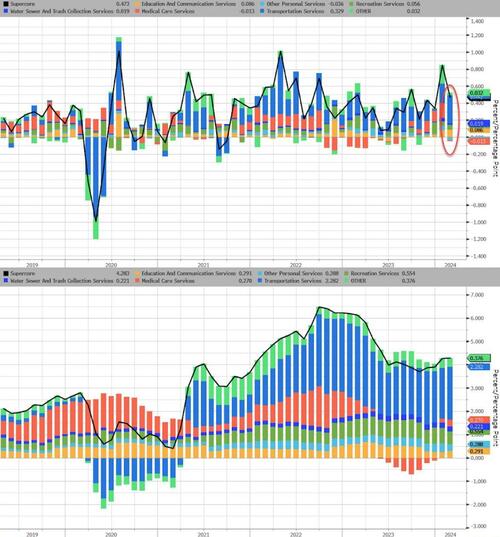

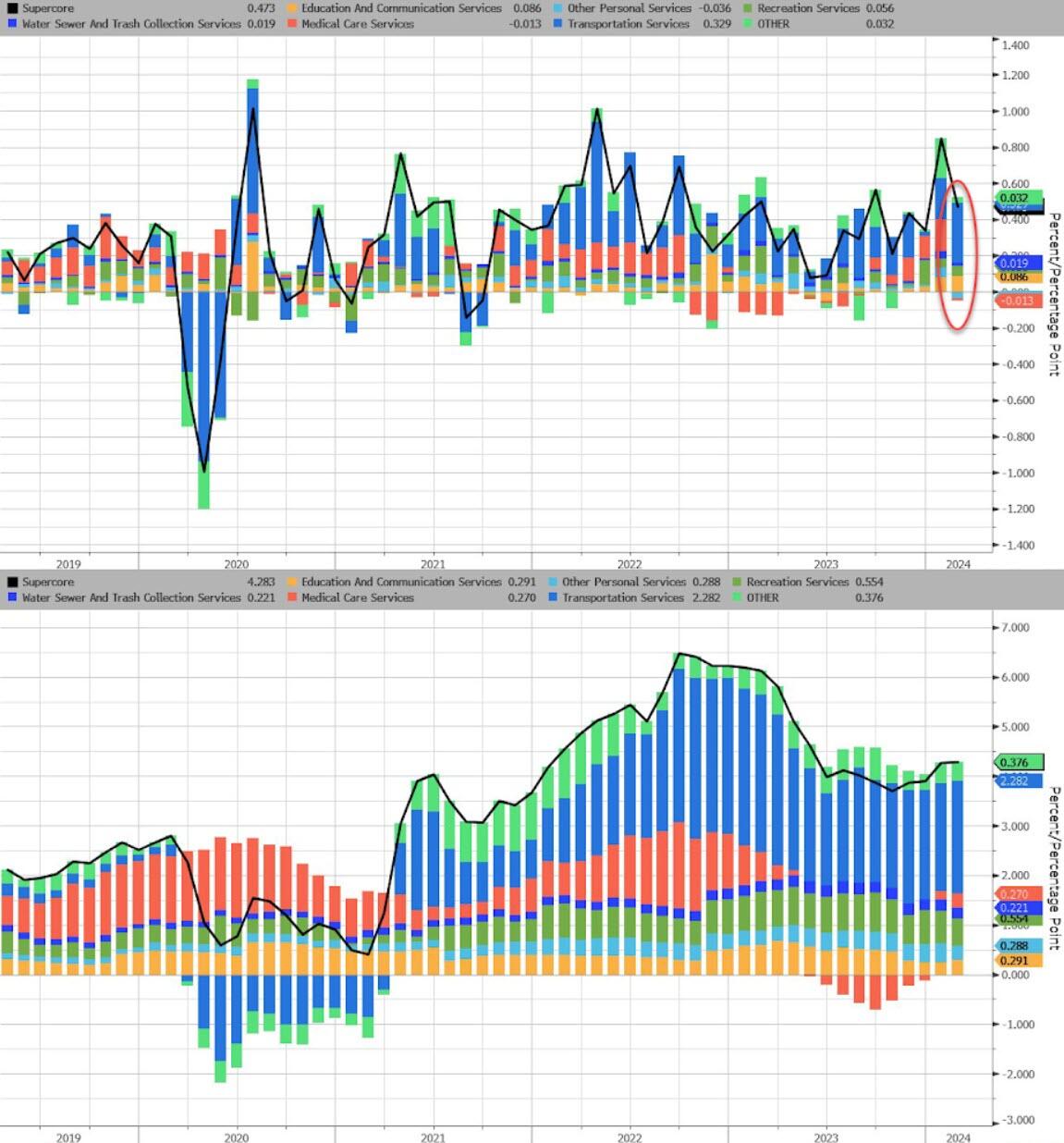

And one step deeper – the so-called SuperCore: Core CPI Services Ex-Shelter index – soared 0.5% MoM up to 4.5% YoY – the hottest since May 2023…

Source: Bloomberg

While SuperCore CPI slowed MoM, there was a large jump in Transportation Services MoM…

Source: Bloomberg

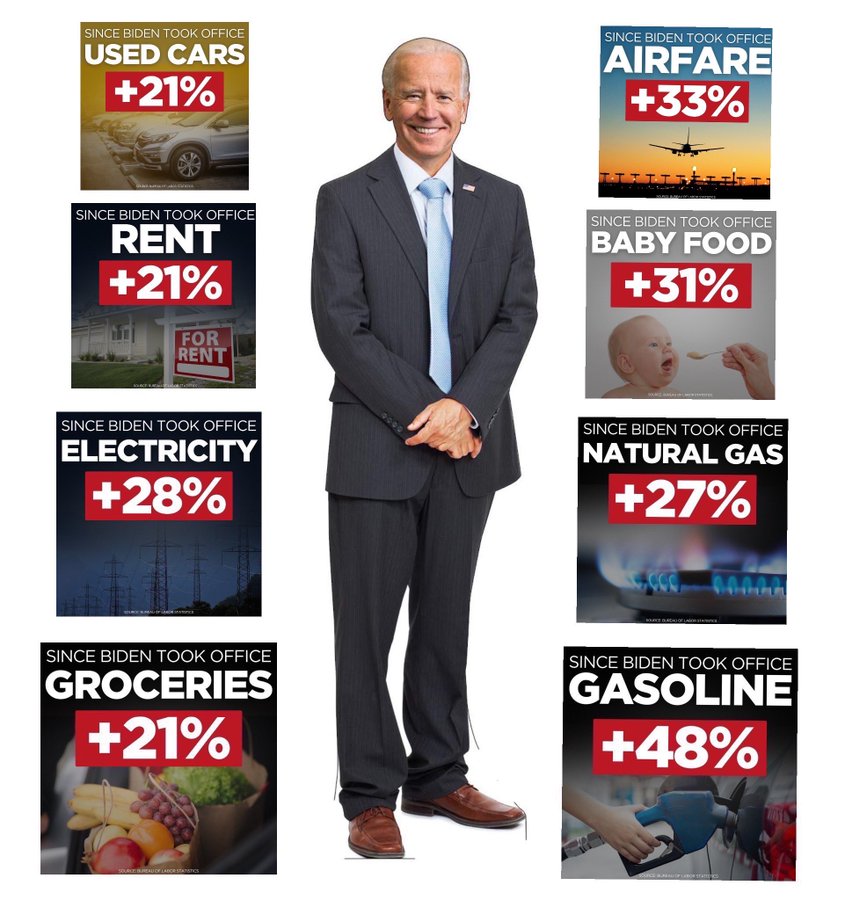

Finally, we note that consumer prices have not fallen in a single month since President Biden’s term began (July 2022 was the closest with ‘unchanged’), which leaves overall prices up 19% since Bidenomics was unleashed. And prices have never been more expensive…

Source: Bloomberg

That is an average of 5.6% per annum (more than triple the 1.9% average per annum rise in price during President Trump’s term).

So, about that shrinkflation – did companies only ‘get greedy’ when Biden took office?

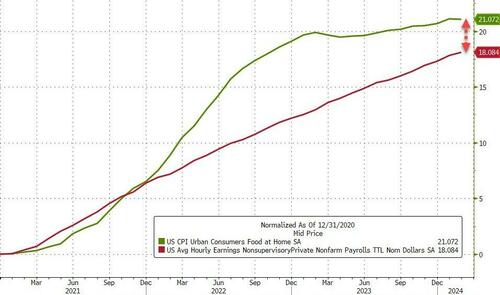

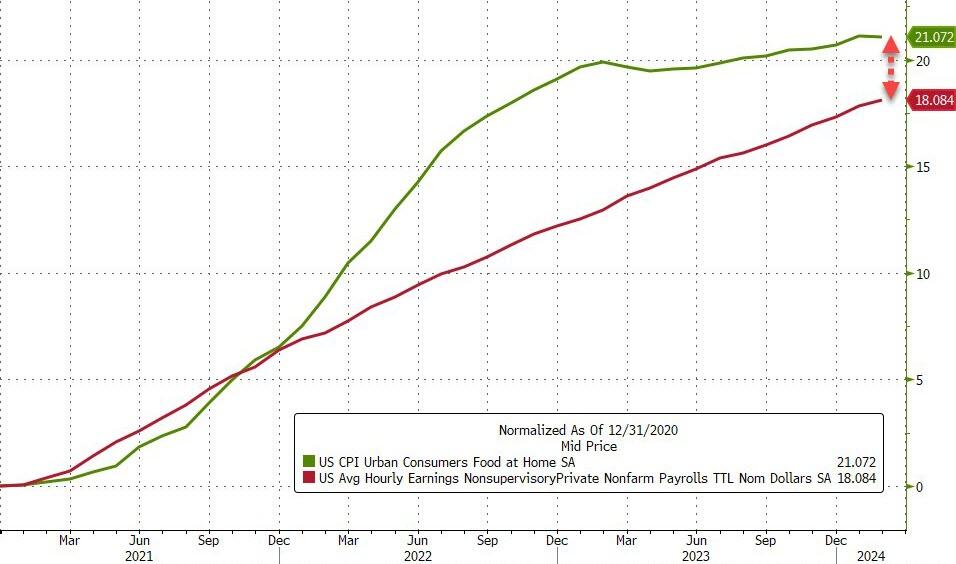

But it gets worse, real wage growth has lagged significantly for the average joe in America…

Source: Bloomberg

Despite a very modest decline in Feb, Food costs are up over 21% since Biden’s term began, but non-supervisory wages are up only 18%.

Bidenomics for the win!

Are we going to see a replay on the ’70s?

Source: Bloomberg

The market narrative of slow and steady disinflation just broke harder.

…or are we still set for a massive wave of depressionary deflation?

Inflation remains hot, hot, hot although Biden/Yellen will undoubtedly say that it is lower than last year. But remember, consumer prices are up a staggering 19% under Bidenomics. THAT is a major tax of those making under $200,000 per year, Joey.

Somehow, Biden left this factoid out of his State of The Union (SOTU) address. In February, immigrants added 1,277 million jobs while native Americans lost -420,000 jobs according to the BLS. Or maybe Biden can change his campaign motto to “Make America Great Again … For Immigrants, NOT Natives.”

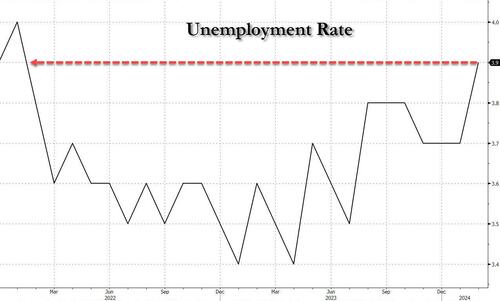

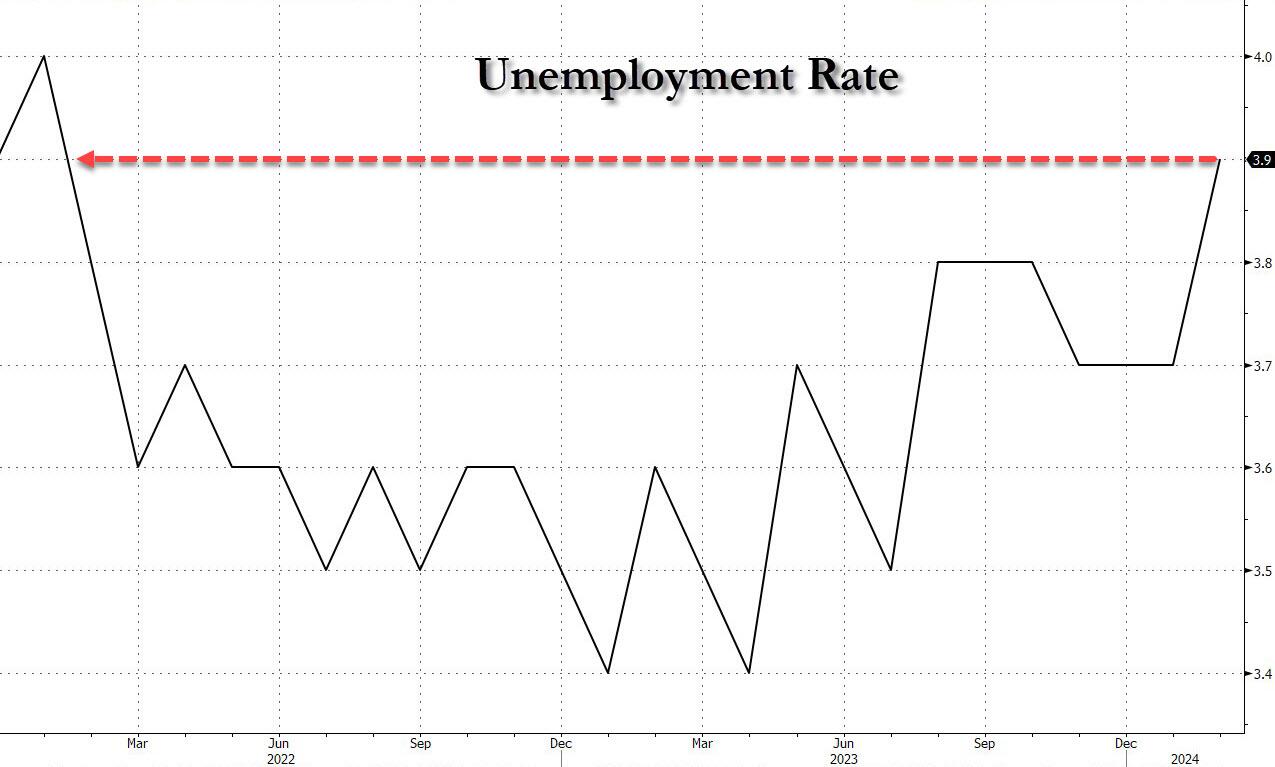

In February, the unemployment rate unexpectedly jumped to 3.9%, the highest since February 2022 (with Black unemployment spiking by 0.3% to 5.6%).

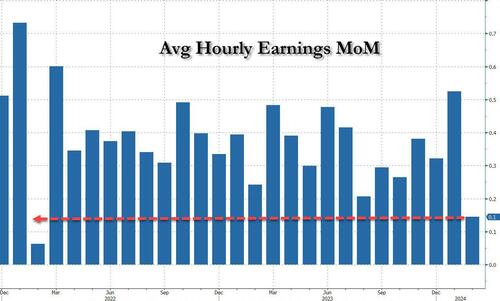

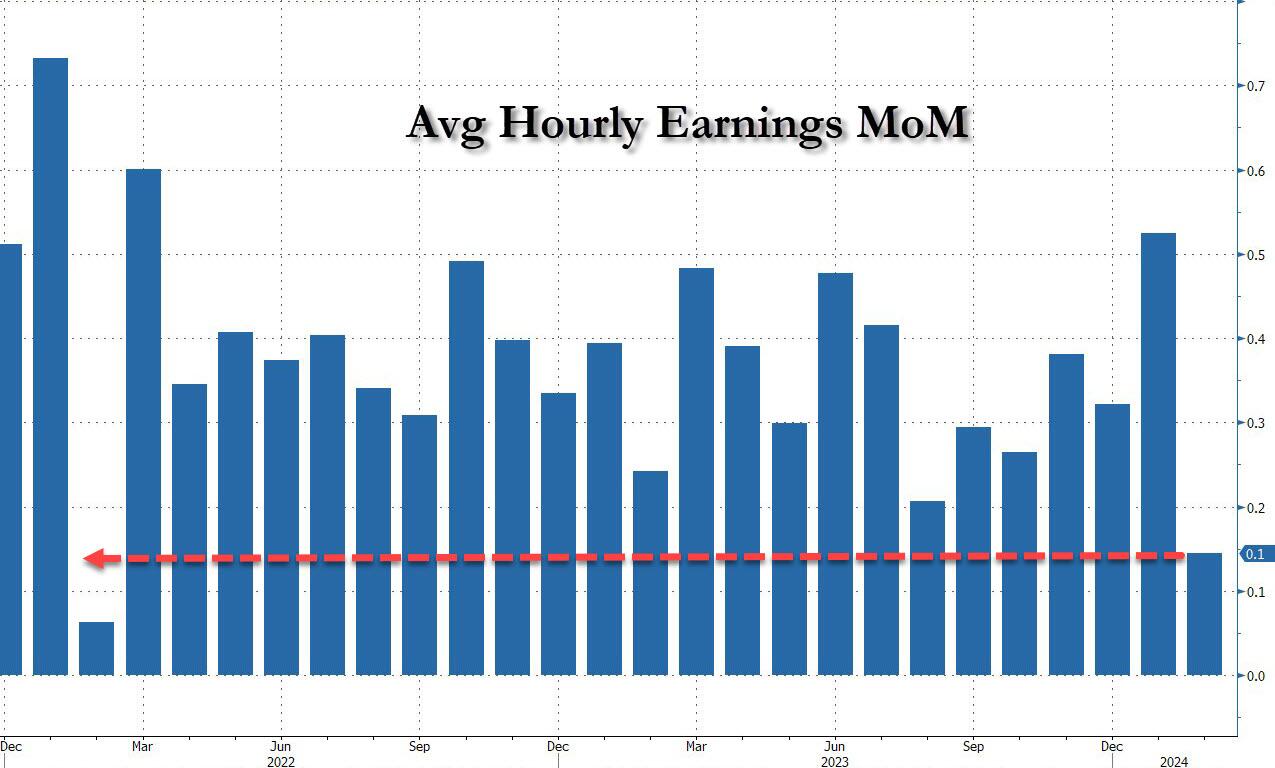

And then there were average hourly earnings, which after surging 0.6% MoM in January (since revised to 0.5%) and spooking markets that wage growth is so hot, the Fed will have no choice but to delay cuts, in February the number tumbled to just 0.1%, the lowest in two years…

It is clear that the labor market is softening, but Biden/Mayorkas will continue to let millions of illegal immigrants pour across the border making the labor market even softer than before. But the top 1% are making out like bandits from the illegal immigration. Bandits benefitting bandits.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.