I am anxiously waiting for the US inflation report tomorrow, so I am just looking at the US Treasury yield curve, mortgage rates and cryptos today.

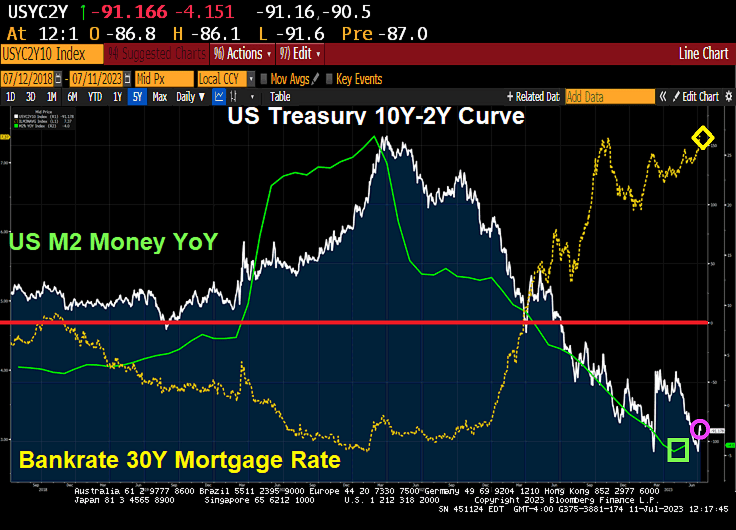

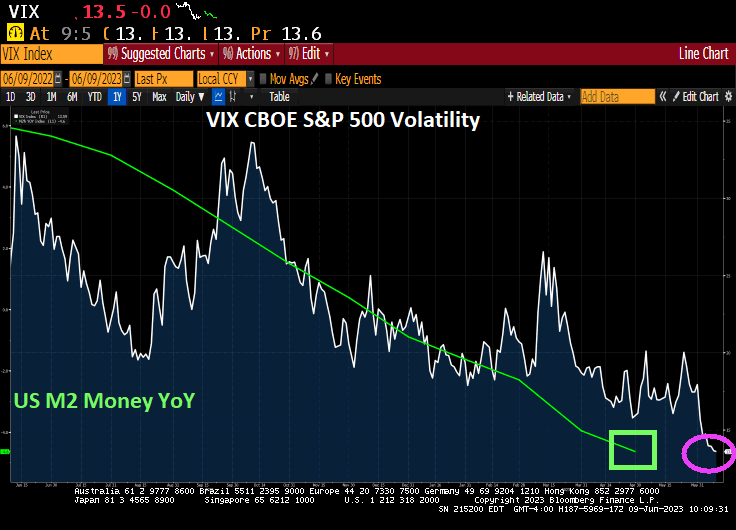

The US Treasury 10Y-2Y yield curve stumbled (just like Biden and Bidenomics) to -91.166 basis points as the turnaround in M2 Money growth has stalled. Bankrate’s 30Y mortgage rate is up to 7.37%, that is UP 156% under Bidenomics.

Bitcoin is down today. At least Solana is up.

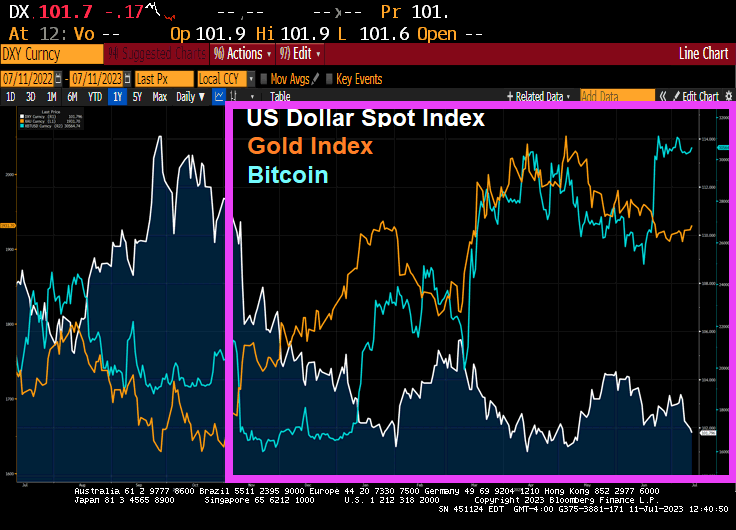

Since November 3, 2022, the US Dollar Index is DOWN -9.68%, Gold is UP 18.55% and Bitcoin (Elizabeth Warren’s latest obsession) is UP 51.11%.

Jay Leno once quipped about the Obama meal. “Order anything you want and hand the bill to the person standing behind you.” Biden, like his boss Obama, is praciticing a similar strategy. Spend like a drunken sailor and just keep borrowing until the whole thing breaks.

The barrage of fresh Treasury bills poised to hit the market over the next few months is merely a prelude of what’s yet to come: a wave of longer-term debt sales that’s seen driving bond yields even higher.

Sales of government notes and bonds are set to begin rising in August, with net new issuance estimated to top $1 trillion in 2023 and nearly double next year to fund a widening deficit. The Treasury is already in the middle of an estimated $1 trillion bump in bills as it seeks to replenish its cash coffers in the wake of the debt-limit deal.

It’s an explosive mix for borrowing costs as debt sales are swelling and the Federal Reserve continues to reduce its balance sheet at a time when traditional buyers of Treasuries overseas are discouraged by currency hedging costs.

“A worsening fiscal profile, amid fairly modest spending cuts, suggests that the upcoming supply deluge will not be limited to T-bills,” wrote Anshul Pradhan, head of US rates strategy at Barclays Plc. “The Treasury will soon need to increase auction sizes meaningfully across the curve. We believe the rates market is too complacent.”

Barclays strategists predict the net rise in coupon-bearing debt from August to year-end will be nearly $600 billion. And that would only ramp up in 2024, they say, with an annual figure of $1.7 trillion. That would be nearly double this year’s expected debt issuance.

Pradhan says he doesn’t think the market appreciates the increase in issuance that’s going to be needed due to wide budget deficits and the fact the Treasury won’t want bills to become a substantial share of the total debt.

Total net new bill sales are set to bring their share of US debt to about 20%, according to JPMorgan Chase & Co. The issuance would hit a threshold seen by the Treasury Borrowing Advisory Committee as the upper limit for the US to fund deficits at the least possible cost to taxpayers.

Bank of America Corp. says the supply deluge could result in a “demand vacuum” for longer maturity bonds that could push yields higher and tighten financial conditions.

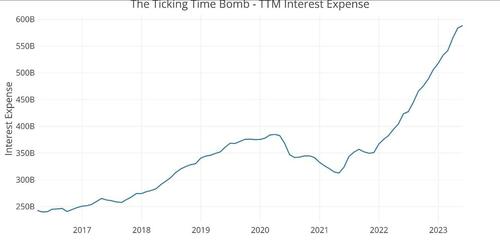

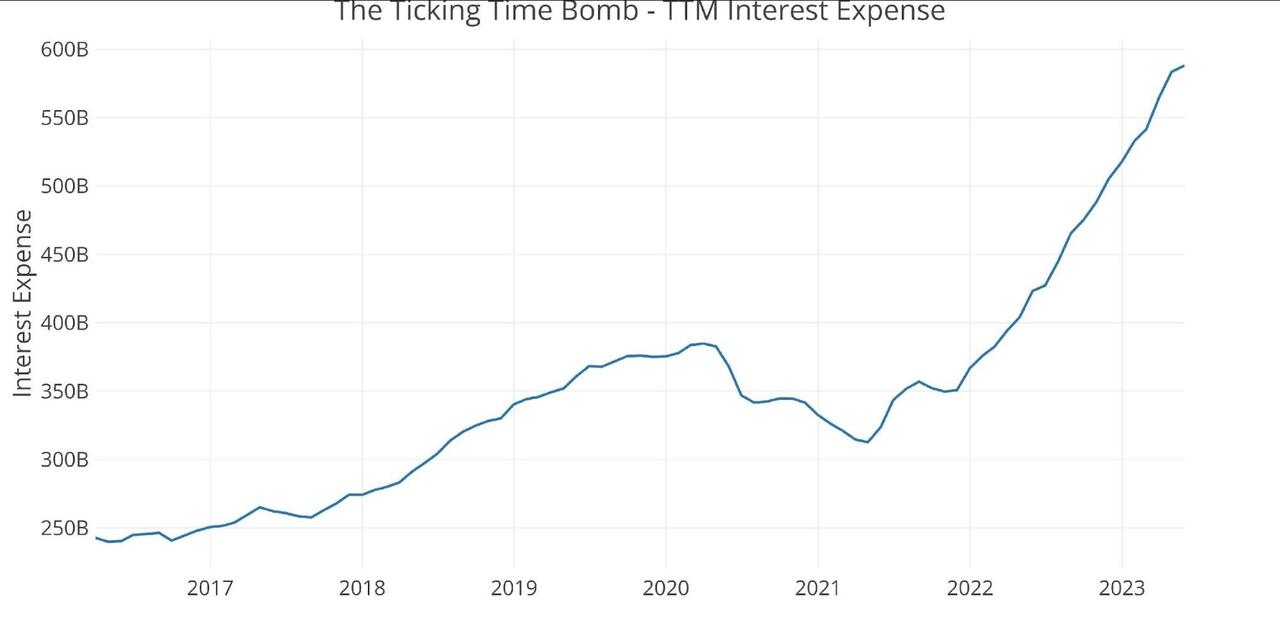

The problem isn’t purely a function of more debt. The bigger issue is that this new debt comes with a much steeper price tag. Interest on the national debt is rising at an alarming clip.

The trailing 12-month (TTM) interest on the debt clocked in at just under $600 billion in May. This was up from $350 billion at the start of 2022, less than 18 months ago. The government has added an extra $250 billion in expenses per year on just debt service.

This is just the beginning of an upward trend. Based on the current interest payments, the Treasury is paying less than 2% interest on the total debt. But a lot of the debt currently on the books was financed at very low rates before the Federal Reserve started its hiking cycle. Every month, some of that super-low-yielding paper matures and has to be replaced by bills, notes and bonds yielding much higher rates. That means interest payments will quickly climb much higher unless rates fall.

Looking at the Treasury sale on June 26 reveals the extent of the problem. The Treasury sold $162 billion in securities, with $120 billion in short-term Treasury bills with high yields.

$58 billion in six-month bills at an investment yield of 5.45%

$62 billion in three-month bills at an investment yield of 5.34%.

$42 billion in two-year notes at a high yield of 4.67%, amid very strong demand. Longer-term yields are still far below short-term yields.

With this flood of Treasury bills, the share of short-term paper underpinning the debt is approaching 20%. That’s considered the upper limit, meaning the Treasury will soon have to turn to issuing longer-term notes and bonds. That means the Treasury will be locking in higher interest rates for the long term.

While I am miserable under Biden and Yellen’s “Reign of Error,” apparently much of the USA is miserable under Biden/Yellen as well compared to the pre-Covid days of Donald Trump. 9.03% misery index (unemployment rate+ core inflation) today compared to 5.86% at the end of 2019 under Trump (before we got Fauci’d and Weingarten’d (the National Teachers’ Union President who pushed public school shutdowns)).

(Bloomberg) If a recession is going to come in the next 12 months — and most economists surveyed by Bloomberg say it probably is — then President Joe Biden should hope it begins sooner rather than later.

The last three one-term presidents — Jimmy Carter, George H.W. Bush, and Donald Trump — have all had their reelection hopes felled by an economic downturn.

But the list of presidents who survived recessions on their watch is just as long. Richard Nixon, Ronald Reagan and George W. Bush all won reelection — in the first two cases by landslides.

The difference, for the most part, is timing.

Two-term presidents get recessions out of the way early. One-term presidents have bad economic news as voters are deciding.

That means a short recession that begins soon — offering the chance for a rebound by Election Day 2024 — might be the best-case scenario for Democrats.

“The historical record suggests that a recession in the second half of 2023 would probably be less damaging to the president’s reelection prospects than a recession in the first half of 2024,” said Larry Bartels, who studies the intersection of politics and economics at Vanderbilt University. But he also said there’s not much that Biden can do at this point to change the direction of the economy in the short term.

The economic projections accompanying the Federal Reserve’s decision to hold interest rates Wednesday suggest that policymakers see less likelihood of a downturn than before. Officials’ median forecast for gross domestic product growth rose from 0.4% to 1% in 2023, with the expansion expected to pick up slightly in 2024 and 2025.

Bond traders responded to the rate decision with a signal that they’re expecting an increased likelihood of a recession in the next year.

A 65% Chance

The typical modern recession lasts 10 months, so an early, short and shallow recession would give Biden time to regain his economic footing. A late, long and deep recession could put Biden among the list of one-term presidents whose time in the White House was cut short by an untimely slump.

The consensus of economists in a Bloomberg survey shows a 65% chance of a recession in the next 12 months, up from 31% a year ago.

The same survey shows an expectation for a return to modest growth in real gross domestic product next year, with growth approaching 2%. That’s tepid in historical terms, but could be a welcome trajectory for Democrats.

“It’s not the absolute level of the economy. It’s the direction of the economy six months out from the elections that really influences the vote,” said Celinda Lake, who served as Biden’s pollster in 2020.

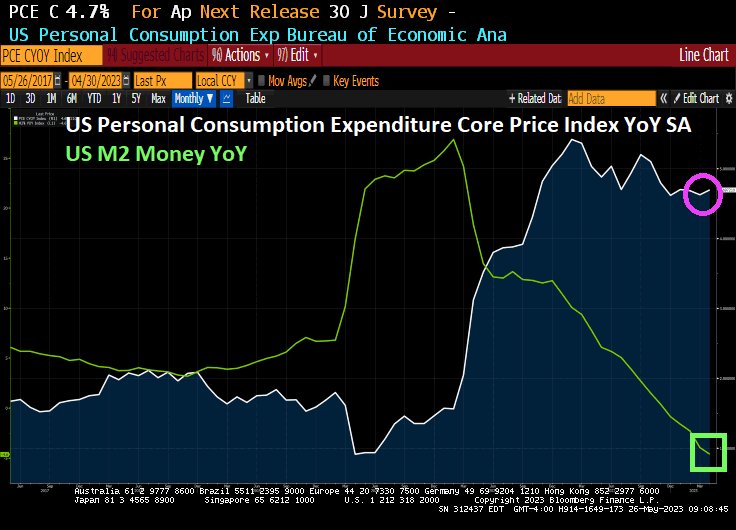

While they’ve largely directed their fire on each other over social and cultural issues, 2024 Republican presidential candidates have criticized Biden’s stewardship of the economy, blaming him for an inflation rate that in mid-2022 reached 9.1%, its highest point in four decades. But that spike has now ebbed to 4% in data out Tuesday.

Former Vice President Mike Pence mentioned “a looming recession” in his campaign announcement video last week, and former President Donald Trump has asserted for nearly a year that the US is already in a recession.

Biden, for his part, isn’t conceding that a recession is inevitable. “They’ve been telling me since I got elected we’re going to be in a recession,” he said earlier this year.

In a campaign speech to union members in Philadelphia Saturday, Biden touted the progress the economy has made since the pandemic recession, and said legislation on infrastructure, clean energy and semiconductors will help build for the long term.

“The investments we’ve made these past three years have the power to transform this country for the next five decades,” he said. “And guess who’s going to be at the center of that transformation? You.”

White House spokesman Andrew Bates said recession predictions “keep turning out like pollsters’ calls before the midterms: wrong.”

But in a Wall Street Journal op-ed this month, Biden also acknowledged that the US “must look out for risks and guard against them.”

Lake said that’s the right tone. “There was a time in the economic conversation when his optimism seemed out of touch with what’s going on,” she said. “Now he says, ‘I get it. It’s good but it’s not good enough.’”

‘Misery index’

Yes, the Misery Index remains elevated under Biden’s “Reign of Error” compared to pre-Covid levels under Trump.

On the commodity side, Spot Silver is up 1.46%. Iron Ore is up 1.60%, but I don’t think my neighbors would appreciate me taking delivery on 10 tons of iron ore on my driveway! Heating oil is up 2.90%.

On the crypto side, bitcoin is up 20.84 (0.08%) with Ethereum up slightly more.

Bitcoin and silver doing well as the US Dollar loses ground since September 2022.

The Fed will annouce a pause at today’s FOMC meeting, so don’t look for mortgage rates to do much today.

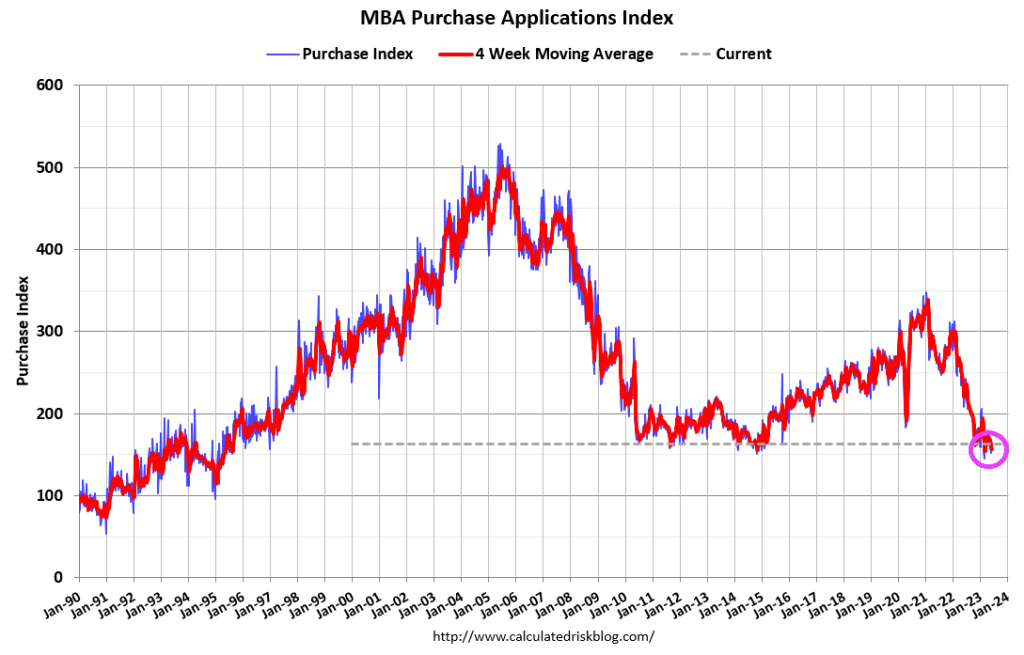

Mortgage applications increased 7.2 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending June 9, 2023.

The Market Composite Index, a measure of mortgage loan application volume, increased 7.2 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index increased 18 percent compared with the previous week. The Refinance Index increased 6 percent from the previous week and was 41 percent lower than the same week one year ago. The seasonally adjusted Purchase Index increased 8 percent from one week earlier. The unadjusted Purchase Index increased 17 percent compared with the previous week and was 27 percent lower than the same week one year ago.

Mortgage rates declined for the second straight week, with the 30-year fixed rate decreasing to 6.77 percent. Mortgage applications were up over the week, but remained well below levels from a year ago.

Joe Biden’s new nickname is “The 5 Million Dollar Bribe Man.” Sort of like Steve Austin.

Well, Kevin McCarthy (RINO-CA) and Patrick McHenry (RINO-NC) along with Jim Jordan (RINO-OH) and Marjorie Taylor Greene (RINO-GA) sold out America to Green Joe Biden (the Jolly Green Giant?) and pretty much guaranteed a Biden reelection as President and Democrats winning the House majority at the next election. Way to go McCarthy, McHenry, Jordan an Greene! You sold out America to the Progressive, destructive Left.

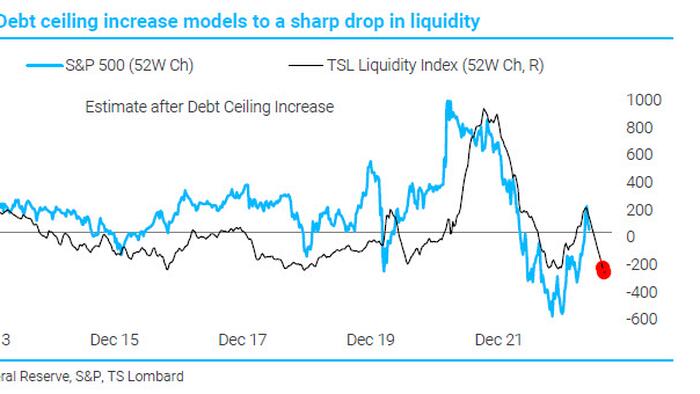

With a debt ceiling deal freshly inked, the US Treasury is about to unleash a tsunami of new bonds to quickly refill its coffers.This will be yet another drain on dwindling liquidity as bank deposits are raided to pay for it — and Wall Street is warning that markets aren’t ready.

The negative impact could easily dwarf the after-effects of previous standoffs over the debt limit. The Federal Reserve’s program of quantitative tightening has already eroded bank reserves, while money managers have been hoarding cash in anticipation of a recession.

JPMorgan Chase & Co. strategist Nikolaos Panigirtzoglou estimates a flood of Treasuries will compound the effect of QT on stocks and bonds, knocking almost 5% off their combined performance this year. Citigroup Inc. macro strategists offer a similar calculus, showing a median drop of 5.4% in the S&P 500 over two months could follow a liquidity drawdown of such magnitude, and a 37 basis-point jolt for high-yield credit spreads.

The sales, set to begin Monday, will rumble through every asset class as they claim an already shrinking supply of money: JPMorgan estimates a broad measure of liquidity will fall $1.1 trillion from about $25 trillion at the start of 2023.

“This is a very big liquidity drain,” says Panigirtzoglou. “We have rarely seen something like that. It’s only in severe crashes like the Lehman crisis where you see something like that contraction.”

It’s a trend that, together with Fed tightening, will push the measure of liquidity down at an annual rate of 6%, in contrast to annualized growth for most of the last decade, JPMorgan estimates.

The US has been relying on extraordinary measures to help fund itself in recent months as leaders bickered in Washington. With default narrowly averted, the Treasury will kick off a borrowing spree that by some Wall Street estimates could top $1 trillion by the end of the third quarter, starting with several Treasury-bill auctions on Monday that total over $170 billion.

What happens as the billions wind their way through the financial system isn’t easy to predict. There are various buyers for short-term Treasury bills: banks, money-market funds and a wide swathe of buyers loosely classified as “non-banks.” These include households, pension funds and corporate treasuries.

Banks have limited appetite for Treasury bills right now; that’s because the yields on offer are unlikely to be able to compete with what they can get on their own reserves.

But even if banks sit out the Treasury auctions, a shift out of deposits and into Treasuries by their clients could wreak havoc. Citigroup modeled historical episodes where bank reserves fell by $500 billion in the span of 12 weeks to approximate what will happen over the following months.

“Any decline in bank reserves is typically a headwind,” says Dirk Willer, Citigroup Global Markets Inc.’s head of global macro strategy.

Bitcoin Faces Downside Risks After Debt Deal Moves Forward

Just when markets appear to be moving past the months-long drama around the US debt ceiling, holders of risky assets such as cryptocurrencies are likely facing a fresh challenge while the Treasury looks to rebuild its depleted cash balance with an estimated $1 trillion Treasury-bill deluge.

“The impending reserve drawdown, due to the [Treasury General Account] rebuild, may prove to be a headwind,” Citi Research strategists including Alex Saunders wrote in a note.

Citi analyzed the performance of risky assets during drawdowns and found that they were vulnerable to higher volatility and weaker returns. As such, the near-term outlook doesn’t seem too rosy for Bitcoin and Ether. “Both coins average negative returns in these scenarios, and BTC has significantly underperformed in the median case,” the strategists wrote Thursday.

The TGA, which keeps money for the Treasury, ballooned during the pandemic. It expanded again last year and is now about as low as it has ever been. Treasury, as a result, will need to replenish its dwindling cash buffer to maintain its ability to pay its obligations through bill sales, estimated at well over $1 trillion by the end of the third quarter. This supply burst may drain liquidity from the banking sector and raise short-term funding rates against an economy many say is likely to fall into recession.

This doesn’t bode well for digital-asset investors, who were just recovering from fears of a no-deal scenario for the US debt ceiling. While Bitcoin edged higher on Friday, it’s still hovering around the $27,000-mark that it has failed to break away from for several weeks.

“Crypto markets were not immune to fears of the US defaulting on its debt, selling off on negative developments and rallying on headlines suggesting progress,” the strategists said. They added that crypto has typically “fared well” amid issues concerning traditional financial institutions, citing the banking turmoil in March, a period in which Bitcoin outperformed. But perhaps risks of an institution such as the US government defaulting “doesn’t paint a favorable outlook for decentralized digital assets.”

To illustrate, the strategists used the Cboe Volatility Index, or VIX, as an indicator of the market’s fear to gauge whether a resolution would be passed before hitting the ceiling. And whenever equity market concerns were eased, that’s when Bitcoin outperformed.

“While in theory the potential default of an institution as impactful as the US government would bode well for decentralized technologies and systems, this may not currently be the case given that the crypto industry is still in its infancy and regulation has yet to be well-defined,” they wrote. “Another theory is that not raising the debt ceiling would lead to reduced US government debt and a lower fiscal deficit, and provide more credibility to fiat, particularly the dollar.”

On Friday, the Senate passed legislation to suspend the US debt ceiling and impose restraints on government spending through the 2024 election. The measure now goes to President Joe Biden, who forged the deal with House Speaker Kevin McCarthy and plans to sign it just days ahead of a looming US default.

Year-to-date, Bitcoin has rebounded some 60% after starting the year at around $16,500. Such optimism comes after 2022’s 64% drop, its second-worst year in its history. It rose about 1% to $27,178 as of 3:32 p.m. in New York, and is marginally higher from last Friday.

Bitcoin’s support hovers around $26,500, said Fiona Cincotta, senior market analyst at City Index, adding that a break below $25,000 could mean a deeper sell-off.

“The problem is the macro backdrop, which is relatively uncertain going forward with recessionary fears,” she said. “I think what will be looking for to make Bitcoin shine is a nice dovish pivot from the Federal Reserve. That might be the tide where we will see another decent leg higher.”

Range-bound trading has been Bitcoin’s defining characteristic of late, with its 30-day volatility reigning low at 1.8%, firmly staying firm within its two-month-long trading range. Despite growing short-term volatility, options implied volatility trended lower over the past week, according to K33’s Bendik Schei and Vetle Lunde. Even so, Bitcoin exchange-traded products continued to see steady outflows while Bitcoin volumes — spot and futures — are trending lower.

McCarthy, McHenry, Jordan and Greene, honorary Frenchmen!

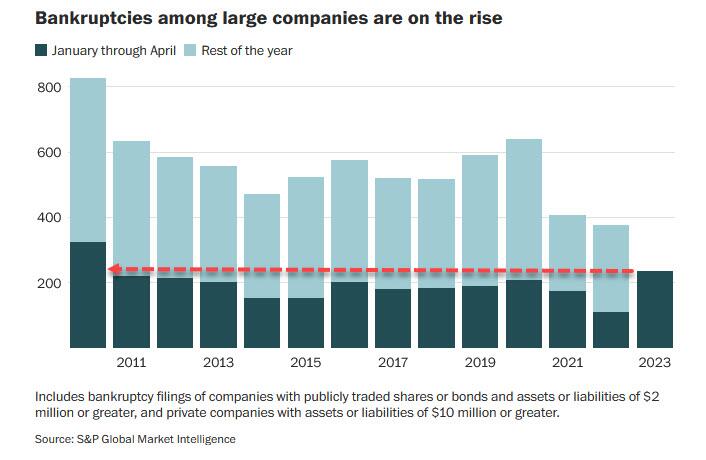

It is not a surprise that the ill-advised COVID economic shutdowns would harm small businesses that large corporations.

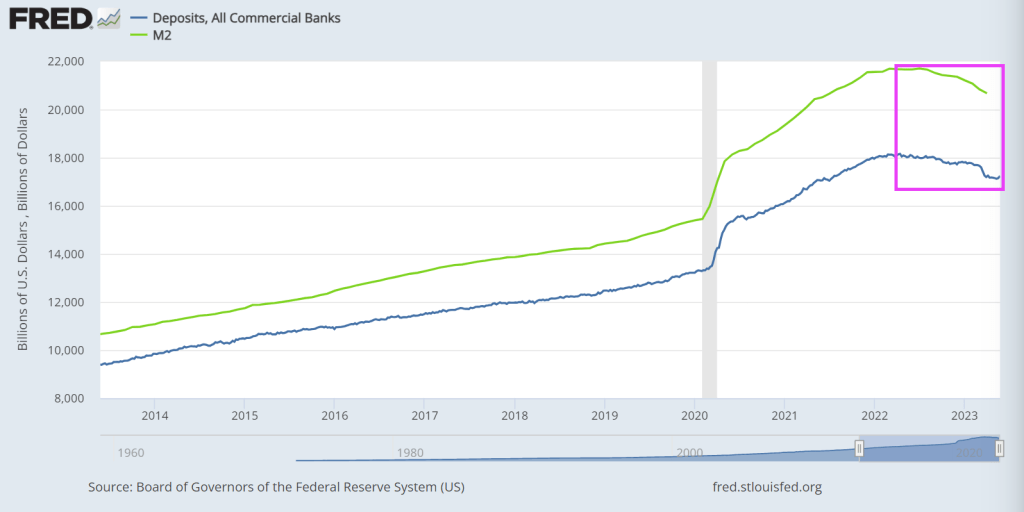

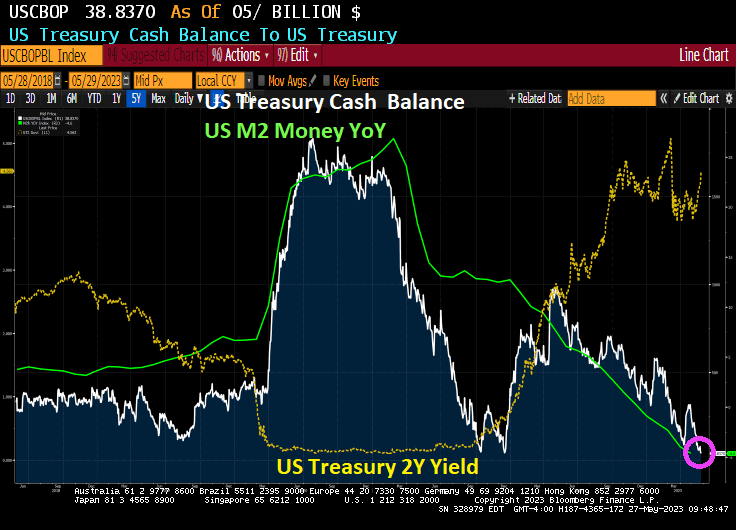

Yes, The Fed’s M2 Money printing press went wild with COVID emergency refief. And so did the discrepancy between the top 1% and the bottom 50% in terms of “Share of Total Net Worth Held.” The top 1% is in blue and the bottom 50% is in red. M2 Money is in green.

Compared to pre-COVID, the top 1% increased their share of total net worth from 29.7% to 31.9%, an increase of 7.4% since January 2020. The bottom 50% fell from 30% to 28.5%, a -5% decline. An elitist wonderland!

And The Biden family keeps raking in the money far about Joe’s salary.

And I assume Fed Chair Jerome Powell and Treasury Secretary Janet Yellen also made fortunes from COVID relief.

White House and Republican negotiators tentatively narrowed differences but were still clashing Friday on key issues as the Treasury Department signaled extra time was available before a potential US default.

Treasury Secretary Janet Yellen announced the department expects to be able to make payments on US debts up until June 5 if lawmakers fail to act on the US debt ceiling. That set a more pointed date for a potential default but is also four days later than her previous comments eyeing trouble as soon as June 1.

The new so-called X-date buys negotiators for House Speaker Kevin McCarthy and President Joe Biden more time to strike a deal. The negotiating teams haven’t met in person since Wednesday but spoke late into the night Thursday and were in regular communication throughout the day Friday.

Yes, there isn’t really a crisis folks. Treasury collects tax dollars continuously so Treasury can prioritze debt payments and other disbursements. The only crisis is in the minds of the media.

Deputy Treasury Secretary Wally Adeyemo warned Friday that payments to Social Security beneficiaries, veterans and others would be delayed if there’s a default. But he said he’s gaining some confidence an agreement will be reached.

We’re making progress and our goal is to make sure that we get a deal because default is unacceptable,” Adeyemo said in an interview on CNN. “The president has committed to making sure that we have good-faith negotiations with the Republicans to reach a deal because the alternative is catastrophic for all Americans.”

The accord would also include a measure to upgrade the nation’s electric grid to accommodate sham renewable energy, a key climate goal, while speeding permits for pipelines and other fossil fuel projects that the GOP favors, people familiar with the deal said.

The deal would cut $10 billion from an $80 billion budget increase for the Internal Revenue Service that Biden won as part of his Inflation Reduction Act (big whoop). Republicans have warned of a wave of agents and audits while Democrats said the increase would pay for itself through less tax cheating.

What is taking shape would be far more limited than the opening offer from Republicans, who called for raising the debt ceiling through next March in exchange for 10 years of spending caps. House conservatives were already balking Thursday at the notion of a small deal, with the House Freedom Caucus sending a letter to McCarthy demanding he hold firm.

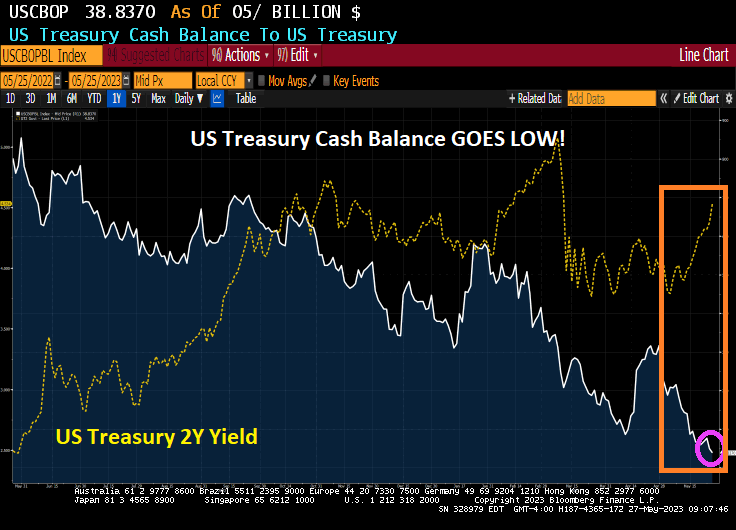

Treasury’s cash balance is at a low point and The Administration threatens Social Security recipients and veterans of delayed payments … while Biden goes on vacation for Memorial Day weekend to honor veterans??

Of course, Yellen know that all The Fed has to do to increase M2 Money growth again.

Meanwhile, bankrupties among large companies are highest since 2010.

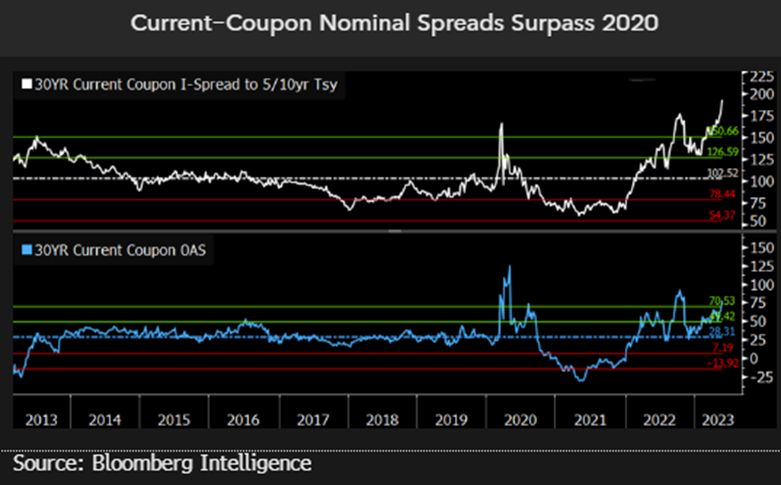

In the mortgage market, current coupon nominal spreads 9Agency MBS 30Y coupon over Treasuries) are soaring.

Meanwhile, to honor US veterans, Biden goes on Memorial Day weekend and threaten veterans with delays in veteran benefits. Sigh.

Is Joe Biden REALLY Reverend Kane from Poltergeist II??

{kind=link}

You must be logged in to post a comment.