1. Everybuddy: 100% of workforce 2. Wisense: 100% of workforce 3. CodeSee: 100% of workforce 4. Twig: 100% of workforce 5. Twitch: 35% of workforce 6. Roomba: 31% of workforce 7. Bumble: 30% of workforce 8. Farfetch: 25% of workforce 9. Away: 25% of workforce 10. Hasbro: 20% of workforce 11. LA Times: 20% of workforce 12. Wint Wealth: 20% of workforce 13. Finder: 17% of workforce 14. Spotify: 17% of workforce 15. Buzzfeed: 16% of workforce 16. Levi’s: 15% of workforce 17. Xerox: 15% of workforce 18. Qualtrics: 14% of workforce 19. Wayfair: 13% of workforce 20. Duolingo: 10% of workforce 21. Rivian: 10% of workforce 22. Washington Post: 10% of workforce 23. Snap: 10% of workforce 24. eBay: 9% of workforce 25. Sony Interactive: 8% of workforce 26. Expedia: 8% of workforce 27. Business Insider: 8% of workforce 28. Instacart: 7% of workforce 29. Paypal: 7% of workforce 30. Okta: 7% of workforce 31. Charles Schwab: 6% of workforce 32. Docusign: 6% of workforce 33. Riskified: 6% of workforce 34. EA: 5% of workforce 35. Motional: 5% of workforce 36. Mozilla: 5% of workforce 37. Vacasa: 5% of workforce 38. CISCO: 5% of workforce 39. UPS: 2% of workforce 40. Nike: 2% of workforce 41. Blackrock: 3% of workforce 42. Paramount: 3% of workforce 43. Citigroup: 20,000 employees 44. ThyssenKrupp: 5,000 employees 45. Best Buy: 3,500 employees 46. Barry Callebaut: 2,500 employees 47. Outback Steakhouse: 1,000 48. Northrop Grumman: 1,000 employees 49. Pixar: 1,300 employees 50. Perrigo: 500 employees

But, according to the government-supplied data…

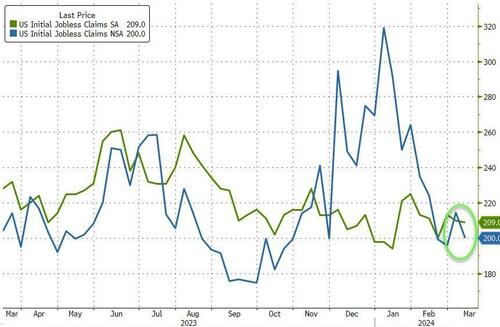

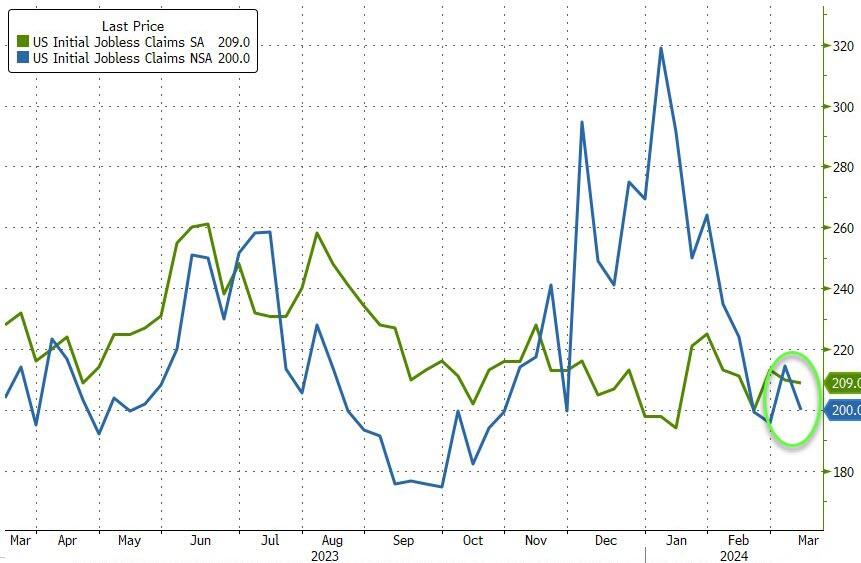

The number of American filing for jobless benefits for the first time last week dropped to 209k (vs 218k exp) with the NSA number tumbling to 200k…

Source: Bloomberg

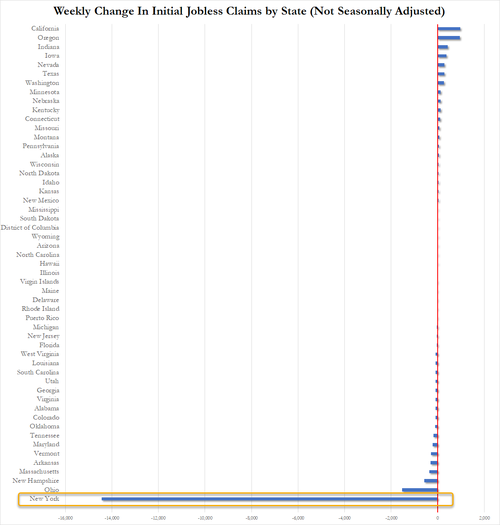

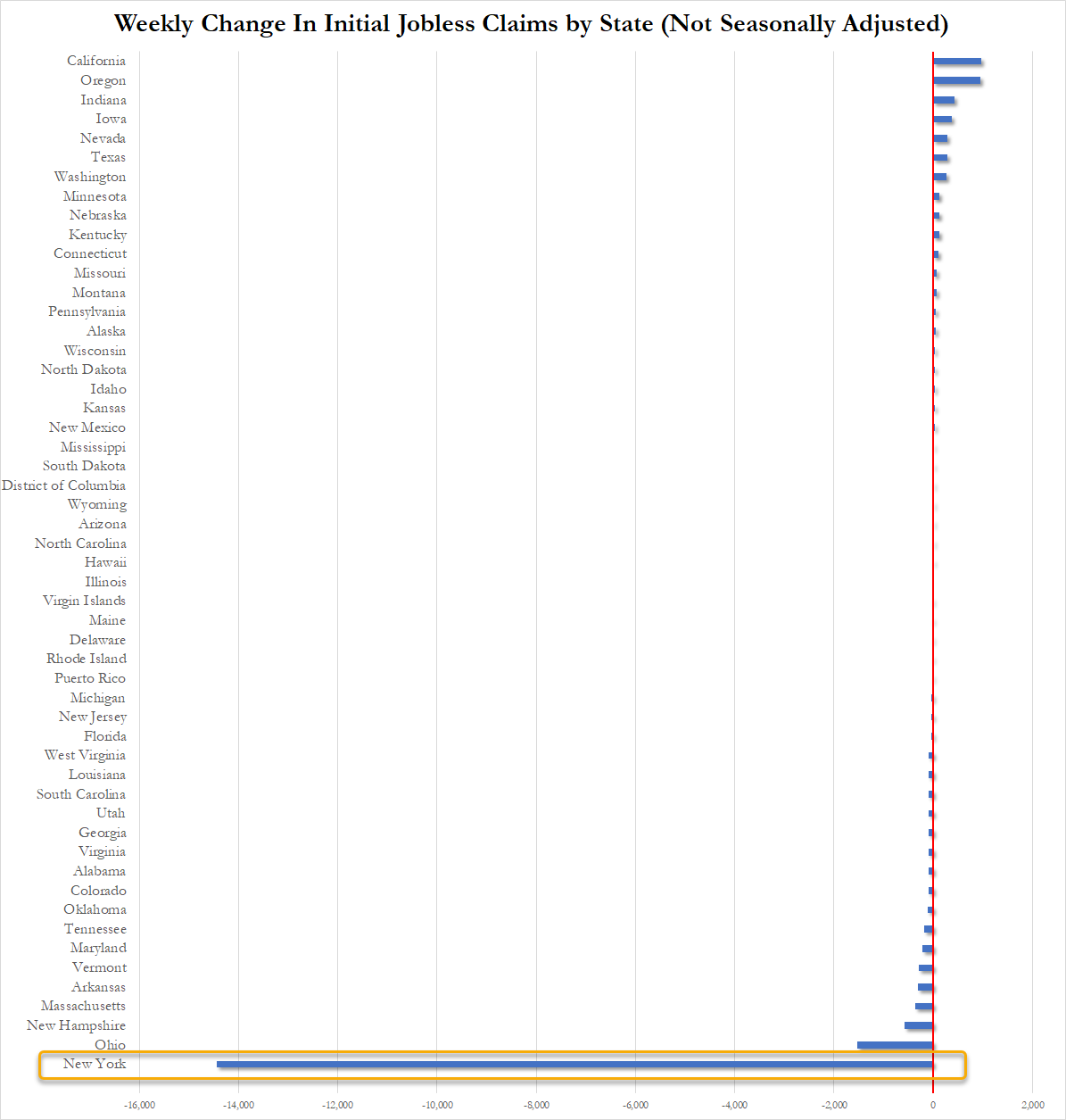

How is this possible, you may ask… well let us show you the ways… New York State claims that its jobless benefits rolls collapsed last week. New York accounted for 99.75% of the weekly change in initial claims across the entire US as shown below…

Source: Bloomberg

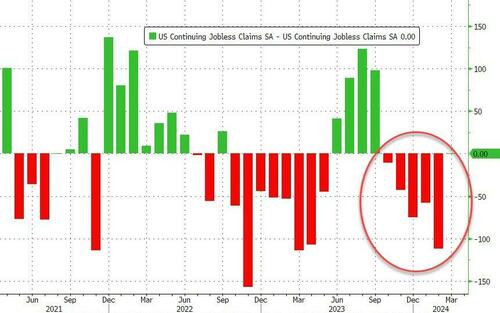

Continuing Claims was a shit show – with a massive 112k person downward revision for last week from 1.906 million to 1.794mm. That is the 5th straight weekly downward revision of continuing claims…

Source: Bloomberg

But thanks to the adjustments, it all looks ‘normal’ and ‘stable’ at around 1.8 million Americans…

Source: Bloomberg

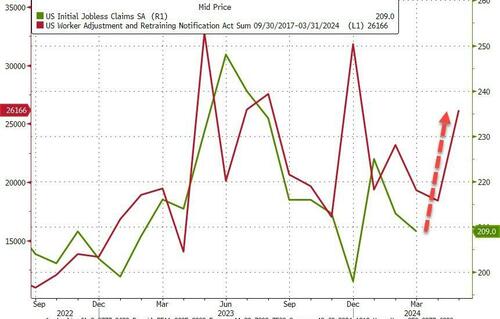

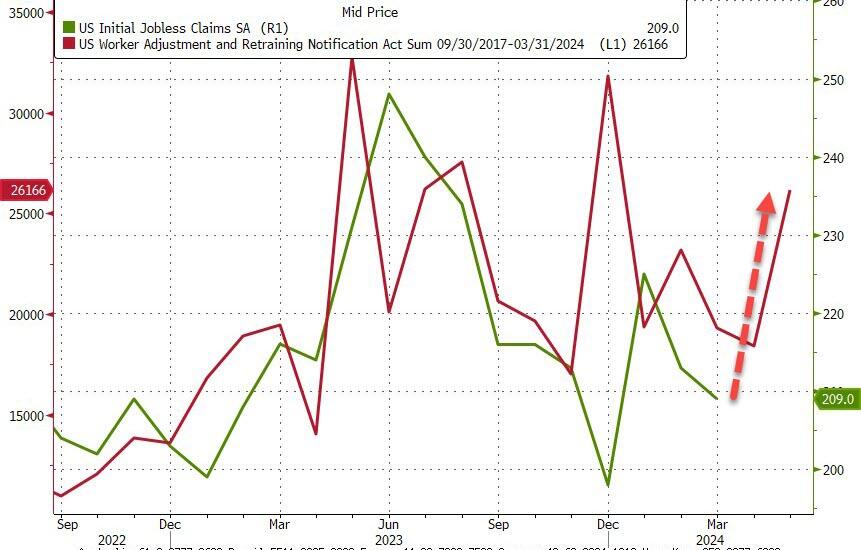

And WARN numbers are rising rapidly…

Source: Bloomberg

As a reminder, if you doubt the accuracy of the Biden admin’s data, here’s what the most recent FOMC Minutes said:

“While the recent trends prior to the meeting had been remarkably positive, Fed officials judged that some of the recent improvement “reflected idiosyncratic movements in a few series.”

Even they aren’t buying it, and neither should you!

Unlike what Grand-dad Joey Biden screamed at the State of The Union (SOTU) address, inflation is NOT been defeated. In fact, inflation has defeated Biden and The Federal Reserve.

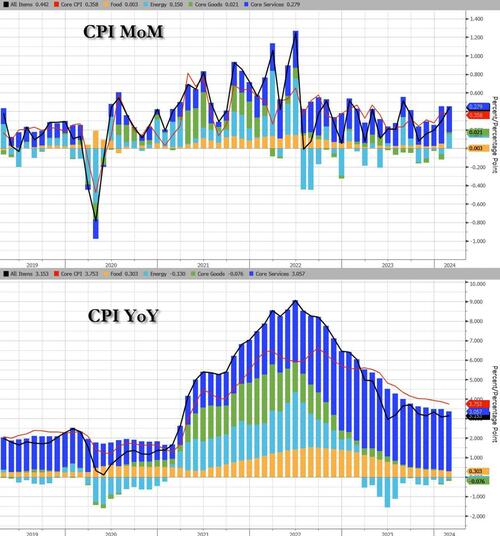

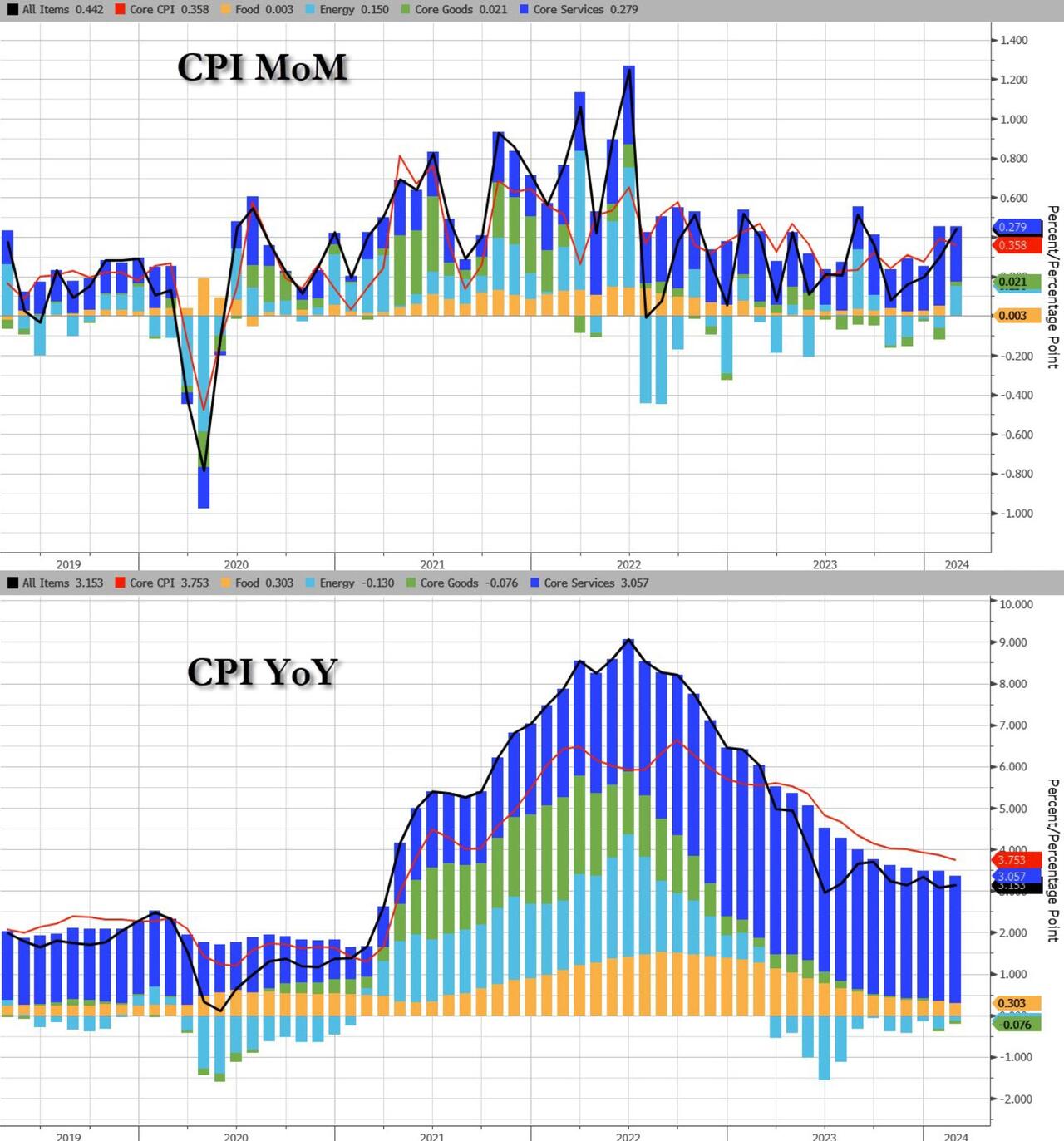

The 3-month annualized CPI rate was rose to 2.8% from 1.9%. The 6-month annualized core rate dropped to 3.2% from 3.3%.

Energy costs surged MoM as Core Services inflation slowed MoM…

Source: Bloomberg

Full CPI MoM breakdown:

The index for all items less food and energy rose 0.4 percent in February, as it did the previous month.

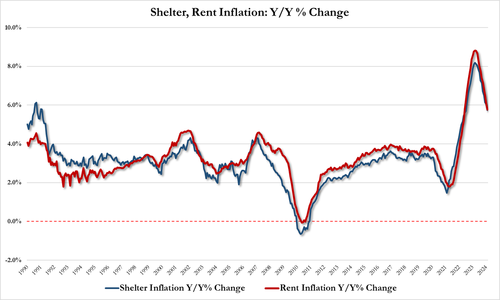

The shelter index increased 0.4 percent in February and was the largest factor in the monthly increase in the index for all items less food and energy.

The index for rent rose 0.5 percent over the month, while the index for owners’ equivalent rent increased 0.4 percent.

The lodging away from home index increased 0.1 percent in February, after rising 1.8 percent in January.

The airline fares index rose 3.6 percent in February, following a 1.4-percent increase in January.

The index for motor vehicle insurance increased 0.9 percent over the month.

The medical care index was unchanged in February after rising 0.5 percent in January.

The index for hospital services decreased 0.6 percent over the month and the index for physicians’ services decreased 0.2 percent.

The prescription drugs index fell 0.1 percent in February.

The index for dental services was among those that rose in February, increasing 0.4 percent.

The index for personal care fell 0.5 percent in February, following a 0.6-percent increase in January.

The household furnishings and operations index fell 0.1 percent over the month, as did the new vehicles index.

Among other indexes that rose in February were apparel, recreation, and used cars and trucks.

Full CPI YoY breakdown:

The index for all items less food and energy rose 3.8 percent over the past 12 months.

The shelter index increased 5.7 percent over the last year, accounting for roughly two thirds of the total 12-month increase in the core CPI index

Feb Shelter inflation: 5.74% down from 6.04% in Jan

Feb rent inflation: 5.77%, down from 6.09% in Jan

Other indexes with notable increases over the last year include motor vehicle insurance (+20.6 percent), medical care (+1.4 percent), recreation (+2.1 percent), and personal care (+4.2 percent).

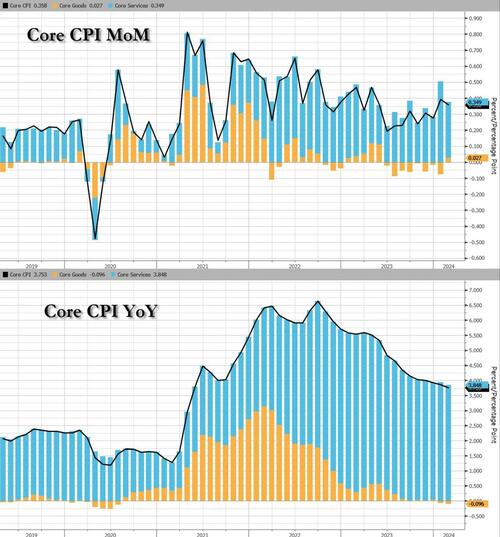

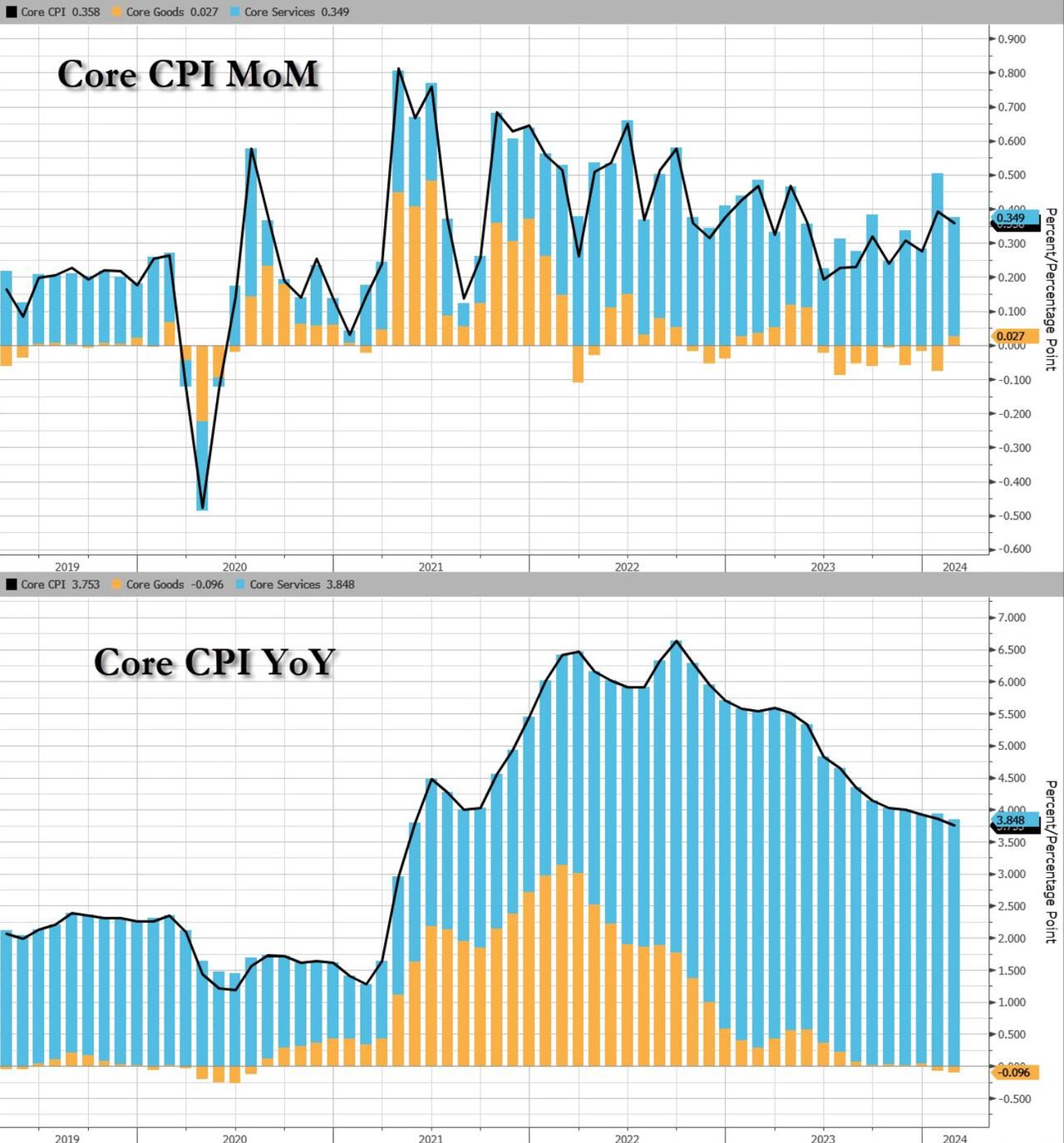

Core CPI rose 0.4% MoM (hotter than the +0.3% exp) and up 3.8% YoY (hotter than the +3.7% exp), but still the lowest since April 2021…

Source: Bloomberg

The 3-month annualized Core CPI rate was rose to 4.1% from 3.9%. The 6-month annualized core rate rose to 3.8% from 3.5%.

Core Goods actually rose MoM for the first time since June 2023…

Goods deflation continues (-0.3% YoY) but has flattened out, while services inflation remains stubbornly high at +5.2% YoY…

Source: Bloomberg

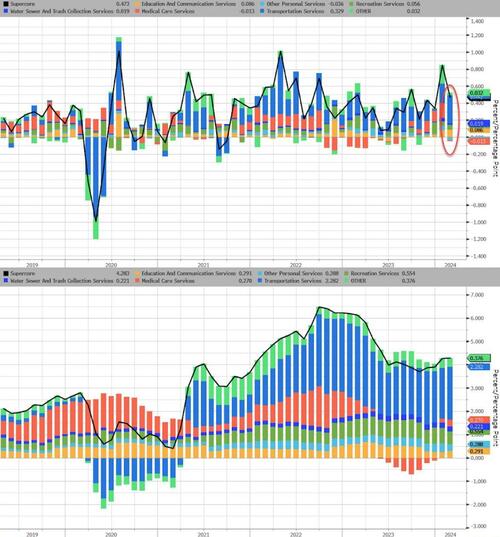

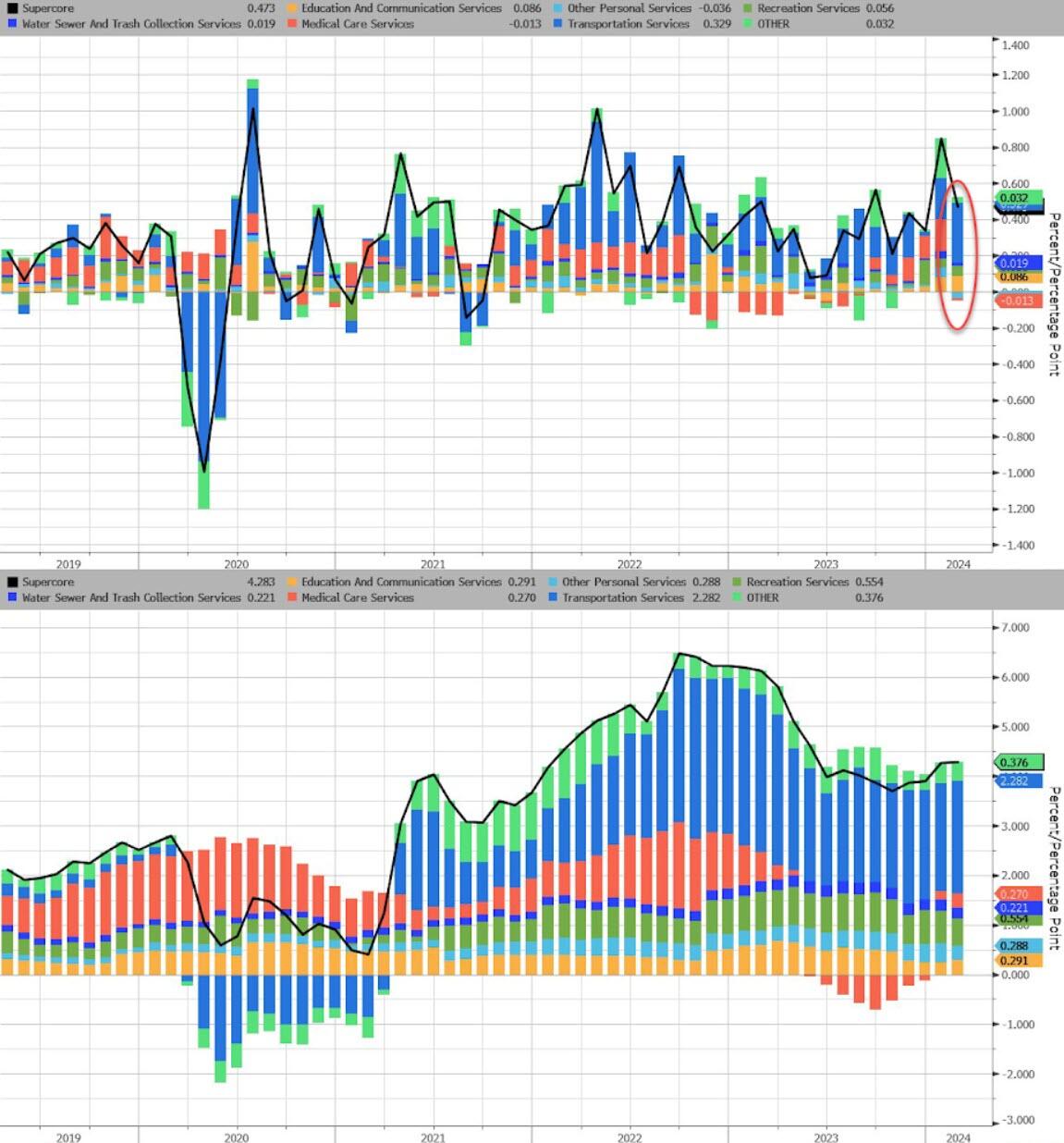

And one step deeper – the so-called SuperCore: Core CPI Services Ex-Shelter index – soared 0.5% MoM up to 4.5% YoY – the hottest since May 2023…

Source: Bloomberg

While SuperCore CPI slowed MoM, there was a large jump in Transportation Services MoM…

Source: Bloomberg

Finally, we note that consumer prices have not fallen in a single month since President Biden’s term began (July 2022 was the closest with ‘unchanged’), which leaves overall prices up 19% since Bidenomics was unleashed. And prices have never been more expensive…

Source: Bloomberg

That is an average of 5.6% per annum (more than triple the 1.9% average per annum rise in price during President Trump’s term).

So, about that shrinkflation – did companies only ‘get greedy’ when Biden took office?

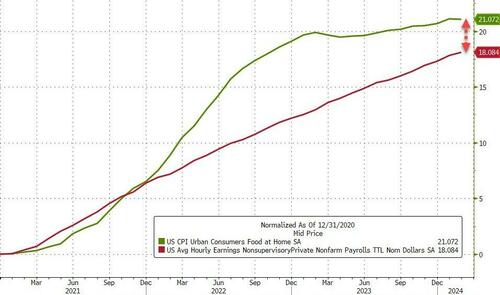

But it gets worse, real wage growth has lagged significantly for the average joe in America…

Source: Bloomberg

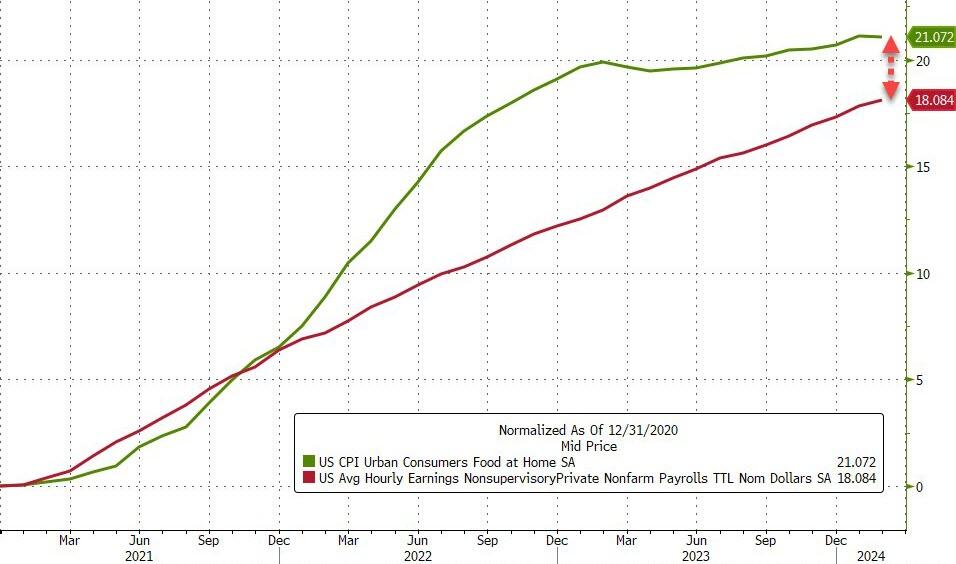

Despite a very modest decline in Feb, Food costs are up over 21% since Biden’s term began, but non-supervisory wages are up only 18%.

Bidenomics for the win!

Are we going to see a replay on the ’70s?

Source: Bloomberg

The market narrative of slow and steady disinflation just broke harder.

…or are we still set for a massive wave of depressionary deflation?

Inflation remains hot, hot, hot although Biden/Yellen will undoubtedly say that it is lower than last year. But remember, consumer prices are up a staggering 19% under Bidenomics. THAT is a major tax of those making under $200,000 per year, Joey.

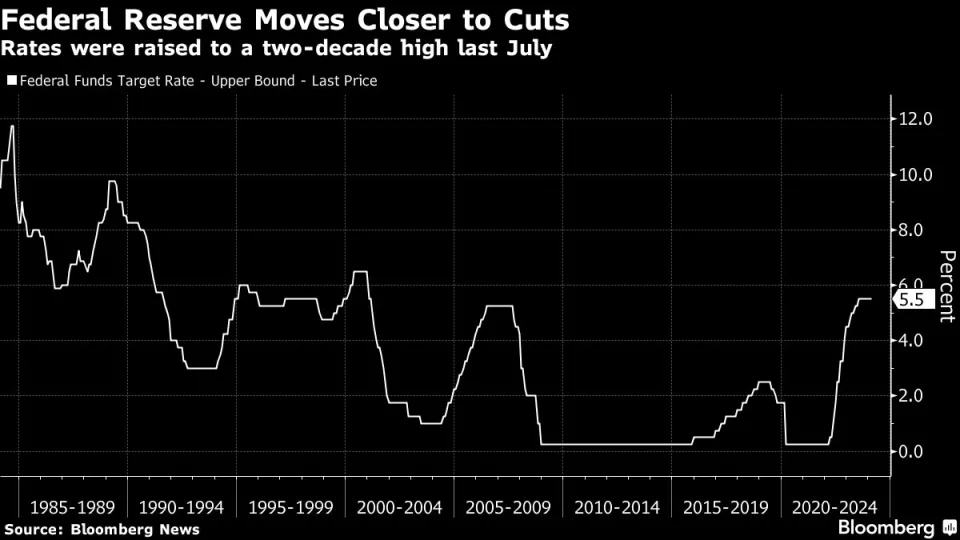

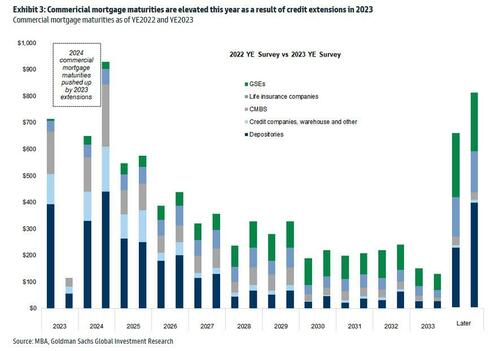

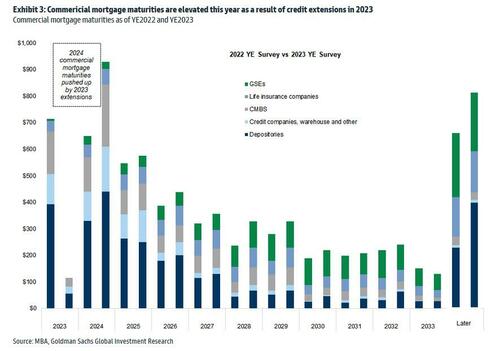

Holders of commercial real estate (CRE) debt are riding the tiger. Meaning that if interest rates don’t come down, there will be a lot of pain and suffering.

“We’re far from neutral now,” said America’s Fed Chairman, Jerome Powell, to the Senate Banking Committee. As The Fed moves closer to cutting rates.

All those rent-seekers stacked up with commercial real estate holdings nodded in violent agreement. That of course includes the nation’s regional banks, which continue to succumb to the power of their systemically important rivals, now so big that they cannot possibly be allowed to fail.

And this has turned America’s banking behemoths into for-profit wards of the state, recipients of an unspoken but ironclad insurance policy that underwrites catastrophic losses and adds them to the national debt.

“Interest rates right now are well into restrictive territory. They’re well above neutral,” added Chairman Powell without, well, sharing his definition of the word ‘well’. And truth be told, no one really knows the definition of ‘neutral’ when it comes to interest rates.

Economic PhDs will generally tell you that the neutral real interest rate is 0.50%. Their level of confidence is inversely proportional to the amount of capital they have at risk in markets — which would have been Newton’s Fourth Law had he bothered to study the art of economics.

Those of us less academically gifted, who must resort to taking risk for a living, lack the conviction of Nobel Laureates. We see that there are times in an economic cycle when 0.50% real rates stimulate growth, and times when they restrict economic activity.

Sometimes neutral rates have no effect at all. Which is to say that the economic impact of real rates simply depends. Like now when signals are far from uniform. Stock markets hit all-time highs despite collapsing commercial real estate, crypto and gold prices are soaring to records, massive government stimulus programs like the IRA are cranking up, student debt is being forgiven in successive waves, unemployment is near record lows, core inflation is starting to rise again, and the budget deficit is around 6% despite robust GDP growth.

All of which screams that a 0.50% real rate is preposterously low to everyone but economic PhDs.

After witnessing the debacle called “The State of the Union Address” or “Crazy Grandfather Screams At Nation To Get Off His Lawn,” I was hoping that today’s jobs report would make me happier. It didn’t. In fact, the February jobs report was downright awful.

Maybe now you can understand why Biden gave his angry SOTU speech. Perhaps he saw how bad February’s jobs report was for Middle class America and was trying to redirect the rage away from himself towards the Supreme Court, MAGA Republicans, corporate America (his biggest donors?), and the 6 year old that walked across The White House Lawn uninvited.

Well, if a $73 billion dollar deficit isn’t bad enough, the California State Assembly took a giant step towards bankruptcy by … seriously … A controversial bill that would let illegal immigrants receive the same kind of homebuyer assistance as U.S. citizens has advanced in the California state legislature, drawing criticism from those who object to granting perks to people who break the law by entering the country illegally.

The measure, Assembly Bill 1840, was first introduced in mid-January, and after several amendments, it advanced last week to the Committee on Housing and Community Development, where it awaits further action.

Assembly Bill 1840 would change existing law to allow illegal immigrants to be eligible for the California Dream for All Fund, which provides interest-free loans for a down payment on a home for first-time buyers.

The bill was introduced by California Assemblyman Joaquin Arambula, a Democrat, who last month told GV Wire, a Fresno-based news outlet, that he “wanted to ensure that qualified first-time homebuyers include undocumented applicants.” (Note to Arambula: According to Redfin, there are no homes for $150,000 or less.

Last week, as the bill advanced to committee after amendments, Mr. Arambula told the Los Angeles Times that, historically, homeownership has been the main way people accumulate generational wealth in the United States.

“The social and economic benefits of homeownership should be available to everyone,” he said, arguing that it’s wrong to exclude people from the benefits of the California Dream for All Fund program just because they’re illegal immigrants.

Some lawmakers expressed opposition to the measure as it moves closer to becoming law.

“Assembly Bill 1840 is an insult to California citizens who are being left behind and priced out of homeownership. I’m all for helping first-time homebuyers, but give priority to those who are here in our state legally,” California Sen. Brian Dahle, a Republican, said in a post on X, formerly Twitter.

More Details

The California Dream for All Fund program, administered by the state’s Housing Finance Agency, provides loans for 20 percent of a home’s value but no greater than $150,000. (Good luck finding a house in Los Angeles for under $150,000!) Here is a home in Chico California for $55,000!

Qualifying homebuyers repay the loans when selling or transferring the property plus 20 percent of any appreciation in its value. Applicants who earn less than their county’s area median income get a slight break, having to pay 15 percent of the appreciation. If a home doesn’t appreciate in value, only the principal will be paid back, meaning the loan is technically interest-free.

To make matters worse, Los Angeles housing prices are up 33% under China Joe Biden and California Governor Gavin Newsom. NOW they want to drive housing into even more unaffordable territory with allowing illegal immigrants to buy a home with 100% loan-to-value (100% LTV and NO INTEREST!).

The proposed bill seeks to amend Section 51523 of the California Health and Safety Code to include a subsection that reads: “An applicant under the program shall not be disqualified solely based on the applicant’s immigration status.”

Mr. Arambula has defended the program, arguing in the interview with GV Wire last month that it won’t affect the state budget because the loans are supposed to be paid back with an appreciation fee.

Even though the net impact of the program on the state budget is technically neutral-to-positive, some critics argue that it sends the wrong message and effectively rewards illegal immigration.

“We have a huge housing crisis in California and anything we can do to get people into housing we should do. However, we should help our own first. This next generation of people growing up can’t afford a house. I’ve got two kids in their early 30s and most of their friends do not own houses,” San Diego County Supervisor Jim Desmond, a Republican, told NBC 7 San Diego.

Mr. Desmond has been a vocal critic of policies that he says create incentives for people to enter the country illegally.

“You incentivize illegal immigration by providing free healthcare, free unemployment benefits and tons of other freebies,” he wrote in a recent post on X, reacting to a post by California Gov. Gavin Newsom, a Democrat, who called on Congressional Republicans to back President Joe Biden’s border deal.

“It’s no wonder we are getting thousands of people by the day. This is on you as much as the Federal Government,” Mr. Desmond added.

Mr. Desmond said on March 3 that over 5,000 illegal immigrants had been released in San Diego County over the past 10 days.

“What’s striking about the people being dropped here by the Border Patrol is about 70 percent of them are single males,” he told Fox News.

While many of the new arrivals are being taken to the airport by local nongovernmental organizations to fly out to someplace else in the country, Mr. Desmond lamented that “in the meantime, our airport is now the new migrant shelter.”

His remarks come as the United States remains in the throes of an illegal immigration crisis of historic proportions, with some border patrol officials and others warning of a national security risk.

Military-Aged Men Crossing Border

The head of the Border Patrol union recently warned about the sharp rise in the number of military-aged Chinese men crossing the U.S.–Mexico border illegally.

National Border Patrol Council President Brandon Judd said in a recent interview on “Just the News, No Noise” TV program that he believes some of them may be spies working on behalf of China’s communist regime to infiltrate the United States.

“At best, they’re here for a better life,” Mr. Judd said. “At worst, they’re here to be part of the Chinese government to infiltrate our own country.”

Buses drop off large groups of illegal immigrants in San Ysidro, Calif., on Feb. 29, 2024. (John Fredricks/The Epoch Times)

His remarks came as U.S. Customs and Border Protection (CBP) released its latest data for January encounters with illegal immigrants who crossed the border into the United States.

Aside from showing that Border Patrol agents encountered a record number of illegal immigrants (242,587) in January 2024 compared to any previous January, the CPB numbers show an alarming trend in the number of military-aged Chinese nationals entering the country illegally.

Border Patrol agents encountered 5,717 single Chinese adults in January, more than twice the number of any other January on record, CBP data shows. In December 2023, that figure rose to a record of 7,581, while the total since January 2023 stands at 64,979.

Some analysts say that deteriorating economic conditions in China, along with human rights abuses and policies such as strict COVID-19 lockdowns, are likely driving the increase.

The San Diego Sector has seen a more than 500 percent jump in the number of Chinese nationals entering the country illegally, according to Jason Owens, the chief of the U.S. Border Patrol.

We are living in a banker’s paradise. Where a top administrative official pushes to change forecasts of the economy. Hey, it’s a Presidential election year and literally anything goes.

The disagreement was over forecasts for 10-year Treasury yields in the budget, a linchpin estimate that is intertwined with other measures, like debt service costs.

Forecasts in the president’s budget proposal — scheduled for release Monday — are typically set by Treasury Secretary Janet Yellen, Office of Management and Budget Director Shalanda Young and the chair of the Council of Economic Advisers, Jared Bernstein. The group is known in fiscal circles as the troika.

An October meeting, however, included a fourth invited principal: Brainard, who directs the National Economic Council. Brainard at one point disagreed with Yellen, Young and Bernstein on the 10-year interest rate projections and predicted a slightly lower rate, the people said, speaking on condition of anonymity to detail the discussions.

The difference between the forecasts was modest and both were well within range of private-sector estimates, the people said. The exact scope of Brainard’s changes aren’t clear.

Brainard’s forecast painted a modestly better picture for Biden. A lower interest-rate forecast would have the effect of an improved overall outlook by offering more support for growth and suggesting less concern about inflation. It also would lower borrowing cost projections at a time of rising worries about the US deficit and debt.

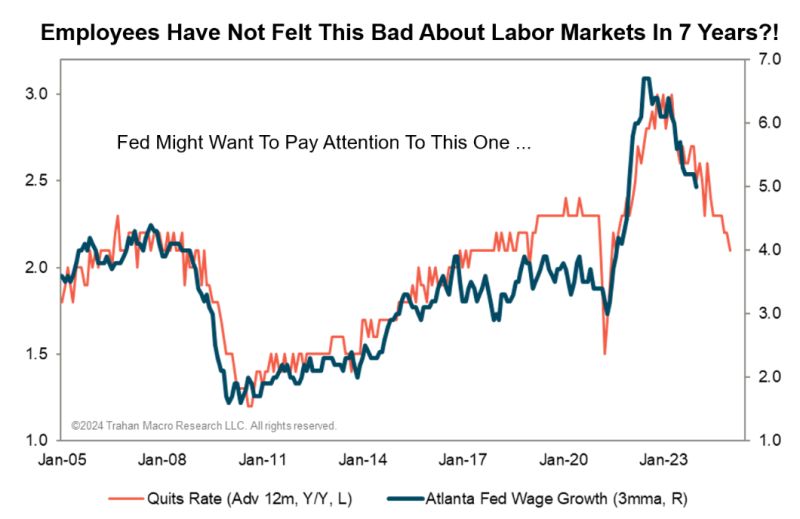

Let’s see what the Troika have to say about the quits rate.

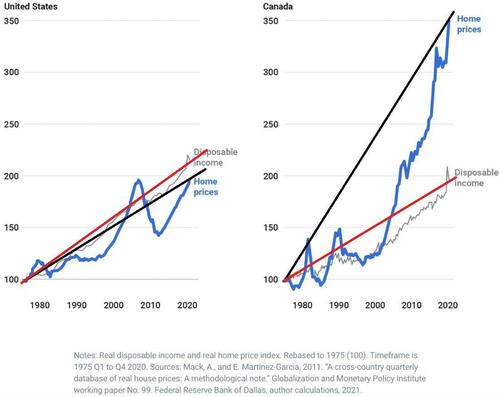

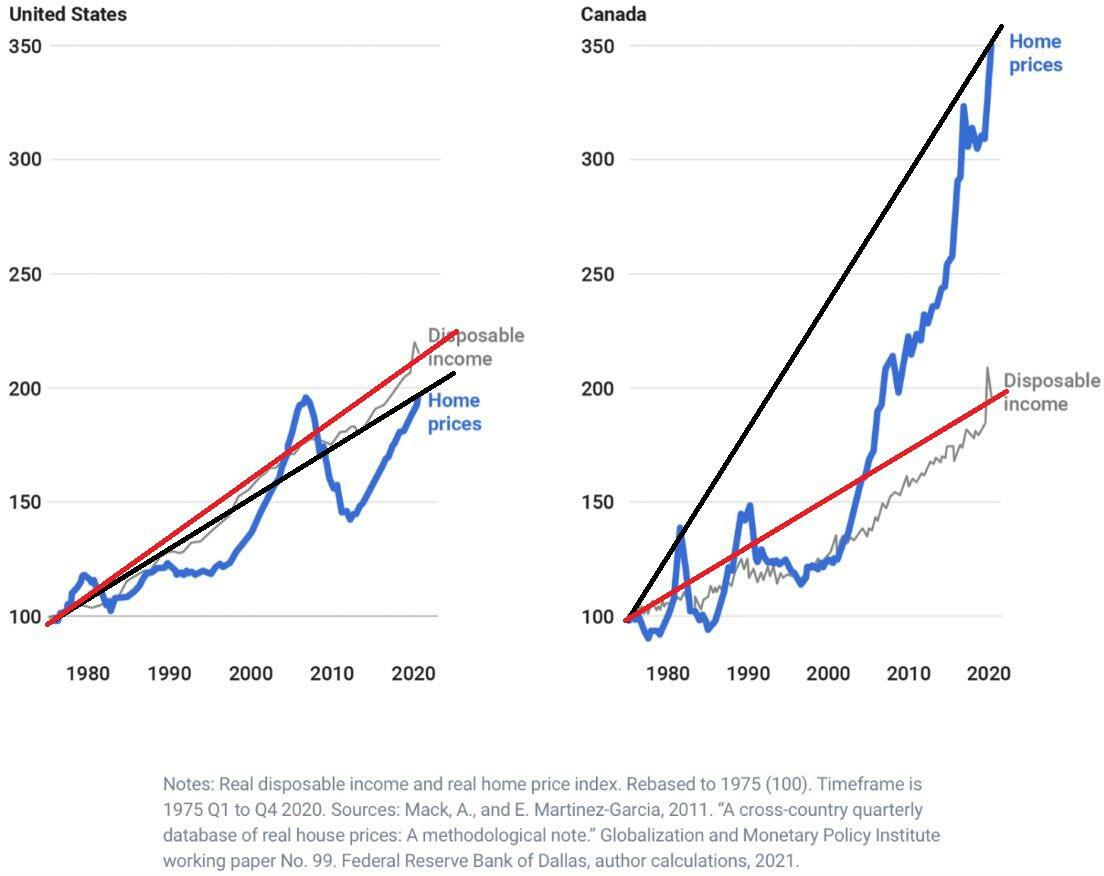

Housing is simply unaffordable for millions of Americans. Home prices are up 33% under Biden’s Reign of Error, while mortgage rates are up 146% under Vacation Joe. Somehow I doubt if Biden will brag about home prices and mortgage rate in his State of the Union address.

On the mortgage side, the Market Composite Index, a measure of mortgage loan application volume, increased 9.7 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index increased 12 percent compared with the previous week. The seasonally adjusted Purchase Index increased 11 percent from one week earlier. The unadjusted Purchase Index increased 13 percent compared with the previous week and was 8 percent lower than the same week one year ago.

The Refinance Index increased 8 percent from the previous week and was 2 percent lower than the same week one year ago.

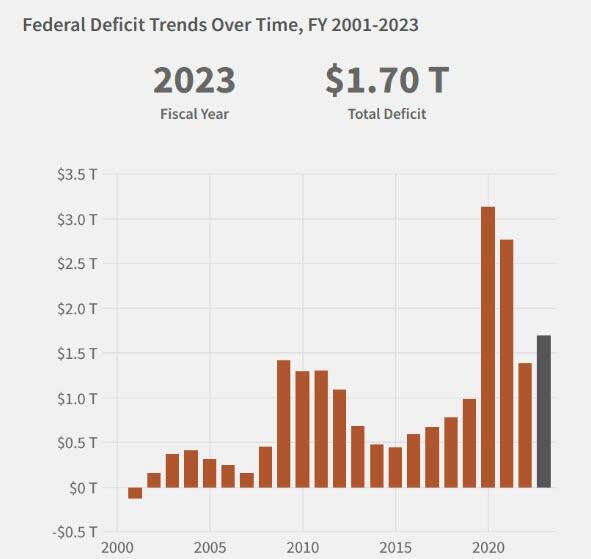

Too much debt! US politicians are spending too much money and borrowing too much. Unfortunately, that is what Biden and Bidenomics is all about: Federal targeted spending and loads of debt.

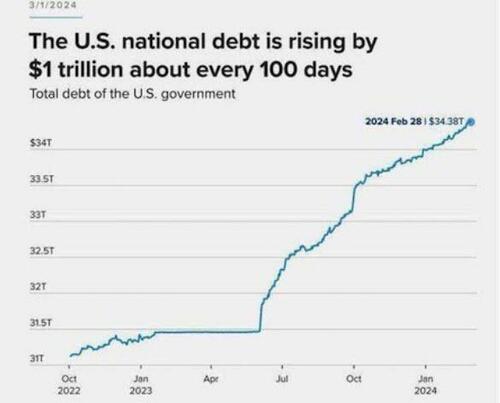

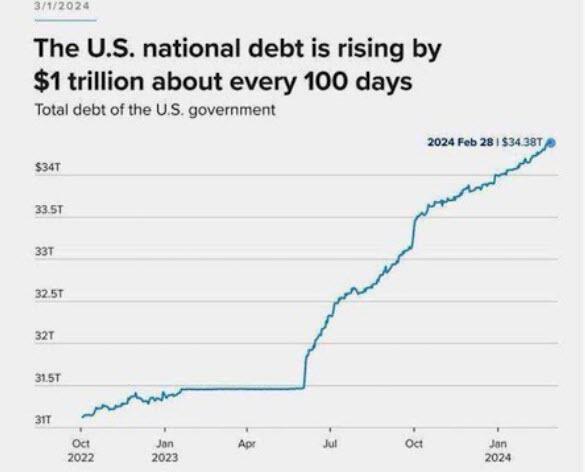

Now it requires $1 trillion of new debt every 100 days to achieve nothing but remaining static economically. The regime media pundits and the cabal on Wall Street tell us the economy is doing great. No recession in sight. All is well. The dumbed down and distracted ignorant masses don’t realize all the reported “economic growth” is “created” by the government, enabled by The Fed, spending billions on their wars in Ukraine and the Middle East, funneling the money into the Military Industrial Complex corporations; paying for the transportation, feeding, and housing of the illegal invading hordes; hiring more government drones to harass the citizenry, and desperately trying to prop up a corrupt tottering empire in its final death throes.

Anyone with even the slightest mathematical acumen knows increasing the national debt at a rate of $1 trillion every 100 days is a death wish. Why would those pulling the strings behind the scenes of this acceleration towards the cliff of national suicide be doing so at this point in time? It’s almost as if the November elections are a deadline for them to complete their exit strategy plan.

I believe we are entering the Great Taking phase of this clown show.

They are purposely creating a global financial disaster in order to take everything you and I have. It sounds crazy, but so is adding $1 trillion of debt every 100 days.

Cash on the barrelhead. To pay for outrageous inflation and food prices under Joe “Nero” Biden.

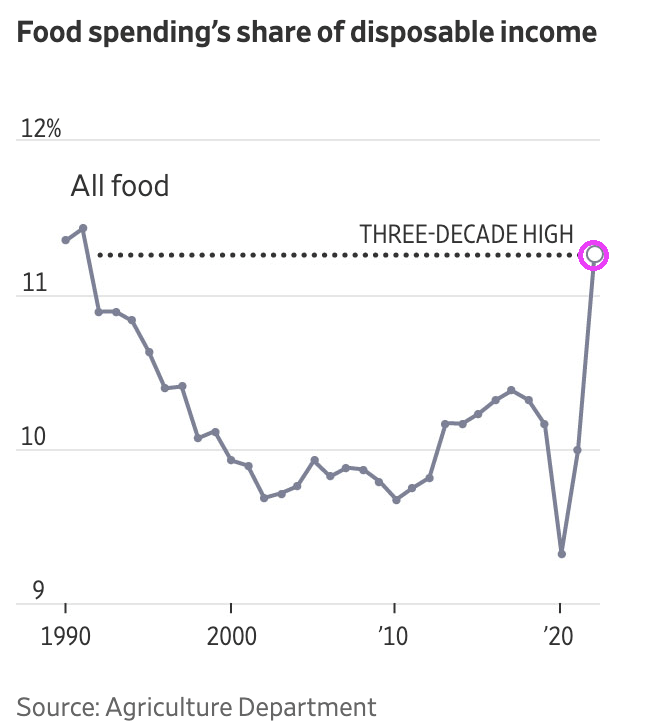

President Biden: “Inflation is the lowest it has been in nearly three years. And wages, wealth, and jobs are higher than they were before the pandemic.”

Paul Krugman, Nobel Laureate in economics and propaganda expert (ala, Leni Riefenstahl) pointed to this chart to illustrate that inflation is declining or at least hasn’t doubled under Biden, (although it looks like food prices are up 21% under Biden). Most elites won’t notice since someone does the shopping for them. Can you imagine Joe and Jill Biden at the local Kroger grocery store? Or Barrack and Mike Obama at the local grocery store on Martha’s Vineyard??

A counter to Biden’s and Krugman’s claims of “everything is peachy!” is that the situation is actually dire.

1. Prices have never been higher and are starting to accelerate to the upside again

2. All the jobs created in the past year have been part time.

3. There has been zero job growth for native-born Americans since 2018; all jobs have gone to immigrants (mostly illegal immigrants)

4. Real wages have not only been negative for most of the Biden presidency, they just turned negative again

In addition, food spending’s share of disposable income is at its highest in three decades.

Nero supposedly fiddled while Rome was burning. Joe “Nero” Biden eats ice cream while the USA burns.

First, online shopping has crushed retail commercial space. Second, crime is rampant in The Big Apple. A slowing economy is contributing to the malaise in commercial real estate (CRE).

According to Bloomberg, Canadian pension funds – which until recently had been among the world’s most prolific buyers of real estate, starting a revolution that inspired retirement plans around the globe to emulate them because, in the immortal words of Ben Bernanke, Canadian real estate prices never go down…

Canada Pension Plan Investment Board has recently done three deals at deeply discounted prices, selling its interests in a pair of Vancouver towers, and a business park in Southern California, but it was its Manhattan office tower redevelopment project that shocked the industry: the Canadian asset manager sold its stake for just $1. The worry now is that such firesales will set an example for other major investors seeking a way out of the turmoil too, forcing a wholesale crash in the Manhattan real estate market which until now had managed to avoid real price discovery.

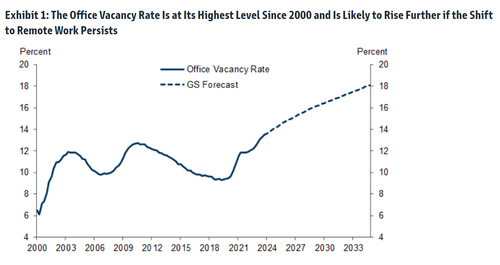

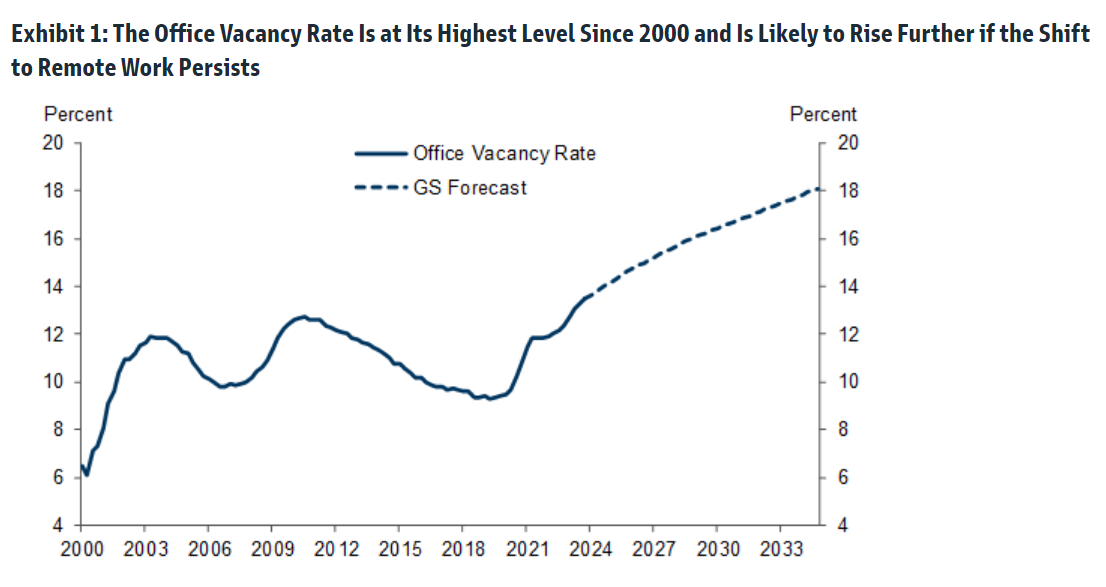

Indeed, as Goldman wrote earlier this week, while office vacancy rates are expected to keep rising well into the next decade..

… the average price of many nonviable offices has fallen only 11% to $307/sqft since 2019 (left side of Exhibit 6). The bank goes on to note that in the hardest-hit cities, as many as 14-16% of offices may no longer be viable, and their average transaction prices have already declined by 15-35%. However, because of lack of liquidity in this market, these recent transaction prices have not yet started to reflect the current values of many existing offices. Goldman ominously concludes that “alternative valuation methods, like those that are based on repeat-sales and appraisal values, suggest that actual office values may be far lower than the average transaction price.” Well, a $1 dollar price would certainly confirm that actual office values are far, far lower (more in the full Goldman note available to professional subscribers).

And going back to the historic firesale, at the end of last year the Canadian fund sold its 29% stake in Manhattan’s 360 Park Avenue South for $1 to one of its partners, Boston Properties, which also agreed to assume CPPIB’s share of the project’s debt. The investors, along with Singapore sovereign wealth fund GIC Pte., bought the 20-story building in 2021 with plans to redevelop it into a modern workspace.

360 Park Avenue South

“It’s the opposite of a vote of confidence for office,” said John Kim, an analyst tracking real estate companies for BMO Capital Markets. “My question is, who could be next?”

As office building anxiety has swept the financial world, as the persistence of both remote work and higher borrowing costs undercuts the economic fundamentals that made the properties good investments in the first place, a wave of banks from New York to Tokyo recently conceded that loans they made against offices may never be fully repaid, sending their share prices plunging and prompting fears of a broader credit crunch.

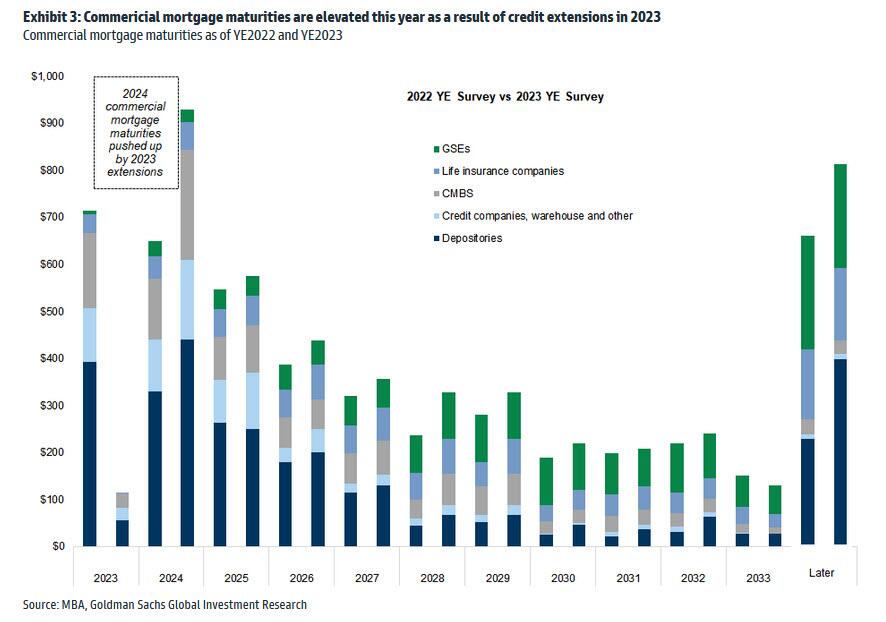

But the real test will be what price office buildings actually trade for – especially once the hundreds of billions of loan backing the properties mature….

…. and until now there have been precious few examples since interest rates started rising. That’s why industry-watchers see such shocking liquidations like CPPIB’s as a very ominous sign for the market.

The Manhattan firesale isn’t the pension fund’s first sale: last month, CPPIB sold its 45% stake in Santa Monica Business Park, which the fund also owned with Boston Properties, for $38 million. That’s a discount of almost 75% to what CPPIB paid for its share of the property in 2018. The deal came just after the landlords signed a lease with social media company Snap that required they spend additional capital to improve the campus, Boston Properties Chief Executive Officer Owen Thomas said on a conference call.

Peter Ballon, CPPIB’s global head of real estate, declined to comment on the recent deals, but said the fund has continued to invest in office buildings, including a recently completed, 37-story tower in Vancouver.

“Selling is an integral part of our investment process,” Ballon said in an emailed statement. “We exit when the asset has maximized its value and we are able to redeploy proceeds into higher and better returns in other assets, sectors and markets, including office buildings.”

As Bloomberg notes, the pension fund isn’t actively backing away from offices, but it’s not looking to increase its office holdings either. And where a property requires additional investment, CPPIB might simply look to sell so it can put that cash somewhere it can get higher returns instead, said the person, who asked not to be identified discussing a private matter.

CPPIB’s C$590.8 billion ($436.9 billion) fund is one of the world’s largest pools of capital, and its C$41.4 billion portfolio of real estate — stretching from Stockholm to Bengaluru — includes almost every property type, from warehouses, to life sciences complexes, to apartment blocks.

While that scale would mitigate any potential losses from individual transactions, it also means even a small shift in CPPIB’s office appetite has the power to cause ripple effects in the market.

While the 360 Park liquidation may be shocking, it’s just the first of many: with hybrid work schedules set to depress demand for office space in the long term, and higher interest rates increasing the cost of the constant upgrades needed to attract and keep tenants, even the best office buildings may not be able to compete with investment opportunities elsewhere.

“To get even better returns in your office investment you’re going to have to modernize, you’re going to have to put a lot more money into that office,” said Matt Hershey, a partner at real estate capital advisory firm Hodes Weill & Associates. “Sometimes it’s better to just take your losses and reinvest in something that’s going to perform much better.”

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.