As Connor MacLeod said in the film Highlander, “There can only be one!” The US banking system under Joe Biden’s Reign of Error is like the film Highlander: apparently, there can only be one bank. And it is likely JP Morgan Chase.

Take the JP Morgan Chase (JPMC) acquisition of First Republic Bank:

In Acquiring First Republic Bank, JP Morgan Has:

- Bypassed laws against acquiring bank while controlling 10%+ of US deposits

- Shared $13 billion in losses with the FDIC

- Received a $50 billion loan from the FDIC

- Effectively bought back its own deposits

- Expects to profit $5 billion+ over the next 5 years

This crisis has taught us that rules don’t matter in times of panic, particularly to regulators.

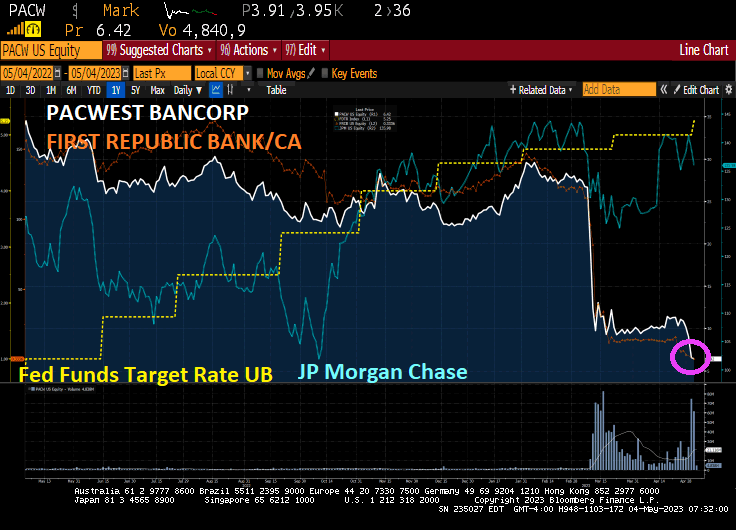

And now we have PacWest Bancorp. Lender says it’s been approached by potential investors. Bill Ackman warns US regional banking system at risk.

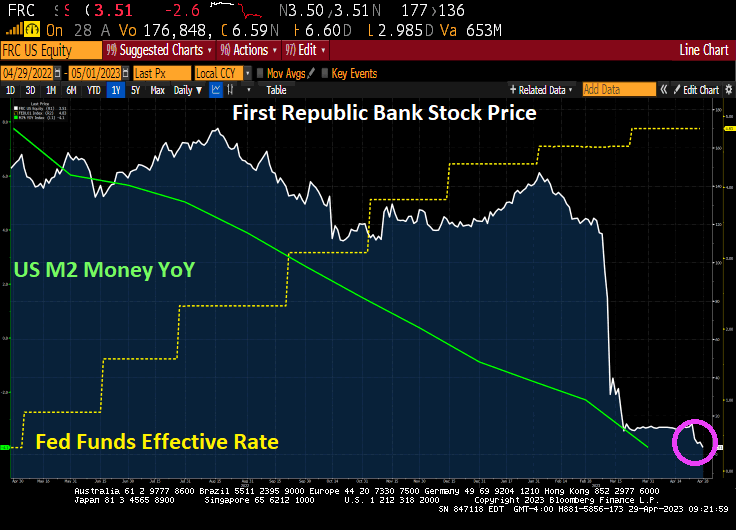

The turmoil at PacWest shows how investor angst still remains elevated after a string of failures and deposit outflows in the sector despite Federal Reserve Chair Jerome Powell’s assurance Wednesday that authorities were closer to containing the crisis. It’s reignited the debate over whether more US regional lenders will fall after this year’s collapse of SVB Financial Group’s Silicon Valley Bank, Silvergate Capital Corp., Signature Bank and most recently First Republic Bank.

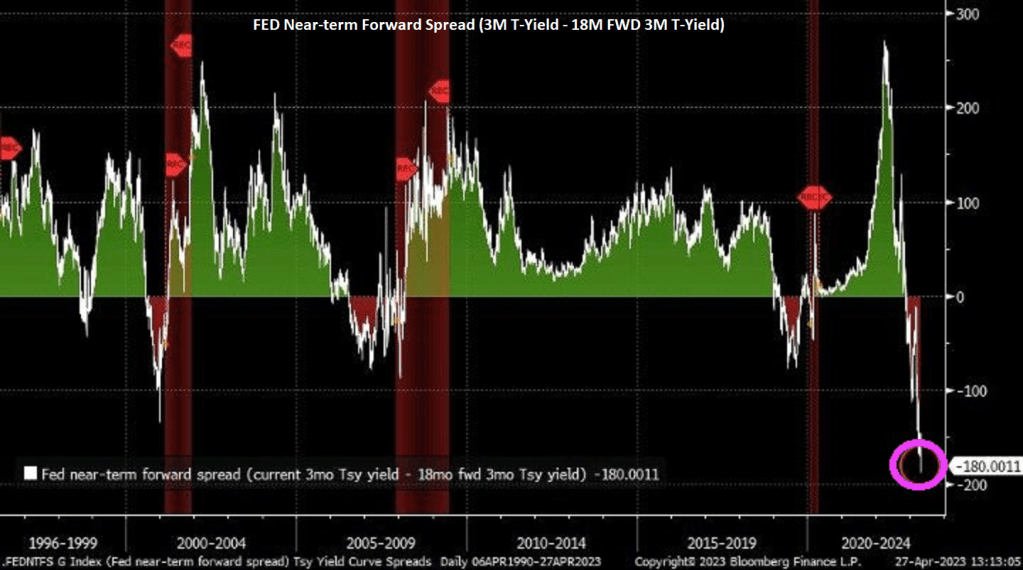

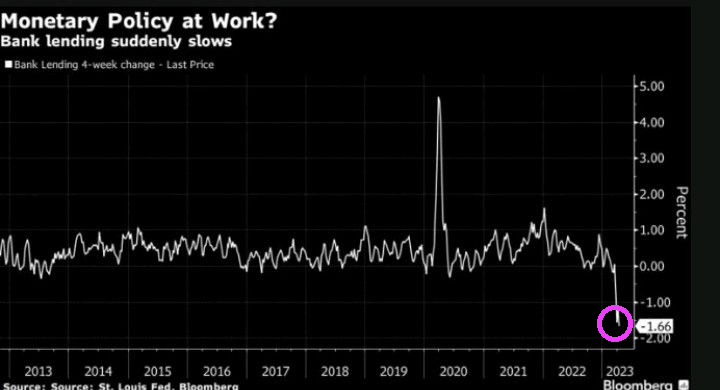

Smaller banks are under pressure after a year of interest-rate hikes hammered the value of their bond holdings and drove unrealized losses to an estimated $1.84 trillion. Trouble in commercial real estate is adding to the pain, while depositors take their money out to seek better returns elsewhere. These stresses have put the spotlight on these lenders, which typically have fewer resources to defend themselves.

We are seeing a consolidation of the banking system .. again as smaller and regional banks fail and get gobbled up by the Too-Big-To-Fail (TBTF) banks like … JP Morgan Chase.

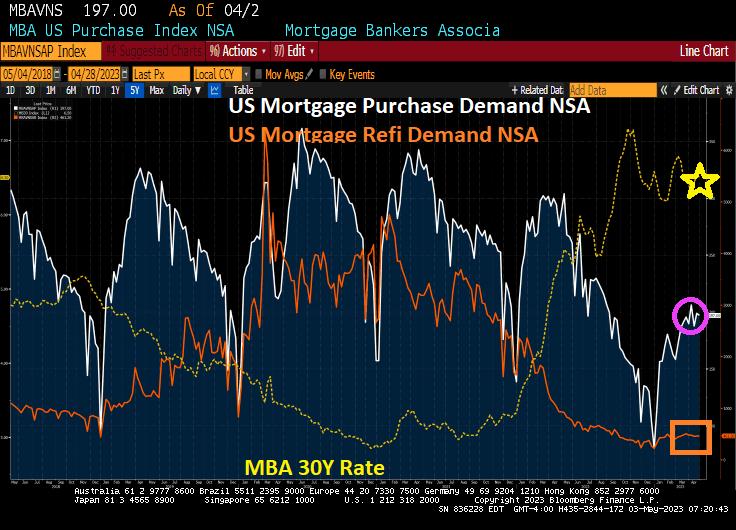

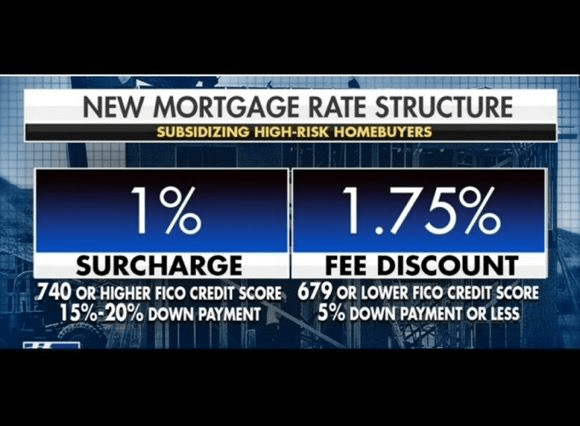

Biden’s Reign of Error is not over yet. His campaign slogan (which was also Bill Clinton’s campaign reelection slogan) is “Finish the job!” With Biden’s idiotic mortgage idea of punishing borrowers with good credit and giving subsidies to those with bad credit, Biden is trying to finish off the US economy and banking system.

We are in for more hell.

You must be logged in to post a comment.