When we look at tomorrow’s US jobs report, it is important to acknowledge that 1) The Federal Reserve has not yet removed the Covid stimulus (green line) and 2) the ADP payroll jobs added was only 132k in August while non-farm payrolls jobs added in July was 528k. That is quite a spread!

(Bloomberg)The hotly anticipated US jobs report has the potential to tip the scales toward a third jumbo-sized hike in interest rates later this month after a wave of data that point to a resilient consumer and high labor demand.

Friday’s report is one of the last marquee releases Fed officials will have in hand before the mid-September policy meeting to help them decipher a complex economic and inflationary puzzle.

Forecasts call for a healthy, yet more moderate 298,000 gain in August payrolls and for the unemployment rate to hold steady at 3.5%, matching the lowest in five decades. Solid wage growth is also expected amid a persistent mismatch between labor demand and supply.

Such figures, in conjunction with a blowout July employment print, improving consumer sentiment figures and a surprise pickup in job openings, could be enough to push the Fed to raise borrowing costs by 75 basis points, extending the steepest interest-rate hikes in a generation to curb an inflation surge.

As of this morning, Fed Funds futures data is still pointing to The Fed Funds Target rate rising from 2.50% to around 4% by the March FOMC meeting. That is still a large jump of another 150 basis points anticipated.

Under President Biden, inflation has soared and The Federal Reserve claims that they want to extinguish the inflation fire by tightening monetary policy … resulting in rising mortgage rates. Under Biden, mortgage purchase applications are DOWN -41.5% while mortgage rates are UP 96%.

(Bloomberg)The US mortgage industry is seeing its first lenders go out of business after a sudden spike in lending rates, and the wave of failures that’s coming could be the worst since the housing bubble burst about 15 years ago.

There’s no systemic meltdown coming this time around, because there hasn’t been the same level of lending excesses and because many of the biggest banks pulled back from mortgages after the financial crisis. But market watchers nonetheless expect a string of bankruptcies broad enough to trigger a spike in layoffs in an industry that employs hundreds of thousands of workers, and potentially an increase in some lending rates. More of the business is now controlled by independent lenders, and with mortgage volumes plunging this year, many are struggling to stay afloat.

Please note that mortgage purchase applications are DOWN -41.5% under Biden while mortgage rates are UP 96%.

Margin Calls Many other lenders have seen the value of their loans drop, said Scott Buchta, head of fixed-income strategy at Brean Capital, an independent investment bank. The Federal Reserve has tightened rates by 2.25 percentage points this year in an effort to tame inflation, and 30-year US mortgage rates have surged above 5% for government-backed loans. That’s close to their highest levels since the financial crisis, from around 3.1% at the end of last year.

That’s beaten down the value of home loans made just a few months ago. A mortgage made in January and not eligible for government backing could have traded in early August somewhere around 85 cents on the dollar. Lenders usually try to make loans worth somewhere around 102 cents to cover their upfront costs.

For a lender whose loans dropped to 85 cents, the losses can be debilitating, even if they aren’t realized yet. On top of that, business is broadly plunging. Overall mortgage application volume has plunged by more than 50% this year, according to the Mortgage Bankers Association. These business conditions are spurring banks that provide lines of credit known as warehouses to make margin calls and cut credit.

“The warehouse lenders in this industry seem to be extremely on top of things in this downturn, unlike in ‘08,” said bankruptcy attorney Mark Power, who is representing creditors in the First Guaranty bankruptcy. “They are making margin calls quickly.”

Banks have emergency funding they can tap in times of crisis, which can often allow them to stay afloat in hard times. But not always: emergency financing from the Federal Reserve is usually only available for solvent institutions with a chance of recovering. In the last downturn, so many banks had so many soured loans and struggling assets of all kinds that hundreds failed. Nonbanks went bust as well.

Mortgage applications decreased 2.3 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending August 12, 2022.

The seasonally adjusted Purchase Index decreased 1 percent from one week earlier. The unadjusted Purchase Index decreased 2 percent compared with the previous week and was 18 percent lower than the same week one year ago.

The Refinance Index decreased 5 percent from the previous week and was 82 percent lower than the same week one year ago.

Today’s jobs report was … strange. While the US economy added more jobs than expected, we also saw labor force participation contract and real wage growth decline again.

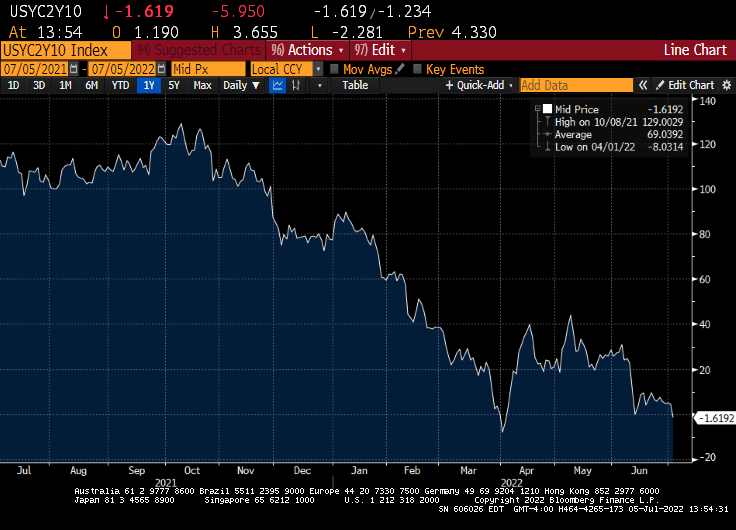

The reaction in the bond market? US Treasury 10-year yields exploded by +14 basis points. As I used to tell my fixed-income students, any basis point jump or decline of 10 basis points or more is a BIG DEAL.

The implied target rate for The Fed (based on Fed Funds Futures) is now lower for the Jan 1, 2024 FOMC meeting (3.025%) than it is for the Sept 21, 2022 FOMC meeting (3.034%).

Mortgage rates? They will go up as The Fed removes its Brawndo, the economy mutilator.

Hold on, The Fed is coming! To raise their target rate by 75 basis points at Wednesday’s FOMC meeting. Will this stem the tide of rising inflation?

Under Biden, we have seen regular gasoline prices rise 82% despite recent declines. Diesel fuel is up 121% and foodstuffs are up 46%. And house rents keep rising at a staggering 14.75% YoY. The recent declines is more due to the global economic slowdown and central bank rate increases than anything Washington DC is doing.

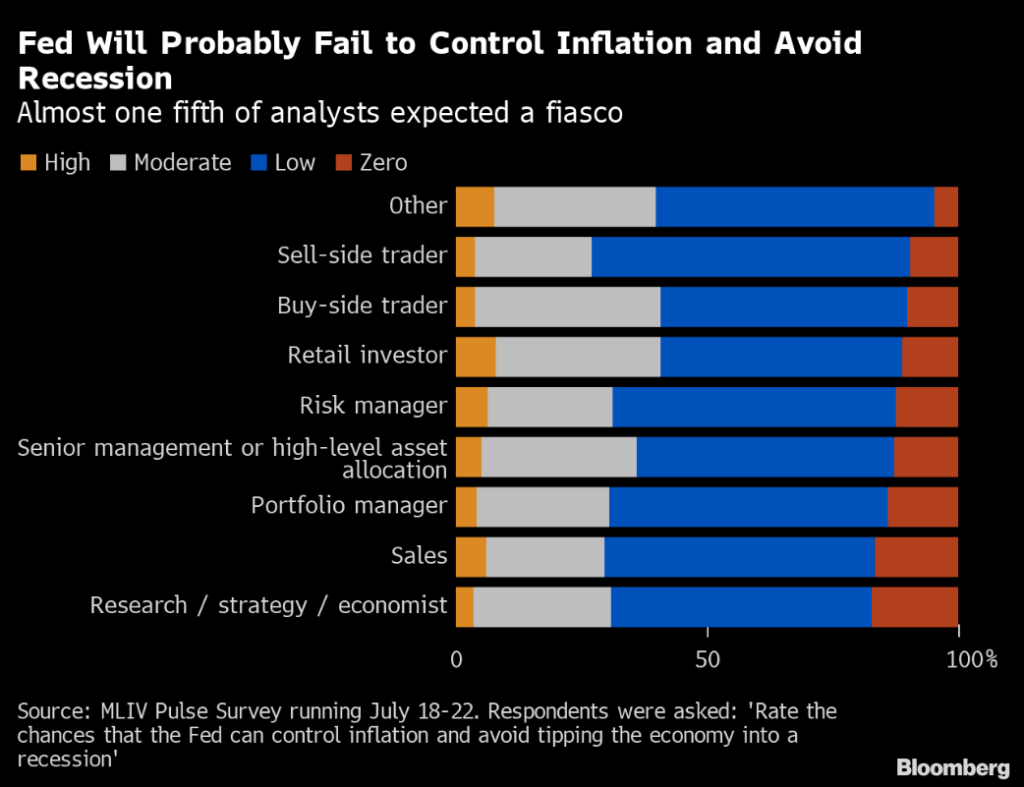

(Bloomberg) Investors are skeptical that the Federal Reserve can tame the worst inflation in four decades without driving the economy into a recession.

That’s bad news for Americans, who face the prospect of a downturn as their bills for food, rent and fuel swell. But to bond investors hit by deep losses this year, it may mean any further pain will be short-lived, as a recession will spark the US central bank to cut rates next year. That’s according to the results of the latest MLIV Pulse survey.

Over 60% of 1,343 respondents in the survey said there’s a low or zero probability that the US central bank can rein in consumer-price pressures without causing an economic contraction. The survey was conducted July 18-22 and included retail and professional investors.

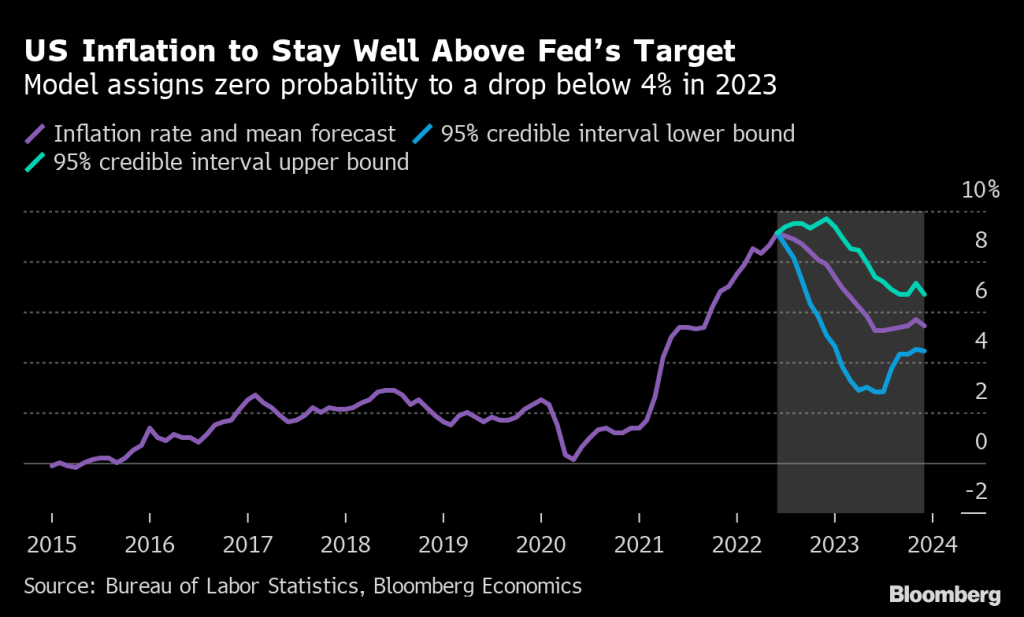

US inflation may be close to a peak, but it’s very likely to stay above 8% through year-end. Bloomberg Economics’ model assigns zero probability to a drop below 4% in 2023. Taken together with increasing recession risks, the Fed faces a tough balancing act as it attempts to bring stubborn price pressures under control without tipping the economy into contraction.

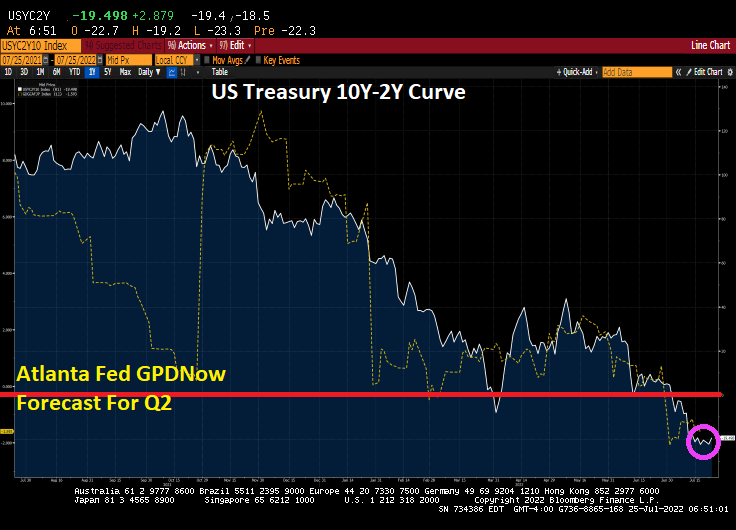

Of course, The Federal Reserve doesn’t really consider energy or food inflation, which are typically higher than core inflation. But going into Wednesday’s meeting, we see the US Treasury 10Y-2Y curve remains inverted (a signal of impending recession) and the Atlanta Fed GDPNow Q2 tracker at -1.6% after a negative Q1 reading.

Will raising the target rate (or ACTUALLY shrinking their balance sheet) reduce inflation? We shall see, but it has got to be better than Lawrence Summer’s suggestion to reduce inflation: raise taxes. Wait a minute, Larry. Inflation was caused by 1) overstimulus by The Fed combined with 2) massive Covid spending by Biden, Pelosi, Schumer and 3) Biden’s anti-fossil fuel policies. So instead of suggesting a decrease in Federal spending, Summer’s wants to give MORE of your money to Biden and Congress to spend. What an unbelievable nitwit.

Here is a picture of Larry Summers, Jay Powell and Janet Yellen attending the FOMC meeting in Washington DC.

Face it. The Biden Administration has little interest in trying to increase the supply fossil fuel energy which would anger his “green” base (like building more refineries or allowing for more crude oil and natural gas exploration). So, the burden of “inflation fighting” falls on the frail shoulders of The Federal Reserve.

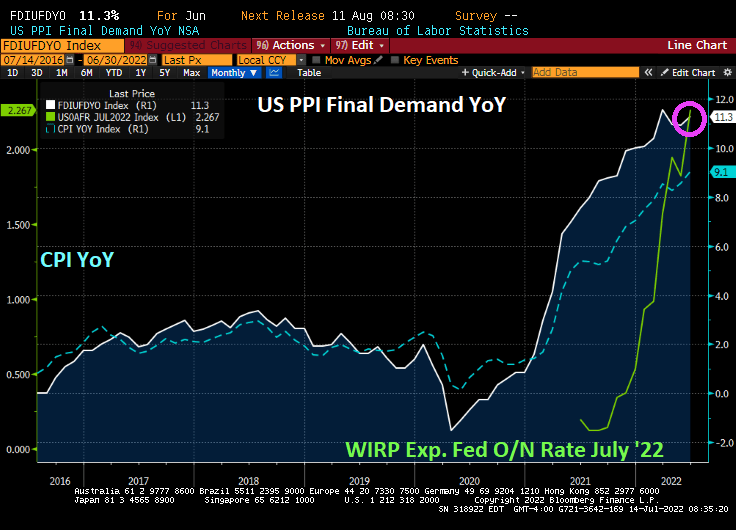

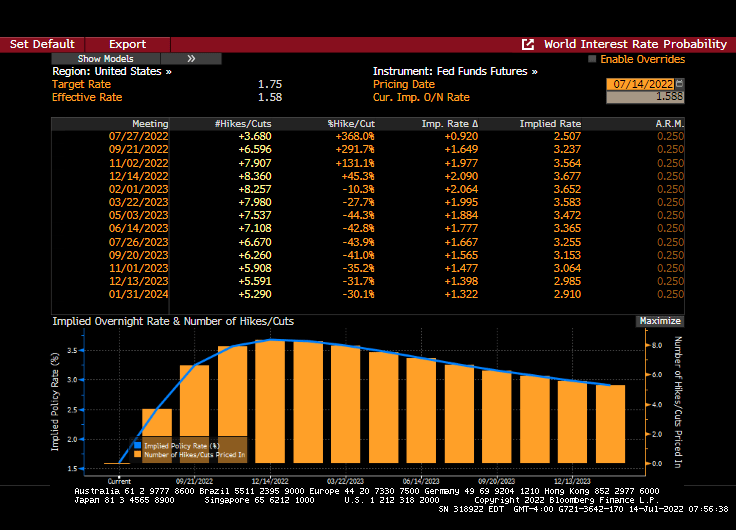

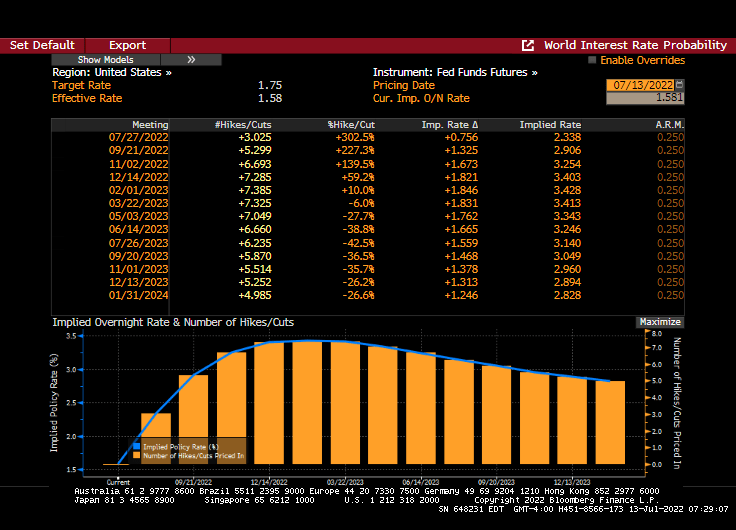

Given today’s US Producer Price Index Final Demand prices rising +11.3% YoY in June, it seems that The Fed has not been able to extinguish the “Tower of Inflation.” But, Fed Funds Futures are pointing to a near 100 basis point (or 1%) increase in The Fed Funds target rate at the July 27th Fed Open Market Committee (FOMC) meeting.

The Fed Funds Futures Data points to a +0.920 (almost 1%) increase at the July 27th FOMC meeting. Followed by rate cuts.

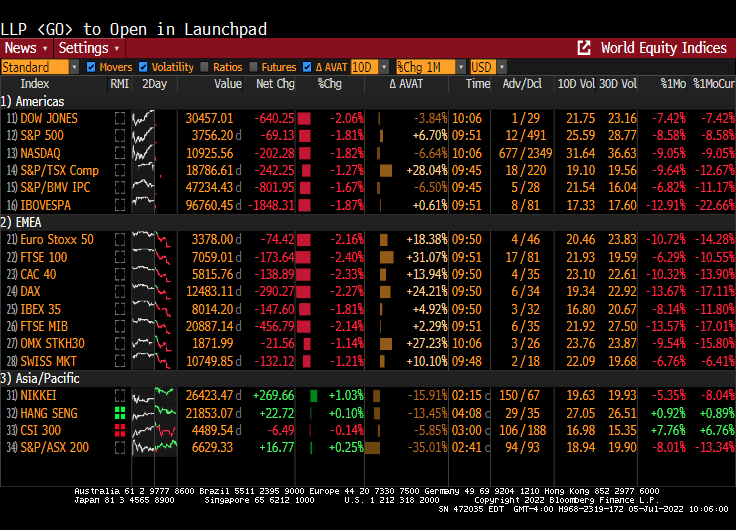

And with the fear of a near 100 basis point increase, today’s stock markets are a sea of red.

It is up to Fed Chair Jerome Powell and policy error brigade to extinguish price increases caused by 1) bad Biden energy policies and 2) too much spending by Biden and Congress. It is like trying to wave-down the Super Chief train with a cigarette lighter.

Yet, the Frail Fed will try to waive down The Super Chief inflation engine with Fed Fireballs. Aka, rate increases of 100 basis points.

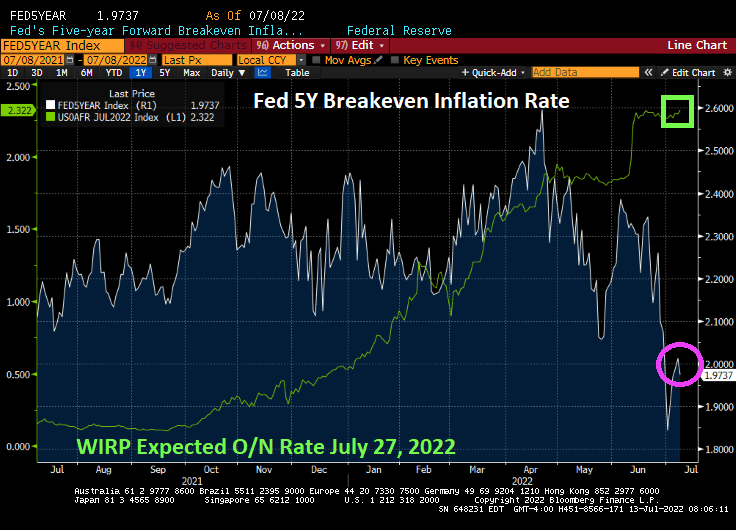

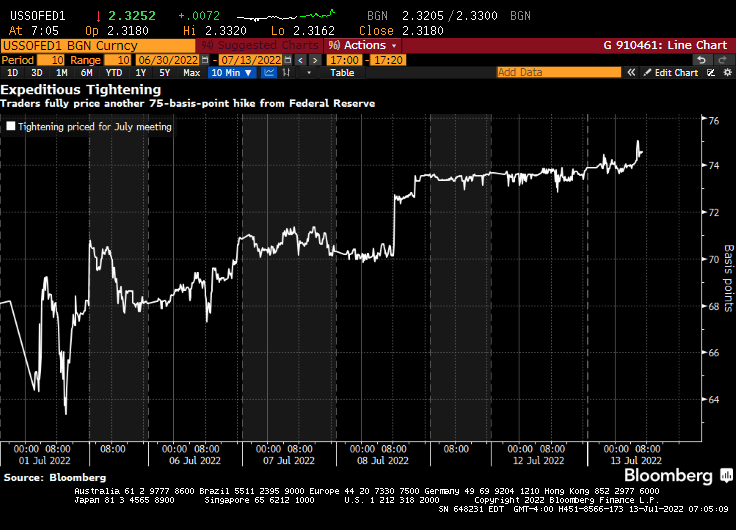

Here we go loop de loop! Traders are pricing in a 75 basis point rate increase at the July FOMC meeting despite collapsing Fed 5-year inflation breakeven rates.

Money markets are betting on a three quarter-percentage point hike by Federal Reserve officials later this month, wagering the US will need to ramp up the pace of monetary tightening to tame inflation.

The repricing comes ahead of a key inflation report due Wednesday. The headline figure for June is set to accelerate to 8.8% year over year, the highest since 1981.

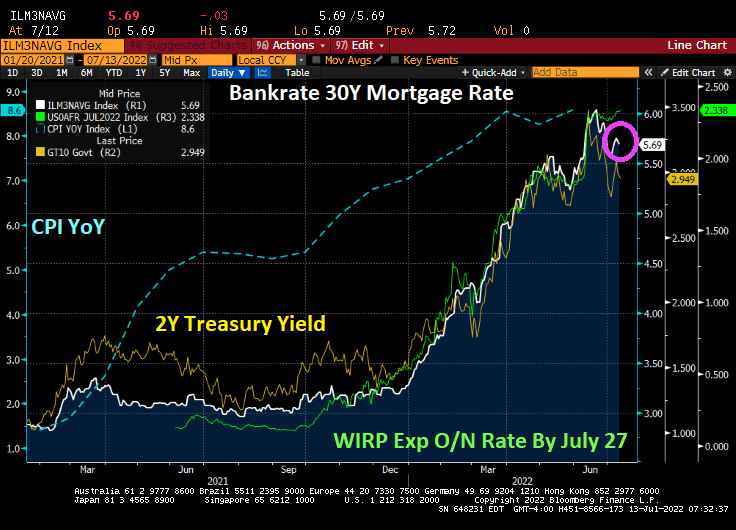

Bankrate’s 30Y mortgage rate fell slightly ahead of today’s inflation report with the expectation of The Fed hiking their target rate by 75 basis points to 2.338% at the July 27th Fed Open Market Committee meeting.

Trader expectations from Fed Funds Futures data:

Last night I watched “The Shallows” on Peacock TV. I thought from the title that it was going to be a biography of The Federal Reserve, but it was a film about a surfer being attacked by a shark.

US inflation is the highest in 40 years, yet inflation may be slowing as 1) The Fed cranks up interest rates and 2) the global economy is slowing.

US inflation data in the coming week may stiffen the resolve of Federal Reserve policy makers to proceed with another big boost in interest rates later this month.

The closely watched consumer price index probably rose nearly 9% in June from a year earlier, a fresh four-decade high. Compared with May, the CPI is seen rising 1.1%, marking the third month in four with an increase of at least 1%.

While persistently high and broad-based inflation is seen persuading Fed officials to raise their benchmark rate 75 basis points for a second consecutive meeting on July 27, recession concerns are mounting. There are signs, though, that price pressures at the producer level are stabilizing as commodities costs — including energy — retreat.

But the expectations of inflation, as measured by The Fed’s 5-year forward breakeven inflation rate, just crashed to 1.8437%.

The breakeven inflation rate is a market-based measure of expected inflation. It is the difference between the yield of a nominal bond and an inflation-linked bond of the same maturity.

The USD Inflation Swap Forward 5Y5Y is also falling like a rock as The Fed hikes their target rate (green line).

Could it be that inflation is cooling with Fed rate hikes (but not the shrinking of their $8 trillion balance sheet)?

Currently, Fed Funds Futures are pointing to a Fed target rate of 3.552% by February 2023. And with that, Bankrate’s 30-year mortgage rate rose to 5.75%. Once again, like velociraptors from Jurassic Park, The Fed’s balance sheet is still out in force.

Fed Chair Jerome Powell and Atlanta Fed President Raphael Bostic are keeping The Fed’s balance sheet at near $9 trillion as they hunt assets to inflate.

You must be logged in to post a comment.