Inflation started with Biden’s misguided war on US energy, then Biden/Congress helped inflation with an epic spending splurge. The Federal Reserve counterattacked with Fed rate hikes.

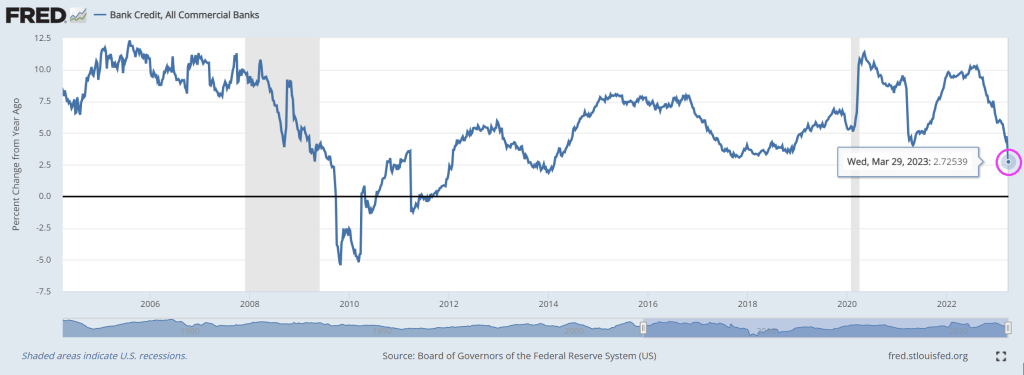

Over the past year, The Fed Funds Effective rate has risen and US bank credit has crashed to 2.73% year-over-year.

Do I detect a trend?

Since 2005, the crash in US bank credit is looking like 2008/2009 all over again.

Whether Biden is Cap’n Crunch or Jerome Powell or Janet Yellen, they are all crunching the US economy.

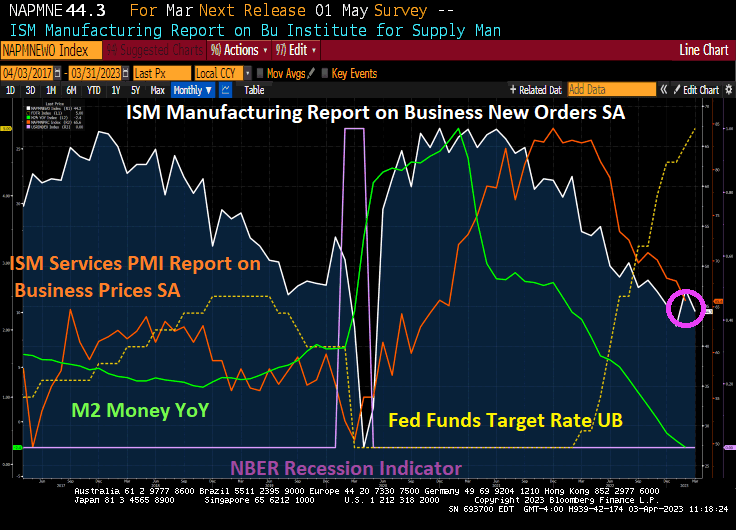

Not only did the ISM Manfacturimng Report on New Business Order fall to 44.3, but price PAID also fell as The Fed hikes rates (yellow line) and slowing M2 Money growth (green line).

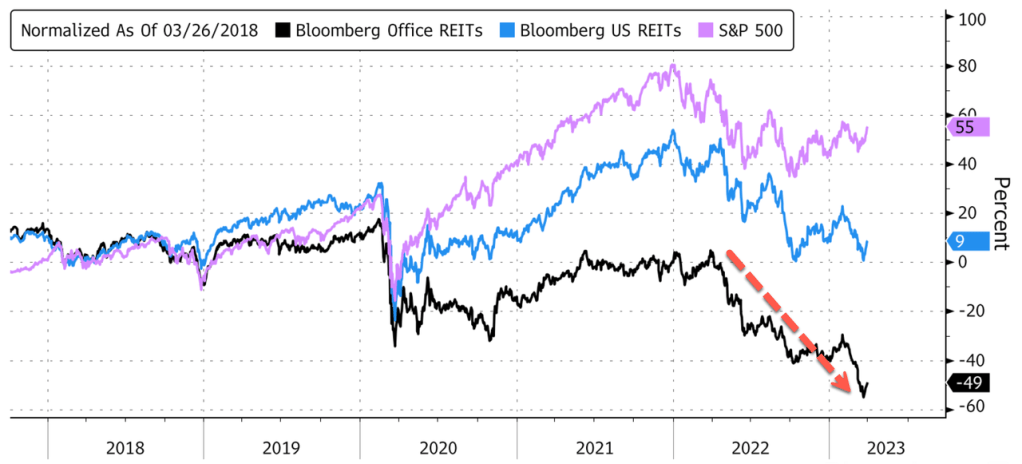

Office REITs are really hurting as Count Powellula sucks the blood (liquidity) from the market.

Count Powellula. “I vant to suck the blood from your economy.”

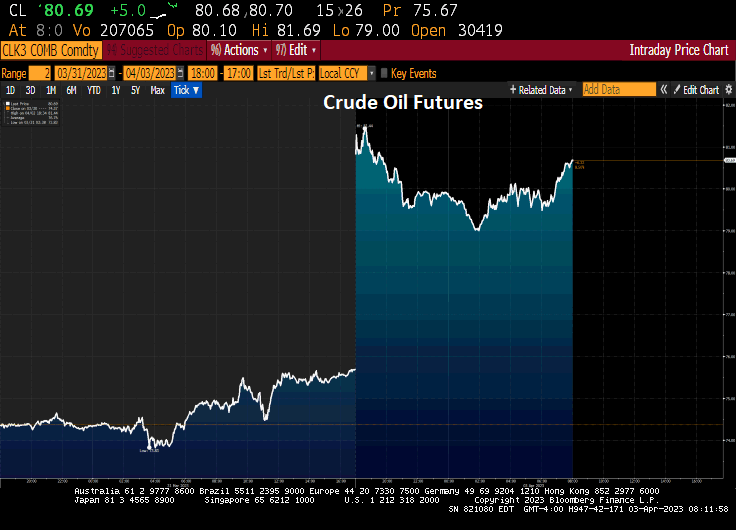

While Resident Biden is on good terms with the Mexican drug and sex trafficing cartels that control our southern border, the oil cartel just stuck their fingers in Biden’s eyes by cutting oil productions. Riyadh, Saudi Arabia was irritated last week that the Biden administration publicly ruled out new crude purchases to replenish SPR

Cartel removes more than 1 million barrels a day from market

Analysts say the decline in oil inventories will accelerate

Today, crude oil futures are up 6.62% to over $80 per barrel.

Sunday’s surprise OPEC+ production cuts have redefined the outlook for crude prices, bringing $100 a barrel back into the frame.

Prior to the announcement, the cartel’s own numbers suggested the group would need to pump more oil, not less, in the second half. With the International Energy Agency expecting a demand surge later this year, there’s now renewed risk of a fresh inflationary impetus for the global economy.

Under Biden’s Reign of Error, diesel prices are up 64% while the Strategic Petroleum Reserves (SPR) have been drained by -42%.

St. Benedict, help protect us from Biden and The Federal Reserve.

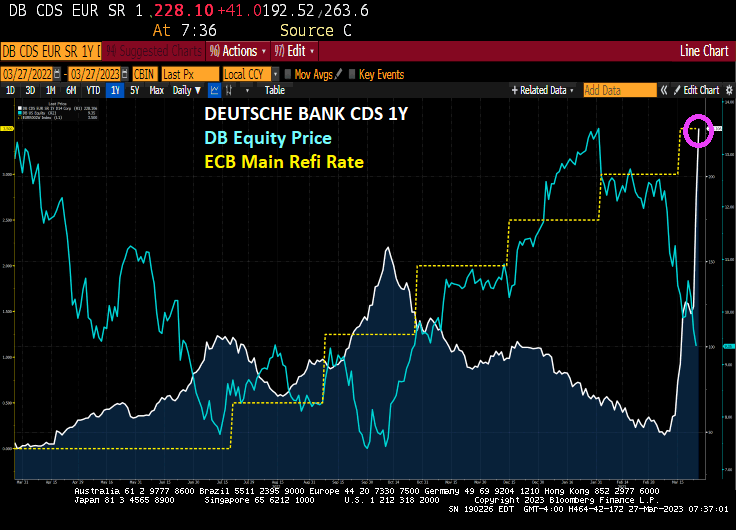

Are central banks like The Federal Reserve and European Central Bank ({ECB) sinking the banks?

Deutsche Bank, Germany’s largest bank (eerily like Germany’s World War II battleship The Bismarck) is seeing a blow out in its 1-year credit default swaps (CDS) as the ECB cranks up it main refinancing rate to fight inflation.

And then we have Deutsche’s Banks gross notional derivatives exposure (Euro 55.6 TRILLLION) dwarfing German GDP (Euro 2.7 Trillion). By a factor of greater than 20! Now, THAT’S a lot of derivatives exposure.

On the bond front (the NEW eastern front), we see the US Treasury 2-year yield rising 17.1 basis points. But European sovereign yields are up double digits as well (except for Italy).

The Federal Reserve raised their target rate just once under President Obama until Donald Trump was elected. Then raised their target rate 8 times AFTER Trump was elected. In other words, Bernanke/Yellen kept the target rate near 0% for too long. When you throw the insane level of spending by Biden and Congress on top of the massive Fed stimulus. Now The Fed is trying to remove the excessive monetary stimulus by raising rates which is crushing banks.

Small bank reserces are low.

In any case, rate hikes are causing turmoil at small banks (as witnessed by the failures of SVB, Silvergate, First Republic and Signature Banks. Even worse, small banks hold 70% of commercial real estate loans.

Money managers have stepped up their bearish bets against office landlords, wagering that the US regional banking crisis will slash the availability of credit to property owners that were already suffering from the pandemic and rising interest rates.

Hedge funds are using credit derivatives and equities to bet against the companies and their debt. Almost 40% of shares in the iShares US Real Estate ETF are sold short, the highest proportion since June, according to data from analytics firm S3 Partners.

At Hudson Pacific Properties Inc., short interest reached a record 7.4% earlier this week before dropping to about 5% of shares outstanding, according to data compiled by IHS Markit Ltd. That’s almost double the level a month ago. For Vornado Realty LP, short interest is the highest since January.

Three regional banks have failed in the US, raising concerns about the implications for commercial real estate finance. Many lenders are losing deposits, which might cut into their ability to finance real estate in the future. Regional banks account for about 80% of bank lending to commercial properties, according to economists at Goldman Sachs Group Inc.

“What’s changed in the last few weeks is the credit markets,” said Rich Hill, chief of real estate strategy research at Cohen & Steers Capital Management Inc. “It went from a story of work-from-home and the impact on occupancy and the lack of rent growth to also the compounding of tighter financial conditions given everything happening with banks.”

Fears of tighter credit are adding to risks for offices that have been building for some time, Green Street analysts wrote in a Tuesday report. Hedge fund manager Jim Chanos, Marathon Asset Management and Polpo Capital Management founder Daniel McNamara are among those who have been betting for months that landlords will struggle to lure staff back to workplaces.

“This regional banking crisis is just throwing fuel on the fire,” McNamara said in a telephone interview. “I just don’t see a way out of this without a lot of pain in the office sector.”

Vulnerable Landlords

Real estate was already the most shorted industry across global equities, according to a March 17 report by S&P Global Inc. It was the third most-shorted sector in the US.

That’s in part because interest rates have been climbing for the last year, which pressures real estate owners. Defaults remain low for now. But office assets are the collateral for about $100 billion of the $400 billion of US commercial real estate debt maturing this year, according to MSCI Real Assets.

Workplaces worth nearly $40 billion face a higher probability of distress, more than apartments, hotels, malls or any other type of commercial real estate, MSCI said on Wednesday. Almost $20 billion of office loans that were bundled into commercial mortgage-backed securities and are due to mature by the end of next year are already potentially distressed, Moody’s Investors Service estimates.

Credit availability for commercial real estate was already challenged this year as investors have grown less interested in buying commercial mortgage bonds, JPMorgan Chase & Co. analysts including Chong Sin wrote in a note. Sales of CMBS deals without government backing have fallen more than 80% this year, according to data compiled by Bloomberg News.

Smaller banks potentially retreating may bring a credit crunch to smaller markets, the JPMorgan analysts wrote.

Lenders advanced a record $862 billion to commercial real estate last year, a 15% increase from a year prior, data provider Trepp estimates. Much of that was driven by banks, which originated 50% more loans in the period. The pace of growth has slowed since then, Federal Reserve data show, as the outlook for real estate grows increasingly negative.

The pressure on offices means lending standards are now being tightened, bad news for landlords that have high levels of leverage and putting lenders at a higher risk of defaults.

“Recent developments have increased downside risk to commercial real estate values from expectations of tightening lending standards,” Morgan Stanley analysts including Ronald Kamdem wrote in a note on Monday. Office REITs may have to sell assets to help them successfully refinance, they said.

Shorts soared on office landlords last year as rising interest rates weighed on the industry. They dropped subsequently as investors wagered that borrowing benchmarks would top out at a lower level than initially expected or the Federal Reserve would begin to cut the rates earlier than previously expected.

Cohen & Steers, which oversees about $80 billion, including $48 billion in real estate investments, went under weight on offices during the pandemic and will steer clear until the market shows signs of hitting a floor.

“I actually want to see more signs of weakness,” Hill said. “The more headlines I see that things are really, really bad, the closer I think we are to the end.”

Chanos Short

Chanos said on CNBC in January that he had been betting against SL Green Realty Corp., short interest in which reached the highest since the financial crisis in recent days. The landlord’s assets include a New York building occupied by Credit Suisse Group AG, the lender taken over by UBS Group AG after government-brokered talks. Short sellers borrow stock and sell it, planning to profit by buying it back at a lower price later.

An SL Green spokesperson directed Bloomberg to company comments at a March 6 investor conference, before the recent bank failures.

The landlord plans to sell $2 billion of properties, cut its debt by $2.5 billion and refinance a $500 million mortgage, Chairman and CEO Marc Holliday said at the Citigroup Inc. conference. Because the securitization market and life insurance financing weren’t receptive to deals, the firm is dependent on banks, which were already an uphill challenge.

“Banks are more likely to say no these days than to execute,” Holliday said. “Knock on wood, hopefully we can get that done.”

Mark Lammas, president of Hudson Pacific, said in an emailed statement that the firm is confident in its business fundamentals and long-term prospects. The company is investment-grade, a majority of its assets are unencumbered, it has $1 billion of liquidity, and no material debt maturities until 2025, Lammas said.

Chanos and representatives of Vornado and Boston Properties didn’t immediately reply to requests for comment.

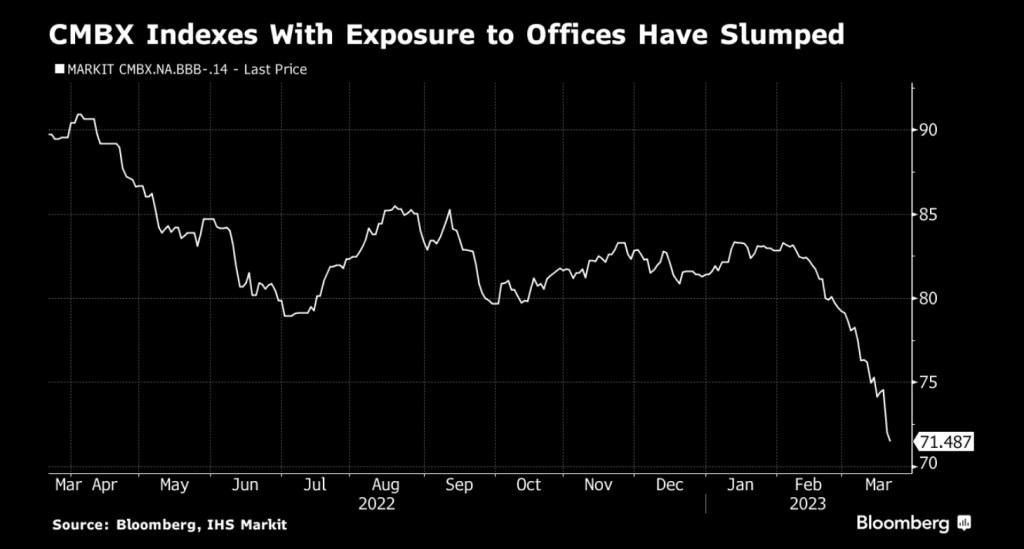

‘The Widowmaker’

Hedge funds have also been using credit-default swaps indexes known as CMBX to bet against CMBS that are most exposed to offices. The derivatives are tied to portions of bonds backed by commercial mortgages and a number of them reached a record low this week amid fears about a number of regional banks.

Betting against commercial real estate has historically been a hard way to make money, because it can take a long time for losses to emerge, and the range of possible outcomes for even troubled property can be wide. “Shorting CMBX BBB- is regarded as the widowmaker — the undoing of many a young trader’s career,” Morgan Stanley trader Kamil Sadik wrote in a March 6 note.

But the spate of bad news means the BBB- portion of the 14th CMBX index is at the lowest level ever and the same part of the 13th index is at its lowest since the pandemic in 2020. Similar declines are also being seen in share prices of office landlords.

“Our conversation with investors suggests that there has been some capitulation and forced selling as the stocks have continued to underperformed,” Morgan Stanley analysts led by Kamdem wrote.

So far in 2023, there has been 17 downgrades of CMBS deals with no upgrades.

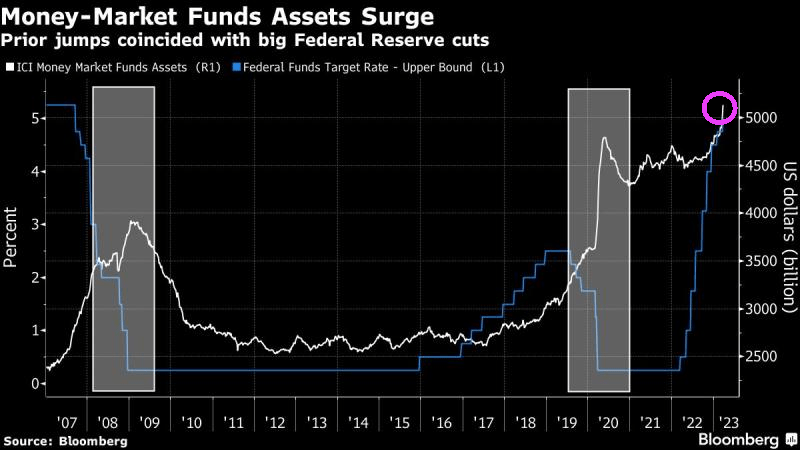

Investors are fleeing to money market funds as The Fed hits the brakes.

The Federal Reserve never died. In fact, The Fed is growing its balance sheet again. Why? A slowing economy and weakness in the banking sector (thanks to inflation and the Fed trying to get inflation back to 2%.

And the banking fiasco keeps rolling, particularly in Europe where Credit Suisse has been in the news for failing and now my former employer, Deutsche Bank (aka, The Teutonic Titanic).

Deutsche Bank AG became the latest focus of the banking turmoil in Europe as ongoing concern about the industry sent its shares slumping the most in three years and the cost of insuring against default rising.

The bank, which has staged a recovery in recent years after a series of crises, said Friday it will redeem a tier 2 subordinated bond early. Such moves are usually intended to give investors confidence in the strength of the balance sheet, though the share price reaction suggests the message isn’t getting through.

“It is a clear case of the market selling first and asking questions later,” said Paul de la Baume, senior market strategist at FlowBank SA. “Traders do not have the risk appetite to hold positions through the weekend, given the banking risk and what happened last week with Credit Suisse and regulators.”

Deutsche Bank slumped as much as 15%, the biggest decline since the early days of the pandemic in March 2020. It was the worst performer in an index of European bank stocks, which fell as much as 5.7%. Crosstown rival Commerzbank AG, Spain’s Banco de Sabadell SA and France’s Societe Generale SA also saw steep drops.

The widespread declines undermine hopes among authorities that the rescue of Credit Suisse Group AG last weekend would stabilize the broader sector. Central banks from the Federal Reserve to the Bank of England this week raised interest rates once again, keeping their focus on inflation amid hopes that the worst of the financial turmoil was past.

All week, regulators and company executives have sought to reassure traders about the health of the banking industry. Deutsche Bank management board member Fabrizio Campelli said Thursday that the government-brokered takeover of Credit Suisse by UBS is “no indication” of the state of European banks.

Standard Chartered Plc Chief Executive Bill Winters said Friday that while there are still some issues to be addressed, “it seems that the acute phase of the crisis is done.”

The latest moves in Europe follow losses in US banks, which tumbled Thursday even after Treasury Secretary Janet Yellen told lawmakers that regulators would be prepared for further steps to protect deposits if needed.

And apparently bank bailouts never died. They just got relabeled.

And on growing banking fears, the 10-year Treasury yield is down -11.7 basis points.

The Philly Fed non-manufacturing sentiment index just tanked to -12.8 as The Federal Reserve removes its Covid-related stimulus.

The banking fiasco (SVB, Signature, etc.) has caused The Fed’s balance sheet to expand … again.

And Fed Funds Futures are pricing in a meager 20 basis points increase at tomorrow’s FOMC meeting (some betting on no change, some betting on 25 basis points). Then another rate hike at the May FOMC meeting, then all downhill from there.

Its Gov’t Gone Wild! Insane spending budget by “Sloppy Joe” Biden, Yellen asking Warren Buffet for banking advice (seriously??), a war in Ukraine that America doesn’t seem to actually want to win, etc. But its the banking system where banks are getting crushed by rising inflation and interest rates (but failed to hedge). Sigh.

As I always told my investments and fixe-income students at University of Chicago, Ohio State University and George Mason University, a 10 basis point change in the 2-year and 10-year US Treasury yield is a big deal. This morning, the US Treasury 2-year yield fell -32 basis points while the 10-year Treasury yield fell -14.8 basis points.

At the same time, gold 3.8% and silver rose 4.7% on banking fears.

Debt would hit a new record by 2027, rising from 98 percent of GDP at the end of 2023 to 106 percent by 2027 and 110 percent by 2033. Nominal debt would grow by $19 trillion, from $24.6 trillion today to $43.6 trillion by 2033.

Deficits would total $17.1 trillion (5.2 percent of GDP) between FY 2024 and 2033, rising to $2.0 trillion, or 5.1 percent of GDP, by 2033.

Spending and revenue would average 24.8 and 19.7 percent of GDP, respectively, over the next decade, with spending reaching 25.2 percent of GDP and revenue totaling 20.1 percent by 2033. The 50-year historical average is 21.0 percent of GDP for spending and 17.4 percent of GDP for revenue.

Proposals in the budget would reduce projected deficits by $3 trillion through 2033, including $400 billion through 2025 when it could help fight inflation. The budget proposes $2.8 trillion of new spending and tax breaks, $5.5 trillion of revenue and savings, and saves $330 billion from interest.

The budget relies on somewhat optimistic economic assumptions, including stronger long-term growth, lower unemployment, and lower long-term interest rates than the Congressional Budget Office (CBO). The budget assumes 0.4 percent growth this year, 2.1 percent growth next year, and 2.2 percent by the end of the decade – compared to CBO’s 0.1 percent, 2.5 percent, and 1.7 percent, respectively. The budget also assumes ten-year interest rates fall to 3.5 percent by 2033, compared to CBO’s 3.8 percent.

And then we have Sloppy Joe and Statist Janet Yellen meeting with mega donor Warren Buffet for advice on dealing with the banking crisis … made by Biden’s energy policy and insane Covid spending by the Administration. And, of course, The Fed’s “too low for too long” monetary policy. What is 92-year old Warren Buffet going to say?

Meanwhile, Fed Funds Futures are pointing to one more rate hike then a series of rate cuts down to 3.737 by January 2024.

You must be logged in to post a comment.