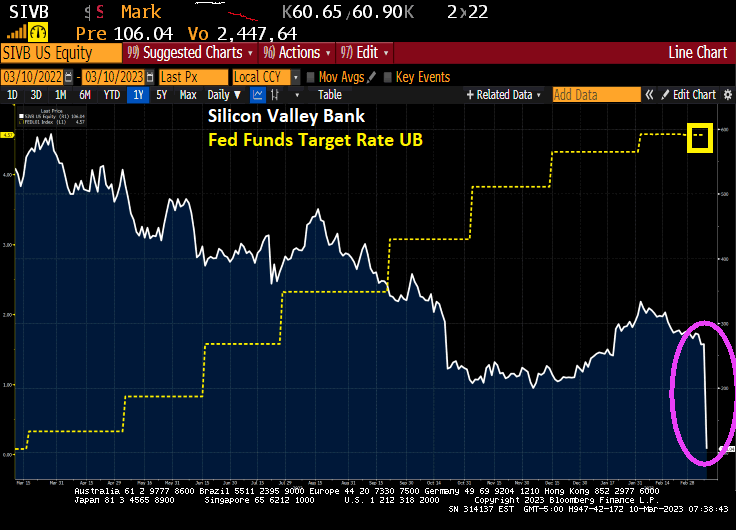

Its no mystery to me that San Francisco’s First Republic Bank is hurting. Senator Elizabeth Warren (D-MA) is calling for hearings into the banking meltdown. Hey Liz, look at San Francisco’s First Republic Bank as a case study.

The infamous Covid surge in M2 Money supply (green line) produced a big surge in bank price stocks, thanks in part to the insane spending that Congress made following Covid (I’m looking at you, Liz!). But now The Fed is slowing M2 Money growth and banks like First Republic are paying the price.

As The Fed tightens, earnings per share for First Republic (red line) have crashed and burned. Along with its stock price.

So, its not mystery to me what happened. Bernanke and Yellen’s “too low for too long” monetary policies were suddenly taken away to fight inflation (partially caused by Biden and Congress’ spending spree).

Since The Fed has been removing the punch bowl to fight inflation, the S&P 500 index and the KBW bank index have gotten crush. Since February 2nd, the S&P 500 index is down -6.3% while the KBW Bank index is down -31.4%.

In short, banks take in short-term deposits and lend long, earning the spread. But when rates start to rise, watch out!!

You must be logged in to post a comment.