Inflatiion Joe Biden (or Unaffordable Joe). Bidenflation has led to The Federal Reserve tightening interest rates. As I said on Stuart Varney’s show years ago, “When The Fed starts raising rates, KABOOM!”

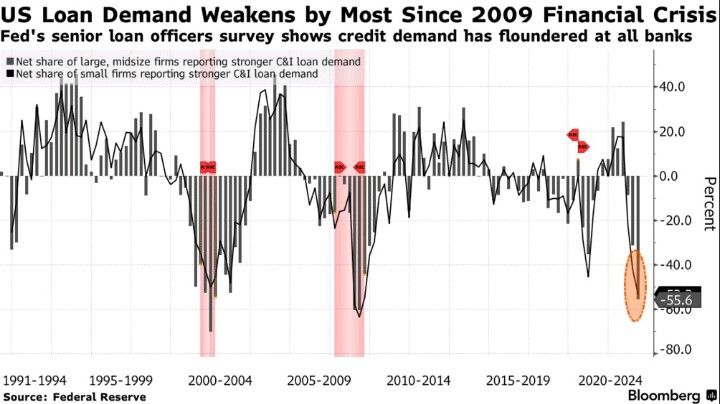

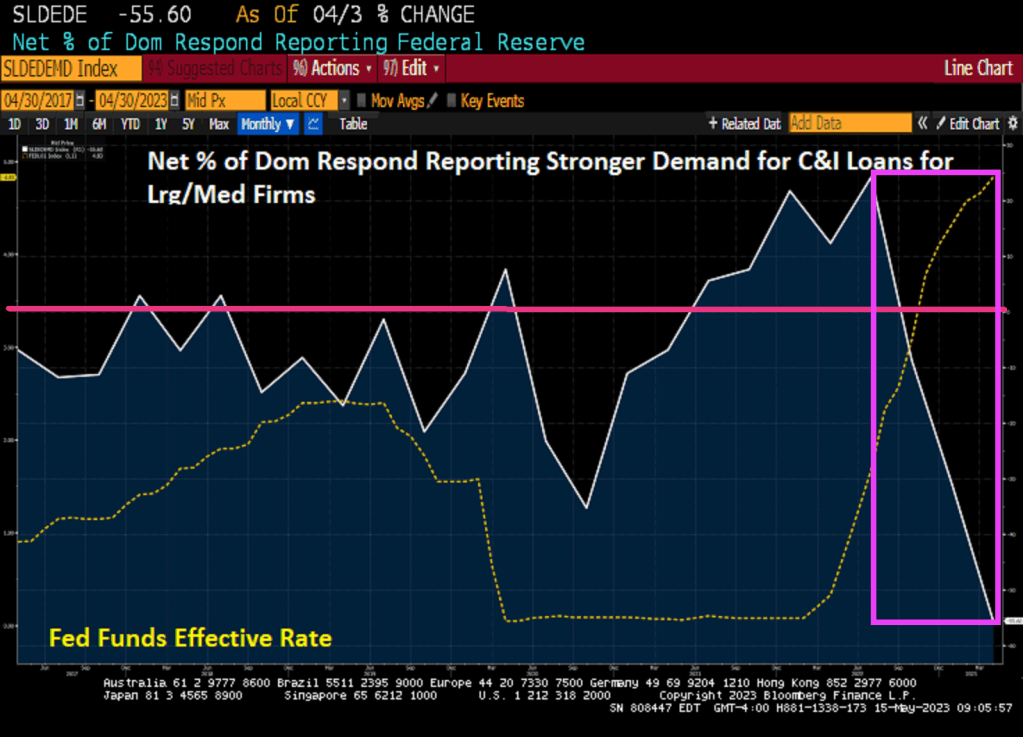

Now we are seeing US Loan Demand weakening by the most since the 2009 financial crisis.

Then we have large/medium sized banks reporting a crash in stronger demand for C&I loans.

I wish Biden would spend more time trying to negotiate with McCarthy to end the debt crisis rather than stir up race hatred like he did at Howard University graduation. C’mon Joe! White “supremacy” is not the most dangerous terrorist threat. I would actually say that Biden, Yellen and Schumer (throw in Pelosi’s spending splurge as Speaker) are the biggest terrorist threat. They are the 4 horsemen of the US debt apocalypse.

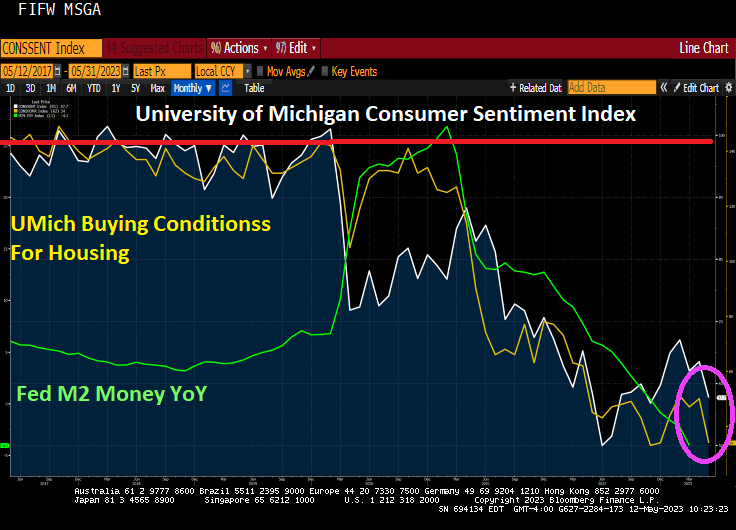

Let’s see how Bidenflation (caused by staggering Federal misspending) and years of Yellen’s TLTL (too low too long) monetary policy has caused a massive dislocation in the housing market.

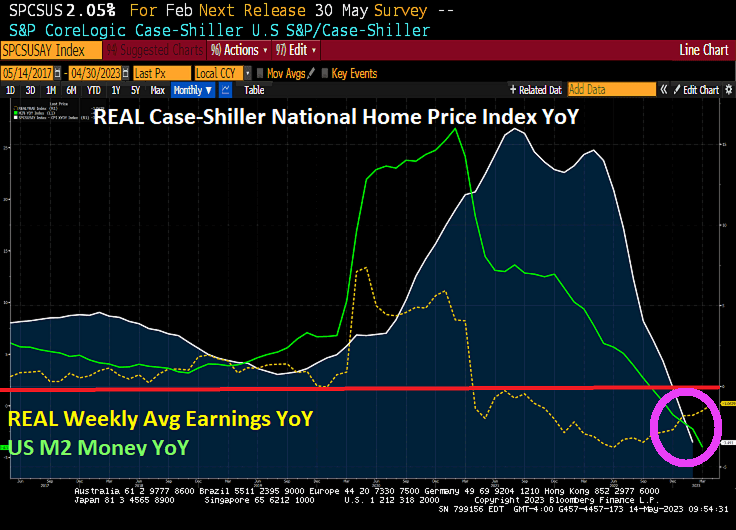

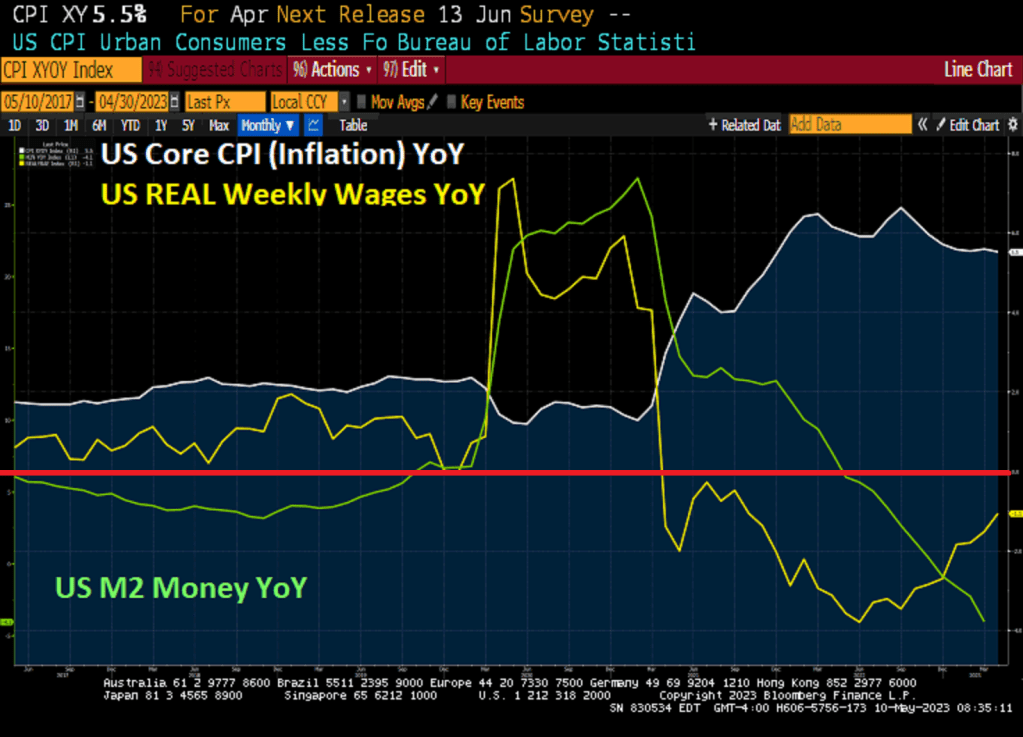

The February Case-Shiller National home price index less core inflation (CPI less food and energy) year-over-year is declining by -3.5%. This is happening as REAL average weekly earnings growth is at -1.06% YoY and has been negative growth for 25 straigth months.

Look at The Fed’s massive overreaction to the unnecessary government shutdowns of economies and schools. It really sent home price growth soaring, then when The Fed starts slowing the monetary stimulus, we get the largest slowdown of REAL home price growth since 2012.

The 4 Horsemen of the US Debt Apocalypse. I would add Mitch McConnell and Fed Chair Powell, but then would have an entire Cavalry company like George Armstrong Custer had at Little Big Horn.

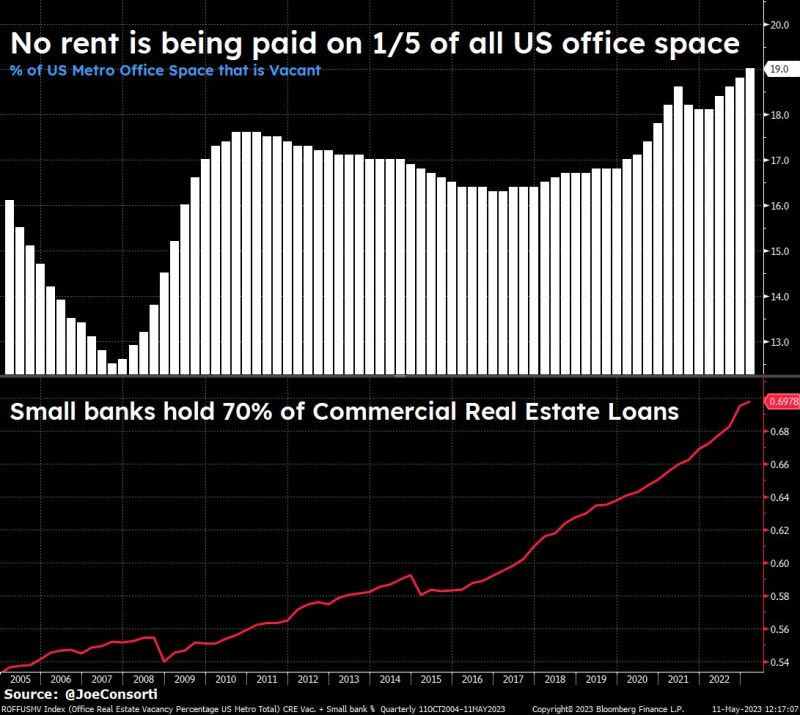

And the sad headline of the day (other than pure chaos on the Mexican border) is that NO RENT IS BEING PAID ON 20% OF ALL US OFFICE SPACE! And small banks hold 70% of commercial real estate loans!

Things are so bad, in fact, that 26 Empire State Buildings could fit into New York City’s empty office space, as occupancy in the city is hovering around 50% of prepandemic levels,

As The Fed momentarily pauses rate hikes, office vacancy rate just hit an all-time high. Another Biden first!! And the NCREIF office property index falling as The Fed tightens.

Face it, nothing has been the same since 1) the Covid economic shutdowns, 2) the massive spending spree by Congress, the massive expansion of monetary stimulus by The Federal Reserve and 3) the election of Unaffordable Joe Biden,

The latest University of Michigan consumer survey is out and it is ugly, reflecting Biden’s ugly approval ratings. A sentiment value of 100 is a good baseline and US consumers were about at 100. Then Covid struck and the ensuing economic and school shutdowns (thank a lot Randi Weingarten, President of the American Federation of Teachers). Then we have the selection of Joe Biden as President, the WORST President in history.

Housing sentiment? It is now near the lowest level since 1982.

Here is Parks and Recreation’s Leslie Knope, one of the only political non-donor class that still likes unaffordable Joe. But big Democrat donors LOVE Biden doling out billions to them!

Treasury Secretary Janet “The Evil Hobbit” Yellen is a Statist. She can only think of an all powerful central government calling the shots since the private sector and individual liberties are something to be eliminated.

Yellen has mostly declined to spell out what her department would do if Congress fails to raise or suspend the debt limit before the Treasury finds itself unable to cover all the government’s obligations.

Back in Mordor on The Potomac, President Joe Biden and House Speaker Kevin McCarthy postponed a meeting on the debt ceiling set for Friday. People familiar with the talks said the postponement was a sign that staff-level talks were yielding progress.

Biden and congressional Republicans have been locked in disagreement for weeks over raising the US federal government’s $31.4 trillion borrowing limit. GOP leaders have demanded promises of future spending cuts before they approve a higher ceiling. Biden has jinsisted on a “clean” increase, with budget talks kept separate.

Now what no one in our lame pro-government media or Congress or Administration has said is the a US debt default does NOT necessarily mean that the US walks away from its debt. Very likely, China and Japan, our two biggest foreign debt holders, will insist on debt restructuring so that the US pays some fraction of debt owed, like 80%.

But foreign debt holders are a relatively small percentage of US debt holders. The Federal Reserve is the largest single borrower, thanks in part to Yellen who has formally Federal Reserve Chair,

Of course, financial entities like Vanguard, Blackrock and Fidelity are the largest holders of US debt. Since pensions invest heavily with these enetitites, the Federal government would restructure the debt rather than outright default.

US CDS 1Y continues to remain high as Biden/Yellen/Schumer play chicken with the lives of the American middle class while the political donor class is clamoring for endless spending and wealth transfers.

Remember, Biden, Yellen and Schumer all Statists and believe that their job is growing Federal government to wear it is all powerful and their donors get billions in subsidies and wealth transfers. You don’t think green energy subsidies make any common sense, do you? Wind turbines (aka, whale and eagle killing machines) are ineffective. We need nuclear power but Progressives fear nuclear power as much as they have Donald Trump.

Bankrate’s 30-year mortgage rate is down slighty to 6.89%, but that masks the reality that mortgage rates were only 2.88% when Biden was sworn in as President. That is a staggering increase of 140 in the 30-year mortgage rate.

In fairness to Unaffordable Joe, Congress went on a crazy spending spree with Covid, much of which had nothing to do with Covid. Green energy spending for the donor class is helping drive core inflation up 291% since Biden was installed as President.

And yes, The Fed is playing catch up for former Fed Chair Janet Yellen’s “Too low for too long (TLTL) monetary policy. So, now she is creating mayhem as US Treasury Secretary. And she was a terrible Fed Chair, now a terrible Treasury Secretary.

And yes, The Fed looks like they are pausing rate hikes.

Another dismal economic report under “Middle class” Joe Biden.

April’s inflation report is out and … it sucks. Core inflation (CPI less food and energy) remains elevated at 5.5% YoY, much higher than The Fed’s target rate of 2%. Even worse, US REAL average weekly wage growth is negative again at -1.1% YoY, negative growth for the 25th straight month.

Turns out that core inflation is higher than overall inflation. 4.9% YoY compared to core of 5.5% YoY.

Despite the hot core inflation report, Fed Funds Futures are pointing to declining rates over time.

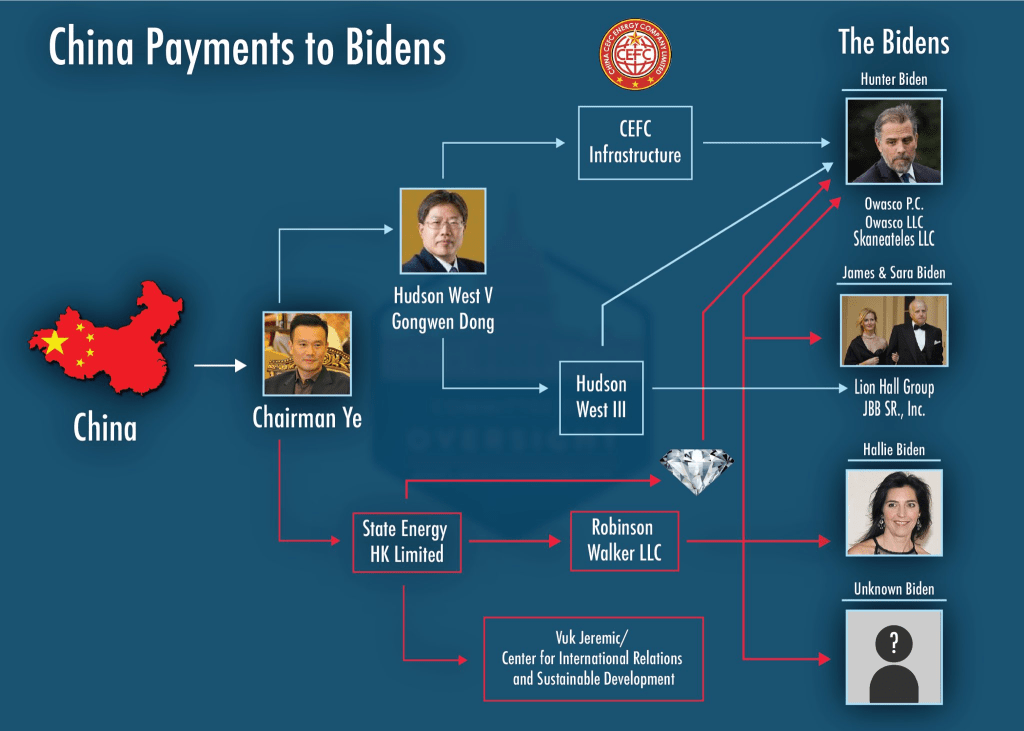

While the US middle class is getting screwed, The Biden family are raking in millions …. from China.

Resident Biden has been an unmitigated disaster for the US middle class, but fantastic for BIG corporate America and the donor class.

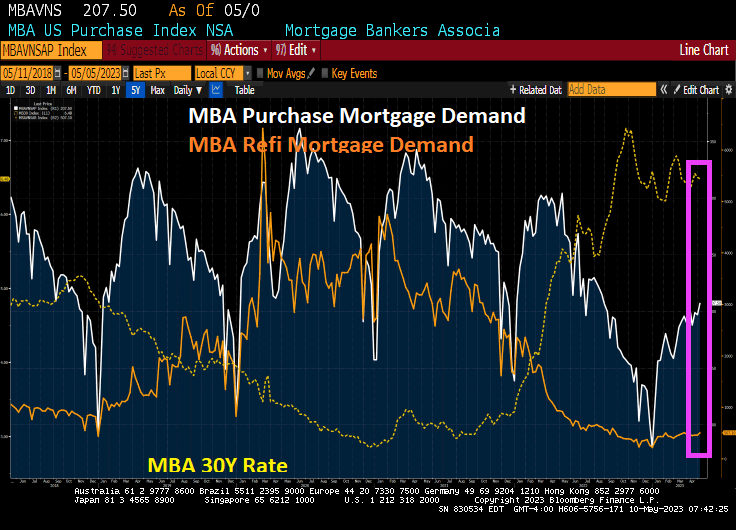

Mortgage applications increased 6.3 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending May 5, 2023.

The Market Composite Index, a measure of mortgage loan application volume, increased 6.3 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index increased 7 percent compared with the previous week. The Refinance Index increased 10 percent from the previous week and was 44 percent lower than the same week one year ago. The seasonally adjusted Purchase Index increased 5 percent from one week earlier. The unadjusted Purchase Index increased 5.3 percent compared with the previous week and was 32 percent lower than the same week one year ago.

Here is the data.

Middle class Joe as he likes to call himself is actually BIG CORPORATE Joe. A friend of big donor and BIG pharmam, BIG banks, BIG tech, BIG defense contractors, BIG media. No wonder Hunter Biden refers to Joe as “The BIG guy!”

Biden’s approval ratings are terrible. Okay, Biden is the worst President in history, weak, can’t speak coherently and is letting chaos reign on the southern border. But from a consumer standpoint, he and crazy spending Congress have helped make America simply unaffordable for miillions.

Once again, Biden’s obsession with foolish green energy, Congress using Covid to spend trillions, then the green energy subsidy Act (aka, Inflation Reduction Act) where Biden and Congress agreed to make massive payoffs to big donors (the donor class). All this resulted in 40 year highs in inflation leading The Federal Reserve to raise interest rates to combat inflation.

For autos, the interest rate on an auto purchase has soared to it highest level since 2008. And car prices at up 19% under Biden’s Reign of Error.

And when we consider that US Real Average Weekly Earnings growth continues to be negative under Unaffordable Joe.

Housing? At least home price growth is slowing and even negative in some cities. But housing is still unaffordable for millions of Americans.

The housing situation will only get worse as Title 42 expires and millions of illegal immigrants invade the US. Texas Governor Abbot should ship all of them to Wilmington Delaware, home of Unaffordable Joe Biden. Let him suffer for once from his own folly.

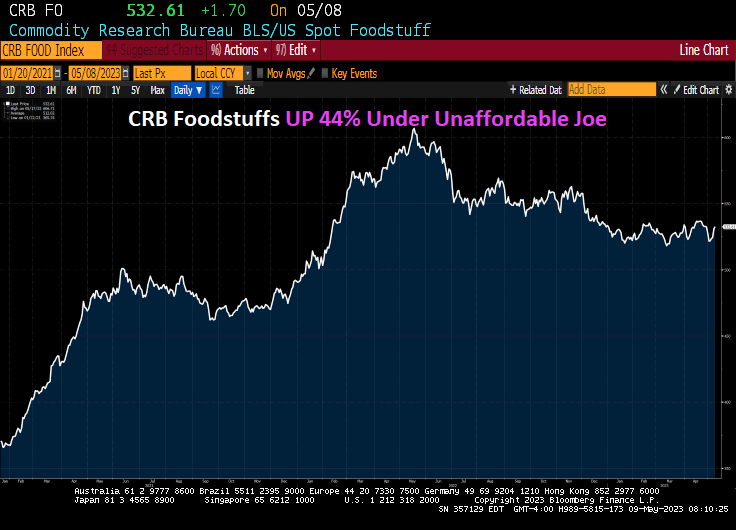

Food? Don’t get me started. The Commodity Research Bureau is up 44% under Unaffordable Joe.

Okay, Biden is a useful idiot for BIG banks, BIG Pharma, BIG tech, BIG defense, and BIG government. He is popular with the 1% and people who watch “The View.” But many of the 99% are suffering under Unafforable Joe.

California just did what Slow Joe Biden and Senate Majority Leader Chuckles Schumer are threatening to do. Biden and Schumer still refuse to negotiate (allegedly) sending the US Federal government careening towards a staggering debt default. The source of both California and US Federal government fiscal problems? Out of control government spending, aka, government gone wild!

In any case, California borrowed approximately $20 billion from the federal government to cover unemployment benefits during the pandemic, and with Gov. Gavin Newsom’s recent decision to not pay it back, employers are now saddled with the expense, according to experts.

“The state should have taken care of the loans with the COVID money it received from the government in 2021,” Marc Joffe, policy analyst at the Cato Institute—a public policy think tank headquartered in Washington, D.C.—told The Epoch Times.

In the proposed 2023–2024 budget, $750 million was allocated to start paying down the loans, but Newsom made changes to the plan in January and withdrew the funding.

The Epoch Times’ request for comment from Newsom’s office was not returned on deadline.

The decision leaves businesses in the state responsible for the loans—as mandated by federal regulations—so the federal unemployment tax rate of .6 percent is set to increase by .3 percent annually, starting in 2023, until the loan is extinguished.

“California is just not really an employer-friendly state,” Joffe said. “This one thing will not be a difference between a business remaining open or closing, but it’s just another burden on top of the many burdens the state puts on employers.”

Twenty-two states borrowed money for unemployment insurance from the federal government during the pandemic, with all but four—California, Colorado, Connecticut, and New York—paying back their debts.

California owes the most, by far, with approximately $18.6 billion outstanding as of May 2, followed by New York’s $8 billion, Connecticut’s $187 million, and Colorado’s $77 million, according to U.S. Treasury Department data.

The discrepancy in amounts borrowed and owed by states lies in the different approaches to managing the pandemic, with California’s stricter lockdown causing unemployment to remain higher and longer, according to experts

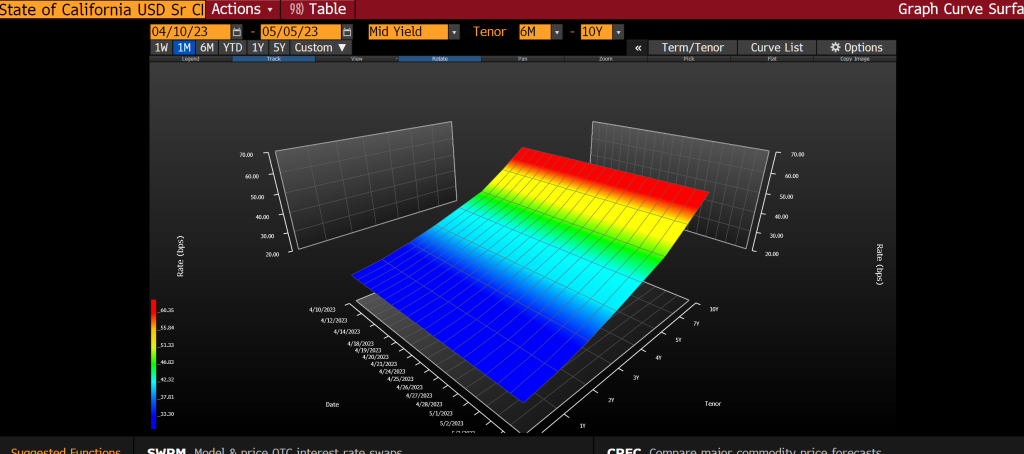

And CA CDS 1Y is tame (only 31), the CDS curve over a longer time frame looks miserable.

Now, Gruesome Newsom only default on Covid-related loans. The California municipal bond market is huge and CA has defaulted on those loans …. yet.

Speaking of insane fiscal “management,” a repartations plan in California could cost billions.

California’s reparations task force, which first convened nearly two years ago, has given the final approval to a list of recommendations on how the state may compensate and apologize to Black residents for historical discrimination. “Reparations are not only morally justifiable, but they have the potential to address long standing racial disparities and inequalities,” Representative Barbara Lee (D-CA) said during a weekend meeting. The proposals now go to state lawmakers to consider reparations legislation and a final sum, which some economists could cost the state upwards of $800B, or almost 3x the state’s annual budget.

To be initially eligible, applicants must be a descendant of Black people who were in the country by the end of the 19th century, thouqh there are not yet details on how the payments would be funded. Age, state residence, and other factors will also play a role in determining compensation.

There is the rub – how does California finance the reparations? Raise taxes (unfair to people who never did anything wrong to blacks)? Borrow billions? Given that Newsom just defaulted on loans to California might mean that there will be relucatance to lend CA billions more.

CA Governor Gavin “Slick” Newsom. The Defaulter In Chief of California.

You must be logged in to post a comment.