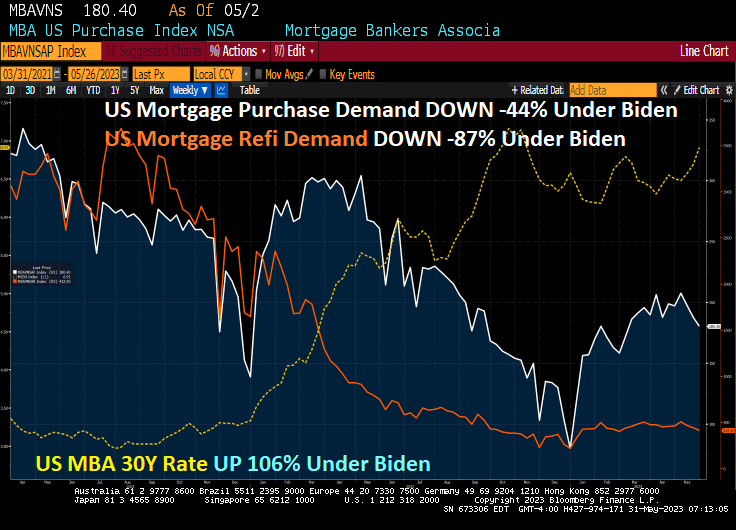

Under Biden, the US economy is a land of confusion. Under Biden’s Reign of Error, Mortgage Purchase Demand is down -44%, Refi Demand is down -87%, and Mortgage Rates are UP 106%.

Mortgage applications (demand) decreased 3.7 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending May 26, 2023.

The Market Composite Index, a measure of mortgage loan application volume, decreased 3.7 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index decreased 5 percent compared with the previous week. The Refinance Index decreased 7 percent from the previous week and was 45 percent lower than the same week one year ago. The seasonally adjusted Purchase Index decreased 3 percent from one week earlier. The unadjusted Purchase Index decreased 4 percent compared with the previous week and was 31 percent lower than the same week one year ago.

Here is the rest of the story.

1% down payment mortgages when home prices are falling? Truly, a land of economic confusion under Country Joe.

Well, Biden and McCarthy have agreed in principle to a budget revision, raise the debt ceiling and avoid a US debt default. The Uniparty strikes again! No restraint of reckless Federal spending t speak of . The big donor class wins and middle class Americans lose.

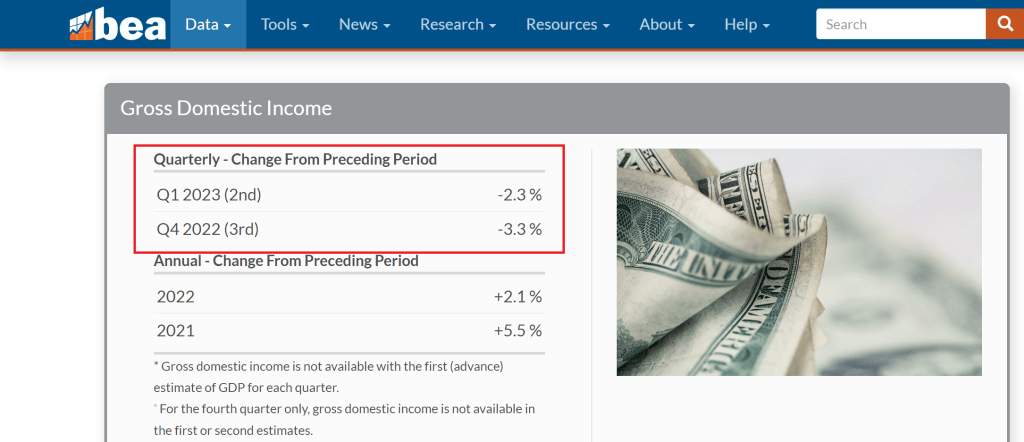

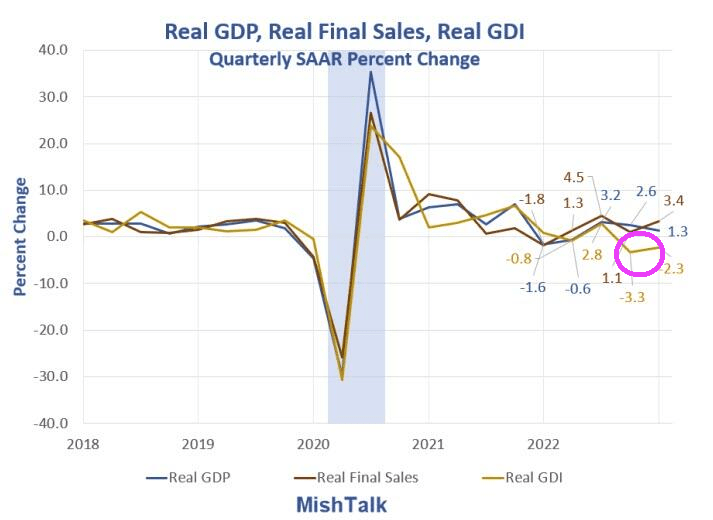

Mike Shedlock (aka, Mish) makes a good point: the US is already in recession if we look at GDI (gross domestic income) rather than GDP (gross domestic product). The US has already declined two consecutive quarters in terms of negative GDI growth.

White House and Republican negotiators tentatively narrowed differences but were still clashing Friday on key issues as the Treasury Department signaled extra time was available before a potential US default.

Treasury Secretary Janet Yellen announced the department expects to be able to make payments on US debts up until June 5 if lawmakers fail to act on the US debt ceiling. That set a more pointed date for a potential default but is also four days later than her previous comments eyeing trouble as soon as June 1.

The new so-called X-date buys negotiators for House Speaker Kevin McCarthy and President Joe Biden more time to strike a deal. The negotiating teams haven’t met in person since Wednesday but spoke late into the night Thursday and were in regular communication throughout the day Friday.

Yes, there isn’t really a crisis folks. Treasury collects tax dollars continuously so Treasury can prioritze debt payments and other disbursements. The only crisis is in the minds of the media.

Deputy Treasury Secretary Wally Adeyemo warned Friday that payments to Social Security beneficiaries, veterans and others would be delayed if there’s a default. But he said he’s gaining some confidence an agreement will be reached.

We’re making progress and our goal is to make sure that we get a deal because default is unacceptable,” Adeyemo said in an interview on CNN. “The president has committed to making sure that we have good-faith negotiations with the Republicans to reach a deal because the alternative is catastrophic for all Americans.”

The accord would also include a measure to upgrade the nation’s electric grid to accommodate sham renewable energy, a key climate goal, while speeding permits for pipelines and other fossil fuel projects that the GOP favors, people familiar with the deal said.

The deal would cut $10 billion from an $80 billion budget increase for the Internal Revenue Service that Biden won as part of his Inflation Reduction Act (big whoop). Republicans have warned of a wave of agents and audits while Democrats said the increase would pay for itself through less tax cheating.

What is taking shape would be far more limited than the opening offer from Republicans, who called for raising the debt ceiling through next March in exchange for 10 years of spending caps. House conservatives were already balking Thursday at the notion of a small deal, with the House Freedom Caucus sending a letter to McCarthy demanding he hold firm.

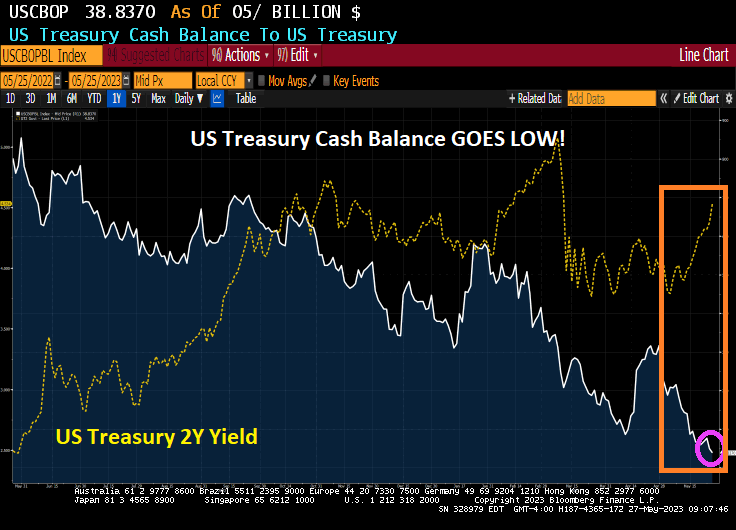

Treasury’s cash balance is at a low point and The Administration threatens Social Security recipients and veterans of delayed payments … while Biden goes on vacation for Memorial Day weekend to honor veterans??

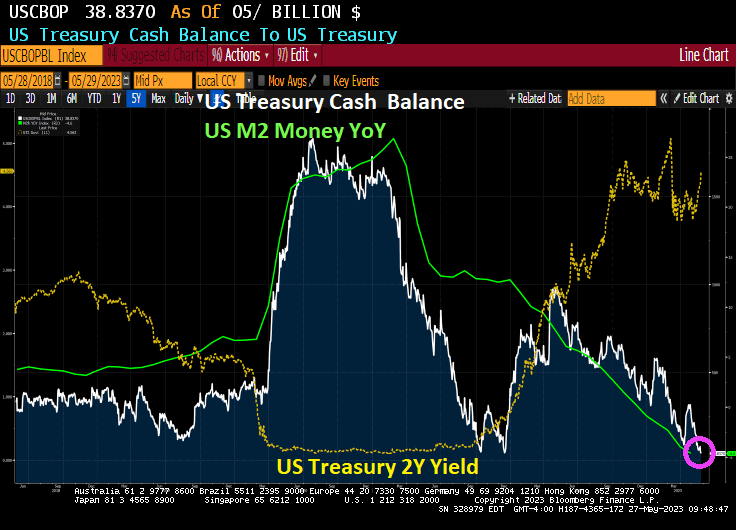

Of course, Yellen know that all The Fed has to do to increase M2 Money growth again.

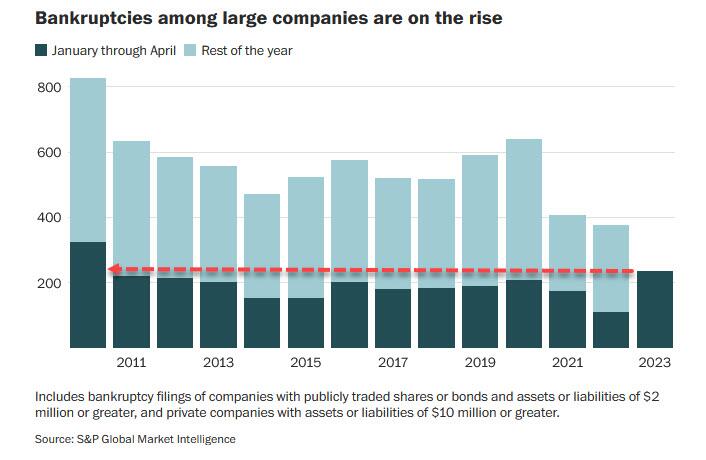

Meanwhile, bankrupties among large companies are highest since 2010.

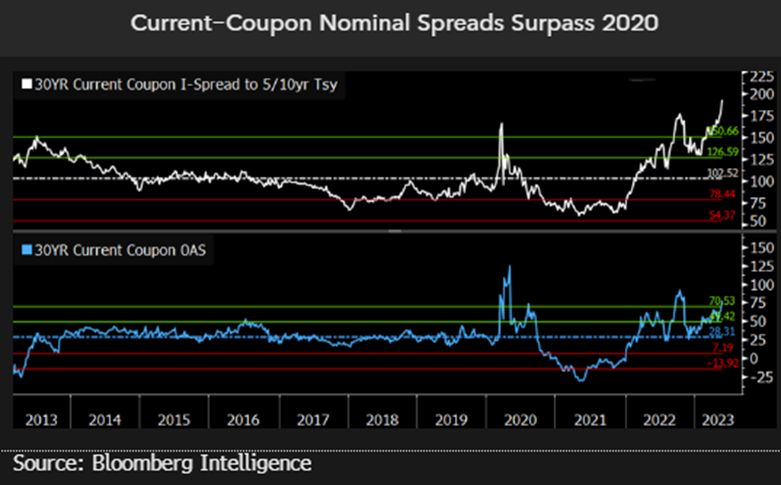

In the mortgage market, current coupon nominal spreads 9Agency MBS 30Y coupon over Treasuries) are soaring.

Meanwhile, to honor US veterans, Biden goes on Memorial Day weekend and threaten veterans with delays in veteran benefits. Sigh.

Is Joe Biden REALLY Reverend Kane from Poltergeist II??

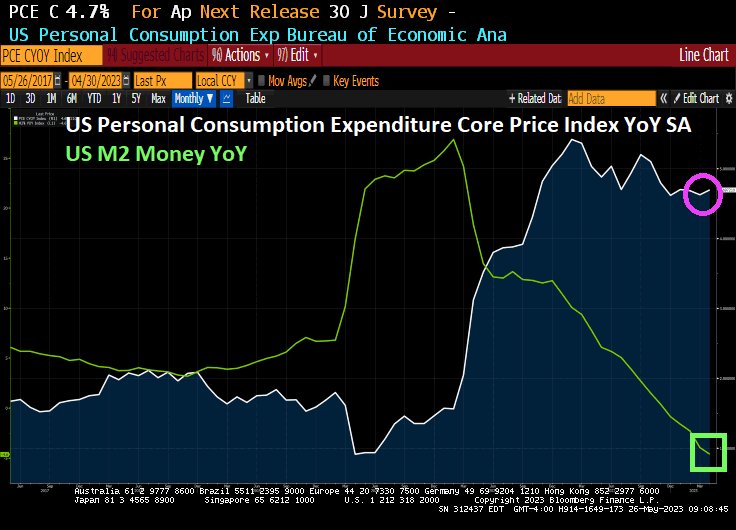

So much for Treasury Secretary Janet Yellen’s proclamtion that inflation is transitory and would subside to under 2%. April’s core inflation (PCE Deflator) rose to 4.7% YoY. Despite M2 Money growth crashing to -4.6% YoY.

Today’s Fed Funds Futures data is pointing to another rate hike or two.

With Core PCE at 4.7%, the Taylor Rule suggested Fed Funds Target rate is now 10.57%. So, The Fed is only about half way there.

Damn it, Janet, people are suffering from the ravages of inflation and you laugh.

What happened to Biden? He used to be a “reasonable” Senator (reasonable for a racist Democrat, that is), willing to negotiate with the opposition on budgetary issues and the debt ceiling. Now we have “Progressive Joe” who is acting like crazy Progressive Congresswoman Pramila Jayapal from Seattle. {Aka, Seattle’s Worst!} But his newly found Progressive identiy is leading down a terrible path. Rating agencies are putting the US of credit watch because of Biden’s newly found Progressive back bone. (Progressive means progressing towards full blown Communism).

Ratings company warns on worsening political partisanship

US AAA ratings on review with negative implications at DBRS

The tension around the US debt-limit negotiations ratcheted up after Fitch Ratings warned the nation’s AAA rating was under threat from a political standoff that’s preventing a deal.

Fitch may downgrade its assessment to reflect the increased partisanship that is hindering a resolution despite the fast-approaching so-called X date, it said, referring to the point at which Washington runs out of cash. It moved the US to “rating watch negative” under its classification. Meantime, DBRS Morningstar placed the US ratings of AAA under review “with negative implications.”

Markets have been showing increasing nervousness over the standoff, with Treasury-bill yields slated to mature early next month surging past 7%, while the S&P 500 Index has declined for two days. Economists project a US default could trigger a recession, with widespread job losses and a surge in borrowing costs.

Fitch’s warning “underscores the need for swift bipartisan action by Congress to raise or suspend the debt limit and avoid a manufactured crisis for our economy,” said Lily Adams, a spokesperson from Treasury.

Biden’s childish refusal to reduce his insanely huge budget (crammed with pork for large donors and Progressives) is causing ripples to be felt overseas. Look look at the Japanese Yen.

Pramila Jayapal, Joe Biden’s intellectual soulmate.

I have gotten a flood of emails and text messages asking about what happens if Biden defaults on the US debt. In short, Biden has made a career out of spending money, as has Speaker McCarthy. They both have an incentive to raise the debt ceiling, but whether it is cuts to Biden’s insane budget (higher than Covid-era spending) and wants to raise taxes on the middle class to pay for it. McCarthy wants a trimmed budget (aka, back to pre-Covid spending levels) and NOT raises taxes. They will eventually agree somewhere in the middle (US Congress member Pramila Jayapal will be outraged, but then again, she is ALWAYS outraged like Senator Elizabeth Warren) and AOC.

The Federal Reserve has taken a brief respite from fighting inflation that they helped cause. But with $188 TRILLION in unfunded entitlements promised by politicians, The Fed will undoubtedly start buying assets again (aka, QEInfinity) and the debt ceiling will keep being raised. In essence, the DC merry-go-round is broken and politicians will keep pushing it around until it collapses.

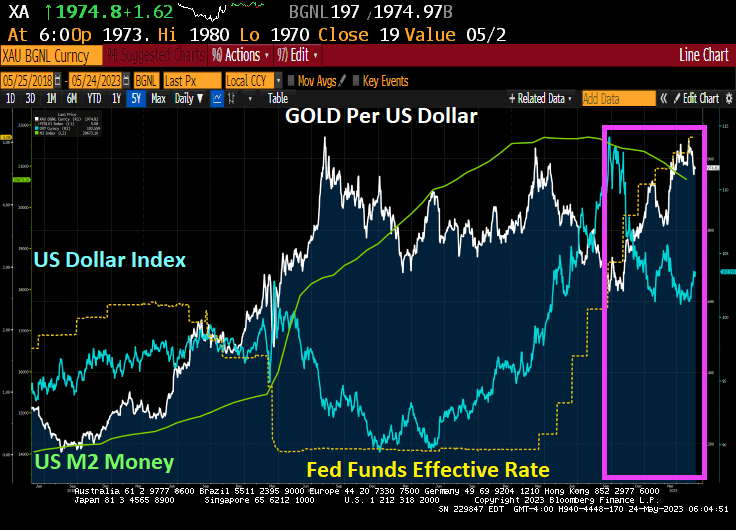

For the moment, The Federal Reserve is reducing M2 Money (green line). With it, the US Dollar (blue line) has declined. Gold (white line fever) is on the rise along with The Fed’s effective funds rate.

WTI crude is up over 1% this AM. And gold is up 2.29%. Heating oil is up 3.56%.

Face it, I have no confidence in Treasury Secretary Janet Yellen, one of the biggest propronents of MMT (modern monetary theory or borrow and spend without consequences). Yellen is NOT making lose my blues.

The US middle class is wasting away in Bidenville. While Climate Envoy John Kerry threatens to seize farms in the name of … climate change? The moral hazard problems associated with farm seizures boggle the mind.

So, everyone keeps talking about the debt ceiling and the fact that America is about to run out of money. How did we just find $375 million dollars AGAIN to ship on over to Zelenskyy?

Biden and McCarthy met on the debt ceiling and nothing has been resolved. They both represent the BIG donor class and big Pharma, big defense, big tech, big media, big tech, anything that is big runs Congress and the Administration. So of course they will finally agree to raise the debt ceiling and continue their insane spending on the donor class.

As of right now, there is no deal to raise the debt limit. Biden wants to raise the already insane and irresponsible Federal budget. McCarthy wants no new taxes. Who will cave in this game of chicken? My guess is that McCarthy will cave. Biden may whip out the 14th Amendment to bypass McCarthy and Congress, but this makes Biden a dictator (which would suit him fine, but would be a horrible precedent).

Core Inflation Rate UP 244% under Biden, Food UP 46%, Gasoline Prices UP 60%, Rental Growth UP 268%. What a disaster under Biden’s Reign of Error.

But at least the Biden family are getting wealthy beyond comprehension. Isn’t that Ashley Biden in the blue?

Its May 21st and Biden still refuses to budge on paring back his massively bloated budget of green energy payoffs. Yet Biden laughingly stated it isn’t his fault if the US defaults on its debt. It is absolutely 100% Biden’s fault and he should be impeached if he fails to meet Republicans half way.

(Bloomberg) Treasury Secretary Janet Yellen said the US is unlikely to reach mid-June and still be able to pay its bills, underscoring the urgency of the White House reaching a deal with Republicans to raise the debt limit.

“Well, there’s always uncertainty about tax receipts and spending,” Yellen said on NBC’s “Meet the Press” on Sunday. “And so it’s hard to be absolutely certain about this, but my assessment is that the odds of reaching June 15 while being able to pay all of our bills is quite low.”

Biden and McCarthy have been at an impasse since January over raising the government’s $31.4 trillion borrowing limit. The Treasury has been deploying special accounting measures since January to stay within the statutory ceiling.

“On June 15, there are tax payments that are made that are substantial,” Yellen told NBC. “But early June, I interpret as before that, and it would be very difficult to get to that date.”

This is coming from the former Federal Reserve Chair who raised interest rates once while Obama was President, then raises rates 8 time after Trump won the election.

Surprisingly, cryptos are down today despite Biden’s incompetence and Yellen’s dire warning. Atleast TRON is up!

Yes, Yellen is the same person who raised interest rates just once under Obama, then 8 times after Trump was elected. And Yellen is the same person who said inflation was transitory, yet remains elevated. Yellen is truly The Deep State’s fuiancial manager.

But that is where we are in the US. A President who acts like a spoiled 12 year old bully, members of Congress like Cori Bush and AOC who think The Fed can just print trillions MORE and give it to preferred groups. Senator Diane Feinstein (soon to be replaced by a horrible human being in the person of Adam Schiff). John Fetterman, the next Bernie Sanders?? C’mon DC. A true ship of fools. And dangerous ones at that.

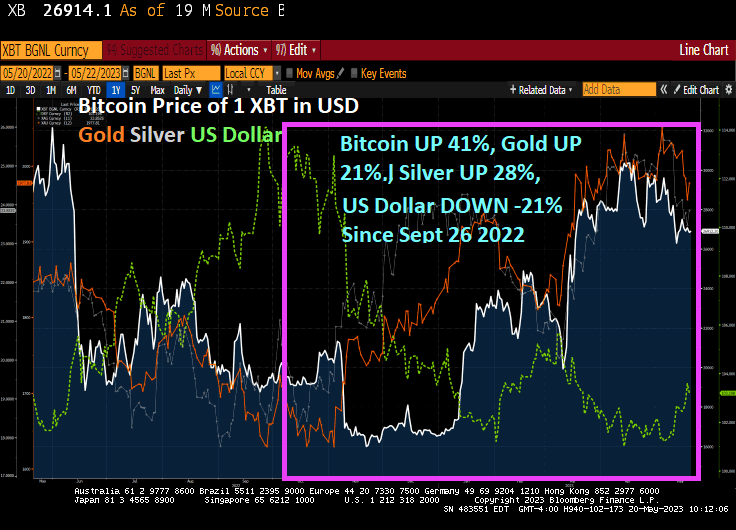

So since September 26, 2022, we have seen a fundametal shift in markets. The US Dollar is down -21% since September 26, 2022 while Bitcoin is up 41%, Gold is up 21% and Silver is up 28%.

Biden is sitting pretty, If McCarthy chickens out and agrees to Biden’s outrageous budget, Biden looks like a hero. If Biden defaults, the MSM media will blame McCarthy and Republicans, so Biden wins. No wonder Biden said he isn’t worried about the debt ceiling negotations. He wins no matter what, And we the 99% get screwed.

Reminder, the US already has $32 TRILLION in debt and politicians have promised $188 TRILLION in entitlement spending. yet we are sending billions to Ukraine, etc. Yet Biden is visiting Japan (hide your little girls, Hiroshima!) and Biden/Congress still haven’t solved the debt limit crisis and Biden’s insane budget yet. Meanwhile, Americans are suffering from Biden’s inflation (aka, Bidenflation) and bad economic policies.

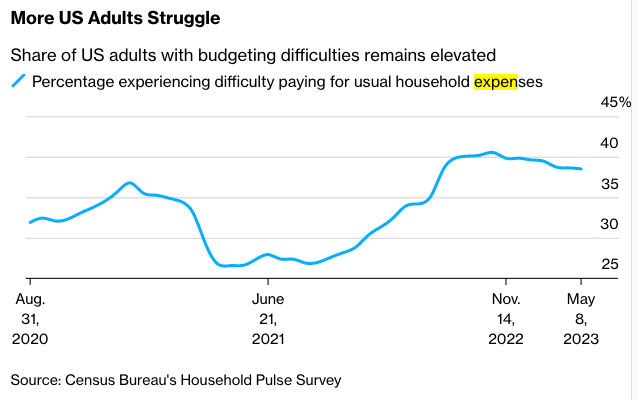

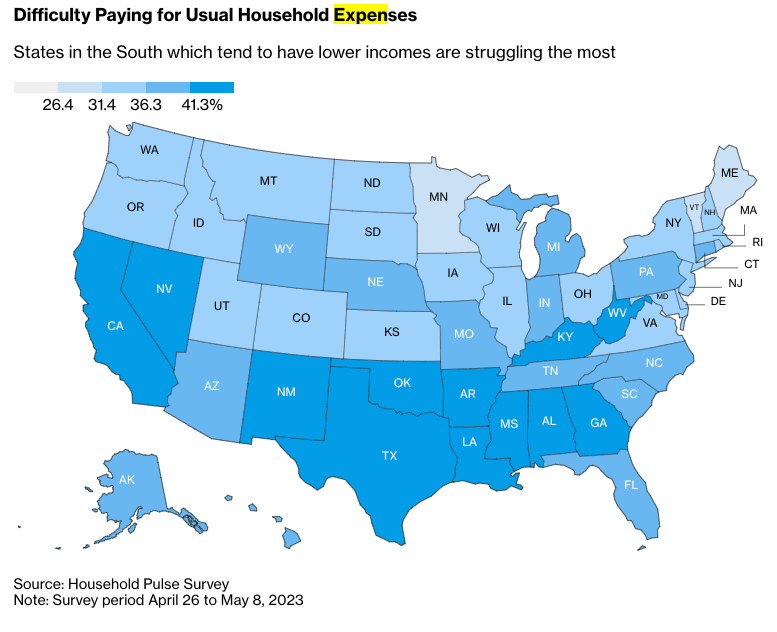

As many as 89.1 million American adults (or about 38.5%) were found to experience some form of difficulty in covering expenses between April 26 and May 8, according to Bloomberg, citing new data from the Household Pulse Survey. This is up from 34.4% in 2022 and 26.7% during the same period in 2021.

The rising trend is alarming but not surprising. Consumers have been battered by two years of negative real wage growth.

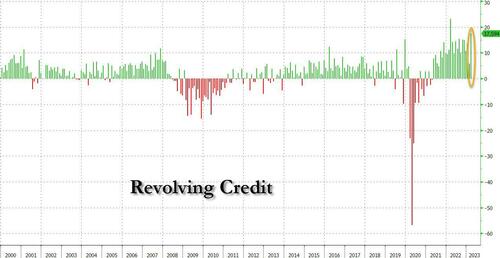

As wages fail to outpace the cost of living, many consumers have burned through savings and resorted to credit cards. The latest revolving credit data shows consumers appear to be ‘strong,’ but that’s only because they use their plastic cards more than ever to survive.

The Household Pulse Survey found struggling households were primarily based across West Coast and the South.

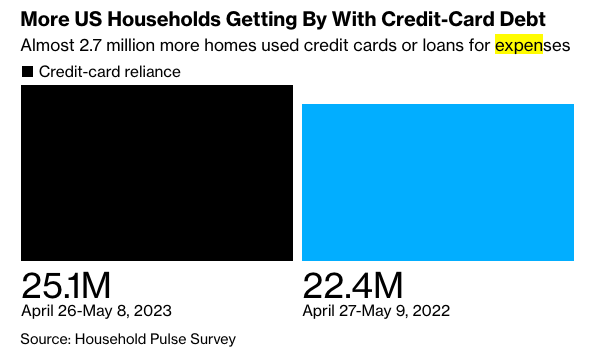

Compared with the same period last year, the survey found 2.7 million more households were relying on credit cards to cover expenses.

Consumers have record card debt and ultra-low savings rates and are paying some of the highest borrowing costs in a generation (the average interest rate on cards now exceeds 20%). This debt is becoming insurmountable for some as delinquencies rise.

And what we have now is new debit and credit card data published by the Bank of America Institute that shows not just spending slowdown for lower-income consumers, but also the upper-income cohort is finally starting to crack.

However, it is appropriate that Biden is visiting Hiroshima Japan where a nuke was detonated to help end World War II.. Biden is doing the same to the US.

{kind=link}

{kind=link}

You must be logged in to post a comment.