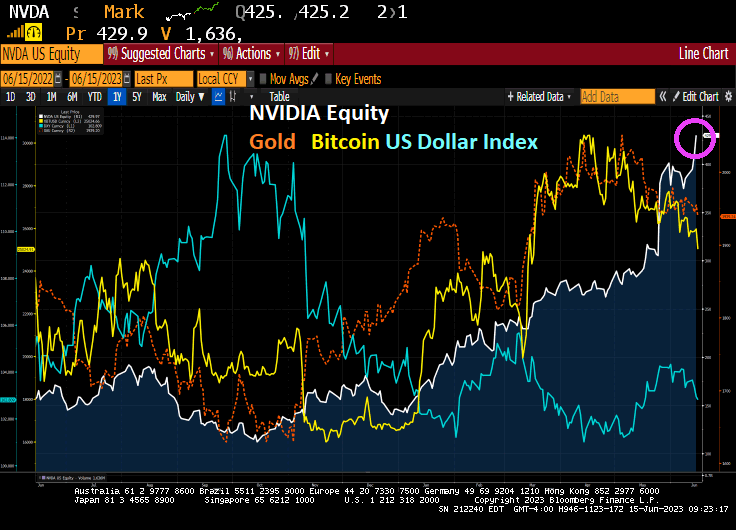

The Artificial intelligence (AI) boom is resulting in Nvidia’s stock soaring to 429.9. At the same time, Bitcoin (yellow), the US Dollar (blue) and Gold (gold) are declining.

Of course, markets are dynamic and gold/silver are likely to start up again along with bitcoin and other cryptos..

The leading crypto today? Dogecoin!

AI versus no intelligence. I give you Resident Joe Negan.

Now that I know that the US is building a railroad from the Pacific Coast to the Indian Ocean (according to Resident Joe Negan), I feel so much better. /sarc

On the other hand, The Philadelphia Fed’s Business Outlook index for June fell to -13.7.

On the positive side, retail sales surprised to the upside which would ordinarily trigger more rate hikes from The Fed. +0,3% MoM in May versus -0.2% MoM expected.

Now Fed Funds Futures are pointing to a rate hike at the July FOMC meeting.

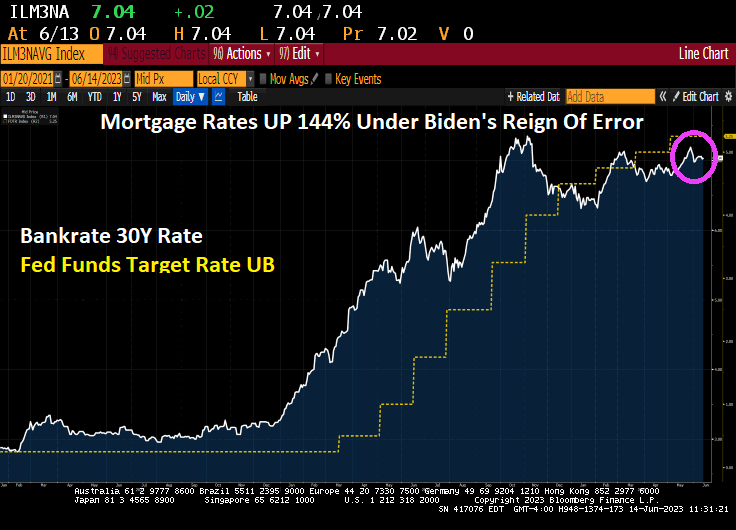

Biden’s “reign of error” is horrific. The inflation caused by Biden’s policies, The Federal Reserve and insane Federal spending has caused mortgage rates to soar 144% since Biden took office.

While The Fed is likely to pause today, but Fed Funds are pricing in a July rate hike.

The Fed will annouce a pause at today’s FOMC meeting, so don’t look for mortgage rates to do much today.

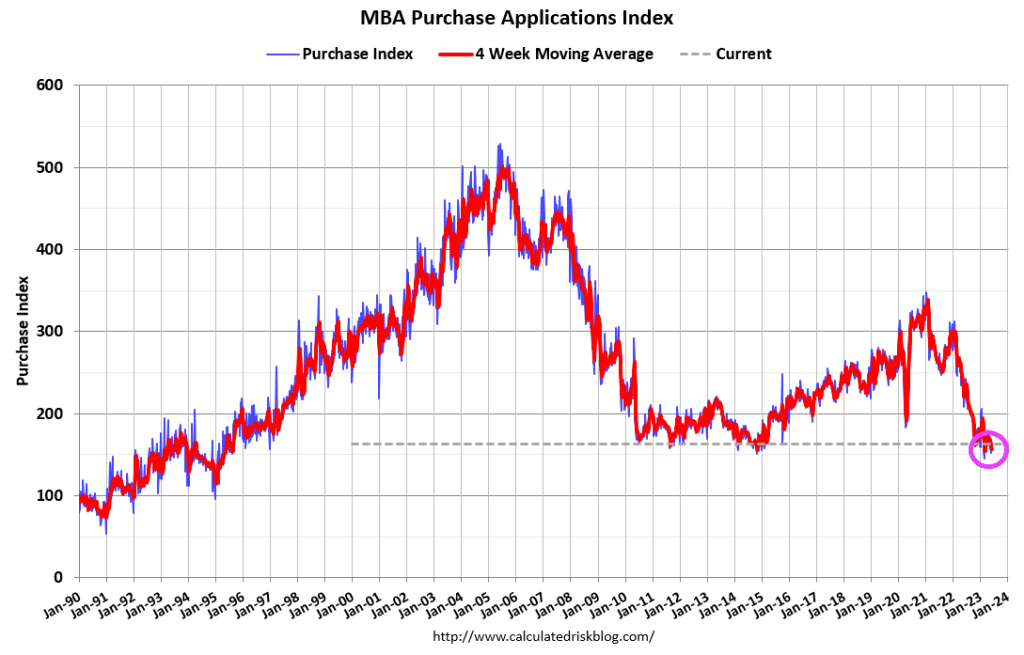

Mortgage applications increased 7.2 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending June 9, 2023.

The Market Composite Index, a measure of mortgage loan application volume, increased 7.2 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index increased 18 percent compared with the previous week. The Refinance Index increased 6 percent from the previous week and was 41 percent lower than the same week one year ago. The seasonally adjusted Purchase Index increased 8 percent from one week earlier. The unadjusted Purchase Index increased 17 percent compared with the previous week and was 27 percent lower than the same week one year ago.

Mortgage rates declined for the second straight week, with the 30-year fixed rate decreasing to 6.77 percent. Mortgage applications were up over the week, but remained well below levels from a year ago.

Joe Biden’s new nickname is “The 5 Million Dollar Bribe Man.” Sort of like Steve Austin.

Okay, Joe Biden was generally regarded as the dumbest member of the US Senate and mean-spirited (I won’t repeat podcaster Joe Rogan’s opinion of Biden). Now we realize how brazenly corrupt Biden is (taking bribes from China and Ukraine to influence American poliicies). Not only is Biden an attrocious human being, but his policies have damaged the US middle class terribly thanks to inflation.

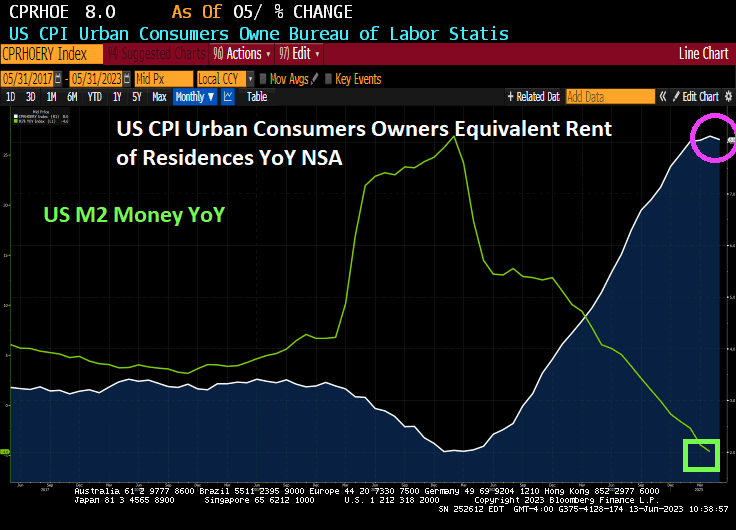

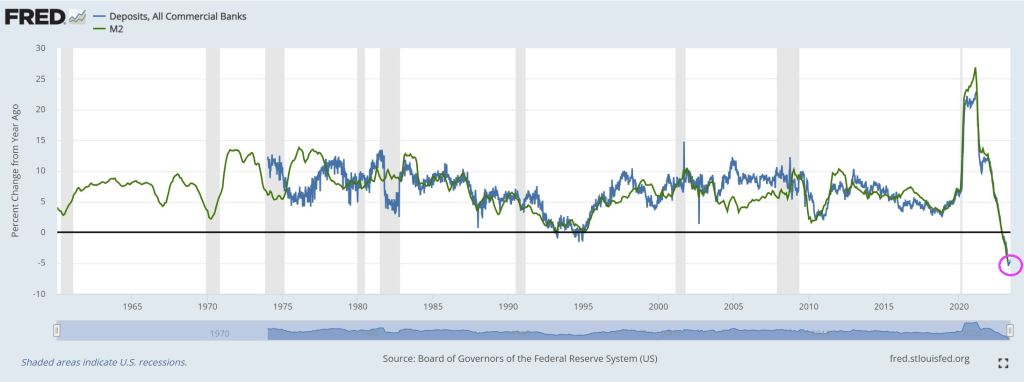

Tomorrow is the Federal government’s inflation report. As it stands today, overall inflation is slowing as M2 Money growth crashed. Core inflation remains persisitently high (white line), rent is still getting worse (orange dotted line at 8.1% YoY. What about food? Online food prices are up 8.2% YoY.

Shopping online is a good place to find cheaper computers and appliances, but grocery prices are still rising at a fast clip.

Prices of consumer goods sold online fell 2.3% in May in the US, the ninth consecutive month of declines and the biggest drop since the pandemic started, according to data from Adobe Inc. That was mainly due to steep decreases in discretionary categories.

Essential items like food, pet products and personal care, however, are seeing persistent inflation. Online grocery prices increased 8.2% from last year — although the pace of inflation has been abating since peaking at 14.3% last September.

Americans have been shifting more of their discretionary purchases to services over the past year, cutting spending on items for the home.

Online prices for appliances were down 7.9% in May from last year, the largest drop in digital-prices data from Adobe going back to 2014. Online prices for computers slumped 16.5% and electronics were down 12%.

The Adobe Digital Price Index was developed with the help of Austan Goolsbee before he became president of the Federal Reserve Bank of Chicago this year. The gauge analyzes one trillion visits to retail sites and more than 100 million items to track price changes.

Yes, Biden and Congress have levied a devastating tax on Americans. Rent and food are two of the largest household expenditures and they are up 8.1-8.,2% YoY.

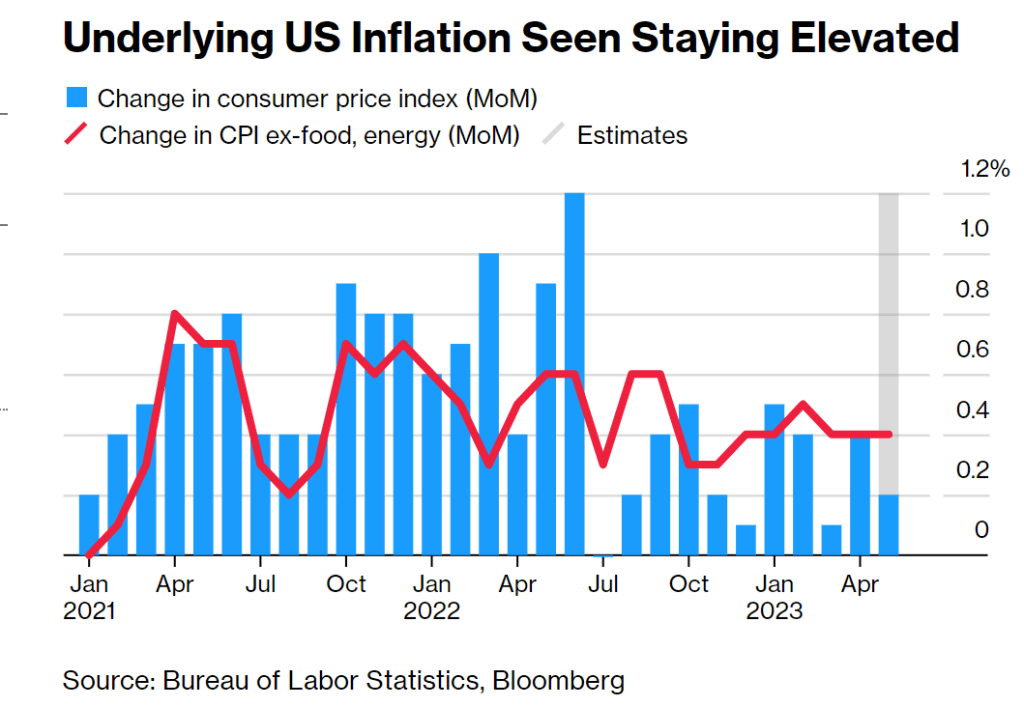

Federal Reserve policymakers are about to take their first break from an interest-rate hiking campaign that started 15 months ago, even as they confront a resilient US economy and persistent inflation.

The Federal Open Market Committee on Wednesday is expected to maintain its benchmark lending rate at the 5%-5.25% range, marking the first skip after 10 consecutive increases going back to March of last year. While officials’ efforts have helped to reduce price pressures in the US economy, inflation remains well above their goal.

Source: Bureau of Labor Statistics, Bloomberg

Investors’ focus will be on the Fed’s quarterly dot plot in its Summary of Economic Projections, which is expected to show the policy benchmark rate at 5.1% at the end of 2023.

By contrast, markets are pricing in the possibility of a quarter-point hike in July followed by a similar-sized cut by December, and some Fed policymakers have emphasized that a pause in the hiking cycle shouldn’t be seen as the final increase.

Fed Chair Jerome Powell, who’ll hold a press conference after the meeting, has suggested he favors a break from hiking to assess the impact both of past moves and of recent banking failures on credit conditions and the economy. His commentary will be scrutinized for hints of the committee.

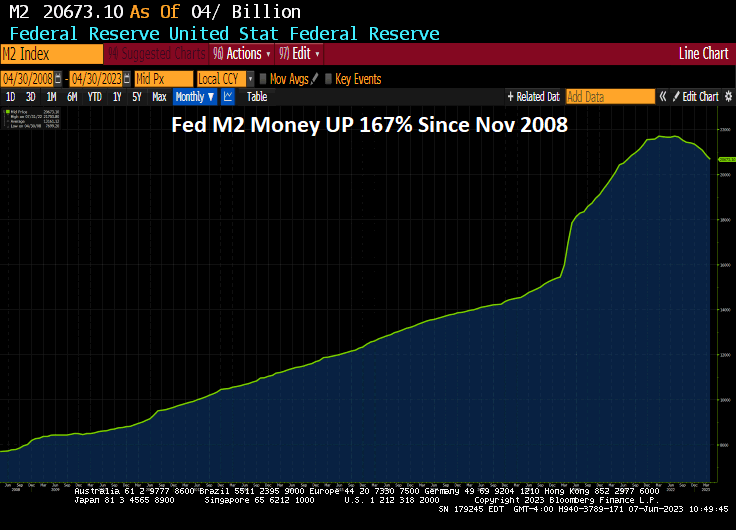

Remember, there is still over $8 TRILLION in Fed assets held sloshing around the economy. The Fed never really removed the excess liquidity and it continues to stoke asset bubbles.

Bear in mind that The Fed is pausing at 5.25% Fed Target Rate, while the Taylor Rule suggests rate hikes to 10.12%. So, Foul Powell is pausing at just over the half way mark.

Of course, Biden’s and Congress’ massive spending spree is causing inflation, and The Fed has no control over Biden/Congress irresponsible spending.

Nicolas Maduro of Venezuela must be envious of Joe Biden. I don’t think even Maduro has the stones to have his politiical opponent charged with espionage in the run-up to a Presidential election. Particularly when the US President has been bribed by China and Ukraine and has similiar sensitive document hoarding issues (at least Trump didn’t leave boxes of sensitive documents in a garage like Biden did when he keeps his Chevy Corvette).

So where do we sit today after Biden has signed the debt ceiling increase and massive spending splurge?

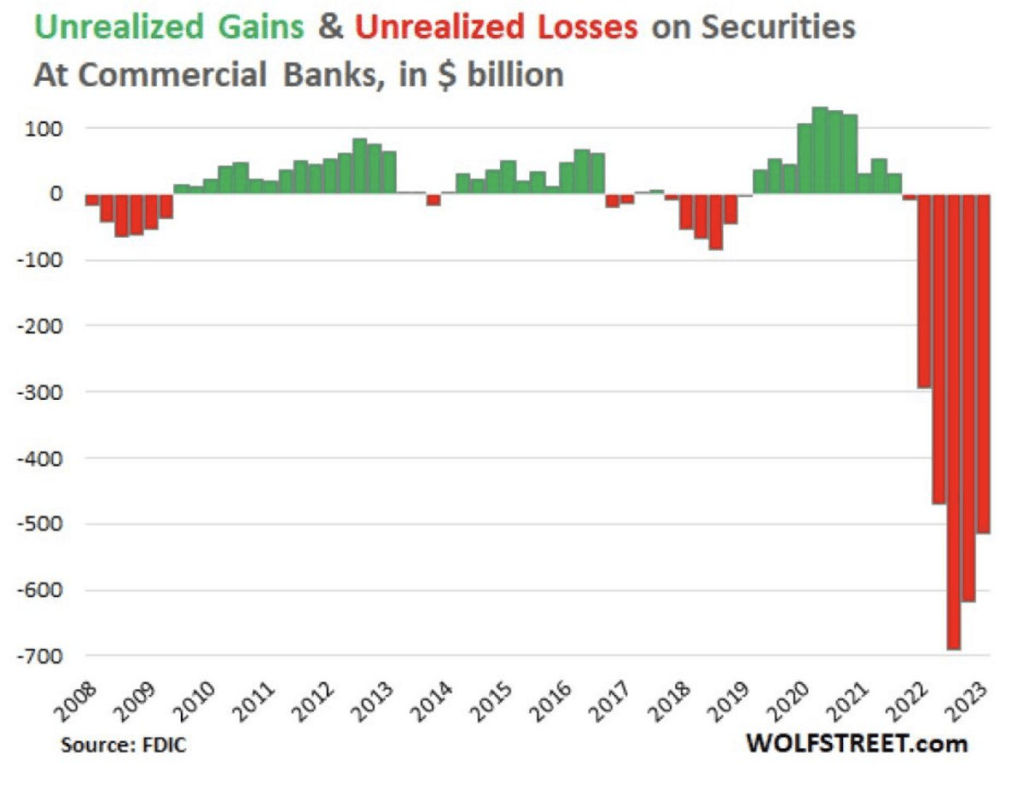

First, look at the crashing bank deposit problem. Well, the solution is for The Fed to fire up the money printing press! Keep on printing!

This not surprising if you have read Nobel Laureate George Stigler’s treastise on regulatory capture. Essentially, big corporations (big media, big tech, big banking, big pharma, big defense, big agriculture, etc.) essentially own Congress, the Biden Administration and Federal regulators. After all, Biden has been bribed with millions of dollars by China and Ukraine and, like a Banana Republic, has is avoiding prosecution and instead prosecuting his political opponent, Trump. Don’t worry, if they get Trump that will indict DeSantis for something.

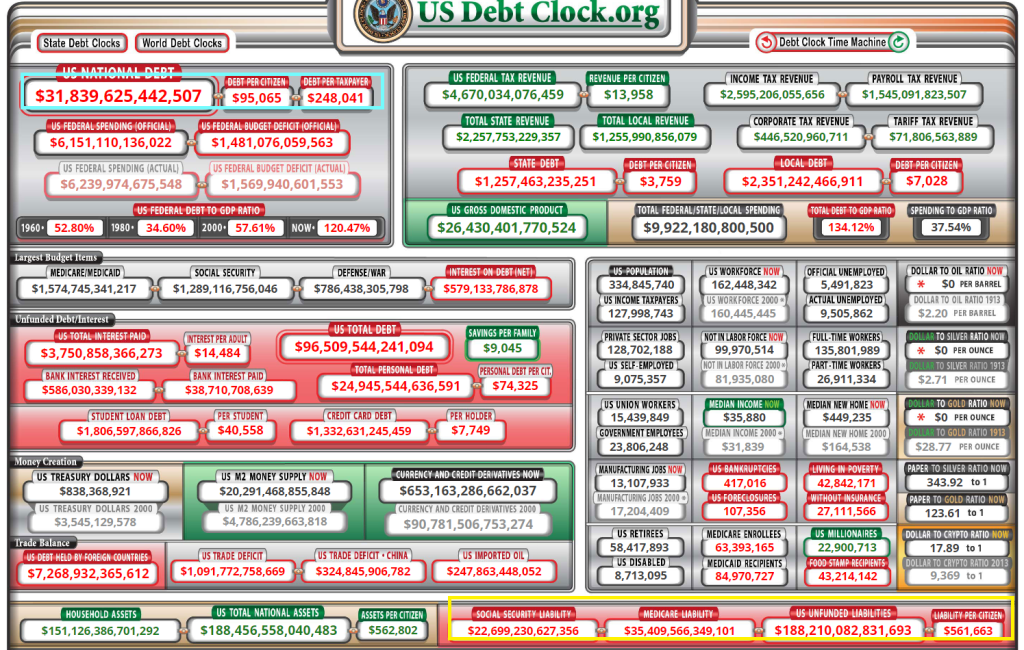

US debt stands at $31.8 TRILLION with $188 TRILLION in unfunded liabilities (which means higher personal taxes and much more debt).

Treasury Secretary Janet “Too Low For Too Long” Yellen, and former Federal Reserve Chair, is partly responsible for a phenomenon plaguing America: the death of starter homes.

As Mish has discussed, with main markets no longer an option for first-time buyers, Point2 looked at the country’s 100 largest secondary cities for the median price of a starter home and renter households’ median income. Defined as large non-core cities within a metro, these cities used to be fruitful house-hunting grounds for first-time buyers exploring less-expensive options away from main cities. But as it turns out, unaffordability can put a dent in homeownership plans regardless of city type or size.

In 41 of the 100 largest secondary cities in the U.S., renters earn half or less than half of the income they would need to buy a median-priced starter home.

There are no non-core cities in which renters could comfortably make a move toward homeownership: In 10 cities, the necessary income is about triple what they earn.

Would-be buyers in Burbank and Glendale, CA have it worst: They lack 67% of the income they would need in order to make the move from renter to homeowner.

Renters in 9 California cities would need to earn about $100,000 more in order to afford a starter home. Based on the latest renter income figures, starter home prices, and mortgage rates, non-core cities in the LA and San Diego metros are the toughest for first-time homebuyers.

In 15 of the 100 largest secondary cities, renters would need less than 4 months’ worth of extra income to afford the transition to owning a starter home.

Homeownership is within reach in Independence, MO, and Broken Arrow, OK. Those who dream of owning here would need less than one month’s worth of extra income to afford a starter home.

California Tops the List of Worst Places to Look

California has the dubious distinction of having the top least affordable starter home cities.

A starter home, according to the Census Department is priced in the bottom third of homes in the area.

Pomona, CA, is in fourteenth place. The average renter in Pomona makes $49,000 a year and needs to get to $121,000 a year. That’s nearly 2.5 times current salary.

In Burbank, CA, the average renter makes $63,000 year an needs to get to $193,000. That’s over 3 times current salary.

Within Grasp

In no market can the average renter make the plunge.

But in Independence, Missouri, or Broken Arrow, Oklahoma, the average renter is respectively just 2% and 5% short of the amount needed for a starter home

Not Shocking

None of this is shocking. It matches one one should expect looking at Case-Shiller home prices and mortgage rates.

The Fed wanted to produce inflation and it did. But for years the Fed did not even see the inflation because the manifestation of inflation was in asset prices, not the price of consumer goods.

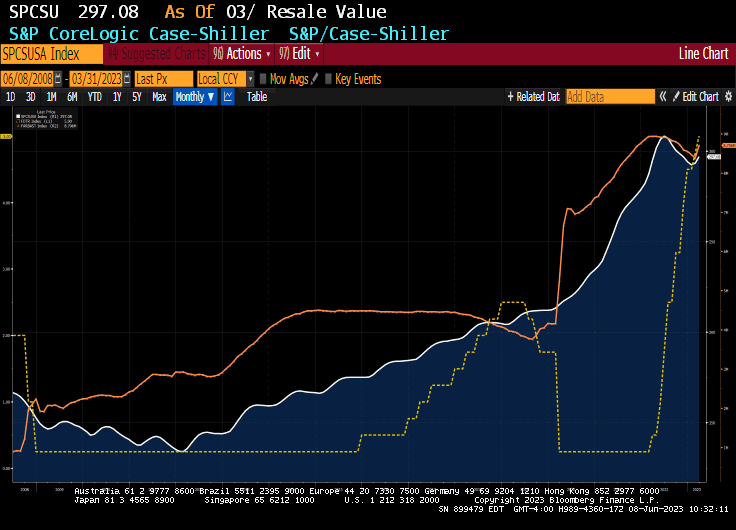

Case-Shiller Top City Home Prices Decline From Year Ago for the First Time Since May 2012

Housing starts, like mortgage purchase demand, remains depressed compared to the housing bubble of the 2000s.

Now, will The anticipated Fed pause in rate hiking help? Not likely. The Fed still has over $8 trillion in monetary stimulus chasing assets. Too much Stimulypto.

One has to wonder about The Feral Reserve. Since The Great Recession of 2008, The Federal Reserve has printed a staggering amount of money (know as QE). There is still about $8.3 TRILLION in monetary stimulus sloshing around the economy.

And M2 Money printing is up 167% since November 2008.

So, despite the talking heads from The Fed and CNBC, etc blathering about Fed tightening, there remains over $8 TRILLION in monetary stimulus chasing asset prices.

Is The Fed ACTUALLY the US economy? Or is The Fed the financing arm of the Democrat party?

Yes, The Fed looks like they are pausing .. rate hikes.

You must be logged in to post a comment.