Goodbye free markets! Hello heavy-handed government cronyism.

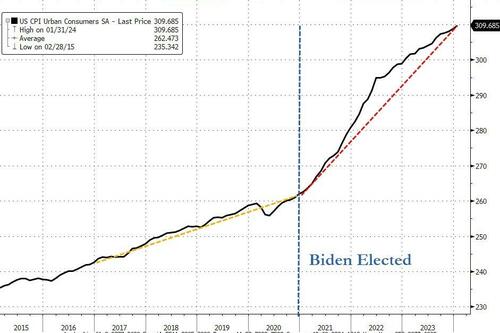

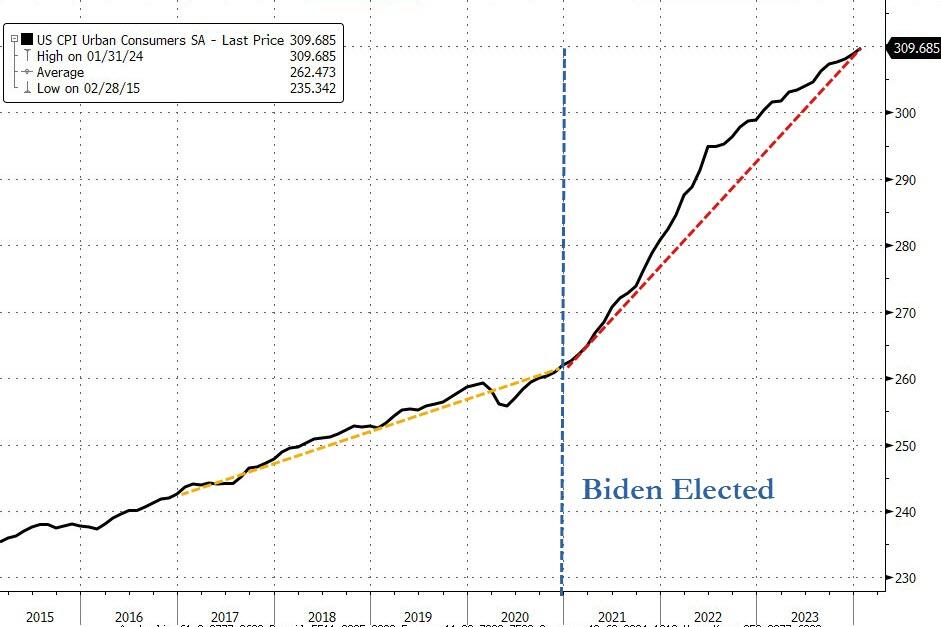

So, despite recent declines in energy prices, gasoline prices are still up 46.25% under “Green Joe” and the all important for shipping, diesel prices, are still up 55.6% under Brainless Joe.

One would think that massive rises in gasoline and diesel prices would make everyone buy an electric vehicle (EV). But alas, the high cost and unreliability of EVs is turning off consumers. (I own a hybrid and wish I didn’t).

This time it deals with supply chain logistics, with Bloomberg reporting this week that in the year and a half since passing the Inflation Reduction Act, automakers are finding out the hard way that the rigorous criteria for manufacturing batteries using materials from the United States and its free-trade allies could render them cost-inefficient compared to global competitors.

Companies like Tesla are instead taking advantage of a temporary shift in the rules to stock up with cheaper batteries from countries like China.

The Biden administration’s new rules will all but cut out China from the supply chain, however, which will make it tougher to find affordable metal suppliers.

This, in turn, will threaten President Biden’s goal to boost the domestic electric vehicle market. Bloomberg writes that mining companies and labor unions insist that without curtailing the influx of cheaper, Chinese-subsidized materials, the U.S. can’t develop a competitive EV market.

Meanwhile, the higher costs are driving automakers away from EVs. And as battery material requirements are set to double by 2027, fulfilling these mandates will be increasingly difficult, putting Biden’s ambitious EV strategy at risk.

The demand side of the equation also looks less than favorable. We wrote just hours ago about how Ford was slashing prices on its Mach E and Lightning 150. Tesla has been slashing prices to stoke demand for nearly a year now.

Both Ford and GM have said they’re going to curtail their investment in EVs. General Motors, who posted better than expected earnings earlier this month, said that it plans on changing its product lineup to include more hybrid vehicles, drifting away from pure electric vehicles.

CEO Mary Barra said on the earnings call: “Let me be clear, GM remains committed to eliminating tailpipe emissions from our light-duty vehicles by 2035, but, in the interim, deploying plug-in technology in strategic segments will deliver some of the environment or environmental benefits of EVs as the nation continues to build this charging infrastructure.”

Recall, a report from Consumer Reports last year found that electric vehicles have almost 80% more problems and are “generally less reliable” than conventional internal combustion engine cars.

But hey, what good is a “free” market if the government doesn’t have complete and total control of consumer choice, right Joe? After all, Biden drives a gas guzzling Chevy Corvette. When Biden sells his Corvette and buys a Chevy Bolt, I might believe him. Nah!

So, the free market is standing up to Biden’s hard left tyranny.

My new nickname for Biden is Dopey. And Kamala Harris is Happy (because she laughs constantly). Mayorkas is Bashful (he doesn’t do anything). NY Senator Chuck Schumer is Grumpy. Jill Biden is Doc (for her pathetic PhD in Education). The intellectual seven dwarves are running our country into the ground.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.