Under Bidenomics, with its high inflation rate and crushing negative wage growth, consumers are draining their savings and living on a prayer …. and consumer credit to cope.

What is worriesome in the transition rates (like current to 90-days delinquent) Credit cards (blue) and auto loans (red).

A closer look at credit card delinquency rates on a year-over-year (YoY) basis, showing the fastest growth in delinquencies since the Covid economic lockdowns.

Then we have commercial real estate delinquencies are now the highest the have been since 2013.

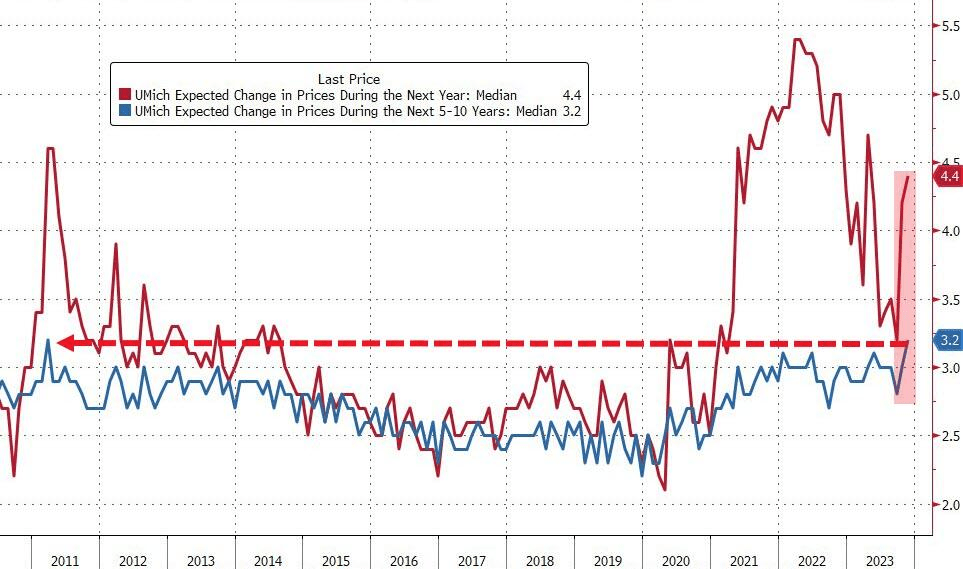

Meanwhile, University of Michigan consumer sentiment about inflation spiked to 4.4%. That is the highest medium-term inflation expectation since 2011.

Call it “The Rich Men North Of Richmond” economy. Where the coastal elites drive the US economy off the cliff with insane spending and borrowing with much of the benefits flowing to big political donors, not the middle class. Think of Span Bankfraud Parboiled as an example.

President Biden loves to spend billions and go on endless vacations (he is in Rehobeth Beach Delaware yet again). He (illegally) forgave student debt, keeps spending billions on Ukraine and keeps spending on failed green energy nightmares.

Biden and his allies will tout the latest GDP numbers as an example of how marvelous Bidenomics is. BUT that GDP report was driven largely by consumer spending.

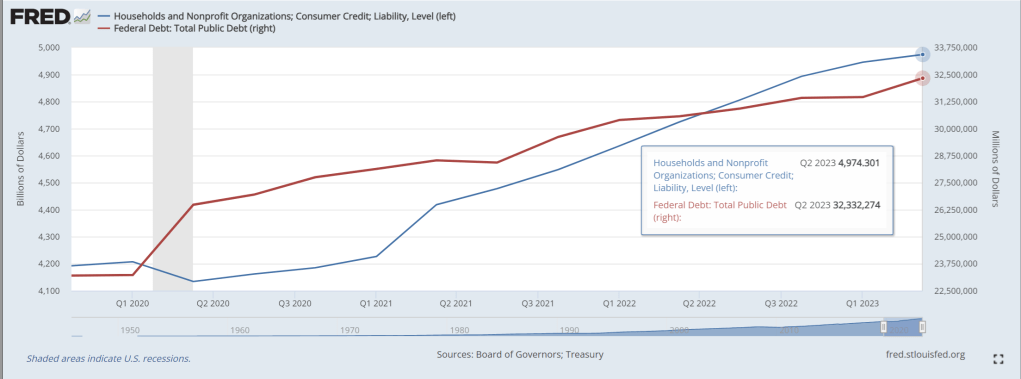

Since the Covid outbreak in 2020, Federal (public) debt is up 45%! Wow. And consumer debt is up 19% under Biden to cope with inflation (caused primarily by massive Federal spending).

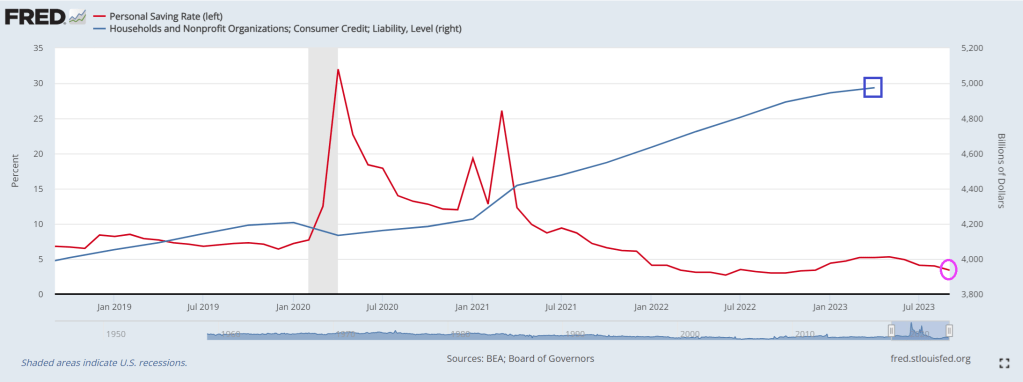

To fuel consumer spending, the personal savings rate has fallen to 3.4%. For point of reference, the personal savings rate in Februray 2020 was 7.7%, so the consumer is running out of gas thanks to inflation and spending.

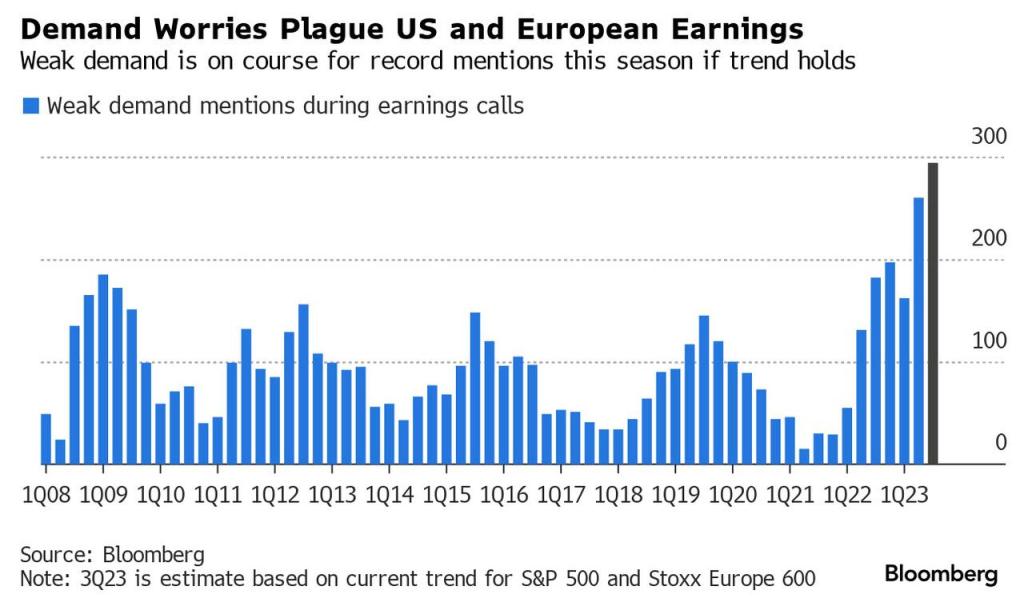

And with a debt-stressed consumer, earnings call revealed concern about continued demand.

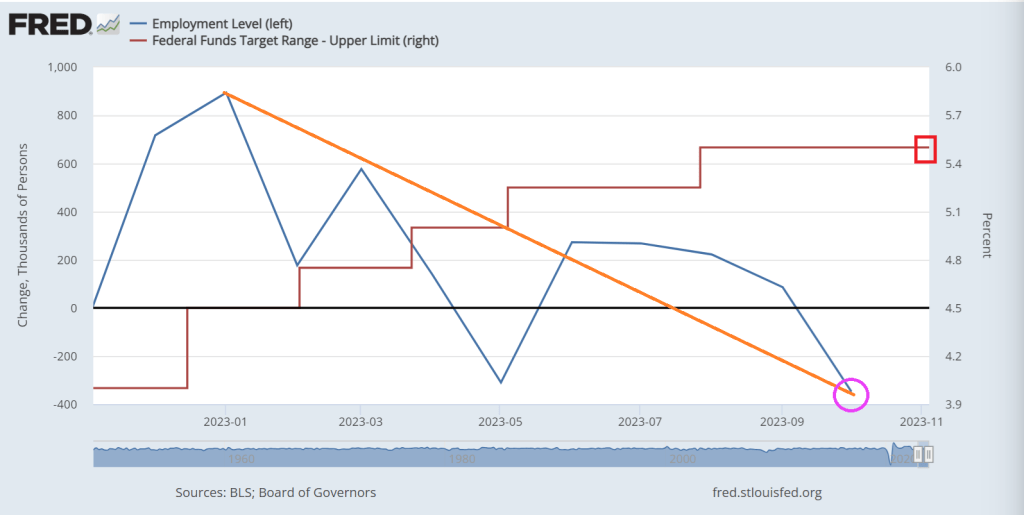

Note the trend in jobs added as The Fed tightened to fight inflation.

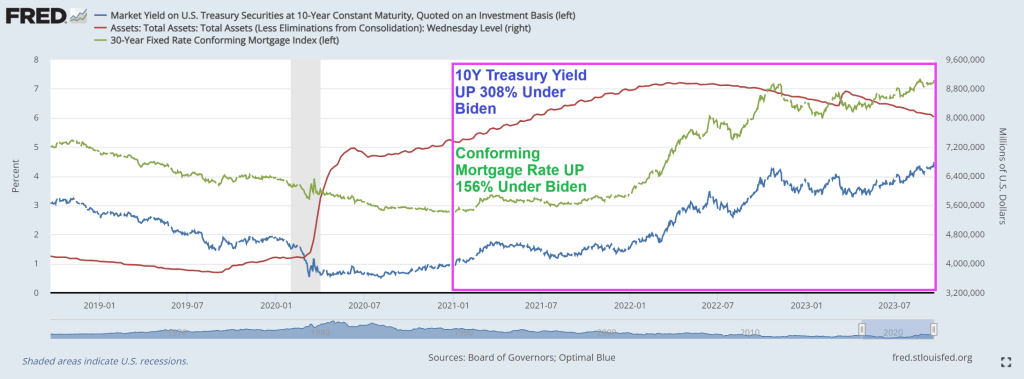

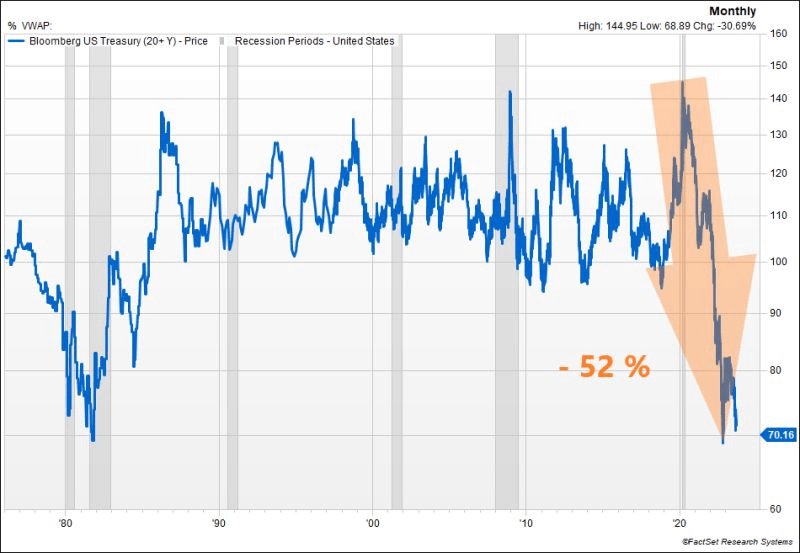

Alarm! US 10-year Treasury yields are soaring along with mortgage rates.

The US Treasury market is witnessing another significant selloff, pushing the 10y UST yield close to the 4.50% mark. The surge in real rates is remarkable, reaching 2.12% for the 10y, a level not seen since 08’. While this might appear attractive in real terms compared to historical benchmarks, could we be on the brink of a third consecutive year of negative performance for US Treasuries? To put this into perspective, such a scenario has never occurred in history.

The conforming mortgage rate is at 7.3%, up 156% under since Biden’s coronation as El Presidente of the United Banana Republics of America. Where political opponents are indicted prior to elections.

In Biden’s Banana Republic economy, the US Treasury 10y-2y yield curve remains inverted.

And then we have Mish’s chart on debt as a percentage of GDP from CBO. Remember, we used to worry about the US breaking the 80% debt to GDP level. It is now projected to be 181%. Wow.

Bidenomics is a train wreck. But unlike E. Palestine Ohio, the site of a train derailment and massive toxic spill (for which Biden has yet to visit), Bidenomics is a continuing train wreck.

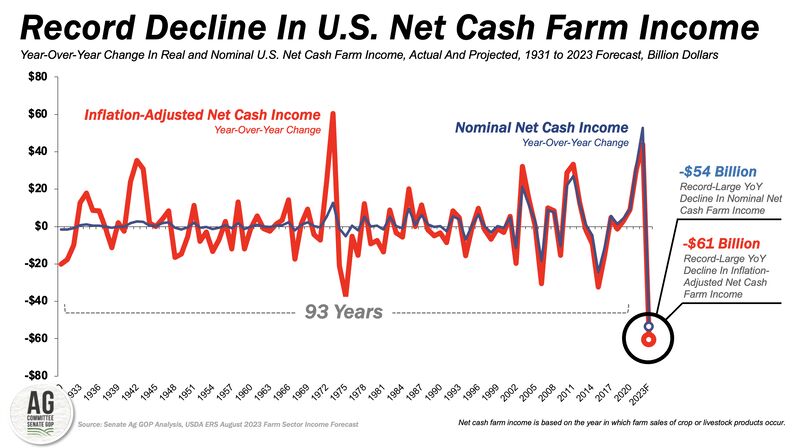

The first chart is the record decline in US net cash farm income. Now in negative growth!

Second, US office vacancy rate is now higher than the peak during the financial crisis. Of course, Covid shutdowns and work from home is the primary driver, but Democrat crime policies are making it more hazardous to work in offices in major American cities, so Bidenomics isn’t helping.

Is Biden acting on behalf of World Economic Forum’s Klaus Schwab? Well, Biden appointed John Kerry, another dimwitted former US Senator like Biden, to be his climate Czar. Kerry wants to shut down farms and starve the population, just like his Overlord Klaus Schwab.

Are Biden and America’s Progressives part of Schwab’s “Great Reset?” Where we eat insects while Biden, Kerry, Schwab and the elites feast on Wagyu beef, foie gras, and expensive champagne. Elitist Treasury Secretary Yellen looks like she could use some Ozempic!

And then we have elitist California governor Gavin “Count Yorga” Newsom opining on Biden’s great “success.” 70% of Americans say things are going badly under Biden, but California Democrat Gov. Gavin Newsom says he’s “very inspired by the master class of the last two-and-a-half years”

Ah, the elite class! Reminds me of the French aristocracy under Louis the 16th and Marie Antoinette. “Let them eat crickets!”

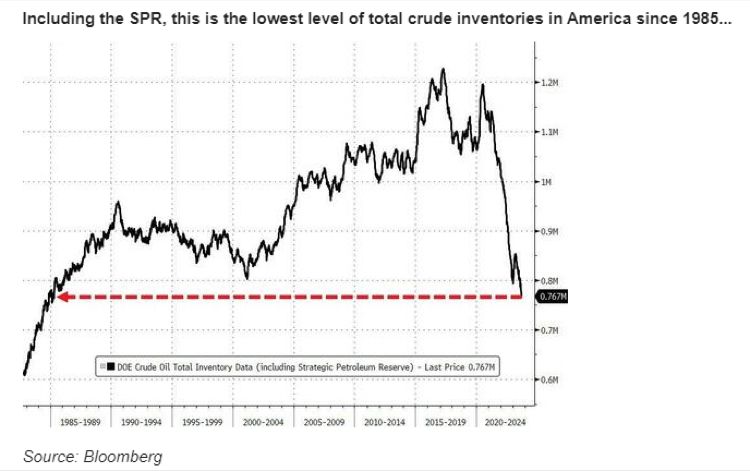

Its hard to watch Biden and The Progressive Greens destroy the enegy security of this great nation. Biden is draining the Strategic Petroleum Reserve, probably in a misguided attempt at ensuring we never go back to abundent petroleum again. Crude oil inventories are now the lowest since 1985.

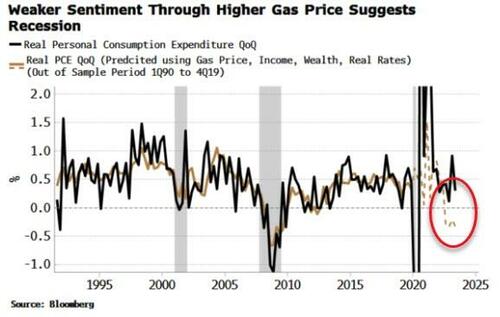

Household spending has kept the US economy afloat, but as growth slows a continued rise in oil and gas prices is poised to push personal consumption expenditure (PCE) lower and thus trigger a near-term recession – with stocks and bonds unpriced for such an outcome.

Once again it has been the redoubtable consumer that has thus far kept a recession at bay. However, Bloomberg Economics (BBE) pointed out in a recent article that negative household sentiment – in confluence with other drivers of household spending – suggests that we should already be in a recession.

A regression model (using income, wealth and real rates) pins PCE growth roughly where it is. But if we add in the University of Michigan’s Consumer Sentiment index, it indicates much weaker PCE growth and thus an economy that would likely be already be in the midst of a slump.

I recreated BBE’s model and got something similar. I then substituted in the Conference Board’s Consumer Index instead of the Michigan survey. This also improves the fit of the original model, but does not paint as negative a picture for PCE. The reason is that the Conference Board’s measure has not deteriorated as much as the Michigan survey.

Why? The divergence between the two likely comes from the Michigan’s greater emphasis on frequent expenditures and business conditions, while the Conference Board’s index is more focused on the jobs market. As an employee, the jobs market has looked pretty good, boosting the Conference Board’s index, while the Michigan survey is more influenced by rising prices and conditions for small-business holders, which have been less rosy.

The Michigan survey is in fact very sensitive to gas prices. In the model, I added the average gas price to the model’s original inputs (i.e. ex Michigan). Doing so also improves the model’s fit, and as the chart below shows, implies notably weaker, and negative, PCE growth – and therefore an economy that would likely already be in a recession.

This highlights that the US economy is potentially on thin ice, with that ice represented by hitherto positive consumer sentiment, driven in no small part by gas prices (and sentiment on how high they are perceived to be) that remain comparatively cheap to the levels they reached last year.

But oil has been rising, driven by excess liquidity, falling inventories and supply cuts.

Tailwinds remain for oil, and therefore the nascent recent rise in gas prices is poised to continue as well. That could be the final straw which unseats the US consumer and tips the US into a recession.

The US warhawks seemed focused on Ukraine’s security, but don’t seem to care about US energy security or the personal welfare associated with open borders. Just ask Mayor Adams of New York City.

The cost of living has been soaring, and our standard of living has been steadily going down.

Coping with inflation is tough for American households where consumer debt is up 19.$ under Biden while the free-spending Federal government’s public debt is up only 16.5%.

“In July 2023, 61% of U.S. consumers live paycheck to paycheck, unchanged from June 2023, but 2 percentage points higher than July 2022. Generally, more consumers of all income brackets reported living paycheck to paycheck in July 2023 than last year,” Alia Dudum, a money expert at LendingClub told FOX Business.

Now, 78% of consumers earning less than $50,000 a year and 65% of those earning between $50,000 and $100,000 were living paycheck to paycheck in July, both up from a year ago, LendingClub found. Of those earning $100,000 or more, only 44% reported living paycheck to paycheck.

Because consumers have so little disposable income these days, retailers all over the nation are experiencing difficulty.

In fact, UBS is projecting that 50,000 stores could close in the United States by the end of 2027…

Analysts at investment bank UBS are forecasting that some 50,000 U.S. stores are likely to close by the end of 2027, because of expected cutbacks in consumer spending, tighter credit and the continued shift to ecommerce.

Store closings could accelerate to 70,000 to 90,000 if retail sales turn out to be weaker than expected, according to UBS.

Actually, I think that losing 50,000 stores is a wildly optimistic scenario.

Hopefully I am wrong about that.

The housing market has also been going haywire.

According to Fortune, the month of August “will become the worst month for housing affordability this century”…

On Monday, the average 30-year fixed mortgage rate reached 7.48%, marking the highest level since the year 2000. Even prior to this recent surge in mortgage rates, housing affordability, as monitored by the Atlanta Fed, had already deteriorated beyond the levels seen at the housing bubble’s peak in 2006. Once this latest mortgage rate surge is factored in, August 2023 will become the worst month for housing affordability this century.

Wow.

Thanks Delaware Joe Biden (as opposed to Country Joe Stalin).

Home prices are going to have to come down, and in some areas they have already fallen quite a bit…

Homeowners are sitting on a negative equity timebomb after losing $108.4 billion on their property values this year, experts say.

The average borrower saw their home equity plummet by $5,400 in the first quarter of 2023 compared to last year – with households in Washington, California and Utah worst affected.

Do you remember the housing crash of 2008 and 2009?

Well, now the next housing crash is here, and it isn’t going to be fun.

For a while there, Joe Biden and his minions could at least boast about the employment market.

But now large companies all over America are laying off workers, and it is being reported that a staggering 1.223 million native-born Americans lost their jobs during the months of July and August…

Staggering figures have revealed that over 1.2 million US-born workers lost their jobs last month while the foreign-born workforce increased by nearly 700,000 – as migrants continue to flood across the border under the Biden administration.

Data from US Bureau of Labor Statistics show that between July and August, there was a staggering decrease of 1.223 million native-born people in the workforce – which is a low not beaten since the jobs crash when Covid hit in April 2020.

The numbers that I have shared with you are nothing to brag about.

But Joe Biden is going to keep trying to pull the wool over the eyes of the American people anyway.

Unfortunately for Biden, it has become quite clear that most Americans have lost faith in him. According to the same Wall Street Journal poll that I mentioned above, 73 percent of U.S. voters now believe that Biden “is too old to run for president”…

For Biden, one of his biggest challenges is age. The Wall Street Journal poll found that about 73% of voters think Biden is too old to run for president while only 47% think Trump is too old. Thirty-six percent of voters think that Biden is mentally up for the job while 46% of voters think Trump is mentally capable of being president.

We have never seen numbers like this for any other president.

Sadly, Biden fully intends to run again. (Especially since half-wit Jill Biden is allegedly running The White House).

And the Democrats will get behind him, because at this point no other candidate is posing a serious threat to Biden. Wait, not Gavin Newsom who almost single handedly destroyed California or Michelle Obama who has absolutely no qualifiications?? Other than being Barry Soetoro’s wife?

“Ice Cream Joe” Biden is at Lake Tahoe for a week, probably to avoid being asked questions about his tin-ear respoonse to the tragic Maui fires that have killed 106 people so far. Instead, Joe is inappropriately chuckling (showing he doesn’t care!) and taking photo ops of him eating ice cream. The Biden administration angered a lot of people when it was announced that households that have been affected by the fires would only be getting a one time emergency aid payment of $700 while he gives billions for Ukraine.

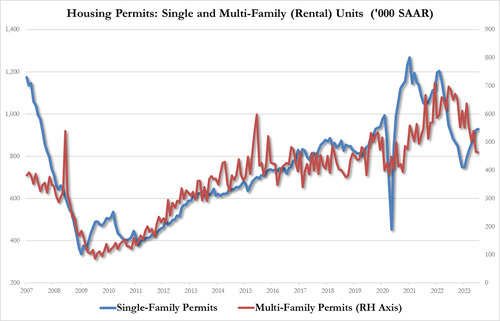

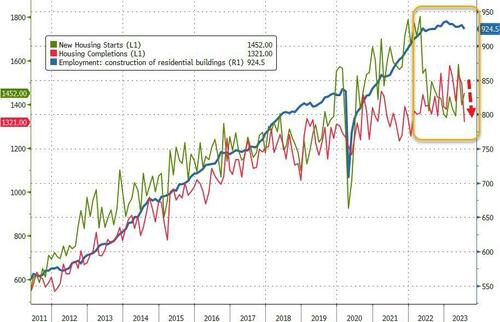

At least housing starts were up 6% year-over-year (YoY).

However, the picture was more mixed with starts rising 3.9% MoM (vs +1.1% exp), but that was impacted by a notable downward revision in June (from -8.0% to -11.7%).Building Permits rose just 0.1% MoM (well below the 1.5% MoM expected).

On a SAAR basis, Permits disappointed (1.442mm vs 1.463mm exp) while Starts were in line at 1.452mm (up from a significantly downwardly-revised 1.398mm in June).

Source: Bloomberg

On the Permits side, single-family rose as multi-family fell:

Single-family up to 930K from 924K, highest since June 2022

Multi-family down to 464K from 465K, lowest since Oct 2020

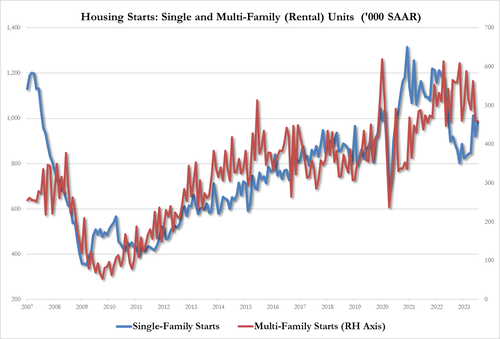

July Housing Starts data followed the same trajectory with rental units growth underperforming single-family:

single-family housing up 6.7% to 983K, up from 921K, highest since May

multi-family housing unch at 460K, tied for lowest since July 2022

Additionally, we note that while Housing Starts and Completions remain well off their 2022 highs, Construction Jobs remain very close to those highs…

Source: Bloomberg

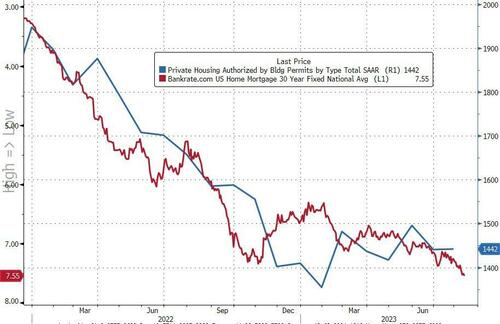

Finally, we note that Mortgage Bankers Association data released earlier this morning showed applications for home purchases dropped again last week (back near 1996 lows) as the contract rate on a 30-year fixed mortgage surged above 7% (highest since Dec 2001).

Source: Bloomberg

This won’t end well.

Speaking of not ending well, mortgage applications decreased 0.8 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending August 11, 2023.

The Market Composite Index, a measure of mortgage loan application volume, decreased 0.8 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index decreased 2 percent compared with the previous week. The Refinance Index decreased 2 percent from the previous week and was 35 percent lower than the same week one year ago. The seasonally adjusted Purchase Index decreased 0 percent from one week earlier. The unadjusted Purchase Index decreased 2 percent compared with the previous week and was 26 percent lower than the same week one year ago.

We quickly found out in June that one downtown San Francisco office building sold for roughly 70% less than its previously estimated value, an ominous sign of what would come as the commercial real estate market dominos appear to be falling.

Now Sixty Spear St., an 11-story building that is 30% occupied and is expected to be entirely vacant by summer 2025, has been sold to Presidio Bay Ventures for $40.9 million, about a 66% discount versus the most recent assessed property value of $121 million, according to local media SFGATE.

“We acknowledge the formidable challenges that confront San Francisco,” Cyrus Sanandaji, founder and managing principal of Presidio Bay, who is now the office tower’s proud new owner. He remains a bull on the San Francisco office market and wants to expand the building’s square footage from 157,436 to 170,000 square feet and transform it into a “Class-A trophy office building with exceptional design and hospitality-driven amenities.”

All we have to say to Sanandaji’s CRE bet is good luck. The crime-ridden metro area covered in poop must come to terms with City Hall’s horrendous progressive policies that have entirely backfired and led to an exodus of businesses and people. Until Mayor London Breed can instill law and order once more — the ability for the downtown area to thrive once more will remain challenging.

Marc Benioff, the chief executive officer of Salesforce, the city’s largest employer and anchor tenant in its tallest skyscraper, warned last month that the metro area is in danger. He offered a grim outlook: The downtown area is “never going back to the way it was” in pre-Covid times when workers commuted to offices daily.

“We need to rebalance downtown,” Benioff said, adding Breed needs to initiate a program to convert dormant office space into housing and hire additional law enforcement to restore law and order.

… and documenting how the downtown area has rapidly transformed into a ghost town is Youtuber METAL LEO, who walks around with a video camera, revealing empty stores, malls, and towers.

Besides Sixty Spear, SFGATE provided data on other recent tower transactions:

The 13-story 180 Howard St. building, known for being the headquarters of the State Bar of California, sold for about $62 million after being expected to sell for about $85 million.

The offices at 350 California St. reportedly sold for roughly 75% less than its previously estimated value in May, and the 22-story Financial District edifice mostly sits empty. Just a few weeks later, nearby 550 California changed hands for less than half of what owner Wells Fargo paid for the building in 2005.

Things are so bad that some building owners are just walking away from properties:

If you’re curious where we could be in the CRE crisis cycle, a recent analysis by CoStar Group shows 55% of office leases signed before the pandemic that were active during Covid haven’t expired, meaning vacancies will continue to rise.

Here’s what could be next: The collapse of WeWork will only cause more pain for CRE markets nationwide. The coworking company occupies 16.8 million square feet across the US.

Commercial real estate (CRE), particularly office space, reminds me of the Arthur Brown tune “Fire!” except that Jerome Powell of The Federal Reserve is the God of Hellfire! While fighting inflation caused by … The Federal Reserve and insane Federal spending (aka, Bidenomics). Call this the Over, Under, Sideways Down economy. The top 1% are doing quite well, while the lower 50% of net worth households are struggling.

The Q1 2023 NCREIF Office property (value) index shows declining office value since Q2 2022 as The Fed began raising its target rate to combat inflation.

From Trepp, we have this shocking table showing the decline the average total value loss over the span of around a decade. The oldest buildings experienced the largest reduction in value of 60%, and the newest experienced the least (but quite substantial) reduction of 52%. Although the newest buildings performed the best relatively, their 52% value reduction is easily the most concerning, and displays truly how much distress is present in the office sector. This group has the highest percentage of Class A buildings, but its reduction value over the past decade is still approximately on par with buildings constructed over half a century prior. With north of $150 billion in securitized maturities beyond 2023, these trends set a gloomy tone for their future and the performance of office properties as a whole.

Then we have this alarming headline from Trepp: “Commercial Mortgage Sector Faces Another Wall of Maturities as $2.75 Trillion Rolls by 2027.” An estimated $528.7 billion of commercial mortgages mature this year, according to Trepp data, which projects that next year, maturities will increase to $532.8 billion. The projections are based on data for the first quarter compiled using the Federal Reserve’s flow of funds and made various assumptions regarding loan terms for each of the major lender categories. The data would indicate that the market is facing a wall, if not a mountain of maturities that would make the 2015-2017 wall of maturities look almost inconsequential. During that period, roughly $1.1 trillion of loans were scheduled to come due. But attention was focused on the CMBS market, as more than $335 billion of loans were set to mature during the period.

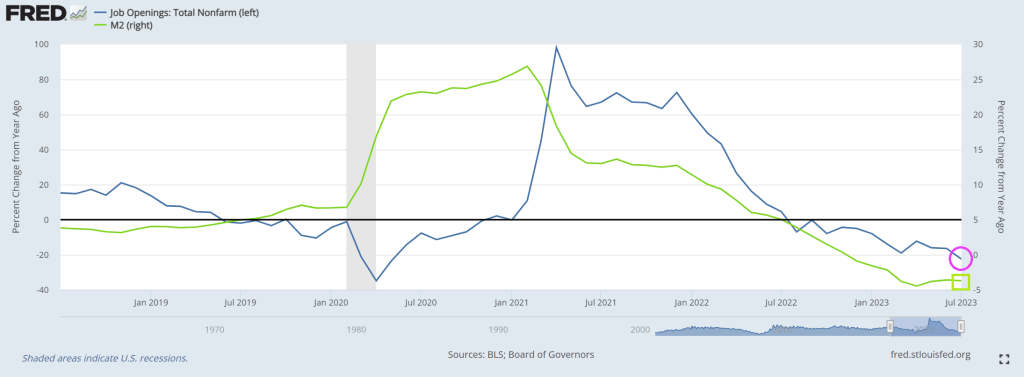

Well, REAL gross domestic income fell -0.8% YoY in Q1 2023 as M2 Money growth crashes. Not a good sign for the US economy or commercial real estate.

Of course, office properties are suffering from almost out-of-control crime in major American cities and the desire of workers to work from home rather than commute to work in cubicles.

But never fear! We have massively corrupt and compulsive liar Joe Biden as President!! He is the President of The 1%! Not the other 99%.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.