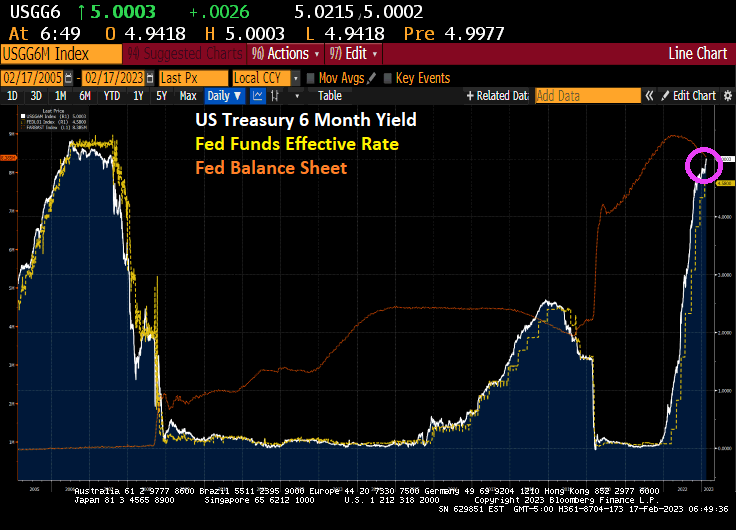

Well, here we are again. Back to 2007 and the housing bubble and subsequent financial crisis. The US Treasury 6-month yield is back over 5%, a yield we haven’t seen since August 8, 2007.

Well, there is one notable difference. The Fed’s balance sheet is still at $8.4 TRILLION whereas it was only $866 billion on August 8, 2007.

The US Treasury yield curve? It remains deeply inverted as The Fed withdraws liquidity.

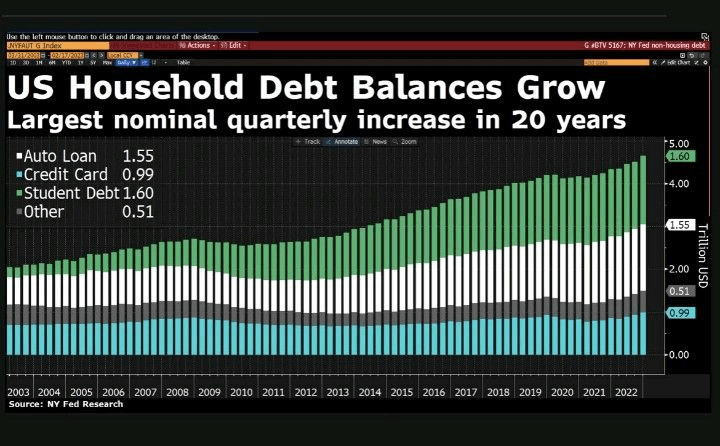

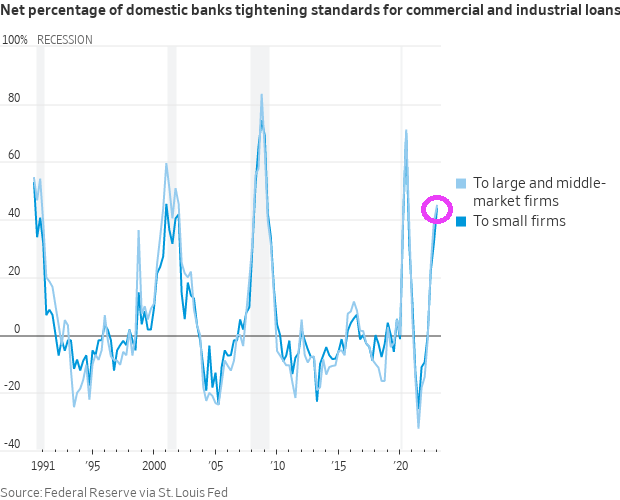

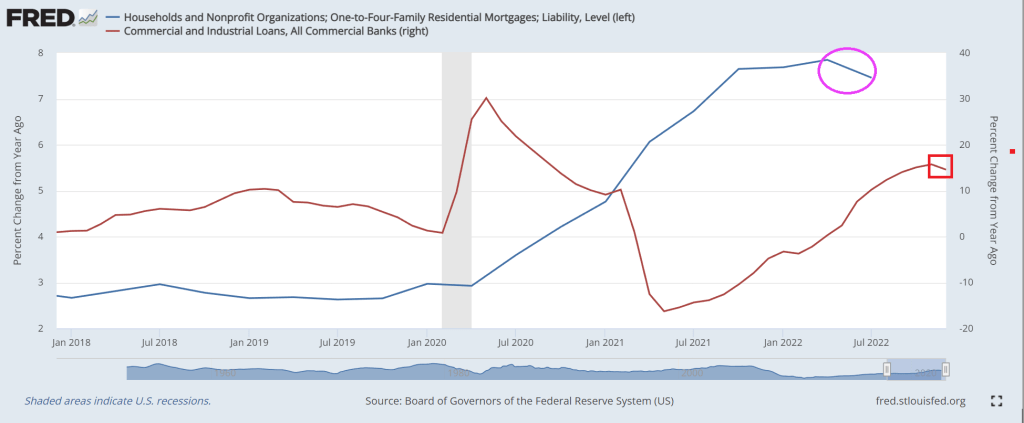

And then we have this diddy. US household debt balances increase, the largest nominal quarterly increase in 20 years.

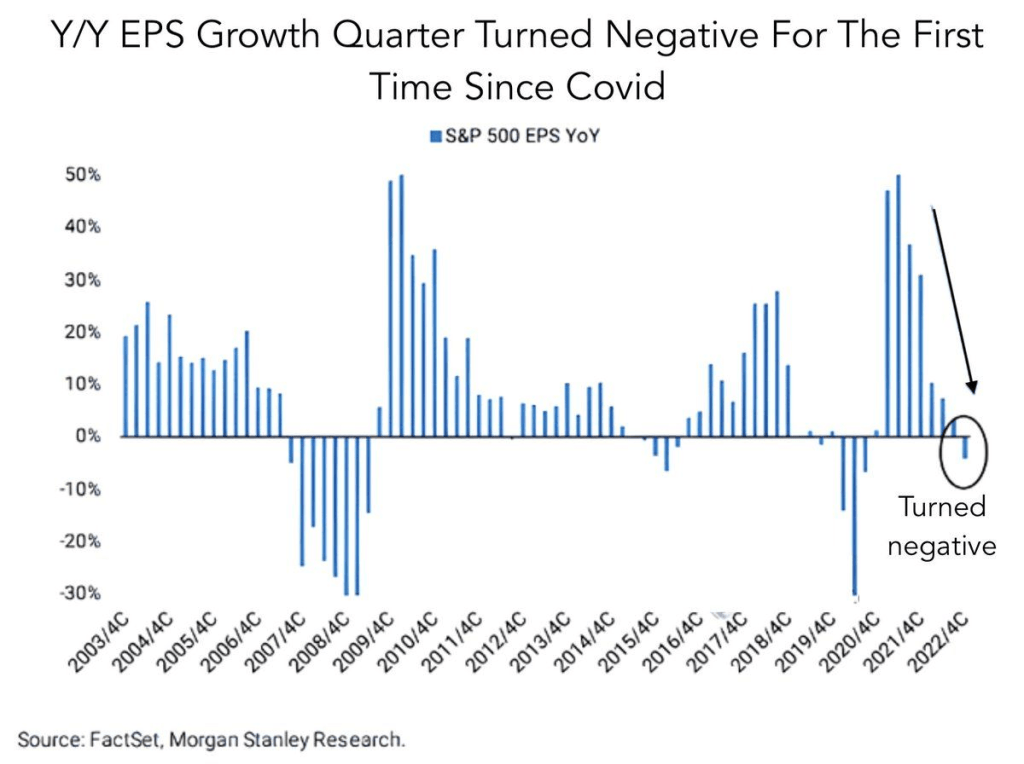

Also, we have the year-over-year EPS growth has turned negative for the first time since Covid.

President Biden loves to demonize his opponents like Republicans over spending and the Federal budget. Biden argued that his budget won’t increase taxes on Americans making less than $400,000 a year and will ultimately cut the deficit by $2 trillion over the next decade. The president has yet to release his budget plan but has promised to do so by March 9.

Of course, Biden ignores “the inflation tax” which is crippling American households (negative REAL hourly earnings growth for 22 straight months). And while he won’t raise taxes on Americans making less than $400,000 (he doesn’t have the authority), he loves to spend money like most of Congress. Without tax increases, The Federal Government will have to issue MORE debt and run budget deficits in perpetuity.

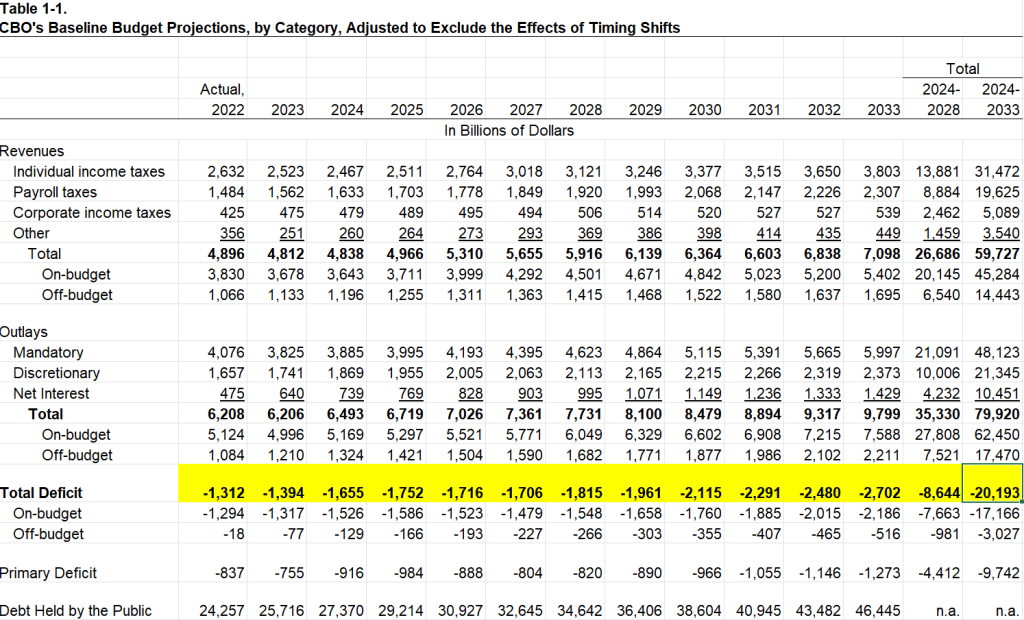

Here is the sickening forecast of Federal budget deficits. Budget deficits are forecast to keep rising and are project to hit -$20 TRILLION over the next 10 years.

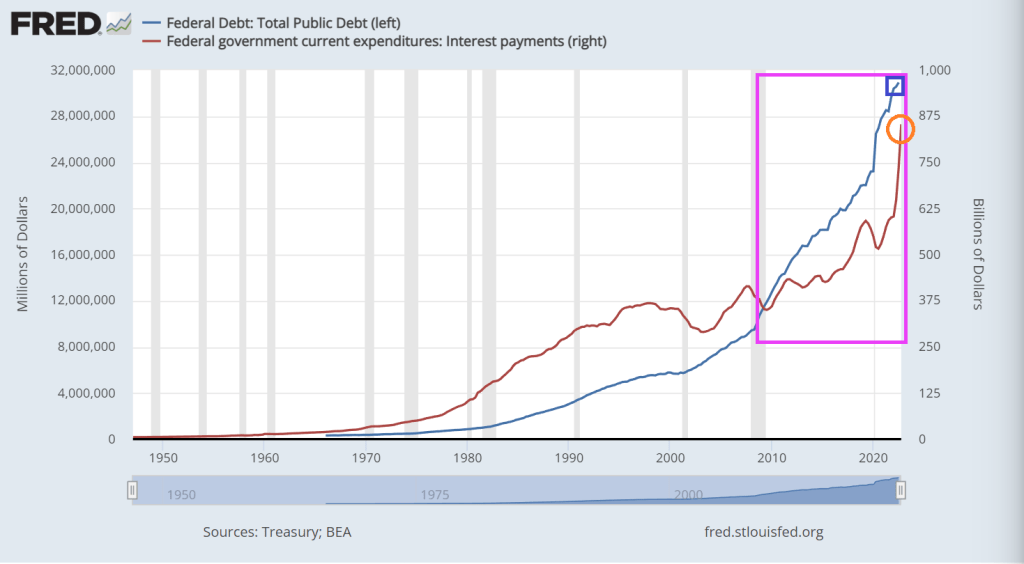

The US is already experiencing irresponsible growth in Federal debt and interest payments on the Federal debt.

Interest costs will nearly triple in the next decade. The Federal Reserve has increased interest rates eight times since early 2022 to combat high inflation — which has contributed to the significant increase in the federal government’s cost of borrowing. In CBO’s projections, such costs would rise from $475 billion in 2022 to $1.4 trillion in 2033. Over the upcoming decade, CBO projects that net interest payments will total $10.5 trillion; relative to the size of the economy, net interest would grow from 2.4 percent this year to 3.6 percent in 2033. In 2030, the ratio of interest to GDP would total 3.3 percent, the highest recorded since 1940 (the first year for which such data are reported).

US REAL average hourly earnings fell … again … to -1.8% year-over-year (YoY) from a revised -1.6% YoY in Deember. That makes 22 straight months of negative hourly earning growth.

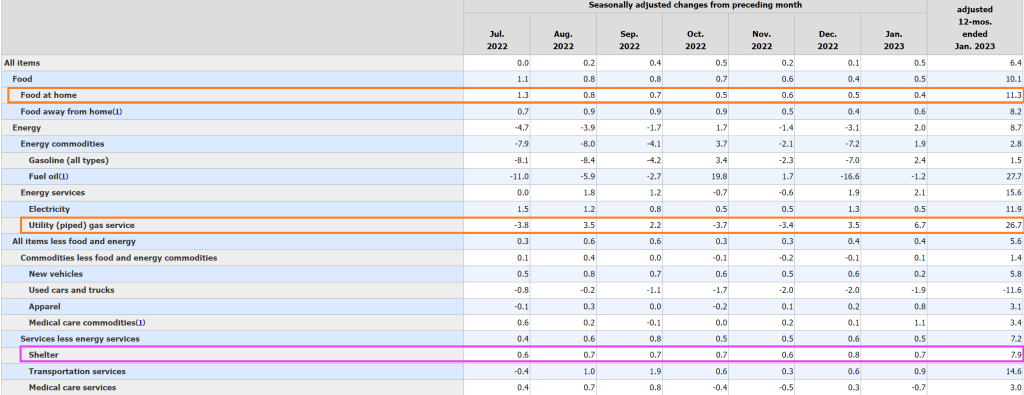

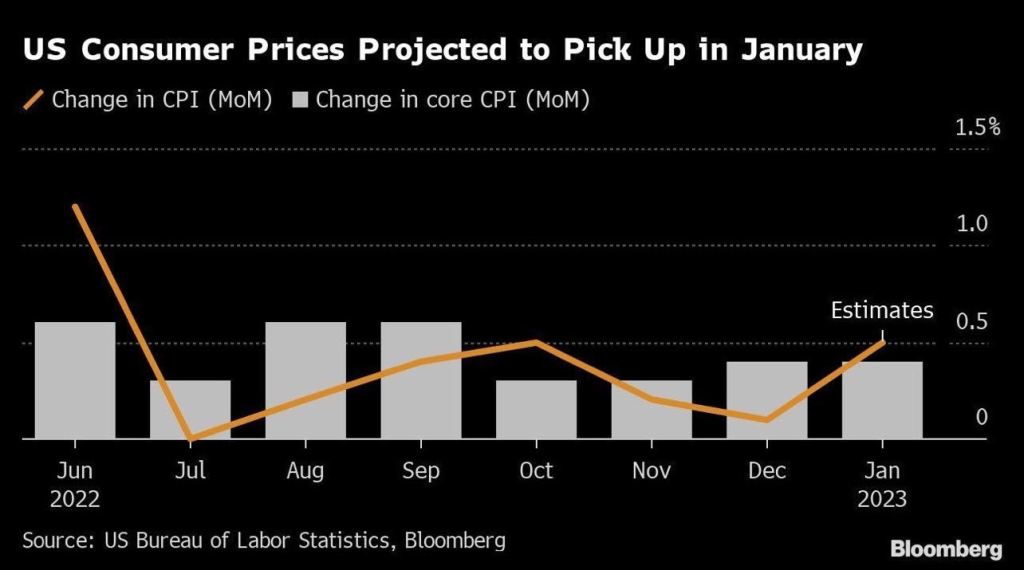

CPI Month-over-month (MoM) was revised upward for December, and increased from 0.1% in December to 0.5% in January. CORE CPI remained unchanged from the upward revision in December to 0.4% MoM.

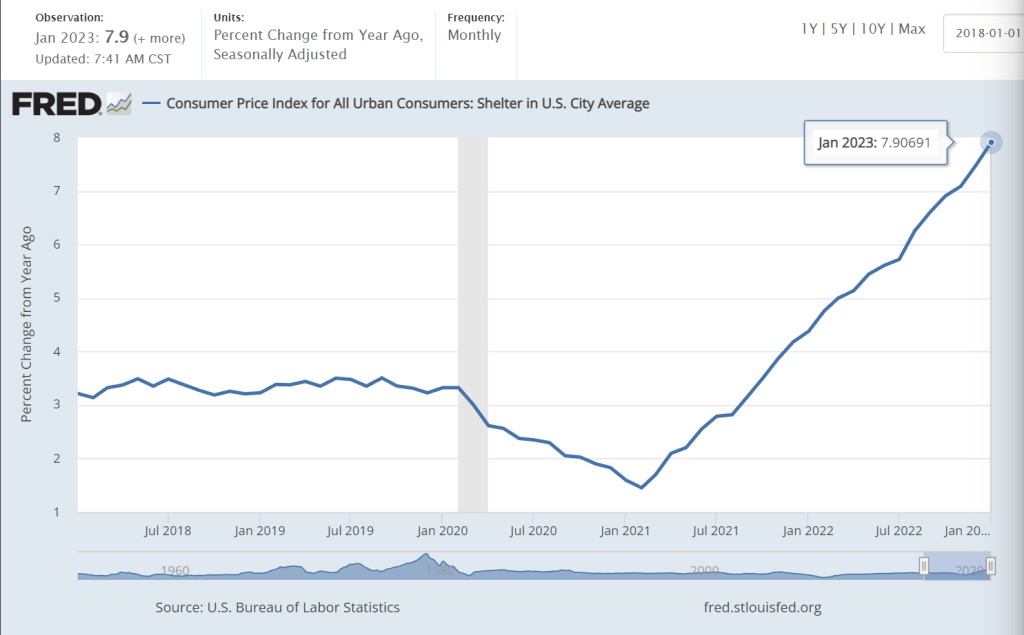

Components of inflation include FOOD AT HOME (up 11.3% YoY), utility (piped) gas service (up 26.7% YoY) and shelter (up 7.9% YoY). So, the middle-class inflation tax (food, heating, housing) remains high.

Do I detect a trend in shelter inflation??

Hey, I thought Treasury Secretary Janet Yellen said inflation was transitory. 22 straight months of negative hourly earnings growth seems more permanent than transitory.

While much of the US is down from 2022 peaks in home price. but it is The West where home prices are down the most (just like 2008 where the Inland Empire of California, Phoenix and Las Vegas crashed in term of home prices).

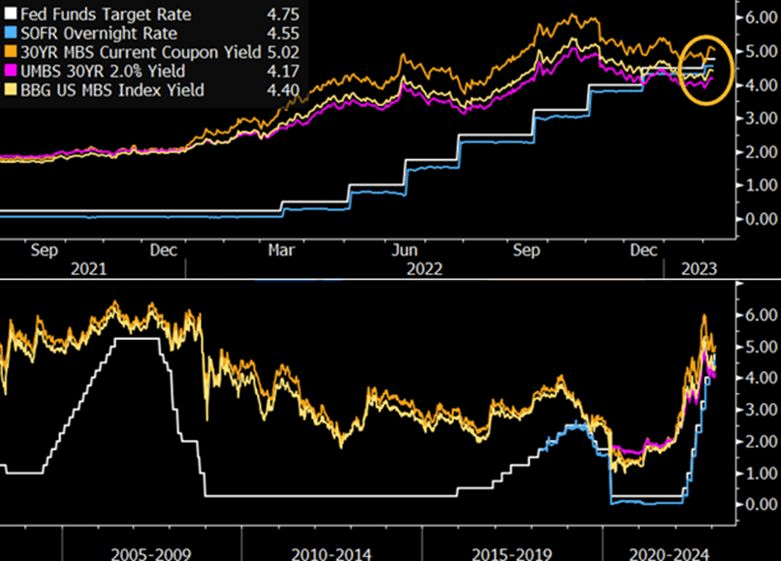

The most recent tightening by the Federal Reserve has pushed the federal funds target rate above mortgage-backed securities yields for the first time in history. Though this poses clear challenges of carry for MBS holders, selective investments in specified pool and collateralized mortgage obligations (CMOs) could provide incremental returns.

Inflation started under Biden, but the massive expansion in money supply (M2) begin with Covid in 2020.

Once this latest spending splurge kicks in, we will see rising inflation again. After all, Biden and Congress have gotten the taste for massive spending bills (like vampires) and spending likely won’t slow down.

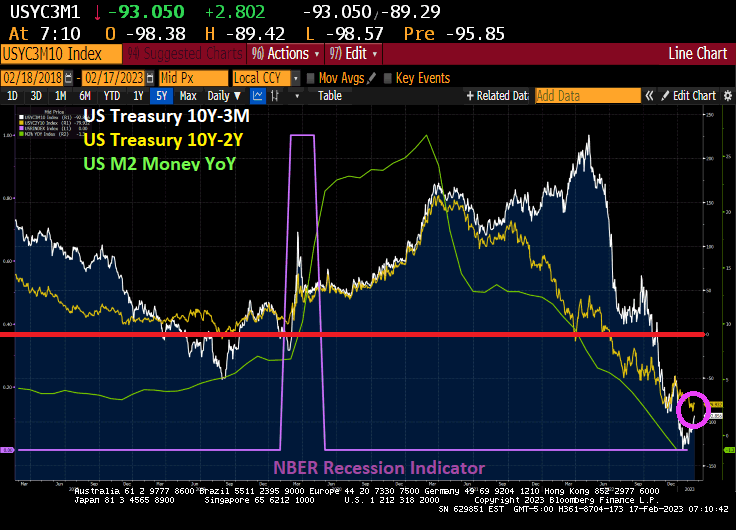

Biden’s State of the Union address saw him bragging about his record job creation (actually, it was the private sector, not Biden than created jobs) and historic unemployment rate. What Biden didn’t mention (along with not discussing the porous Mexican border with fentanyl pouring across or why he failed to shoot down a Chinese spy balloon until after it has passed over numerous military reservation) is that the unemployment rate always hit a low point just prior to a recession.

So, here we sit at 3.4% unemployment. But we also see the US Treasury yield curves (10Y-3M and 10Y-2Y) remaining deeply inverted.

The US Treasury 10-year yield is up 5.5 basis points today.

And Bankrate’s 30-year mortgage survey rate is up slightly today.

Here is where we set today. The cost of insuring for a US debt default remains elevated as the US has hit its statutory debt limit. This is happening at the effective rate of interest on US mortgage debt is rising.

Help us McCarthy! Because Biden and Schumer don’t want to cut ANY spending.

The one statement that Biden made in his State of the Union Address that was factually accurate was that inflation is coming down. Of course, he then blew it by saying he inherited inflation from Trump which was not true. Headline inflation (CPI YoY) was only 1.4% when Biden was sworn-in as President and rose to 9.1% YoY by June 2021 before finally starting to decline.

But despite the cooling of inflation (and M2 Money growth), The Fed seems hell bent on increasing their target rate, now forecast by Fed Funds Futures to peak in July 2023 at 5.123% before pivoting.

President Biden had better give his State of the Union Address before the economy worsens any more.

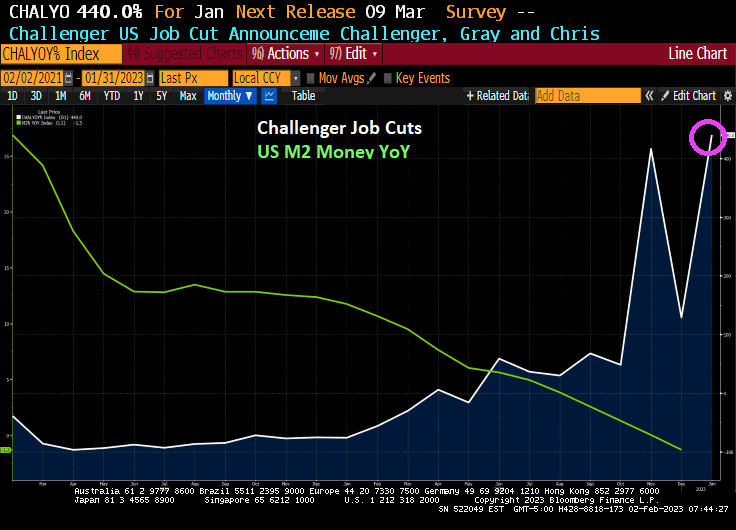

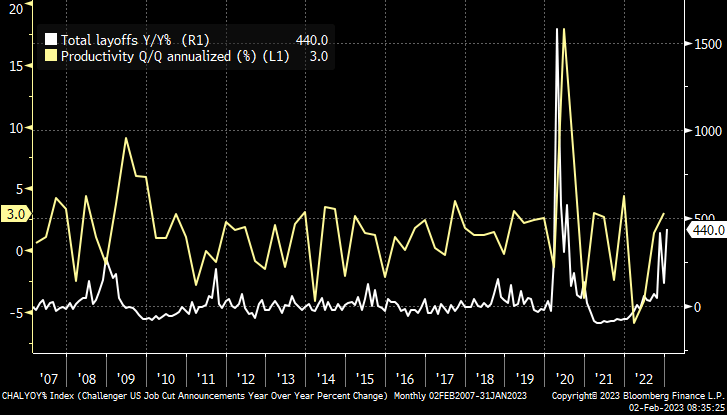

In January, the Challenger, Gray and Christmas jobs cuts index was a doozy. Jobs cuts rose 440%. This is happening as The Federal Reserve keeps its feet on the monetary brake pedal.

The Challenger report shows a big jump of 135.8 percent in layoff intentions to 102,943 in January, up from 43,651 in December and 440.0 percent higher than the 19,064 in January 2022. Many of the job cuts are in the tech sector, but job cuts are now spreading across the economy as a recession looms.

This morning, the US Treasury 10-year yield is down only -3.5 basis points, but it is Europe where the action is. UK is down -16.2 basis points and Italy is down -14.8 bps. UPDATE: US 10Y yield down -5.3 BPS, Italy 10Y down -29 bps.

You must be logged in to post a comment.