Okay, Joe Biden was generally regarded as the dumbest member of the US Senate and mean-spirited (I won’t repeat podcaster Joe Rogan’s opinion of Biden). Now we realize how brazenly corrupt Biden is (taking bribes from China and Ukraine to influence American poliicies). Not only is Biden an attrocious human being, but his policies have damaged the US middle class terribly thanks to inflation.

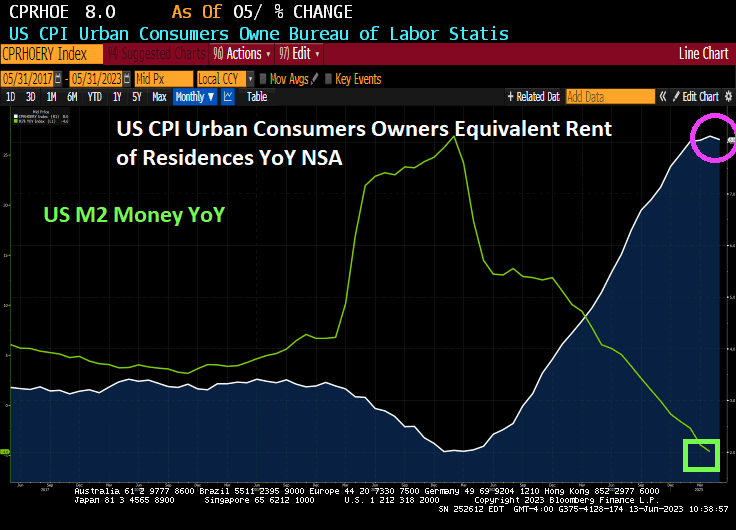

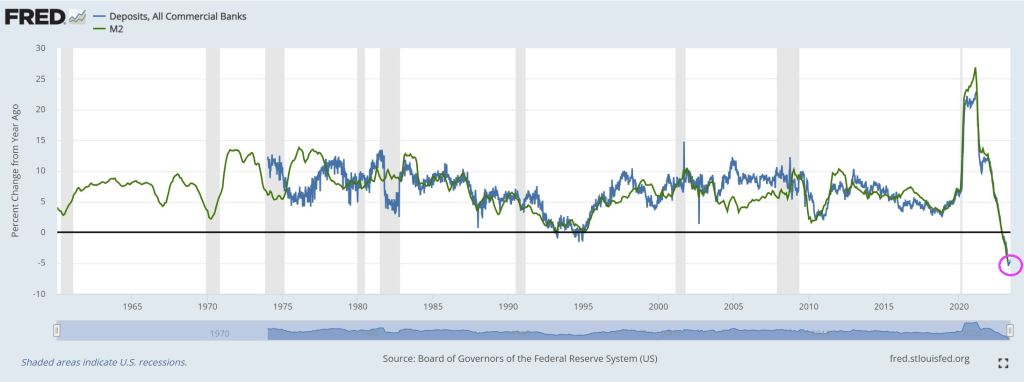

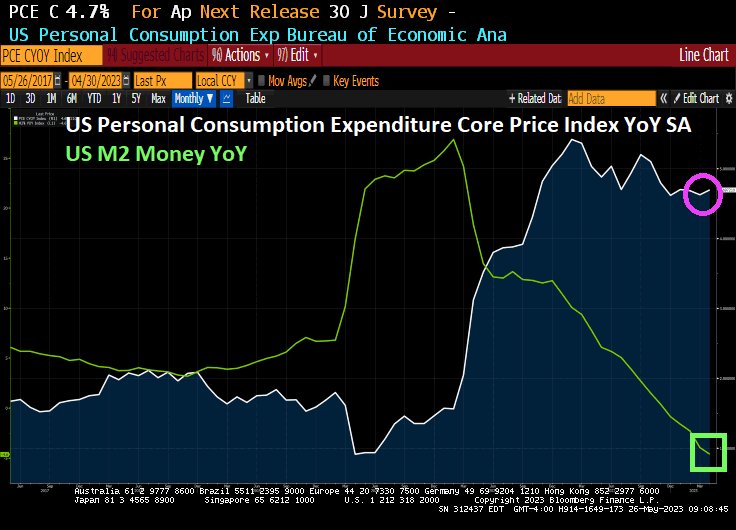

Tomorrow is the Federal government’s inflation report. As it stands today, overall inflation is slowing as M2 Money growth crashed. Core inflation remains persisitently high (white line), rent is still getting worse (orange dotted line at 8.1% YoY. What about food? Online food prices are up 8.2% YoY.

Shopping online is a good place to find cheaper computers and appliances, but grocery prices are still rising at a fast clip.

Prices of consumer goods sold online fell 2.3% in May in the US, the ninth consecutive month of declines and the biggest drop since the pandemic started, according to data from Adobe Inc. That was mainly due to steep decreases in discretionary categories.

Essential items like food, pet products and personal care, however, are seeing persistent inflation. Online grocery prices increased 8.2% from last year — although the pace of inflation has been abating since peaking at 14.3% last September.

Americans have been shifting more of their discretionary purchases to services over the past year, cutting spending on items for the home.

Online prices for appliances were down 7.9% in May from last year, the largest drop in digital-prices data from Adobe going back to 2014. Online prices for computers slumped 16.5% and electronics were down 12%.

The Adobe Digital Price Index was developed with the help of Austan Goolsbee before he became president of the Federal Reserve Bank of Chicago this year. The gauge analyzes one trillion visits to retail sites and more than 100 million items to track price changes.

Yes, Biden and Congress have levied a devastating tax on Americans. Rent and food are two of the largest household expenditures and they are up 8.1-8.,2% YoY.

Nicolas Maduro of Venezuela must be envious of Joe Biden. I don’t think even Maduro has the stones to have his politiical opponent charged with espionage in the run-up to a Presidential election. Particularly when the US President has been bribed by China and Ukraine and has similiar sensitive document hoarding issues (at least Trump didn’t leave boxes of sensitive documents in a garage like Biden did when he keeps his Chevy Corvette).

So where do we sit today after Biden has signed the debt ceiling increase and massive spending splurge?

First, look at the crashing bank deposit problem. Well, the solution is for The Fed to fire up the money printing press! Keep on printing!

This not surprising if you have read Nobel Laureate George Stigler’s treastise on regulatory capture. Essentially, big corporations (big media, big tech, big banking, big pharma, big defense, big agriculture, etc.) essentially own Congress, the Biden Administration and Federal regulators. After all, Biden has been bribed with millions of dollars by China and Ukraine and, like a Banana Republic, has is avoiding prosecution and instead prosecuting his political opponent, Trump. Don’t worry, if they get Trump that will indict DeSantis for something.

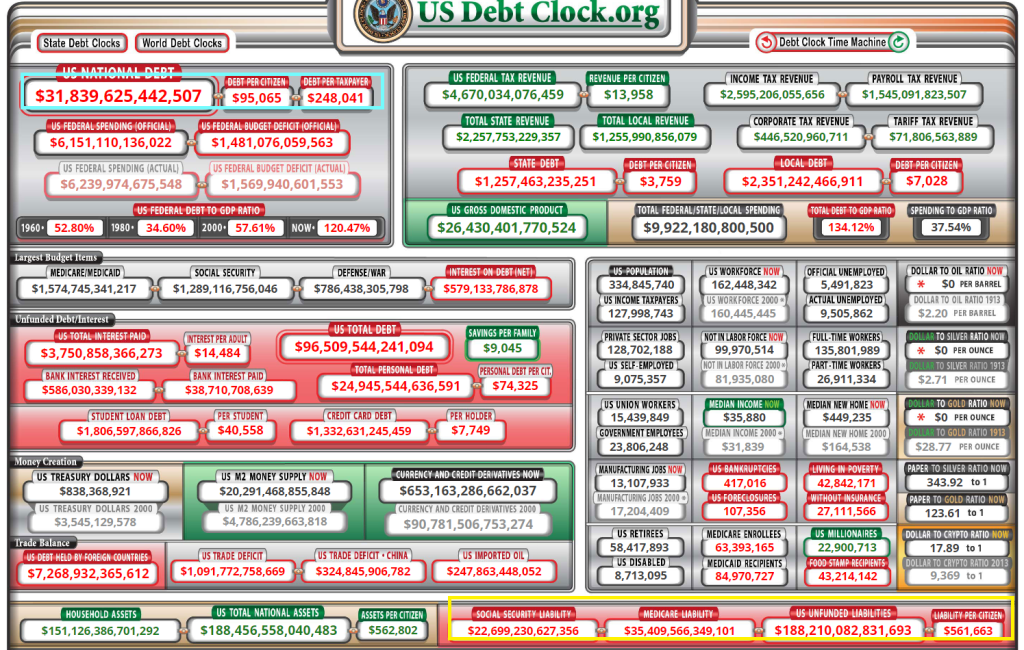

US debt stands at $31.8 TRILLION with $188 TRILLION in unfunded liabilities (which means higher personal taxes and much more debt).

Treasury Secretary Janet “Too Low For Too Long” Yellen, and former Federal Reserve Chair, is partly responsible for a phenomenon plaguing America: the death of starter homes.

As Mish has discussed, with main markets no longer an option for first-time buyers, Point2 looked at the country’s 100 largest secondary cities for the median price of a starter home and renter households’ median income. Defined as large non-core cities within a metro, these cities used to be fruitful house-hunting grounds for first-time buyers exploring less-expensive options away from main cities. But as it turns out, unaffordability can put a dent in homeownership plans regardless of city type or size.

In 41 of the 100 largest secondary cities in the U.S., renters earn half or less than half of the income they would need to buy a median-priced starter home.

There are no non-core cities in which renters could comfortably make a move toward homeownership: In 10 cities, the necessary income is about triple what they earn.

Would-be buyers in Burbank and Glendale, CA have it worst: They lack 67% of the income they would need in order to make the move from renter to homeowner.

Renters in 9 California cities would need to earn about $100,000 more in order to afford a starter home. Based on the latest renter income figures, starter home prices, and mortgage rates, non-core cities in the LA and San Diego metros are the toughest for first-time homebuyers.

In 15 of the 100 largest secondary cities, renters would need less than 4 months’ worth of extra income to afford the transition to owning a starter home.

Homeownership is within reach in Independence, MO, and Broken Arrow, OK. Those who dream of owning here would need less than one month’s worth of extra income to afford a starter home.

California Tops the List of Worst Places to Look

California has the dubious distinction of having the top least affordable starter home cities.

A starter home, according to the Census Department is priced in the bottom third of homes in the area.

Pomona, CA, is in fourteenth place. The average renter in Pomona makes $49,000 a year and needs to get to $121,000 a year. That’s nearly 2.5 times current salary.

In Burbank, CA, the average renter makes $63,000 year an needs to get to $193,000. That’s over 3 times current salary.

Within Grasp

In no market can the average renter make the plunge.

But in Independence, Missouri, or Broken Arrow, Oklahoma, the average renter is respectively just 2% and 5% short of the amount needed for a starter home

Not Shocking

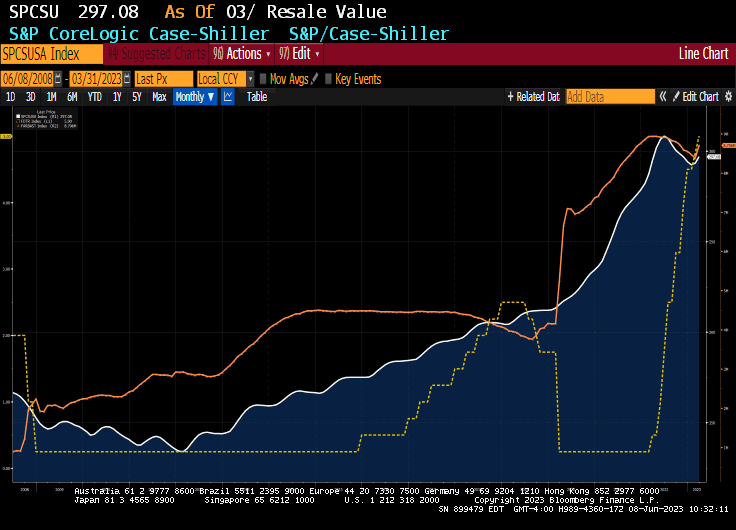

None of this is shocking. It matches one one should expect looking at Case-Shiller home prices and mortgage rates.

The Fed wanted to produce inflation and it did. But for years the Fed did not even see the inflation because the manifestation of inflation was in asset prices, not the price of consumer goods.

Case-Shiller Top City Home Prices Decline From Year Ago for the First Time Since May 2012

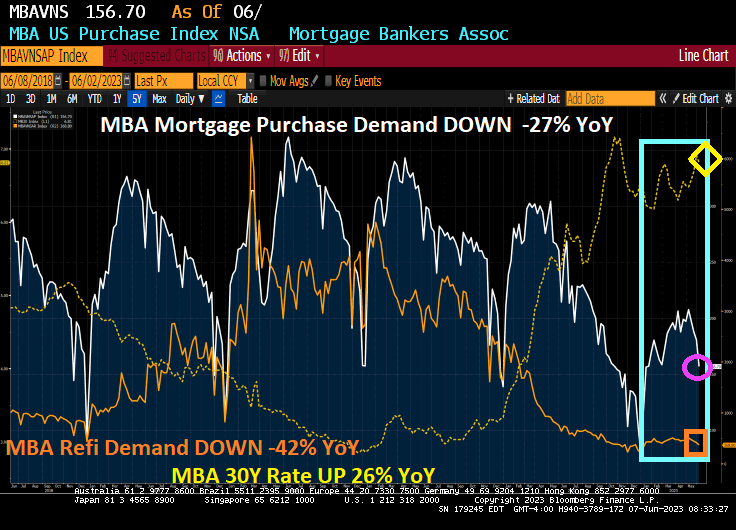

Housing starts, like mortgage purchase demand, remains depressed compared to the housing bubble of the 2000s.

Now, will The anticipated Fed pause in rate hiking help? Not likely. The Fed still has over $8 trillion in monetary stimulus chasing assets. Too much Stimulypto.

Welcome to the Bidenville Mortgage Depot! Where Bidenflation (caused by idiotic energy policies, crazy Fed money printing and insane Federal spending) has caused The Fed to raise rates crushing the US mortgage market.

Mortgage applications decreased 1.4 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending June 2, 2023. This week’s results include an adjustment for the Memorial Day holiday.

The Market Composite Index, a measure of mortgage loan application volume, decreased 1.4 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index decreased 12 percent compared with the previous week. The Refinance Index decreased 1 percent from the previous week and was 42 percent lower than the same week one year ago. The seasonally adjusted Purchase Index decreased 2 percent from one week earlier. The unadjusted Purchase Index decreased 13 percent compared with the previous week and was 27 percent lower than the same week one year ago.

The rest of the story.

The East Palestine Ohio train wreck is symbolic of Biden’s economic programs. I don’t think the Vacationer in Chief (40% of time as President has been on vacation) has been there yet.

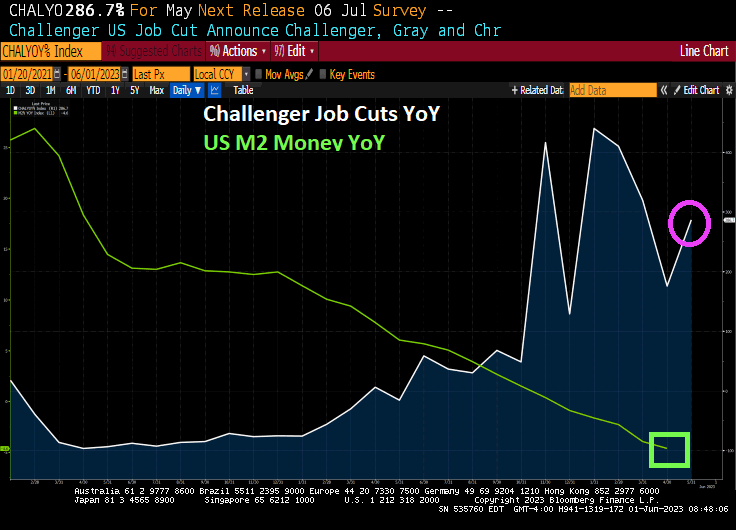

So much for Biden’s “miracle economy.” Challenger jobs cuts report is out for May and job cuts soared 286.7% year-over-year (YoY). As M2 Money growth crashes.

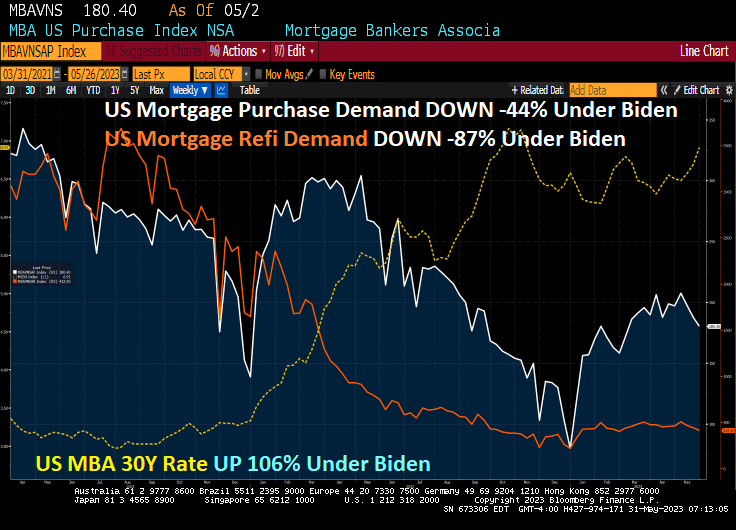

Under Biden, the US economy is a land of confusion. Under Biden’s Reign of Error, Mortgage Purchase Demand is down -44%, Refi Demand is down -87%, and Mortgage Rates are UP 106%.

Mortgage applications (demand) decreased 3.7 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending May 26, 2023.

The Market Composite Index, a measure of mortgage loan application volume, decreased 3.7 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index decreased 5 percent compared with the previous week. The Refinance Index decreased 7 percent from the previous week and was 45 percent lower than the same week one year ago. The seasonally adjusted Purchase Index decreased 3 percent from one week earlier. The unadjusted Purchase Index decreased 4 percent compared with the previous week and was 31 percent lower than the same week one year ago.

Here is the rest of the story.

1% down payment mortgages when home prices are falling? Truly, a land of economic confusion under Country Joe.

Well, Biden and McCarthy have agreed in principle to a budget revision, raise the debt ceiling and avoid a US debt default. The Uniparty strikes again! No restraint of reckless Federal spending t speak of . The big donor class wins and middle class Americans lose.

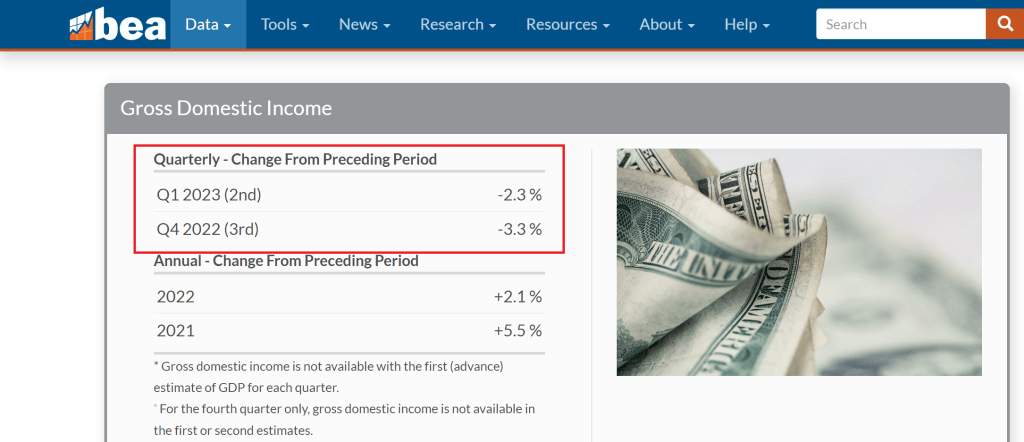

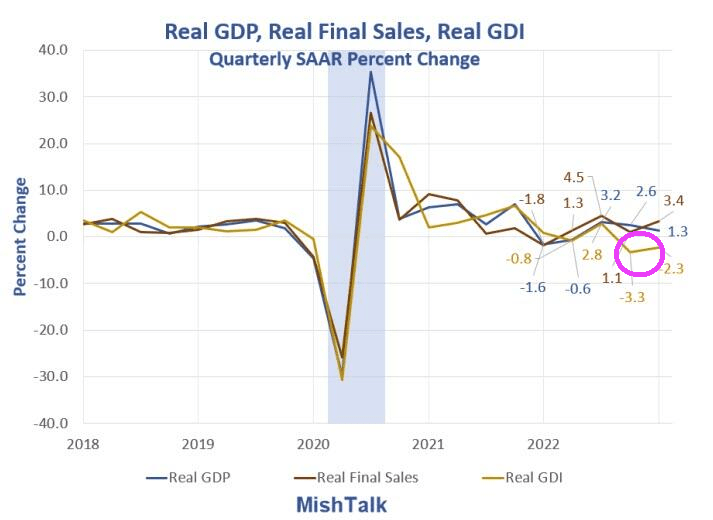

Mike Shedlock (aka, Mish) makes a good point: the US is already in recession if we look at GDI (gross domestic income) rather than GDP (gross domestic product). The US has already declined two consecutive quarters in terms of negative GDI growth.

White House and Republican negotiators tentatively narrowed differences but were still clashing Friday on key issues as the Treasury Department signaled extra time was available before a potential US default.

Treasury Secretary Janet Yellen announced the department expects to be able to make payments on US debts up until June 5 if lawmakers fail to act on the US debt ceiling. That set a more pointed date for a potential default but is also four days later than her previous comments eyeing trouble as soon as June 1.

The new so-called X-date buys negotiators for House Speaker Kevin McCarthy and President Joe Biden more time to strike a deal. The negotiating teams haven’t met in person since Wednesday but spoke late into the night Thursday and were in regular communication throughout the day Friday.

Yes, there isn’t really a crisis folks. Treasury collects tax dollars continuously so Treasury can prioritze debt payments and other disbursements. The only crisis is in the minds of the media.

Deputy Treasury Secretary Wally Adeyemo warned Friday that payments to Social Security beneficiaries, veterans and others would be delayed if there’s a default. But he said he’s gaining some confidence an agreement will be reached.

We’re making progress and our goal is to make sure that we get a deal because default is unacceptable,” Adeyemo said in an interview on CNN. “The president has committed to making sure that we have good-faith negotiations with the Republicans to reach a deal because the alternative is catastrophic for all Americans.”

The accord would also include a measure to upgrade the nation’s electric grid to accommodate sham renewable energy, a key climate goal, while speeding permits for pipelines and other fossil fuel projects that the GOP favors, people familiar with the deal said.

The deal would cut $10 billion from an $80 billion budget increase for the Internal Revenue Service that Biden won as part of his Inflation Reduction Act (big whoop). Republicans have warned of a wave of agents and audits while Democrats said the increase would pay for itself through less tax cheating.

What is taking shape would be far more limited than the opening offer from Republicans, who called for raising the debt ceiling through next March in exchange for 10 years of spending caps. House conservatives were already balking Thursday at the notion of a small deal, with the House Freedom Caucus sending a letter to McCarthy demanding he hold firm.

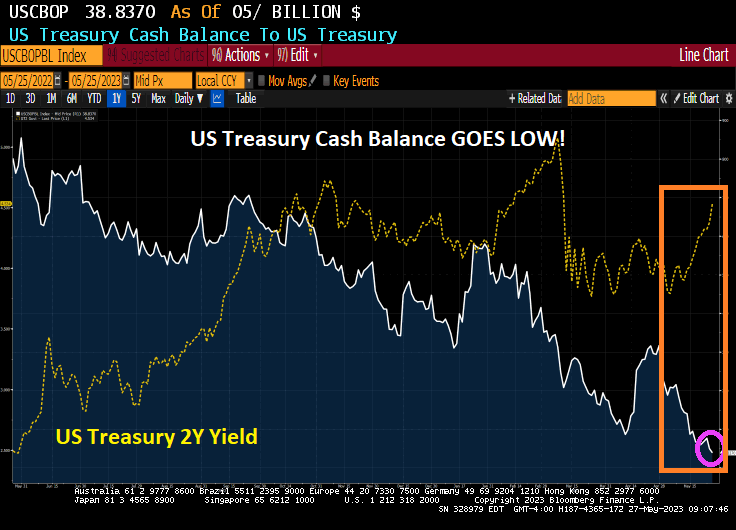

Treasury’s cash balance is at a low point and The Administration threatens Social Security recipients and veterans of delayed payments … while Biden goes on vacation for Memorial Day weekend to honor veterans??

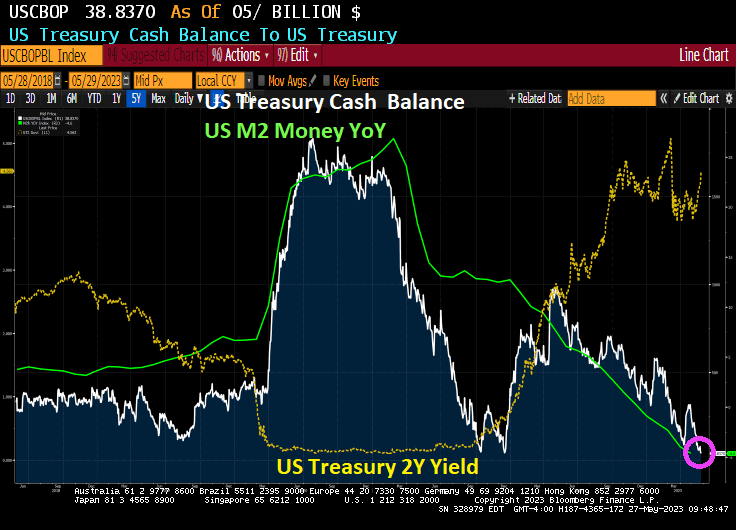

Of course, Yellen know that all The Fed has to do to increase M2 Money growth again.

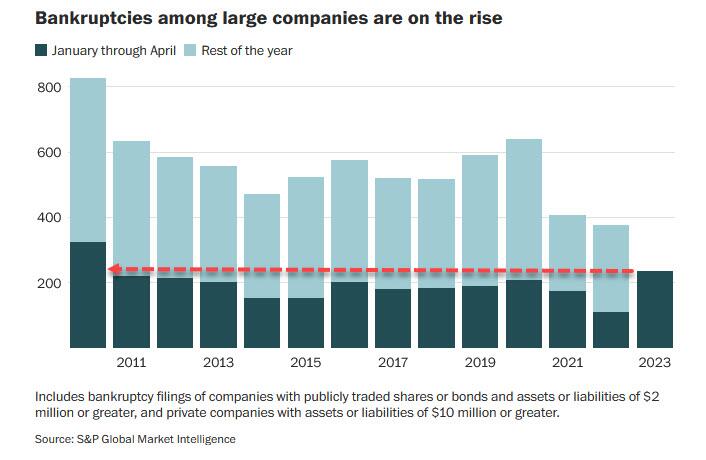

Meanwhile, bankrupties among large companies are highest since 2010.

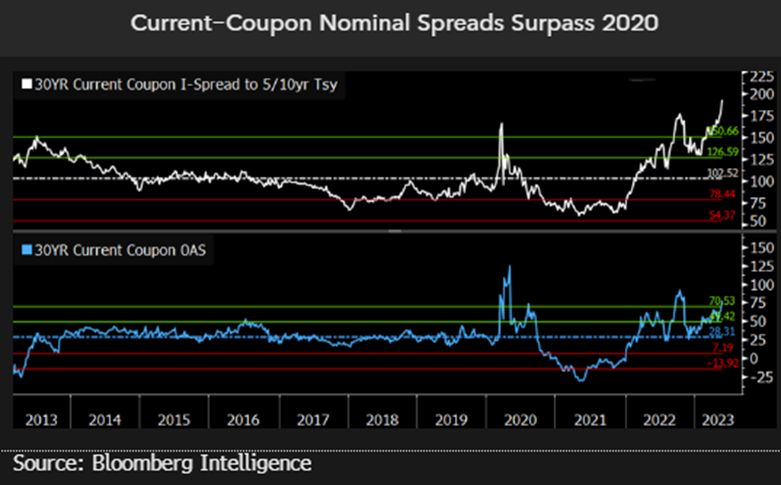

In the mortgage market, current coupon nominal spreads 9Agency MBS 30Y coupon over Treasuries) are soaring.

Meanwhile, to honor US veterans, Biden goes on Memorial Day weekend and threaten veterans with delays in veteran benefits. Sigh.

Is Joe Biden REALLY Reverend Kane from Poltergeist II??

You must be logged in to post a comment.