Dear Mr. Fantasy, play us a tune, something to make us all happy (like hitting 2% inflation WITHOUT crashing the economy).

Do anything take us out of this gloom (caused by The Fed, Biden’s energy policies and Federal spending).

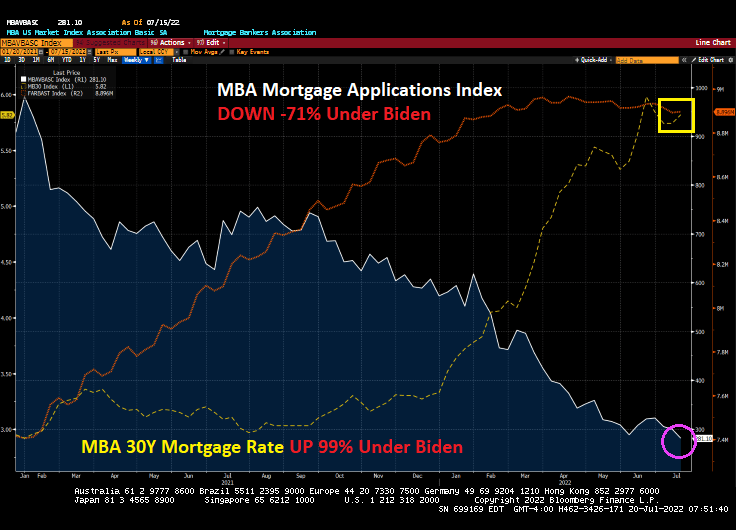

Sing a song, play guitar, Make it snappy. Or in the case of housing, make it crappy.

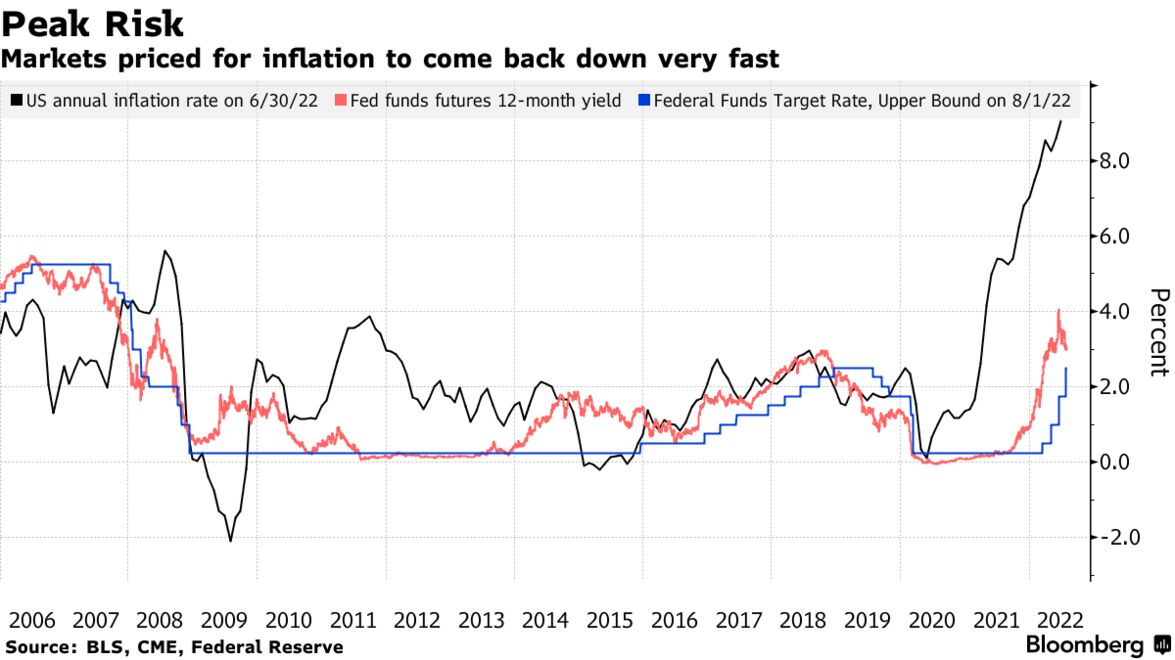

(Bloomberg) — Federal Reserve Bank of Richmond President Thomas Barkin said the central bank was resolved to curb red-hot inflation, even if that meant risking a US economic recession.

“We’re committed to returning inflation to our 2% target and we’ll do what it takes to get there,” Barkin said Friday during an event in Ocean City, Maryland. He said that this could be achieved without a “tremendous decline in activity” but acknowledged that there were risks.

“There’s a path to getting inflation under control but a recession could happen in the process,” he said.

The US central bank hiked interest rates by 75 basis points in July for the second straight month as policy makers tackle inflation that’s running near 40-year highs. Fed officials speaking in recent days have said more rate increases are needed, but they are still deciding how big to move at their next policy meeting.

St. Louis Fed President James Bullard, one of the most hawkish policy makers, on Thursday urged another 75 basis-point move while Kansas City’s Esther George struck a more cautious tone.

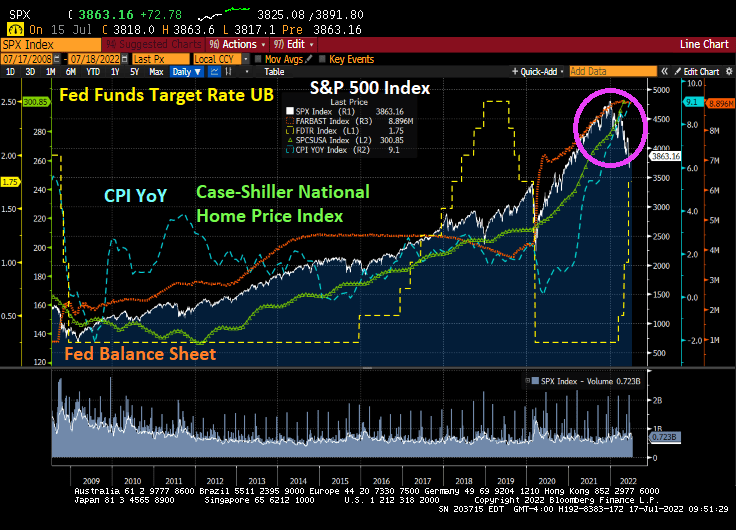

Well, The Fed (aka, Der Kommissars) let the monetary stimulus blow out of control since 2000.

With the 2001 recession, The Fed crashed the target rate (white line) causing home price growth (blue line) to soar. Then The Fed decided that the economy was overheated and cranked up their target rate. This sudden rise in The Fed’s target rate helped to slow/crash housing prices. Resulting in … a frantic decrease in the target rate (late 2007- late 2008) and the adoption of asset purchases of Treasury Notes/Bonds and Agency Mortgage-backed Securities in late 2008.

The Bernanke/Yellen “loose as a goose” policies from late 2008 to Feb 2018 created a total mess. Bernanke/Yellen raised the target rate only one before Trump was elected President, and 8 times AFTER Trump was elected. And Yellen’s Fed began to let the balance sheet shrink a bit before Covid struck in early 2020. And with Covid came another massive expansion of The Fed’s Balance Sheet WHICH HAS NOT YET BEEN WITHDRAWN (despite Fed talking heads saying it would be reduced).

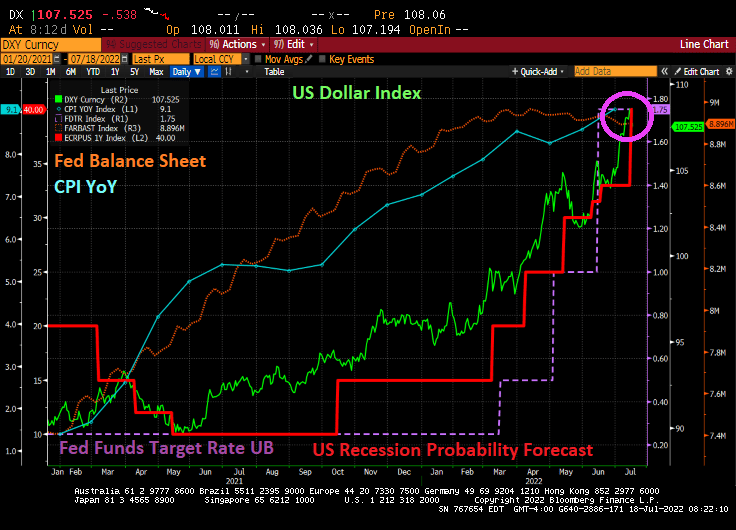

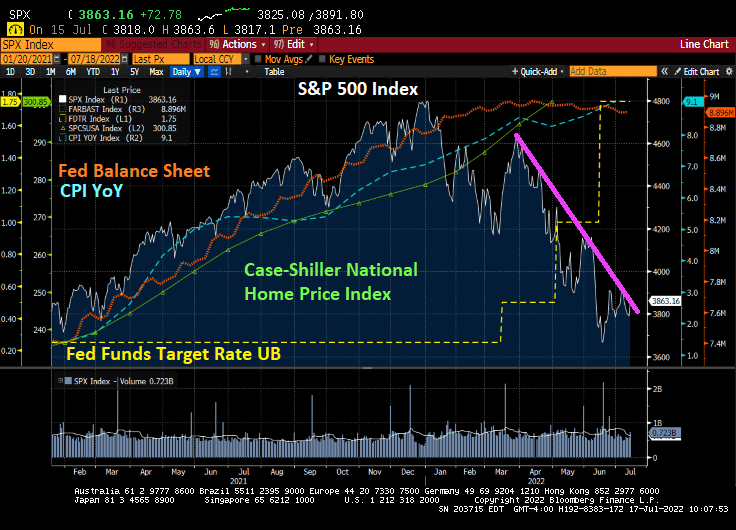

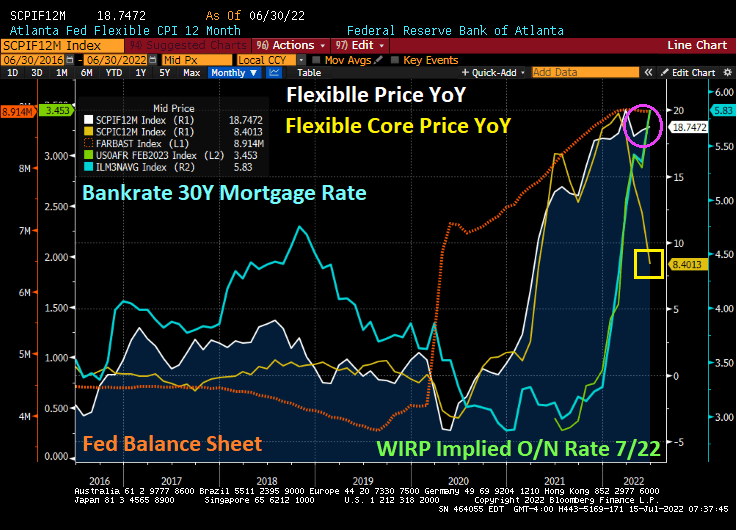

Here we sit with The Fed NOW trying to extinguish inflation (yellow line) by raising their target rate (white line) but NOT shrinking the balance sheet (orange line).

Wonder why this is a horrible homeless problem in the US, particularly in California? While Stanford University has an excellent study of the causes of California’s homeless problem, there is another cause of homelessness … The Federal Reserve’s insane monetary policies since late 2008. The Case-Shiller National Home Price Index is 65% higher in May than during the calamitous home price bubble of 2005-2007, helping to exacerbate the homeless problem.

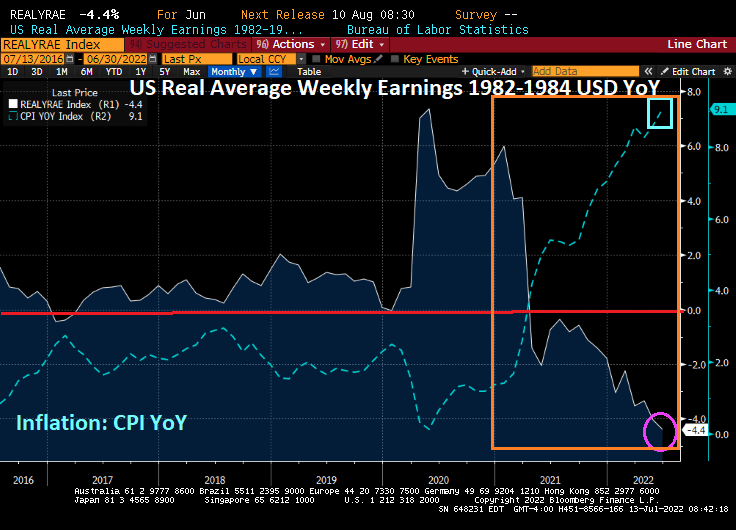

One of the many problems created by the reckless Bernanke/Yellen/Powell monetary policies is the M2 Money Velocity is near an all-time low making a return to “easy money policies” far more difficult.

I won’t post any photos of the homeless encampments in Los Angeles since it is very sad. But here is a photo of the Dunder-Mifflin paper company “office” on Saticoy Street. The point is that thanks to The Federal Reserve’s loose monetary policies, housing is unaffordable for millions of households forcing many to live on the streets.

Figure 2: Median Rent for a Two-Bedroom Apartment, California, 2022

And a point of trivia. The Office’s Charles Miner (played by the GREAT Idris Elba) was allegedly hired from Saticoy Steel. The Dunder-Mifflin paper company site was on Saticoy Street in sunny LA, not Scranton PA.

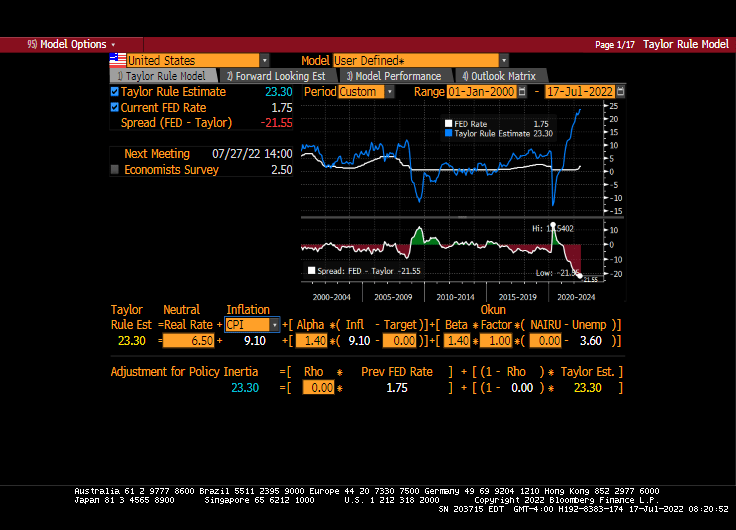

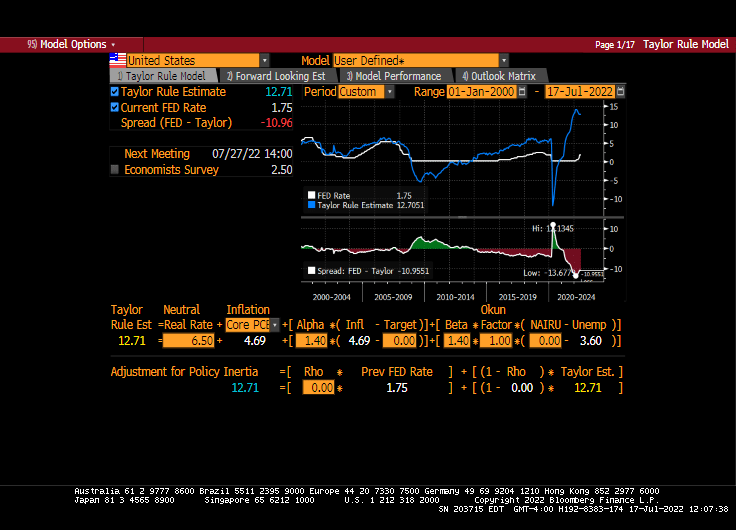

Good luck to The Federal Reserve in combating inflation without causing a recession.

You must be logged in to post a comment.