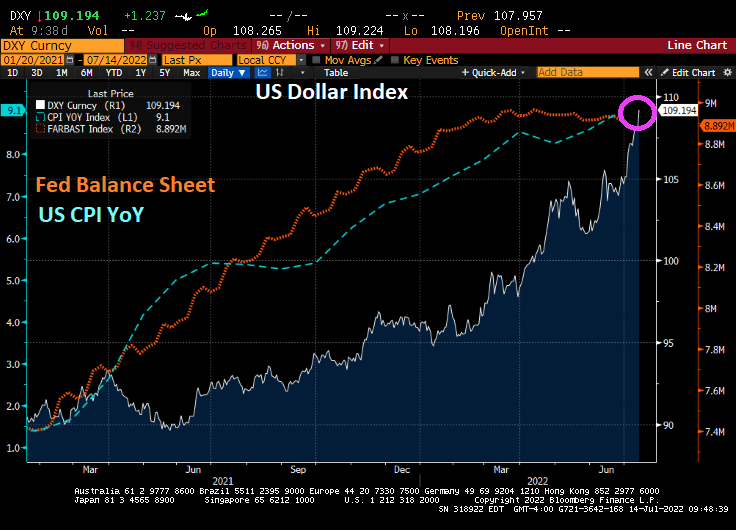

Bear in mind that a strong dollar is a two-edged sword. The US Dollar Index has risen 16% year-over-year, presenting a big hurdle for US firms with business overseas.

That strength of the greenback will rise until the Fed makes a dovish policy pivot.

And that pivot is forecast to occur at the Feb ’23 FOMC meeting.

Face it. The Biden Administration has little interest in trying to increase the supply fossil fuel energy which would anger his “green” base (like building more refineries or allowing for more crude oil and natural gas exploration). So, the burden of “inflation fighting” falls on the frail shoulders of The Federal Reserve.

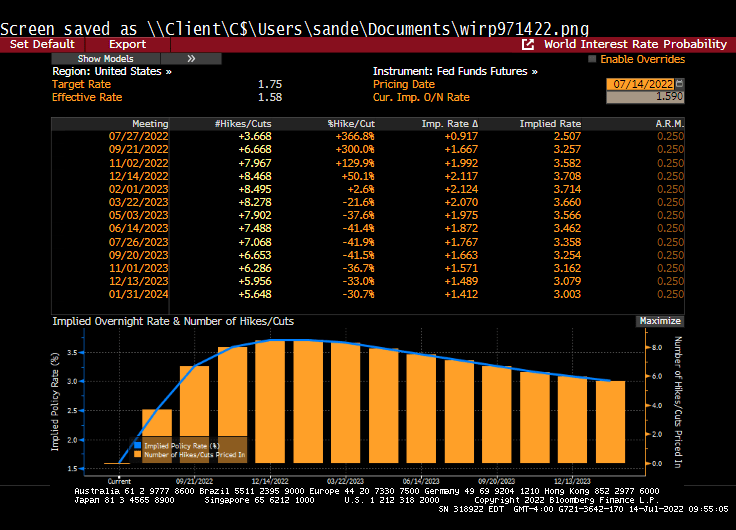

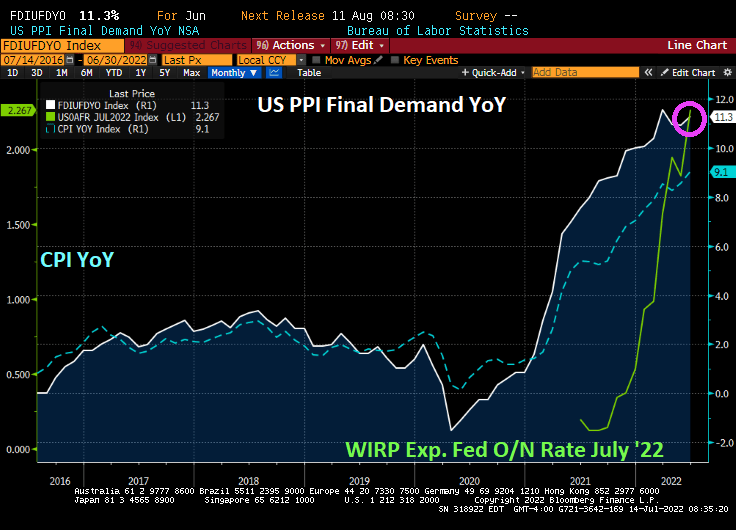

Given today’s US Producer Price Index Final Demand prices rising +11.3% YoY in June, it seems that The Fed has not been able to extinguish the “Tower of Inflation.” But, Fed Funds Futures are pointing to a near 100 basis point (or 1%) increase in The Fed Funds target rate at the July 27th Fed Open Market Committee (FOMC) meeting.

The Fed Funds Futures Data points to a +0.920 (almost 1%) increase at the July 27th FOMC meeting. Followed by rate cuts.

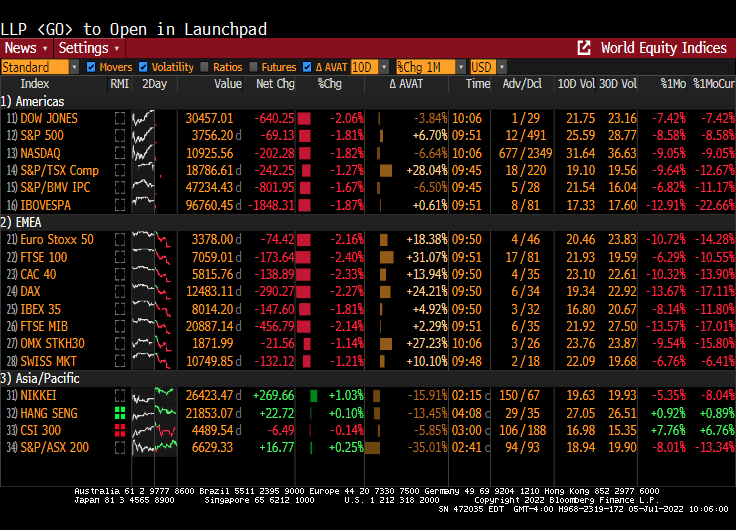

And with the fear of a near 100 basis point increase, today’s stock markets are a sea of red.

It is up to Fed Chair Jerome Powell and policy error brigade to extinguish price increases caused by 1) bad Biden energy policies and 2) too much spending by Biden and Congress. It is like trying to wave-down the Super Chief train with a cigarette lighter.

Yet, the Frail Fed will try to waive down The Super Chief inflation engine with Fed Fireballs. Aka, rate increases of 100 basis points.

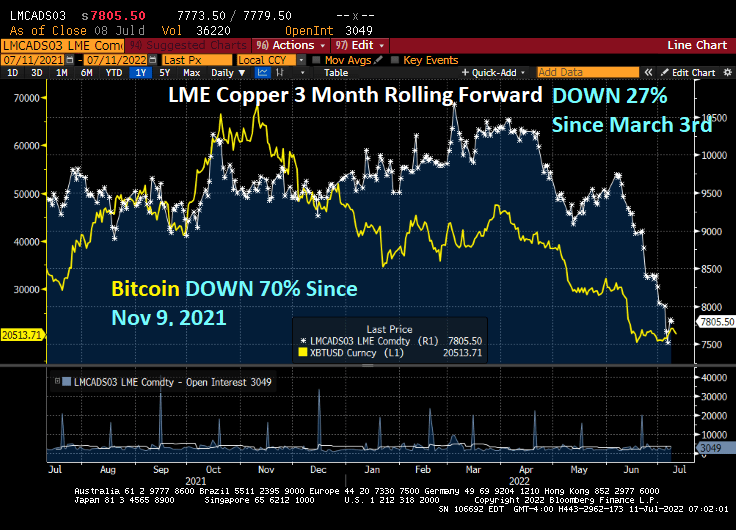

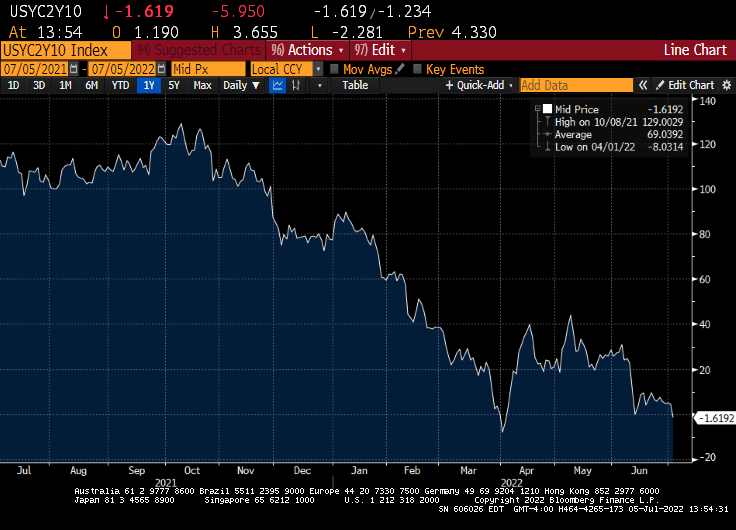

Copper, one of the economic measures of a growing economy, is down -27% since March 3, 2022 as recession looks more likely.

Let’s compare copper with another famous asset, Bitcoin. Bitcoin, a cryptocurrency, is down 70% since November 9, 2021.

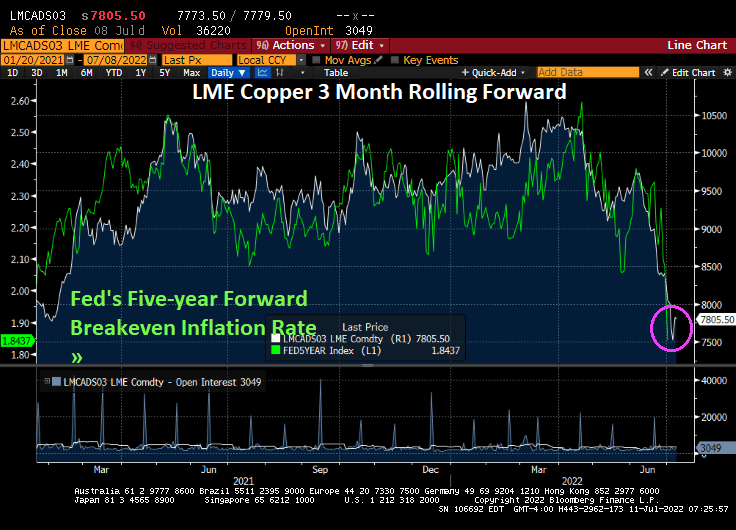

As I discussed yesterday, The Fed’s five-year forward breakeven inflation rate has plunged to its lowest levels under Biden as the global economy is slowing.

Notice that copper prices fit pretty well with The Fed’s 5-year breakeven inflation rate.

It looks like The Fed is killing-off the economy in their quest to tame inflation.

US inflation is the highest in 40 years, yet inflation may be slowing as 1) The Fed cranks up interest rates and 2) the global economy is slowing.

US inflation data in the coming week may stiffen the resolve of Federal Reserve policy makers to proceed with another big boost in interest rates later this month.

The closely watched consumer price index probably rose nearly 9% in June from a year earlier, a fresh four-decade high. Compared with May, the CPI is seen rising 1.1%, marking the third month in four with an increase of at least 1%.

While persistently high and broad-based inflation is seen persuading Fed officials to raise their benchmark rate 75 basis points for a second consecutive meeting on July 27, recession concerns are mounting. There are signs, though, that price pressures at the producer level are stabilizing as commodities costs — including energy — retreat.

But the expectations of inflation, as measured by The Fed’s 5-year forward breakeven inflation rate, just crashed to 1.8437%.

The breakeven inflation rate is a market-based measure of expected inflation. It is the difference between the yield of a nominal bond and an inflation-linked bond of the same maturity.

The USD Inflation Swap Forward 5Y5Y is also falling like a rock as The Fed hikes their target rate (green line).

Could it be that inflation is cooling with Fed rate hikes (but not the shrinking of their $8 trillion balance sheet)?

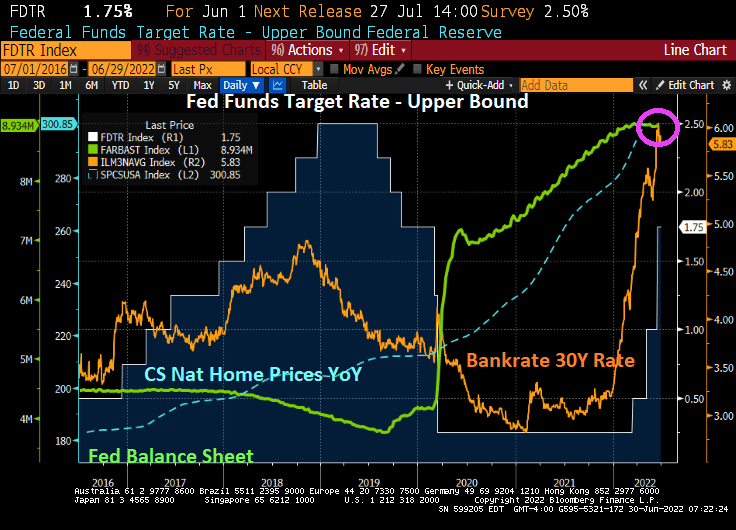

Currently, Fed Funds Futures are pointing to a Fed target rate of 3.552% by February 2023. And with that, Bankrate’s 30-year mortgage rate rose to 5.75%. Once again, like velociraptors from Jurassic Park, The Fed’s balance sheet is still out in force.

Fed Chair Jerome Powell and Atlanta Fed President Raphael Bostic are keeping The Fed’s balance sheet at near $9 trillion as they hunt assets to inflate.

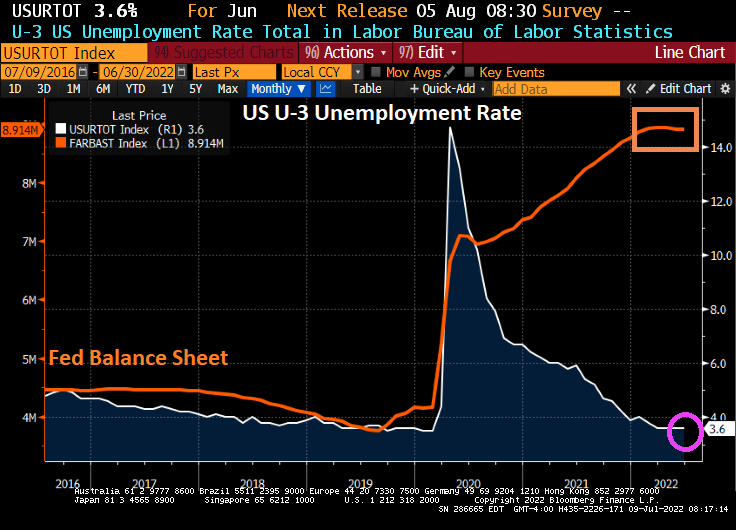

Take the US U-3 unemployment rate. The Biden Administration is proud of the unemployment rate of 3.6%. But if you look at the chart of unemployment relative to The Fed’s balance sheet expansion due to Covid lockdowns, there is still almost $9 trillion of Fed stimulus outstanding.

Of course, the lockdowns were pure economy killers, so opening the economies again led to the unemployment rate falling to 3.6% which is still higher than before the Covid outbreak. But The Federal Reserve has been painfully slow at shrinking its balance sheet, leaving almost $9 trillion in monetary stimulus outstanding.

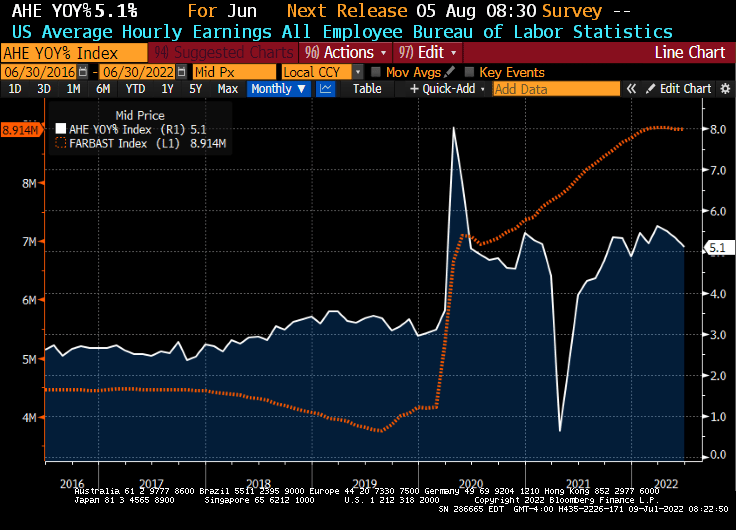

Take average hourly earnings growth. The media is all smiles as US wage growth declined to 5.1%, much higher than pre-Covid.

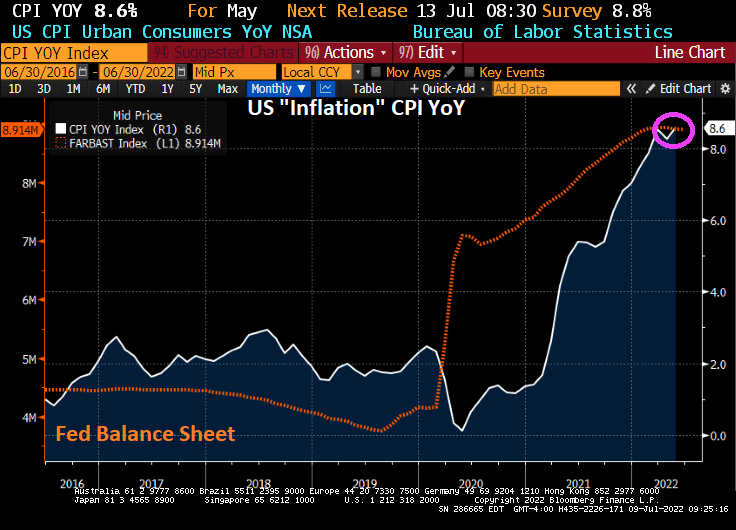

Then we have inflation, at 40-years highs thanks to massive Fed stimulus (and Federal spending).

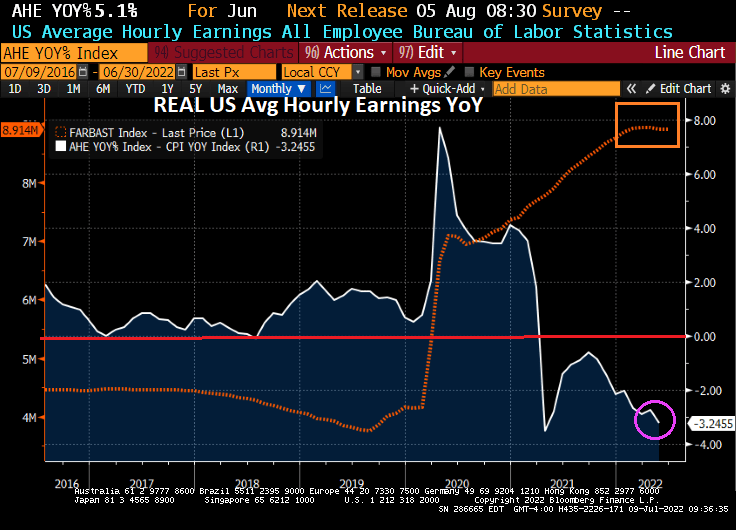

And if we deduct inflation from average hourly wage growth, we see REAL wage growth declining at a -3.25% YoY clip.

Lastly, we have the US Dollar. Nothing has been the same since the financial crisis of 2008 and the entrance of The Federal Reserve distorting the economy and prices. Not to mention the US Dollar.

The Fed leaving its monetary stimulus out in force for so long is a major policy error. So what happens when The Fed actually gets serious about withdrawing the monetary stimulus (likely after the midterm elections)?

The US economy is slowing as inflation ravages consumers. US Regular Gasoline prices, for example, are up 104% under President Biden which helps to slow the economy.

US personal consumption expenditures fell to +0.2% MoM in May as “inflation” or real personal consumption expenditures PRICES rose +6.3% YoY as The Fed’s balance sheet (aka, Master Blaster!) remains.

As I mentioned above, US regular gasoline prices are UP 103% under President Biden, diesel prices (the cost of shipping goods to markets like … food is up 119% under Biden while CRB foodstuffs is up 55% under China Joe.

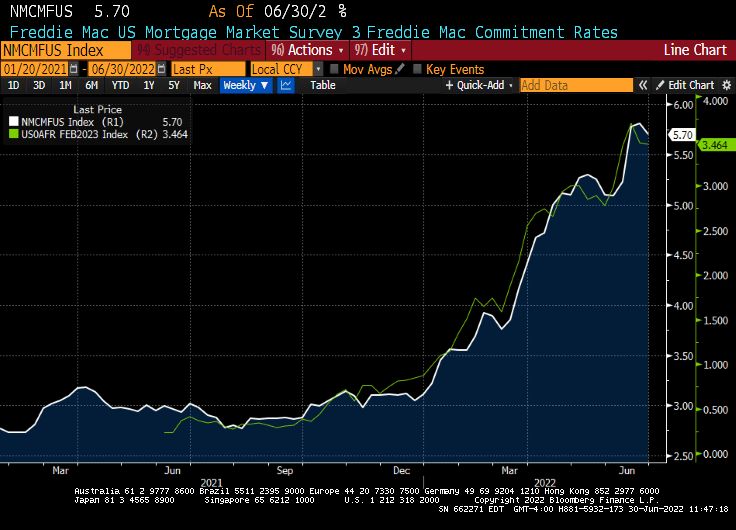

Now we have mortgage rates in the US falling for the first time in four weeks. The average for a 30-year loan was 5.7%, down from 5.81% last week, Freddie Mac said in a statement Thursday.

This year’s Fourth of July celebration is going to cost 18% more than last year’s celebration.

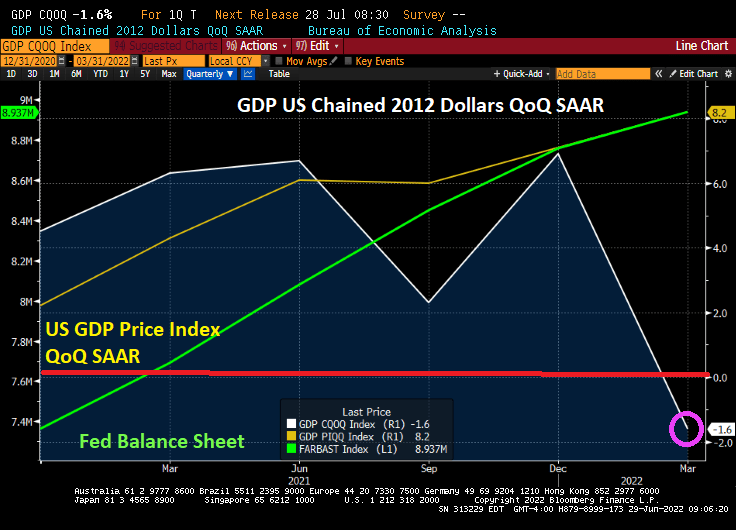

Lastly, the Atlanta Fed GDPNow real time tracker for Q2 is showing … -1% GDP “growth.”

The Federal Reserve under Berananke, Yellen and Powell kept monetary stimulus out there too long and rates too low, but Powell is now trying to reverse that trend to fight inflation. But how will that impact the housing market?

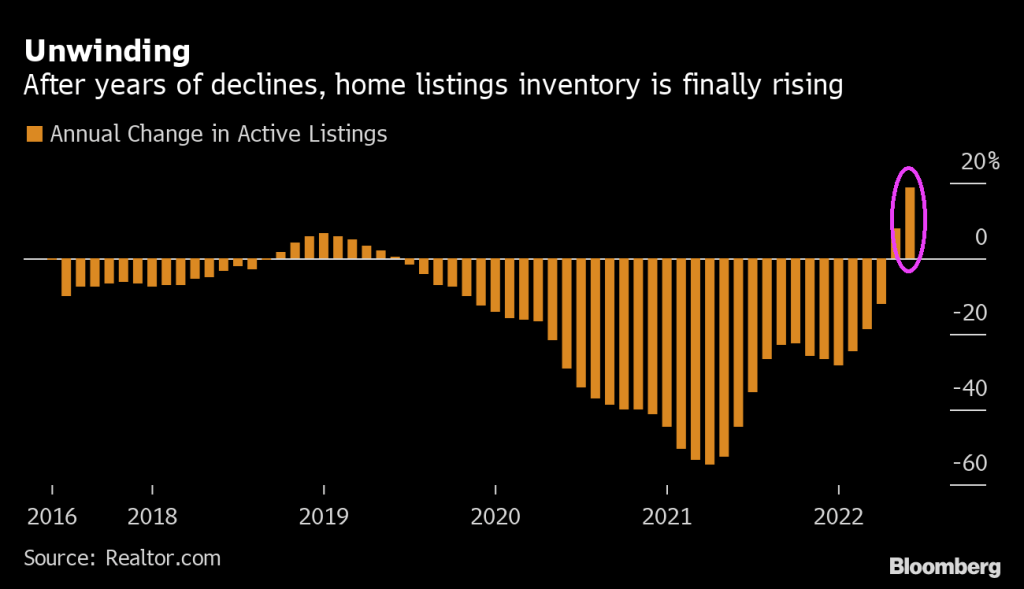

(Bloomberg – Prashant Gopal) The housing slowdown is helping to solve one of the US real estate market’s most intractable problems: tight inventory.

With fewer buyers competing, the number of active US listings jumped 18.7% in June from a year earlier, the largest annual increase in data going back to 2017, Realtor.com said in a report Thursday. And new sellers entered the market at an even faster rate than before the pandemic housing rally began.

The Federal Reserve is cooling off the red-hot housing market as it fights to curb inflation by driving up interest rates. The resulting spike in mortgage costs is making homes less affordable and pushing would-be buyers to the sidelines. That means properties aren’t selling as quickly and must compete with the growing number of new offerings.

I wonder if it is all the Covid monetary and fiscal stimulus that is finally getting homeowners to put their houses on the market, perhaps fearing the end of the housing price run-up with Fed-induced rate hikes?

Let’s see if The Fed’s Frolic Room (aka, open market committee) keeps driving rates up and home affordability down. Or is it The End for the house price bubble?

It took a while and trillions in fiscal and monetary stimulus to recover from Covid-era economic lockdowns, but now that the monetary stimulus is being withdrawn, the economy is stalling.

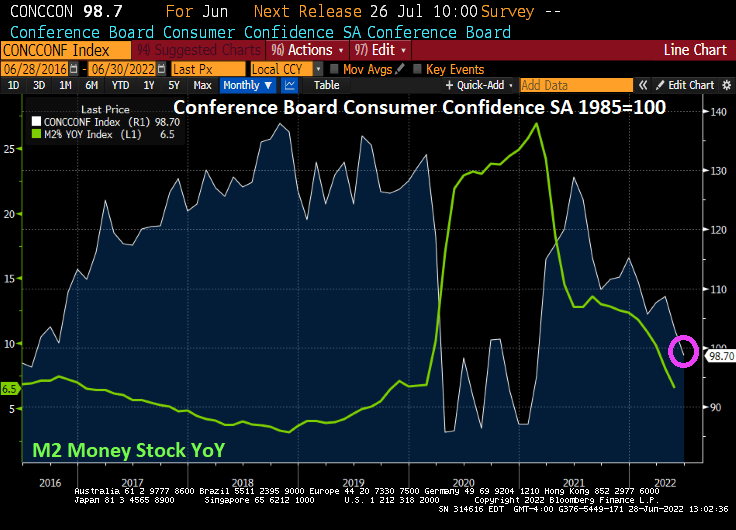

If you look at the chart below, you can see that “The Thrill Is Gone” from monetary and fiscal stimulus.

And The Conference Board’s Consumer Confidence Index fell below 100 as M2 Money Stock YoY returns to pre-Covid levels.

You must be logged in to post a comment.