The US has a bad case of failed leadership and misguided economic policies.

Joe Biden is an incredibly weak President. I am not talking about his age or his deteriorating mental faculties. I am talking about ordering his attorney general to indict his chief political opponent, Donald Trump. How does the world interpret this weakness? BADLY.

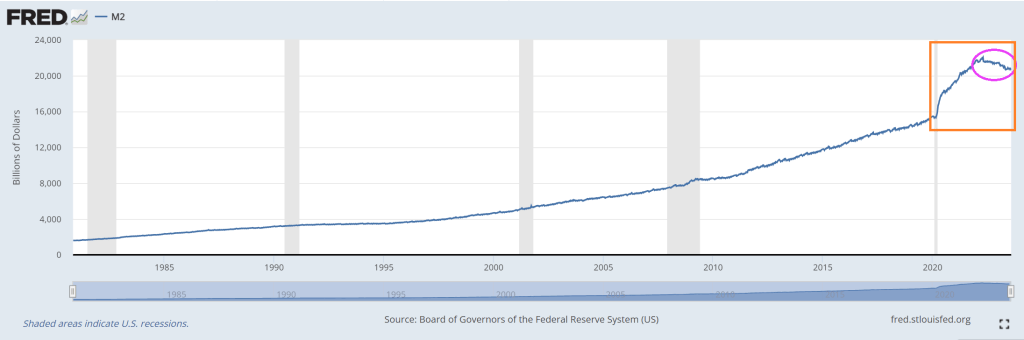

The US has gone off the rails in terms of printing money, particularly since COVID struck and money printing went wild.

Under Biden’s Reign of Error and the US reckless money printing, more countries are abandoning King Dollar (based of fiat currency) and joining BRICS. Brazil, Russia, India, China, South Africa and a host of countries joining like Argentina, Saudi Arabia, Iran, Egypt, UAE, etc.

Now, the rest of the world is still stuck on the US Dollar as reserve currency … for now. But as Biden gets weaker and weaker, watch more countries join BRICs.

According to Reuters, there are over 40 countries that have expressed interest in joining BRICS. A smaller group of 16 countries have actually applied for membership, though, and this list includes Algeria, Cuba, Indonesia, Palestine, and Vietnam. Pretty soon, under Biden’s crazy leadership, we may be the last man standing in using the US Dollar as reserve currency.

Then we have the other shoe dropping with Bidenomics.

As soon as Biden took office, he set out to destroy industries that produce reasonably priced energy. He focused tremendous effort on deficit spending and borrowing to hand out “government goodies” to buy votes; recipients of this government largesse, in large part, included debt-saddled students, the green mafia, and leftist activists.

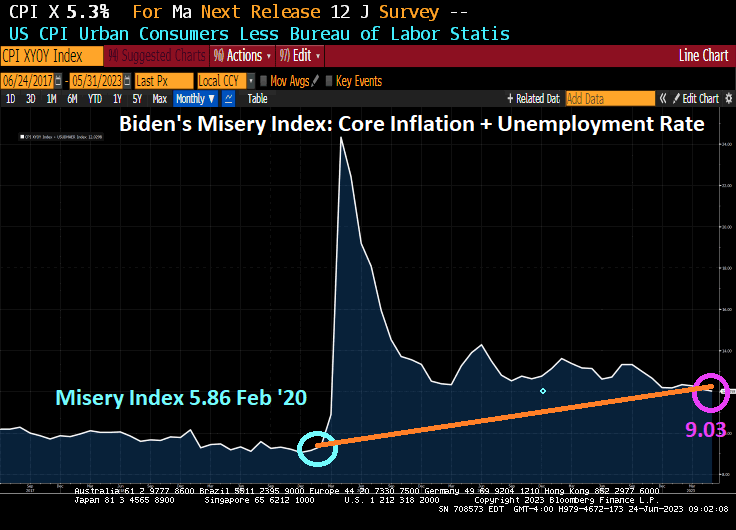

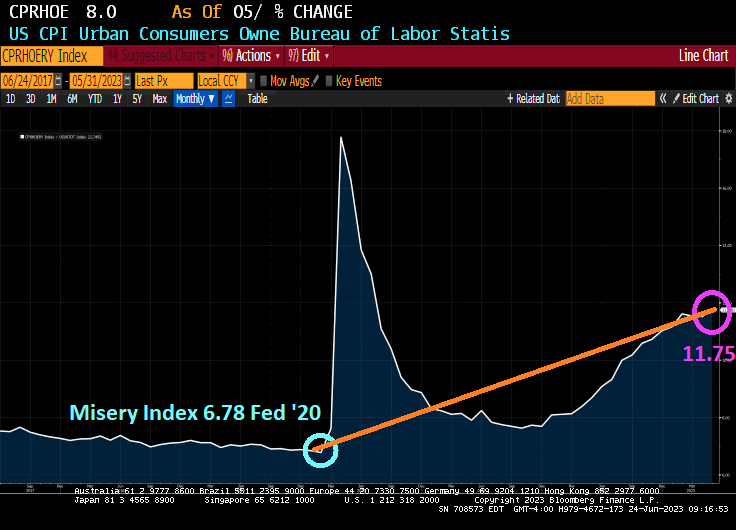

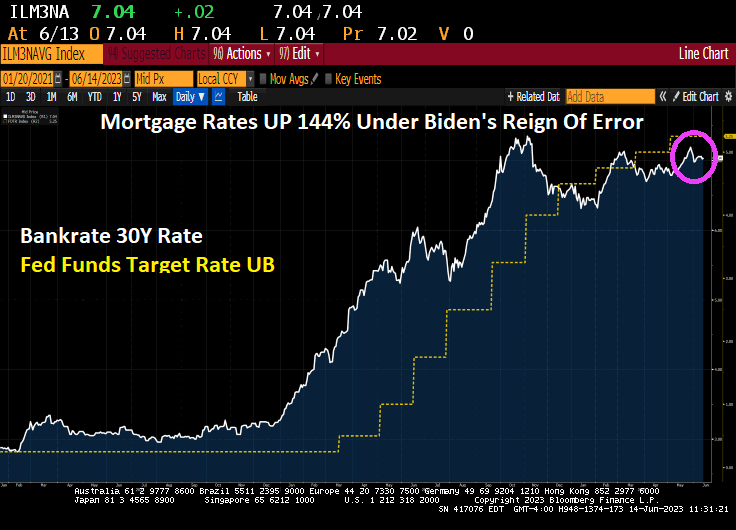

When Biden took office, inflation was under 2%, despite COVID and supply chain disruptions; shortly after, it skyrocketed to over 9%. Now inflation increases are “down” but prices remain exceptionally high compared to pre-Biden.

For example, crude oil prices, which affect almost everything and are used in over 6,000 products, are roughly double what they were when Biden took over.

President Trump focused on reduced regulations and energy independence, and implemented lower tax rates, all moves that greatly helped the American people. In contrast, Biden focuses on ensuring bureaucrats rapidly increase regulations which raises costs for everyday Americans; he’s waging economic war against us. Very few of Biden’s regulations go through Congress. From the White House archives:

Between FY 2017 and FY 2019, the Trump Administration has cut nearly eight regulations for every new, significant regulation….

The Council of Economic Advisers (CEA) estimates that this pro-growth approach to Federal regulation will raise real incomes by upwards of $3,100 per household per year.

Here are some recent reports of how well Biden policies are working:

Leading economic indicators have fallen for sixteen straight months. Maybe that is why people think the economy is moving in the wrong direction?

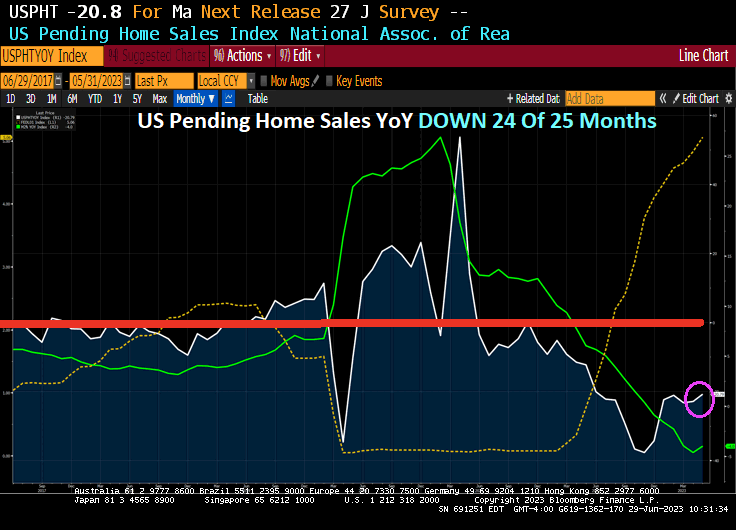

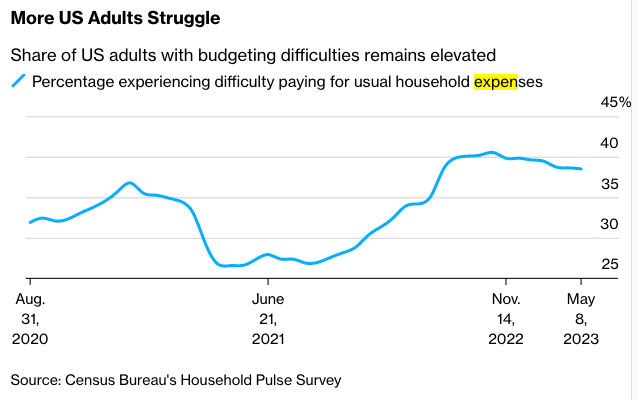

The current cost-of-living crisis is a manufactured one. As inflation rose, the Federal Reserve was forced to raise interest rates, which saw fewer people move. The cycle is very understandable, as simply explained in this one headline, “Housing Crunch: Home Sales Fall To Six Month Low…But Prices Rise Anyway”.

Parcel volumes are dropping by so much, freight pilots are “worried” about job security.

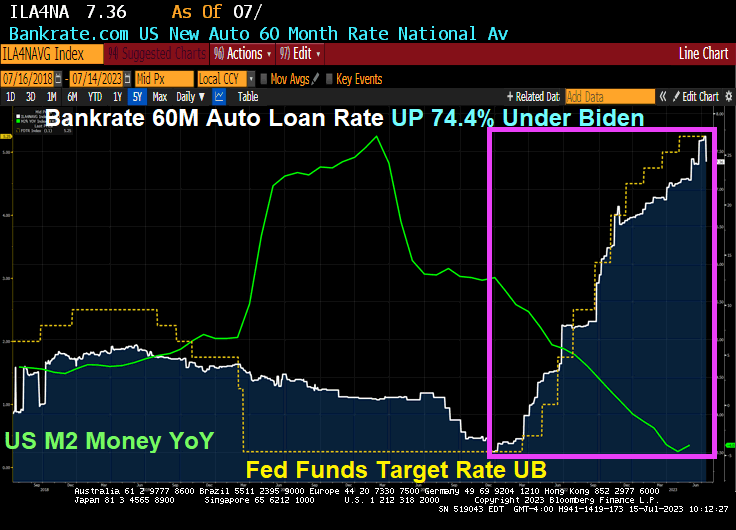

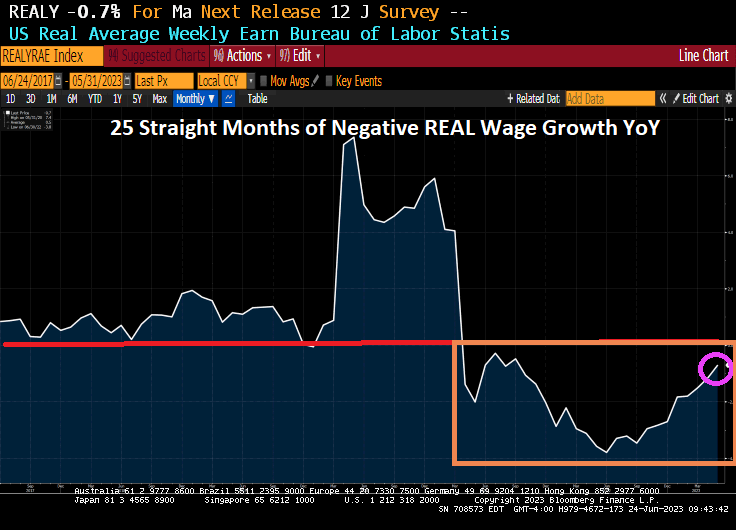

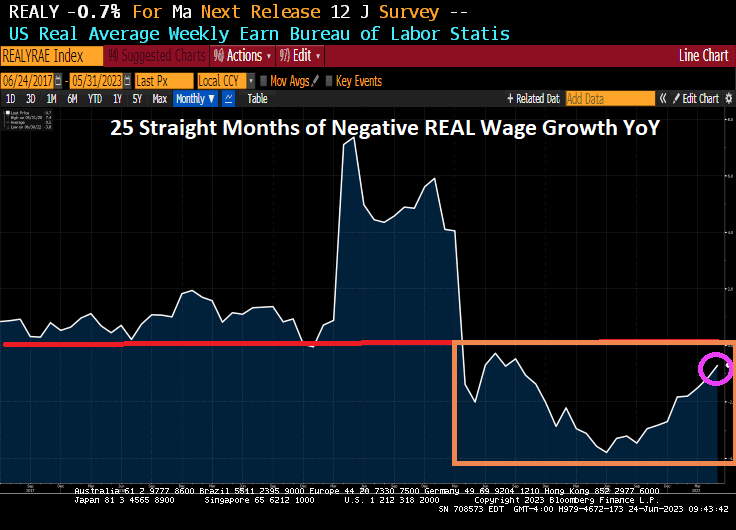

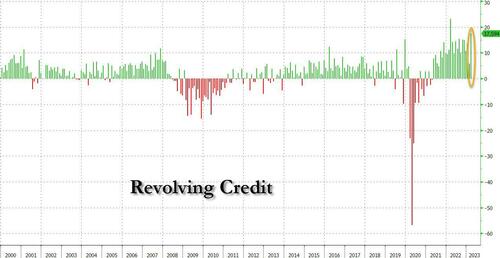

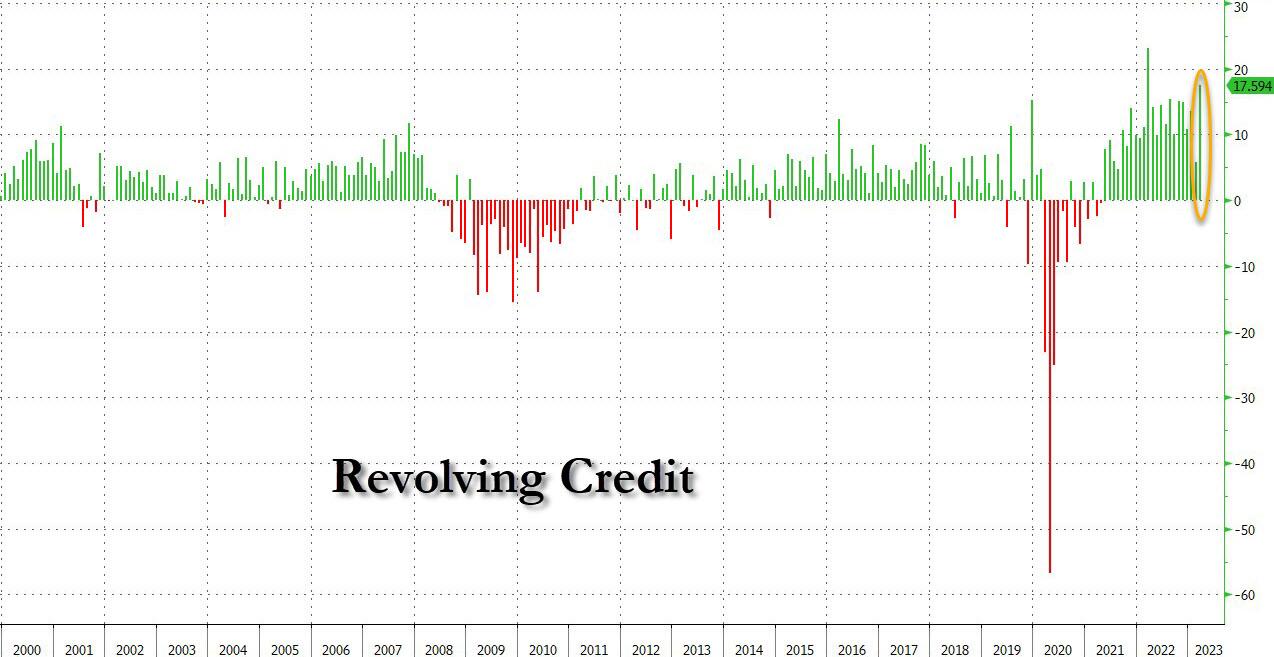

People are running up credit card debt and defaulting on car loans because of high inflation, and because their real wages haven’t been able to sustain them. Now, even more are falling behind on their payments. From CNN:

More Americans are failing to make payments on their credit cards and auto loans, another sign of rising financial pressure on consumers.

New credit card and auto loan delinquencies have now surpassed pre-Covid levels, according to a Wednesday report issued by Moody’s Investors Service.

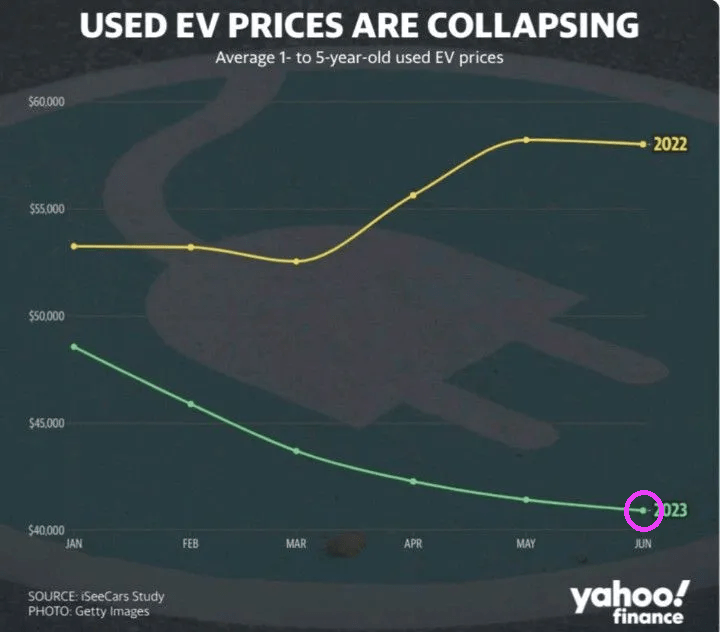

After years of promoting and subsidizing electric cars, they represent around 6% of total sales, and demand is clearly slowing. It wasn’t that long ago that well-to-do people were buying these electric toys so quickly that they were placed on waiting lists; now, inventories are building because they are too impractical and expensive:

Auto News understands that there is currently a 103-day supply of unsold EVs in the United States. While it did not specify how many units are sitting on dealership lots, it says there is a higher supply of unsold EVs than any other automotive segment, except those in the ultra-luxury and high-end luxury segments with supplies also reaching over 100 days.

So what is Biden’s solution? Force people to buy them.

Here are some simple economics questions for the media and other Democrats:

Does flooding the U.S with illegals help or hurt housing availability and affordability?

Will the intentional destruction of oil and coal companies help or hurt the middle class and the poor?

Yet, the media and other Democrats brag that Biden’s economic policies are great, and when the public gives Biden poor marks, they say that we just don’t understand, and we’re not willing to get behind a candidate if they fail to make us feel “warm and fuzzy.”

Are journalists really that unaware?

Of course, they always sought to destroy Trump as his policies, even as poverty sank to record lows amongst minorities, because they don’t really care about anything but big government. According to Census data:

In 2019, the poverty rate for the United States was 10.5%, the lowest since estimates were first released for 1959.

Poverty rates declined between 2018 and 2019 for all major race and Hispanic origin groups.

Two of these groups, Blacks and Hispanics, reached historic lows in their poverty rates in 2019.

Results and facts haven’t mattered to the complicit leftist media for a long time.

And perhaps the worst mistake Biden made (amongst his laundry list of horrible mistakes, [Afghanistan retreat, not showing up to E Palestine Ohio, Bidenomics that is a payoff to green donors and BIG corporate interests, an embarrasing visit to Maui two weeks after the fire, indicting his leading political opponent, ….) is the appointment of the WORST Federal Reserve Chair (Janet Yellen) as Treasury Secretary.

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.