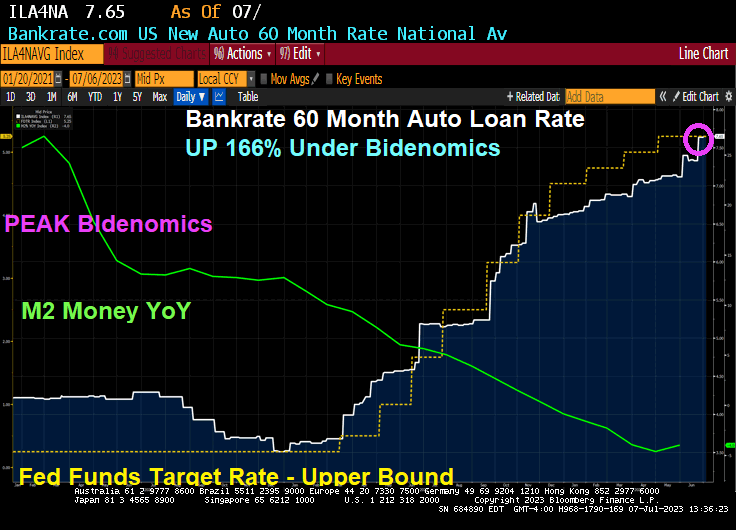

Auto loan rates are now up to 7.65%, a gut-wrenching 166% increase under Bidenomics.

Average monthly payments also reached a new record of $733. That compares with $730 in the first quarter and $678 in the second quarter of 2022. Buyers were financed with an average APR of around 7.1%, the highest since the fourth quarter of 2007.

2 out of every 3 consumers who agreed to a $1,000+ monthly payment in Q2 signed up for an average APR between 8.5% and 9.6%. (via Edmunds).

As for buyers who took on $1,000 monthly auto payments, about 65% of them had an average loan-term range of 67 months and 84 months, their average APR rate was between 8.5% and 9.6%.

Bidenomics. Crushing the soul of America’s middle class and low wage workers.

I love how the most secure building in Washington DC with cameras 24/7 EVERYWHERE and the Secret Service claims they don’t know who left the cocaine on a table. I will bet they pin the blame on VP Kamala Harris as an excuse to replace her word salads for the 2024 Presidential election.

Bidenomics, the massive Federal spending spree that helped drive inflation to 40 year highs, is the most top-down Soviet-style command economy model imaginable.

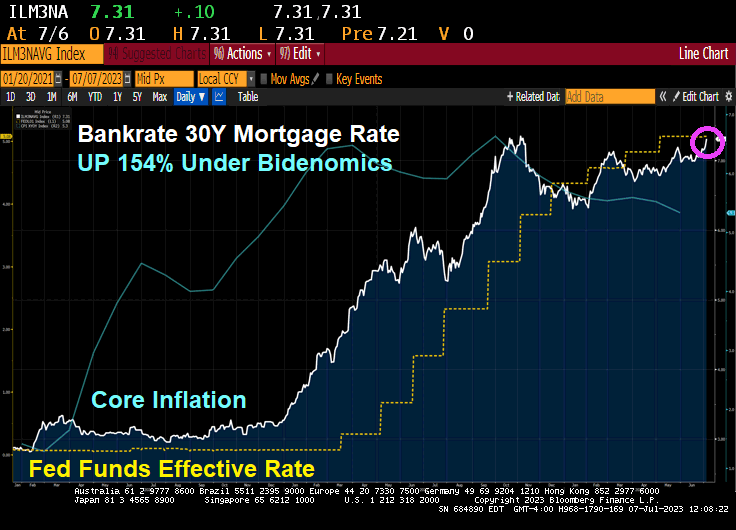

As The Fed battles Bidenflation, the 30-year mortgage rate has now risen to 7.31%, a far cry from 2.88% when Biden was installed as President. That is a 154% increase in the 30-year mortgage rate under Bidenomics.

Biden’s massive spending spree (aka, Build Back Better) has a new name: Build Back Bankrupt!

According to Epiq, Commercial Chapter 11 Filings Increased 68 Percent in the First Half of 2023.

NEW YORK – July 03, 2023— The 2,973 total commercial Chapter 11 bankruptcies filed during the first six months of 2023 represented a 68 percent increase over the 1,766 filed during the same period in 2022, according to data provided by Epiq Bankruptcy, the leading provider of U.S. bankruptcy filing data. Individual Chapter 13 filings increased by 23 percent during the same period.

Overall commercial filings registered 12,107 for the first half of 2023, representing an 18 percent increase from the commercial filing total of 10,258 for the first half of 2022. Small business filings, captured as Subchapter V elections within Chapter 11, totaled 814 in the first six months of 2023, a 55 percent increase from the 525 elections during the same period in 2022.

Overall commercial filings increased 12 percent in June 2023, as the 2,123 filings were up from the 1,891 commercial filings registered in June 2022. The 404 commercial Chapter 11 filings in June represented a 9 percent increase from the 371 filings in June 2022. Total Subchapter V elections within Chapter 11, experienced a 111 percent increase from 94 in June 2022 to 198 in June 2023.

“The increase in commercial and individual bankruptcy filings during the first half of 2023 underscores the economic challenges faced by businesses and individuals,” said Gregg Morin, Vice President of Business Development and Revenue at Epiq Bankruptcy. “Our objective is to provide bankruptcy professionals with timely and accurate data necessary for analyzing stakeholder volumes and trends for making informed business decisions.”

Total bankruptcy filings were 217,420 during the first six months of 2023, a 17 percent increase from the 185,352 total filings during the same period a year ago. Total individual filings also registered a 17 percent increase, as the 205,313 filings during the first half of 2023 were up from the 175,094 filings during the first six months of 2022. The 85,390 individual Chapter 13 filings in the first half of 2023 represent a 23 percent increase over the 69,367 filings during the same period in 2022.

All chapters increased in June 2023 compared to June 2022, with 37,700 total bankruptcy filings representing an increase of 17 percent from the 32,198 filed in 2022. Total commercial filings were up 12 percent from 1,891. Total Individuals were up 18 percent from 30,307.

While not the Epiq data, the Bloomberg Corp Bankruptcy Index shows the rise in bankruptcies as The Fed fights Bidenflation.

The good news (if true)? ADP announced that 497k jobs were added in June.

The bad news? A 497k print on jobs (many seasonal, it is summer!) almost guarantees that The FOMC (Fed Open Market Committe) will raises rates again at at the July meeting.

The 2-year Treasury yield is up over 10 basis points.

The 2-year Treasury yield is up 16.5 basis points.

Bticoin Cash is up 10% today.

I should have bought nickel!

Why is Biden sending Treasury Secretary Janet “The Marxist Midget” Yellen to China? A Treasury Secretary and former Federal Reserve Chair? Likely trying to convince China that our $32 TRILLLION AND GROWING national debt is not a problem, since China is the third largest holder of US Treasury debt (after The Fed and Japan). Note that China has decreased its holdings of US Treasuries by -25.6% since January 2018.

Hopefully, Yellen isn’t acting as a bag man for The Biden Crime Family. 10% for The Big Guy?? How much does Yellen get??

Joe Biden, or “Blow Biden” after the cocaine was discovered in the White House the other day, owns the abysmal mortgage and housing market thanks to The Fed fighting inflation caused by Bidenomics (massive Federal spending and massive Fed stimulus).

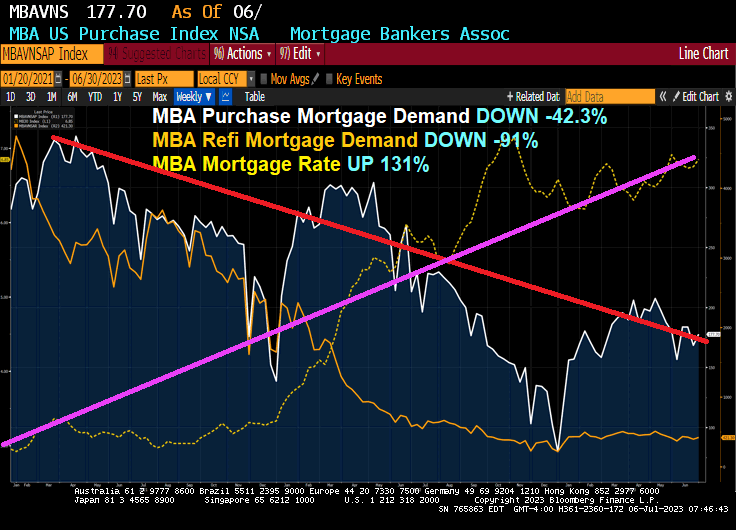

Mortgage applications decreased 4.4 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending June 30, 2023. Last week’s results included an adjustment for the Juneteenth holiday.

The Market Composite Index, a measure of mortgage loan application volume, decreased 4.4 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index increased 6 percent compared with the previous week. The Refinance Index decreased 4 percent from the previous week and was 30 percent lower than the same week one year ago. The seasonally adjusted Purchase Index decreased 5 percent from one week earlier. The unadjusted Purchase Index increased 6 percent compared with the previous week and was 22 percent lower than the same week one year ago.

Here is the rest on the story:

As liquidity dries up under Bidenomics. Or Yellenomics. Take your pick!

Seriously, can The Biden Administration get any more embarrassing? Or dangerous to American civil liberties?

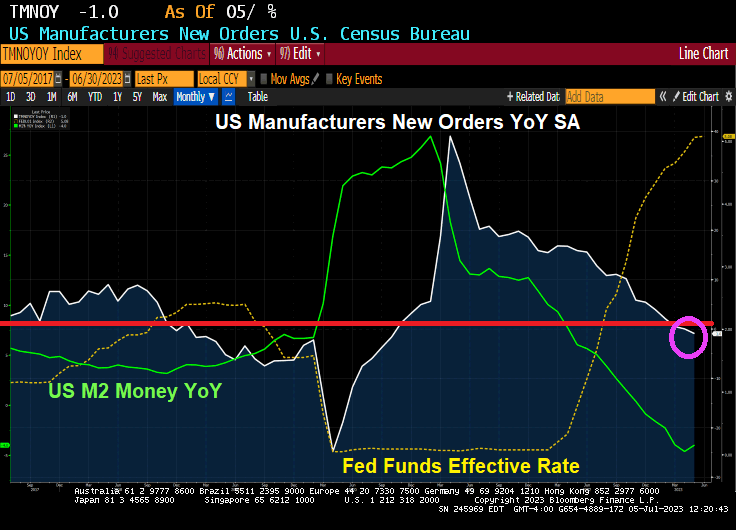

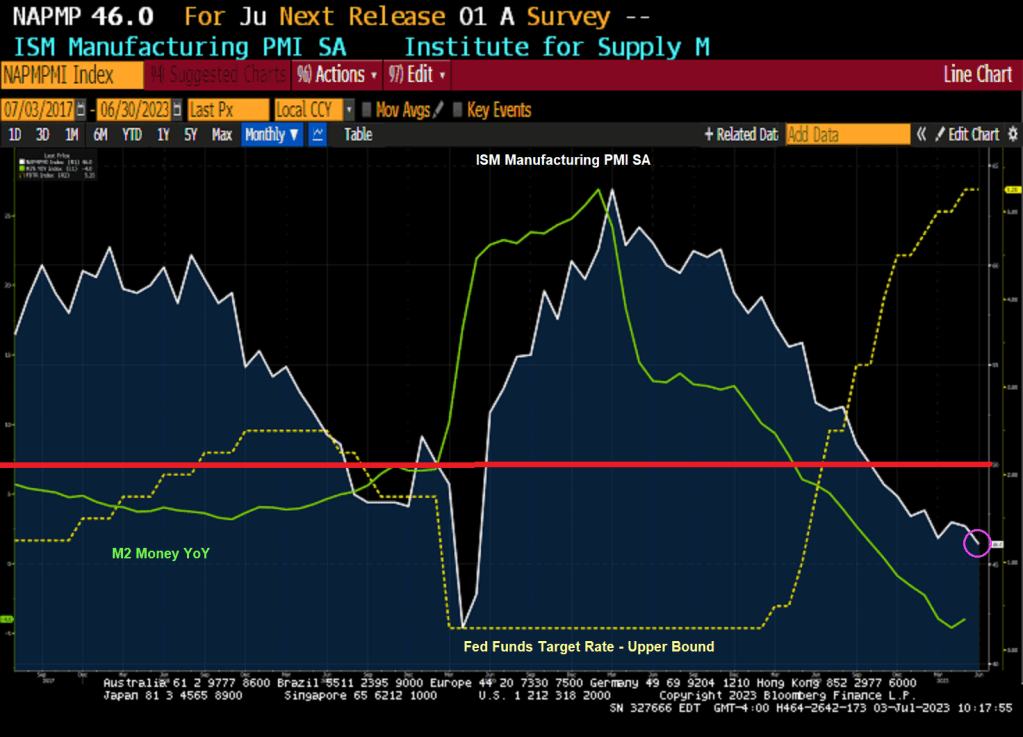

As Powell and The Gang raise interest rates, the more the economy is … slip slidin’ away. US Manufacturers New Orders YoY in May declined -1.0% for the first time since Covid.

The Federal Home Loan Bank system (aka, FLUBs), a relic of FDR and The Great Depression, subsidizes banks, not individuals. Much like its twin sibling, The Federal Reserve system, it is a Socialist institution that rely of manipulation rather than free markets.

The first sign of deep trouble in US banking this year came from a sunbaked office complex in a San Diego suburb. There, a small firm called Silvergate Capital Corp. assured investors it was weathering a run on deposits. Its lifeline: about $4.3 billion from a Federal Home Loan Bank.

Heads turned across the financial industry.

Silvergate didn’t have a network of branches serving consumers, and it barely offered mortgages. It specialized in moving dollars for cryptocurrency ventures.

Soon it became apparent that a roster of troubled regional banks was leaning on FHLBs — a relic of the Great Depression originally aimed at ensuring financial firms have cash to lend to homebuyers. Yet the banks had little to do with everyday mortgage lending.

Silicon Valley Bank, catering to venture capitalists and tech startups, said it held $15 billion from an FHLB at the end of 2022. Signature Bank, with clients including crypto platforms, had $11 billion. And by April, First Republic Bank, offering mortgages to millionaires on unusually sweet terms, ended up with more than $28 billion. All four banks collapsed.

For many, that was a crystallizing moment for the 90-year-old Federal Home Loan Bank system, which has ballooned to more than $1.5 trillion while playing a growing role as a backstop for banks taking all kinds of risks — and a diminishing role in funding new mortgages. That’s raising questions about the purpose of FHLBs and why the private institutions enjoy so much government support.

As Milton Friedman once said, “Nothing is so permanent as a temporary government program.”

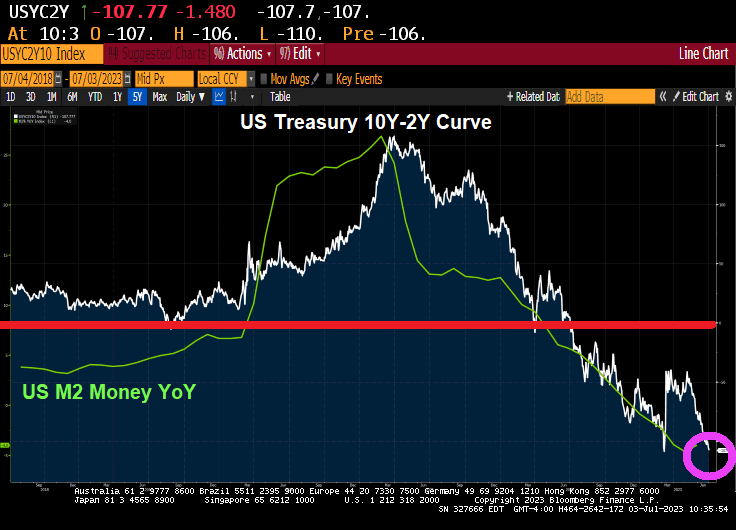

Of course, rate increases are crushing regional banks as well as the middle class. But as M2 Money growth crashes, home price growth is slowing into negative territory.

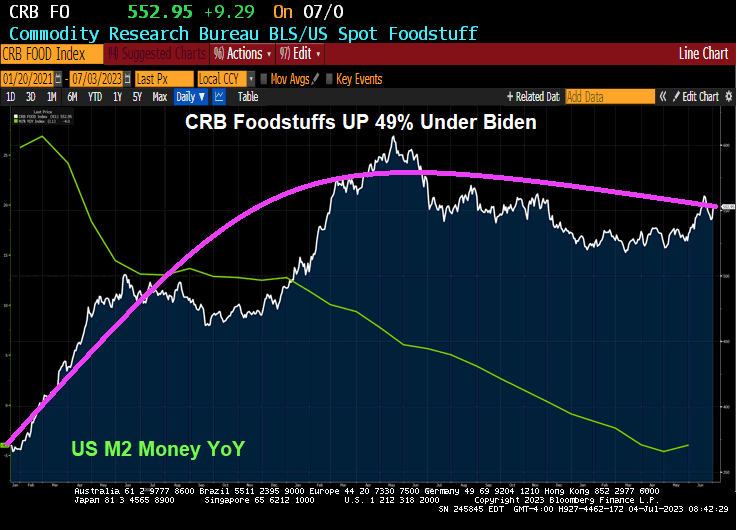

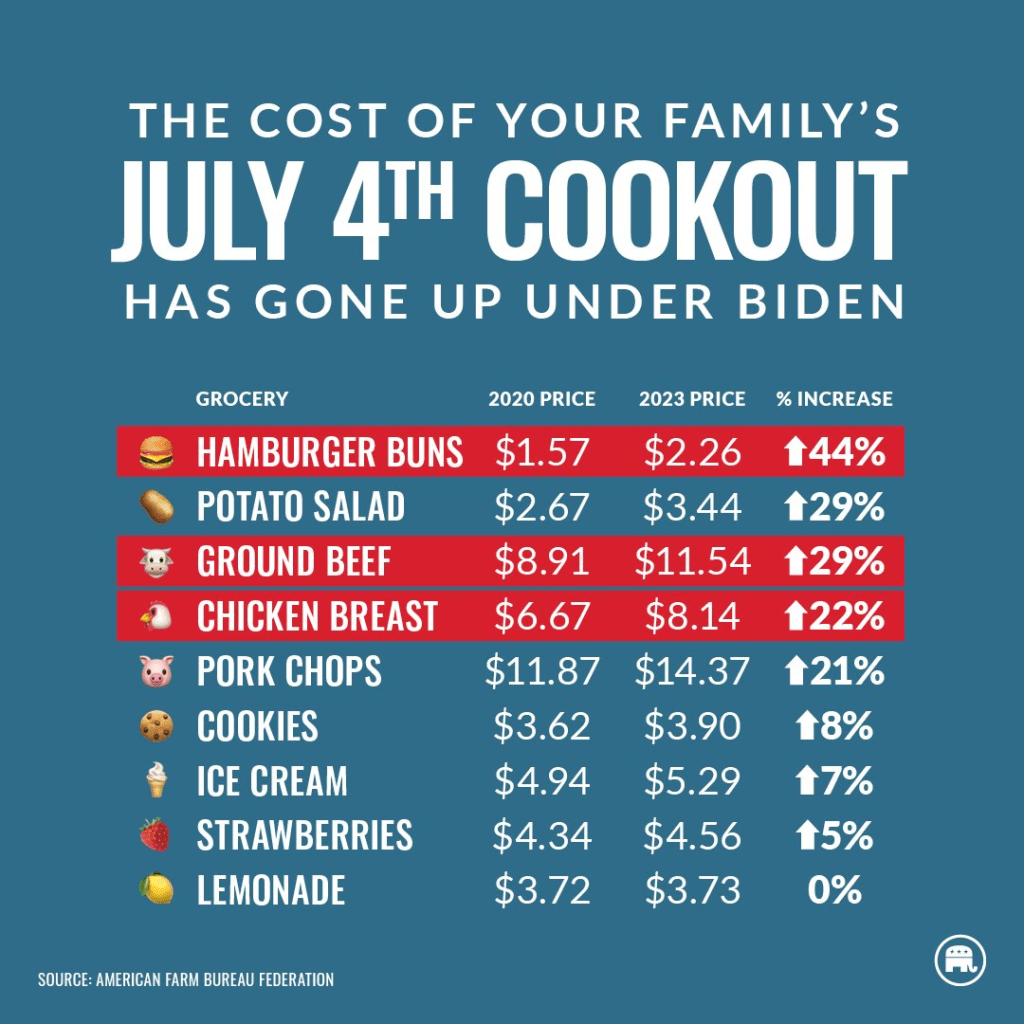

Happy 4th of July! Enjoy those burgers and hot dogs, at least until you consider that food prices have risen a staggering 49% under Biden’s Reign of Economic Error.

The only good news is that The Fed’s monetary stimulus growth is slowing. But don’t worry! Biden and Congress will keep introduce massive spending bills to avert a recession. Which will cause downline inflation.

I was hoping that the week of July 4th would start off with fireworks, but we got bad news about the economy.

US factory activity contracted for an eighth month in June, slipping to the weakest level in more than three years as production, employment and input prices retreated.

The Institute for Supply Management’s manufacturing gauge fell to 46, the weakest since May 2020, from 46.9 a month earlier, according to data released Monday. The current stretch of readings below 50, which indicates shrinking activity, is the longest since 2008-2009.

The decline in the ISM production gauge, which also stands at the lowest level since May 2020, suggests demand for merchandise remains weak. The index of new orders contracted for the 10th straight month and order backlogs shrank, which may help explain a pullback in a measure of manufacturing employment.

The ISM gauge retreated to a three-month low and, at 48.1, indicates fewer producers adding to payrolls.

Many Americans continue to limit their spending on merchandise as they rotate to services and experiences. Others are simply tightening their belts as still-high inflation takes a toll on their incomes.

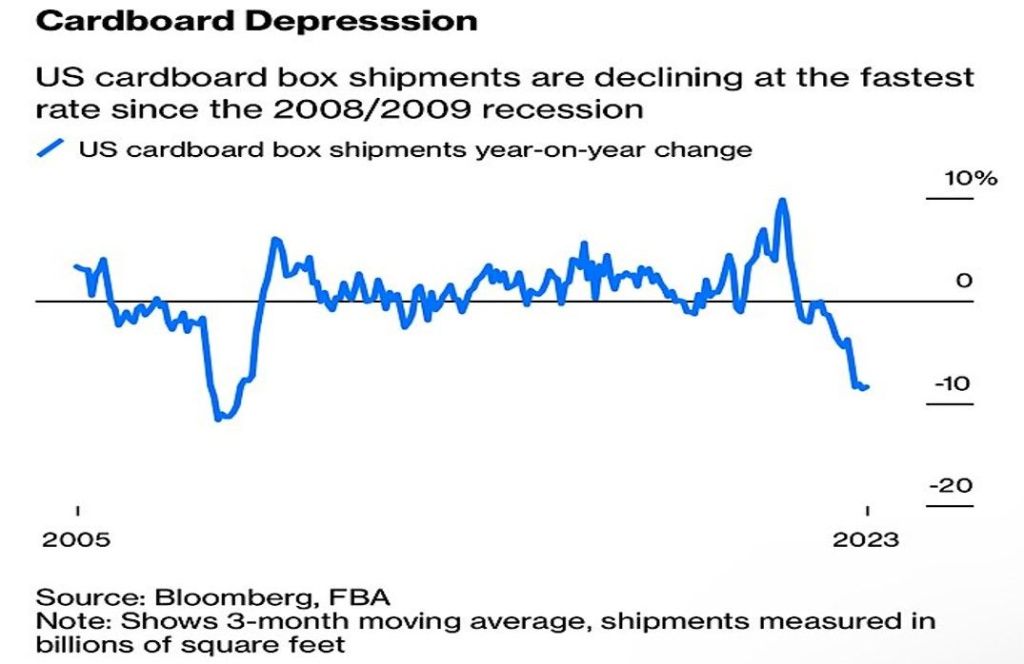

And then we have cardboard box shipments declining at fastest rate since 2008/2009.

At least Ethereum is up over 2% this morning.

And the US Treasury 10Y-2Y keeps on diving deeper into inversion.

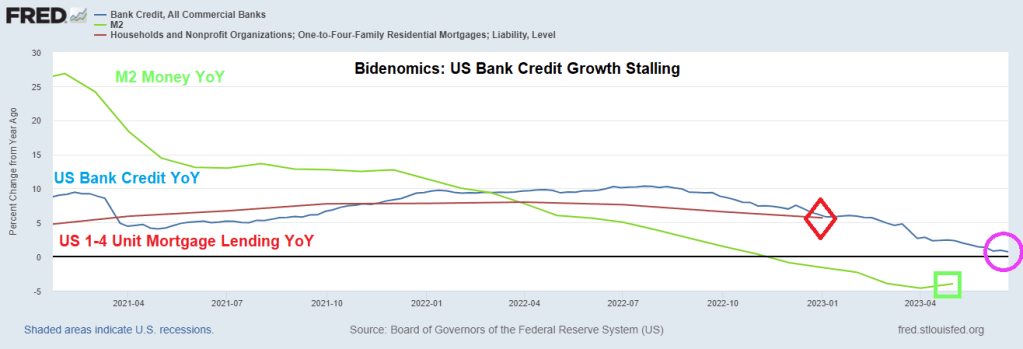

Bidenomics is based on massive Federal spending and massive Fed monetary stimulus. But like all stimulus, it wears off. Such is the case with bank lending as The Fed raises interest rates.

US bank credit year-over-year (YoY) has stalled to a lowly 0.7% rate as M2 Money growth YoY increases slightly to -4%.

Its figures. With the Socialist Federal Reserve manipulating interest rates and Biden/Congress spending like drunken sailors trying to manipuate economic growth, it makes sense that Biden wants to explore Bill Gate’s idiotic idea of blotting out the sun to prevent global warming.

Of course, Biden can hide at any of his 4 mansions and wear his Ray-ban Aviators to avoid the horror of his policies.

You must be logged in to post a comment.