Under Bidenomics, with its high inflation rate and crushing negative wage growth, consumers are draining their savings and living on a prayer …. and consumer credit to cope.

What is worriesome in the transition rates (like current to 90-days delinquent) Credit cards (blue) and auto loans (red).

A closer look at credit card delinquency rates on a year-over-year (YoY) basis, showing the fastest growth in delinquencies since the Covid economic lockdowns.

Then we have commercial real estate delinquencies are now the highest the have been since 2013.

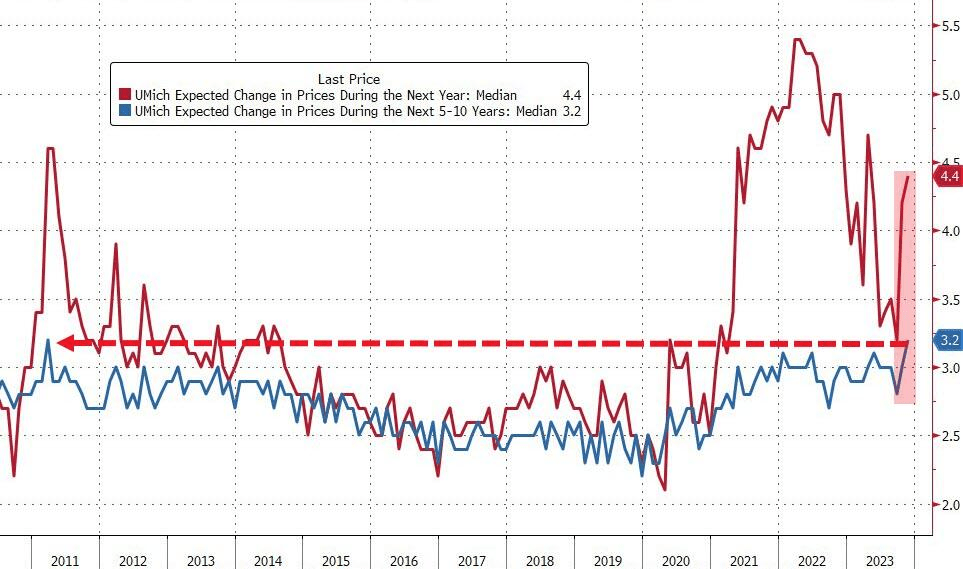

Meanwhile, University of Michigan consumer sentiment about inflation spiked to 4.4%. That is the highest medium-term inflation expectation since 2011.

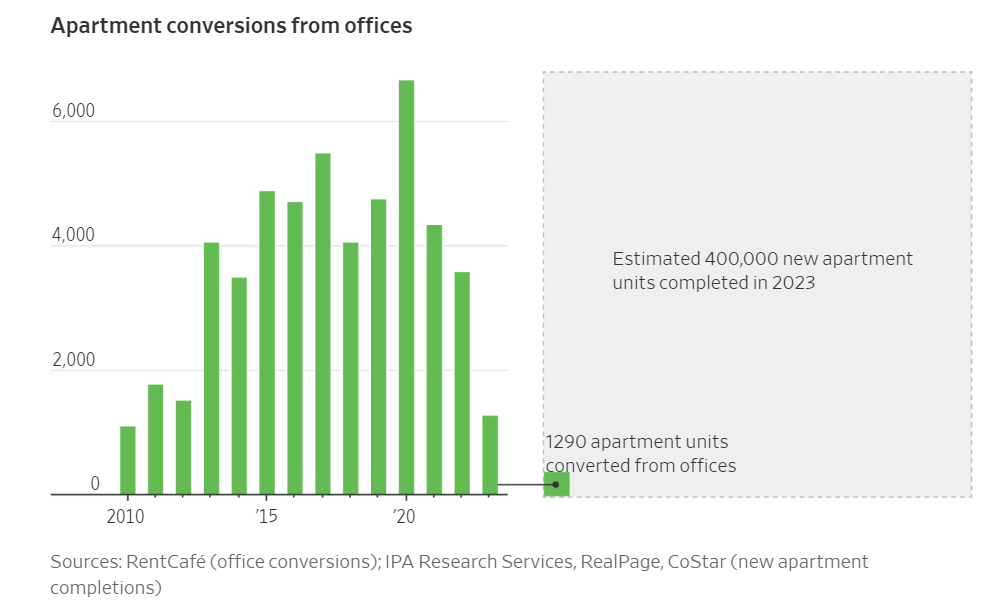

Has anyone considered the impact of Biden/Mayorkas’s open southern border with Mexico? Other than the crime, stress on existing services like healthcare, schools and Social Security. But where will the 8 million illegal immigrants reside? Well. the Biden Administration has an answer: throw money at it! This time, $45 billion to convert empty office space to homes. Not just for illegals, but for anyone.

Cities hoping to convert emptying office buildings into apartments are running into financing issues, stagnating rental markets and other challenges that are bottling up their efforts.

Developers last year created just 3,575 apartment units in the U.S. through office conversions, according to an analysis by rental listing site RentCafe. That amounts to less than 1% of all apartments built that year through new construction.

Federal and local governments are also trying to give conversions a boost. The White House said last month that it was updating guidance for existing grants and spending programs to make billions in federal dollars available for these projects. It also said it would seek the conversion of more government-owned properties into housing.

Some cities, such as Washington, D.C., New York and San Francisco, are also taking steps to encourage more conversions. Tax incentives and faster approvals are “rocket fuel” for these projects, said Sheila Botting, a principal at commercial property brokerage Avison Young.

Even so, the process has always been fraught with difficulty and few office buildings are natural candidates. Conversions are easiest in older, lower-quality and mostly empty buildings with small floors. But less than 1% of office space in the biggest U.S. cities ticks those boxes, according to Avison Young.

In significant ways, the conversion process is getting even harder now. Slowing rent growth might make apartment conversions less attractive to investors, if the trend persists into next year. Asking rents for apartments have fallen 1.2% nationally over the past 12 months, according to rentals website Apartment List.

Projects Not Economical

Without massive subsidies these projects are not economically feasible. Many aren’t even with massive subsidies.

In downtown Dallas, developer Wolfe Investments seeks to convert an 18-story, 1950s office tower into residential apartments, but has recently been fighting off foreclosure from its lender, Thistle Creek Partners, court records show.

Developers of One Camelback, a 200,000-square-foot office building in central Phoenix, are trying to convert it into what would be one of the city’s most expensive rental-apartment properties. A website advertises $8,000-a-month apartments, with floor-to-ceiling windows and crystal-clear views of nearby mountains.

But the developers, Sagamore Capital and partners defaulted on a loan of about $70 million. The project’s lender, Delphi Financial Group, has moved to foreclose. An auction of One Camelback is set for later this month, according to documents filed in Maricopa County, Ariz.

Biden Throws $45 Billion in Federal Funds to Convert Offices into Homes

Questions abound. Assume you can convert offices into homes, who wants to live in them? Is a tear down cheaper?

The government has 1,500 office buildings nationally and leases on almost 200 million square feet of additional space that it does not need. Instead of canceling leases and selling the real estate, it’s going to convert them into clean energy spaces.

With enough subsidies, developers will try nearly anything. Then when the projects fail, the developers ask for more money.

How is this Being Paid For?

Taxpayers of course. But Biden is funneling $45 billion from clean energy incentives in the ridiculously named Inflation Reduction Act (IRA) into housing conversions.

You might also be wondering what this has to do with clean energy, and the answer is nothing. The questions keep piling up and I have answers.

What’s Really Going On Here?

Biden is hoping to spread the IRA dollars around to buy more votes.

But to do so, he is taking money away from his other pet projects to fund the idea of the moment. His idea of the moment is to do something about the price of rent.

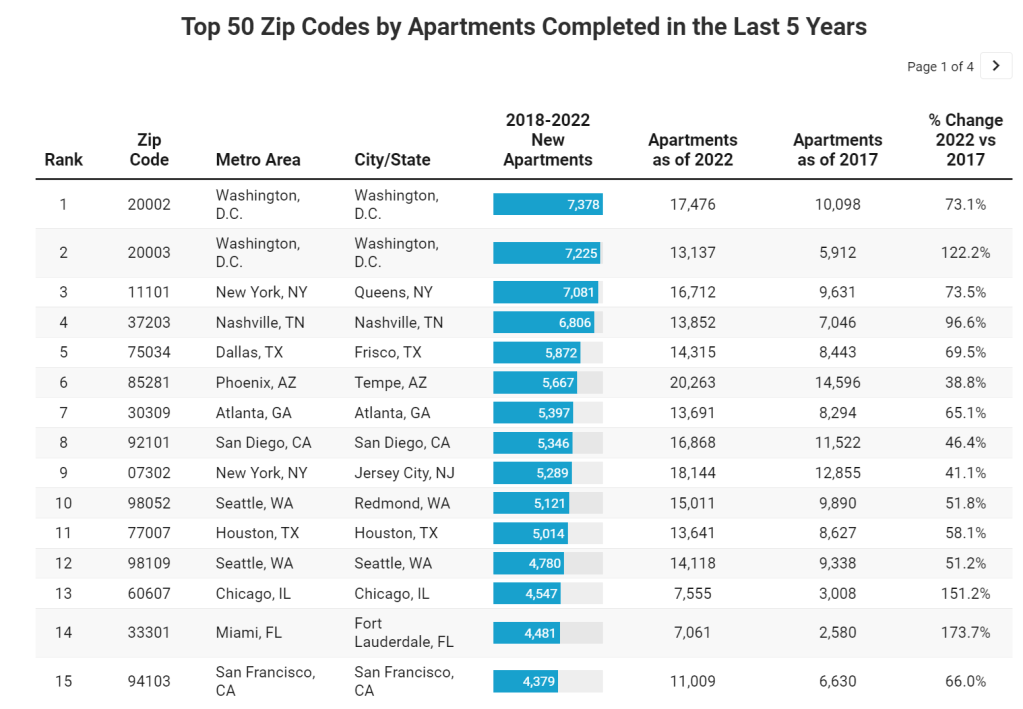

According to RentCafe, Washington DC had two zip codes that led the nation in apartments completed in the last five years (up to 2022).

Why is the private sector doing so few conversions? THAT is the right question. The answer? Office-to-housing conversion is hard and the demand may not be there. But with 8 million illegal immigrants having crossed the border, Biden has to do something. So Biden steps in with $45 billion to convert empty office space to homes. And I have to ask: is this a shadow wealth transfer to large Democrat-controlled cities as an apology for the havoc caused by Biden/Mayorkas open border policy?? Just asking!

So if an idea is really bad and won’t work, like solar power in areas with limited/spotty sunlight or wind turbines in areas with little/sporadic wind, Federal and State governments are always on stand-by to do something really stupid. Like rent control, which creates even worse distortions.

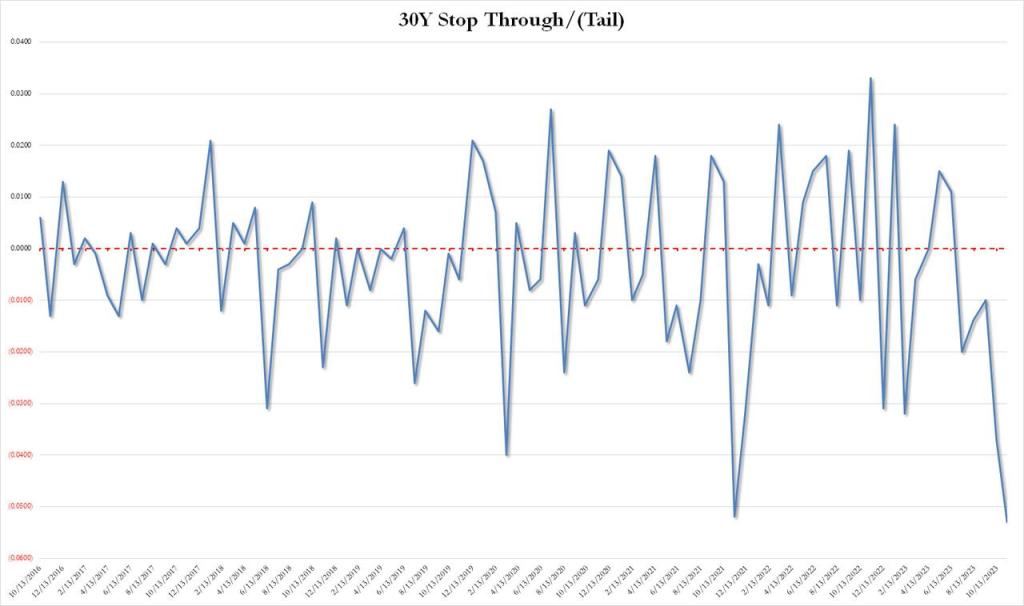

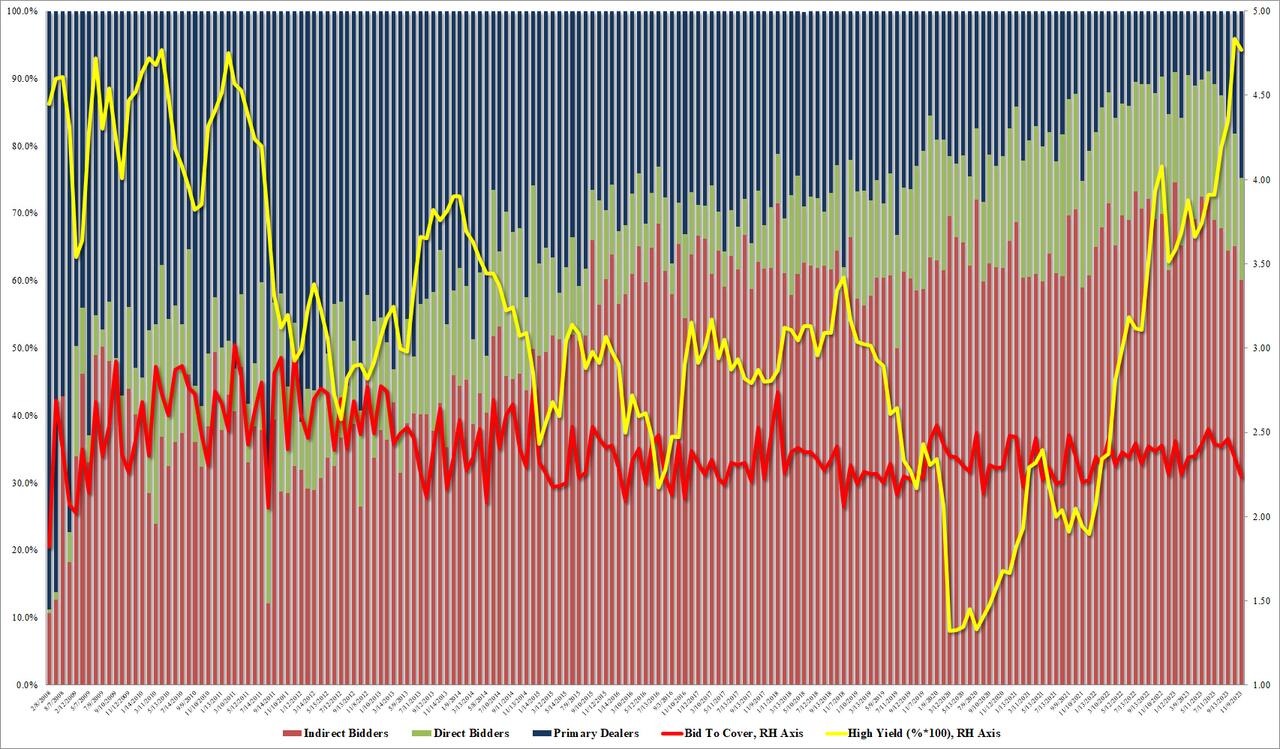

The bond priced at a high yield of 4.769%, which was below last month’s 4.837%, and just shy of the April 2010 high. But more importantly, it tailed the When Issued by a whopping 5.3bps, which was… well… terrible, because as shown in the chart below, this was the biggest tail on record (going back to 2016).

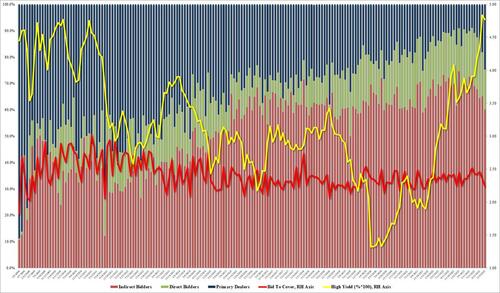

The bid to cover was just as bad: at 2.236 it was the lowest since Dec 2021.

The internals were even worse as foreign bidders (Indirects) tumbled from 65.1% to 60.1%, the lowest since Nov 2021, and with Directs taking down only 15.2%, banks (Dealers) were forced to step up and take the balance, or a whopping 24.7%, double the recent average of 12.7%, and the highest since Nov 2021.

This is a big warning flag because every time we have seen a surge in Dealer takedowns, some sort of Fed intervention – QE or otherwise – has usually followed and we doubt this time will be different.

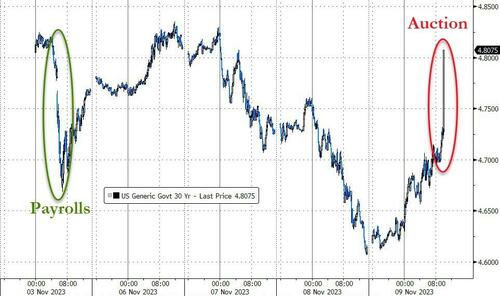

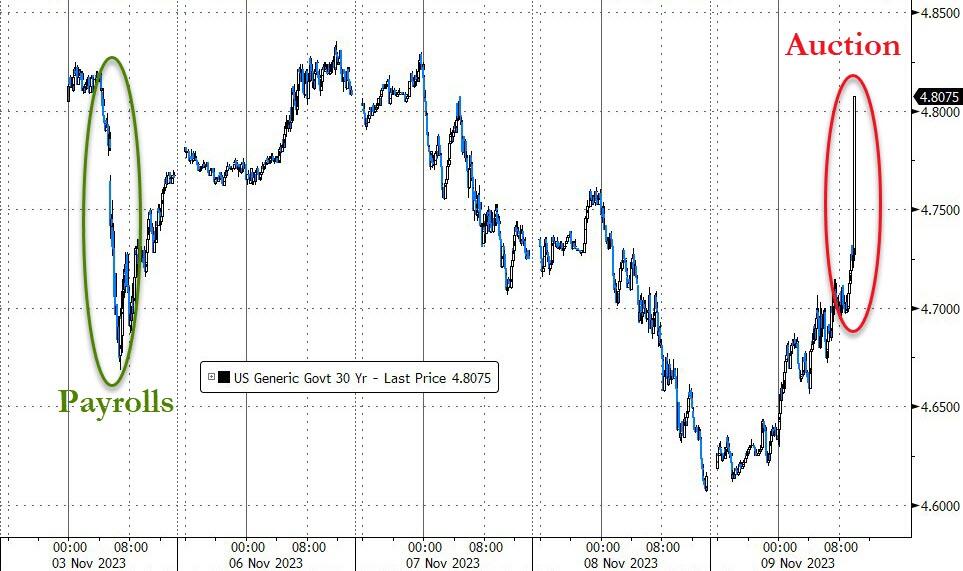

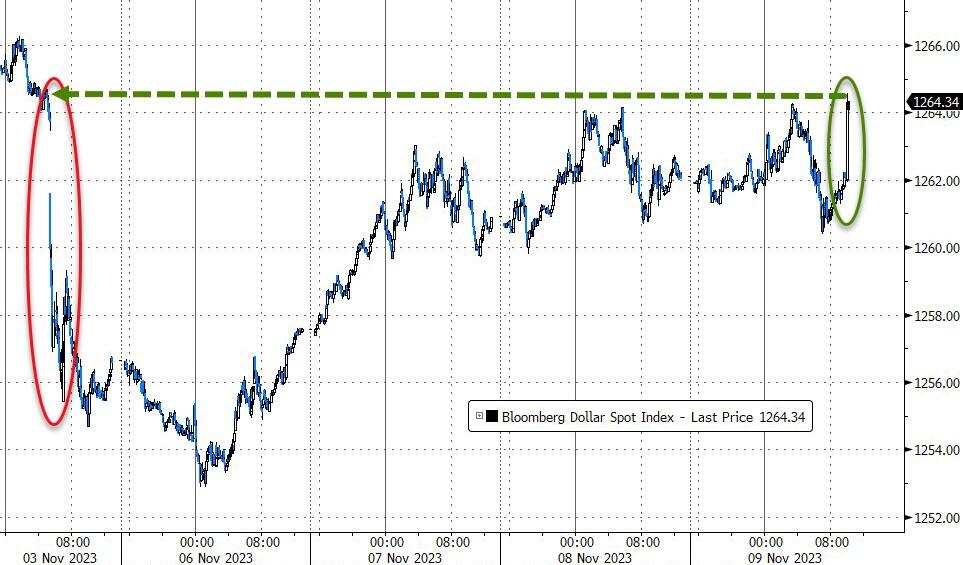

The market reaction to the catastrophic 30Y auction was immediately, sparking a swift and painful response across markets with bonds and stocks hammered lower and the dollar spiking.

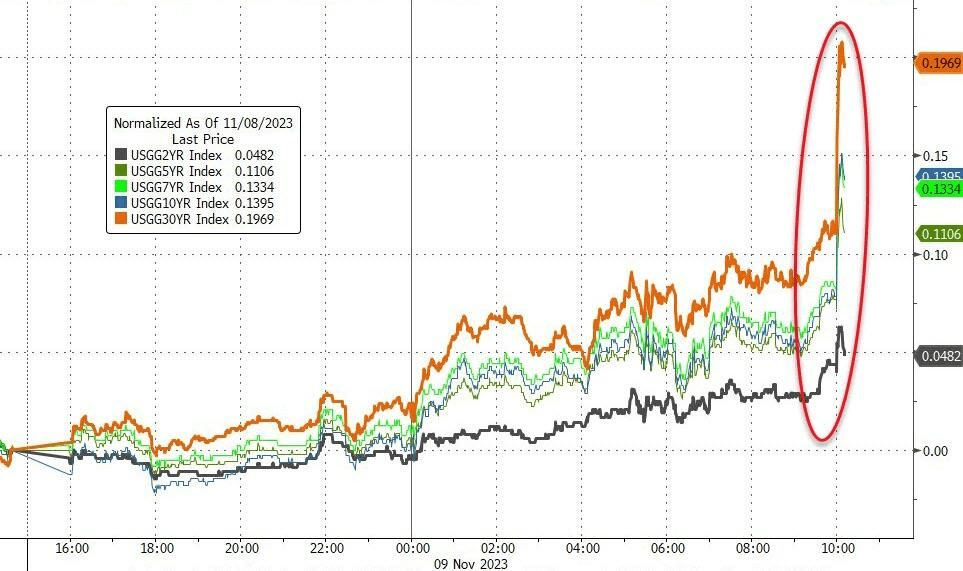

Treasury yields – as you would expect – exploded higher, with 30Y Yields back up to pre-payrolls levels…

That is the biggest spike in 30Y yields since March 2020…

But the entire curve is higher in yields…

Stocks tanked…

Regional bank stocks tumbled…

The dollar ripped back up to pre-payrolls levels…

Finally, we note that this ugly auction comes as Treasury Liquidity is evaporating dramatically…

The Fed (and The Treasury) have a problem!! Particularly since the 30Y yield reversed course and is on the rise again.

And at the 10 year tenor, the rate rose to 4.638%.

All together now!!

The Edmund Fitzgerald, symbolic of the US under Biden and Janet Yellen.

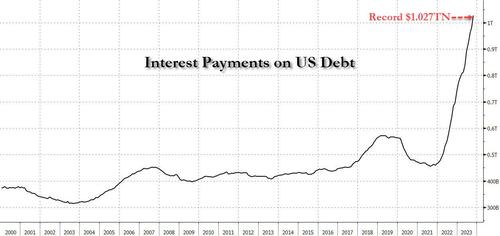

$1.027 trillion in interest is calculated by multiplying the average interest rate on marketable US Treasury debt (which according to the Treasury is 3.096% as of Oct 31) by the $26.003 trillion in marketable US debt (as of Oct 31) which nets off to $805 billion, and adding to this non-marketable debt interest (which as of Oct 31 was 2.884% multiplied by the amount of non-marketable debt which is $7.696 trillion) and which in turn is an additional $222 billion in interest. Add across and you get $1.027 trillion.

Naturally, this calculation of estimated real-time interest costs – which is entirely based on Treasury data – is different than what the Treasury actually paid. Interest costs in the fiscal year that ended Sept. 30 ultimately totaled $879.3 billion, up from $717.6 billion the previous year and about 14% of total outlays, however that number is merely lagging what the pro forma print currently is, and will inevitably catch up to it, and then lag on the other side even as pro forma interest payment start dropping (once interest rates plunge after the next QE/YCC is launched).

Fans of exponential functions, we got you covered: the unprecedented surge in both interest rates and interest expense in the past two years means that total US interest has doubled since April 2022 and that’s with the inherent lag in interest catch up – as a reminder, the vast majority of 5, 7, 10 and 30 year debt is still locked in at much lower interest rates, and as such, rates will continue to rise as all of the existing debt rolls into much higher rates over the coming years.

Looking ahead, the staggering surge in both yields and total long-term Treasuries in recent months confirms the government will continue to face an escalating interest bill. As a reminder, we were the first to point out that it took just one month after US federal debt first rose above $33 trillion for the first time, to spike by another $600 billion.

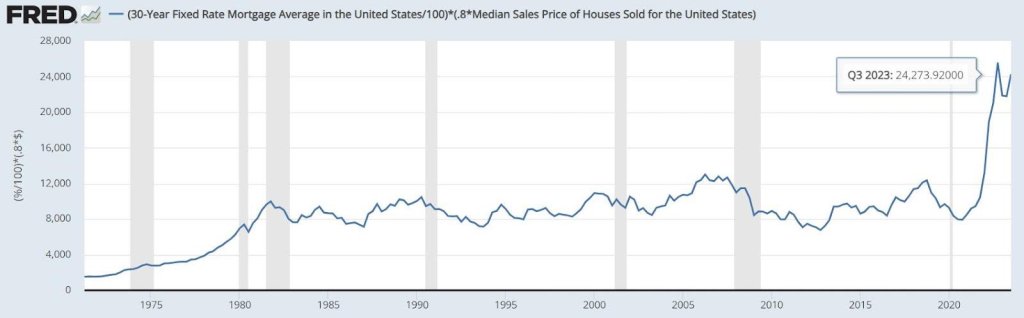

On the personal finance side, annual Interest payments on a 30-year, fixed-rate mortgage before Biden was $8,500, but after Biden it almost tripled to $24,300! That means that annual mortgage interest rose 186% under Biden.

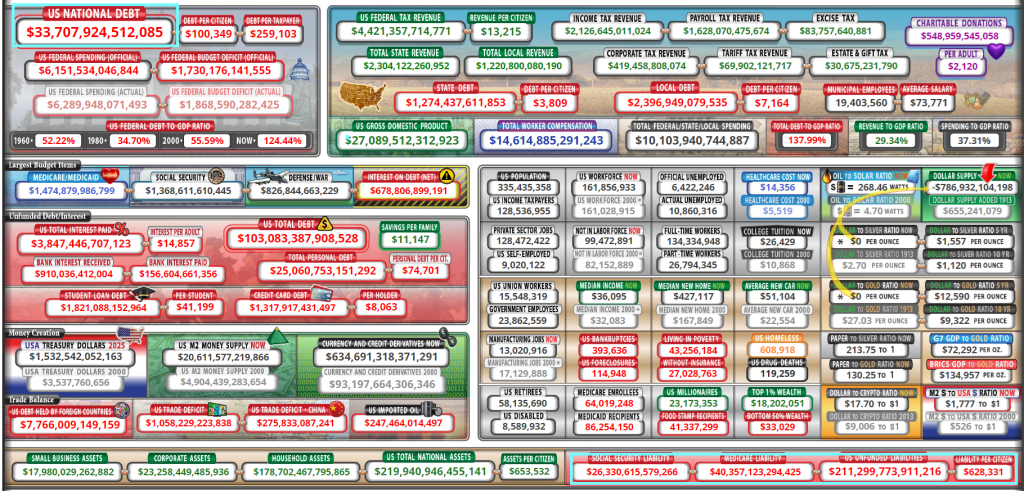

US Federal debt just hit $33.71 TRILLION. And unfunded liabilities (promises from Uncle Spam) are now $211 TRILLION. That is 526% of the the current debt load. Which means either lots of additional debt, higher tax rates or cuts in entitlements.

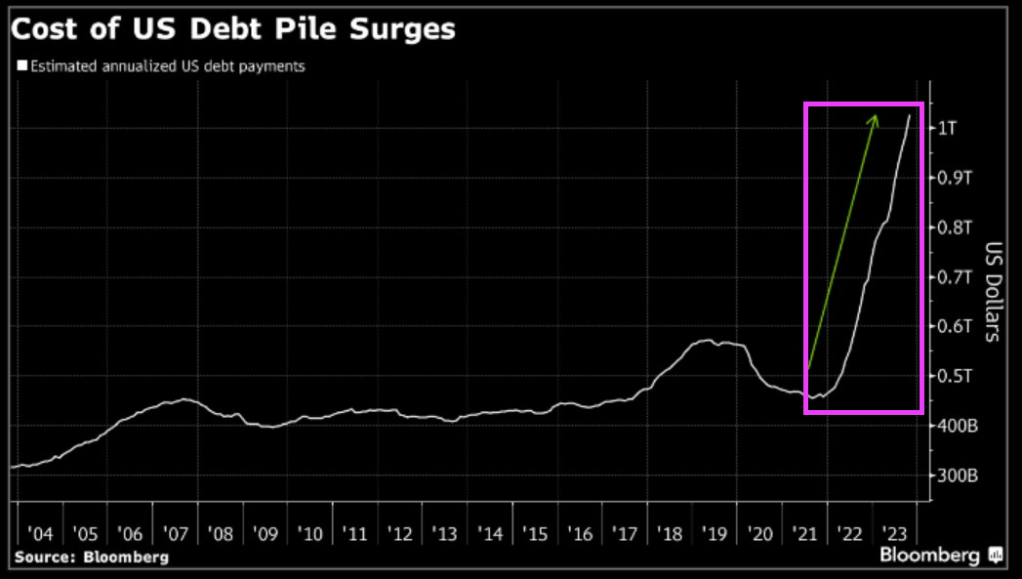

The cost of US debt continues to soars as The Fed combats Bidenflation.

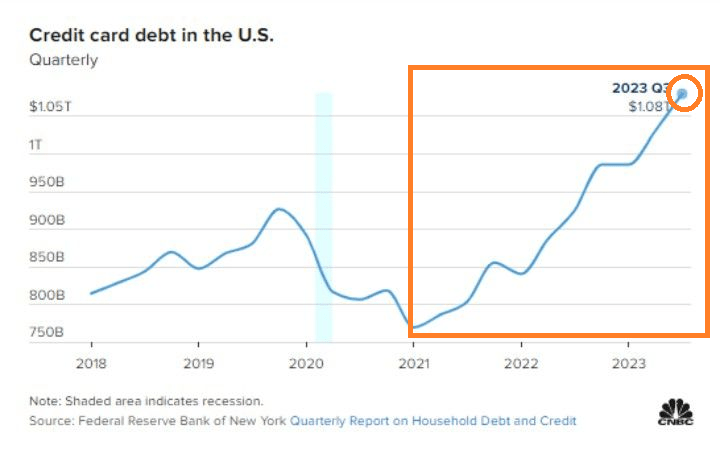

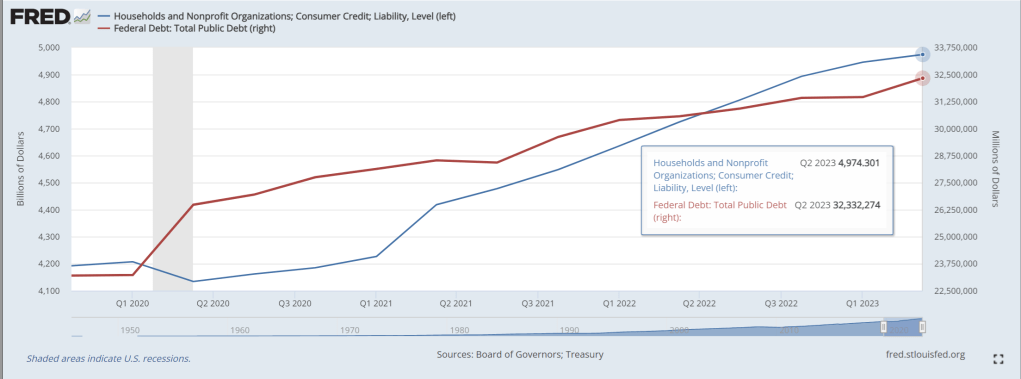

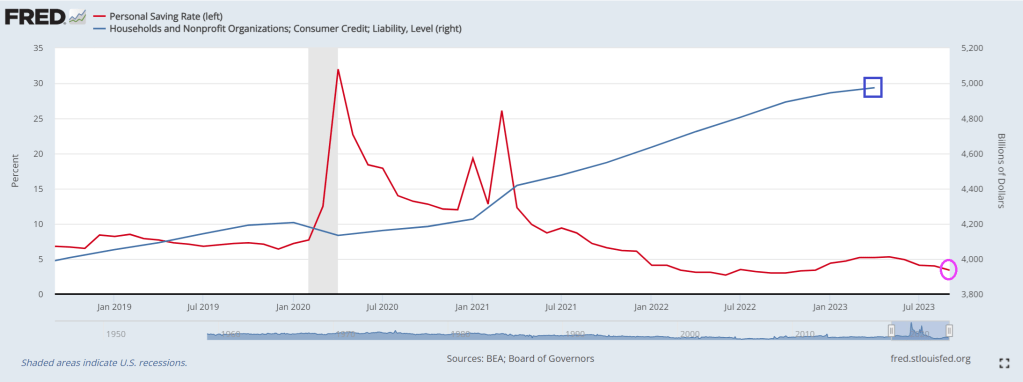

But it isn’t just Federal government debt that is exploding under Bidenomics. Consumer credit card debt has exploded under Bidenomics as consumer struggle with inflation.

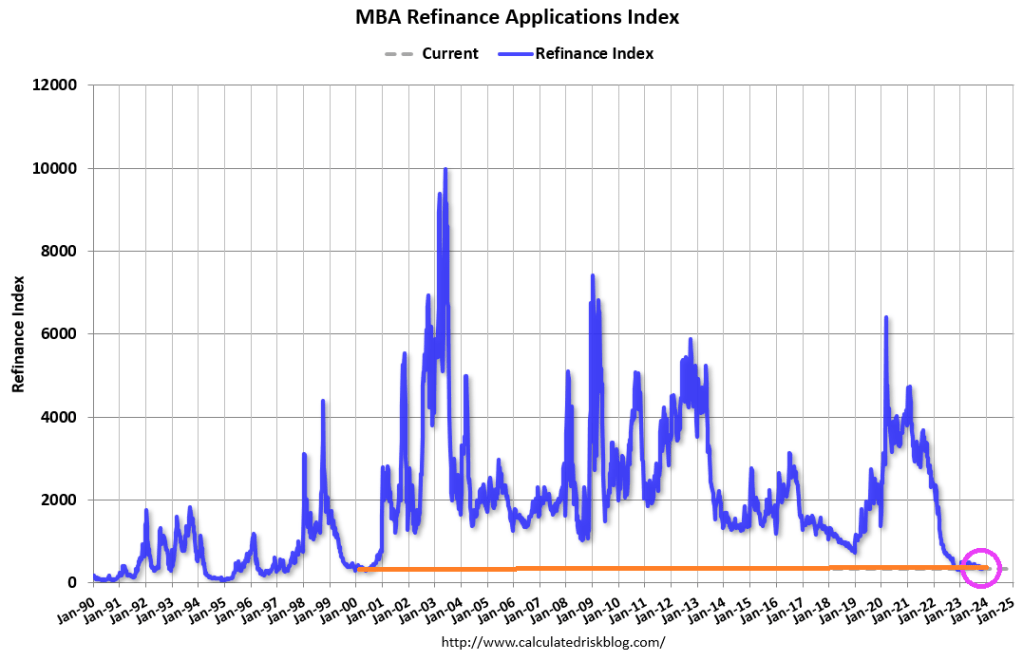

US inflation is lower than it was a year ago (cheers from The View CNN and MSNBC cheerleaders), but inflation remains stubborning above The Fed’s 2% target rate and will likely remain above 2% for the nexf few years. So mortgage demand is much like inflation … mortgage demand increased in the latest week but generally is very low compared to last year.

Mortgage applications increased 2.5 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending November 3, 2023.

The Market Composite Index, a measure of mortgage loan application volume, increased 2.5 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index increased 1 percent compared with the previous week. The Refinance Index increased 2 percent from the previous week and was 7 percent lower than the same week one year ago.

The seasonally adjusted Purchase Index increased 3 percent from one week earlier. The unadjusted Purchase Index increased 1 percent compared with the previous week and was 20 percent lower than the same week one year ago.

The 30-year fixed mortgage rate dropped by 25 basis points to 7.61 percent, the largest single week decline since July 2022. But, mortgage rates are up 169% under Biden and Bidenomics.

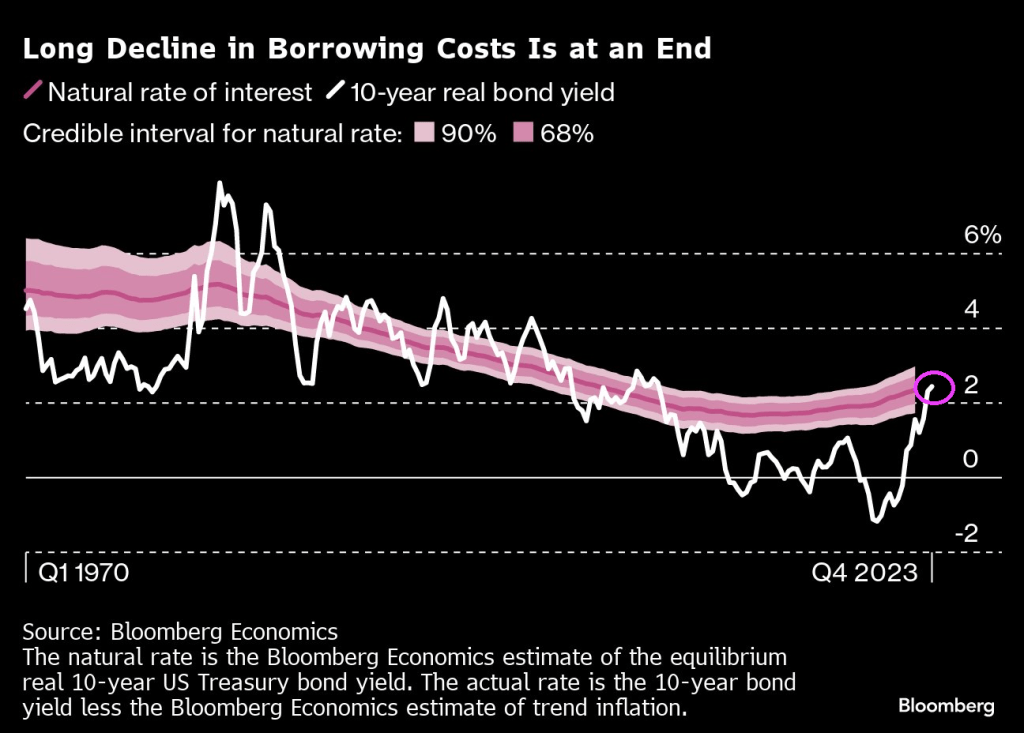

But on the middle class front, we can see “cheap rates” are a thing of the past as markets have to deal with Biden’s inflation problem and Fed rate hikes.

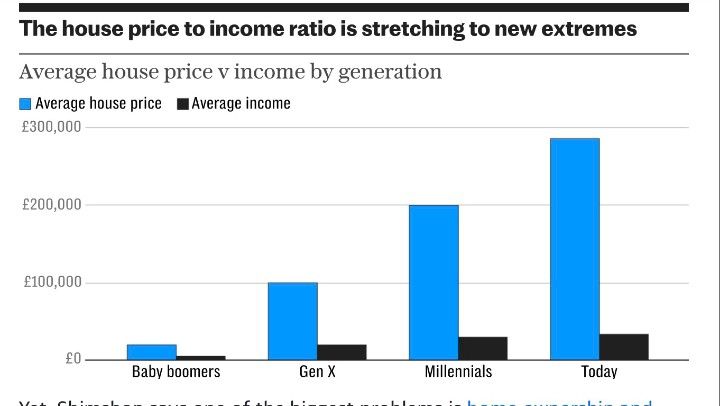

And with rising home prices under Biden, the house price to income ratio is out of control and causing pain for the middle class.

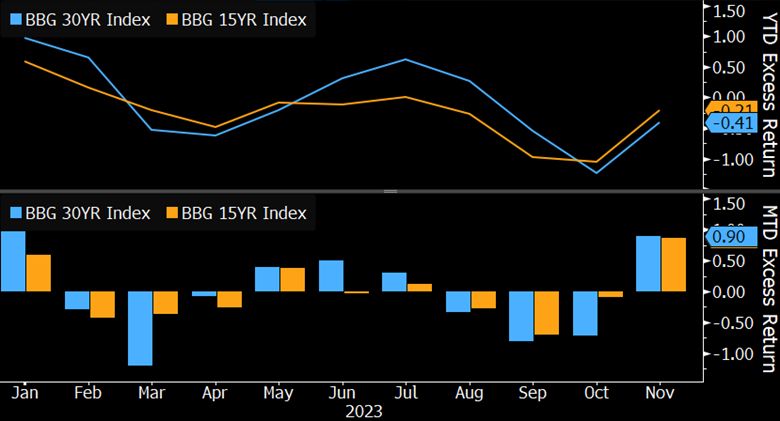

On the MBS front, we see negative returns.

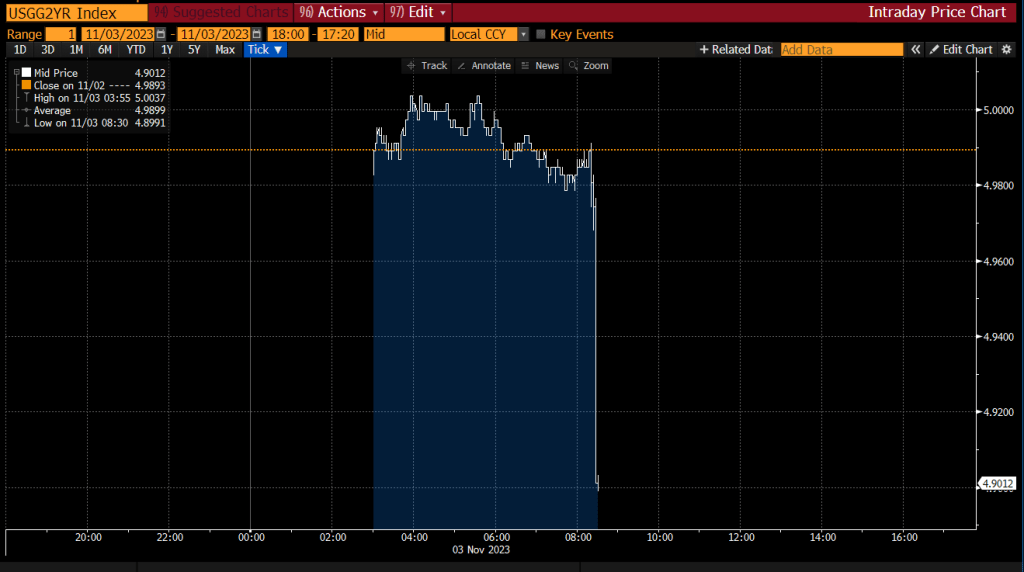

The 2-year Treasury yield is dropping faster than Biden’s polling numbers.

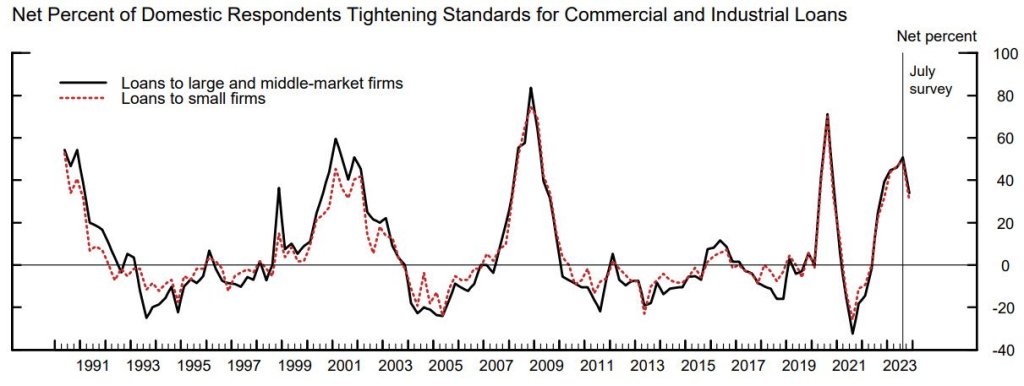

On the credit side, more lenders are tightening standards for C&I loans.

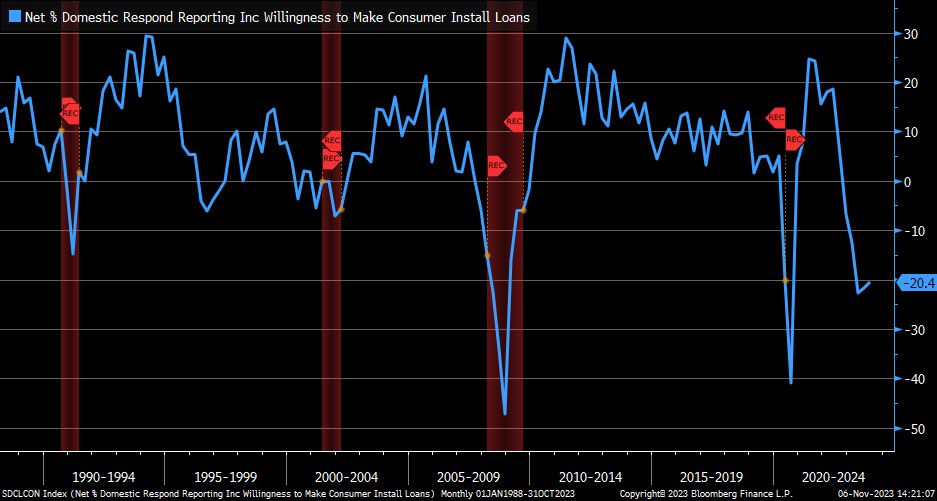

And banks remained restrictive in their willingness (or lack thereof) to make consumer loans, but there was a marginal improvement from prior release.

On the global front, Maersk announces plans to cut at least 10,000 jobs due to weakening global trade.

Here is a picture of Hinky Dink (Joe Biden) and Bathhouse Barry Soetoro. I mean Bathhouse John Coughlin, the Lords of the Levee.

No, this isn’t the tilt effect in the mortgage market where inflation is front-loaded in mortgage rates making mortgage payments quite unaffordable. Although inflation is causing mortgage rates to be up 174% under Biden (while Biden continues to brag about how Bidenomics is helping). Meanwhile, the 10Y Treasury yield is up 402% under Biden (making refinancing the US staggering debt load more difficult to refinance. Higher mortgage rates tilt the present value of mortgage payments to the front, making housing even more unaffordable. Thanks Joe!

But the Tilt effect I am talking about is the TLT effect. TLT (iShares US Treasuries 20y+ ETF) calls. Friday was the largest TLT call volume ever.

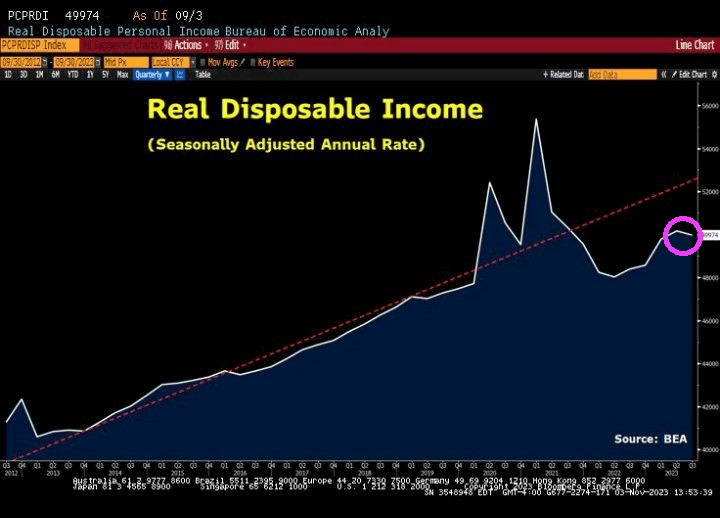

Meanwhile, US real disposable income is declining.

Call it “The Rich Men North Of Richmond” economy. Where the coastal elites drive the US economy off the cliff with insane spending and borrowing with much of the benefits flowing to big political donors, not the middle class. Think of Span Bankfraud Parboiled as an example.

President Biden loves to spend billions and go on endless vacations (he is in Rehobeth Beach Delaware yet again). He (illegally) forgave student debt, keeps spending billions on Ukraine and keeps spending on failed green energy nightmares.

Biden and his allies will tout the latest GDP numbers as an example of how marvelous Bidenomics is. BUT that GDP report was driven largely by consumer spending.

Since the Covid outbreak in 2020, Federal (public) debt is up 45%! Wow. And consumer debt is up 19% under Biden to cope with inflation (caused primarily by massive Federal spending).

To fuel consumer spending, the personal savings rate has fallen to 3.4%. For point of reference, the personal savings rate in Februray 2020 was 7.7%, so the consumer is running out of gas thanks to inflation and spending.

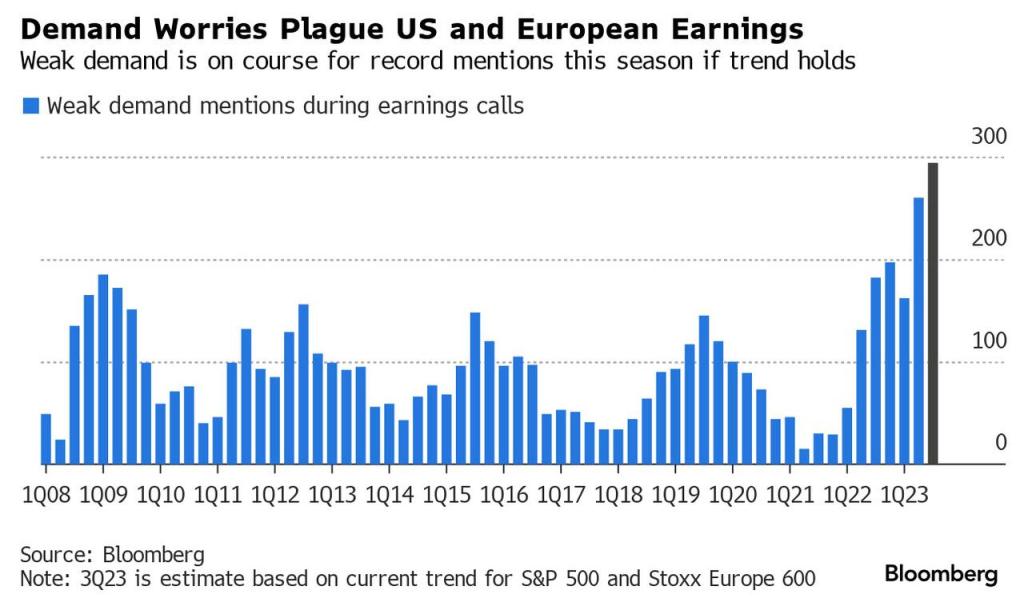

And with a debt-stressed consumer, earnings call revealed concern about continued demand.

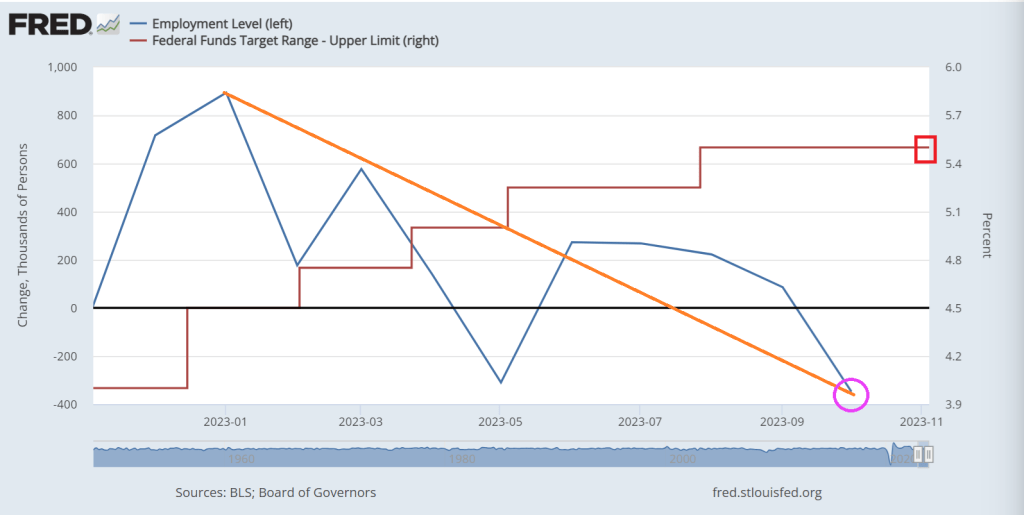

Note the trend in jobs added as The Fed tightened to fight inflation.

Appartently, Joe Biden and fellow big spenders in Washington DC, Mordor on The Potomac, don’t care about fiscal discipline. With seemingly endless spending of wars (Ukraine, Israel, Taiwan and the invasion at our southern border, and inane “green” spending,

Janet Yellen and the US Treasury will be auctioning off $776 billion of debt in the final quarter of calendar 2023, a bit below market expectations. Treasury said it will auction another $816 billion in the first quarter of 2024. So, that is yet another $1.6 TRILLION in debt.

Such large payments are negative for the economy. Interest is likely to be paid for using higher-velocity money (e.g. taxes) and received by holders less likely to spend the proceeds in the broad economy, and instead re-invest it. Independent monetary policy becomes increasingly difficult when the equivalent of 6% of US GDP is being diverted towards interest payments each year.

It’s not only the size of Treasury borrowing that’s a problem, but it’s maturity composition.

Issuance has latterly been skewed to bills, which has ameliorated the impact on liquidity as money market funds have been able to intermediate through the reverse repo (RRP) facility at the Fed. But as issuance skews back towards longer-term debt (watch for increases in auction sizes in 2y, 3y, 5y, 7y, 10y, 20y and 30y debt for insight on this), that will have an increasingly negative impact on liquidity, especially if the Treasury maintains its large cash balance at the Fed (as it said on Monday it expected to do).

The Fed has little (or no) say over any of this.

Monetary policy will become increasingly overwhelmed in such an environment, which is why today’s Fed meeting, where it is expected to keep rates on hold, is a bit of an afterthought.

Also of more consequence currently is Japan.

The BOJ’s decision to maintain negative yields and keep its yield curve control policy largely intact ladles on yet more underlying risks to the global macro environment.

Allegedly, The Fed isn’t interested in buying additional US debt, and likely China and Japan won’t be buying our debt either. But maybe the REAL Federal government, Blackrock and their friends will buy the debt!

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.