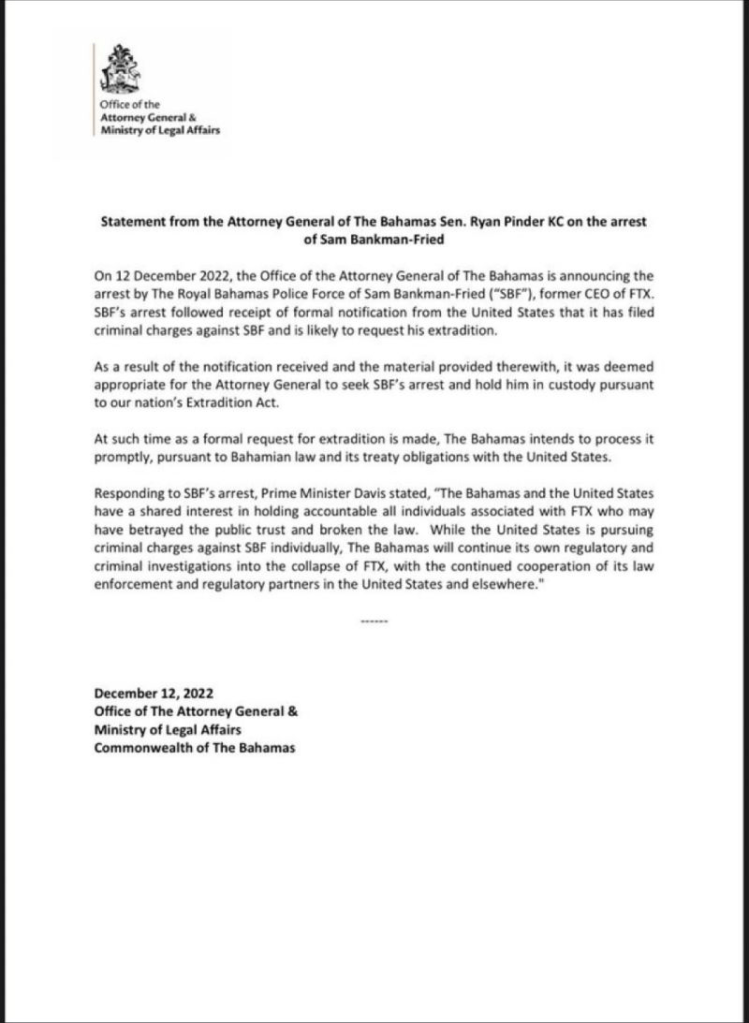

First, Sam Bankman-Fried agreed to testify in the House Financial Services Committee meeting on December 13, 2021. Then Bankman-Fried said he would testify remotely. Then ,,, he was arrested by the Bahama’s police. How convenient!

Does this mean that SBF will testify from behind closed doors?

According to Reuters, FTX’s Bankman-Fried says he will testify remotely at congressional hearing.

WASHINGTON, Dec 12 (Reuters) – Sam Bankman-Fried, the founder and former CEO of now-bankrupt crypto exchange FTX, on Monday said he would testify remotely at Tuesday’s U.S. House Financial Services Committee hearing to examine the collapse of the company.

FTX filed for U.S. bankruptcy protection last month and Bankman-Fried resigned as chief executive, triggering a wave of public demands for greater regulation of the cryptocurrency industry.

That might be kind of difficult, since Sam Bankman-Fried has been arrested in the Bahamas.

Perhaps, The SEC Gary Genslar will testify as to why he met with SBF and gave him the green light for his trading? And why did Genslar erase Hillary Clinton from his schedule after meeting with her? And why was Genslar meeting with Hillary in the first place since she is now just an American cititzen??

Will SBF be extricated by tomorrow morning hearing time?

You must be logged in to post a comment.