Harry Truman once uttered the phrase “The buck stops here.” Joe Biden’s catchphrase should be “It’s Russia’s fault!”

Well, all roads led to Joe and Jay. Here is a chart of Producer Price Index (Final Goods) prices YoY, now the highest in history. At least, gasoline prices are declining to $4.083 (they were $2.40 when Biden was installed as President). But inflation is out of control and the 30-year mortgage rate is now 5.14% (mortgage rates were 2.82% in February 2021 just after Biden took control).

Just in case you wonder why I follow Fed Funds Futures data so closely.

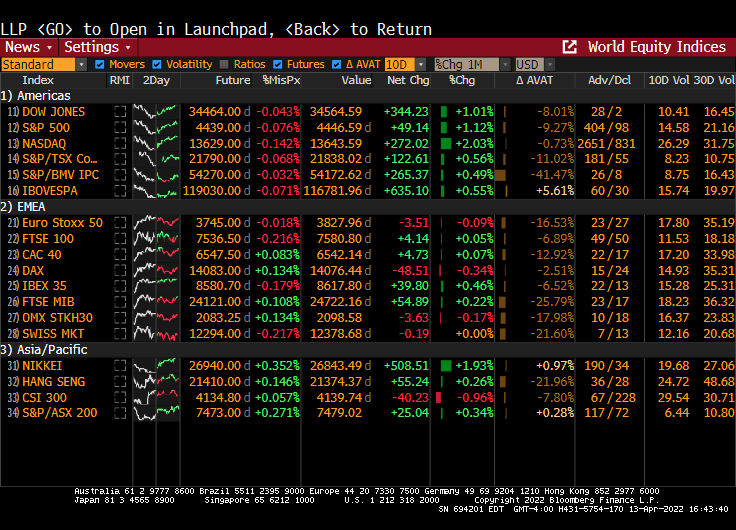

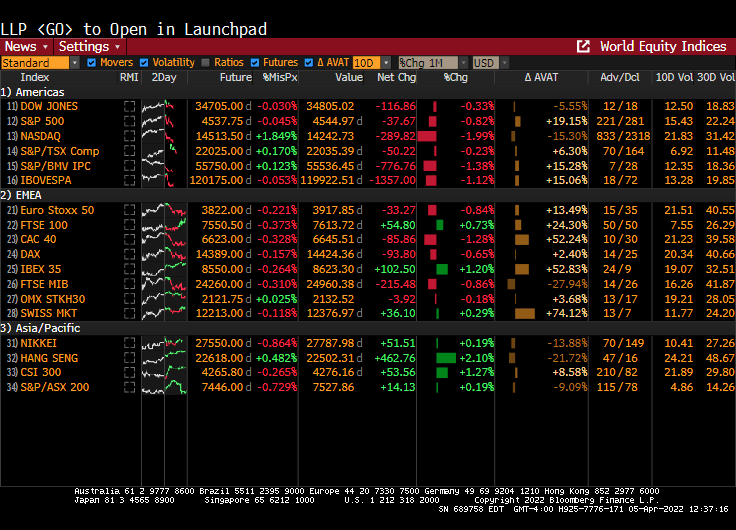

Equity markets are up strongly today as markets sense a weakening in resolve by The Federal Reserve (number of expected rate hikes dropped at 10AM EST).

It appears that we have a “Powell in the headlights” problem.

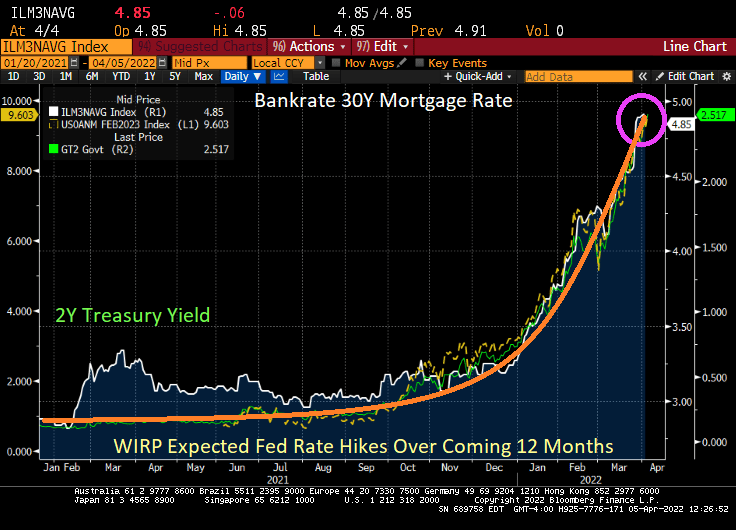

As the US Treasury 2-year yield hits 2.507% (up from 0.128% when Biden was installed as President) and the number of Fed rate hikes over by February 2023 hits 9.6, Bankrate’s 30-year mortgage rate breached the 5% mark at 5.04%.

The most recent data from on existing home sales show YoY sales in negative territory as The Fed begins in monetary fireball tightening.

St Louis Fed’s Bullard said The Fed is “behind the curve.” Ya think??

The Fed’s minutes from the most recent meeting indicates that The Fed will shedding $95 billion a month from it swollen balance sheet. At almost $9 trillion mostly populated by Treasuries will be the first asset to run-off the balance sheet (there is almost $1 trillion of Treasuries maturing in 2022 and $856 billion maturity in 2023, etc), The Fed plans to shrink the balance sheet while, at the same, raising The Fed Funds target rate from it near zero levels.

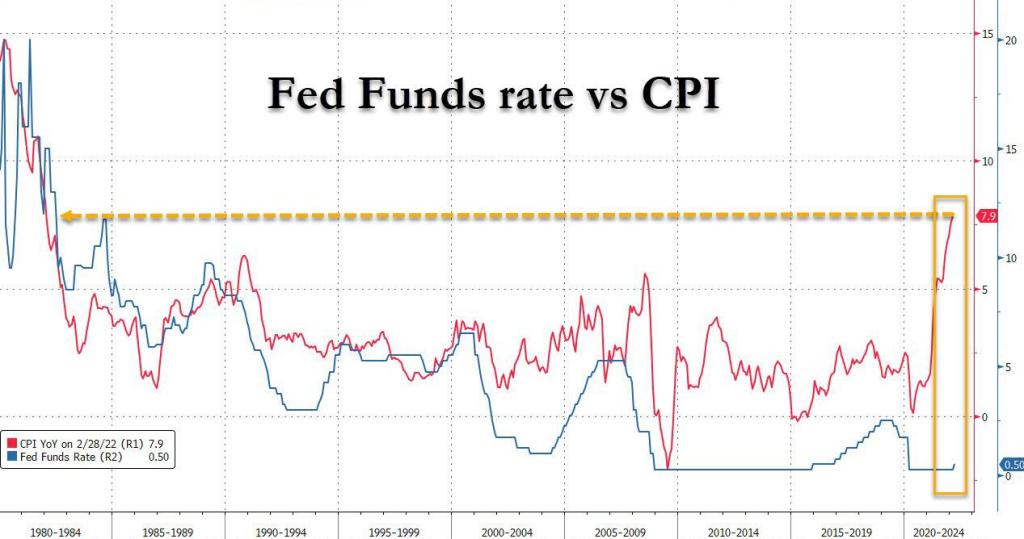

The Federal Reserve has ignoring rules like the Taylor Rule since the financial crisis of 2008-2009, but seemingly are paying attention to the Taylor Rule because of 7.9% inflation. The Taylor Rule is suggesting a 20.42% Fed Funds target while the current target rate is 0.50%. Now THAT would be a real shock to the economy.

Federal Reserve Governor Lael Brainard said the U.S. central bank will continue to tighten policy methodically and shrink its balance sheet at a rapid pace as soon as May.

Brainard’s hawkish remarks sent bond prices crashing and 10Y bond yields up over 16 bps.

While Bankrate’s 30Y mortgage rate is down slightly today, the surge in the 10Y and 2Y Treasury yields could push mortgage rates above 5% by tomorrow,

Even Europe is feeling Brainard’s wrath. Italian 10Y sovereign yields are up almost 20 bps.

The NASDAQ index is down 300 points on Brainard’s utterance.

Gee thanks Lael from all us wanting to finance the purchase of a house.

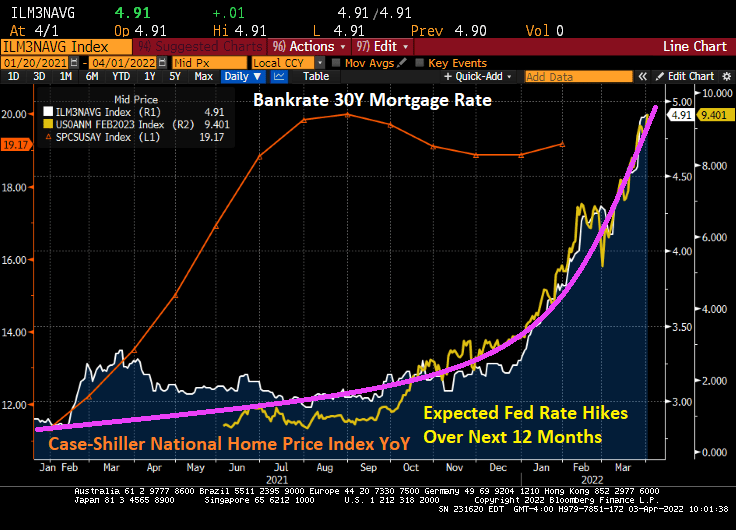

Consider what has happened since President Biden was elected. The S&P 500 total return index (green index) has risen thanks to The Federal Reserve’s balance sheet expansion (orange line) with COVID. Until 2022 when the expectation of Fed rate hikes surged from 3 in late December 2021 to 9.4 expected rate hikes over the next 12 months (yellow line).

The US Treasury total return index (white line) has gotten crushed with The Fed’s signals of rate hikes and quantitative tightening (QT). Call it “White Line Fever.” The commodity total return index (blue line) has surged as The Fed’s expected rate hikes have risen from 3 to 9.4 in 2022.

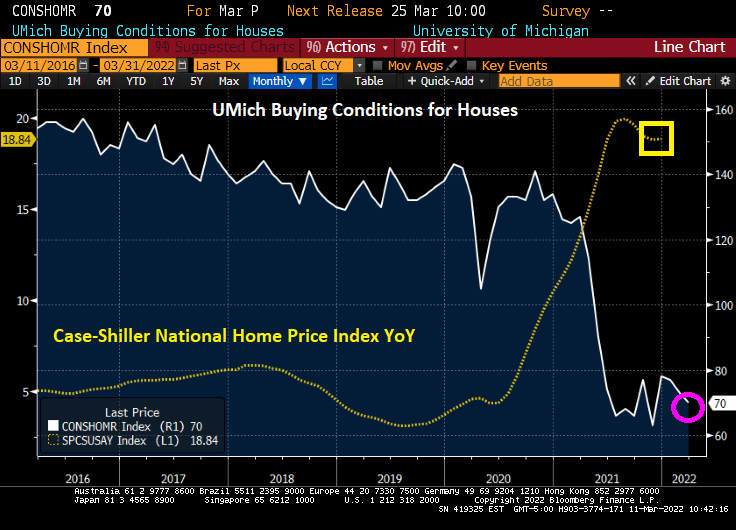

Is The Fed causing a Great Reset in housing? In 2022, we see the surge in Fed rate hike expectations leading the 30-year mortgage rate to be nearly 5%. The last Case-Shiller home price index was for January and it was still raging at 19.17% YoY growth. Let’s see if The Fed’s QT will slow down home price growth. But home prices are growing at 4x 30-year mortgage rates.

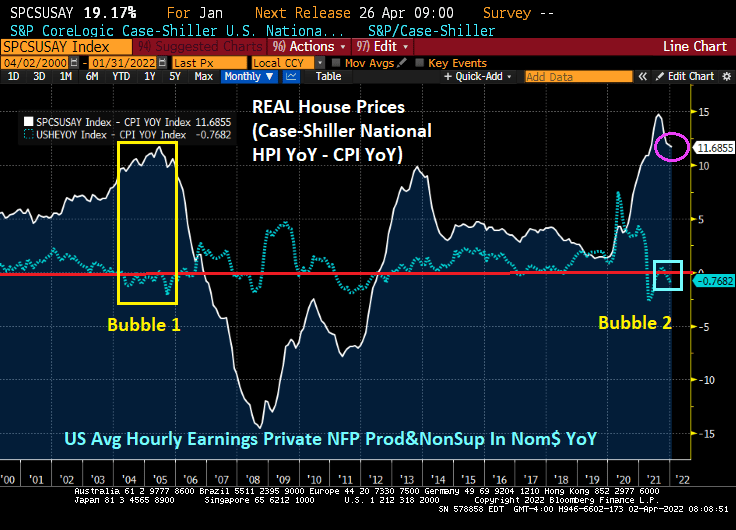

The Dallas Federal Reserve issued a warning recently that a housing bubble is brewing … after the economy drank its magic monetary elixir. We can see the housing bubble clearly (defined as the spread between REAL home price growth and REAL average hourly earnings). Notice that the current housing bubble looks similar to the infamous 2005 housing bubble. And the US is seeing several months of the spread between REAL home price growth and REAL hourly earnings be even higher than the peak of the 2005 bubble.

The Federal Reserve is starting to slow down its asset purchases, so we should see a cooling of the housing bubble. Unless, of course, The Fed changes its tune from quantitative tightening (QT) back to quantitative easing (QE) … again.

The Dallas Fed has a measure of housing “exuberance” which shows a bubble forming, but not there yet. I like the spread between real house price growth and real hourly earnings better.

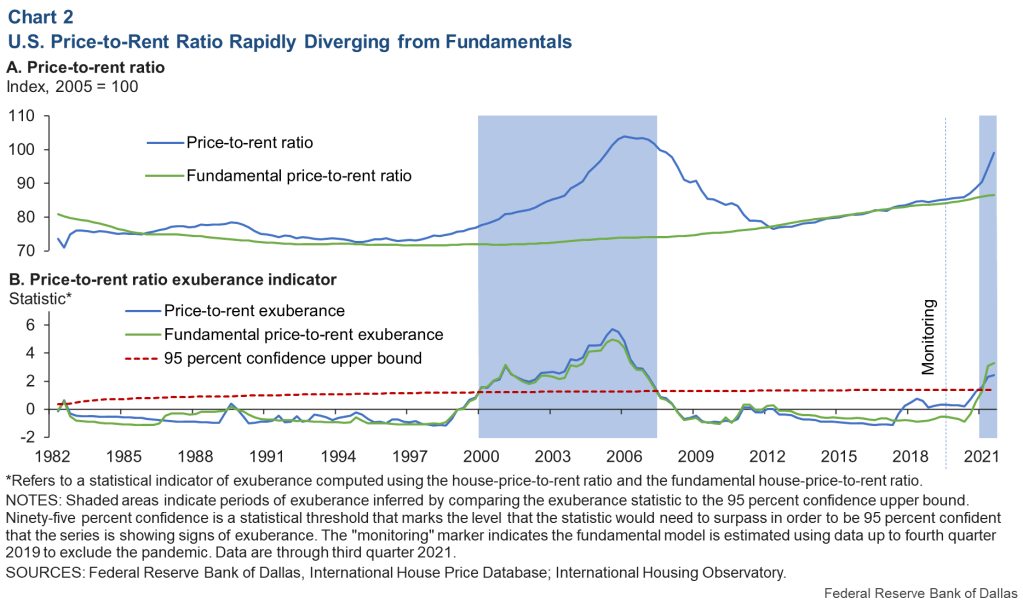

The Dallas Fed also has a price-to-rent chart also showing growing exuberance.

But if we look at the Case-Shiller National HPI YoY to US CPI Urban Consumers Owners Equivalent Rent of Residences YoY we see that the US is currently experiencing a price-to-rent ratio higher than the peak of the 2005 house price bubble. What is the culprit? The vast expansion of monetary and fiscal Stimuylpto surrounding the Covid outbreak in early 2020.

So, the Dallas Fed thinks that is a house price bubble is brewing, but it has actually been in the works since QE3 in 2013 (bubble 2), but really took off with The Fed’s stimulypto and Federal COVID spending surrounding the COVID outbreak in early 2020.

Wasting away again in Biden/Pelosiville, looking for my lost inexpensive gasoline and food. Some people say that Putin is to blame, but we know its Biden/Pelosi’s fault.

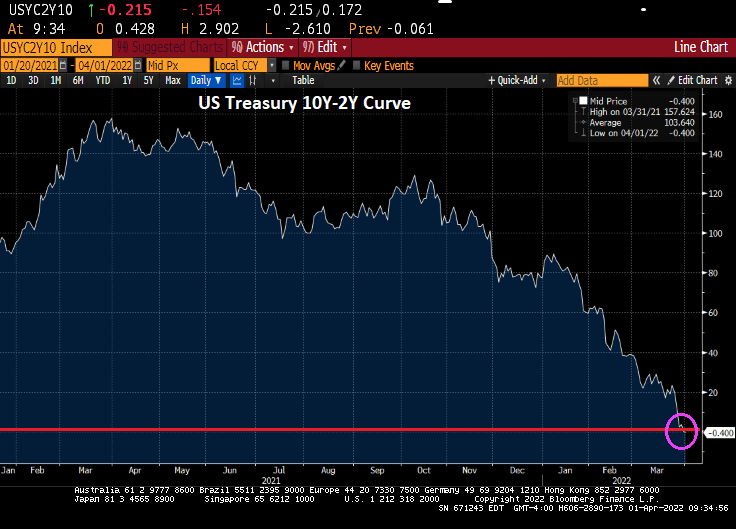

The US Treasury 10Y-2Y yield curve just inverted, generally a precursor to a recession. Called it, nothing but net!

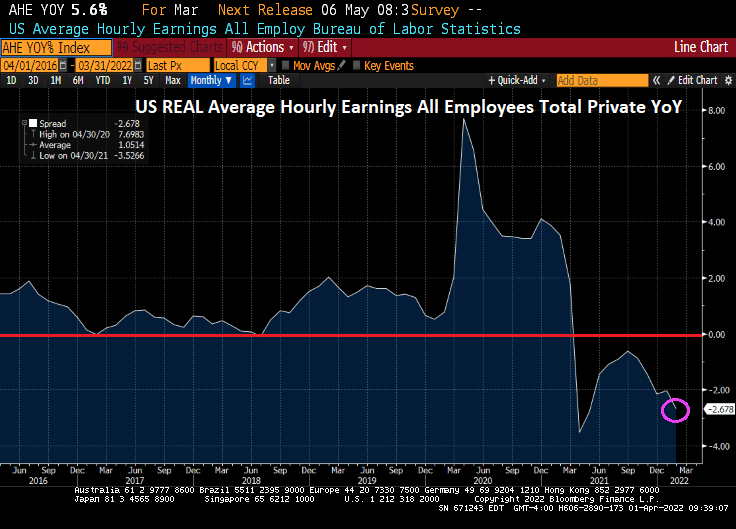

Meanwhile, today’s jobs report shows that Bidenflation is crushing America’s wage growth. While average hourly earnings grew to 5.6% YoY, we are still seeing inflation growing at 7.9% YoY meaning that inflation is reeling hurting the middle class and lower-income households.

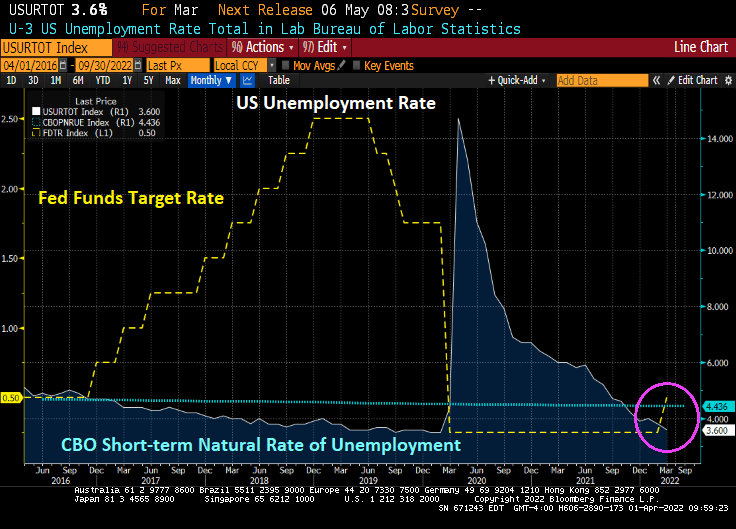

The good news is that the U-3 unemployment rate fell to 3.6%, almost back to the Trump-era unemployment rate of 3.5% prior to the Covid outbreak. And the unemployment rate remains below the CBO’s short-term natural rate of unemployment indicating that the labor market is OVERHEATED.

Today’s jobs report was pretty good, as we would expect from a recovery caused by governments shutting down economies, then reopening them. 431k jobs were added, but less than last month’s jobs added of 678k and less than the forecast 490k.

The number of people NOT in the labor force fell slightly, but it still around 100 million. The number of people holding multiple jobs to overcome Bidenflation rose to 7.5 million.

On the mortgage front, Bankrate’s 30-year mortgage rate rose to 4.90% as the 2-year Treasury rate (yellow) rises and the number of expected Fed rate hikes over the coming year is 9.26%.

As of today, Jerome “Nero” Powell and The Gang at The Federal Reserve have not trimmed the Fed’s balance sheet and have only raised their target rate once under President Biden.

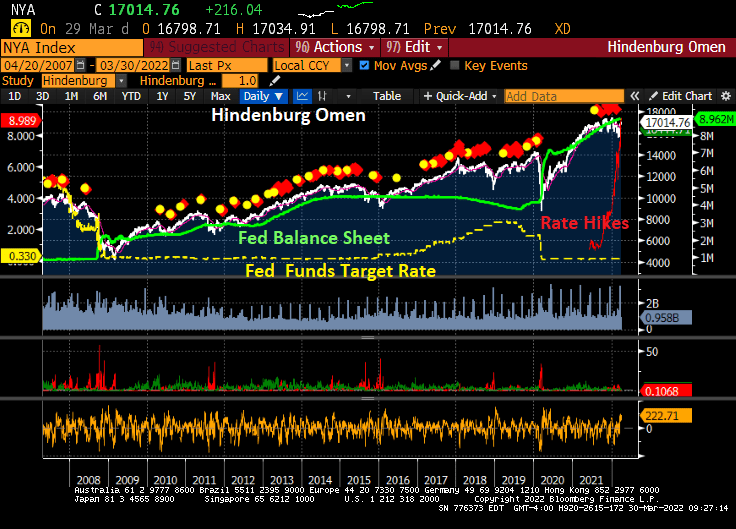

Here is the Hindenburg Omen, named for the catastrophic explosion on May 6, 1937 at Lakehurst Naval Air Station in New Jersey. The Hindenburg Omen was flashing red before the stock market correction of late 2007-2009. But, the Hindenburg Omen has flashed red repeatedly since the financial crisis, yet the S&P 500 index has kept rising. The reason? Repeated policy errors by The Fed leaving monetary stimulus in place for too long leading to a bubble forming in the stock market.

The Shiller CAPE (Cyclically-adjust price-earnings) ratio is at the second highest level since the 1800s. The highest point was the infamous Dot.com bubble and bust in 2000/2001.

Since The Fed continues to say “We have a plan!” to slow/shrink The Fed’s balance sheet and raise their target rate … it has not done anything yet (other than a 25 basis point bump at the March meeting).

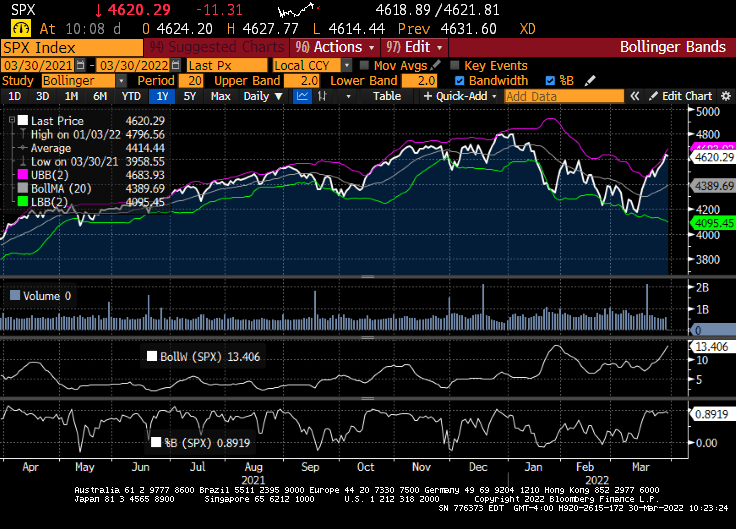

I am not advocating technical analysis for stocks, but the Bollinger Band analysis for the S&P500 index is showing the S&P 500 index near the top band indicating that a decline in likely.

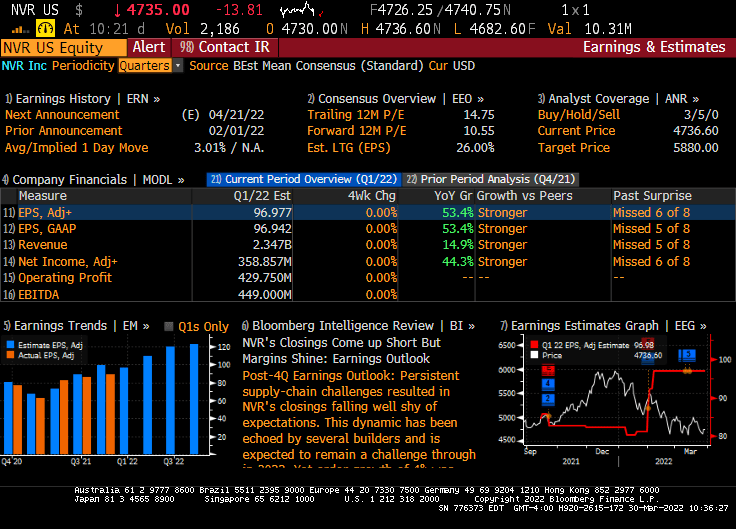

Today, the US equity market in essentially flat given the massive uncertainty about the Russia/Ukraine situation and whether the US economy is slipping into darkness. But this morning, Federal government blessed companies (healthcare, solar energy and Blackrock) are doing quite well, while homebuider NVR is taking it on the chin thanks to hints that The Fed will raising rates.

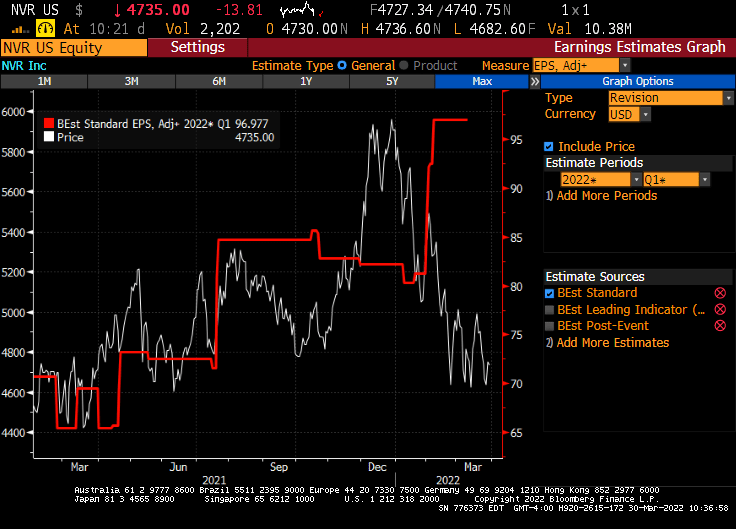

Now, NVR (Northern Virginia Homes, Ryan Homes) had explosive earnings growth in their February 1, 2022 report.

But the market is pricing in the crushing Fed rate hikes that are expected.

So, will Foul Powell pull a Volcker and raise rates and crush the economy (and stocks)? Or will Foul Powell And The Fed gang let inflation burn out of control, but preserve the massive asset bubbles?

According to Fed Funds Futures data, The Federal Reserve is now forecasting 9 rate increases over the next year.

Fed Funds Futures are pointing to 8.924 rate hikes by the Fed FOMC meeting on February 1, 2023.

The US Treasury 10Y-2Y curve flattened by 5.5 bps today with the entire curve downshifting.

The Federal Reserve reminds me of The Office episode “Malone’s Cones.” They can’t really explain why they kept rates so low for so long (policy error) and seem to risk collapsing the market with rapid rate hikes without much sensible explanation.

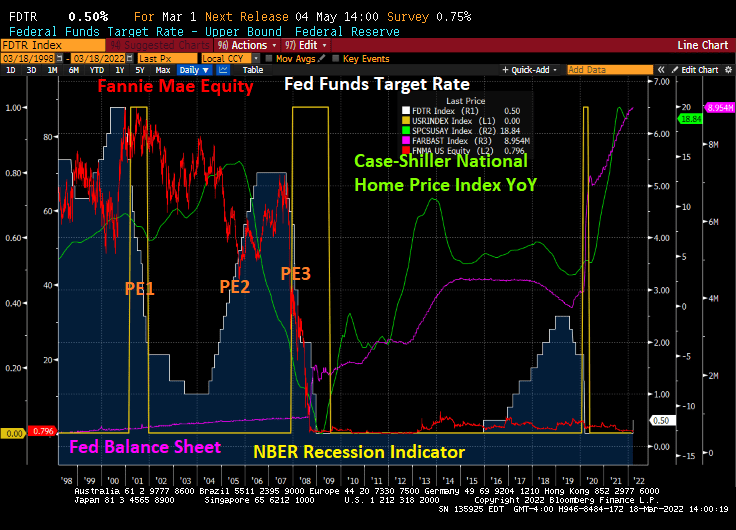

The Federal Reserve is not mentioned in the movies “The Big Short” or “Margin Call”, but The Fed’s policy errors played a big role in the demise of Fannie Mae’s and Freddie Mac’s equity prices.

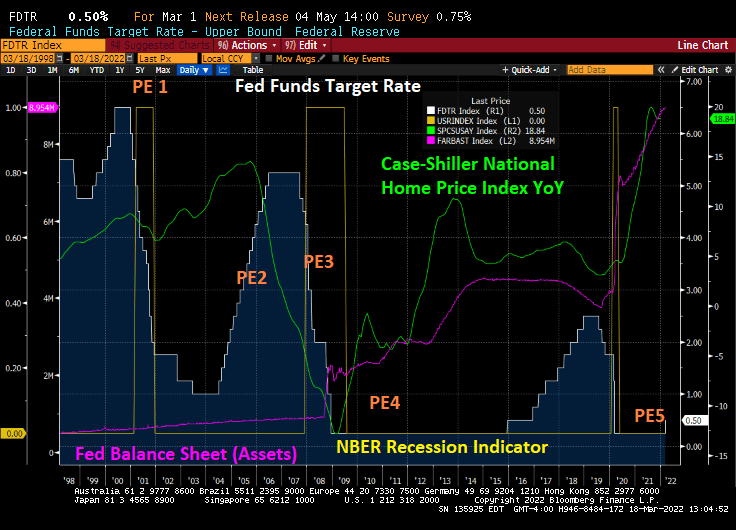

Here is a chart of The Fed’s many policies errors. Let’s start with The Fed lowering rates too fast around the 2001 recession. They pushed their target rate from 6.5% in December 2000 down to 1.75% after one year and then down to 1% (PE1). As home price growth accelerated, The Fed engaged in their second policy error — raising rates too fast resulting in a dramatic cooling of home price growth. Then came Policy Error 3: the dropping of The Fed Funds Target rate from 5.25% in September 2007 to an eventual 0.25% in December 2008.

With the election of President Obama, The Fed engaged in Policy Error 4: keeping The Fed Funds Target rate too low for too long, combined with their massive asset purchase programs (QE).

Finally, The Fed (under Yellen) finally raised The Fed’s target rate ONCE under Obama, but started raising rates once Trump was elected. The Fed also slowed their QE under Trump which as called “Fed policy NORMALIZATION.” Then COVID struck and The Fed engaged in Policy Error 5: keeping rates too low for too long … again while massively expanding their balance sheet.

Fannie Mae and Freddie Mac, the DC mortgage giants were done in by The Fed’s whipsaw Policy Error machine.

Now we are embarking on PE 5: Powell and The Fed Gang not raising rates but signalling that they will. Like the play “Waiting for Godot.”

You must be logged in to post a comment.