Preliminary benchmark revision smaller than some had projected

Biggest payrolls adjustment in transportation and warehousing

Are you surprised that the Biden Administration has been lying about job creation?? Not really since Biden compulsively lies about everything. Including his corruption.

US job growth was probably less robust in the year through March than previously reported, according to government data released Wednesday.

The number of workers on payrolls will likely be revised down by 306,000 for March of this year, according to the Bureau of Labor Statistics’ preliminary benchmark revision.

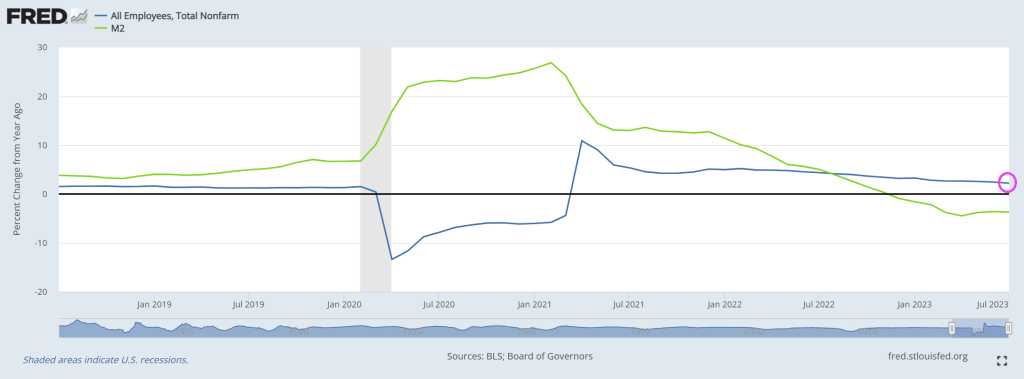

Even without the revision, job growth has slowed to 2.2% YoY in July as M2 Money growth slowed to -3.7% YoY.

Let see what our Overlords say at the Jackson Hole Fed symposium.

We quickly found out in June that one downtown San Francisco office building sold for roughly 70% less than its previously estimated value, an ominous sign of what would come as the commercial real estate market dominos appear to be falling.

Now Sixty Spear St., an 11-story building that is 30% occupied and is expected to be entirely vacant by summer 2025, has been sold to Presidio Bay Ventures for $40.9 million, about a 66% discount versus the most recent assessed property value of $121 million, according to local media SFGATE.

“We acknowledge the formidable challenges that confront San Francisco,” Cyrus Sanandaji, founder and managing principal of Presidio Bay, who is now the office tower’s proud new owner. He remains a bull on the San Francisco office market and wants to expand the building’s square footage from 157,436 to 170,000 square feet and transform it into a “Class-A trophy office building with exceptional design and hospitality-driven amenities.”

All we have to say to Sanandaji’s CRE bet is good luck. The crime-ridden metro area covered in poop must come to terms with City Hall’s horrendous progressive policies that have entirely backfired and led to an exodus of businesses and people. Until Mayor London Breed can instill law and order once more — the ability for the downtown area to thrive once more will remain challenging.

Marc Benioff, the chief executive officer of Salesforce, the city’s largest employer and anchor tenant in its tallest skyscraper, warned last month that the metro area is in danger. He offered a grim outlook: The downtown area is “never going back to the way it was” in pre-Covid times when workers commuted to offices daily.

“We need to rebalance downtown,” Benioff said, adding Breed needs to initiate a program to convert dormant office space into housing and hire additional law enforcement to restore law and order.

… and documenting how the downtown area has rapidly transformed into a ghost town is Youtuber METAL LEO, who walks around with a video camera, revealing empty stores, malls, and towers.

Besides Sixty Spear, SFGATE provided data on other recent tower transactions:

The 13-story 180 Howard St. building, known for being the headquarters of the State Bar of California, sold for about $62 million after being expected to sell for about $85 million.

The offices at 350 California St. reportedly sold for roughly 75% less than its previously estimated value in May, and the 22-story Financial District edifice mostly sits empty. Just a few weeks later, nearby 550 California changed hands for less than half of what owner Wells Fargo paid for the building in 2005.

Things are so bad that some building owners are just walking away from properties:

If you’re curious where we could be in the CRE crisis cycle, a recent analysis by CoStar Group shows 55% of office leases signed before the pandemic that were active during Covid haven’t expired, meaning vacancies will continue to rise.

Here’s what could be next: The collapse of WeWork will only cause more pain for CRE markets nationwide. The coworking company occupies 16.8 million square feet across the US.

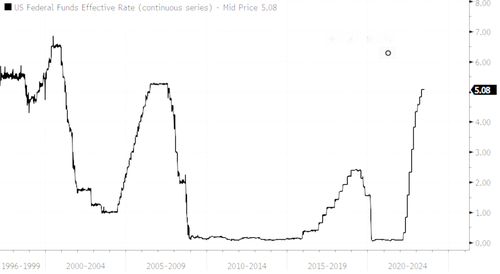

US office space vacancies (white line) have soared since 2008 as The Fed’s massive monetary expansion (blue and green line) has not helped. But Fed monetary expansion DID help drive office prices! At least until 2022, when office space values began to fall. Notice that office values are falling as The Fed withdraws monetary stimulus.

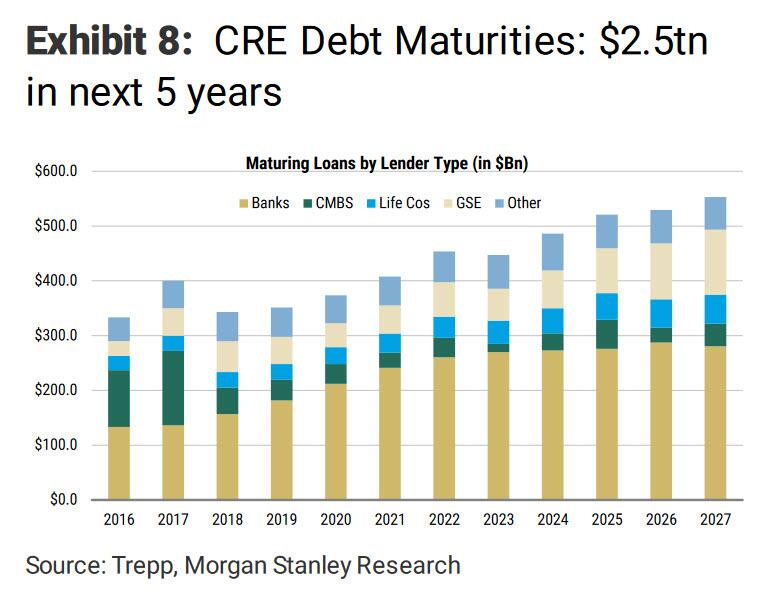

During the regional bank failures in March, we directed our readership to focus on the next potential crisis: “CRE Nuke Goes Off With Small Banks Accounting For 70% Of Commercial Real Estate Loans.”By late March, Morgan Stanley warned clients of an upcoming maturity wall in commercial real estate, which amounts to $500 billion of loans in 2024, and a total of $2.5 trillion in debt that comes due over the next five years.

In a recent Bloomberg interview, Barry Sternlicht’s Starwood Capital Group warned that the CRE space is in a “Category 5 hurricane.” He said, “It’s sort of a blackout hovering over the entire industry until we get some relief or some understanding of what the Fed’s going to do over the longer term.”

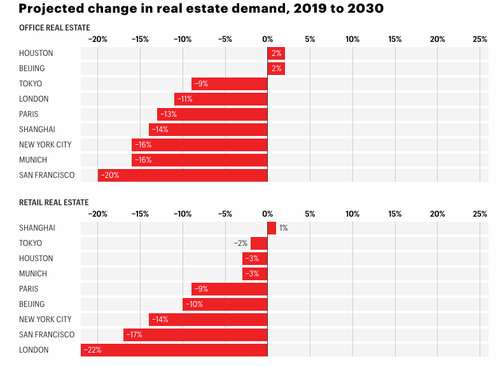

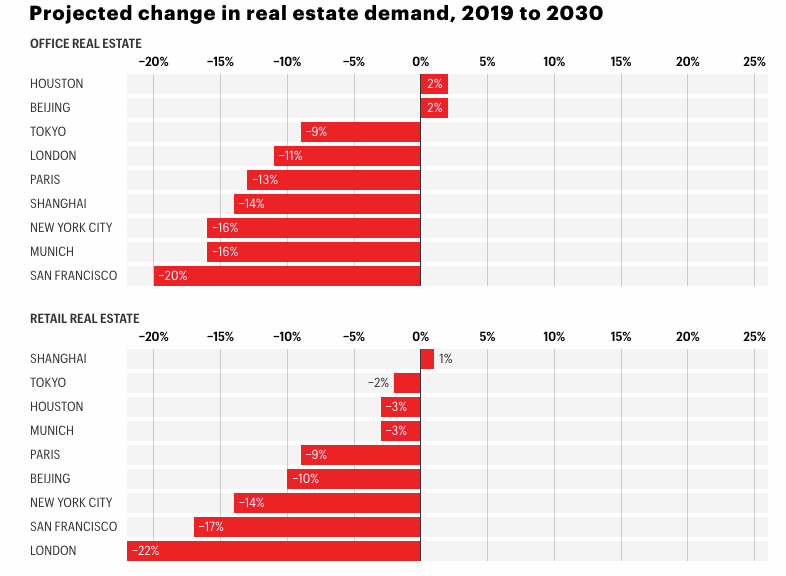

The current downturn in CRE could persist for years, if not through the end of this decade. Jan Mischke, a partner at the McKinsey Global Institute, along with Olivia White, a senior partner at McKinsey, and Aditya Sanghvi, a senior partner and leader of McKinsey’s real estate special initiative, published a note in Fortune, warning “$800 billion of office space in just nine cities could become obsolete by 2030.”

The authors of the report blame the CRE downturn on the “shift to remote and hybrid work prompted two further shifts in people’s behavior”:

First, many residents, untethered from their offices and therefore less fearful of long commutes, moved away from urban cores. New York City’s urban core (that is, the dozen densest counties in the metropolitan area) lost 5% of its population from mid-2020 to mid-2022. San Francisco’s urban core (San Francisco County, Alameda County, and San Mateo County) lost 6%.

Second, consumers began shopping less at brick-and-mortar stores–and far less at stores in urban cores, where people were now less likely either to work or to live. Foot traffic near stores in metropolitan areas remains 10 to 20% below pre-pandemic levels, but the differences between urban and suburban traffic recovery are substantial. For example, in late 2022, foot traffic near New York’s suburban stores was 16% lower than it had been in January 2020, while foot traffic near stores in the urban core was 36% lower.

As fewer employees work in the office, demand for office space will fall. By 2030, such demand will be as much as 20% lower, depending on the city–even in a moderate scenario in which office attendance goes up but remains lower than it was before the pandemic.

And as fewer consumers shop at brick-and-mortar stores, demand for retail space will fall as well, according to our model. In the urban core of London, the hardest-hit city, demand for retail space will be 22% lower in 2030 than it was in 2019 in a moderate scenario.

Some of the most significant declines in office and retail space demand through 2030 will be in major US cities such as San Francisco and New York City.

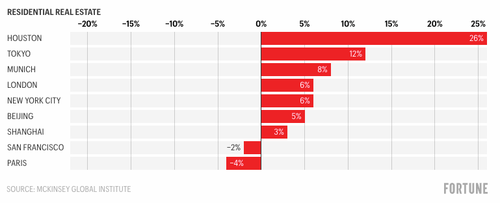

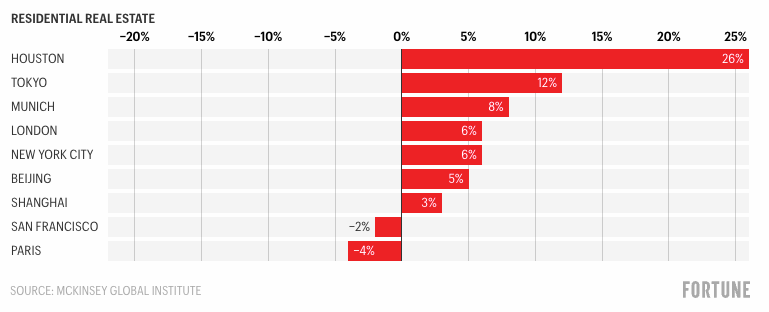

The authors note that the demand for “residential space will suffer less”… Well, according to their forecasting model.

“The reduced demand will have major impacts on urban stakeholders. For example, in just nine cities that we studied especially closely, $800 billion of office space could become obsolete by 2030. And macroeconomic complications could make matters even worse,” the authors continued. Without office workers in downtown areas, economic recoveries in major cities will be a “U” shape or, in some cases, an “L.”

The unraveling of downtowns is already underway. We shared a video this week of scenes of San Francisco’s downtown transformed into a ‘ghost town.’ Building owners in the crime-ridden metro area are already giving up and defaulting as vacancies rise, crime surges, and refinancing is near impossible in today’s climate as the Federal Reserve keeps interest rates sky-high to tame the worst inflation in a generation.

We shift our attention to Baltimore City, where office towers are being dumped in an apparent firesale.

The authors failed to report that the sliding demand for office towers isn’t just because of “remote and hybrid work” but also due to an exodus of companies fleeing crime-ridden progressive cities that fail to enforce law and order.

If McKinsey’s predictions are correct, certain segments of the CRE market are expected to experience prolonged turmoil for years. Some US mayors have proposed an immediate solution to convert office towers into multi-family units. However, this transformation could take years due to the time-consuming processes of obtaining permits and construction.

Yes, the maestros of real estate asset bubbles (Yellen) and eventual deflation (Powell)!

No, this isn’t a John Kerry/Greta Thunberg hysterical warning about climate change. But a storm created by 1) Biden/Congress spending splurge and 2) excessive monetary stimulypto by The Federal (Feral) Reserve. Now that The Fed is withdrawing the excess stimulus, we are seeing a world of pain for commercial real estate. A financial climate change!

“We’re in a Category 5 hurricane,” Sternlicht said in an interview on June 28 taped for a July 25 release in an upcoming episode of Bloomberg Wealth with David Rubenstein.

Sternlicht warned, “It’s sort of a blackout hovering over the entire industry until we get some relief or some understanding of what the Fed’s going to do over the longer term.”

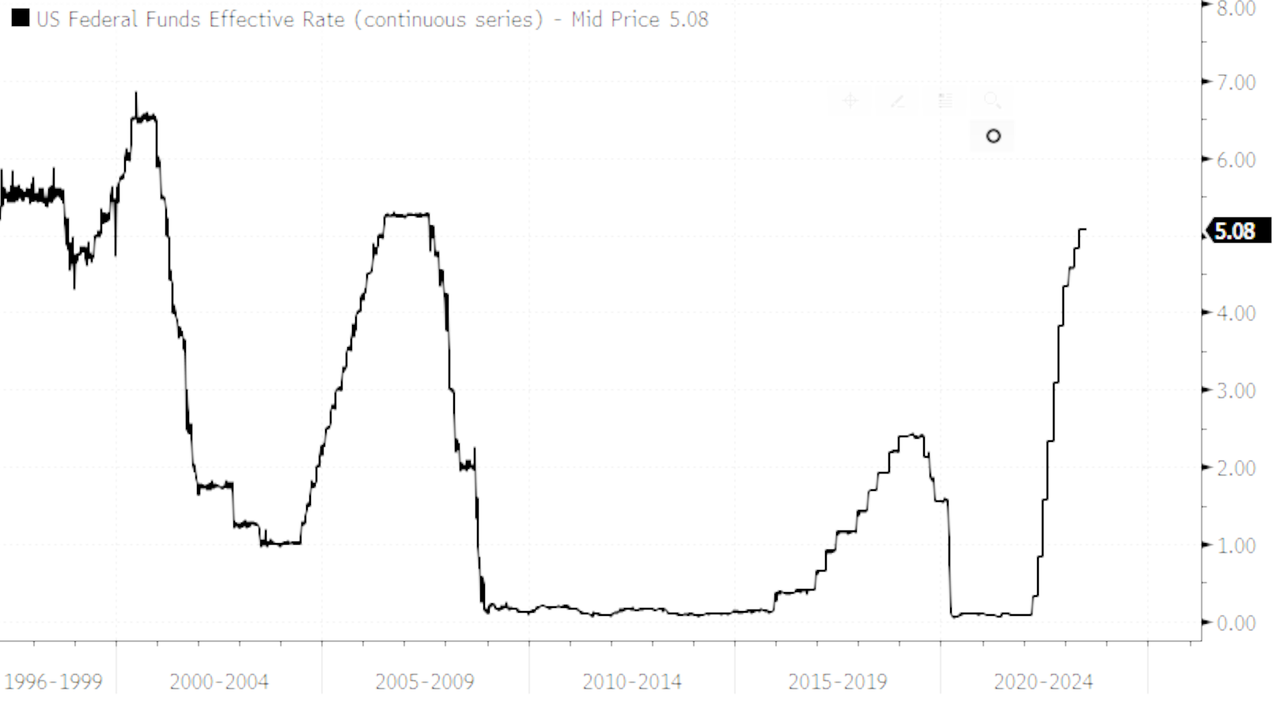

He explained the CRE downturn was sparked by the Federal Reserve’s sixteen months of aggressive interest rate hikes to tame inflation — and unlike past downturns — not due to reckless speculation.

Tighter credit conditions following the regional bank crisis in March have made refinancing existing buildings exceptionally hard for landlords and come as vacancies rise.

Sternlicht recalled that his firm tried to obtain a bank loan for a small property not too long ago. He said his staff reached out to 33 banks, and only two came back with offers.

According to Morgan Stanley, the elephant in the room is a massive debt maturity wall of CRE loans that totals $500 billion in 2024 and $2.5 trillion over the next five years.

As we’ve seen in San Francisco, the inability to refinance as some properties sustain rising vacancies will pressure landlords to sell properties or walk away from them.

Sternlicht said there’s a very real possibility of a “second RTC” event playing out, referring to Resolution Trust Corp., the government entity that led the effort to liquidate assets of the savings and loan associations that failed three decades ago.

“You could see 400 or 500 banks that could fail,” he said. “And they will have to sell. It also will be a great opportunity.”

Sternlicht launched his real estate firm during the era of RTC, purchasing multi-family units and flipping them to billionaire Sam Zell 18 months later for triple the price.

Sternlicht said the Federal Deposit Insurance Corp would likely begin offloading CRE loans on Signature Bank’s books, which failed in March. He said, “The government’s going to prop up the value of that portfolio by providing very cheap financing to it.”

* * *

Transcript of the interview:

David Rubenstein:

Sometimes people are saying that the best investment opportunity now is distressed real estate debt — that you can buy the debt from banks at a discount. But do you think it’s too early for that?

Barry Sternlicht:

You know, we were gonna give back an office building. And they said, “Well, not so fast. If you want to, we’ll restructure the loan. And we’ll cut the loan in half. And you put the money in here. And we’ll take this as a junior note.” Because the banks don’t want the assets back. They’re not set up to carry these assets. It’s not their business.

So you’re beginning to see stuff. We’re going to see this big trade of the [Signature] Bank portfolio. That’s going to be a benchmark for market.

David Rubenstein:

A lot of fortunes were made in the real estate world in’ 07-’08 when people bought distressed real estate. The late ’80s too, when the RTC was here. Do you see funds being formed to buy these assets? But you think they won’t be available for a year or two?

Barry Sternlicht:

Right now you have an unusual situation in the real estate markets because everyone’s sort of looking at the yield curve. And it says rates will be lower later. Everyone says, “You know, survive till ’25. Hold onto your assets.” So transaction volumes have plummeted.

Unless you have to sell something today, nobody wants to sell anything today. They think tomorrow will be rosier. So for the most part, everybody’s pushing any sales back. But what you’re seeing is when a loan is maturing and a borrower can’t cover the current debt service. Something’s gotta give. Unfortunately, we’re also a lender.

David Rubenstein:

Are we going to change the way office buildings are really valued in the future because tenants aren’t going to need as much space? Or do you think eventually the tenants will come back and the employees will come back?

Barry Sternlicht:

The work-from-home phenomenon is a US phenomenon. If you go to England or Germany, rents are up, and vacancy rates in the top German property markets — Berlin, Frankfort, Munich, Hamburg — are less than 5%. People are back in the office. You and I go to the Middle East, they’re full. We have offices in Asia, they’re full. So this is a US situation.

In the US you have two markets. The nice buildings will stay rented and my guess is at pretty good rates. And the B and C stuff is going to be — maybe fields of grain or something. It’ll be very pretty. We’ll have all these little mid-block parks in New York City because there won’t be anything else to do with those buildings.

The other thing about office is AI. AI is going to hit a couple of these industries that have been big users of office space. So that’s sort of a big question mark in the investment equation.

David Rubenstein:

Let’s suppose I’m an average person. Where should I put my money as an investor in real estate?

Barry Sternlicht:

High interest rates are depressing the number of single-family home units that have been built so now you’re having an ever-increasing scarcity of residential. Given the cost of construction, the whole residential complex — including single-families for rent, multi-family, the housing market, even residential land — I think they make interesting investment opportunities today.

David Rubenstein:

Is it a good thing for people to now invest in a real REIT?

Barry Sternlicht:

I think real estate has a nice place in the balance sheet of any individual. In the pandemic, we raised a special-situations fund and bought 15 names in the REIT business, and we were up, like 70% at one point. We’re going to do that again. And if you take a long-term view, some of these are good companies with the wrong interest-rate environment. I wouldn’t even say they have the wrong balance sheet, but they are so out of favor. There are some really good buys out there. So if you’re clever, you could buy some public REITs.

David Rubenstein:

What kind of return should an average REIT investor expect?

Barry Sternlicht:

In the mortgage REIT, Starwood Property Trust, we’re paying a 10% dividend. So you get that and any appreciation in the stock, and the stock’s currently trading below book value. It usually trades above book value. It used to trade at 1.23 times and now it’s trading at .9. So if it reverts, you’ll get a 15% return. We’ve averaged 11.3% over 10 years.

David Rubenstein:

Why should somebody want a career in real estate? Why is that a good business to be in?

Barry Sternlicht:

You’ve got to find niches, and there are a lot of niches in real estate. And it’s very micro, block by block. If I didn’t have my firm today, could I buy — even in a city like New York — and redo apartments and housing. I could make money doing that. I have a friend of a friend who’s bought 300 homes. He turned living rooms into bedrooms, put them all on Airbnb. He’s earning a fortune and using Airbnb as his distribution set. It’s a giant industry. There’s always something to do.

David Rubenstein:

You were based in the northeast part of the US for much of your career. You grew up in Connecticut, you were born in Long Island. But you picked up and moved to Miami. Why did you do that a few years ago? And any regrets about moving to Miami?

Barry Sternlicht:

Well, my mom’s down there. And I got divorced. That was one reason. Change your life, start over. There was obviously a tax benefit to doing so. And I had sold an interest in my firm at the time. I was based in Connecticut. I was based in Greenwich, our headquarters was there. I looked at my travel calendar in a normal year and I was only home for about a third of it. So I didn’t think it’d be that hard to move and make that my base of operations. It turned I caught the wave perfectly.

I was an early settler into Miami. And, you know, the home prices probably tripled there. I should have bought everything with my house. I would have had the best-performing real estate fund in the world.

David Rubenstein:

If your mother came to you and said, “I have $100,000. I need to invest it somewhere. Where should I invest it?” You would say where, real estate?

Barry Sternlicht:

Today if you look at my portfolio, I have a significant amount of cash that I never had before because I’m getting 5% for the cash. Pretty soon I’m going to just start deploying that capital when I can see the sun coming through the clouds of the Fed’s movement. When the Fed basically tells you they’re done, I think real estate will catch a very firm bid.

Greta Kerry? John Thunberg?? They are the same repeater, and non thinker.

Here the real (financial) climate terrorists!! Yellen and Powell.

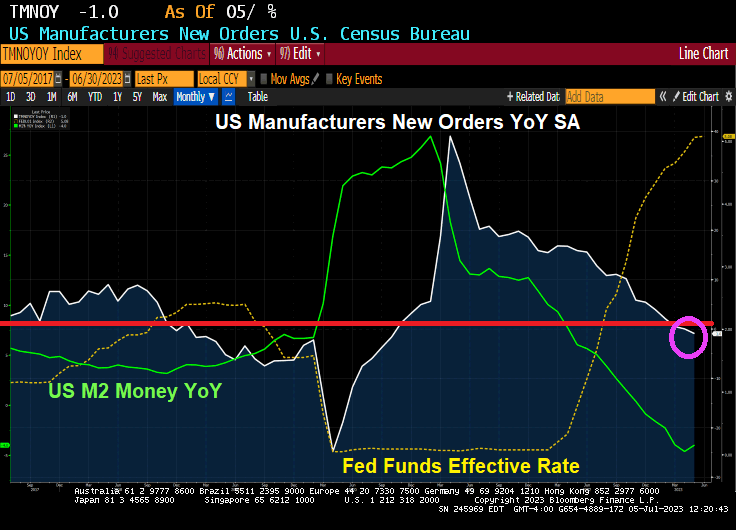

As Powell and The Gang raise interest rates, the more the economy is … slip slidin’ away. US Manufacturers New Orders YoY in May declined -1.0% for the first time since Covid.

I was hoping that the week of July 4th would start off with fireworks, but we got bad news about the economy.

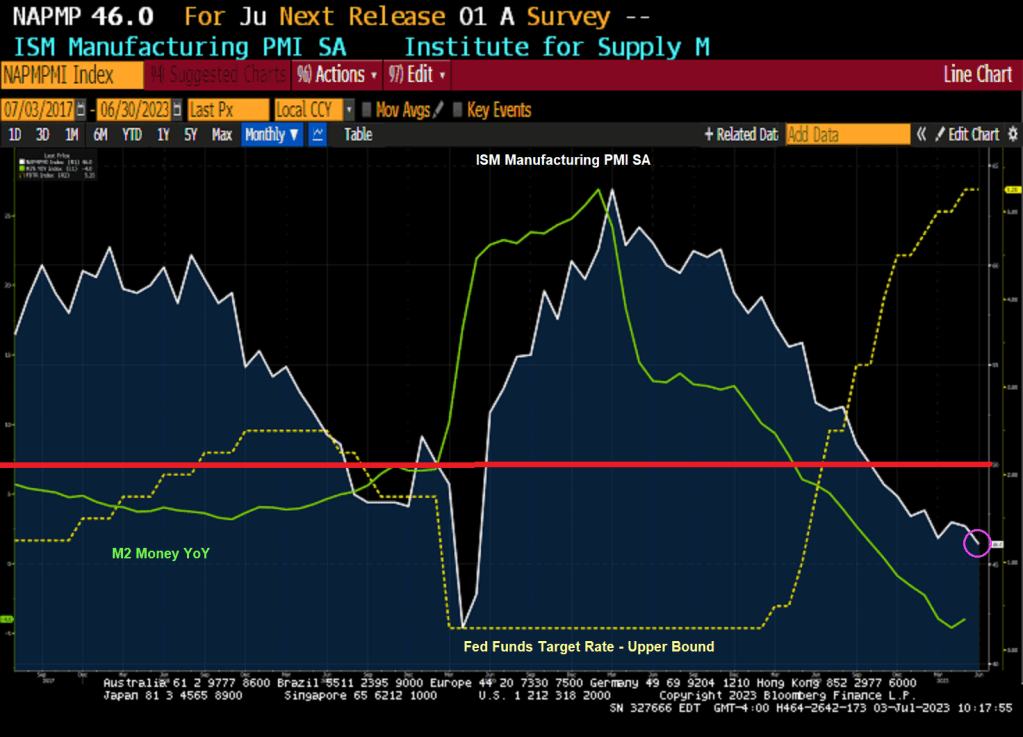

US factory activity contracted for an eighth month in June, slipping to the weakest level in more than three years as production, employment and input prices retreated.

The Institute for Supply Management’s manufacturing gauge fell to 46, the weakest since May 2020, from 46.9 a month earlier, according to data released Monday. The current stretch of readings below 50, which indicates shrinking activity, is the longest since 2008-2009.

The decline in the ISM production gauge, which also stands at the lowest level since May 2020, suggests demand for merchandise remains weak. The index of new orders contracted for the 10th straight month and order backlogs shrank, which may help explain a pullback in a measure of manufacturing employment.

The ISM gauge retreated to a three-month low and, at 48.1, indicates fewer producers adding to payrolls.

Many Americans continue to limit their spending on merchandise as they rotate to services and experiences. Others are simply tightening their belts as still-high inflation takes a toll on their incomes.

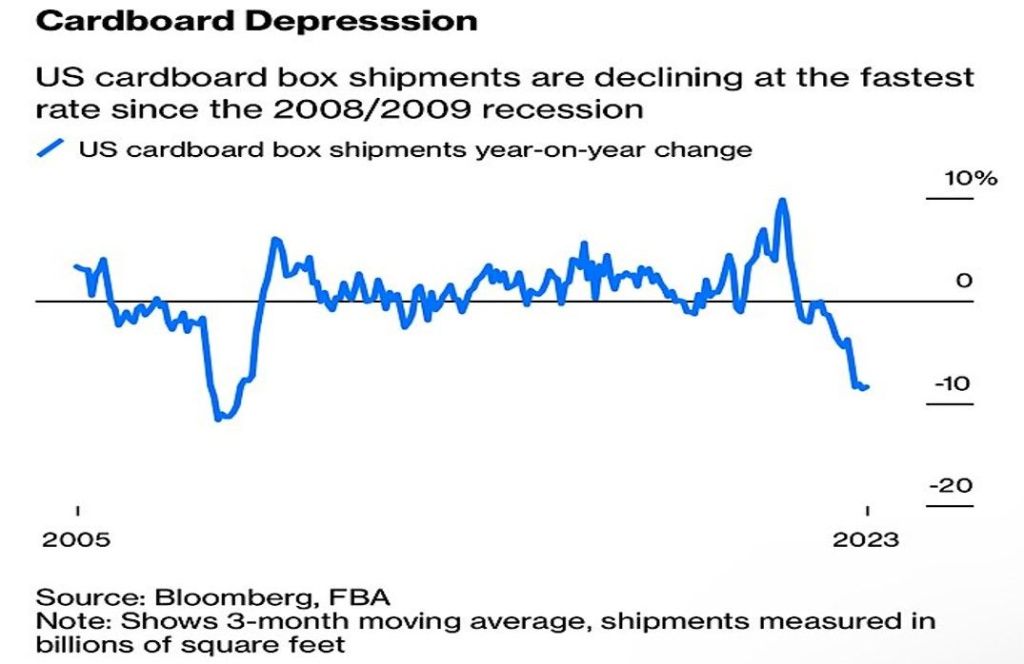

And then we have cardboard box shipments declining at fastest rate since 2008/2009.

At least Ethereum is up over 2% this morning.

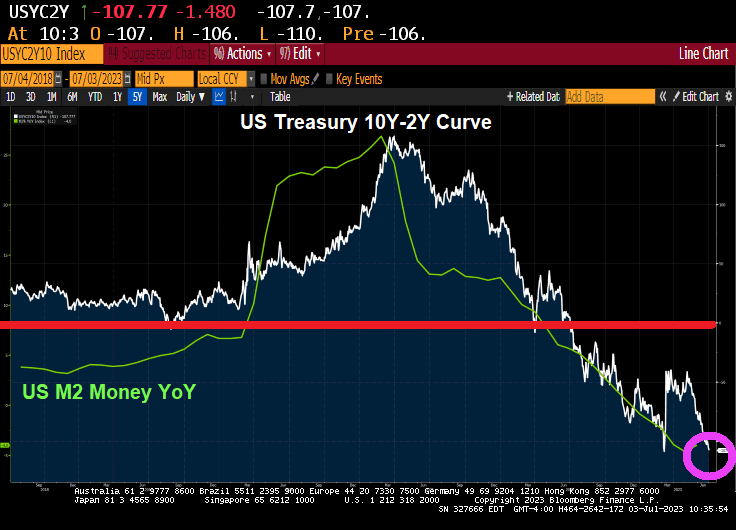

And the US Treasury 10Y-2Y keeps on diving deeper into inversion.

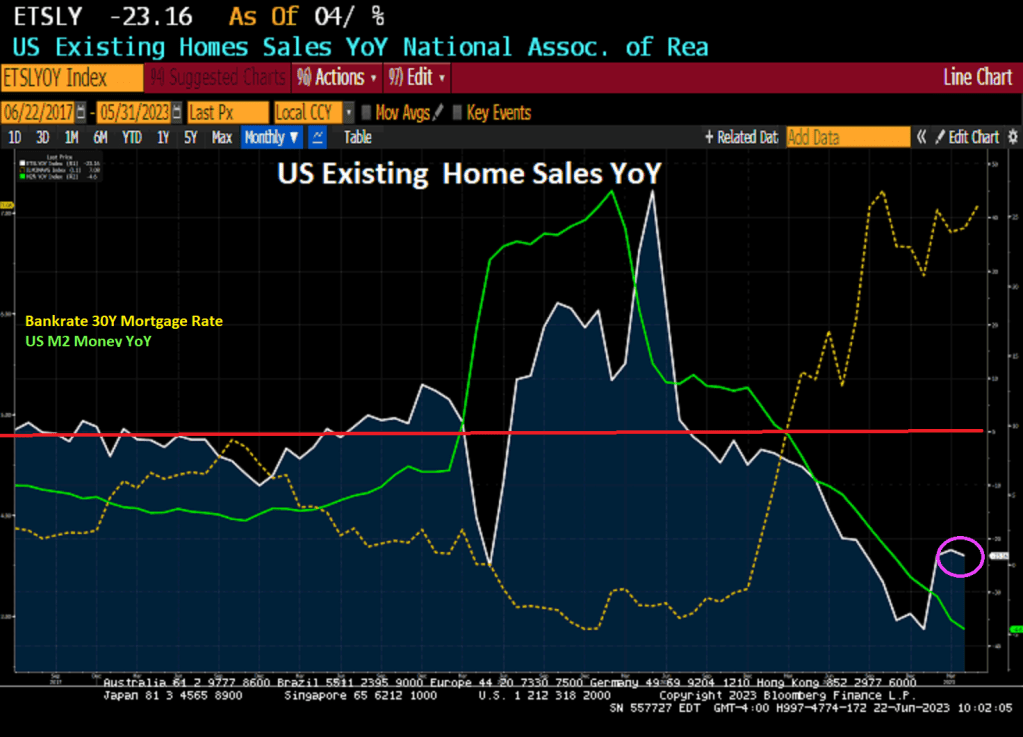

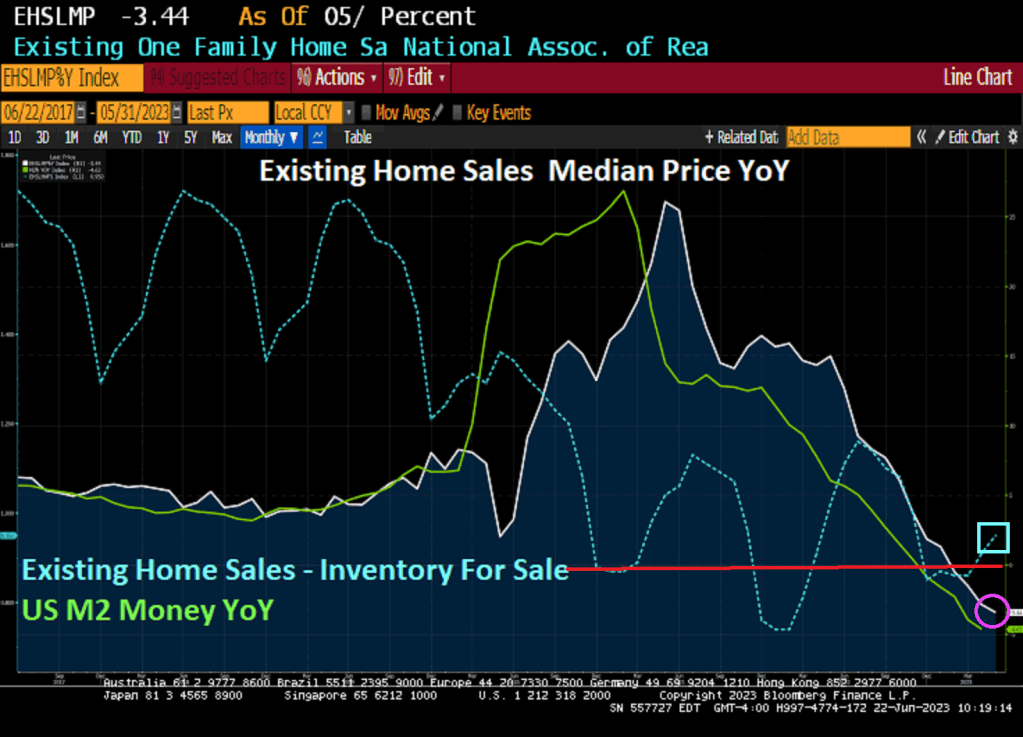

Like a bad good news, bad news joke, the good news is that US existing home sales ROSE 0.2% in May. The bad news? Existing home sales are DOWN -23.16% on a year-over-year basis.

And the median price of existing home sales fell -3.44% YoY as inventory for sales remains missing in action (like Biden debating Democrat challengers).

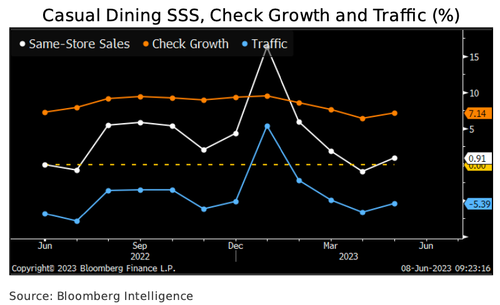

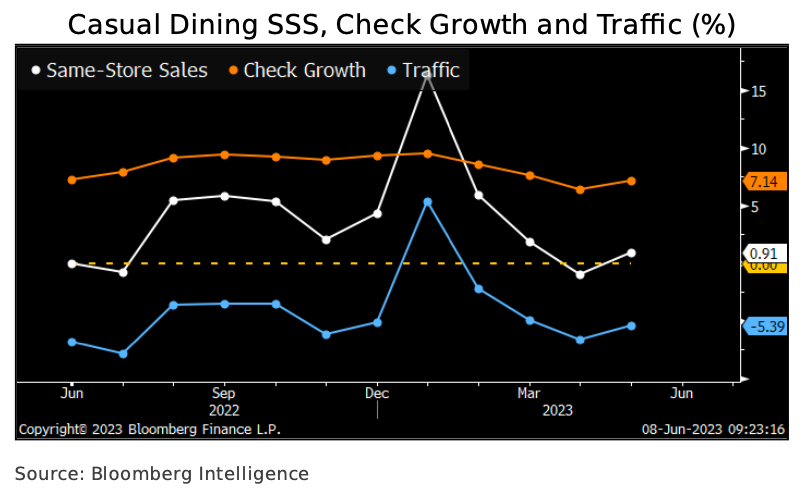

Bloomberg Intelligence’s Michael Halen penned a new note titled “2H Restaurant Sales: Inflation Killing Appetites.” It outlines, “Consumer spending finally buckles under more than two years of inflation and price hikes,” and the likely result is a trade-down of casual-dining chains like Brinker and Cheesecake Factory for quick-service chains like McDonald’s and Wendy’s.

The trade-down, which could start as early as this summer, is expected to dent consumer spending in restaurants such as Cheesecake Factory, Texas Roadhouse, and at brands operated by Brinker and Darden, Halen said.

Casual-dining industry same-store sales rose just 0.9% in May, according to Black Box Intelligence, as traffic dropped 5.4%. We expect cash-strapped low- and middle-income diners to cut restaurant visits and checks through year-end due to more than two years of real income declines and ballooning credit-card balances.

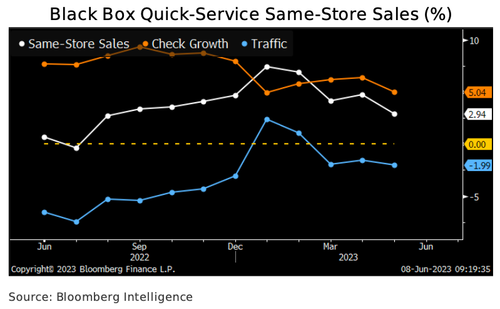

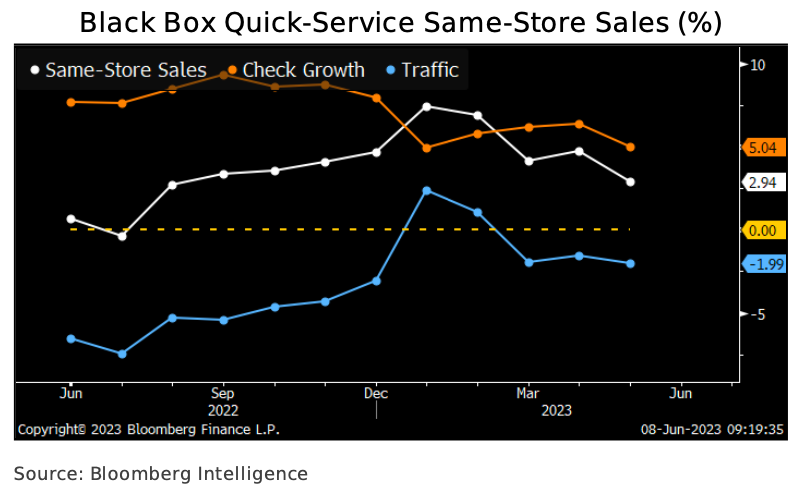

Halen provides more details about quick-service restaurants to fare better than causal-dining ones as “consumer spending finally buckles.”

Quick-service restaurants’ same-store sales could moderate with consumer spending in 2H but should fare better than their full-service competitors. Results rose 2.9% in May, according to Black Box data, as a 5% average-check increase was partly offset by a 2% guest-count decline. Check- driven comp-store sales gains are unsustainable, and we think inflation and menu price hikes will motivate low- and middle-income diners to reduce restaurant visits and manage their spending in 2H. On Domino’s 1Q earnings call, management said lower-income consumers shifted delivery occasions to cooking at home. Still, a trade-down from full-service dining due to cheaper price points may cushion the blow.

McDonald’s, Burger King, Wendy’s, and Jack in the Box are among the quick-service chains in Black Box’s index.

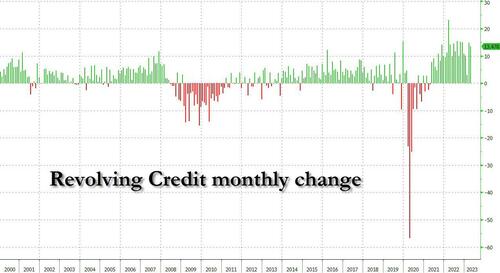

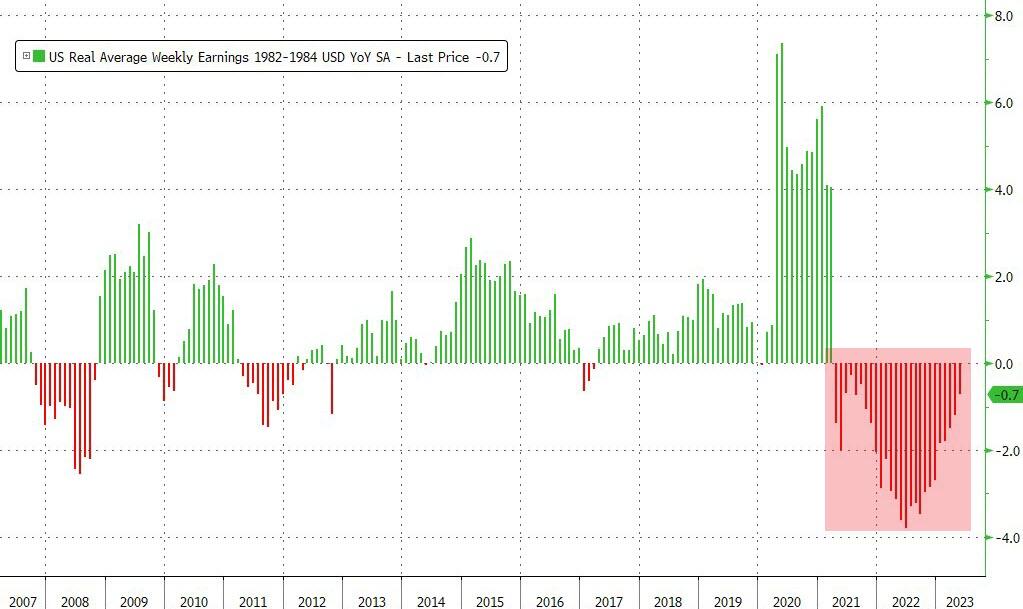

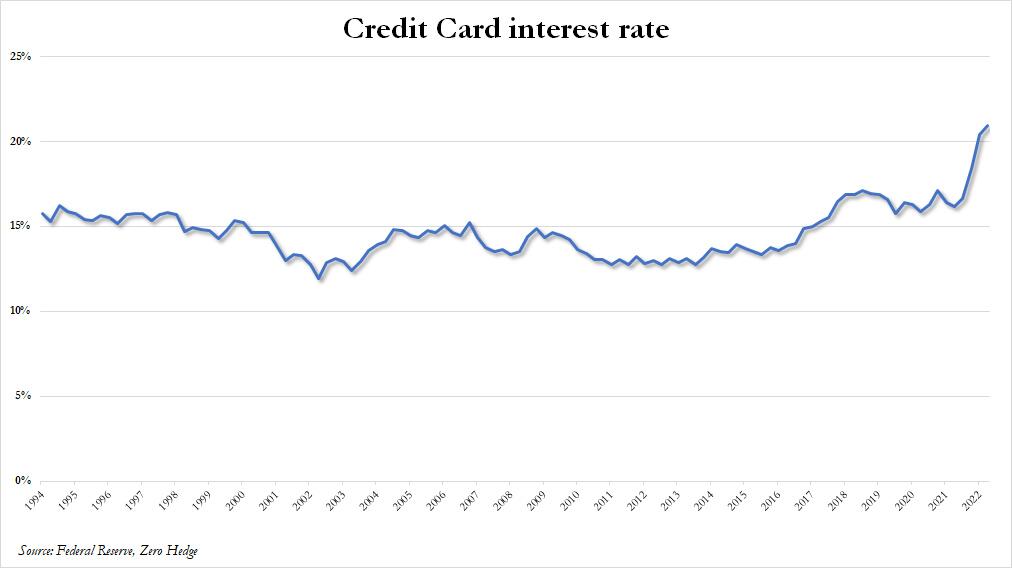

The latest inflation data shows consumers have endured the 26th straight month of negative real wage growth. What this means is that inflation is outpacing wage gains. And bad news for household finances, hence why many have resorted to record credit card usage.

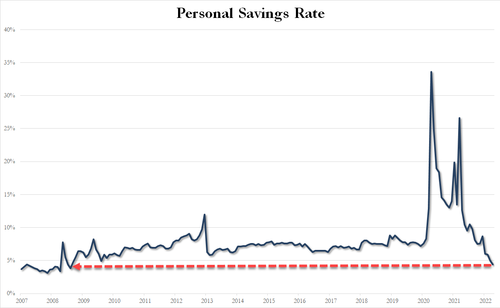

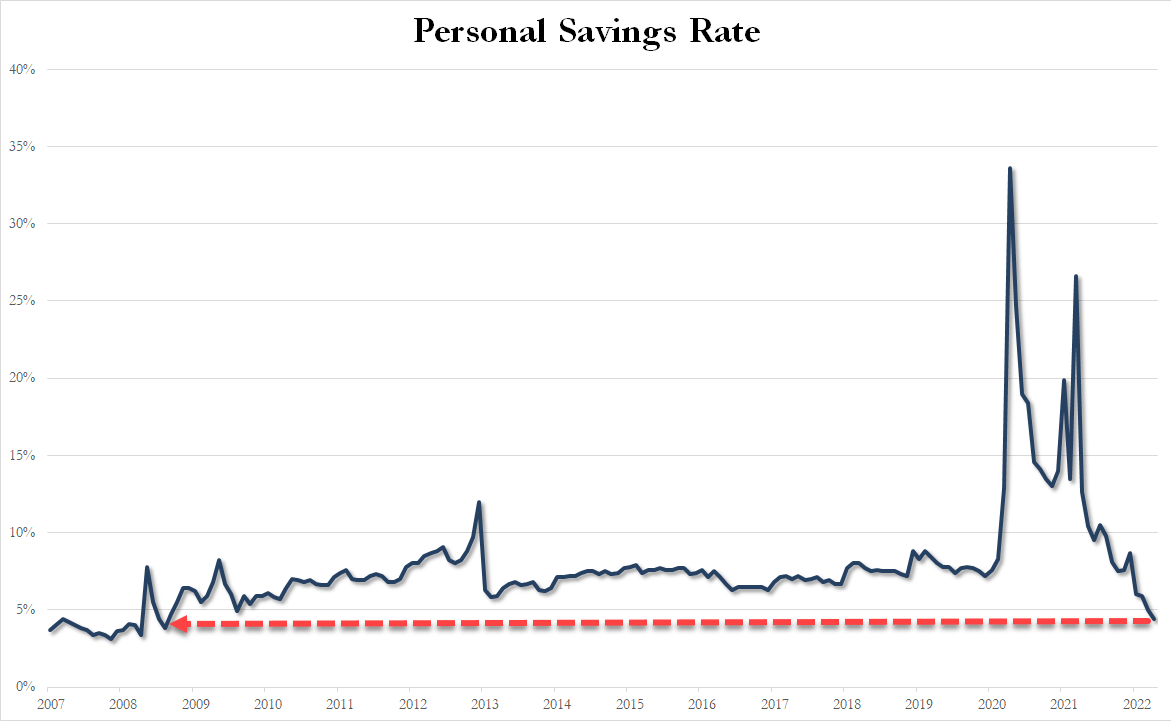

And the personal savings rate has collapsed to just 4.4%, its lowest level since Sept. 2008 (the dark days of Lehman). And why is this? To afford shelter, gas, and food, consumers are drawing from emergency funds due to the worst inflation storm in a generation.

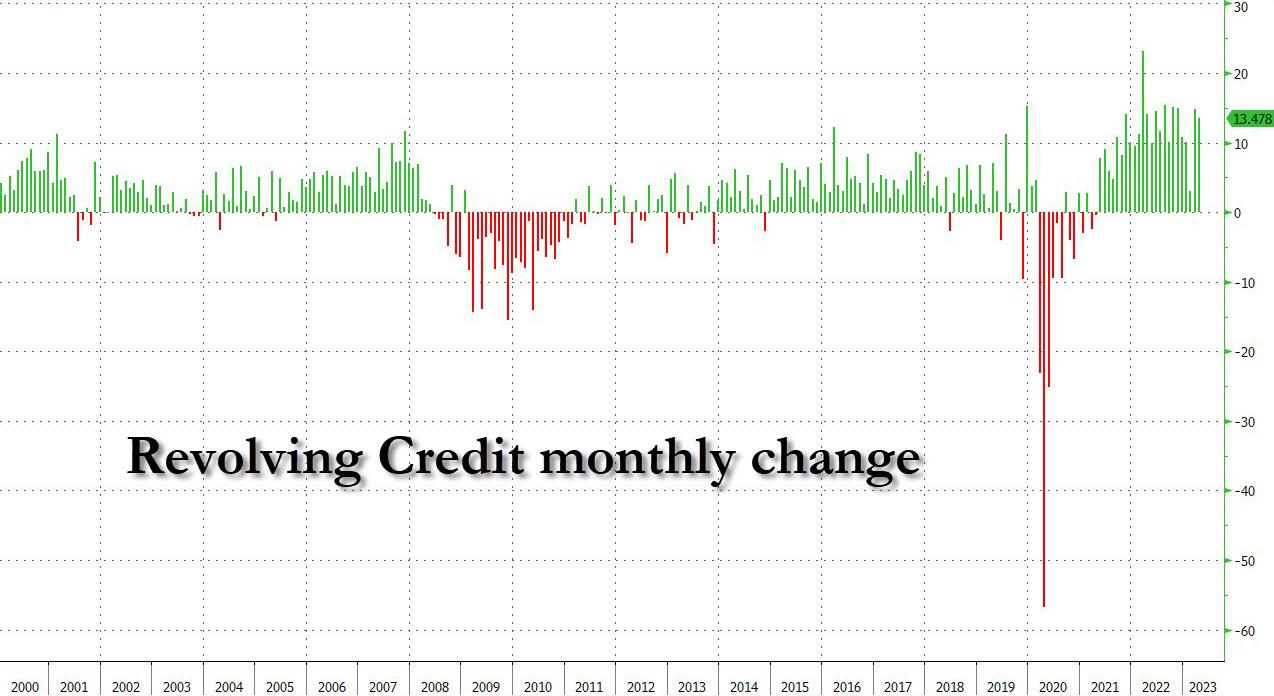

As revolving consumer credit has exploded higher and the last two months have seen a near-record increase…

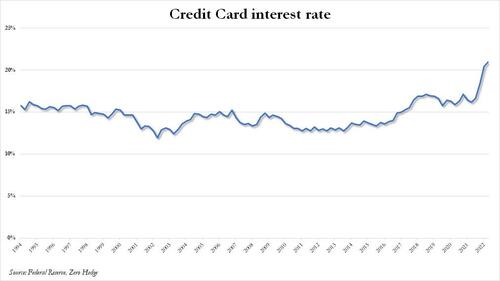

… even as the interest rate on credit cards has jumped to the highest on record.

With record credit card debt load and highest interest payments in years, plus depleted savings, oh yeah, and we forgot, the restart of student loan payments later this year, this all may signal a consumer spending slowdown at causal diners while many trade down for McDonald’s value menu. Even then, we’ve reported consumers have shown that menu items at the fast-food chain have become too expensive.

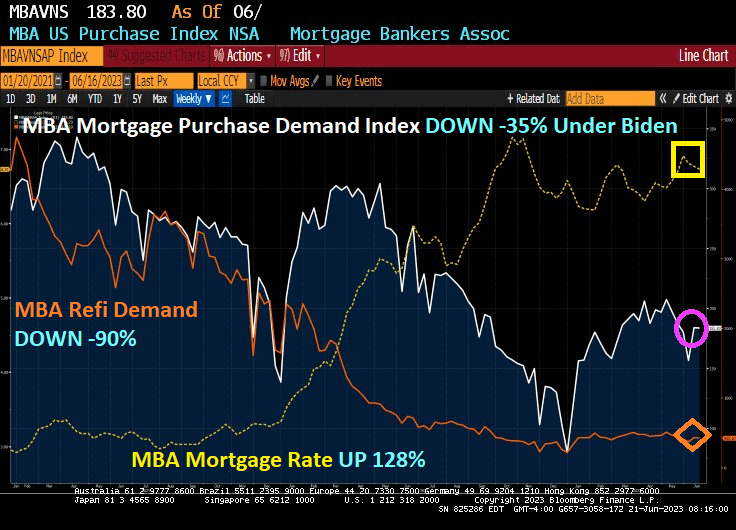

The good news? Mortgage purchase demand fell only -0.05% from last week. The bad news? Mortgage purchase demand is down -35% since Resident Biden was sworn in. And mortgage refinancing demand is down a whopping -90%. Reason? Mortgage rates are up 128% under Clueless Joe.

Mortgage applications increased 0.5 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending June 16, 2023.

The Market Composite Index, a measure of mortgage loan application volume, increased 0.5 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index decreased 1 percent compared with the previous week. The Refinance Index decreased 2 percent from the previous week and was 40 percent lower than the same week one year ago. The seasonally adjusted Purchase Index increased 2 percent from one week earlier. The unadjusted Purchase Index decreased 0.1 percent compared with the previous week and was 32 percent lower than the same week one year ago.

And as Paul Harvey used to say, here is the rest of the story.

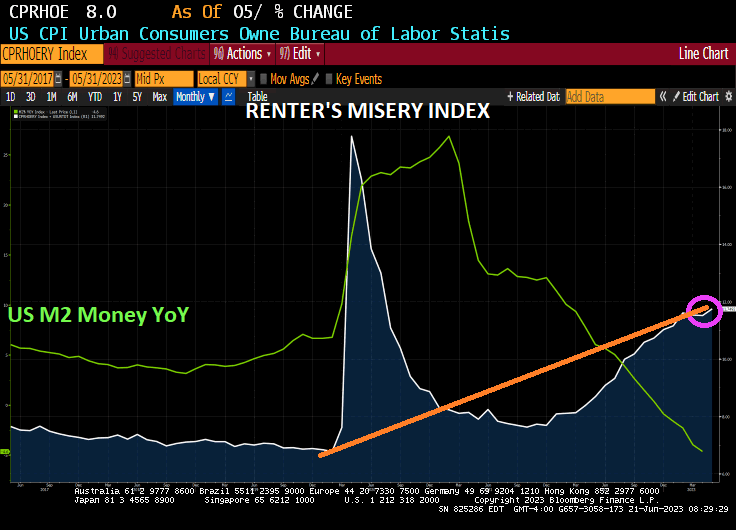

And the renter’s misery index, CPI for owner’s equivalent rent YoY + U-3 unemployment rate, is now a staggering 11.75% verus 6.78% in February 2020, the last month before the Chinese Wuhan virus led to economic and school shutdowns. And we have Donald Trump as President instead of this corrupt clown.

What is the difference between baseball legend Shoeless Joe Jackson and Clueless Joe Biden? While both sold out their teams for personal wealth, at least Shoeless Joe was good at baseball. Clueless Joe is a corrupt bully. Shoeless Joe was allegedly stupid, but so is Clueless Joe.

On the commodity side, Spot Silver is up 1.46%. Iron Ore is up 1.60%, but I don’t think my neighbors would appreciate me taking delivery on 10 tons of iron ore on my driveway! Heating oil is up 2.90%.

On the crypto side, bitcoin is up 20.84 (0.08%) with Ethereum up slightly more.

Bitcoin and silver doing well as the US Dollar loses ground since September 2022.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.