The Fed’s favorite yield curve measure, the implied yield on 3-month T-Bills in 18 months less the 3-month T-bill yield has inverted. Note that this curve inverts prior to a recession.

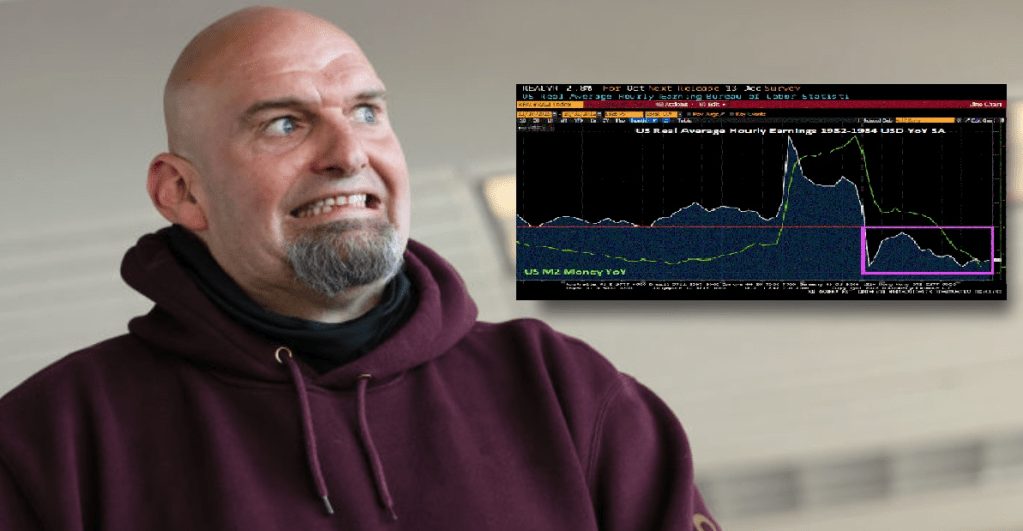

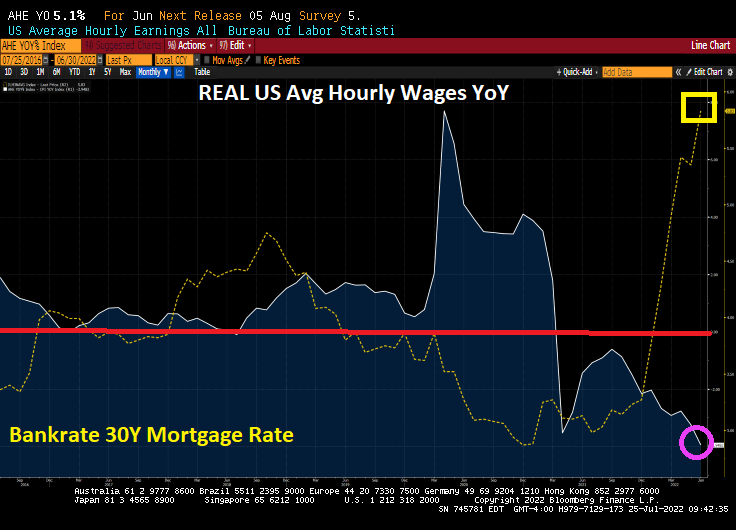

The new face of reckless Fed policy and Federal spending. 19 straight months of negative REAL earnings growth as America re-elects the same irresponsible fools that are turning the US into Venezuela.

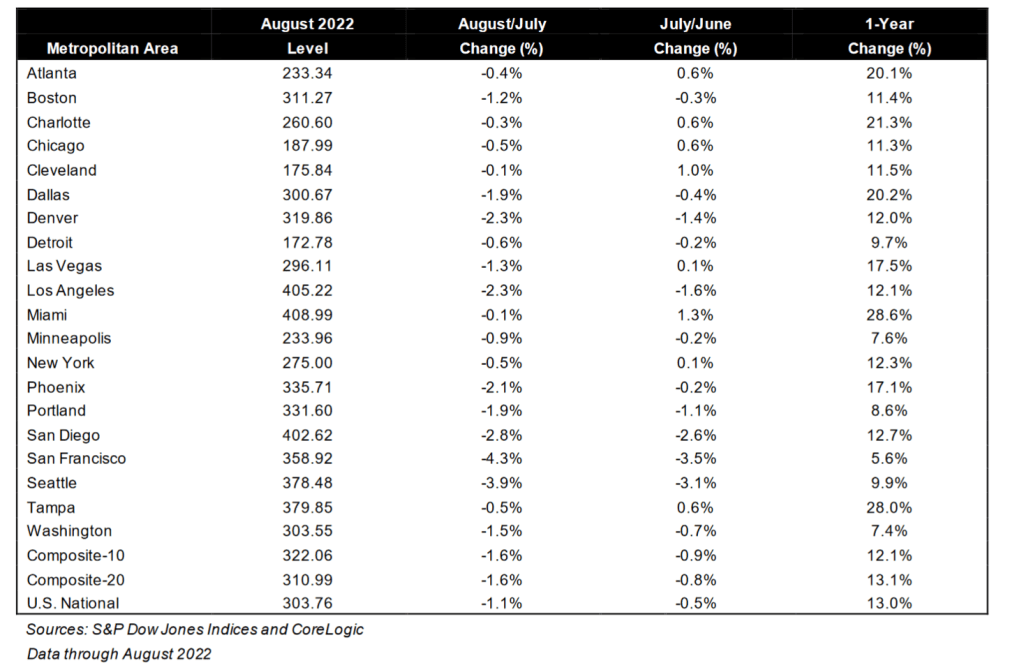

Alarm! US home prices are decelerating as inflation rages and The Fed tightens.

Home price growth in the US slowed the most on record as a doubling of borrowing costs (thanks to the US Federal Reserve) has sapped demand.

A national measure of prices increased 13% in August from a year earlier, but is down from 20.79% in March, the S&P CoreLogic Case-Shiller index showed Tuesday. That’s the biggest deceleration in the index’s history.

The housing market has started to slump as the Federal Reserve hikes interest rates to curb the hottest inflation in decades. Even with the deceleration, prices remain high compared to last year. Coupled with mortgage rates that are edging closer to 7%, many would-be buyers have been shut out, while some sellers have retreated.

While 13% growth sounds good, it is not good for renters looking to buy a home.

According to S&P/CoreLogic/Case-Shiller, Southern (red) cities Atlanta, Charlotte, Dallas, Miami and Tampa all still grew at over 20% YoY. Other cities like blue cities Detroit, Minneapolis, Portland, San Francisco, Seattle and Washington DC are grew at UNDER 10% YoY.

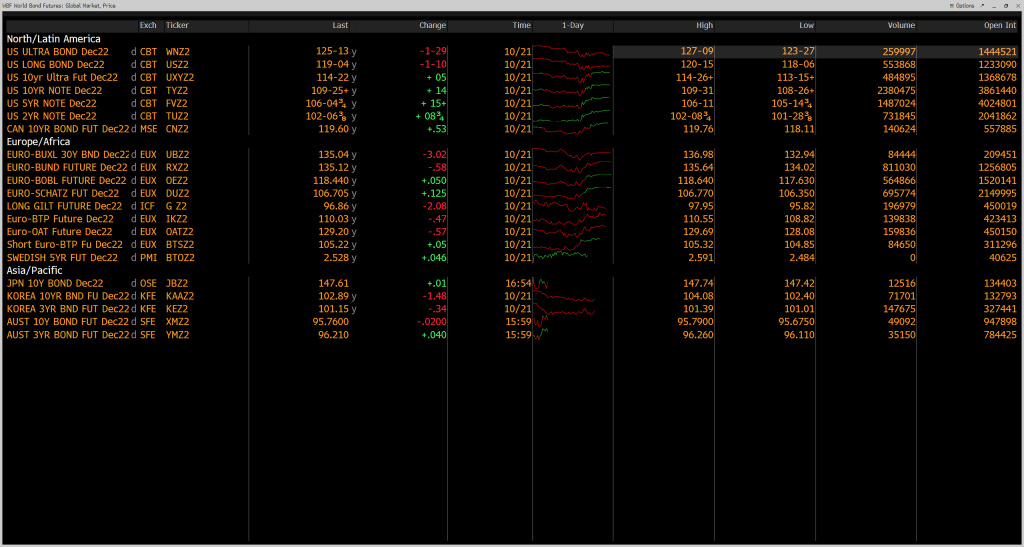

On related news, I always said in my classes that +/- 10 basis point in the US Treasury yield is a big deal. This morning, the US Treasury 10-year yield is DOWN -16.1 bps. In fact, the 10-year yields are down across the board globally.

Things are getting interesting in DC, to say the least. The US is 100% likely to face a recession in the next 12 months while The Federal Reserve is on its crusade to fight inflation caused by … The Federal Reserve, Biden’s green energy shenanigans and massive, irresponsible Federal spending that even Former Obama economist Lawrence Summers warned would cause inflation. So what will The Fed do? Lower rates and expand their assets purchases to fight the impending recession OR keep tightening to fight Bidenflation? But where we are now is that the fixed-income market could be in big, big trouble.

For months, traders, academics, and other analysts have fretted that the $23.7 trillion Treasuries market might be the source of the next financial crisis. Then last week, U.S. Treasury Secretary Janet Yellen acknowledged concerns about a potential breakdown in the trading of government debt and expressed worry about “a loss of adequate liquidity in the market.” Now, strategists at BofA Securities have identified a list of reasons why U.S. government bonds are exposed to the risk of “large scale forced selling or an external surprise” at a time when the bond market is in need of a reliable group of big buyers.

“We believe the UST market is fragile and potentially one shock away from functioning challenges” arising from either “large scale forced selling or an external surprise,” said BofA strategists Mark Cabana, Ralph Axel and Adarsh Sinha. “A UST breakdown is not our base case, but it is a building tail risk.”

In a note released Thursday, they said “we are unsure where this forced selling might come from,” though they have some ideas. The analysts said they see risks that could arise from mutual-fund outflows, the unwinding of positions held by hedge funds, and the deleveraging of risk-parity strategies that were put in place to help investors diversify risk across assets.

In addition, the events which could surprise bond investors include acute year-end funding stresses; a Democratic sweep of the midterm elections, which is not currently a consensus expectation; and even a shift in the Bank of Japan’s yield curve control policy, according to the BofA strategists.

The BOJ’s yield curve control policy, aimed at keeping the 10-year yield on the country’s government bonds at around zero, is being pushed to a breaking point.

Well. Bidenflation certainly isn’t helping, but Statist Economist and Cheerleader Janet Yellen can’t bring herself to blame green energy policies, rampant Federal spending or irresponsible Federal Reserve policies for the crisis.

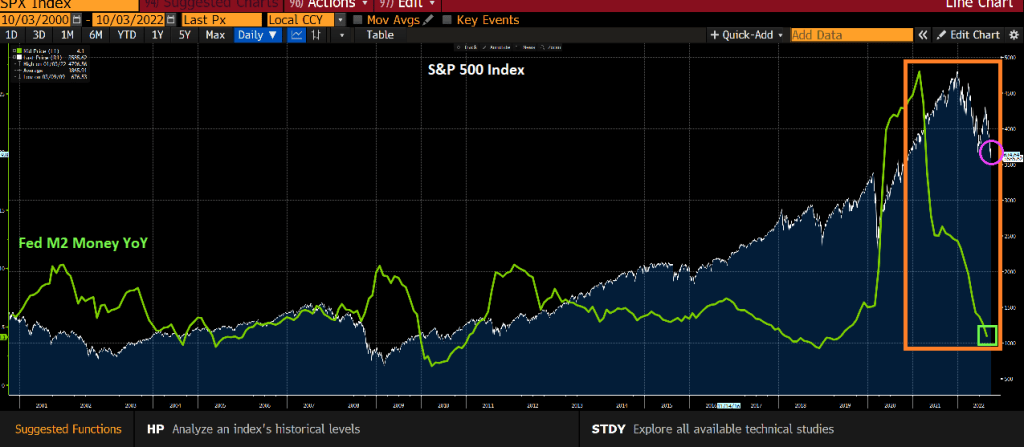

You will note the differences between today and the financial crisis of 2008-2009. The financial crisis gave us a massive surge in government securities liquidity thanks to then Fed Chair Ben Bernanke imitating Japan’s Central Bank and buying US government securities. Fast forward to today and the liquidity index hasn’t budged much since 2010 (except for a little blip around the Covid Fed intervention of early 2020), but we are now seeing near 40-year highs in inflation and a barely declining Fed balance sheet. And M2 Money YoY (mostly commercial bank deposits) are crashing.

I am guessing that The Fed will pivot given that stock futures are way up for Monday. The Dow Jones mini is up 770 points and the S&P 500 mini is up 88.75 points.

Bond market futures (specifically the US Ultra Bond) is down for Monday, meaning yields will be climbing.

I remember giving a speech at The Brookings Institute in Washington DC. Talk about stranger in a strange land. One person who I was debating got frustrated and said “You are such a … Republican!!!” As if that was the worst slur he could throw at me.

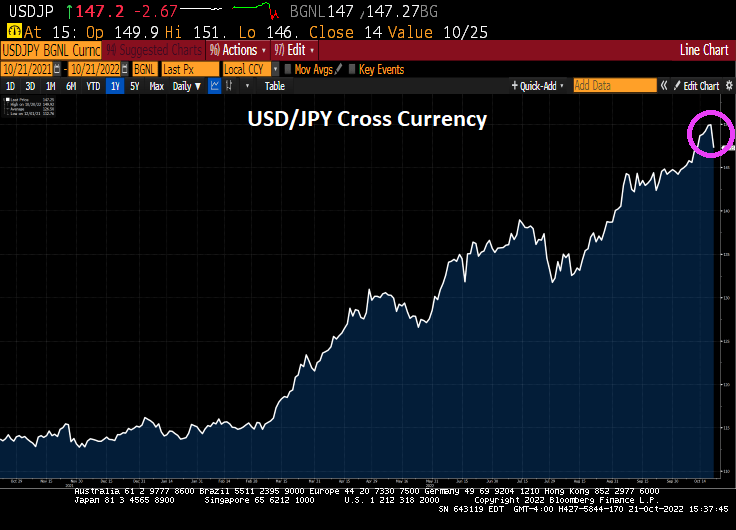

Wall Street saw another day of stunning reversals, with stocks rallying after a Treasury selloff sputtered. The yen jumped as Japan intervened again to prop up the currency.

After many twists and turns, the S&P 500 pushed solidly into the green and headed for its best week since June as 10-year yields fell from the highest since 2007.

Probably because The Fed is likely to pivot with impending recession. The Dow is up 774 points this Friday. And today was a huge option expiration day!!

And the 10-year Treasury yield fell -2.2 basis points.

Here is the result of Japan’s intervention.

But today’s numbers were largely monthly stock index option expiration.

Why did it fall upon Powell to be the wielder of the Fed tightening scimitar? Why didn’t Yellen? Because “Good Girls Don’t.” But Powell did.

Have a nice weekend. I will be rooting for Ohio State to annihilate the Iowa Hawkeyes at noon on Saturday.

As I frequently told my investment and fixed-income securities students at Chicago, Ohio State and George Mason University, any 10 basis point change in the US Treasury 10-year yield is significant.

But how about today’s 20 basis point decline in the US Treasury 10-year yield?

The UK’s 10-year yield is down even more at -24.1 basis points. Germany is down -18 bps and France is down -10.3 bps.

Speaking of credit default swaps, Credit Suisse is back to financial crisis levels while UBS and Deutsche Bank are not … yet.

With all the turbulence in markets thanks to the war in Ukraine and Biden’s green energy mandates and spending (not to mention Statists like Klaus Schwab screaming about a Great Reset), I was reminiscing about more simple times.

New CEO Koerner sought to reassure employees in Friday memo

Shares fall to a fresh record low, gauge of credit risk rises

It is like the Lehman Brothers debacle in 2008 all over again.

(Bloomberg) — Credit Suisse Group AG was plunged into fresh market turmoil after Chief Executive Officer Ulrich Koerner’s attempts to reassure employees and investors backfired, adding to uncertainty surrounding the bank.

The stock, which had already more than halved this year before Monday’s sell-off, fell as much as 12% in Zurich trading to a record low that values the firm at less than $10 billion. That was accompanied by a spike in the cost to insure the bank’s debt against default, which jumped to its highest ever.

Koerner, for the second time in as many weeks, had sought to calm employees and the markets with a memo late Friday stressing the bank’s liquidity and capital strength. Instead, it focused attention on the dramatic recent moves in the firm’s stock price and credit spreads, and investors rushed for the exit when trading reopened after the weekend.

One notable difference between 2008 and today is that Credit Suisse’s equity was flying high in June 2007 then crashed a the global banking crisis went into full motion. We then saw Credit Suisse’s credit default swaps soar in early 2009. But today Credit Suisse’s equity is a pale imitation of its former self, but its credit default swap is now higher than it was at its peak in early 2009.

Credit Suisse is now trading lower than its European rival Deutsche Bank (aka, The Teutonic Titanic).

Yes, this brings back sickening memories of the 2008-2009 global financial crisis. Let’s see how The Federal Reserve, ECB and Bank of Switzerland handle this debacle, particularly with M2 Money growth so low.

It appears that we are in another Lehman debacle. Or should I say “Lemur Bros.”

$32 TRILLION of global stock value has been wiped out since December 2021.

Today’s core PCE deflator reading of 4.9% YoY shows that the inflation surge is not over. With a core PCE deflator of 4.9%, the Taylor Rule suggests that The Fed Funds Target Rate should be at 9.65%, far below its current level of 3.25%. So, IFF The Fed is following any sort of rule, rates should continue to soar.

And if we use headline inflation of 8.30% YoY, the Taylor Rule suggests hiking the target rate to 14.75%.

The Federal government reaction to the Covid outbreak in early 2020 included massive monetary stimulus, Federal government spendathons and Biden’s green energy policies have resulted in a sizzling 8.5% inflation rate (update on Monday morning).

The problem is that The Federal Reserve is far behind the inflation curve with their target rate at only 2.5%. And The Fed’s balance sheet remains near $9 TRILLION in assets held.

In Euroland, we are seeing a similar problem (Frankfurt, we have a problem!). The Eurozone inflation rate is at 9.1% while their version of The Fed Funds Target rate is only 0.75%, a large catch-up gap.

If we look at the Taylor Rule for the US using headline inflation, we see that The Fed needs to raise their target rate to … 21.72% to crush inflation.

In Euroland, the problem is similar. At 9.10% inflation, the ECB will have to raise their version of The Fed’s target rate to 16.80% to combat inflation. As if that will happen in either the US or Euroland.

On a different note, is it my imagination or does US Democrat Senate candidate from Pennsylvania John Fetterman look like the alien from the flick “Battleship”?

Just remember, the US economy had strong employment figures just prior to the 2008 Great Recession and financial crisis, so US Treasury Secretary Yellen, Biden’s economic cheerleader Bernstein and Obama’s economic cheerleader Sperling are all relying on a bad indicator of economic health to justify that the US economy is in great shape.

(Bloomberg) — Treasury Secretary Janet Yellen expressed confidence in the Federal Reserve’s fight against inflation and said she doesn’t see any sign that the US economy is in a broad recession.

“We’re likely to see some slowing of job creation,” Yellen said on NBC’s “Meet the Press” on Sunday. “I don’t think that that’s a recession. A recession is broad-based weakness in the economy. We’re not seeing that now.”

With US consumer prices rising at the fastest rate in four decades, a growing number of analysts say it will take a recession and higher joblessness to ease price pressures significantly. The Federal Reserve raised rates in June by the most since 1994 and is expected to approve another 75 basis-point hike this week.

Inflation is “way too high,” Yellen said, while renewing the Biden administration’s argument that it’s also high in many other advanced economies.

“The Fed is charged with putting in place policies that will bring inflation down,” said Yellen, a former Fed chair. “And I expect them to be successful.”

Dammit, Janet. All of Biden’s anti-fossil fuel orders are still in place and Biden/Pelosi/Schumer are still trying to pass the highly-inflationary Build Back (Inflation) Better bill. And The Fed still has not shrunk it massive balance sheet yet.

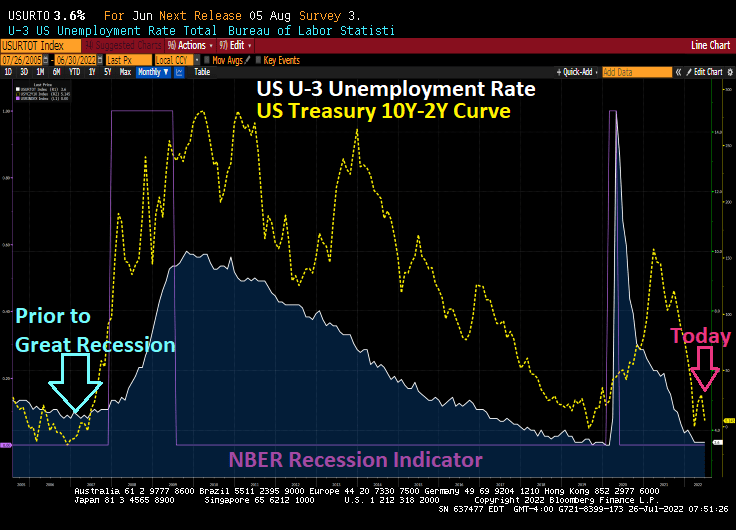

But Janet, the US Treasury 10Y-2Y yield curve remains inverted (historically ahead of a recession) while the Atlanta Fed GDPNow Q2 tracker is at -1.6% which would make the second quarter in a row of negative real GDP growth in a row (historically a definition of recession).

My preferred 10Y-2Y chart shows the yield curve more inverted than even prior to The Great Recession!

But in Yellen’s defense, The Fed’s preferred yield curve (implied yield on 3-month T-Bills in 18 month – 3 month T-Bill yield) is still positive, though crashing like a paralyzed falcon.

So, the Biden administration is sticking to the strong labor market story. But what the Biden Administration (and Yellen) fail to acknowledge is 1) unemployment is a lagged indicator of a recession (unemployment was low prior to the 2008 GREAT recession, then exploded and 2) there is still a tremendous amount of monetary stimulus outstanding that The Fed has taken away … yet.

Essentially, the Biden Administration is panicking over the coming mid-year election and will say anything at this point to stay in power. So, I would probably ignore anything said by Biden, Yellen and their talking heads before the midterms elections. But when Biden’s economic advisor says that the US economy is strong, I want to ask him how having NEGATIVE wage growth is a good thing,

Let’s see if Yellen is correct and The Fed’s Fireball will tame inflation. Frankly, I think the global slowdown is the only thing that will tame inflation.

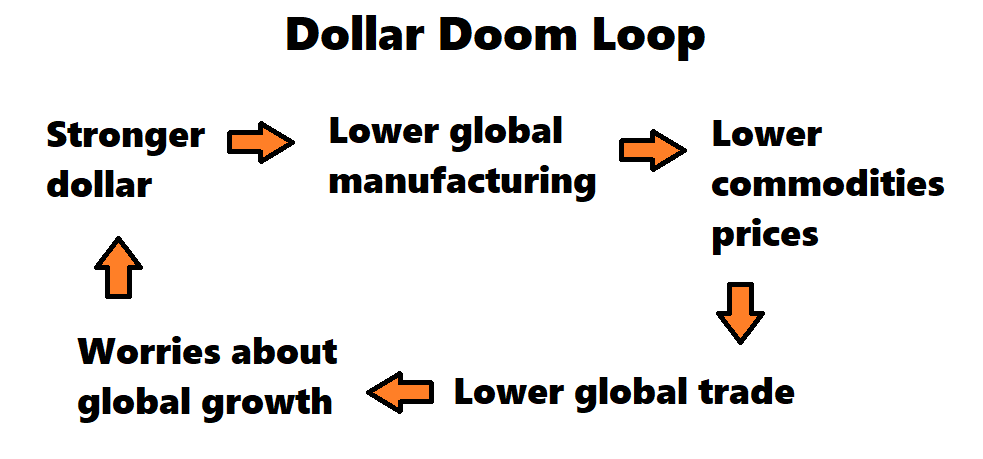

The dollar’s gain is the world’s pain — and based on its current trajectory, the world may be in for a whole lot more discomfort.

Concerns over global growth have recently sent the US Dollar Index to the strongest level on record, with the greenback hitting multi-decade highs against currencies like the euro and the yen.

But the move risks becoming a self-reinforcing feedback loop given that the vast majority of cross-border trade is still denominated in dollars, and a stronger US currency has historically translated into a broad hit to the world economy.

Against the backdrop of higher-than-expected inflation and still-elevated commodities prices, the concern is that we’re in for a dollar ‘doom loop’ like never before, according to Jon Turek, the founder of JST Advisors and author of the Cheap Convexity blog.

With the Federal Reserve hiking interest rates at the fastest pace in decades, he says, it’s much less clear what could break the feedback loop in the next few months.

The Dollar Doom Loop with US inflation causing The Fed to tighten

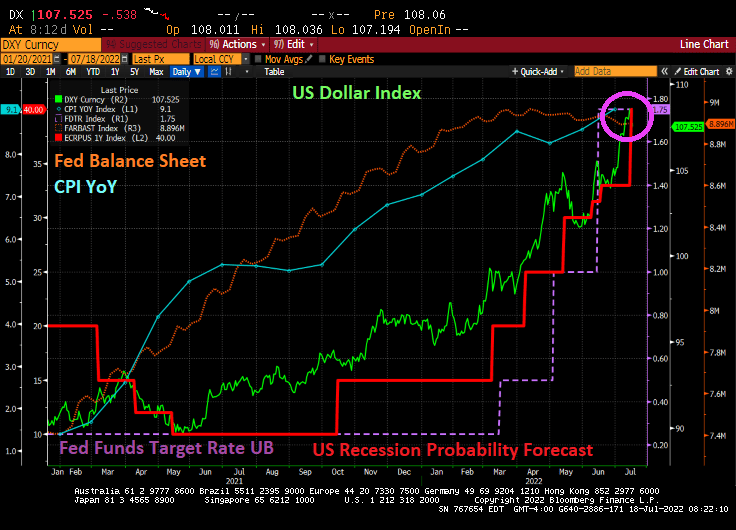

Under Biden’s policies, inflation hit a 40-year high (blue line), and the US Dollar (green line) is strengthening. Then we have The Fed raising the target rate (purple line) and the probability of recession rising with Fed tightening.

Is a US recession coming? The US Treasury 10Y-2Y yield curve is inverted at almost -20 basis points.

There is a Fed open market committee meeting in one week and they are expected to raise their target rate by 75 basis points according to Fed Fund Futures data. Inflation keeps rising as does the probability of a US recession. So, The Fed will keep on tightening.

You must be logged in to post a comment.