Holders of commercial real estate (CRE) debt are riding the tiger. Meaning that if interest rates don’t come down, there will be a lot of pain and suffering.

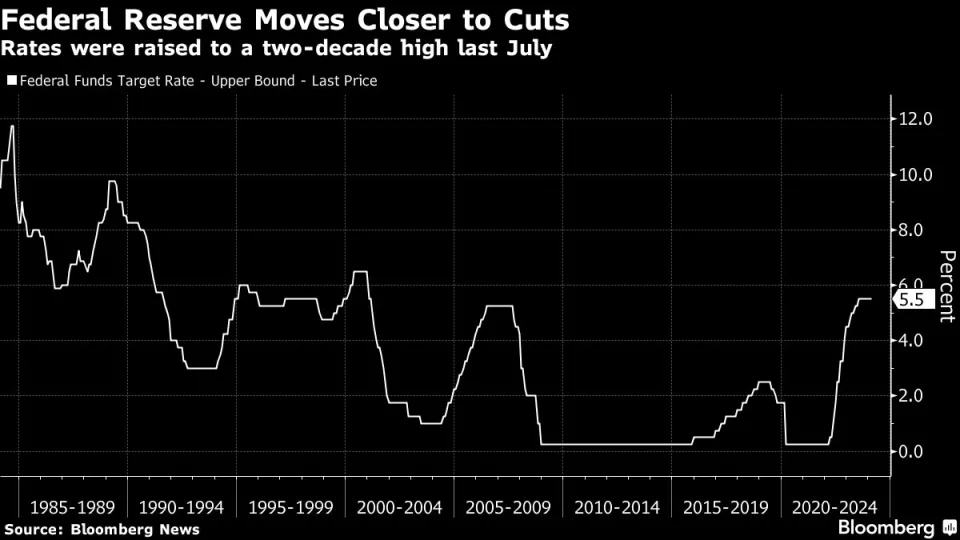

“We’re far from neutral now,” said America’s Fed Chairman, Jerome Powell, to the Senate Banking Committee. As The Fed moves closer to cutting rates.

All those rent-seekers stacked up with commercial real estate holdings nodded in violent agreement. That of course includes the nation’s regional banks, which continue to succumb to the power of their systemically important rivals, now so big that they cannot possibly be allowed to fail.

And this has turned America’s banking behemoths into for-profit wards of the state, recipients of an unspoken but ironclad insurance policy that underwrites catastrophic losses and adds them to the national debt.

“Interest rates right now are well into restrictive territory. They’re well above neutral,” added Chairman Powell without, well, sharing his definition of the word ‘well’. And truth be told, no one really knows the definition of ‘neutral’ when it comes to interest rates.

Economic PhDs will generally tell you that the neutral real interest rate is 0.50%. Their level of confidence is inversely proportional to the amount of capital they have at risk in markets — which would have been Newton’s Fourth Law had he bothered to study the art of economics.

Those of us less academically gifted, who must resort to taking risk for a living, lack the conviction of Nobel Laureates. We see that there are times in an economic cycle when 0.50% real rates stimulate growth, and times when they restrict economic activity.

Sometimes neutral rates have no effect at all. Which is to say that the economic impact of real rates simply depends. Like now when signals are far from uniform. Stock markets hit all-time highs despite collapsing commercial real estate, crypto and gold prices are soaring to records, massive government stimulus programs like the IRA are cranking up, student debt is being forgiven in successive waves, unemployment is near record lows, core inflation is starting to rise again, and the budget deficit is around 6% despite robust GDP growth.

All of which screams that a 0.50% real rate is preposterously low to everyone but economic PhDs.

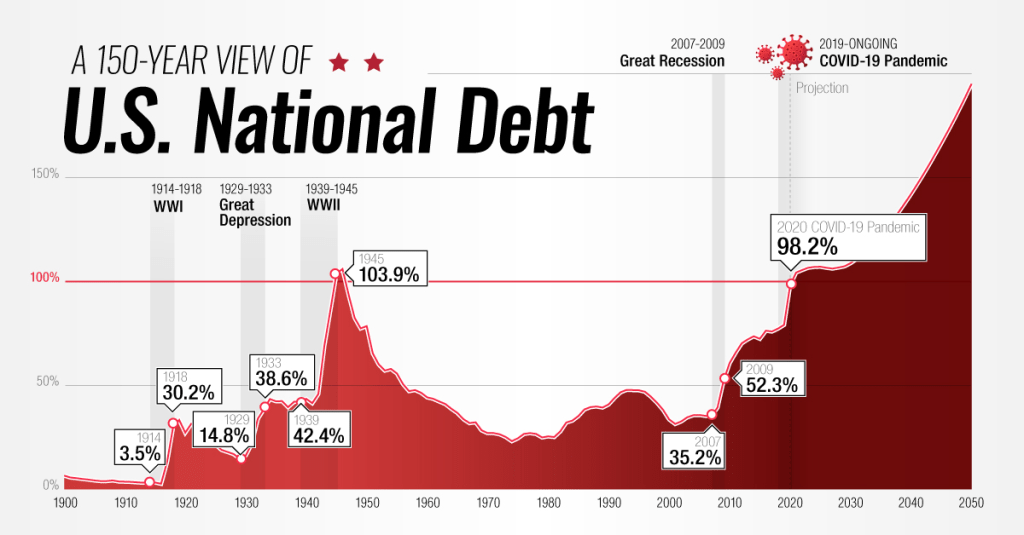

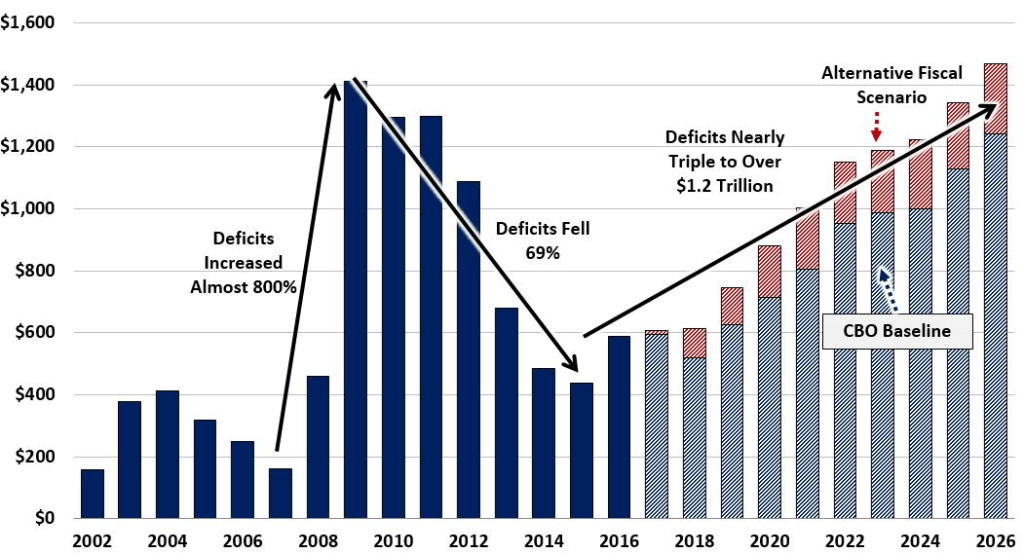

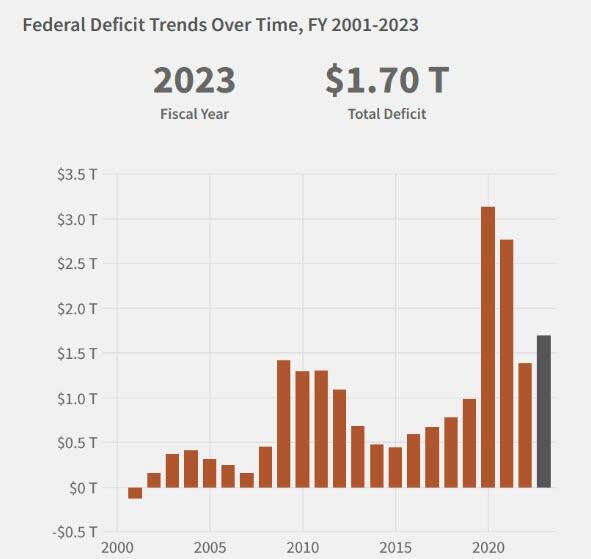

In statistics we talk about “jump processes.” Like Federal government spending every time there is a financial crisis like the subprime crisis of 2008-2009 and the Covid lockdowns of 2020. Each crisis brought a jump in the level of spending and jump in Federal debt.

Federal debt under Biden started at $27.7 trillion and is currently at $34.5 trillion, that amounts to $6.75 TRILLION in additional debt under Old Grand-dad Joe Biden. Federal spending, of course, is out of control with Biden/Congress spending $569 BILLION since Joey took office.

Generally speaking, the Federal government needs to justify the elevated levels of Federal spending, like another COVID outbreak, escalate the war in Ukraine, get into a hot war with Iran and China, or … say … Washington DC pols never need much of an excuse to go on a spending spree.

If only Biden would retire gracefully. He could be the new face of “Old Grand-dad Bourbon Whiskey.” Except Biden’s version would be an angry 80+ year old man with dementia.

Somehow, Biden left this factoid out of his State of The Union (SOTU) address. In February, immigrants added 1,277 million jobs while native Americans lost -420,000 jobs according to the BLS. Or maybe Biden can change his campaign motto to “Make America Great Again … For Immigrants, NOT Natives.”

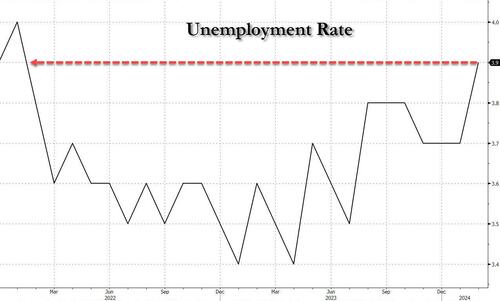

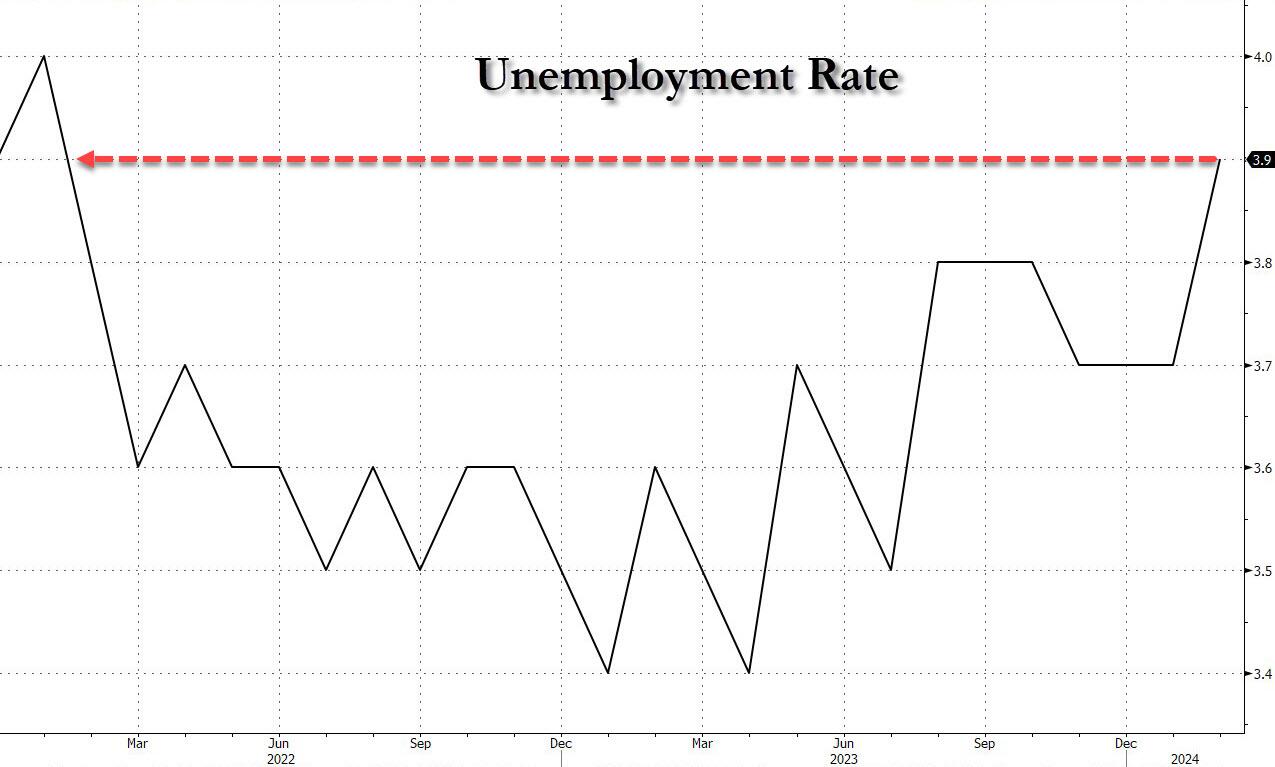

In February, the unemployment rate unexpectedly jumped to 3.9%, the highest since February 2022 (with Black unemployment spiking by 0.3% to 5.6%).

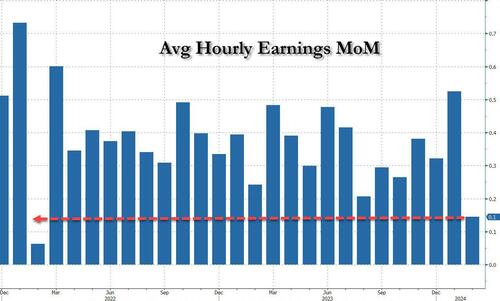

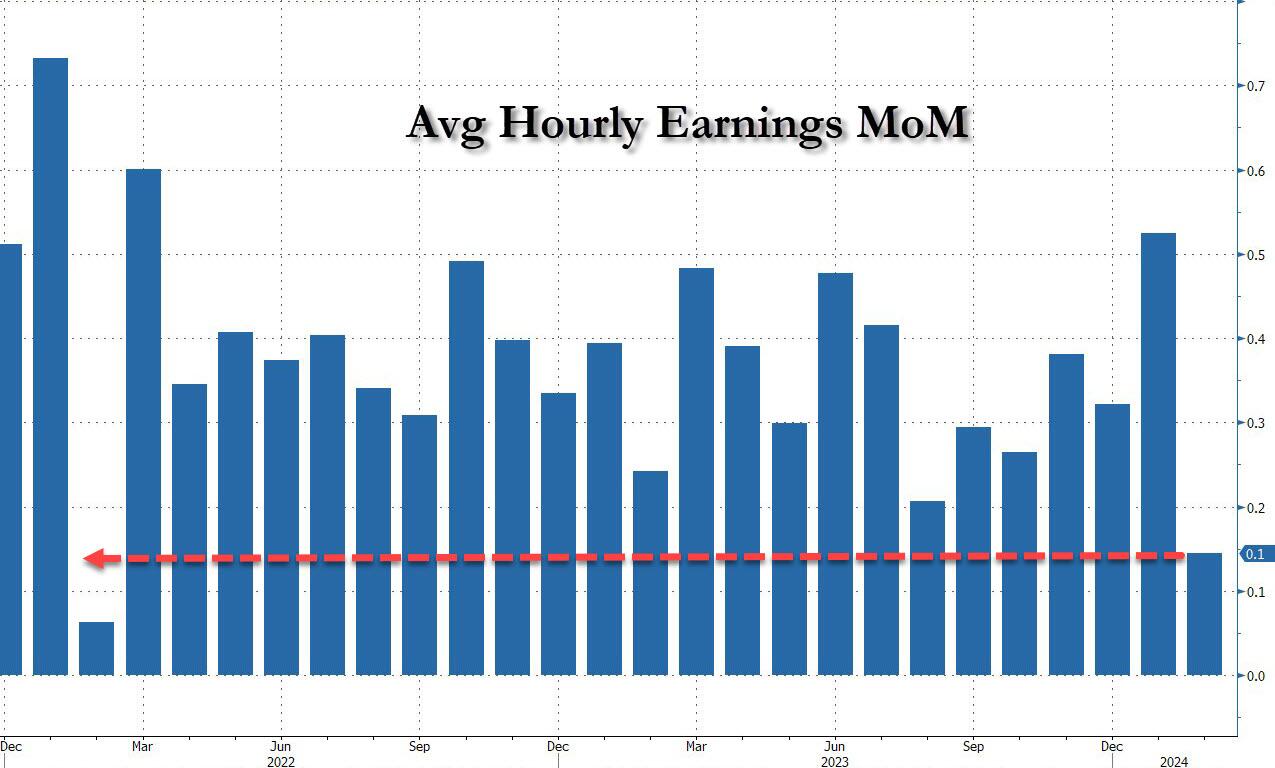

And then there were average hourly earnings, which after surging 0.6% MoM in January (since revised to 0.5%) and spooking markets that wage growth is so hot, the Fed will have no choice but to delay cuts, in February the number tumbled to just 0.1%, the lowest in two years…

It is clear that the labor market is softening, but Biden/Mayorkas will continue to let millions of illegal immigrants pour across the border making the labor market even softer than before. But the top 1% are making out like bandits from the illegal immigration. Bandits benefitting bandits.

After witnessing the debacle called “The State of the Union Address” or “Crazy Grandfather Screams At Nation To Get Off His Lawn,” I was hoping that today’s jobs report would make me happier. It didn’t. In fact, the February jobs report was downright awful.

Maybe now you can understand why Biden gave his angry SOTU speech. Perhaps he saw how bad February’s jobs report was for Middle class America and was trying to redirect the rage away from himself towards the Supreme Court, MAGA Republicans, corporate America (his biggest donors?), and the 6 year old that walked across The White House Lawn uninvited.

We are living in a banker’s paradise. Where a top administrative official pushes to change forecasts of the economy. Hey, it’s a Presidential election year and literally anything goes.

The disagreement was over forecasts for 10-year Treasury yields in the budget, a linchpin estimate that is intertwined with other measures, like debt service costs.

Forecasts in the president’s budget proposal — scheduled for release Monday — are typically set by Treasury Secretary Janet Yellen, Office of Management and Budget Director Shalanda Young and the chair of the Council of Economic Advisers, Jared Bernstein. The group is known in fiscal circles as the troika.

An October meeting, however, included a fourth invited principal: Brainard, who directs the National Economic Council. Brainard at one point disagreed with Yellen, Young and Bernstein on the 10-year interest rate projections and predicted a slightly lower rate, the people said, speaking on condition of anonymity to detail the discussions.

The difference between the forecasts was modest and both were well within range of private-sector estimates, the people said. The exact scope of Brainard’s changes aren’t clear.

Brainard’s forecast painted a modestly better picture for Biden. A lower interest-rate forecast would have the effect of an improved overall outlook by offering more support for growth and suggesting less concern about inflation. It also would lower borrowing cost projections at a time of rising worries about the US deficit and debt.

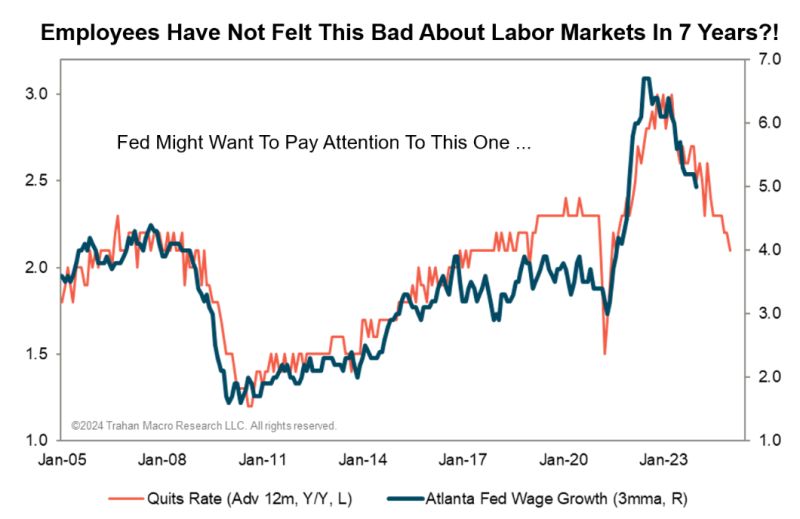

Let’s see what the Troika have to say about the quits rate.

Yes, it is the Ides of March. No, not Nikki Haley trying to sabotage Donald Trump’s campaign after Nikki got clobbered in all but two state primaries. So in a sour grapes move, Haley didn’t endorse Trump. But the Ides of March refers to the stabbing of Julius Caesar (led by Brutus).

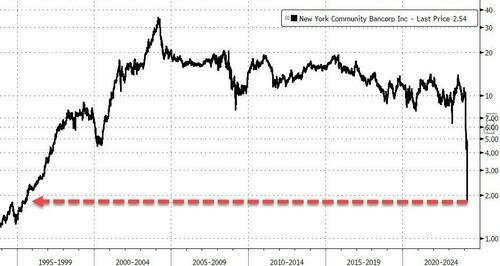

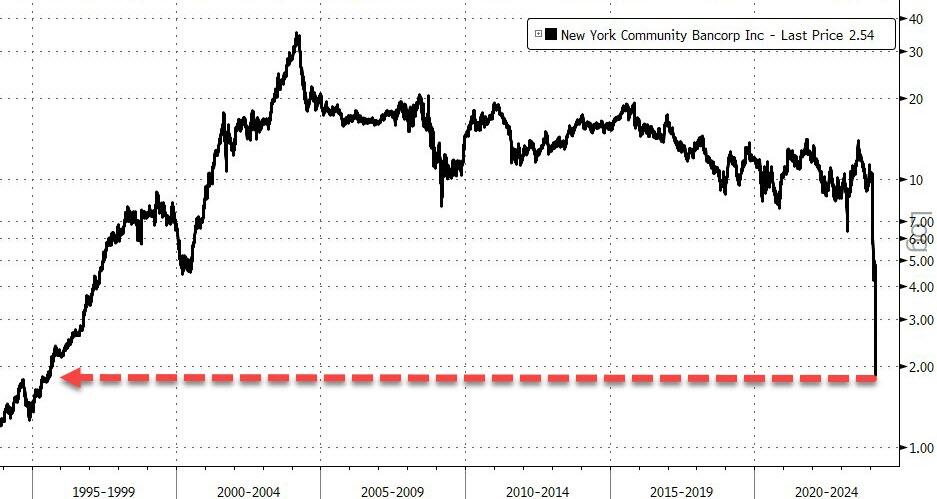

Once the darling of the small banking crisis comeback, New York Community Bancorp has crashed 45% to fresh 30 year lows after The Wall Street Journal reportsthe bank is seeking to raise equity capital in a bid to shore up confidence in the troubled regional lender.

According to people familiar with the matter, NYCB has dispatched bankers to gauge investors’ interest in buying stock in the company.

There’s no guarantee there will be a deal, or that one would succeed in addressing the bank’s challenges, which as of Wednesday morning had led to a roughly 80% decline in its stock price since January.

This is not a good picture for a bank… Would you hold your deposits there?

Last month, DiNello laid out a series of options the bank could explore to bolster its balance sheet, including selling assets from certain non-core businesses. The bank has also considered turning to newfangled financial instruments that would share the risks of those loans with outside investors, people familiar with the matter said.

As WSJ reports, finding takers for those assets, at least at prices that would make a deal worthwhile, has been challenging and U.S. officials have expressed reservations with banks pursuing credit-risk transfers that would shift the burden of potential losses to entities outside of the regulated banking system.

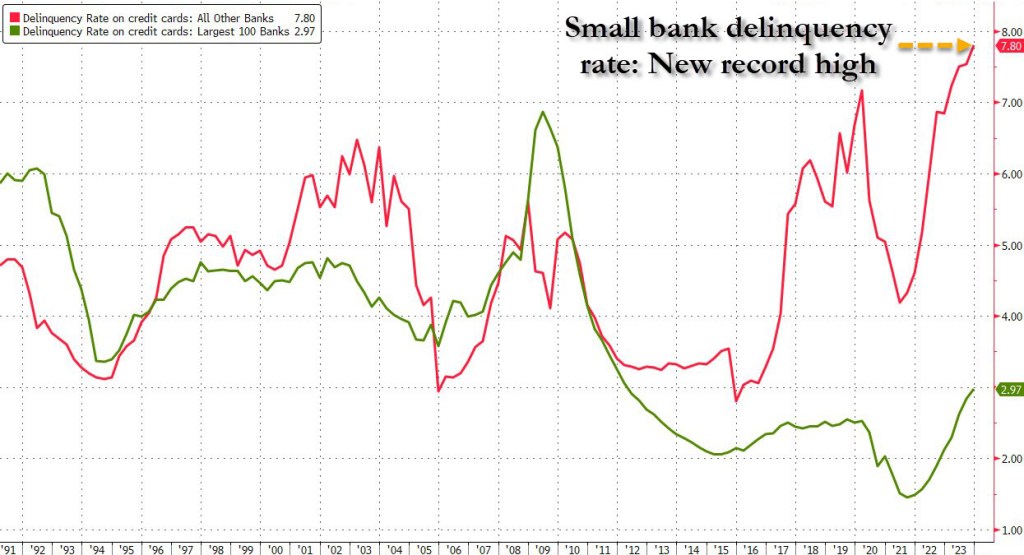

Finally, as a reminder, NYCB is not alone. The red line below shows ‘small banks’ are in trouble absent The Fed’s BTFP facility…

Housing is simply unaffordable for millions of Americans. Home prices are up 33% under Biden’s Reign of Error, while mortgage rates are up 146% under Vacation Joe. Somehow I doubt if Biden will brag about home prices and mortgage rate in his State of the Union address.

On the mortgage side, the Market Composite Index, a measure of mortgage loan application volume, increased 9.7 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index increased 12 percent compared with the previous week. The seasonally adjusted Purchase Index increased 11 percent from one week earlier. The unadjusted Purchase Index increased 13 percent compared with the previous week and was 8 percent lower than the same week one year ago.

The Refinance Index increased 8 percent from the previous week and was 2 percent lower than the same week one year ago.

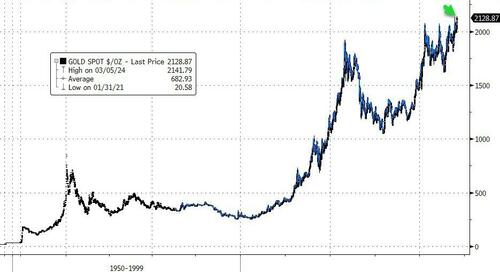

Let’s start with gold. Extending their run of the last few days, spot gold prices just exceeded their all-time highs, topping $2140 for the first time in history…

Source: Bloomberg

A longer view.

Source: Bloomberg

What is gold pricing in about future Fed action? Real rates dramatically negative? As Luke Gromen noted on X:

“When gold rises in your currency DESPITE positive real rates, the gold market is saying ‘Your government will have a debt spiral if real rates remain positive’.“

Source: Bloomberg

Bitcoin just hit $68,567.57, also an all-time high.

The Alt-Assets (gold, silver, Bitcoin) have counterattacked!!

Or as Bonnie Beecher almost sang in a Twilight Zone episode, “Come wander with China Joe Biden.” On The White House lawn. Or wander with The Federal Reserve!

The USA is a runaway train with a dead man (China Joe is about as dead as one can be) in the engineer’s seat.The conductor goes through the cars assuring the passengers that everything is fine. . . never mind the screeching wheels on the curves. . . or the blinding strobe effect of low sunlight passing through the trees out the window at a hundred and forty mph. . . or the bump that made half the stuff in the overhead luggage rack jump out. More than half the people on-board are at tachycardia levels of fright — some are screeching — but the other less than half just remain fixed on their phones and laptop screens. They can’t be bothered to look out the window…

Okay, that’s a metaphor.

But if you’re a citizen of our country and care about it, these are the matters you’d better pay attention to, because they are all going off the rails.

The war in Ukraine. We started it in 2014 to mess with Russia and Russia is going to finish it. Who knows what our real motives were. A resource grab? A desperate ploy to erase our national debt by creating a global fiasco? Sheer psychopathic hatred of this Putin fellow? We can’t bring ourselves to acknowledge the failure of this ill-conceived venture. Instead, our feckless allies in Europe are foolishly rattling their sabers, apparently forgetting that you don’t bring a sword to a nuclear missile fight.

Mr. Macron in France affects to offer up his army for slaughter on the blood-soaked plains of Ukraine, just as the Ukrainians offered up a half a million of their young men so that Victoria Nuland could feel good about herself. Mr. Macron is insane, but the society he presides over is collectively insane, so perhaps he represents them well. Similarly, Olaf Scholz in Germany, whose top generals were caught on a leaked recording last week discussing their plan to blow up the Kerch Bridge that connects Crimea to Russia. Do you understand that this would be a direct attack on Russia, an act of War by NATO? And what the obvious consequence would be?

The phantom government of “Joe Biden” is too weak and mindless to join any negotiation. Ukraine and Russia are up to some kind of cross-talk down in Riyadh with Prince MBS. Even Mr. Zelensky went down for a day, though video appears to show him coked-up, sniffling and snarfling, not a good sign. If ever there was a time to end this stupid conflict, it’s now, before the Russian election. After that, terms will only be more difficult for Ukraine, up to direct custodial supervision instead of remaining a nation. It was never any of our business (though the Biden family, BlackRock, and the CIA saw fabulous opportunity to profit there).

Next is the border. You saw last year how the blob elite greeted the transfer of illegal immigrants to their happy little island of Martha’s Vineyard. (They were not amused by Governor DeSantis’s prank, and off-loaded the mutts post-haste.) But that same smug demographic doesn’t care if hundreds of thousands are distributed to the big cities, which are now fiscally destabilized by them to an extreme, probably to bankruptcy.

Of course, that is not the main thing to worry about with what altogether amounts to millions of border-jumpers flooding our land. The main reason to worry is what the blob that invited them here intends for them to do, which, you may suspect, is to unleash mayhem in the streets, malls, stadiums, and upon our infrastructure just in time to derail the election — perhaps even to make war on us right in our homeland. The US government is paying for this whole operation, you understand, funneling our tax money to international cut-out orgs who set up the transfer camps in Panama, and buy the plane tickets for the mutts to cross the ocean, and coordinate with the Mexican cartels to shuttle this horde of mystery people among us to work their juju for the Democratic Party. The pissed-off-ness of the public has passed the red line on this.

A third FUBAR is the lawfare campaign of the Democratic Party and its regime in power against the citizens of this land. This folder includes overt and obvious political prosecutions by DA’s and AG’s who make election promises to “go after” individuals without such niceties as probable cause. It includes the gigantic new scaffold of inter-agency censorship and propaganda. It includes the psychopathic struggle sessions mandated by “diversity and inclusion” policy. It includes election-rigging directed by the likes of Marc Elias and Norm Eisen, getting states to fiddle laws on voter ID and mail-in ballots. It includes the political protection of rogue groups ranging from looter flash-mobs to Antifa anarchists who bust up things and people and burn buildings down. It includes state officials who peremptorily kick candidates off the ballot. It includes a nakedly biased judiciary, and especially the use of the DC federal district court to punish people extralegally, unjustly, extravagantly, and cruelly. In short, lawfare is the complete perversion of law, and we-the -people are entreated by reprobate officials such as Merrick Garland and Letitia James to accept it.

A fourth item on this list is the US economy which has been overwhelmed by maladministration of an overgrown monster bureaucracy, and the gross (perhaps fatal) mismanagement of the government’s money. The people of this land are not being allowed to do business, to find a livelihood, to transact fairly. “Joe Biden’s” shadow string-pullers are messing as badly with the oil and gas producers as they have messed with Ukraine. And they are doing it in pursuit of a laughable mirage: their “green new deal.”

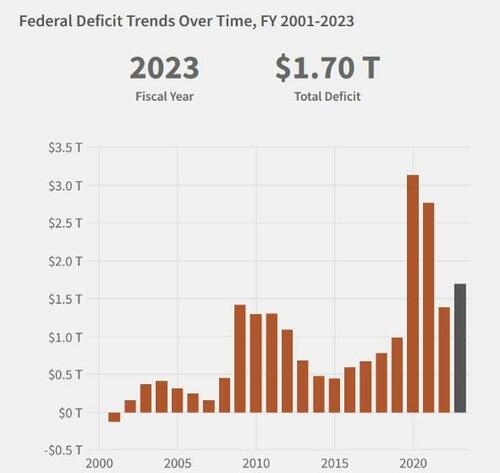

John Podesta, the “clean energy czar” who replaced the Haircut-in-search-of-a-brain called John Kerry, sits on a $370-billion slush fund that can be used to just dole out to anyone and everyone a political patronage payoff, especially to janky “community” orgs and NGOs with fake agendas. This really just amounts to an asset-stripping operation that will leave the American people busted and with broken supply chains for everything. Instead of annual budgets, Congress raises the US debt ceiling by “continuing resolutions” to keep the government from shutting down. The national debt races to the $35-trillion mark. As interest rates on debt rise, our debt payments now exceed our military spending. You can be sure that our country will break down financially very soon.

The capper on today’s list is the nation’s health, the racketeering system we’ve set up to care for it, and the public health agencies of the government that enabled the Covid-19 operation to happen. The CDC continues to push vaccines that have killed millions of Americans and more millions around the world, and has probably compromised the well-being of millions more going forward. Corporate medicine — that is, your doctor, and your hospitals — is a sinking Titanic of grift and chaos. Try to get an appointment to even see a doctor for an emergency. Try to avoid being bankrupted by your treatment. Try to get out of a hospital alive. Yeah, it’s that bad.

The doctors have surrendered your trust in them with their lying and their bullshit. The current director of the CDC, Mandy Cohen and her predecessor, Rochelle Walensky, have knowingly presided over the mass killing and injuries imposed on the mRNA vaccinated. Hundreds of their deputies should be liable for prosecution, and so should many of the other prominent characters in the Covid Saga: Fauci, Birx, Collins, Baric, Bourla, Daszak, Califf, Woodcock, Hahn, and many more.

What are we going to do about any of this? Return to the metaphor. The runaway train is still picking up speed. You can’t just jump off at 150 mph. If you’re one of the passengers watching this in horror, maybe you can decouple your car, or get the conductor to do it by any means necessary. Let’s say that each car behind the engine of this train is a state of the United States. Let the engine up front with the dead man at the controls ride that runaway to its terrible conclusion. Cut loose the cars behind it to take care of themselves, to slow down, get a grip on their situation, and make plans to find a better engine to pull the train. Decouple. Cut loose. It’s the only way.

Too much debt! US politicians are spending too much money and borrowing too much. Unfortunately, that is what Biden and Bidenomics is all about: Federal targeted spending and loads of debt.

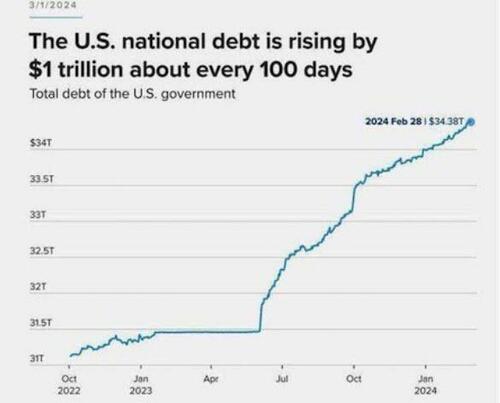

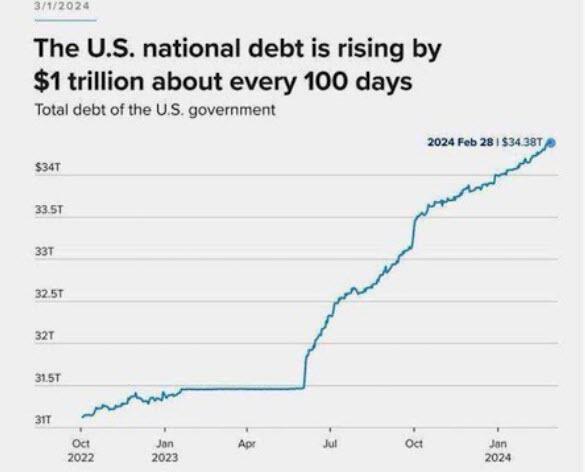

Now it requires $1 trillion of new debt every 100 days to achieve nothing but remaining static economically. The regime media pundits and the cabal on Wall Street tell us the economy is doing great. No recession in sight. All is well. The dumbed down and distracted ignorant masses don’t realize all the reported “economic growth” is “created” by the government, enabled by The Fed, spending billions on their wars in Ukraine and the Middle East, funneling the money into the Military Industrial Complex corporations; paying for the transportation, feeding, and housing of the illegal invading hordes; hiring more government drones to harass the citizenry, and desperately trying to prop up a corrupt tottering empire in its final death throes.

Anyone with even the slightest mathematical acumen knows increasing the national debt at a rate of $1 trillion every 100 days is a death wish. Why would those pulling the strings behind the scenes of this acceleration towards the cliff of national suicide be doing so at this point in time? It’s almost as if the November elections are a deadline for them to complete their exit strategy plan.

I believe we are entering the Great Taking phase of this clown show.

They are purposely creating a global financial disaster in order to take everything you and I have. It sounds crazy, but so is adding $1 trillion of debt every 100 days.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.